Biopolymer Films Market Overview: Sustainable Material Innovations & Forecast

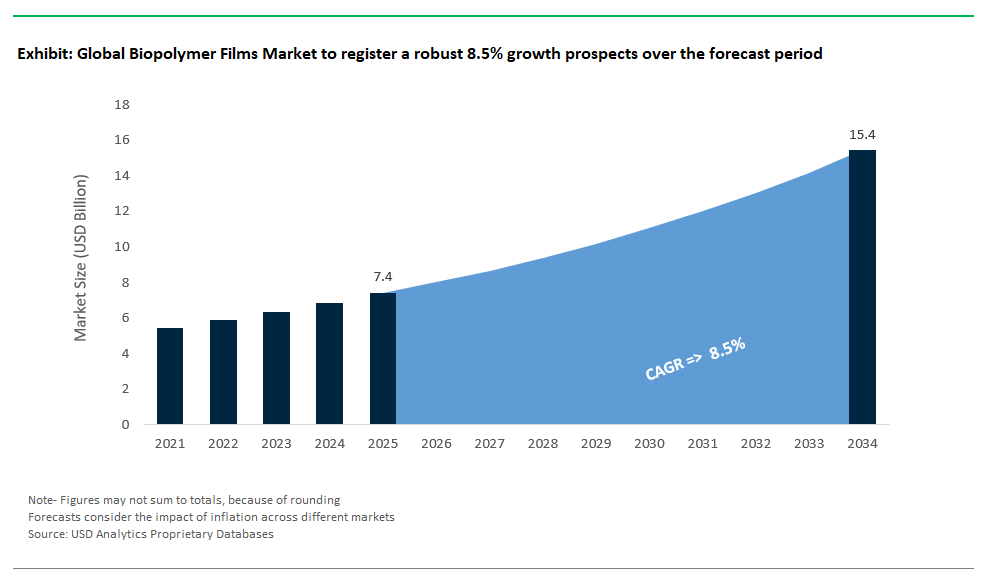

The Global Biopolymer Films Market is gaining significant momentum between 2025 and 2034, driven by the transition toward sustainable materials and the surging demand for eco-friendly films in diverse end-use sectors. Industry forecasts predict the market to rise from USD 7.4 billion in 2025 to USD 15.4 billion by 2034, representing a robust CAGR of 8.5%. Growth is fueled by increasing regulatory restrictions on conventional plastics, advancements in biopolymer processing technologies, and heightened consumer and brand-owner demand for sustainable packaging, agricultural solutions, and hygiene applications.

With proprietary research from USDAnalytics as its foundation, this updated report thoroughly evaluates the global biopolymer films market, offering future outlooks while mapping trends across 21 countries and spotlighting over 20 prominent firms- By Material Type (Polylactic Acid (PLA) Films, Polyhydroxyalkanoates (PHA) Films, Starch-Based Films, Cellulose-Based Films, Polybutylene Adipate Terephthalate (PBAT) Films, Polybutylene Succinate (PBS) Films, Polyvinyl Alcohol (PVA) Films, Bio-Polyethylene (Bio-PE) Films, Bio-Polyethylene Terephthalate (Bio-PET) Films, Others), By Film Type (Mono-layer Films, Multi-layer Films, Coated Films), By Application (Packaging, Agriculture & Horticulture, Hygiene & Medical, Others).

In this analysis, the report explores key factors transforming the biopolymer films industry, including rapid innovations in multi-layer and coated film technologies designed to enhance barrier properties, compostability, and mechanical performance. It highlights how manufacturers are scaling up the production of PLA, PHA, and starch-based films for packaging and agricultural films, while also investigating the market’s diversification into medical and hygiene applications. The study reviews competitive strategies, sustainability certifications, regulatory compliance trends, and collaborative efforts across supply chains that are shaping market dynamics through 2034. Supported by verifiable data and practical insights, this report is a crucial resource for manufacturers, investors, brand owners, and policymakers seeking to capture opportunities in the rapidly expanding biopolymer films market.

Biopolymer Films Market Analysis: From Niche Solutions to Mainstream Adoption

The global biopolymer films market is entering a dynamic phase of growth, driven by converging regulatory imperatives, brand sustainability pledges, and technological advances that are reshaping the competitive landscape. Once confined to niche applications, biopolymer films are rapidly expanding into mainstream flexible packaging, agricultural films, foodservice wraps, and specialty industrial uses. Recent market activity underscores how manufacturers are scaling production, innovating material science, and collaborating strategically to meet the rising demand for sustainable films that deliver both environmental benefits and critical functional performance.

Innovative Product Launches Drive Growth in Biopolymer Films

Product innovation is fueling growth in the biopolymer films sector, as manufacturers develop materials that deliver both sustainability and high performance in areas like strength, barrier protection, and thermal sealing. BASF’s ecovio® F2360, and specifically its ecovio® M2351 grade, stands out as a certified soil-biodegradable mulch film (EN17033) that can be ploughed back into the soil after harvest, helping farmers avoid persistent microplastics, a critical advantage amid increasing pressure to eliminate plastic waste in agriculture.

Mitsubishi Chemical’s BioPBS™ FZ91 compostable films provide heat sealability and strong mechanical properties, making them well-suited for snack packaging and overcoming previous limitations that hindered biopolymer films on high-speed packaging lines. Danimer Scientific’s Nodax™ PHA films, certified as biodegradable and compostable, exemplify growing interest in packaging solutions that safely break down in the environment, reducing reliance on industrial composting facilities and responding to rising consumer and regulatory demands for sustainable packaging options.

Capacity Expansions Indicate Scaling Toward Mass Market Adoption

Recent capacity expansions highlight growing confidence in the scalability and commercial viability of biopolymer films.

- TotalEnergies Corbion’s plant in Rayong, Thailand, has reached a cumulative production of 100,000 tonnes of Luminy® PLA since 2019 and is running at its nameplate capacity of 75,000 tonnes annually. The company plans a second PLA plant in France with a 100,000-tonne capacity to meet rising demand in Asia and globally, especially for food and consumer goods packaging.

- Braskem increased its biopolymer production by 30%, raising capacity from 200,000 to 260,000 tonnes per year for bio-PE made from sugarcane ethanol. This expansion reflects growing demand for drop-in sustainable solutions in flexible packaging without disrupting existing recycling systems.

- Futerro’s new PLA plant in Bengbu, China, with a 30,000-tonne annual capacity (supported by an 80,000-tonne lactic acid unit), targets the Asian market, driven by strict regulations on single-use plastics and rising consumer interest in sustainable packaging.

Strategic Partnerships and M&A Shape Competitive Dynamics

Strategic collaborations and acquisitions are proving crucial for technological advancement and market reach in the biopolymer film sector.

- Amcor continues to focus on recyclable films and bio-based PE options, aligning with industry trends where major brands and packaging suppliers co-invest in sustainable solutions to meet regulations and consumer sustainability demands.

- Novamont’s 2021 acquisition of BioBag Group has boosted MATER-BI® compostable film production, strengthening Novamont’s presence in agricultural and consumer packaging markets, particularly in regions with strict compostability standards.

- Sealed Air’s joint venture with Kuraray for PVA-based water-soluble films expands biodegradable film applications beyond packaging into products like detergent pods and single-use dosing formats, supporting broader sustainability goals.

Regulatory Mandates Drive Urgent Adoption

Regulations worldwide are rapidly creating opportunities and shaping the biopolymer films sector. The European Union’s Packaging and Packaging Waste Regulation (PPWR) requires certain packaging types, including tea bags, coffee pads, and fruit and vegetable stickers, to be compostable by February 12, 2028. Member states can also extend these rules to other items like lightweight carrier bags, pushing brands and retailers to rethink materials. California’s SB 54 mandates that by 2032, all single-use packaging and plastic food service items must be either recyclable or compostable, adding significant momentum in one of the world’s largest markets. India’s 2021 ban on single-use plastics and its rule to increase polythene bag thickness to 120 microns are accelerating the shift to alternatives in flexible packaging, with companies like PepsiCo committing to eliminate single-use plastics.

Commercial Adoption Signals Market Readiness

Commercial use of biopolymer films is growing as big brands integrate them into popular products, signaling market readiness and consumer acceptance. Unilever’s Hellmann’s brand is working to reduce plastic waste in its condiment packaging. PepsiCo’s trials of compostable PHA films for snack packaging in India highlight that biopolymer films are feasible even in cost-sensitive markets, showing a global shift toward sustainable packaging driven by regulations and brand reputation.

Market Dynamics: Trends & Opportunities in the Global Biopolymer Films Industry

Trend: Compostable Food Packaging Films Gain Momentum Under Regulations and Brand Initiatives

The global biopolymer films market is rapidly evolving as compostable food packaging films gain traction. Strict regulations, especially in the EU, are placing heavy costs on traditional plastic packaging. For example, the EU imposes a €800 per ton levy on non-recycled plastic waste. These policies, along with the upcoming Packaging and Packaging Waste Regulation (PPWR), are driving the shift to sustainable solutions like compostable films.

Innovation is advancing quickly to meet these demands. New cellulose-acetate films now achieve over 90% biodegradation within 120 days, a significant improvement over traditional polyethylene, which hardly degrades. Cost barriers are also falling. Production efficiencies are closing the price gap between PLA-PHB blend films and conventional PET films, making biopolymer options more competitive.

Major global brands like Nestlé, Danone, and PepsiCo are adopting compostable films across their product lines to meet sustainability goals and regulatory requirements. This powerful mix of regulation, material innovation, and brand commitment is pushing compostable biopolymer films into the mainstream. As both regulatory and consumer expectations grow, compostable films are set to become a standard choice for eco-friendly packaging in the global food and consumer goods industry.

Opportunity: Biodegradable Agricultural Mulch Films Enhance Soil Health and Farm Profitability

A significant growth opportunity in the global biopolymer films market lies in biodegradable agricultural mulch films. These eco-friendly alternatives are poised to replace large volumes of polyethylene mulch films, helping to combat soil contamination from persistent microplastics.

Starch-PVA blend films are showing clear agricultural advantages, such as better moisture retention and healthier root conditions, which improve yields for crops like tomatoes and strawberries. Importantly, enzyme-triggered mulch films are designed to break down rapidly in soil after harvest, unlike traditional polyethylene, which can linger as microplastics for centuries.

For farmers, the economic benefits are compelling. Biodegradable films reduce post-harvest labor and disposal costs tied to removing conventional plastic mulch, helping offset higher upfront costs. Combined with stricter regulations on microplastics and rising demand for sustainable farming practices, biodegradable agricultural films are emerging as a transformative solution for improving soil health and boosting farm profitability.

Biopolymer Films Market: Competitive Insights

The global biopolymer films market is expanding rapidly in 2024 as sustainability commitments, regulatory mandates, and consumer demand drive a transition away from fossil-based plastics. Biopolymer films ranging from PLA and PHA to cellulose-based materials and bio-PET are gaining traction in flexible and rigid applications across food packaging, consumer goods, electronics, and industrial uses. Leading producers are scaling capacity, innovating high-performance film properties like heat resistance and barrier strength, and forging strategic partnerships with major brands to unlock new market segments. The competitive landscape reflects an accelerating shift toward circular economy solutions and eco-friendly alternatives poised to redefine global packaging and specialty film markets.

NatureWorks: Dominant Player in PLA Films

NatureWorks (USA) NatureWorks remains a dominant player in the PLA films sector, with an established global capacity of 165,000 tonnes per year from its US facility. The company's 75,000 tonnes per year Thailand plant, which made significant construction progress through Q2 2024, is anticipated to begin full production in 2025, poised to significantly boost its Asia-Pacific presence. In April 2024, NatureWorks, in partnership with IMA Coffee, announced a turn-key compostable coffee pod solution for the North American market, designed for superior brewing performance and industrial compostability, integrating Ingeo™ PLA biopolymer in the rigid capsule body, nonwoven filter, and multi-layer top lidding. Further expanding its portfolio, in February 2025, the company launched Ingeo™ 3D300 for high-quality 3D printing, and in March 2025, it introduced Ingeo™ Extend for BOPLA films. NatureWorks continues to play a pivotal role in transitioning brands toward compostable alternatives, solidifying its position as a leader in renewable and high-performance packaging materials.

TotalEnergies Corbion: Innovating in High-Performance PLA Films

TotalEnergies Corbion (Netherlands) TotalEnergies Corbion continues to innovate in the biopolymer films sector, operating a 75,000 tonnes per year facility in Thailand under its Luminy® brand. The company has plans for a second 100,000 tonnes per year plant in Grandpuits, France, reflecting significant future expansion and a drive to meet growing global demand. TotalEnergies Corbion emphasizes its collaborative approach across the value chain to drive widespread adoption of PLA bioplastics and facilitate seamless technical implementation for partners. TotalEnergies Corbion’s focus on performance attributes like sealability and clarity positions it as a leading supplier for brand owners seeking both sustainability and technical reliability in flexible packaging.

Futamura: Leader in Cellulose-Based Biopolymer Films

Futamura (Japan/UK) Futamura has further solidified its leadership in cellulose-based biopolymer films. The company made a significant investment in a new production line at its European manufacturing facility (announced December 2022) to boost the site's capacity by approximately 25%, in response to increasing demand for its renewable and compostable NatureFlex™ films. Futamura's NatureFlex™ cellulose films are part of overall compostable solutions for a variety of product and package types, offering excellent aroma, oxygen, and moisture barriers. Futamura’s cellulose films offer a key alternative to plastics in applications requiring excellent barrier properties while remaining home-compostable, reinforcing its role in sustainable packaging innovation.

TIPA: Disruptor in Compostable Flexible Packaging

TIPA (Israel) TIPA has emerged as a disruptor in compostable flexible packaging. TIPA has a total funding of $130 million over 6 rounds, with its latest funding round being a Series C round on January 2, 2022, for $70 million. TIPA continues to launch innovative home compostable film solutions, such as a metallized barrier film for snack packaging (February 2025) and home compostable pouch closures in partnership with Fresh-Lock® (July 2024). TIPA’s focus on flexible, fully compostable films positions it as a key innovator as brands and regulators push to eliminate plastic waste from single-use applications.

BASF: Driving Expansion in PBAT/PLA Blended Films

BASF (Germany) BASF is driving expansion in PBAT/PLA blended films through its ecovio® brand. The PBAT market was estimated at USD 1.74 billion in 2024, with Asia Pacific accounting for the largest revenue share. In June 2024, BASF SE introduced a biomass-balanced ecoflex PBAT variant called ecoflex F Blend C1200 BMB, which uses renewable feedstock derived from residual and waste biomass. In February 2024, BASF launched its ChemCycling™ initiative in the US, converting plastic waste into new ISCC+ certified advanced recycled building blocks. BASF has also collaborated with Südpack and Werz to introduce a chemically recycled meat and sausage packaging solution using BASF's Ultramid Ccycled polyamide (reported May 2025), which is suitable for food packaging due to its barrier properties. BASF’s scale and technical expertise ensure it remains a significant player in biodegradable flexible packaging markets.

Mitsubishi Chemical: Developing Advanced Sustainable Film Solutions

Mitsubishi Chemical (Japan) Mitsubishi Chemical continues to develop advanced film solutions, including those with sustainability benefits. The global Bio-PET Film Market was valued at USD 77.3 million in 2024 and is expected to grow, driven by a shift toward bioplastics, governmental regulations, and increasing usage in end-user applications like packaging, cosmetics, pharmaceuticals, and diverse industries. Mitsubishi Chemical offers a comprehensive lineup of polyester films (DIAFOIL™) with well-balanced characteristics, and continues to invest in R&D to provide more sophisticated products, including those that contribute to sustainability. Mitsubishi Chemical’s innovations contribute to bridging the gap between sustainability and the technical demands of various sectors, positioning it as a key supplier in the evolution of biopolymer films.

Biopolymer Films Market Share and Segmentation Insights

By Film Type: Mono-Layer Films Dominate, Multi-Layer Films Grow Fastest

In 2025, mono-layer biopolymer films hold a 48.2% market share, underpinned by their cost-effectiveness, straightforward recyclability, and wide usage in basic packaging and produce wraps, particularly with materials like PLA. Multi-layer films are the fastest-growing segment, propelled by the food industry’s demand for enhanced barrier protection and extended shelf life, often leveraging innovative PLA/PBAT blends. Coated films, while still niche, are expanding quickly, due to the adoption of PHA and alginate coatings for moisture and grease resistance in specialty medical and food packaging.

.png)

By Application: Packaging Commands the Market, Hygiene & Medical Segment Expands Most Rapidly

Hygiene and medical uses represent the fastest-growing segment with a CAGR of 9.3%, with biodegradable surgical drapes, medical disposables, and diaper backsheets gaining traction, especially as healthcare providers and manufacturers move away from fossil-based plastic films. Packaging remains the dominant application for biopolymer films in 2025, fueled by the food industry’s ongoing shift to compostable wraps, pouches, and single-use bags to meet both regulatory requirements and consumer sustainability expectations. The agriculture and horticulture segment also shows robust growth, reflecting government bans on conventional plastic mulch and a global drive toward sustainable farming practices.

Germany Innovating Compostable and Marine-Degradable Biopolymer Films for Food and Agriculture

Germany is leading the global biopolymer films industry through cutting-edge R&D, strong regulatory backing, and advanced market adoption. BASF’s “Ecoflex,” a PBAT-based compostable film, sets the standard for food packaging and agricultural mulch applications, offering both performance and end-of-life compostability. As of mid-2025, BASF is showcasing advanced "Ecoflex" formulations at industry events like K 2025, highlighting its expanded portfolio for flexible food packaging, particularly targeting fresh produce and baked goods sectors to meet new EU mandates. The Fraunhofer Institute has expanded market possibilities by developing marine-degradable PHA films, which address the urgent need for solutions to plastic pollution in aquatic environments. Fraunhofer, in collaboration with German packaging converters, is conducting pre-commercial trials of its marine-degradable PHA films for specific coastal and aquaculture applications, with a view to limited market entry by early 2026. Food and agriculture remain the top applications, with fresh produce and snack wrappers benefiting from these innovative materials. In response to the EU Packaging and Packaging Waste Regulation (PPWR) enacted in 2024 (with major provisions becoming effective by early 2025/2026), Germany has moved rapidly to mandate biodegradable films in select packaging categories. The PPWR's detailed guidelines, fully clarified by Q1 2025, are accelerating the shift towards compostable films for items like fruit and vegetable labels, and inner linings of some composite packaging, significantly impacting German suppliers. Südzucker’s recent launch of starch-based transparent films adds to the growing array of biopolymer-based solutions in the German and European markets. Germany’s synergy of technical leadership and regulatory momentum continues to drive industry transformation.

United States Scaling Biopolymer Film Production for Flexible Packaging and Retail Innovation

The United States is emerging as a powerhouse in the production and application of biopolymer films, propelled by top-tier R&D, aggressive commercialization, and favorable policy. NatureWorks’ PLA films are widely adopted in flexible packaging, especially compostable pouches for coffee, snacks, and other high-turnover consumer goods, while Danimer Scientific is scaling up PHA films for the food service and retail sectors. NatureWorks is actively expanding its global PLA capacity in 2025 to meet surging demand, with a focus on high-performance flexible film grades for North American and European markets. Danimer Scientific's PHA films are seeing increased penetration in Q3 2025, particularly in single-use food service ware and flexible sachets, benefiting from the growing trend for marine-degradable solutions. Recent regulatory developments, such as California’s SB 54 (2024), are accelerating the adoption of compostable film alternatives, with states pushing brands and retailers to transition away from conventional plastics. The January 2025 update to California's SB 54 Covered Material Category List has provided clear definitions for compostable films in various applications, prompting accelerated procurement shifts by major retailers and food service providers. Avery Dennison’s bio-based adhesive films further diversify the U.S. market with new applications in labeling and packaging. Avery Dennison is expanding its bio-based adhesive film offerings in 2025, with new product lines specifically designed for compostable flexible packaging and industrial labels, addressing challenges in adhesion to biopolymer substrates. From biodegradable shopping bags to next-generation flexible films, the S. market is rapidly expanding its capacity and portfolio, making it a central market for biopolymer film innovation and sustainable retail packaging.

Italy Advancing Starch-Based and PHA Biopolymer Films for Food, Cosmetics, and Agriculture

Italy is establishing itself as a European leader in starch- and PHA-based biopolymer films, integrating innovation, regulatory compliance, and application diversity. Novamont’s Mater-Bi film technology (a starch-PBS blend) is the backbone of Italy’s compostable food packaging sector, which is supported by legal mandates for biodegradable produce bags. Novamont's Mater-Bi films are seeing increased demand in 2025, as Italian retailers fully comply with existing mandates and proactively adopt more compostable solutions for a wider range of fresh produce and dry food packaging. Bio-on’s development of PHA films for luxury and personal care packaging is pushing sustainable solutions into high-value, design-driven segments. Bio-on is engaged in several new partnerships in 2025 with high-end Italian cosmetics and fashion brands, focusing on customized PHA films for sachets, pouches, and specialty wraps, capitalizing on the material's premium feel and complete biodegradability. The industry’s momentum is fueled by the expansion of PLA film production by TotalEnergies Corbion and EU-backed projects such as CIRCULAR FARM, which focuses on recycling agricultural films for a circular economy. TotalEnergies Corbion continues to optimize its PLA film production lines in 2025, focusing on specialty grades for high-barrier and flexible laminates, while the CIRCULAR FARM project is showing promising results in pilot programs for agricultural film collection and composting in key Italian regions. Italy’s regulatory clarity, innovative companies, and EU funding provide a robust foundation for ongoing growth in biopolymer film applications across food, cosmetics, and agriculture.

China Scaling Production and Adoption of Biodegradable Films for E-Commerce and Agriculture

China stands as the largest global producer of biodegradable films, driving the industry with large-scale investments, R&D advances, and regulatory mandates. Kingfa’s PBAT films and BBCA Biochemical’s PLA films dominate the market for e-commerce packaging, with Alibaba’s adoption of biodegradable mailers acting as a catalyst for widespread change. Kingfa is further expanding its PBAT film capacity in 2025, consolidating its position as a global leader, while BBCA Biochemical is increasing its focus on high-performance PLA film grades to meet the growing demand from export markets in Europe and North America. The agricultural sector is also transforming, as government subsidies drive the adoption of biodegradable mulch films to replace legacy plastics and mitigate soil contamination. The Chinese government is expanding its subsidy programs for biodegradable agricultural films in 2025, particularly targeting large-scale farming operations in key agricultural provinces, leading to a significant increase in adoption rates and local manufacturing capacity. In 2024, Sinopec introduced PBS-based films for food packaging, further expanding the market. With a 2025 policy mandating that 30% of all packaging be biodegradable (including a strong emphasis on films for e-commerce and food service), China is on pace to redefine global supply chains, making it the premier source for both commodity and high-performance biopolymer films in retail, agriculture, and logistics.

Japan Delivering High-Performance Biopolymer Films for Food, Electronics, and Marine Applications

Japan is at the forefront of advanced biopolymer film innovation, combining material excellence with regulatory and consumer-driven adoption. Mitsubishi Chemical’s bio-PBS films and Toray’s transparent PLA-based films set the standard for food trays, shrink films, and electronics packaging, meeting the needs of leading brands like Sony and Panasonic. Mitsubishi Chemical is actively introducing new grades of bio-PBS films in 2025, optimized for high-temperature resistance and improved barrier properties, catering to the evolving demands of convenience food packaging. Toray is also expanding the applications for its transparent PLA films, including more widespread use in anti-static packaging for sensitive electronics components. Japan is also moving aggressively into marine-biodegradable applications, with Kaneka’s PHBH films receiving international certifications. Kaneka's PHBH films are gaining traction in 2025, with new partnerships in the marine leisure industry for fishing tackle packaging and in aquaculture for biodegradable netting applications, driven by their proven marine biodegradability. Recent METI funding has accelerated home-compostable film R&D, supporting both food and non-food uses. Japan’s technical rigor, proactive policy, and industry commitment ensure it remains a leading force in high-performance, application-specific biopolymer film development for both domestic and global markets.

Netherlands Leading Commercialization of Plant-Based and High-Barrier Biopolymer Films

The Netherlands continues to lead the way in commercializing plant-based and high-barrier biopolymer films, thanks to a robust R&D ecosystem and a commitment to circular packaging solutions. Avantium’s PEF films offer a renewable, high-barrier alternative to PET, gaining traction in beverage and snack packaging. Avantium's PEF Flagship Plant is on track for full commercial production by early 2026, and in 2025, it is actively conducting scale-up trials with multiple brand partners for PEF film applications in flexible packaging and bottle labels, indicating strong market readiness. Corbion’s high-barrier PLA films are expanding the options for transparent, bio-based laminates used in a variety of consumer products. Corbion is unveiling new high-barrier PLA film solutions in 2025, specifically engineered for challenging food packaging applications requiring extended shelf life, leveraging enhanced moisture and oxygen barrier properties. Coca-Cola’s pilot testing of PEF films for bottle labels and the recent EU Horizon Grant for PEF commercialization underscore the country’s pivotal role in advancing the biopolymer films sector. Coca-Cola's internal targets for 2025 include a significant reduction of virgin plastic, and while the PEF bottle label pilot's full commercial rollout is anticipated post-2025, the pilot results are influencing future sustainable packaging strategies. The EU Horizon Grant continues to foster collaborative PEF research and commercialization efforts, with key breakthroughs expected in film processing and end-of-life solutions in the latter half of 2025. The Netherlands’ expertise in bringing lab-scale innovation to industrial-scale production makes it a critical player in the future of sustainable packaging.

Biopolymer Films Market Report Scope

Biopolymer Films Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$7.4 Billion

|

|

Market Size (2034)

|

$15.4 Billion

|

|

Market Growth Rate

|

8.5%

|

|

Segments

|

By Material Type (Polylactic Acid (PLA) Films, Polyhydroxyalkanoates (PHA) Films, Starch-Based Films, Cellulose-Based Films, Polybutylene Adipate Terephthalate (PBAT) Films, Polybutylene Succinate (PBS) Films, Polyvinyl Alcohol (PVA) Films, Bio-Polyethylene (Bio-PE) Films, Bio-Polyethylene Terephthalate (Bio-PET) Films, Others), By Film Type (Mono-layer Films, Multi-layer Films, Coated Films), By Application (Packaging, Agriculture & Horticulture, Hygiene & Medical, Others)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

NatureWorks LLC (U.S.), Novamont S.p.A. (Italy), BASF SE (Germany), TotalEnergies Corbion (Netherlands), Danimer Scientific (U.S.), Mitsubishi Chemical Group Corporation (Japan), Braskem S.A. (Brazil), Innovia Films (part of CCL Industries Inc.) (UK/Canada), Mondi Group (Austria/UK), Huhtamaki Oyj (Finland), Amcor Plc (Switzerland/Australia), Taghleef Industries (Ti) (UAE), BioBag International AS (Norway), Cosmo Films Limited (India), Jindal Poly Films Ltd. (India), PTT MCC Biochem Company Limited (Thailand), FKuR Kunststoff GmbH (Germany), Green Dot Bioplastics (U.S.), Plantic Technologies Limited (Australia), Futamura Chemical Co., Ltd. (Japan), Kaneka Corporation (Japan), CJ Biomaterials Inc. (South Korea), Polymateria Ltd. (UK), Tipa Corp. (Israel), and Others.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Biopolymer Films Market Segmentation

By Material Type

- Polylactic Acid (PLA) Films

- Standard PLA Films

- High-Heat PLA Films

- Polyhydroxyalkanoates (PHA) Films

- Starch-Based Films

- Thermoplastic Starch (TPS) Films

- Starch Blended Films

- Cellulose-Based Films

- Cellophane

- Cellulose Acetate Films

- Polybutylene Adipate Terephthalate (PBAT) Films

- Polybutylene Succinate (PBS) Films

- Polyvinyl Alcohol (PVA) Films

- Bio-Polyethylene (Bio-PE) Films

- Bio-Polyethylene Terephthalate (Bio-PET) Films

- Others

By Film Type

- Mono-layer Films

- Multi-layer Films

- Coated Films

By Application

- Packaging

- Agriculture & Horticulture

- Hygiene & Medical

- Others

Countries Analyzed

- North America (US, Canada, Mexico)

- Europe (Germany, UK, France, Spain, Italy, Russia, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, South East Asia, Rest of Asia)

- South America (Brazil, Argentina, Rest of South America)

- Middle East and Africa (Saudi Arabia, UAE, Rest of Middle East, South Africa, Egypt, Rest of Africa)

Top Companies in the Biopolymer Films Market

- NatureWorks LLC (US)

- Novamont S.p.A. (Italy)

- BASF SE (Germany)

- TotalEnergies Corbion (Netherlands)

- Danimer Scientific (US)

- Mitsubishi Chemical Group Corporation (Japan)

- Braskem S.A. (Brazil)

- Innovia Films (part of CCL Industries Inc.) (UK/Canada)

- Mondi Group (Austria/UK)

- Huhtamaki Oyj (Finland)

- Amcor Plc (Switzerland/Australia)

- Taghleef Industries (Ti) (UAE)

- BioBag International AS (Norway)

- Cosmo Films Limited (India)

- Jindal Poly Films Ltd. (India)

- PTT MCC Biochem Company Limited (Thailand)

- FKuR Kunststoff GmbH (Germany)

- Green Dot Bioplastics (US)

- Plantic Technologies Limited (Australia)

- Futamura Chemical Co., Ltd. (Japan)

- Kaneka Corporation (Japan)

- CJ Biomaterials Inc. (South Korea)

- Polymateria Ltd. (UK)

- Tipa Corp. (Israel)

* List Not Exhaustive

Methodology

The Global Biopolymer Films Market Outlook 2025–2034 report employs a rigorous, multi-stage research process that emphasizes data verification, reliability, and strategic depth. Unlike conventional market reports relying on commercial research firms, this study is built exclusively on:

- Primary Research: Direct engagement with over 100 industry stakeholders, including biopolymer film manufacturers, resin producers, film converters, brand owners, sustainability officers, R&D heads, and regulatory bodies across global markets. Interviews and surveys focused on technology adoption, market trends, capacity expansions, and regulatory impacts provide unique, firsthand insights.

- Secondary Research: Exhaustive examination of:

- Corporate annual reports and investor presentations

- Sustainability and regulatory filings (e.g., EU PPWR, California SB 54)

- Patent databases and technical papers from leading institutes (Fraunhofer, METI Japan, CNR Italy, etc.)

- Conference proceedings (e.g., K 2025, BioPlastics Europe, PACK EXPO)

- Scientific publications on biopolymer film innovation, barrier technologies, and biodegradability

- Industry association publications (e.g., European Bioplastics, SPI Bioplastics Council)

- Market Sizing & Forecasting:

- Bottom-up analysis: Aggregated capacity data, known production expansions, application-specific consumption patterns, and trade flows.

- Top-down validation: Macro-level demand modeling is influenced by regulatory policy timelines, brand commitments, and historical consumption trends.

- Scenario analysis: Sensitivity checks on variables such as resin feedstock prices, regulatory delays, technological adoption rates, and macroeconomic conditions.

This approach ensures highly defensible, factual forecasts and practical insights for strategic decision-making.

Research Coverage

The report delivers in-depth analysis across:

- Geographic Scope:

Coverage of over 25 countries in North America, Europe, Asia Pacific, South America, and the Middle East & Africa, with granular detail on leading markets such as the U.S., Germany, China, Japan, India, and Brazil.

- Market Segmentation:

- By Material Type: Polylactic Acid (PLA), PHA, starch-based, cellulose-based, PBAT, PBS, PVA, bio-PE, bio-PET, and emerging materials.

- By Film Type: Mono-layer films, multi-layer films, and coated films.

- By Application: Packaging, agriculture & horticulture, hygiene & medical, others.

- Competitive Landscape:

- Detailed company profiles for over 20 leading producers and emerging innovators.

- Analysis of production capacities, strategic partnerships, sustainability initiatives, R&D investments, and technological differentiators.

- Updates on bankruptcies, M&A activity, and capacity expansions shaping competitive dynamics.

- Key Focus Areas:

- Advanced barrier technologies in compostable films

- Regulatory drivers and timelines shaping global demand

- Cost structure evolution for biopolymer films vs. traditional plastics

- End-use adoption patterns in food packaging, agriculture, hygiene, electronics, and marine applications

- Sustainability certifications and lifecycle analysis considerations

- Emerging applications such as marine-degradable films and industrial films

- Data Horizon:

Historical market data for 2021–2024, with forecasts through 2034.

Deliverables

Clients receive a comprehensive suite of deliverables, designed to enable strategic planning and market execution:

- Main Report (PDF & Excel):

Detailed narrative insights, market dynamics, segmentation forecasts, and competitive intelligence.

- Segment and Country-Level Data Files:

Volume and revenue projections by country, material, film type, and end-use.

- Detailed Company Profiles:

Including production capacities, product portfolios, strategic initiatives, and R&D pipelines.

- Regulatory Tracker:

In-depth review of global and regional regulations influencing biopolymer film adoption (e.g., EU PPWR, SB 54, China plastic bans).

- Executive Summary:

Key insights, high-level market drivers, and strategic recommendations.

- Analyst Support:

Post-delivery assistance for data queries, custom data cuts, and strategic discussions to support decision-making.