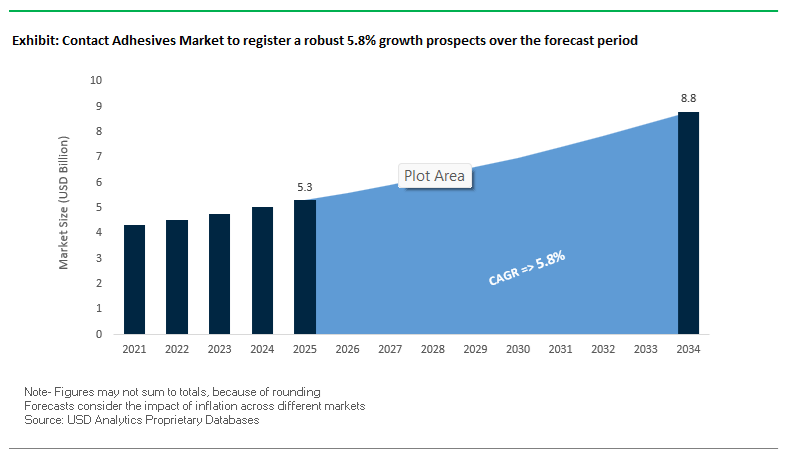

The global contact adhesives market occupies a critical position in industrial manufacturing and construction where instant bonding, large-area lamination, and heat resistance are non-negotiable. Valued at USD 5.3 billion in 2025 and forecast to reach USD 8.8 billion by 2034 at a CAGR of 5.8%, the market is expanding in parallel with growth in interior fit-out, modular construction, transportation interiors, furniture manufacturing, and industrial maintenance. Unlike structural epoxies or reactive systems, contact adhesives remain indispensable for applications where immediate green strength, high peel resistance, and flexible substrate compatibility directly translate into faster installation cycles and lower labor intensity.

Demand is being reshaped by a clear structural transition away from solvent-heavy legacy formulations toward engineered neoprene, polyurethane (PU), and water-based contact adhesive systems that meet tightening VOC and workplace exposure limits without compromising performance. Manufacturer-qualified neoprene contact adhesives continue to set the benchmark for high initial tack and peel adhesion exceeding 15 N/25 mm, supporting permanent bonding of high-pressure laminates (HPL), rubber flooring, acoustic panels, insulation foams, and metal skins. Industrial-grade formulations validated by suppliers such as 3M (Scotch-Weld™ 1357) and Bostik maintain bond integrity at service temperatures approaching 300°F (148°C), making them standard in transport interiors, furniture lamination, elevator panels, and HVAC insulation where vibration and thermal cycling are persistent stressors. In parallel, water-based contact adhesives—including ranges positioned for interior construction and joinery—are gaining specification share as they comply with SCAQMD Rule 1168, low-odor requirements, and green building programs across North America and Europe.

From a business and operations perspective, contact adhesive performance is increasingly evaluated through throughput, rework reduction, and substrate versatility, not just bond strength. Modern formulations offering open times of up to 20 minutes allow precise alignment on large surfaces, reducing scrap rates in flooring, wall cladding, and panelized construction systems. Multi-substrate compatibility—bonding wood, foam, plastics, composites, and metals without primers—continues to favor contact adhesives over mechanical fastening and liquid structural systems in cost-sensitive, high-volume production. Over the forecast period, competitive differentiation in the contact adhesives market will center on VOC-compliant chemistries, temperature-stable neoprene and PU systems, and scalable manufacturing aligned with construction codes, OEM material approvals, and sustainability audits, reinforcing the category’s role as a productivity-critical bonding solution rather than a commodity adhesive class.

The global contact adhesives industry is witnessing a dynamic phase of portfolio realignment, facility expansion, and sustainability-driven innovation, with major producers reinforcing regional supply chains and focusing on environmentally compliant chemistries.

In November 2024, INX Group Limited completed the acquisition of Coatings & Adhesives Corporation (C&A), forming INX International Coatings and Adhesives. The merger aims to integrate coating and specialty adhesive technologies for packaging and industrial laminates, potentially expanding the company’s footprint into flexible and contact adhesive systems. Around the same period, Ahlstrom expanded its capabilities through the acquisition of ErtelAlsop (November 2024), strengthening its role in release coatings and tape base papers, materials foundational to pressure-sensitive and contact adhesive applications.

Henkel AG & Co. KGaA reported 2% organic growth in H1 2024, driven by consistent volume improvements across its Adhesive Technologies segment. The company’s May 2024 guidance revision, projecting 2–4% organic growth, underscores its confidence in demand from construction, MRO, and flexible bonding markets. Additionally, Henkel’s facility expansion in South Dakota (2024) reinforces its focus on regionalized production for contact adhesives and consumer-grade construction solutions.

Huntsman Corporation, a major raw material supplier, started commercial operations at its $180 million MDI splitter in Louisiana (July 2022). This development enhances the production of differentiated MDI grades, critical in polyurethane-based contact adhesives and sealants, which rely on MDI for flexibility and chemical resistance. Parallelly, ATP Adhesives announced a new manufacturing facility in South Carolina, signaling growing North American demand for pressure-sensitive and contact-style adhesives.

Market restructuring has also been observed in material sourcing and sustainability strategy. Ahlstrom’s divestment of its Aspa pulp mill (October 2024) allowed it to streamline operations and concentrate on adhesive substrate innovation.

The contact adhesives market is experiencing a paradigm shift as manufacturers transition from solvent-based to water-based and low-VOC contact adhesives, responding to tightening air quality regulations and the global green construction movement. The environmental and health implications of volatile organic compounds (VOCs) are driving the adoption of next-generation aqueous dispersions and polyurethane-based formulations that maintain the high tack and cohesive strength of traditional solvent systems.

The regulatory foundation for the shift lies in California’s SCAQMD Rule 1168, which imposes stringent emission limits of 80 g/L for general-purpose contact adhesives, effectively eliminating legacy solvent-based formulations from key U.S. markets. In Europe, similar pressure under the Deco-Paint Directive (2004/42/EC) has positioned low-VOC adhesives as a default specification across construction and furniture applications.

Leading manufacturers are responding with significant R&D investments. A major adhesives producer announced that over 40% of its industrial R&D expenditure through 2025 will focus on advancing waterborne polyurethane dispersions (PUDs) and acrylic-based systems designed for flooring, insulation, and furniture bonding. These formulations are engineered to deliver fast initial tack, long open times, and high peel strength while remaining compliant with LEED and Green Seal standards.

The construction sector is also a major adoption driver. In both commercial and residential projects, LEED-compliant water-based contact adhesives are increasingly specified for bonding acoustic panels, decorative laminates, and wall coverings, especially in large-scale developments targeting WELL or BREEAM certification. As the global construction industry continues its low-carbon transition, the dominance of solvent-based adhesives is rapidly eroding in favor of sustainable, compliant, and high-performance waterborne alternatives.

The next generation of contact adhesives for automotive, footwear, and upholstery applications is defined by two essential characteristics: plasticizer migration resistance and thermal durability. These advanced formulations ensure long-term adhesion performance when bonding flexible PVC, synthetic leather, or polymeric composites—materials that experience both high heat and plasticizer diffusion during use.

In automotive interiors, particularly in dashboards, headliners, and seat assemblies, contact adhesives are engineered to withstand continuous exposure to temperatures above 120°C without bond degradation or discoloration. The performance benchmark is critical for vehicle interiors exposed to high solar loads and extreme thermal cycling. Additionally, leading adhesive manufacturers are utilizing high molecular weight polymeric plasticizers that exhibit drastically lower migration rates compared to monomeric counterparts, ensuring long-term bond integrity when used with flexible PVC.

According to recent vinyl industry technical papers, polymeric plasticizers not only reduce the risk of adhesive failure but also extend the product’s service life, making plasticizer-resistant contact adhesives essential for premium automotive interiors, marine applications, and industrial upholstery. These adhesives are being refined through the inclusion of advanced polymer backbones and reactive curing agents, allowing for superior creep resistance, improved adhesion to low-surface-energy substrates, and reduced solvent dependency.

The global surge in modular and prefabricated construction represents a major opportunity for the contact adhesives sector. Prefabrication’s industrialized approach to building—featuring off-site assembly of wall, floor, and roof panels—relies on fast-tack, high-cohesion adhesives that enable rapid lamination, secure bonding, and defect-free finishes in controlled factory environments.

According to the Global Construction Outlook (2024–2025), off-site manufacturing can accelerate project completion by up to 50% compared to traditional construction methods, directly amplifying the need for high-tack contact adhesives that deliver immediate bonding for laminated insulation boards, decorative laminates, and structural insulated panels (SIPs). The demand for factory-optimized bonding solutions has surged as the modular building industry scales up production across Europe, North America, and Asia-Pacific.

Further, multi-material modular assemblies—combining steel framing, composite insulation, and acoustic layers—require adhesives with exceptional multi-substrate compatibility. Industry testing has confirmed that structural-grade contact adhesives can achieve peel strengths exceeding 2.5 N/mm, meeting or surpassing international building code requirements for load-bearing laminated systems.

The marine manufacturing industry presents one of the most technically demanding yet profitable niches for contact adhesives, where long-term moisture resistance, UV stability, and high shear strength are mandatory performance metrics. Contact adhesives are indispensable in bonding composite hulls, bulkheads, decking, and interior liners, offering high initial tack for alignment during assembly and exceptional durability in submerged or humid environments.

Marine-grade formulations must meet stringent durability thresholds, including less than 5% bond strength loss after 2,000 hours of saltwater and UV exposure, as outlined in ISO 11341 and ASTM G154 protocols. The performance standard far exceeds conventional interior-grade adhesives, creating a high-value market for premium products.

Additionally, the use of composite materials such as fiberglass and advanced polymer laminates in modern watercraft construction necessitates contact adhesives with superior gap-filling capabilities—typically up to 2 mm—to compensate for surface irregularities in large molded components. These adhesives are further optimized for chemical resistance, ensuring long-term stability when exposed to fuels, lubricants, and cleaning agents commonly encountered in marine environments.

With the expansion of recreational boating, offshore energy platforms, and composite hull manufacturing, adhesive producers are actively developing solvent-free, water-resistant contact adhesives that combine environmental compliance with marine-grade reliability. These innovations will drive significant revenue streams across shipbuilding, yacht design, and advanced composite fabrication.

Contact Adhesives Market Share Insights, 2025-2034

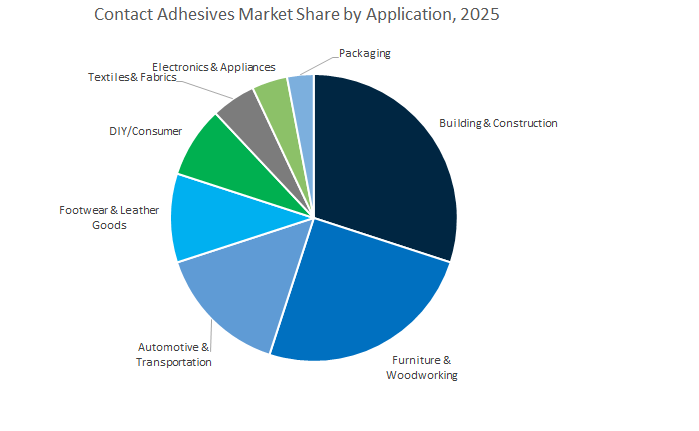

The building & construction segment dominates the global contact adhesives market, accounting for 33.4% of the projected 2025 share, driven by its extensive use in flooring, countertop lamination, panel bonding, and HVAC duct assembly. Contact adhesives are indispensable in construction due to their instant tack, high bond strength, and versatility across diverse materials such as wood, plastic laminates, metal, and rubber. They enable rapid installation with minimal clamping time, a crucial advantage for commercial and residential projects where productivity and reliability are essential. Furthermore, the increasing adoption of modular and prefabricated building techniques is bolstering demand for high-performance solvent-based and water-borne contact adhesives that can deliver strong bonds in controlled factory environments.

The furniture and woodworking segment, holding 25.9% of global market share, is the second-largest contributor, reflecting the adhesive’s central role in laminate bonding, veneering, edge banding, and foam-to-substrate assembly. Contact adhesives are particularly valued in this sector for their ability to provide strong, heat-resistant bonds and their compatibility with common materials such as particleboard, MDF, and decorative laminates. The rise in custom furniture production and interior remodeling activities across Asia-Pacific and North America further supports segment expansion. Additionally, growing environmental regulations are accelerating the shift toward low-VOC and water-based contact adhesives, aligning with sustainable furniture manufacturing trends.

Beyond these core markets, automotive and footwear industries represent vital industrial segments. Automotive manufacturers rely on contact adhesives for bonding interior components such as headliners, door panels, and carpeting, benefiting from their instant grab and vibration-resistant properties that streamline assembly line processes. Similarly, in footwear and leather goods manufacturing, contact adhesives are a cornerstone for sole attachment, upper lamination, and insole bonding, particularly in regions like Southeast Asia and Latin America, where footwear production volumes are high. The DIY and consumer segment, though smaller, remains stable, driven by increasing home improvement activities and retail availability of aerosol and brush-grade contact adhesives. Emerging niche applications in textiles, electronics, and flexible packaging are further expanding the market’s technological scope, particularly for precision bonding in small-scale or specialty assemblies.

The liquid form of contact adhesives leads the market, representing 50.9% of global consumption by 2025, due to its versatility, affordability, and strong performance in high-volume applications. Typically based on solvent-borne or water-borne polychloroprene (neoprene) and polyurethane formulations, liquid adhesives offer excellent spreadability, strong initial tack, and superior heat resistance, making them the standard for use in laminate bonding, furniture manufacturing, and flooring installation. Their widespread use across both industrial and residential projects ensures consistent demand, while the ongoing transition to low-VOC and non-toxic formulations enhances their acceptance in regions with strict environmental regulations such as the EU and North America. In particular, the construction and furniture sectors’ reliance on manual and roller-based application methods ensures that liquid adhesives remain the preferred choice for both large surface coverage and intricate bonding needs.

Aerosol spray adhesives represent the next major form factor, increasingly favored for ease of application, precision, and uniformity. Their ability to deliver consistent coating thickness across irregular surfaces makes them ideal for automotive interiors, HVAC systems, insulation, and DIY applications, where traditional liquid application can be cumbersome. The growth of portable packaging formats and high-efficiency spray canisters is further driving adoption among small-scale fabricators and on-site contractors. Additionally, their role in reducing waste and improving process speed aligns with industrial trends toward efficiency and cleaner production.

Pressure-sensitive tapes and films (PSA) are gaining traction as solvent-free and clean alternatives to conventional liquids. They are particularly valued in electronics assembly, appliance manufacturing, and architectural applications where low-VOC, mess-free bonding is essential. PSAs provide instant adhesion without curing or drying, supporting lightweight designs and automation-friendly processes.

The contact adhesives market landscape is dominated by global chemical innovators that integrate polymer science, sustainable formulation, and process automation to deliver differentiated bonding solutions. Industry leaders including Henkel, 3M, Arkema (Bostik), Huntsman, H.B. Fuller, and Sika are strategically diversifying portfolios toward VOC-free, water-based, and fast-curing polyurethane (PUR) systems, while expanding production in key growth markets.

Henkel, under its flagship brands LOCTITE, Pattex, and Technomelt, dominates the contact adhesive space with a strong focus on high-performance construction, MRO, and industrial bonding. Its PL Premium Max line delivers 100% solid, solvent-free adhesion compliant with global green building standards. Henkel is pioneering debonding-on-demand adhesive technology, facilitating material recyclability and circular manufacturing. With expanded North American manufacturing in South Dakota, Henkel has strengthened its regional supply chain and sustainability leadership in professional-grade contact adhesives.

Huntsman Corporation plays a critical upstream role by supplying MDI-based polyurethane precursors for contact adhesives under its Rubinate and Suprasec brands. Its $180 million MDI splitter investment in Geismar, Louisiana, enhances access to high-value, flexible MDI grades for downstream adhesive manufacturers. These modified MDI systems improve viscosity control, elasticity, and chemical adhesion, essential for reactive hot-melt and PUR contact adhesives used in automotive, aerospace, and wood lamination. Huntsman’s R&D focus on low-viscosity, high-flexibility systems supports the next generation of high-performance contact bonding.

3M remains a global benchmark for industrial-grade contact adhesives, particularly its Scotch-Weld 1357 and High-Performance Neoprene series, engineered for HPL-to-metal bonding and heat-intensive laminations. These products exhibit exceptional handling strength, heat endurance up to 300°F, and long-term durability under mechanical load. With a global distribution network and deep R&D capabilities, 3M continues to expand into low-halogen, high-strength acrylic chemistries for battery and composite applications, targeting fast-growing EV manufacturing segments.

H.B. Fuller stands out for its eco-friendly adhesive formulations targeting FMCG packaging, industrial lamination, and durable goods. Its high-tack, fast-set adhesives are critical in contact-style packaging applications that demand instant adhesion and low migration. The company’s ongoing focus on biodegradable hot-melt systems and CO₂ reduction technologies reinforces its sustainability leadership. Its adaptive R&D enables custom solutions for fast-changing industries such as automotive interiors, flexible packaging, and industrial assembly lines.

Through its Bostik brand, Arkema offers an extensive range of water-based and SMP (Silyl-Modified Polymer) contact adhesives, designed for construction, flooring, and DIY applications. These solvent-free formulations deliver strong adhesion, easy application, and improved indoor air quality compliance. Arkema’s R&D is heavily oriented toward VOC reduction and hybrid polymer chemistry, bridging polyurethane and silicone properties for next-gen adhesives. Continuous product expansion in resilient flooring and tiling adhesives underscores Bostik’s growing dominance in sustainable construction bonding systems.

Sika AG leverages its global presence and technical expertise to deliver polyurethane and elastomeric contact adhesives for construction and automotive glass bonding. Its product portfolio emphasizes mechanical strength, elasticity, and long-term weathering resistance, making Sika adhesives ideal for façade assembly, glazing, and transportation interiors. The company is also advancing automated adhesive application technologies, enhancing on-site efficiency for large-scale infrastructure projects. Continuous investment in production and R&D facilities across Asia and Europe positions Sika as a core innovator in industrial-grade adhesive chemistry.

The U.S. contact adhesives market is being reshaped by LEED-aligned, low-VOC requirements across commercial retrofits and new builds, while automotive OEMs mandate lower interior emissions and rapid, defect-free bonding on high-speed lines. 3M has launched a new low-VOC contact adhesive line for construction, pairing durability and reduced emissions to satisfy green building criteria and major GC submittal packages. H.B. Fuller’s acquisition of ND Industries (May 2024) broadens high-performance bonding solutions across industrial, electronics, and automotive use cases, strengthening North American share and distribution depth. Momentum is reinforced by new dispensing and curing technologies that optimize solvent-free/water-based application windows for high-throughput manufacturing and quiet-occupied retrofits (flooring, interior panels) where low odor is a must.

Supply security is also in focus: strategic partnerships and backward integration are being used to offset tariff-linked raw-material volatility, while R&D investment in bio-derived resins and renewable fillers accelerates the shift to sustainable contact adhesives. With residential and commercial retrofit cycles still robust, specifiers increasingly prefer water-based and hot-melt contact systems for flooring, laminates, wall panels, and acoustic builds, ensuring fast bond, low emissions, and long service life.

Germany’s contact adhesives ecosystem is anchored by regulatory-led innovation and advanced chemicals manufacturing. Henkel continues investing in Düsseldorf innovation hubs to deliver next-gen polyurethane and neoprene contact adhesives with faster cure and broader substrate wet-out—vital for premium automotive and precision industrial bonding. BASF’s ACRONAL binders raise performance in flooring adhesives while cutting emissions, supporting EU Green Deal and BREEAM/DGNB pathways. WACKER’s expanded polymer dispersion capacity secures critical inputs for water-borne contact formulations, while DELO’s UV/light-curable contact technologies serve electronics/medical assembly where positional accuracy and tack control are critical.

Automotive lightweighting and electrification push structural contact solutions that reliably bond aluminum, CFRP, PP/PA composites, and coated steels under thermal and vibrational loads. Government-industry initiatives further tighten indoor air quality and isocyanate management, accelerating the transition from solvent-borne to water-based and hybrid chemistries in woodworking, interior fit-out, and transport cabins.

China’s contact adhesives market is scaling on construction, furniture, flexible packaging, and fast-growing NEV manufacturing. Sika strengthened its building portfolio by acquiring Shenzhen Landun Holding (waterproofing expert) and earlier Crevo-Hengxin, expanding sealing & bonding reach across Asia Pacific. Local producers are ramping solvent-free laminating adhesives for converters supplying e-commerce and CPG lines, while policy incentives and subsidies push low-VOC water-based contact systems in woodworking and furniture, combating urban air pollution.

International firms are expanding R&D and manufacturing footprints to tailor contact adhesive formulations to local climates, substrates, and application methods (e.g., high humidity, complex façade laminates). Under the 14th Five-Year Plan, public projects increasingly specify eco-labeled, low-emission adhesives. In mobility, NEV programs accelerate demand for flame-retardant, thermally managed contact adhesives for battery interiors and trim bonding, complementing silicone, epoxy, and acrylic platforms in thermal and acoustic packages.

India’s surge in infrastructure and urban housing under the National Infrastructure Pipeline is expanding demand for high-strength contact adhesives in flooring, laminates, pre-fab modules, and panel systems. Pidilite continues to lead the DIY/woodworking segment while scaling professional-grade offerings for contractors and OEMs. New airport and industrial cluster programs require large volumes of interior fit-out adhesives for panels, wall systems, and composite laminations.

Global suppliers (e.g., WACKER) are localizing dispersible polymer powders for tile/ceramic systems, while converters in flexible packaging and e-commerce adopt solvent-free/water-based laminating adhesives to meet speed, safety, and compliance needs. Tightening environmental norms and rising consumer awareness are shifting furniture/interior markets toward safer, low-VOC contact products. In auto assembly, PU and acrylic contact adhesives deliver trim, NVH, and thermal performance aligned with BIS and OEM specifications.

France remains a European innovation base emphasizing recyclability and low emissions. Arkema/Bostik is prioritizing RecyClass-certified laminating adhesives to enable mono-material flexible packaging recovery, and launched Bostik STIX A600 EVOLUTION, a solvent-free acrylic contact adhesive for flooring, enhancing installer safety and IAQ. Arkema’s acquisition of Polytec PT broadens battery and electronics specialty adhesives—extending know-how into contact formulations for thermally and electrically demanding environments.

National circular-economy policy is catalyzing reversible/biodegradable contact systems for temporary assembly and packaging, while investments scale water-based PU contacts for footwear and leather goods, displacing high-solvent legacy systems. Automotive and aerospace supply chains increasingly specify EU-compliant, high-solid or water-based materials, while bio-sourced monomers enter next-gen contact adhesive R&D pipelines.

Switzerland’s specialty chemicals cluster, led by Sika, is extending global reach through acquisitions (e.g., DriTac in the U.S.; Chema in Peru), strengthening distribution and specification in flooring and construction adhesives, including professional-grade contact systems. R&D is focused on high-performance PU contact adhesives engineered for infrastructure, tunneling, and complex envelopes, where moisture/thermal cycling and substrate variability demand robust, durable bonds.

Swiss producers advance low-VOC, high-solids technologies aligned with Minergie and broader EU efficiency standards, while materials science programs push thermal/moisture resistance for water-based contact adhesives in outdoor and façade service. Precision industries deploy two-component contact solutions for high-stress industrial assembly, ensuring controlled open time and rapid development of green strength.

Japan’s contact adhesives landscape prioritizes high durability, anti-vibration, and electronics reliability. Major firms are advancing shock-absorbing contact systems for high-speed rail, robotics, and miniaturized electronics, while LINTEC scales PSA and contact platforms for display lamination and precision device bonding. Automotive programs specify high-temperature, long-life contact adhesives for interior and under-hood service, with rigorous aging and chemical-resistance thresholds.

Government programs promote reduced petrochemical reliance, accelerating biomass-derived polymers in eco-friendly contact adhesives. Japanese innovators lead in UV-curable contact technologies, enabling ultra-fast assembly and tight takt times for micro-components. For construction and prefab housing, advanced water-based contact adhesives are closing the performance gap with solvent systems, meeting regulatory IAQ preferences without sacrificing bond strength or open time control.

Contact Adhesives Market Report Scope

Contact Adhesives Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$5.3 Billion

|

|

Market Size (2034)

|

$8.8 Billion

|

|

Market Growth Rate

|

5.8%

|

|

Segments

|

By Technology Type (Solvent-Based, Water-Based, Solvent-Free, Reactive Contact, Hot Melt), By Resin Type (Neoprene, Styrene-Butadiene Rubber, Polyurethane, Acrylic, Nitrile Rubber, Epoxy, Vinyl Acetate Ethylene, Natural Rubber), By Application (Building & Construction, Furniture & Woodworking, Automotive & Transportation, Footwear & Leather Goods, Textiles & Fabrics, Electronics & Appliances, Packaging, DIY/Consumer), By Substrate (Wood-to-Wood, Metal-to-Metal, Plastic-to-Plastic, Fabric-to-Fabric, Rubber, Ceramic, Glass, Multi-Substrate Assemblies), By Form (Liquid, Aerosol Spray, Canister Spray, Tape/Film, Paste/Gel

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Henkel AG & Co. KGaA, 3M Company, H.B. Fuller Company, Arkema Group, Sika AG, RPM International Inc., Wacker Chemie AG, Huntsman Corporation, Pidilite Industries Ltd., Avery Dennison Corporation, LINTEC Corporation, The Dow Chemical Company, DELO Industrial Adhesives, Ashland Inc., Jowat SE

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

By Technology Type

- Solvent-Based

- Water-Based

- Solvent-Free

- Reactive Contact

- Hot Melt

By Chemistry/Resin Type

- Neoprene

- Styrene-Butadiene Rubber

- Polyurethane

- Acrylic

- Nitrile Rubber

- Epoxy

- Vinyl Acetate Ethylene

- Natural Rubber

By Application

- Building & Construction

- Furniture & Woodworking

- Automotive & Transportation

- Footwear & Leather Goods

- Textiles & Fabrics

- Electronics & Appliances

- Packaging

- DIY/Consumer

By Substrate

- Wood-to-Wood

- Metal-to-Metal

- Plastic-to-Plastic

- Fabric-to-Fabric

- Rubber

- Ceramic

- Glass

- Multi-Substrate Assemblies

By Form

- Liquid

- Aerosol Spray

- Canister Spray

- Tape/Film

- Paste/Gel

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

- Henkel AG & Co. KGaA

- 3M Company

- H.B. Fuller Company

- Arkema Group

- Sika AG

- RPM International Inc.

- Wacker Chemie AG

- Huntsman Corporation

- Pidilite Industries Ltd.

- Avery Dennison Corporation

- LINTEC Corporation

- The Dow Chemical Company

- DELO Industrial Adhesives

- Ashland Inc.

- Jowat SE

*- List not Exhaustive

Research Coverage

Prepared by USDAnalytics, this report investigates the global Contact Adhesives Market through a performance, compliance, and end-use lens; it delivers analysis reviews that benchmark instant tack, peel strength, thermal endurance, substrate compatibility, and low-VOC progress across construction, automotive, furniture, marine, and modular manufacturing; it highlights breakthroughs in water-based/solvent-free chemistries, plasticizer-resistant and high-temperature formulations, and production efficiency (open time, repositioning windows) that raise throughput and reduce rework; and it connects specification pathways to codes and green standards so decision-makers can derisk sourcing and qualification. By translating lab metrics into install-site reliability and lifecycle value, this report is an essential resource for architects, plant engineers, buyers, and operations leaders optimizing large-area lamination, flexible-to-rigid bonding, and multi-material assemblies.

Scope Highlights

Segmentation:

- By Technology Type: Solvent-Based; Water-Based; Solvent-Free; Reactive Contact; Hot Melt.

- By Chemistry/Resin Type: Neoprene; Styrene-Butadiene Rubber; Polyurethane; Acrylic; Nitrile Rubber; Epoxy; Vinyl Acetate Ethylene; Natural Rubber.

- By Application: Building & Construction; Furniture & Woodworking; Automotive & Transportation; Footwear & Leather Goods; Textiles & Fabrics; Electronics & Appliances; Packaging; DIY/Consumer.

- By Substrate: Wood-to-Wood; Metal-to-Metal; Plastic-to-Plastic; Fabric-to-Fabric; Rubber; Ceramic; Glass; Multi-Substrate Assemblies.

- By Form: Liquid; Aerosol Spray; Canister Spray; Tape/Film; Paste/Gel.

Geographic Scope: Analysis spans 25+ countries across North America, Europe, Asia Pacific, Latin America, the Middle East & Africa.

Time Frame: Historic data 2021–2024; Forecasts 2025–2034.

Companies: 15+ company analyses/profiles covering strategy, product portfolios, capacity moves, M&A, and innovation pipelines.

Deliverables

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.