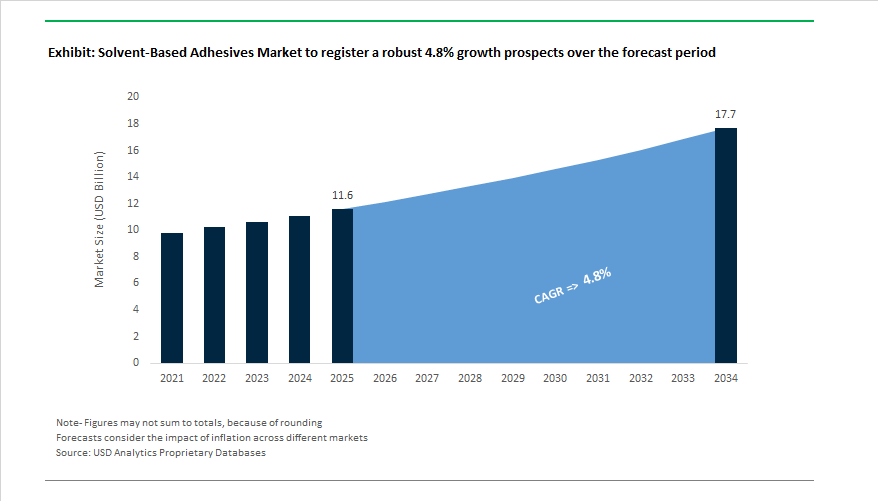

The Global Solvent-Based Adhesives Market is projected to grow from $11.6 billion in 2025 to $17.7 billion by 2034, at a CAGR of 4.8%, supported by enduring applications in automotive interiors, industrial assembly, footwear, construction, and flexible packaging. Despite rising environmental scrutiny, solvent-based adhesives remain irreplaceable in high-performance bonding where heat resistance, initial tack, and substrate versatility are essential.

These adhesives leverage high-strength polymer systems — such as polychloroprene, nitrile, polyurethane, and acrylics — to deliver instant bond strength, durability under mechanical stress, and resistance to heat, humidity, and chemicals. The automotive industry continues to account for a significant share of consumption, with interior bonding adhesives designed to withstand cabin temperatures and prevent delamination in multi-material assemblies (e.g., PET, PP, and composite panels). In these applications, the ability to maintain low VOC emissions while achieving high cohesive strength is a critical design requirement aligned with tightening global automotive environmental regulations.

Regulatory pressure under frameworks such as the European Industrial Emissions Directive (IED) and REACH has led to an ongoing reformulation trend toward high-solids solvent-based systems. These products maintain superior adhesion while cutting VOC emissions by up to 50%, allowing compliance without sacrificing performance. Meanwhile, in the construction and flooring segments, solvent-based adhesives remain vital for their superior wet grab, long open times, and resistance to moisture and temperature variation, key for structural paneling, parquet installation, and façade bonding.

The flexible packaging industry continues to favor polyurethane-based solvent adhesives for lamination, providing excellent interlayer adhesion and chemical resistance required for food and pharmaceutical packaging. Similarly, rubber- and elastomer-based adhesives dominate industrial and footwear sectors, offering high peel strength, instant green bond, and compatibility with foam, leather, and metal substrates.

The global solvent-based adhesives industry is witnessing a blend of technological advancement, sustainability transformation, and regional expansion as manufacturers recalibrate portfolios to align with environmental standards and end-user performance needs.

In April 2025, a major adhesives producer launched a new generation of low-monomer reactive polyurethane hot melt adhesives, demonstrating a market-wide transition away from traditional high-VOC systems. This launch reflects broader industry adaptation to stricter REACH and IED 2.0 emission thresholds, emphasizing low-emission and high-solids alternatives that deliver performance parity with classic solvent systems.

The European Industrial Emissions Directive (March 2025) continues to influence solvent adhesive production, pushing manufacturers toward Best Available Techniques (BAT) in solvent recovery and emission control. The regulation has prompted major producers to re-engineer their production lines, incorporating solvent reclamation units and high-efficiency oxidation systems to maintain competitiveness under new emission caps.

A significant acquisition occurred in February 2025, when a U.S.-based adhesives company expanded into Western Europe by acquiring a specialist manufacturer of high-solids rubber-based adhesives, reinforcing its footprint in industrial insulation and assembly bonding markets. This move highlights a consolidation trend aimed at vertical integration and cross-technology portfolio diversification.

In December 2024, a leading Asian adhesives producer commissioned a new production facility in Southeast Asia to meet surging regional demand for high-performance solvent-based laminating adhesives used in flexible packaging and consumer goods. The new line emphasizes faster cure times and improved thermal resistance, serving as a benchmark for next-generation manufacturing efficiency in high-output packaging environments.

By October 2024, major specialty chemical producers had introduced modified acrylate co-polymers to enhance initial tack and heat resistance in contact adhesives, expanding applicability in furniture, woodworking, and automotive trim assembly. Similarly, a joint R&D initiative launched in July 2024 between a global adhesives company and a leading automotive OEM marked a strategic step toward developing solvent-based structural adhesives for multi-material electric vehicle platforms, addressing crash durability and lightweighting goals.

The market also saw sustained investment activity: in January 2024, a major adhesives producer announced upgrades to its North American solvent-based manufacturing site, enhancing output for footwear and textile bonding applications. Concurrently, by November 2023, a top-tier global manufacturer committed to achieving 80% sustainability compliance across its solvent-based portfolio by 2027 — a signal of the industry’s pivot toward eco-optimized solvent technologies integrating bio-based raw materials and less toxic solvent blends.

Market Trend 1: Accelerated Phase-Out Driven by Stringent VOC and Air Toxics Regulations

The global phase-out of solvent-based adhesives is rapidly intensifying under mounting VOC (Volatile Organic Compound) and HAPs (Hazardous Air Pollutants) restrictions, reshaping product portfolios across the adhesives value chain. Governments in North America, Europe, and Asia-Pacific are enforcing binding VOC thresholds that effectively disqualify traditional solvent-heavy formulations from large-scale production and sale.

For instance, Canada’s 2023 Volatile Organic Compound Concentration Limits for Certain Products Regulations specifically impose emission caps on adhesives and sealants, aligning with commitments under the Gothenburg Protocol for transboundary air pollution control. These regulations reflect a global pattern of enforcement, with parallel measures in regions such as Hong Kong, where the Air Pollution Control (VOC) Regulation governs over 47 adhesive product types—banning import or manufacture of products exceeding prescribed VOC content.

Empirical testing reports that conventional solvent-based adhesives typically contain 85–96% VOC content by weight, compared to less than 10% in compliant low-VOC or water-based alternatives. The data highlights the immense technical challenge of maintaining adhesive performance while adhering to emission caps. As a result, manufacturers are heavily investing in R&D for solvent-replacement technologies, including high-solids, waterborne, and reactive chemistries (like moisture-curing polyurethanes).

The regulatory tightening is not merely compliance-driven; it represents a broader environmental movement toward decarbonized, cleaner manufacturing ecosystems. Companies adapting early through low-VOC reformulation and solvent substitution are gaining strategic advantage in securing eco-label certifications and meeting corporate ESG benchmarks demanded by global construction and automotive OEMs.

Market Trend 2: Strategic Retention in High-Performance, Niche Industrial Applications

Despite the regulatory retreat, solvent-based adhesives continue to hold irreplaceable value in specialized sectors where instant tack, deep substrate penetration, and thermal endurance are critical. The includes aerospace composites, defense structures, automotive lightweighting, and industrial laminates, where alternative chemistries still fall short of delivering equivalent performance.

In the aerospace industry, high-performance solvent-based epoxy and polyurethane adhesives remain essential for structural bonding of dissimilar materials, providing impact resistance and stability up to 140°C. These adhesives maintain mechanical integrity under severe vibration, temperature, and chemical exposure—conditions often beyond the tolerance of waterborne or hot-melt counterparts.

Similarly, in the automotive and EV manufacturing sectors, solvent-borne systems are indispensable for multi-material bonding—specifically steel-aluminum-CFRP joints—where they deliver lightweight yet high-strength adhesion. These properties directly contribute to improved crash safety and lower vehicle weight, critical for EV efficiency.

Chemical durability also underpins solvent adhesive relevance in outdoor, marine, and industrial environments, where exposure to oils, fuels, and UV radiation necessitates robust formulations. As a result, while solvent-based adhesives may exit high-volume commodity markets, they continue to dominate technical-grade and mission-critical segments that require long-term bond stability.

Market Opportunity 1: Development of Low-GWP, Low-Toxicity Solvents for Next-Generation Adhesive Formulations

The transition away from legacy solvents opens a lucrative frontier for next-generation, climate-safe solvent chemistries. These innovations focus on low Global Warming Potential (GWP) and reduced toxicity, bridging the performance gap between traditional solvents and sustainable alternatives.

Leading chemical companies are heavily investing in Hydrofluoroolefin (HFO) and Hydrochlorofluoroolefin (HCFO) technologies, developing new-generation solvents with GWP values 100x lower than conventional HFCs. A notable case includes billion-dollar investments by global firms to expand HFO capacity—targeting use across aerosol, coating, and adhesive solvent systems.

These low-GWP solvent innovations offer strong solvency power while maintaining regulatory compliance under frameworks like the Montreal Protocol and EPA SNAP (Significant New Alternatives Policy). Beyond environmental benefits, such solvents also improve workplace safety by offering non-flammable and low-toxicity profiles, directly addressing manufacturer health and safety concerns.

The successful adaptation of these next-gen solvents in adhesives could enable the continued use of solvent-based systems in precision industries—such as aerospace, electronics encapsulation, and flexible packaging—without the environmental drawbacks associated with legacy chemistries.

Market Opportunity 2: Integration of Closed-Loop Solvent Recovery and Application Systems

For manufacturers unable to fully eliminate solvent-based processes, closed-loop vapor recovery systems present a transformative opportunity to achieve regulatory compliance, cost efficiency, and circular resource utilization. These systems capture, purify, and recycle solvent vapors—turning emissions into reusable assets and minimizing waste generation.

Modern on-site recovery systems, utilizing activated carbon adsorption or distillation, can recover 90% or more of spent solvent waste, drastically reducing VOC emissions and hazardous waste disposal costs. Case studies show that companies implementing solvent recovery technologies cut new solvent purchases by up to 50%, simultaneously lowering operating expenditures (OPEX) and environmental liabilities.

The most advanced models are fully automated closed-loop solvent management systems, capable of collecting waste solvent, distilling it, and reintroducing the purified solvent into the production line. The circular design aligns with “zero liquid discharge” (ZLD) and sustainable manufacturing principles increasingly mandated in chemical and automotive industries.

Beyond cost savings, closed-loop systems strengthen ESG performance metrics by reducing Scope 1 and Scope 3 emissions, while enabling manufacturers to retain the superior performance benefits of solvent-based adhesives in critical operations. The dual advantage—regulatory compliance and operational profitability—is positioning solvent recovery technologies as a defining sustainability trend across the adhesives manufacturing ecosystem.

Solvent-Based Adhesives Market Share Insights, 2025-2034

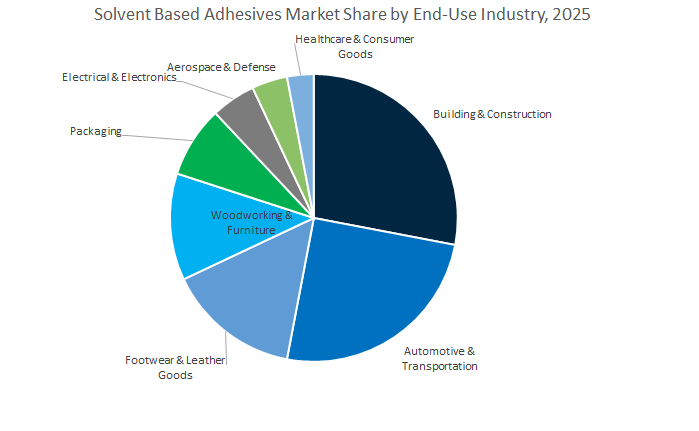

Market Share by End-Use Industry

The Building & Construction sector leads the global solvent-based adhesives market, accounting for an estimated 28.4% of total market share by 2025. This dominance is primarily attributed to solvent-based adhesives’ superior bonding strength, water resistance, and excellent adhesion to porous and non-porous substrates, which make them indispensable in structural and decorative construction applications. These adhesives are widely used in flooring, wall cladding, panel lamination, roofing, and insulation systems, where performance reliability under high humidity and varying temperatures is essential. The construction industry continues to rely on solvent-based formulations for quick bonding and strong mechanical adhesion, particularly in rapid renovation projects and prefabricated building systems. While increasing VOC regulations are prompting gradual adoption of water-based or hybrid alternatives, many contractors and industrial users still prefer solvent-based products due to their proven field performance, long shelf life, and fast-setting properties, which are vital in time-sensitive installations.

The Automotive & Transportation segment remains one of the fastest-growing end-use markets for solvent-based adhesives, driven by applications in vehicle assembly, interior trim, upholstery bonding, and composite component manufacturing. These adhesives provide exceptional durability, heat resistance, and flexibility, which are crucial for automotive and rail systems operating under dynamic conditions. The transition to lightweight materials and electric vehicle production further sustains demand, as solvent-based systems bond dissimilar materials such as metals, plastics, and elastomers with high reliability. Meanwhile, Footwear & Leather Goods continue to represent a strong, traditional market base where solvent-based adhesives are valued for their instant tack, elasticity, and durability under flexing conditions. Despite the emergence of waterborne alternatives, the speed, strength, and consistent bonding performance of solvent-based systems remain critical for mass production in footwear manufacturing hubs across Asia and Latin America.

In Woodworking & Furniture manufacturing, solvent-based adhesives maintain steady demand due to their superior bonding strength on wood composites, veneers, and laminates. They are preferred in edge banding, profile wrapping, and decorative lamination, where immediate handling strength and clear bond lines are essential for production efficiency. Beyond these large-volume sectors, Packaging, Electrical & Electronics, Aerospace & Defense, and Medical & Consumer Goods contribute smaller but technologically advanced portions of the market. In packaging, they are used in laminating flexible films and foil substrates where thermal and chemical resistance are crucial. In electronics and aerospace, solvent-based structural and specialty adhesives provide reliability under extreme conditions, offering unmatched performance in thermal stability and dielectric insulation.

Market Share by Product Type

Contact Adhesives hold the dominant share of the global solvent-based adhesives market, representing approximately 35.9% of total demand by 2025. Their dominance stems from their instant bonding capability, strong adhesion to a wide variety of materials, and suitability for large-surface lamination applications. These adhesives are widely employed in furniture, construction panels, footwear manufacturing, and automotive interiors, where fast assembly and durable joints are critical. The combination of long open time, rapid bond formation, and resilience under heat and moisture makes contact adhesives indispensable for industrial assembly and finishing processes. Their market position remains resilient despite tightening VOC regulations, as industries continue to value their consistent curing behavior and robust bond strength that water-based alternatives cannot yet fully replicate.

Pressure-Sensitive Adhesives (PSAs) and Spray Adhesives follow as significant contributors, particularly in applications requiring ease of application and flexibility. Solvent-based PSAs are used in tapes, labels, and films, delivering strong tack, peel, and shear performance across varying environmental conditions. Spray adhesives, on the other hand, are gaining popularity in automotive upholstery, insulation installation, and general assembly, offering quick, even coating and high productivity. Both these adhesive types benefit from their adaptability across industries and superior adhesion to challenging substrates, including metals, textiles, and composites.

Structural Solvent-Based Adhesives represent a technically advanced segment, serving automotive, aerospace, and industrial assembly applications where high load-bearing capacity, vibration resistance, and environmental durability are mandatory. These adhesives enable manufacturers to achieve lightweighting and improved structural integrity, particularly in bonding aluminum, composite panels, and reinforced plastics. Meanwhile, High-Solids Solvent-Based Adhesives constitute a niche but strategically important category, developed to address VOC emission regulations while maintaining solvent-based performance advantages.

The competitive environment in the solvent-based adhesives market is dominated by global multi-material giants combining chemical innovation, geographic expansion, and regulatory compliance expertise. Leading players—Henkel, H.B. Fuller, Arkema (Bostik), Sika, 3M, and BASF—leverage deep R&D networks to develop high-solids, high-strength solvent-based adhesives tailored for automotive, industrial, and construction end-users.

Henkel’s Adhesive Technologies division is a global leader in automotive bonding and industrial assembly adhesives, emphasizing solvent-based systems with superior heat resistance and cohesive strength. The company’s innovation roadmap centers on sustainability through circular economy design principles and digitally driven R&D for faster market response. Henkel continues to expand its mobility and electronics portfolio while enhancing transparency with life-cycle-based sustainability metrics, cementing its position as a top-tier adhesives innovator.

H.B. Fuller’s extensive product line covers polychloroprene, polyurethane, and nitrile-based adhesives used in footwear, aerospace, automotive, and industrial bonding. Its core strength lies in formulating solutions for challenging substrates—from metals to low-surface-energy plastics—providing high initial tack and low-temperature flexibility. With 81 production sites in 26 countries, Fuller ensures localized technical support and compliance with regional VOC norms. The firm’s balanced approach, offering both solvent-based and next-gen non-solvent adhesives, secures its relevance across evolving regulatory landscapes.

Arkema’s adhesive arm, Bostik, capitalizes on advanced polymer chemistry to deliver smart, high-solids solvent-based formulations for flooring, flexible packaging, and industrial lamination. The company’s R&D centers in France, the U.S., and Asia focus on bio-based and performance-optimized adhesives, aligning sustainability with mechanical excellence. Leveraging Arkema’s upstream polymer synthesis expertise, Bostik continues to set performance benchmarks in construction and transportation adhesives, optimizing strength, durability, and environmental impact.

Sika AG dominates the construction adhesives space, integrating solvent-based polyurethane and reactive technologies into its extensive product lineup. Known for innovation in bonding, damping, and sealing, Sika’s technologies are critical in industrial panel lamination, façade sealing, and modular construction. Its Purform® polyurethane platform exemplifies a strategic move toward low-monomer, safer alternatives, signaling a bridge between traditional solvent-based excellence and the future of sustainable reactive adhesives.

3M continues to lead in industrial bonding and spray adhesive solutions, offering high-tack solvent-based polyurethane and rubber adhesives for transportation, woodworking, and furniture applications. Its proprietary technologies deliver exceptional shear, peel, and thermal stability, essential for high-stress applications. The company also develops high-solids solvent formulations that comply with U.S. VOC regulations, ensuring that productivity, performance, and environmental compliance remain perfectly balanced for industrial users.

BASF serves as the backbone supplier of polyurethane and acrylic polymers essential for solvent-based adhesive manufacturing. Its vertically integrated operations provide high-performance dispersions and polymer systems tailored to enhance chemical resistance, cohesive strength, and substrate adhesion. BASF’s focus on bio-based polymer chemistry and solvent substitution aligns with downstream manufacturers’ sustainability targets, making it a critical enabler in the future evolution of the global solvent-based adhesives value chain.

Country Analysis: Strategic Developments in the Global Solvent-Based Adhesives Market

China: Regulatory Reforms and Industrial Expansion Reinforce Asia-Pacific Market Dominance

China remains the largest producer and consumer of solvent-based adhesives in the Asia-Pacific region, supported by its vast manufacturing base and continuous government-led infrastructure expansion. The nation’s focus on large-scale industrial growth across electronics, automotive, and footwear manufacturing underpins a strong domestic market for high-strength, flexible solvent-based polyurethane adhesives. The government’s active infrastructure push and export-led manufacturing strategy continue to stimulate demand for industrial bonding agents with robust performance and chemical resistance.

In 2021, Henkel AG strengthened its regional presence by inaugurating a major innovation center in Shanghai, aimed at developing next-generation adhesive technologies tailored for Asia-Pacific markets. However, tightening air pollution controls have led to regulatory scrutiny over volatile organic compound (VOC) emissions, compelling manufacturers to reformulate toward low-VOC solvent-based and hybrid adhesive technologies. Studies, such as the 2024 VOC emissions report in Zhengzhou, identified solvent usage as a major source of secondary organic aerosol formation, further accelerating environmental compliance initiatives. Despite The regulations, China’s footwear and leather goods industries remain heavy users of solvent-based systems, while automotive OEMs are rapidly expanding the application of specialty polyurethane adhesives to meet lightweighting and performance needs.

United States: Regulatory Stringency and High-Performance Applications Drive Market Maturity

The United States solvent-based adhesives market is shaped by stringent EPA VOC emission regulations, advanced manufacturing standards, and growing demand from aerospace, electronics, and construction sectors. Continuous environmental oversight by the U.S. Environmental Protection Agency (USEPA) has prompted manufacturers to innovate low-VOC solvent-based formulations and hybrid adhesive systems that balance environmental compliance with industrial strength.

Major corporations like 3M Company are leading technological innovation—launching reactive hot melt adhesives with superior moisture and heat resistance for precision electronics assembly. Simultaneously, significant infrastructure spending on non-residential and residential projects sustains the demand for high-performance polyurethane and epoxy solvent-based adhesives in structural bonding, roofing, and flooring applications. Additionally, the aerospace and defense sectors remain pivotal end users, relying on solvent-based epoxy and polyurethane adhesives that meet rigorous MIL-SPEC and FAA safety standards for thermal and vibration resistance.

Emerging innovation in biomaterial sourcing—such as Conagen’s 2022 development of polymer-based bio-adhesives—is transforming the U.S. market’s sustainability landscape. Regulatory actions like the methylene chloride restriction are also reshaping product portfolios, compelling manufacturers to adopt safer alternatives. Supported by robust R&D funding, high-value end markets, and ongoing mergers and acquisitions (e.g., H.B. Fuller’s Full-Care 5885 introduction), the U.S. continues to serve as a global benchmark for compliant, high-durability solvent-based adhesive solutions.

Germany: European Sustainability and Automotive Engineering Propel Solvent Adhesive Innovation

Germany stands as the technological and regulatory cornerstone of the European solvent-based adhesives industry. Stringent EU frameworks—such as the VOC Solvents Emissions Directive and the Industrial Emissions Directive (IED)—are redefining adhesive production toward low-VOC, high-performance chemistries. The nation’s leadership in precision engineering and sustainable chemistry fosters a continuous pipeline of innovations in automotive bonding, construction, and high-end industrial applications.

Global manufacturers headquartered in Germany, notably Henkel AG & Co. KGaA, drive progress through brands like Loctite and Technomelt, which cater to industrial and MRO (maintenance, repair, and operations) segments worldwide. Parallelly, BASF SE supports the raw materials ecosystem with advanced Acronal dispersions and Elastollan TPU systems, enabling eco-efficient and versatile adhesive formulations. Meanwhile, KLEIBERIT and other specialty firms are scaling the global reach of solvent-based polyester and polychloroprene adhesives, known for their rapid bonding and extreme durability.

Recent strategic activity includes Henkel’s 2024 acquisition of Seal for Life Group, fortifying its presence in sealing and corrosion prevention markets. Combined with the growing automotive focus on lightweight structural bonding and NVH (noise, vibration, and harshness) reduction, Germany continues to define the European standard for performance, compliance, and sustainability in the solvent-based adhesives market.

India: Manufacturing Acceleration and Domestic Industry Expansion Fuel Market Growth

India’s solvent-based adhesives market is witnessing robust expansion, driven by industrial growth, infrastructure investments, and the country’s strategic emergence as a manufacturing hub. In 2024, Henkel India completed Phase III of its Kurkumbh facility, boosting production to meet surging domestic demand across automotive, construction, and consumer goods sectors. Simultaneously, rapid urbanization and government-led programs—such as Smart Cities Mission and PM Awas Yojana—are increasing consumption of durable construction adhesives in glazing, flooring, and waterproofing applications.

Local champions like Pidilite Industries Limited dominate the market through an expansive portfolio spanning woodworking, footwear, and packaging adhesives. The company’s acquisition of Huntsman India’s adhesives business (2020) expanded its footprint in high-performance solvent-based product lines, enhancing its competitive edge in industrial and consumer markets. India’s thriving footwear and leather manufacturing sector—among the world’s largest—remains a critical end-use segment for chloroprene rubber-based solvent adhesives, valued for their flexibility and superior bonding strength.

Japan: Precision Engineering and Specialty Applications Define High-Value Market

Japan’s solvent-based adhesives industry reflects the nation’s expertise in advanced materials science and micro-engineering applications. Key market participants such as LINTEC Corporation and Toagosei Group lead innovation in pressure-sensitive adhesives (PSAs) and solvent-based bonding systems tailored for high-precision electronics, automotive interiors, and semiconductor packaging.

The country’s dominant electronics sector drives significant demand for high-purity, durable, and miniaturization-compatible solvent-based adhesives, particularly for thermal management and micro-component assembly. In addition, automotive OEMs rely on advanced solvent-based polyurethane and acrylic systems for vibration damping, high-temperature bonding, and chemical resistance in electric vehicle powertrains. Japan’s focus on durability, consistency, and purity ensures that its solvent-based adhesive formulations meet stringent international safety and quality standards, keeping the nation at the forefront of specialty adhesive technology for high-performance applications.

South Korea: Automotive Electrification and Electronics Manufacturing Boost Solvent-Based Adhesive Demand

South Korea’s solvent-based adhesives market is thriving, supported by the nation’s dual strengths in automotive manufacturing and consumer electronics production. The rapid transition to Electric Vehicle (EV) platforms has accelerated the use of high-strength, heat-resistant polyurethane and epoxy adhesives for battery pack assembly, sealing, and vibration control. In the electronics sector, Korea’s global dominance in semiconductor and display fabrication fuels consistent demand for solvent-based adhesives and encapsulants used in microcircuit bonding and component protection.

Government initiatives promoting industrial innovation and export competitiveness have encouraged large-scale R&D in low-VOC adhesive chemistries that align with global safety and sustainability standards. Domestic manufacturers are increasingly developing advanced formulations tailored for flexible displays, 5G components, and next-gen mobility solutions. With a strong manufacturing base, high R&D intensity, and established global partnerships, South Korea stands as a critical innovation hub for solvent-based adhesive technologies in Asia-Pacific.

Solvent-Based Adhesives Market Report Scope

Solvent-Based Adhesives Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$11.6 Billion

|

|

Market Size (2034)

|

$17.7 Billion

|

|

Market Growth Rate

|

4.8%

|

|

Segments

|

By Resin Type (Chloroprene Rubber, Polyurethane, Styrene-Butadiene Rubber, Synthesized Rubber, Acrylic, Nitrile Rubber, Epoxy, Polyamide, Vinyl Acetate Copolymers, Natural Rubber, PVC Copolymers, Silicone), By End-Use Industry (Automotive & Transportation, Building & Construction, Packaging, Footwear & Leather Goods, Woodworking & Furniture, Medical & Healthcare, Aerospace & Defense, Electrical & Electronics, Consumer Goods), By Solvent Type (Ketones, Alcohols, Toluene/Xylene, Esters, Aliphatic Hydrocarbons), By Product Type (Contact, Pressure-Sensitive, Structural, Spray, High-Solids), By Curing Mechanism (Solvent-Drying, Reactive

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Henkel AG & Co. KGaA, 3M Company, H.B. Fuller Company, Arkema Group, Sika AG, Avery Dennison Corporation, Dow Inc., Huntsman Corporation, Pidilite Industries Ltd., Wacker Chemie AG, Illinois Tool Works Inc. (ITW), RPM International Inc., LINTEC Corporation, KLEIBERIT SE & Co. KG, Jowat SE

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

By Resin Type

- Chloroprene Rubber

- Polyurethane

- Styrene-Butadiene Rubber

- Synthesized Rubber

- Acrylic

- Nitrile Rubber

- Epoxy

- Polyamide

- Vinyl Acetate Copolymers

- Natural Rubber

- PVC Copolymers

- Silicone

By End-Use Industry

- Automotive & Transportation

- Building & Construction

- Packaging

- Footwear & Leather Goods

- Woodworking & Furniture

- Medical & Healthcare

- Aerospace & Defense

- Electrical & Electronics

- Consumer Goods

By Solvent Type

- Ketones

- Alcohols

- Toluene/Xylene

- Esters

- Aliphatic Hydrocarbons

By Product Type

- Contact

- Pressure-Sensitive

- Structural

- Spray

- High-Solids

By Curing Mechanism

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in Solvent Based Adhesives Market

- Henkel AG & Co. KGaA

- 3M Company

- H.B. Fuller Company

- Arkema Group

- Sika AG

- Avery Dennison Corporation

- Dow Inc.

- Huntsman Corporation

- Pidilite Industries Ltd.

- Wacker Chemie AG

- Illinois Tool Works Inc. (ITW)

- RPM International Inc.

- LINTEC Corporation

- KLEIBERIT SE & Co. KG

- Jowat SE

*- List not Exhaustive

Research Coverage

Prepared by USDAnalytics, this report investigates the Global Solvent-Based Adhesives Market through the prism of performance chemistry, regulation, and end-use productivity; it traces breakthroughs in high-solids and hybrid solvent systems, solvent-recovery process upgrades, and substrate-agnostic bonding that underpin automotive, construction, footwear, woodworking, and flexible packaging adoption; our analysis reviews specification shifts (initial tack, heat/humidity resilience, peel/shear), evolving VOC/HAPs compliance under IED/REACH, and capacity moves across APAC/Europe/North America, and highlights where contact, PSA, spray, structural, and high-solids formats deliver unmatched green strength, temperature endurance, and line speed—making this report an essential resource for operations leaders, R&D chemists, sourcing managers, and investors who need defensible forecasts, competitive benchmarking, and standards-aligned decision support through 2034.

Scope Highlights

Segmentation:

- By Resin Type: Chloroprene Rubber; Polyurethane; Styrene-Butadiene Rubber; Synthesized Rubber; Acrylic; Nitrile Rubber; Epoxy; Polyamide; Vinyl Acetate Copolymers; Natural Rubber; PVC Copolymers; Silicone.

- By End-Use Industry: Automotive & Transportation; Building & Construction; Packaging; Footwear & Leather Goods; Woodworking & Furniture; Medical & Healthcare; Aerospace & Defense; Electrical & Electronics; Consumer Goods.

- By Solvent Type: Ketones; Alcohols; Toluene/Xylene; Esters; Aliphatic Hydrocarbons.

- By Product Type: Contact; Pressure-Sensitive; Structural; Spray; High-Solids.

- By Curing Mechanism: Solvent-Drying; Reactive.

- By Region: North America (United States, Canada, Mexico); Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe); Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC); South & Central America (Brazil, Argentina, Rest of SCA); Middle East & Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa).

Geographic Scope: Analysis spans 25+ countries across North America, Europe, Asia Pacific, Latin America, the Middle East & Africa.

Timeframe: Historic data 2021–2024 and forecasts 2025–2034.

Companies: Analysis/profiles of 15+ companies.

Deliverables

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.