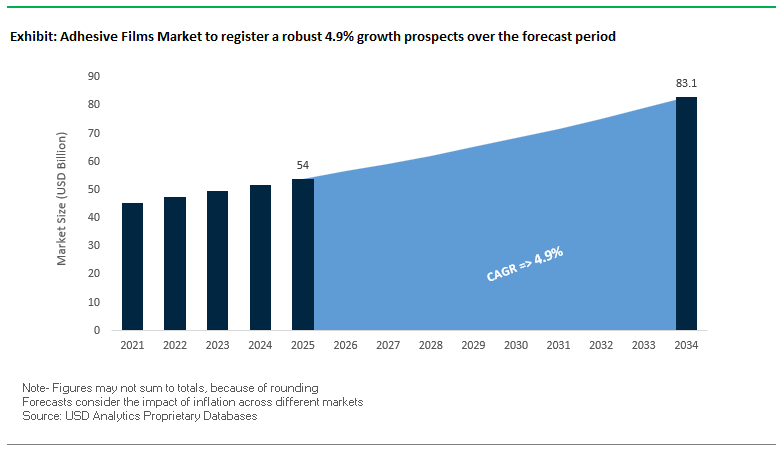

The global adhesive films market, projected to expand from USD 54 billion in 2025 to USD 83.1 billion by 2034 (CAGR 4.9%), is increasingly defined by its role as a functional engineering layer rather than a simple bonding medium. Across packaging, automotive, electronics, construction, and graphics, manufacturers such as 3M, Henkel, Avery Dennison, Covestro, Intertape Polymer Group, and Nitto Denko are positioning adhesive films as multifunctional systems that simultaneously deliver adhesion, protection, insulation, optical performance, and durability under demanding service conditions.

From a manufacturing perspective, adhesive film demand is being shaped by high-speed lamination compatibility, substrate diversity, and performance reliability over extended lifecycles. Polyolefin-based films (PP, PE) continue to dominate high-volume applications because they align with automated packaging lines, chemical resistance requirements, and recyclability targets, while acrylic adhesive systems remain the preferred chemistry for automotive, electronics, and industrial uses due to their long-term adhesion stability, UV resistance, and temperature tolerance. Leading suppliers emphasize adhesive–film–substrate interaction engineering, optimizing coat weight, viscoelastic response, and surface energy matching to support consistent bonding across metals, polymers, glass, and composites.

The market is also undergoing a pronounced sustainability-driven reformulation cycle. Major producers are investing in low-VOC, solvent-free, and recyclable multilayer film architectures, driven by brand-owner requirements and tightening regulations. Examples include PCR-content polyolefin films, mono-material laminates, and debonding-on-demand adhesive layers designed to enable end-of-life separation and recycling—capabilities increasingly demanded in packaging, EVs, and electronics. In parallel, demand is accelerating for high-performance specialty films offering UV stability, thermal resistance, optical clarity, and surface protection, particularly in graphics, electronics assembly, automotive interiors, and construction membranes.

Adhesive Films Market Analysis: Strategic Developments and Industry Direction

The adhesive films industry continues to evolve through strategic mergers, product innovations, and sustainability commitments that redefine market dynamics. In June 2025, Covestro AG announced the acquisition of Pontacol, a Swiss manufacturer of multilayer adhesive films. This acquisition expands Covestro’s specialty film portfolio and strengthens its European manufacturing base, targeting growth markets such as medical technology and mobility, both of which require high-performance multilayer bonding solutions.

In September 2025, 3M Company joined the JOINT3 Consortium, an initiative focusing on next-generation semiconductor packaging. This collaboration demonstrates 3M’s emphasis on co-innovation for electronic adhesive films, supporting precise bonding in miniaturized electronics. Earlier in March 2025, Henkel AG unveiled its Net-Zero Roadmap, aiming for full climate neutrality in Scope 1 and 2 emissions by 2035—an initiative influencing sustainable adhesive film manufacturing and raw material sourcing across its global operations.

Strategic moves across 2024–2025 further reinforced the industry’s competitive momentum. In November 2024, INX Group Limited completed the acquisition of Coatings & Adhesives Corporation (C&A), integrating complementary packaging adhesive solutions under INX International Coatings and Adhesives. Similarly, Intertape Polymer Group (IPG) launched the ExlfilmPlus® PCR polyolefin shrink film in February 2024, containing 35% recycled content, marking a milestone in eco-friendly packaging films. Meanwhile, 3M’s investment in green hydrogen technology (July 2024) aligns with the broader market goal of decarbonizing adhesive film manufacturing, while the 100-year milestone of 3M’s Scotch Brand underscores the industry’s enduring legacy of innovation and material science excellence.

The global transition toward a circular materials economy is accelerating the development of debonding-on-demand (DoD) adhesive films that can enable component separation, repair, and material recovery without compromising bond strength during a product’s functional lifecycle. The emerging class of smart adhesive films is revolutionizing recycling protocols, particularly in the electronics and automotive sectors, where modular assembly and disassembly are critical for sustainability and cost recovery.

Henkel is a front-runner in the domain, promoting its debonding-on-demand adhesive films for EV battery recycling and second-life repair applications. These structural films, capable of maintaining bond strengths up to 12 MPa, can be selectively released via heat or electrical triggers—facilitating the safe disassembly of high-voltage battery modules. The innovation aligns with global EV sustainability goals by reducing waste and improving circular manufacturing efficiency.

Likewise, a 2024 trial by Avery Dennison and The National Test Center Circular Plastics demonstrated that its polymeric film adhesives used on rigid HDPE containers can be completely released during cold-temperature washing. The breakthrough supports closed-loop recycling systems by validating that standard adhesive films can coexist with existing recycling-compatible polymeric materials. Complementing these industrial efforts, Fraunhofer IFAM continues to pioneer electrically responsive adhesives that release at room temperature for delicate electronics disassembly—a vital step toward sustainable consumer electronics recycling and component recovery.

As electronic devices become smaller yet more powerful, managing heat without adding mechanical complexity is a growing challenge. The industry’s response has been the development of thermally conductive adhesive films that not only provide structural bonding but also act as efficient heat transfer media—replacing mechanical fixings and thermal greases in high-density electronic assemblies.

In EV battery systems, these films are crucial for thermal management, achieving thermal conductivity values ranging from 0.6 W/(m·K) to 5 W/(m·K) to efficiently dissipate heat between cells and cooling plates. The lightweight, flexible approach improves battery lifespan, energy efficiency, and system safety. Further, research published in ACS Applied Materials & Interfaces demonstrated a breakthrough elastomer-based structural adhesive with 22 times higher impact resistance than epoxy-based alternatives, enhancing the bonding strength of aluminum and fiber-reinforced plastics in automotive lightweighting applications.

On the industrial front, 3M continues to lead with a comprehensive portfolio of thermally conductive adhesive transfer tapes and pads offering dielectric strengths up to 3 kV. These advanced materials are essential for power transistors, IC packages, and 5G infrastructure, where they simultaneously provide electrical insulation and thermal dissipation. As the data center and telecommunications sectors scale globally, adhesive film solutions offering dual conductivity and insulation are gaining rapid traction as the backbone of next-generation thermal management systems.

The Perovskite Solar Cell (PSC) segment represents one of the most transformative opportunities for the adhesive films industry. The sensitivity of perovskite materials to moisture and heat has created a demand for optically clear, hermetic adhesive films capable of encapsulating and protecting cells without compromising transparency or electrical performance.

A recent study demonstrated that using a commercial polyimide (PI) tape with silicone adhesive as an encapsulation medium enabled a PSC to retain 96.3% of its original power conversion efficiency after prolonged water exposure under continuous illumination—proving that adhesive films can serve as both a moisture barrier and mechanical protector. In addition, adhesive encapsulants address critical degradation factors such as ion migration and thermal stress, two major hurdles limiting PSC longevity in real-world conditions.

Academic studies emphasize that hermetic encapsulation using high-barrier adhesive films is essential for stabilizing PSCs during damp-heat and high-humidity tests. The next generation of adhesive film barrier materials is being designed to extend PSC life cycles beyond 10,000 hours while maintaining optical and electrical integrity. As perovskite solar technologies move from laboratory-scale to commercial deployment, adhesive encapsulation films will become indispensable for thin-film solar cell manufacturing, flexible PV modules, and lightweight energy devices.

The evolution of structural and 3D electronics—such as integrated antennas, curved lighting modules, and embedded sensors—has unlocked new opportunities for conformable adhesive films. These advanced materials enable direct bonding to complex, non-planar geometries without wrinkling, delamination, or stress concentration, supporting the rise of in-mold and post-mold electronics integration.

Recent academic breakthroughs have demonstrated spiral circuit fabrication on hemispherical and saddle-shaped substrates using transfer printing methods reliant on hyperelastic polymeric adhesive systems. These systems ensure high geometric precision, maintaining a conformal area deviation rate below 1%, which is essential for precision electronics like automotive sensors and flexible displays.

Further, research into pressure-sensitive adhesive (PSA) films reports that substrate curvature directly influences adhesion and crack propagation—driving the need for films with tunable elasticity, adhesion energy, and bending modulus. Such advancements are critical for next-generation curved displays, wearable electronics, and integrated vehicle lighting systems, where durability and optical performance must coexist with flexibility.

By combining elasticity, adhesion precision, and material uniformity, these conformable adhesive films are enabling direct-to-shape electronics manufacturing, paving the way for lighter, smarter, and design-flexible electronic architectures across automotive, consumer, and aerospace sectors.

Adhesive Films Market Share Insights, 2025-2034

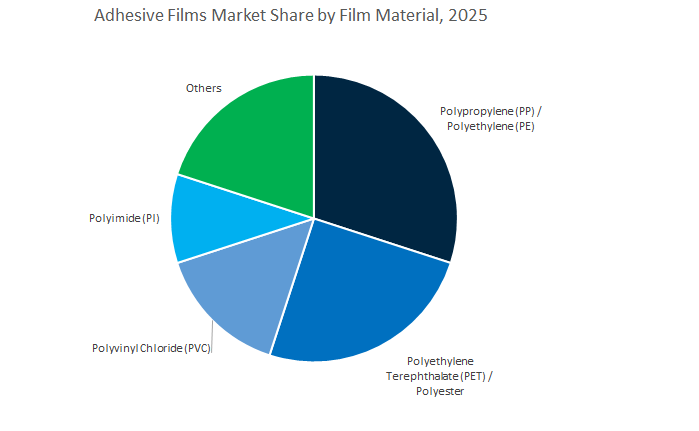

The polypropylene (PP) and polyethylene (PE) segment leads the global adhesive films industry, commanding an estimated 30% market share in 2025. These polyolefin-based adhesive films dominate the market due to their cost efficiency, chemical resistance, and versatility across mass-volume applications. Their flexibility, moisture resistance, and excellent adhesion to diverse surfaces make them the preferred choice for packaging tapes, pressure-sensitive labels, and general-purpose laminates. As sustainability becomes a top priority, PP and PE are gaining additional traction for being recyclable and compatible with circular packaging systems. The rapid expansion of e-commerce and consumer goods packaging, coupled with growing demand for lightweight and durable films in logistics and product branding, is reinforcing their leadership. Furthermore, innovations in biaxially oriented films (BOPP, BOPE) and co-extruded multi-layer film structures are improving performance characteristics like printability, clarity, and tensile strength, allowing polyolefin adhesive films to capture new industrial and decorative applications globally.

The polyethylene terephthalate (PET) and polyester films segment, holding approximately 25% market share, serves as the high-performance backbone of the adhesive films market. PET adhesive films are prized for their dimensional stability, mechanical strength, clarity, and temperature resistance, making them indispensable in electronics, electrical insulation, and optical bonding applications. Their adoption in flexible printed circuits, display laminations, and industrial protective films is expanding rapidly as industries prioritize materials that combine thermal durability and transparency. In the graphic arts and industrial laminates segments, polyester adhesive films are favored for their excellent surface uniformity and compatibility with both water-based and solvent-based adhesives. As the electronics and EV industries increasingly demand heat-resistant and low-shrinkage substrates, PET films are evolving through enhanced coating technologies and ultra-thin formulations designed for precision electronic assembly. This segment’s steady growth underscores its critical role as the bridge between high-volume packaging films and ultra-high-performance materials like polyimide.

The PVC adhesive films segment, though smaller in volume than polyolefins and PET, remains important across decorative, industrial, and construction uses due to its flexibility, printability, and chemical resistance, supporting applications such as vinyl graphics, laminates, signage, labels, and electrical insulation. Regulatory pressure on chlorine-based materials is encouraging a shift toward eco-friendly PVC alternatives, prompting manufacturers to adopt phthalate-free formulations, recyclable vinyl, and bio-based plasticizers. In contrast, the polyimide films segment represents the highest-performance tier of the adhesive films market, offering exceptional thermal stability, dielectric strength, and chemical resistance that make it indispensable in electronics, aerospace, semiconductors, and EV thermal management. As device miniaturization and EV battery innovation accelerate, demand for polyimide films is rising, especially in Asian semiconductor hubs, and despite their higher cost, their unmatched performance ensures sustained adoption in mission-critical applications.

The packaging segment remains the largest consumer of adhesive films globally, holding around 28% of total market share in 2025. The dominance of this sector is propelled by the surge in flexible packaging, pressure-sensitive labels, and sealing tapes, all critical to the global food, beverage, and e-commerce logistics industries. Adhesive films enable secure bonding, tamper-evidence, and product branding while supporting high-speed automated packaging lines. Polyolefin and PVC films dominate this space, offering an optimal balance of cost, flexibility, and print quality. The ongoing shift toward sustainable packaging solutions, including mono-material and recyclable film laminations, is redefining adhesive film design, with brands increasingly demanding eco-friendly, solvent-free, and compostable adhesives. As major consumer brands prioritize plastic reduction and recyclability compliance, adhesive films with low-VOC coatings and biodegradable substrates are witnessing rapid adoption, securing packaging’s position as the largest and most resilient market segment.

The electronics and electrical segment, with approximately 22% of global market share, represents the most technology-intensive and high-value sector for adhesive films. These films play a critical role in display lamination, die attachment, wafer dicing, insulation, and circuit protection, providing thermal stability, dielectric insulation, and mechanical integrity. PET and polyimide films dominate here due to their high purity, dimensional control, and heat resistance, making them indispensable in smartphones, wearable electronics, flexible displays, and semiconductor assembly. The growing electrification trend—spanning EV battery systems, solar modules, and 5G infrastructure—continues to expand the scope of advanced adhesive films. Furthermore, the development of optically clear adhesive (OCA) films for OLED and touchscreen displays is fueling innovation in high-transparency and anti-reflective coatings. This segment’s emphasis on precision engineering and reliability ensures steady growth, supported by continuous advancements in thin-film deposition, nano-adhesive coatings, and hybrid polymer films.

The automotive and transportation sector is rapidly becoming a major growth driver for adhesive films, supported by the industry’s shift toward lightweighting, electrification, and modular design. Adhesive films replace traditional fasteners in interior assembly, surface protection, emblem bonding, and acoustic insulation, while electric vehicles depend on high-performance thermal and double-sided films for battery modules, sensors, and heat management. Parallel to this, the building and construction segment continues to hold a strong, stable share as adhesive films are used extensively in insulation systems, moisture barriers, flooring, roofing membranes, HVAC insulation, glazing, and protective laminates, with new formulations offering UV resistance, self-healing properties, and improved thermal performance. Although smaller in scale, the medical and healthcare segment delivers high-value opportunities, leveraging biocompatible and breathable adhesive films for wound care, drug delivery, surgical applications, and diagnostic devices, and experiencing steady growth as wearable health technologies advance.

The global adhesive films market is characterized by high technological differentiation, with top manufacturers competing through sustainability, innovation, and process integration. Companies such as 3M, Henkel, Nitto Denko, Avery Dennison, and Covestro dominate the landscape with strong R&D capabilities and geographically diverse production networks.

3M Company, headquartered in St. Paul, Minnesota, remains a technological pioneer in advanced performance adhesive films. Leveraging over 51 proprietary technology platforms—including nanotechnology and microreplication—it has created differentiated solutions for high-demand sectors like automotive, aerospace, and electronics. In September 2025, 3M joined the JOINT3 Consortium, strengthening its presence in semiconductor adhesive films. Core products such as the 3M™ 200MP High Performance Acrylic Adhesive continue to lead in high-durability bonding. Its 2024 investment in green hydrogen technology further cements 3M’s leadership in sustainability-driven industrial innovation.

Henkel AG, based in Düsseldorf, Germany, stands as a global leader in adhesive technologies, delivering solutions across 800 industry segments. The company restructured its Adhesive Technologies division in 2023, optimizing financial efficiency for fiscal year 2024. Through its Inspiration Center Düsseldorf (ICD), Henkel fosters co-development with industrial partners to produce functional adhesive coatings and high-bonding films, underscoring its commitment to ESG and customer-centric innovation.

Nitto Denko, headquartered in Osaka, Japan, excels in functional adhesive film technologies for electronics and medical applications. The company invests around ¥50 billion annually in R&D, fueling innovation in sensor films for IoT devices and ultra-thin polarizing films. Recognized as a Clarivate Top 100 Global Innovator in both 2024 and 2025, Nitto continues to pioneer products like the REVALPHA thermal release sheet, essential in advanced display and semiconductor adhesive systems. Its focus on intellectual property and flexible film design secures its position among the most innovative material solution providers.

Avery Dennison Corporation, headquartered in California, specializes in labeling and functional materials with strong emphasis on sustainability and customization. The company’s adhesive tapes and films are designed for electronics, insulation, and component joining applications, known for thermal stability and high adhesion. It is advancing hot melt adhesive tapes with enhanced water resistance, addressing industry needs for high-performance and durable solutions. Avery Dennison’s science-driven approach ensures compliance with evolving environmental standards while maintaining superior functional performance in specialty adhesive films.

Covestro AG, based in Leverkusen, Germany, has taken a major strategic step with its June 2025 acquisition of Pontacol, expanding its specialty adhesive films business into high-value areas such as medical technology, mobility, and textiles. The acquisition adds two advanced manufacturing sites in Switzerland and Germany, boosting Covestro’s European production footprint. The company’s climate neutrality goal for Scope 1 and 2 emissions by 2035 and Scope 3 by 2050 reinforces its sustainability leadership. By integrating multilayer thermoplastic film technologies, Covestro positions itself as a key innovator in next-generation performance adhesive films.

China remains the global epicenter of adhesive film production, leveraging its massive electronics, automotive, and renewable energy sectors to dominate global consumption and export supply. Under the “Made in China 2025” initiative, the government continues to prioritize domestic innovation and localization of high-performance adhesive materials, driving significant R&D into high-temperature resistant polyimide (PI) films and solvent-free adhesives.

The surge in OLED panel and flexible display manufacturing is fueling robust demand for optically clear adhesive films (OCA), which are essential for foldable smartphones, tablets, and advanced infotainment systems. Simultaneously, local and global material companies are injecting large-scale investments into hot-melt adhesive film plants that serve the rapidly expanding EV battery assembly market, particularly for thermal interface and encapsulation applications.

Chinese automotive OEMs are increasingly standardizing structural adhesive films to achieve vehicle lightweighting and NVH (Noise, Vibration, Harshness) control, supporting the shift toward electric mobility. Moreover, regulatory frameworks promoting low-VOC and sustainable adhesives are accelerating the adoption of eco-friendly formulations in both consumer electronics and automotive manufacturing. In parallel, China’s film and tape converting sector is scaling high-speed roll-to-roll coating systems, catering to medical and industrial-grade PSA film production. The strategic moves solidify China’s status as a sustainability-driven, innovation-rich hub in the global adhesive films supply chain.

The United States adhesive films market is a hub of high-performance material innovation, powered by aerospace, defense, medical, and advanced electronics industries. U.S.-based specialty chemical corporations are developing next-generation epoxy film adhesives with enhanced toughness, peel strength, and durability, specifically for carbon composite bonding in commercial and defense aerospace applications.

Recent federal and private R&D initiatives have yielded breakthroughs in electrically conductive adhesive films tailored for flexible electronics, wearables, and IoT devices. Concurrently, several U.S. companies have committed multi-million-dollar investments to expand polyurethane film production for automotive interiors, EV assemblies, and heat-resistant exterior applications. Regulatory guidance from the U.S. Food and Drug Administration (FDA) has spurred innovation in biocompatible and skin-friendly medical adhesive films, particularly for transdermal drug delivery systems and wound dressings.

Federal programs under the Department of Energy (DOE) are indirectly influencing market growth through funding in thermal management films designed for EV battery cooling and high-power electronics. Moreover, U.S. defense and satellite manufacturers are increasingly adopting transfer adhesive films for precision bonding in complex component assembly, reinforcing the country’s technological dominance. The synergy between government-backed R&D, industrial innovation, and sustainability mandates ensures that the U.S. remains a front-runner in advanced adhesive film solutions for strategic applications.

Germany continues to lead the European adhesive films market, renowned for its sustainability focus, engineering precision, and industrial innovation. Driven by the EU’s circular economy targets, major German producers are rapidly transitioning toward water-based and solvent-free adhesive film systems, replacing conventional petrochemical formulations. Industry leaders are aligning R&D with the European Green Deal, promoting the large-scale use of bio-based polymer films in packaging and consumer goods.

Collaboration between automotive Tier-1 suppliers and adhesive producers is intensifying to develop B-stage thermosetting films for EV battery-to-chassis bonding, improving structural integrity, crash resistance, and long-term durability. German materials firms have filed multiple patents for low-outgassing adhesive films, a critical advancement for luxury vehicle interiors, cockpit displays, and smart glass applications.

Government-backed research consortia are exploring smart adhesive films with embedded sensors to monitor structural health and performance in industrial and aerospace machinery. Additionally, German converters are expanding their lamination and coating capacities, supporting the demand for graphic films, industrial tapes, and architectural protection films. With a strong blend of environmental responsibility, process innovation, and product specialization, Germany remains Europe’s benchmark market for sustainable adhesive film manufacturing.

Japan continues to dominate the global high-precision adhesive films industry, underpinned by its leadership in microelectronics, optics, and automotive innovation. The country’s electronics giants are driving strong demand for ultra-thin adhesive films (<25μm) and anisotropic conductive films (ACF), essential for semiconductor interconnections, micro-LED packaging, and display bonding.

Key Japanese material companies are investing in barrier adhesive film R&D, critical for OLED encapsulation and protection of sensitive organic components in flexible electronics. The automotive sector is equally influential, utilizing heat-activated structural adhesive films to bond dissimilar materials such as composites, plastics, and metals, improving crash performance and vehicle integrity.

Meanwhile, Japanese producers are scaling pressure-sensitive adhesive (PSA) films with ultra-high transparency and low haze, catering to next-generation display stack-ups and optical films. Government-backed initiatives continue to strengthen domestic supply chains for acrylic, silicone, and PI-based adhesive film precursors. Manufacturers are also expanding capacity for industrial and protective tapes, particularly for construction, heavy machinery, and electronics protection. Japan’s unique combination of material science expertise, robotics integration, and sustainable innovation cements its role as a global leader in precision adhesive film technology.

South Korea has solidified its position as a global innovation hub for display-grade and functional adhesive films, leveraging its strengths in OLED, semiconductor, and EV manufacturing. Major display manufacturers are securing localized OCA (Optically Clear Adhesive) supply chains through co-development partnerships with domestic material suppliers, ensuring greater control over production quality and intellectual property.

Extensive investments in roll-to-roll manufacturing are improving production efficiency and yield for flexible and foldable displays, addressing the needs of global smartphone and tablet makers. The nation’s rapid EV adoption is driving strong demand for thermal conductive adhesive films that ensure battery cell-to-module bonding stability and effective heat dissipation.

South Korean material science firms are filing increasing numbers of patents for removable and reworkable adhesive films, a vital innovation enabling electronics recycling and repairability. Simultaneously, local coating companies are expanding facilities to meet rising demand for functional films used in semiconductor fabrication, including protective and anti-static coatings. Government-led incentives for homegrown high-performance polymers further strengthen South Korea’s role as a self-sustaining leader in advanced adhesive and functional film technologies.

Adhesive Films Market Report Scope

Adhesive Films Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$54 Billion

|

|

Market Size (2034)

|

$83.1 Billion

|

|

Market Growth Rate

|

4.9%

|

|

Segments

|

By Resin Type (Acrylic Adhesive Films, Epoxy Adhesive Films, Polyurethane (PU) Adhesive Films, Silicone Adhesive Films, Polyvinyl Butyral (PVB) Adhesive Films, Others), By Film Material/Backing (Polypropylene (PP), Polyethylene (PE), Polyvinyl Chloride (PVC), Polyethylene Terephthalate (PET), Polyimide (PI), Polyester, Others), By Technology/Curing (Pressure-Sensitive Adhesive (PSA) Films, Hot-Melt Adhesive Films, Solvent-Based Films, Water-Based Films, UV-Cured/Light-Cured Films, Reactive Adhesive Films), By Function (Optically Clear Adhesive (OCA) Films, Die-Attach Films (DAF), Thermal Conductive Films, Electrically Conductive Films, Structural Bonding Films, Protective Films, Flexible Circuit Films, Barrier Films), By End-Use Industry (Electronics & Electrical, Automotive & Transportation, Packaging, Building & Construction, Medical & Healthcare, Industrial), By Application (Labels, Tapes, Graphic Films, Protective Films, Laminates

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Henkel AG & Co. KGaA, 3M Company, Avery Dennison Corporation, Nitto Denko Corporation, H.B. Fuller Company, Arkema S.A. (Bostik), Dow Inc., Sika AG, DuPont de Nemours, Inc., Tesa SE, Toray Industries, Inc., LINTEC Corporation, LG Chem Ltd., DIC Corporation, Eastman Chemical Company

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

By Resin Type

- Acrylic Adhesive Films

- Epoxy Adhesive Films

- Polyurethane (PU) Adhesive Films

- Silicone Adhesive Films

- Polyvinyl Butyral (PVB) Adhesive Films

- Others

By Film Material/Backing

- Polypropylene (PP)

- Polyethylene (PE)

- Polyvinyl Chloride (PVC)

- Polyethylene Terephthalate (PET)

- Polyimide (PI)

- Polyester

- Others

By Technology/Curing

- Pressure-Sensitive Adhesive (PSA) Films

- Hot-Melt Adhesive Films

- Solvent-Based Films

- Water-Based Films

- UV-Cured/Light-Cured Films

- Reactive Adhesive Films

By Function

- Optically Clear Adhesive (OCA) Films

- Die-Attach Films (DAF)

- Thermal Conductive Films

- Electrically Conductive Films

- Structural Bonding Films

- Protective Films

- Flexible Circuit Films

- Barrier Films

By End-Use Industry

- Electronics & Electrical

- Automotive & Transportation

- Packaging

- Building & Construction

- Medical & Healthcare

- Industrial

By Application

- Labels

- Tapes

- Graphic Films

- Protective Films

- Laminates

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

- Henkel AG & Co. KGaA

- 3M Company

- Avery Dennison Corporation

- Nitto Denko Corporation

- H.B. Fuller Company

- Arkema S.A. (Bostik)

- Dow Inc.

- Sika AG

- DuPont de Nemours, Inc.

- Tesa SE

- Toray Industries, Inc.

- LINTEC Corporation

- LG Chem Ltd.

- DIC Corporation

- Eastman Chemical Company

*- List not Exhaustive

Research Coverage

This report investigates how adhesive films are redefining bonding, protection, and thermal/electrical management across packaging, automotive, electronics, and construction; it consolidates breakthroughs in thermally conductive films, optically clear adhesive (OCA) stacks, recyclable mono-material laminates, and debonding-on-demand architectures into decision-grade insights. Produced by USDAnalytics, the study delivers analysis reviews of performance trade-offs (peel/shear, haze, Tg, thermal conductivity), line convertibility (roll-to-roll, jet/laminate), and spec-in dynamics that influence sourcing and total cost of ownership. It highlights sustainability levers—from low-VOC/water-based chemistries to PCR-compatible films—and maps where innovation raises yield, uptime, and circularity. By translating material science into commercial outcomes, this report is an essential resource for executives, product managers, process engineers, and procurement leaders aligning film portfolios with electrification, lightweighting, and green-building mandates.

Scope Highlights

- By Resin Type: Acrylic, Epoxy, Polyurethane (PU), Silicone, PVB, Others.

- By Film Material/Backing: PP, PE, PVC, PET, PI, Polyester, Others.

- By Technology/Curing: PSA Films, Hot-Melt, Solvent-Based, Water-Based, UV-Cured/Light-Cured, Reactive Films.

- By Function: OCA, Die-Attach Films, Thermal Conductive, Electrically Conductive, Structural Bonding, Protective, Flexible Circuit, Barrier Films.

- By End-Use: Electronics & Electrical; Automotive & Transportation; Packaging; Building & Construction; Medical & Healthcare; Industrial.

- By Application: Labels; Tapes; Graphic Films; Protective Films; Laminates

- Geographic Scope: Analysis spans 25+ countries across North America, Europe, Asia Pacific, Latin America, the Middle East & Africa.

- Historic & Forecast Window: Historic data 2021–2024; forecasts 2025–2034.

- Companies: Analysis/profiles of 15+ companies.

Deliverables

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.