Biodegradable Films Market Overview: Growth Dynamics & Sustainable Opportunities (2025–2034)

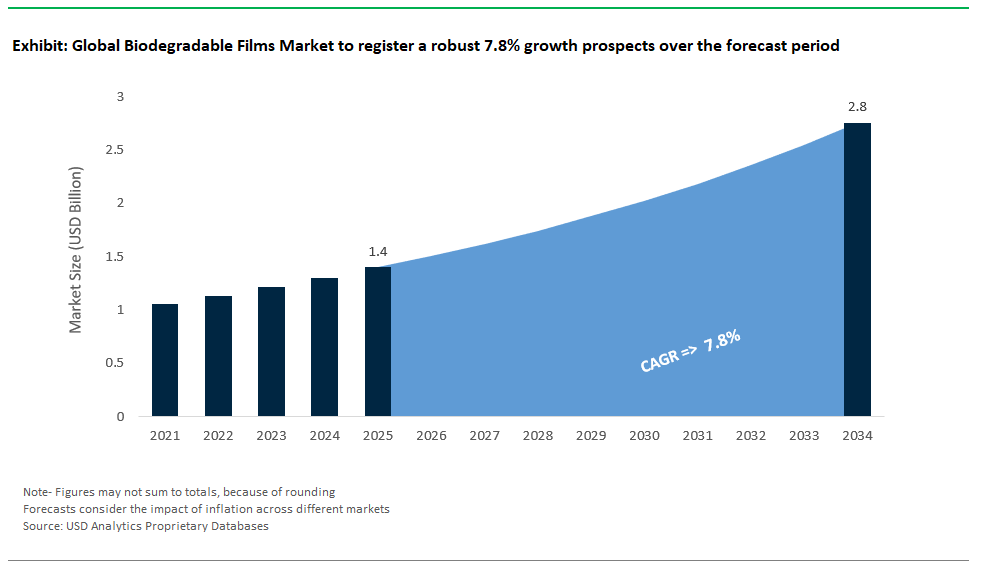

The Global Biodegradable Films Market is on a steady upward trajectory between 2025 and 2034, as environmental regulations tighten and industries seek sustainable alternatives to conventional plastic films. According to industry projections, the market is set to increase from USD 1.4 billion in 2025 to USD 2.8 billion by 2034, achieving a solid CAGR of 7.8%. This growth is being driven by heightened demand for biodegradable packaging, expanding agricultural applications, and significant innovation in film technologies that balance performance with environmental responsibility.

Drawing on exclusive research from USDAnalytics, the new edition delivers a robust evaluation and future outlook for the global Biodegradable Films market, charting developments in 21 regions and profiling 20+ significant industry players- By Material Type (Polylactic Acid (PLA) Films, Starch-Based Films, Polyhydroxyalkanoates (PHA) Films, Biodegradable Polyesters, Cellulose-Based Films, Polyvinyl Alcohol (PVA) Films, Others), By Film Structure (Mono-layer Films, Multi-layer Films, Coated Films), By Application (Packaging, Agriculture & Horticulture, Hygiene & Medical, Others).

This study explores the critical forces shaping the global biodegradable films market, examining technological advances that enable improved barrier properties, flexibility, and compostability in both mono-layer and multi-layer films. It highlights the rising utilization of PLA and starch-based films in sustainable packaging, the emergence of biodegradable polyesters for demanding applications, and the increasing focus on cellulose-based solutions for both industrial and consumer uses. The report also reviews competitive strategies, regulatory developments, and investment trends as key players expand capacity and innovate to meet the evolving needs of end-use industries. Packed with verified insights and practical intelligence, this analysis provides manufacturers, investors, converters, and policymakers with essential tools to navigate the expanding market for biodegradable films through 2034.

Biodegradable Films Market Analysis: Growth and Transformation Analysis

The global biodegradable films market is undergoing rapid transformation as sustainability imperatives, regulatory mandates, and technological advancements converge to redefine material choices across diverse end-use sectors. Historically, a niche segment limited by performance and cost barriers, biodegradable films are now advancing into mainstream markets driven by consumer demand for environmentally responsible solutions and increasing legislative pressure to replace traditional plastic films. Recent market activities reveal a vibrant ecosystem of innovation, capacity scale-up, and commercial adoption that is reshaping the competitive landscape and opening new opportunities across packaging, agriculture, retail, and industrial applications.

Innovative Product Launches Address Diverse Applications

Product innovation is a key driver in the biodegradable films market, as manufacturers develop materials that meet both sustainability goals and performance needs. BASF has introduced ecovio® M2351, a certified soil-biodegradable film designed for agricultural and horticultural mulch applications. This film fully biodegrades in soil through the action of microorganisms, aligning with EN17033 certification standards.

Danimer Scientific is responding to growing regulatory and consumer demand for sustainable food packaging with its Nodax™ PHA films. These films are made from 100% renewable materials and are fully biodegradable, making them suitable for home-compostable food pouches and other direct food contact applications, though formal regulatory confirmations for food contact compliance remain to be clarified.

Mitsubishi Chemical’s BioPBS™ FD92 demonstrates how biodegradable films are entering specialized markets. This ultra-thin, soil-biodegradable film is engineered for applications such as tea bags and fruit labels, sectors historically reliant on conventional plastics. Regulatory requirements mandating compostable solutions for small-format packaging are accelerating the adoption of such specialized biodegradable films.

Overall, these innovative product launches signal how biodegradable films are expanding into diverse applications, helping industries reduce plastic waste and meet evolving environmental regulations.

Capacity Expansions Reflect Market Readiness for Scale

Significant capacity expansions show the market is moving from niche supply to large-scale production to meet rising global demand and lower costs through economies of scale.

- TotalEnergies Corbion plans to build a second PLA plant in France with a capacity of 100 kilotonnes per year, expanding on their existing 75 kTpa Luminy® PLA plant in Thailand. This positions them as a major supplier for flexible packaging, especially in high-growth Asian markets.

- Futerro opened a new 30,000-tonne-per-year PLA plant in Bengbu, China, supported by an 80,000-tonne-per-year lactic acid unit, reinforcing Asia-Pacific’s role as a key driver for biodegradable films amid plastic bans and growing consumer demand for eco-friendly packaging.

- Kaneka increased PHBH™ film production to about 5,000 tonnes per year and is considering a future commercial plant with 20,000-tonne capacity, reflecting growing interest in compostable flexible packaging like pouches and single-use products.

Strategic Partnerships & Acquisitions Drive Technology Integration

Strategic alliances and acquisitions are crucial for accelerating innovation and expanding sustainable packaging solutions.

- Amcor continues developing recyclable films and bio-based PE for fresh produce packaging, aligning with global trends where brands partner with suppliers to deliver sustainable solutions without sacrificing performance or brand recognition.

- Novamont’s acquisition of BioBag Group in January 2021 boosts its global reach for MATER-BI® compostable films, strengthening its position in retail and municipal markets as regulations tighten for compostable bags and sustainable packaging.

- Sealed Air’s joint venture with Kuraray for PVA-based water-soluble films shows how biodegradable film technologies are expanding into new uses like detergent pods and industrial packaging, creating fresh opportunities for sustainable film applications.

Regulatory Drivers Accelerate Adoption Across Regions

Global regulations are rapidly boosting demand for biodegradable films and transforming market dynamics. The EU’s Packaging and Packaging Waste Regulation (PPWR), effective from February 2025, requires items like tea bags, coffee pads, and fruit stickers to be compostable by 2028, setting clear goals for industry compliance. In India, stricter Plastic Waste Management Rules have banned thin plastic carry bags under 120 microns since December 2022, driving brands like PepsiCo to test compostable films for products such as Kurkure snacks. Meanwhile, California’s SB 54 law mandates that all single-use packaging and plastic food service ware be recyclable or compostable by 2032, marking one of North America’s strongest regulatory pushes and opening significant growth opportunities for biodegradable film producers worldwide.

Technological Breakthroughs Elevate Performance Standards

New material innovations are overcoming key challenges in biodegradable films, improving strength, barrier properties, and faster breakdown. Research into nanocellulose-based films shows strong potential to boost oxygen barrier performance, essential for keeping snacks and dry foods fresh longer. Meanwhile, MIT has developed PLA films that can rapidly decompose in soil within 48 hours using enzymes, a major step toward reducing microplastic pollution from single-use packaging. These breakthroughs are closing the performance gap between biodegradable films and traditional plastics, making sustainable solutions more commercially viable and helping industries meet tougher environmental regulations.

Commercial Adoption Validates Market Momentum

Major brands are proving that biodegradable films are ready for large-scale use, driving market confidence and growth. PepsiCo’s pilot of PHA-based compostable packaging for Kurkure snacks in India shows these films can succeed even in price-sensitive markets, where regulations and brand reputation push sustainable change. Although specific details on Unilever’s use of marine-degradable PHA films for Hellmann’s mayonnaise sachets weren’t confirmed, the company’s strong focus on cutting plastic waste highlights how biodegradable films are moving into single-serve applications notorious for high plastic use. Meanwhile, while Walmart’s online offerings still largely feature conventional plastic bags, any shift toward PLA films for private-label produce bags would reflect growing retailer efforts to meet sustainability goals and satisfy eco-conscious consumers. Overall, commercial trials and brand commitments are driving the momentum of biodegradable films into mainstream markets.

Biodegradable Films Market Dynamics: Marine Solutions and Compostable Food Packaging Drive Growth

Trend: Marine-Degradable Film Innovations Transform Coastal and Aquaculture Packaging

The global biodegradable films market is seeing rapid innovation as marine-degradable films emerge as a critical solution to combat ocean pollution. Countries like the EU, Japan, and Indonesia are pushing new regulations and global agreements, such as the UN Global Plastics Treaty, to tackle plastic waste from fishing and aquaculture. These policies are fueling demand for marine-degradable materials, helping industries reduce plastic waste and protect coastal ecosystems.

New materials like polyhydroxyalkanoate (PHA)-based films are proving effective in seawater, breaking down much faster than conventional plastics when tested under standards like ASTM D6691. Advances in manufacturing are also lowering production costs, narrowing the price gap between PHA films and traditional LDPE plastics. As costs drop and regulations tighten, more aquaculture netting and film suppliers are adopting marine-degradable solutions, setting new standards for sustainability in coastal industries worldwide.

Opportunity: Home-Compostable Food Service Films Capture Surging Retail and Consumer Demand

A major opportunity in the global biodegradable films market lies in home-compostable food service films, which are replacing traditional PVC and plastic cling films in both homes and retail stores. Consumers are increasingly demanding sustainable packaging options, and surveys show rising interest in compostable food films that help reduce environmental impact without sacrificing convenience.

Technological advances mean home-compostable films, like cellulose-acetate, now match traditional plastics in clarity and offer strong oxygen barrier properties for food freshness. The compostable foodservice packaging market is already worth billions and continues to grow, fueled by expanding composting infrastructure, especially in places like the U.S. These trends are positioning home-compostable biodegradable films as a leading choice for sustainable packaging in food service and consumer markets globally.

Biodegradable Films Market Competitive Landscape and Strategic Developments

The global biodegradable films industry is surging in 2024 as sustainability regulations, corporate commitments, and consumer demand drive rapid adoption of compostable and bio-based alternatives to conventional plastic films. Innovations span PLA, PHA, PBAT, cellulose, and bio-PET films, targeting diverse applications from food packaging and agriculture to electronics and marine environments. Market leaders are scaling production capacities, launching advanced grades for high-performance uses, and forging strategic alliances to accelerate market penetration. The competitive landscape is marked by intense R&D activity, significant regional investments, and a race to deliver films that combine functionality, cost-effectiveness, and environmental benefits.

NatureWorks: Global PLA Film Pioneer

NatureWorks (USA) NatureWorks remains a global PLA film pioneer, with an established global capacity of 165,000 tonnes per year from its US facility. Its 75,000 tonnes per year Thailand plant, which made significant construction progress through Q2 2024, is anticipated to begin full production in 2025, poised to significantly boost regional capacity. In April 2024, NatureWorks, in partnership with IMA Coffee, announced a turn-key compostable coffee pod solution for the North American market, designed for superior brewing performance and industrial compostability. Further expanding its portfolio, in February 2025, the company launched Ingeo™ 3D300 for high-quality 3D printing, and in March 2025, it introduced Ingeo™ Extend for BOPLA films. NatureWorks continues to play a pivotal role in transitioning brands toward compostable alternatives, solidifying its position as a leader in renewable and high-performance packaging materials.

TotalEnergies Corbion: Leading in PLA Films Capacity and Innovation

TotalEnergies Corbion (Netherlands)TotalEnergies Corbion has carved a leading position in PLA films, operating a 75,000 tonnes per year facility in Thailand under its Luminy® brand. The company has plans for a second 100,000 tonnes per year plant in Grandpuits, France, reflecting significant future expansion and a drive to meet growing global demand. TotalEnergies Corbion emphasizes its collaborative approach across the value chain to drive widespread adoption of PLA bioplastics and facilitate seamless technical implementation for partners. TotalEnergies Corbion’s focus on performance attributes like sealability and clarity positions it as a leading supplier for brand owners seeking both sustainability and technical reliability in flexible packaging.

Futamura: Market Leader in Cellulose-Based Films

Futamura (Japan/UK) Futamura leads the market in cellulose-based films with its NatureFlex™ brand. The company made a significant investment in a new production line at its European manufacturing facility (announced December 2022) to boost the site's capacity by approximately 25%, in response to increasing demand for its renewable and compostable NatureFlex™ films. Futamura's NatureFlex™ cellulose films are part of overall compostable solutions for a variety of product and package types, offering excellent aroma, oxygen, and moisture barriers. NatureFlex™ NE has also been tested in the MITI aqueous biodegradation test (ISO 14851), demonstrating that it will break down in wastewater and soil, as well as under home composting conditions. Futamura’s cellulose films continue to gain traction in premium food packaging and specialized applications requiring high barriers and compostability.

TIPA Corp: Transforming Flexible Packaging with Compostable Solutions

TIPA Corp (Israel)TIPA is transforming the flexible packaging segment with compostable solutions designed for real-world waste systems. TIPA has a total funding of $130 million over 6 rounds, with its latest funding round being a Series C round on January 2, 2022, for $70 million. TIPA continues to launch innovative home compostable film solutions, such as a metallized barrier film for snack packaging (February 2025) and home compostable pouch closures in partnership with Fresh-Lock® (July 2024). TIPA’s focus on flexible, fully compostable films positions it as a key innovator as brands and regulators push to eliminate plastic waste from single-use applications.

BASF: Strengthening Leadership in PBAT-Based Biodegradable Films

BASF (Germany)BASF strengthens its leadership in PBAT-based biodegradable films through its ecovio® portfolio. In June 2024, BASF SE introduced a biomass-balanced ecoflex PBAT variant called ecoflex F Blend C1200 BMB, which uses renewable feedstock derived from residual and waste biomass. In February 2024, BASF launched its ChemCycling™ initiative in the US, converting plastic waste into new ISCC+ certified advanced recycled building blocks. BASF has also collaborated with Südpack and Werz to introduce a chemically recycled meat and sausage packaging solution using BASF's Ultramid Ccycled polyamide (reported May 2025), which is suitable for food packaging due to its barrier properties. BASF’s scale and technological expertise position it as a critical player in the shift toward bio-based and biodegradable plastics.

Mitsubishi Chemical: Expanding Presence in Sustainable Film Solutions

Mitsubishi Chemical (Japan) Mitsubishi Chemical is steadily expanding its presence in sustainable film solutions. Mitsubishi Chemical offers a comprehensive lineup of polyester films (DIAFOIL™) with well-balanced characteristics, and continues to invest in R&D to provide more sophisticated products, including those that contribute to sustainability. Mitsubishi Chemical’s innovations contribute to bridging the gap between sustainability and the technical demands of various sectors, positioning it as a key supplier in the evolution of biopolymer films.

Investment Hotspots in Biodegradable Films

- Southeast Asia: Rapid growth driven by NatureWorks’ expansion in Thailand and continued demand in Asia’s booming packaging markets.

- Western Europe: Major investments from BASF (Germany) and TotalEnergies Corbion (France) reflect strong regulatory support and market demand for sustainable films.

- North America: Significant activity focused on meeting rising US demand for compostable packaging and sustainable materials, despite recent market consolidation challenges for some players.

Biodegradable Films Market Share and Segmentation Analysis

By Material Type: PLA Films Dominate, PHA Films Deliver Fastest Growth

In 2025, PLA films lead the market with a 34.9% share, widely favored for food packaging and rigid trays due to their high clarity and processability. Industry leaders such as NatureWorks and TotalEnergies Corbion drive innovation in this space. PHA films are the fastest-growing segment, valued for their marine-degradability and flexibility, making them increasingly popular in medical and hygiene applications. Blends of PBAT and PBS are also critical for flexible packaging, balancing toughness and compostability, while cellulose-based and PVA films carve out niches for high-barrier and water-soluble applications.

By Film Structure: Mono-Layer Films Lead, Multi-Layer and Coated Films Accelerate Growth

Monolayer films hold the largest market share in 2025, prized for their cost-effectiveness and recyclability, especially in basic packaging applications using PLA and starch blends. Multi-layer films are growing fastest with a CAGR of 7.1%, as food and FMCG brands demand advanced barrier properties for extended shelf life, using combinations like PLA/PBAT and PHA/PBS. Coated films, though niche (18% share), are expanding rapidly with cellulose and PHA coatings delivering functional benefits such as grease and water resistance for food and specialty packaging.

By Application: Packaging Remains Key Driver, Hygiene & Medical Sectors Gain Momentum

Packaging is the leading application, representing 56.1% of market demand in 2025, with bioplastic wraps, pouches, and films increasingly adopted by FMCG brands seeking to meet sustainability commitments. The hygiene and medical sector is the fastest-growing, fueled by the adoption of PHA films for diaper backsheets, surgical drapes, and medical disposables where biocompatibility and rapid degradation are essential. Agriculture also accounts for a significant share, particularly in mulch and silage films using starch-PVA blends.

.png)

Germany Accelerating Biodegradable Film Adoption through Innovation and EU Regulation

Germany stands at the forefront of the global biodegradable films industry, championing both material innovation and large-scale application. Key industry leaders like BASF, Südzucker, and the Fraunhofer Institute are driving advances in PBAT-based films. BASF’s Ecoflex is now widely adopted for flexible packaging and marine-degradable PHA films, offering real solutions for reducing persistent plastic waste. In 2025, BASF is significantly ramping up the availability of its certified compostable and soil-biodegradable Ecoflex® BMB (biomass balanced) portfolio, showcasing these innovations at major trade fairs like K 2025, underlining its commitment to a lower carbon footprint. Germany’s top markets for biodegradable films include food packaging (fresh produce, snack films) and agricultural mulch films, both of which have seen widespread commercial rollout. The EU Packaging and Packaging Waste Regulation (PPWR), with a mandate for biodegradable films in select applications by 2030, is rapidly reshaping industry standards. The PPWR, with its first major provisions becoming effective in 2025, is a significant catalyst, pushing German manufacturers and brands to accelerate the development and adoption of biodegradable film alternatives, especially for hard-to-recycle single-use plastics in food service and e-commerce. Südzucker’s launch of transparent, starch-based films further diversifies Germany’s offering for both food and non-food packaging. Südzucker is reportedly expanding the commercial reach of its starch-based films in 2025, targeting broader adoption in confectionery and bakery packaging across Europe. With a mix of strong regulation, technical leadership, and scalable innovation, Germany is a prime driver of the next wave of biodegradable films adoption across Europe and globally.

United States Scaling Biodegradable Film Production for Food, Retail, and Medical Packaging

The United States is a powerhouse in the production and commercialization of biodegradable films, supported by pioneering companies such as NatureWorks, Danimer Scientific, and Avery Dennison. The industry has seen significant advances in material science, with NatureWorks’ PLA films widely used in compostable pouches and Danimer’s PHA films gaining traction in food service and shopping bag applications. NatureWorks is on track to bring additional PLA production capacity online in Thailand in 2025, which will alleviate supply constraints and support expanded applications for its PLA films in diverse sectors, including fresh food packaging and durable goods throughout the U.S. and Asia. Danimer Scientific's PHA films are projected to see substantial growth in 2025, with market forecasts indicating a surge to USD 36.76 billion globally by 2025 (for the overall PHA film market), particularly in food packaging and biomedical applications, driven by rising consumer demand for compostable and biodegradable solutions. Avery Dennison’s introduction of bio-based adhesive films extends innovation to new areas like labeling and medical packaging. Avery Dennison is further leveraging its bio-based PE film technology in 2025, a sugar cane ethanol-derived material, to develop new pressure-sensitive adhesive label solutions for flexible biodegradable packaging, offering a full bio-based labeling solution. U.S. adoption is spurred by regulatory measures such as California’s SB 54, which requires brands to seek biodegradable alternatives to conventional plastic films. CalRecycle reissued updated draft regulations for SB 54 in May 2025, clarifying requirements for "compostable" labeling (requiring ASTM D6400 or D6868, or OK compost HOME certification), which is pushing brands and retailers to ensure their biodegradable films meet rigorous standards for market entry in California. As snack wrappers, shopping bags, and medical films transition to compostable options, the U.S. market is experiencing a rapid transformation, drawing attention from global brands and investors seeking scalable, sustainable packaging solutions.

Italy Leading Compostable Film Technology for Food, Cosmetics, and Circular Economy

Italy has established itself as a European leader in compostable film technology, thanks to innovators like Novamont and Bio-on. Novamont’s Mater-Bi, a starch-PBS blend, is at the heart of Italy’s mandated compostable food packaging, while Bio-on’s luxury-oriented PHA films open new markets in cosmetics and personal care. Novamont's Mater-Bi films continue to dominate the Italian compostable packaging market in 2025, supported by the country's robust industrial composting infrastructure and mandatory separate collection of organic waste. Biorepack, Italy's national consortium for compostable bioplastics, is well on track to meet its 2025 recycling target of 50% for biodegradable and compostable plastic packaging. The Italian market is distinguished by strong regulatory backing, requiring biodegradable produce bags and supporting R&D for new applications. Recent expansions by TotalEnergies Corbion in PLA film production are broadening Italy’s commercial footprint. TotalEnergies Corbion is focused in 2025 on optimizing its PLA production for high-performance film applications, particularly for flexible food packaging requiring enhanced barrier properties. EU-funded projects such as CIRCULAR FARM emphasize the importance of agri-film recycling, advancing the country’s vision of a circular packaging economy. The CIRCULAR FARM project and similar initiatives are gaining momentum in 2025, contributing to the expansion of collection and recycling systems for biodegradable agricultural films across Italy and other EU member states. Italy’s combination of policy clarity, innovation, and international partnerships positions it as a strategic hub for biodegradable film solutions.

China Leading in Biodegradable Film Production and Policy-Driven Market Expansion

China dominates global biodegradable film production, with industry giants Kingfa, Sinopec, and BBCA Biochemical spearheading market development. Kingfa is the largest PBAT film producer worldwide, and BBCA’s PLA films are making significant inroads in food and agricultural packaging. Kingfa is reportedly expanding its PBAT film production capacity significantly in 2025, reinforcing its position as the primary global supplier, while BBCA Biochemical's PLA capacity is projected to reach 150,000 tons/year with ongoing expansions, positioning it as a major player in the global PLA film market. The e-commerce sector is a major driver, with Alibaba’s push for biodegradable mailers fueling demand. Alibaba's internal target for 2025, requiring a significant portion of its shipments to use paper-only or biodegradable mailers, is demonstrating strong progress, driving demand for innovative film solutions within its vast logistics network. Agricultural mulch films represent another high-volume application, supported by government subsidies and a national mandate requiring 30% of all packaging to be biodegradable by 2025. The 2025 mandate is heavily influencing the Chinese packaging industry, particularly for films used in single-use applications, with significant investment flowing into R&D and manufacturing of compliant biodegradable films. Sinopec’s rollout of PBS-based films for food packaging and the proliferation of cost-effective, high-volume solutions position China as the principal supplier and influencer in global supply chains for biodegradable films.

Japan Delivering Advanced Biodegradable Films for Food, Electronics, and Marine Applications

Japan’s biodegradable films industry is characterized by technical excellence and market versatility. Mitsubishi Chemical leads with bio-PBS films, while Toray’s transparent PLA films support applications in food trays and high-end electronics packaging. In 2025, Mitsubishi Chemical is introducing new advanced grades of bio-PBS films with improved heat resistance and barrier properties, targeting high-demand food packaging segments. Toray is also expanding the use of its transparent PLA films for sensitive electronics, leveraging their anti-static properties and clarity. Kaneka’s PHBH films, certified for marine biodegradability, demonstrate Japan’s focus on environmental responsibility in both domestic and export markets. Kaneka's PHBH films are seeing increased adoption in 2025, particularly in marine-related applications such as biodegradable fishing nets and aquaculture films, addressing growing concerns about ocean plastic pollution. The industry’s R&D momentum is strengthened by government funding for home-compostable film development and a strong push from leading electronics brands (Sony, Panasonic) to adopt bio-based packaging. The Japanese Ministry of Economy, Trade and Industry (METI) has allocated additional funds in 2025 for research into advanced home-compostable films, aiming to develop materials that meet diverse consumer disposal methods. Sony and Panasonic are expanding their use of bio-based films in product packaging, particularly for smaller consumer electronics, aligning with their corporate sustainability goals for 2025 and beyond. Japan’s commitment to quality, sustainability, and regulatory alignment makes it a top player in both the Asian and global biodegradable films markets.

Netherlands: Advancing Plant-Based and High-Barrier Biodegradable Films for Beverage and Snack Markets

The Netherlands is a European innovation hub for plant-based and high-barrier biodegradable films, led by companies like Avantium and Corbion. Avantium’s PEF films, a plant-based PET alternative, are being pilot-tested by Coca-Cola for bottle labels, and Corbion’s high-barrier PLA films are gaining commercial adoption for snacks and food packaging. Avantium's PEF Flagship Plant is on track to be fully operational by early 2026, and in 2025, Avantium is conducting extensive pilot trials of its PEF films with multiple global brands for beverage bottles and flexible packaging, showcasing its potential as a high-performance, renewable alternative to traditional plastics. Coca-Cola's pilot testing of PEF films for labels is providing valuable data for potential broader integration into their sustainable packaging initiatives post-2025. Corbion’s high-barrier PLA films are expanding the options for transparent, bio-based laminates used in a variety of consumer products. Corbion is launching new high-barrier PLA film grades in 2025, specifically designed for challenging flexible packaging applications that require extended shelf life for perishable goods like fresh meat and cheese. The EU Horizon Grant awarded for PEF commercialization is fueling further innovation and industrial scale-up. The ongoing EU Horizon Europe work programme for 2025 has dedicated significant funding towards climate-related objectives and bioeconomy, directly benefiting projects like PEF commercialization, strengthening the Netherlands' position in advanced bio-based materials research. With its commitment to circular packaging, rapid commercialization, and strategic partnerships, the Netherlands is cementing its status as a leader in next-generation biodegradable films.

Biodegradable Films Market Report Scope

Biodegradable Films Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$1.4 Billion

|

|

Market Size (2034)

|

$2.8 Billion

|

|

Market Growth Rate

|

7.8%

|

|

Segments

|

By Material Type (Polylactic Acid (PLA) Films, Starch-Based Films, Polyhydroxyalkanoates (PHA) Films, Biodegradable Polyesters, Cellulose-Based Films, Polyvinyl Alcohol (PVA) Films, Others), By Film Structure (Mono-layer Films, Multi-layer Films, Coated Films), By Application (Packaging, Agriculture & Horticulture, Hygiene & Medical, Others)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

NatureWorks LLC (U.S.), Novamont S.p.A. (Italy), BASF SE (Germany), TotalEnergies Corbion (Netherlands), Danimer Scientific (U.S.), Mitsubishi Chemical Group Corporation (Japan), Innovia Films (part of CCL Industries Inc.) (UK), Mondi Group (Austria/UK), Huhtamaki Oyj (Finland), Taghleef Industries (Ti) (UAE), BioBag International AS (Norway), Futamura Chemical Co., Ltd. (Japan), Kingfa Sci. & Tech. Co., Ltd. (China), FKuR Kunststoff GmbH (Germany), Green Dot Bioplastics (U.S.), Plantic Technologies Limited (Australia), CJ Biomaterials Inc. (South Korea), Polymateria Ltd. (UK), Tipa Corp. (Israel), Cortec Corporation (U.S.), Clondalkin Group (Netherlands), TRIOWORLD INDUSTRIER AB (Sweden), Groupe Barbier (France), Layfield Group (Canada), Polystar Plastics Ltd. (UK), Walki Group Oy (Finland), Plascon Group (U.S.), and Others.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Biodegradable Films Market Segmentation

By Material Type

- Polylactic Acid (PLA) Films

- Starch-Based Films

- Polyhydroxyalkanoates (PHA) Films

- Biodegradable Polyesters

- Cellulose-Based Films

- Polyvinyl Alcohol (PVA) Films

- Others

By Film Structure

- Mono-layer Films

- Multi-layer Films

- Coated Films

By Application

- Packaging

- Agriculture & Horticulture

- Hygiene & Medical

- Others

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in the Biodegradable Films Market

- NatureWorks LLC (US)

- Novamont S.p.A. (Italy)

- BASF SE (Germany)

- TotalEnergies Corbion (Netherlands)

- Danimer Scientific (US)

- Mitsubishi Chemical Group Corporation (Japan)

- Innovia Films (part of CCL Industries Inc.) (UK)

- Mondi Group (Austria/UK)

- Huhtamaki Oyj (Finland)

- Taghleef Industries (Ti) (UAE)

- BioBag International AS (Norway)

- Futamura Chemical Co., Ltd. (Japan)

- Kingfa Sci. & Tech. Co., Ltd. (China)

- FKuR Kunststoff GmbH (Germany)

- Green Dot Bioplastics (US)

- Plantic Technologies Limited (Australia)

- CJ Biomaterials Inc. (South Korea)

- Polymateria Ltd. (UK)

- Tipa Corp. (Israel)

- Cortec Corporation (US)

- Clondalkin Group (Netherlands)

- TRIOWORLD INDUSTRIER AB (Sweden)

- Groupe Barbier (France)

- Layfield Group (Canada)

- Polystar Plastics Ltd. (UK)

- Walki Group Oy (Finland)

- Plascon Group (US)

* List Not Exhaustive

Methodology:

The research methodology for the Global Biodegradable Films Market integrates primary interviews with industry stakeholders, including film manufacturers, resin producers, technology developers, packaging converters, agricultural suppliers, end-user companies, regulatory authorities, and sustainability experts, to gather both qualitative and quantitative insights. Extensive secondary research draws from corporate disclosures, regulatory documents, patent filings, trade association publications, academic research, and publicly available data from organizations such as the European Bioplastics Association, the U.S. Department of Agriculture, the European Commission, and national statistical agencies. Data triangulation techniques ensure the validation and accuracy of market estimates, providing a robust foundation for forecasting growth trends, competitive dynamics, and technology adoption pathways through 2034.

Research Coverage and Deliverables

Research Coverage:

- Geographic Scope: Analysis covers 25+ countries across North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa.

- Segmentation: Detailed segmentation by:

- Material Type: Polylactic Acid (PLA) Films, Starch-Based Films, Polyhydroxyalkanoates (PHA) Films, Biodegradable Polyesters, Cellulose-Based Films, Polyvinyl Alcohol (PVA) Films, Others.

- Film Structure: Mono-layer Films, Multi-layer Films, Coated Films.

- Application: Packaging, Agriculture & Horticulture, Hygiene & Medical, Others.

- Competitive Landscape: Profiles and strategies of 20+ leading manufacturers, technology innovators, and regional players.

- Trends & Disruptions: In-depth analysis of sustainable material innovations, regulatory impacts (e.g., EU PPWR, California SB 54), marine and home-compostable solutions, and evolving end-of-life technologies.

- Industry Dynamics: Comprehensive insights into market drivers, restraints, investment trends, capacity expansions, sustainability certifications, and regional policy landscapes.

- Historic data from 2021 to 2024 and forecast data from 2025 to 2034

Deliverables:

- Full Market Research Report (PDF, Excel): Including comprehensive data tables, charts, and interactive visualizations.

- Country-Level Forecasts & Analysis.

- Segment-wise Revenue Projections (2025–2034).

- Competitive Benchmarking & SWOT Analysis.

- Recent Developments & News Tracker.

- Executive Summary & Analyst Insights.

- Custom Queries/Analyst Support (for Post-sale)