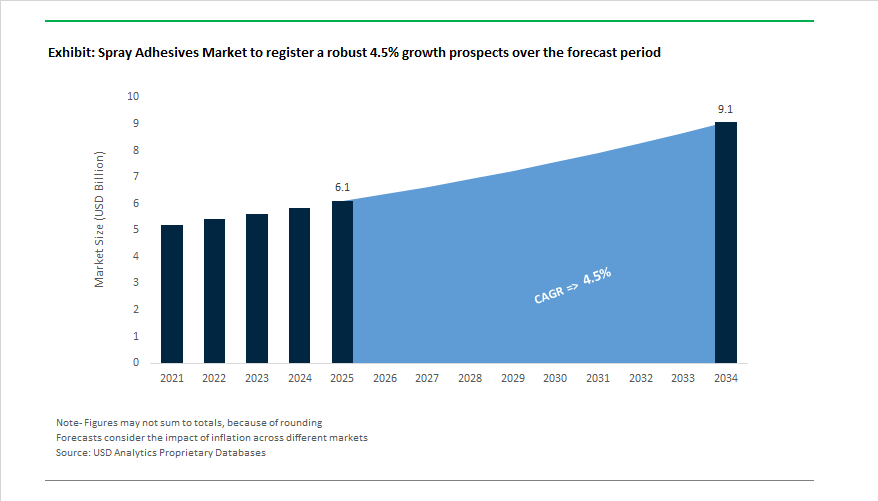

The Global Spray Adhesives Market is forecast to grow from $6.1 billion in 2025 to $9.1 billion by 2034, registering a CAGR of 4.5%. The market’s evolution is shaped by stringent VOC regulations, the rise of eco-friendly water-based systems, and the rapid adoption of high-performance two-component polyurethane (2K PUR) technologies. The increasing need for fast application, strong adhesion, and high coverage efficiency continues to position spray adhesives as a preferred bonding method across industries such as construction, automotive, furniture, packaging, and insulation.

In recent years, low-VOC and no-VOC spray adhesive formulations have gained traction, accounting for over 40% of new product launches in North America and Europe. Manufacturers are also expanding their portfolio to include bio-based solvents, synthetic rubber blends, and recyclable packaging systems in response to tightening environmental standards and end-user sustainability mandates.

Performance remains a central market differentiator. Synthetic rubber-based spray adhesives still dominate due to their high peel strength (100–200 N/cm), making them the benchmark for foam and fabric lamination in furniture and automotive seating. However, water-based systems are closing the performance gap—offering resistance to temperatures up to 93°C (200°F), adjustable open times up to 45 seconds, and compatibility with metal and plastic substrates, key for general assembly and packaging applications.

In addition, 2K polyurethane spray adhesives are emerging as the preferred solution for roofing and large-scale insulation applications, achieving shear resistance up to 3 MPa and rapid curing in minutes, driving adoption in high-throughput commercial construction. The result is a market pivot toward productivity-enhancing, environmentally compliant formulations that combine adhesion versatility with regulatory readiness.

The Spray Adhesives Industry is experiencing a wave of consolidation, sustainability-driven reformulations, and capacity expansions that reflect the market’s transition toward high-performance and eco-compliant systems.

In July 2025, APPLIED Adhesives finalized the acquisition of BTmix, strengthening its position as a leading custom adhesive solutions provider across North America. Earlier in April 2025, the company also acquired Adhesive Solutions, expanding its distribution network and technical service capabilities, enabling localized support for industrial clients transitioning to automated spray systems. These acquisitions highlight a growing market consolidation trend focused on enhancing supply chain agility and customer responsiveness.

H.B. Fuller, in June 2025, unveiled its Millennium PG-1 EF ECO2™ roofing adhesive, a sustainable innovation using atmospheric gases instead of chemical blowing agents. This innovation, part of its broader sustainability roadmap, delivers low-GWP (Global Warming Potential) performance while maintaining industrial-grade adhesion—solidifying its reputation in green building materials and commercial roofing systems.

Sika AG, in April 2025, expanded its regional presence by opening its fourth manufacturing facility in Kazakhstan, adding new production lines for construction chemicals and spray-applied adhesive products for the Central Asian market. Meanwhile, BASF and Sika’s joint R&D (March 2025) led to the development of a new epoxy hardener, setting a benchmark for sustainable structural adhesion technologies used in high-performance spray adhesives.

On the M&A front, Arkema’s Bostik division made significant headlines with its December 2024 acquisition of Dow’s flexible packaging adhesive business, expanding its footprint in high-speed lamination and spray bonding markets. Just months prior, in September 2024, Bostik introduced Kizen™ LIME, a bio-based adhesive containing over 80% renewable materials, underscoring the group’s commitment to decarbonization and circularity.

Simultaneously, Henkel and 3M are accelerating digitalization and efficiency. 3M, following its healthcare business spinoff (April 2024), has renewed focus on its Industrial and Transportation segments, leveraging strong material science R&D to create low-VOC, corrosion-resistant spray solutions for automotive and MRO sectors. Henkel, on the other hand, is investing in renewable raw materials and high-precision application systems that improve process control and reduce overspray—vital for high-volume manufacturing and NVH applications.

Market Trend 1: Accelerated Reformulation to Ultra-Low VOC and Propellant-Free Delivery Systems

The reformulation of spray adhesives to eliminate volatile organic compounds (VOCs) and hydrofluorocarbon (HFC) propellants represents a pivotal shift in the adhesive manufacturing ecosystem. Driven by regulatory, environmental, and economic imperatives, the trend is transforming aerosol-based adhesive systems into mechanically dispensed, water-based, and refillable-canister solutions.

The U.S. Environmental Protection Agency (EPA) 2025 amendments to the National VOC Emission Standards for Aerosol Coatings have introduced a reactivity-based compliance model that goes beyond mass-based VOC limits, compelling chemical formulators to innovate with less-reactive and low-ozone-forming solvents. The shift not only enhances compliance but also elevates formulation complexity—prompting adhesive chemists to explore next-generation polymer backbones and low-reactivity diluents for sustainable aerosol performance.

Parallel to the, water-based spray adhesives have emerged as the dominant low-VOC segment, projected to hold a 59% market share by 2035, fueled primarily by the paper and packaging industry’s rapid transition toward solvent-free, eco-certified bonding agents. Their compatibility with automated coating and laminating equipment has solidified water-based systems as the new industrial standard for mass-market use.

In addition, manufacturers are actively replacing HFC-propelled aerosols with refillable canister and pressure-fed spray systems. These propellant-free delivery mechanisms not only eliminate flammable and greenhouse gas components but also offer up to five times the surface coverage compared to conventional aerosols. The innovation represents a major industrial efficiency breakthrough, reducing waste, cost, and downtime across automotive, furniture, and construction manufacturing environments.

Market Trend 2: Proliferation of High-Tack, Fast-Grab Formulations for Automated Manufacturing and Composite Bonding

The rise of automated production in furniture, automotive interiors, and modular construction has intensified the need for fast-grab, high-tack spray adhesives that deliver immediate handling strength. Modern assembly lines—especially in RV and modular home manufacturing—demand curing times below 30 seconds, enabling uninterrupted throughput and efficient bonding of low-surface-energy substrates such as plastics, foams, and composites.

To meet these operational demands, industry leaders have launched advanced composite spray adhesives capable of maintaining structural integrity across varied materials, including fiberglass, vinyl, and rubberized substrates. For example, one global manufacturer introduced a Hi-Tack Composite Spray Adhesive specifically engineered to resist plasticizing oils while ensuring high-strength adhesion for resin-infused composite panels—applications central to vehicle lightweighting and industrial durability.

The shift toward automation-compatible adhesives reflects a broader industry objective: enhancing production efficiency without compromising bond performance. These new high-tack formulations enable precise, high-speed bonding across diverse surfaces, eliminating the need for mechanical fasteners and accelerating assembly times.

As factories pursue Industry 4.0 integration, the spray adhesives market is responding with smartly engineered, high-tack solutions that support both robotic dispensing and human application, ensuring material versatility and operational consistency across high-throughput manufacturing environments.

Market Opportunity 1: Development of Bio-Based, Circular Formulations for Sustainable Packaging and Consumer Goods

Sustainability is rapidly becoming a core growth driver for spray adhesive innovation. Under Extended Producer Responsibility (EPR) laws and corporate net-zero initiatives, manufacturers are advancing bio-based and repulpable formulations that align with global circular economy goals.

Adhesive producers are increasingly introducing bio-based spray adhesive systems containing 35% to 80% renewable content, derived from natural resins, vegetable oils, and bio-polyols. For instance, an eco-certified soft floor adhesive with a 35% organic renewable content has demonstrated significant CO₂ footprint reduction, proving the feasibility of scaling bio-based solutions without compromising performance.

In parallel, repulpable adhesive technologies are being engineered to dissolve during the paper recycling process, enabling complete fiber recovery without contaminating the recycling stream—a critical advancement given that 45% of packaging applications rely on adhesives during assembly or lamination.

The convergence of bio-content verification, end-of-life recyclability, and reduced emissions is redefining how adhesive manufacturers approach product lifecycle design. As sustainability becomes a competitive differentiator, bio-based and circular spray adhesives are poised to dominate high-volume sectors like packaging, disposable consumer goods, and eco-friendly construction materials.

Market Opportunity 2: Engineering of Thermally Conductive, Electrically Insulating Sprays for Electronics Manufacturing and Repair

The rapid expansion of miniaturized, high-power electronics and 5G infrastructure is generating a lucrative niche for thermally conductive, electrically insulating spray adhesives. These materials, which act as sprayable thermal interface materials (TIMs), provide both structural adhesion and efficient heat dissipation in compact device architectures.

Device failure rates exponentially increase above 75°C, underscoring the critical role of thermal management adhesives in ensuring component longevity. Advanced formulations are leveraging ceramic and graphene-based fillers, such as aluminum nitride, to achieve thermal conductivity values up to 3.7 W/m·K—enabling high-efficiency heat transfer while maintaining dielectric strength and mechanical flexibility.

These materials are being engineered into conformable, sprayable coatings capable of adhering to complex geometries like Ball Grid Arrays (BGAs) and power semiconductor housings, where traditional paste-based TIMs are impractical.

As the 5G and high-performance computing sectors continue to scale, the innovation presents a high-value opportunity for adhesive manufacturers to supply dual-function, thermally conductive spray coatings that combine cooling, insulation, and structural integrity in one application. The integration of sprayable TIMs represents a direct intersection between adhesive chemistry and electronics design, transforming both assembly efficiency and field repair practices.

Spray Adhesives Market Share Insights, 2025-2034

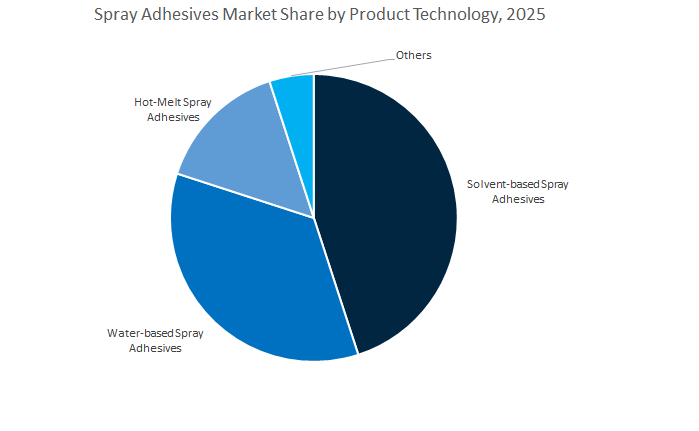

Market Share by Product Technology

Solvent-based spray adhesives dominate the global spray adhesives market, accounting for an estimated 44.3% share by 2025, owing to their fast drying time, high initial tack, and exceptional bonding strength on a wide variety of substrates including plastics, metal, rubber, and wood. These adhesives remain the industry’s workhorse for high-performance applications in construction, furniture, and automotive manufacturing, where instant adhesion and long-lasting durability are critical. Despite increasing environmental scrutiny due to VOC emissions, their ability to deliver consistent bonding under extreme temperature and humidity conditions sustains their strong demand. Solvent-based systems also exhibit superior wet-out properties, making them indispensable in complex assembly environments and large-surface bonding operations.

However, water-based spray adhesives are rapidly gaining traction, supported by stricter environmental regulations and the growing shift toward low-VOC and eco-friendly formulations. Advances in emulsion polymerization and synthetic resin chemistry have significantly improved the water-based systems’ drying speed, adhesion performance, and resistance to moisture, bridging the performance gap with solvent-based products. Hot-melt spray adhesives, though a smaller segment, are emerging as a high-growth niche for industries requiring instant adhesion, solvent-free processing, and 100% solids content—particularly in packaging, automotive, and insulation applications. The market trend reflects a gradual but clear transition toward sustainable, high-efficiency adhesive systems, as end-users seek balance between environmental compliance and performance reliability.

Market Share by End-Use Industry

Building & Construction leads the global spray adhesives market, capturing an estimated 33.4% market share by 2025, driven by the material’s critical role in insulation installation, roofing, flooring, and panel bonding. Spray adhesives are favored in this sector for their ability to deliver uniform coverage, rapid application, and long open times, enhancing productivity on large-scale construction projects. Their use in foam insulation, acoustic panels, drywall lamination, and underlayment bonding continues to expand with growing global construction activities, particularly in infrastructure development and energy-efficient building systems. The push toward green building certifications (such as LEED and BREEAM) also supports the adoption of low-VOC spray adhesive formulations, aligning with sustainability goals.

Furniture & Upholstery remains a major application segment, relying heavily on spray adhesives for foam bonding, fabric lamination, veneer attachment, and furniture assembly. The segment benefits from the adhesives’ fast tack and overspray control, allowing clean, efficient assembly in both mass production and custom fabrication. Automotive & Transportation is another significant contributor, where spray adhesives are widely used in interior trim assembly, headliner bonding, and thermal/acoustic insulation installation, driven by the rising trend of lightweight materials and modular vehicle interiors.

In addition, Packaging & Labeling applications utilize spray adhesives for carton sealing, labeling, and product assembly where quick-setting and high-strength bonds are required, while Textile & Leather industries apply these adhesives for bonding fabrics, foams, and linings in garments, footwear, and leather goods manufacturing. The wide adoption across these sectors highlights spray adhesives’ versatility and operational efficiency.

The Global Spray Adhesives Industry is led by 3M Company, H.B. Fuller, Sika AG, Bostik (Arkema Group), and Henkel AG & Co. KGaA, all leveraging specialized chemistries, automation-ready systems, and ESG-driven innovation to maintain competitive edge.

3M Company continues to dominate the spray adhesives segment with its Scotch-Weld™ and Hi-Strength product lines, known for instant handling strength and high heat resistance, especially in automotive headliners and MRO operations. The company’s Fastbond™ series and Hi-Strength 94 ET lead in low-VOC aerosol performance, meeting indoor air quality (IAQ) standards for commercial applications. With innovations like Accuspray™ spray gun systems, 3M integrates precision atomization and lean manufacturing into adhesive delivery, maximizing coverage and reducing material waste. Strategic focus lies in dissimilar material bonding for advanced metal-plastic composites, supporting industries like electric vehicles and specialty transport.

As the world’s largest pureplay adhesives manufacturer, H.B. Fuller commands a strong position in industrial spray applications across woodworking, panel manufacturing, and transportation. Its HP-Series spray adhesives are engineered for large surface bonding, combining strength with clean application. The company’s Millennium PG-1 EF ECO2™ adhesive represents a sustainability milestone—achieving zero chemical propellant emissions in commercial roofing. With new manufacturing expansions in Egypt and Latin America, H.B. Fuller is enhancing local production and optimizing supply chain resilience for fast-growing markets in construction and automotive assembly.

Sika AG leverages its advanced SikaForce® polyurethane technology for high-strength, flexible bonding in automotive exteriors, roofing, and industrial assembly. Its Purform® adhesive platform offers ultra-low diisocyanate content, minimizing worker exposure and simplifying EU REACH compliance. The company’s IR-accelerated curing systems like SikaForce®-825 enable just-in-time production with rapid set times, catering to high-speed thermoplastic assembly. Furthermore, Sika’s investment in digital construction partnerships (e.g., Giatec™) reinforces its leadership in smart manufacturing and process control for spray adhesives in building envelopes.

Bostik, a core subsidiary of Arkema, is pushing the boundaries of sustainable adhesive chemistry with silane-terminated polymer (STP) and water-based systems that minimize solvent dependency. Following the acquisition of Dow’s flexible packaging adhesive division, Bostik commands one of the most extensive web-based lamination and industrial spray adhesive portfolios globally. Its Kizen™ LIME bio-based adhesive and R3BOND® SYSTEM exemplify innovation in recyclable and end-of-life manageable bonding, essential for flooring and construction circularity. With operations in over 45 countries, Bostik’s 2.7-billion-euro revenue base supports aggressive R&D into multi-substrate adhesion and low-impact technologies.

Henkel remains a dominant global force in adhesives, sealants, and coatings, offering TEROSON® and LOCTITE® spray adhesive lines for automotive maintenance and industrial assembly. The company’s commitment to reducing solvent content and increasing renewable raw material use aligns with its 2030 sustainability goals. Henkel’s systems excel in acoustic management and NVH reduction, enabling efficient bonding of insulation materials within vehicle interiors. Through precision application technologies, Henkel enhances dosing accuracy and minimizes overspray, supporting sustainability through resource efficiency and process optimization across transportation and construction sectors.

Country Analysis: Regional Developments Shaping the Global Spray Adhesives Market

United States (U.S.): Sustainable Formulations and Construction Growth Drive Spray Adhesive Innovation

The United States spray adhesives market continues to dominate North America, led by innovation in low-VOC, water-based adhesive technologies and robust growth in construction, automotive, and defense applications. In October 2024, 3M Company introduced the Fastbond Pressure Sensitive Adhesive 1049, a solvent-free water-based adhesive that integrates with its PowerCore portable cylinder system. The innovation is revolutionizing professional trades by combining low emissions, rapid application, and strong adhesion performance—a benchmark for sustainable product innovation.

Regulatory oversight remains a core market driver. The U.S. Environmental Protection Agency (EPA) continues to tighten VOC standards, directly influencing manufacturers to develop eco-compliant formulations. Meanwhile, Texas Commission on Environmental Quality (TCEQ)’s 2024 regulations eliminated 3.12 tons/day of VOC emissions around Houston, further pushing adoption of low-emission spray adhesive systems. Demand is surging across sectors—particularly in roofing, insulation, and flooring adhesives—with residential construction spending exceeding USD 917.9 billion in 2024, up nearly 6% from the previous year (U.S. Census Bureau). The nation’s emphasis on sustainability, efficiency, and performance-grade adhesives continues to redefine industrial and commercial construction practices.

China – Manufacturing Leadership and Environmental Compliance Reinforce Spray Adhesive Market Strength

China remains the largest spray adhesive market in the Asia-Pacific region, backed by its strong industrial base, government-backed sustainability policies, and rapidly advancing automotive and furniture manufacturing sectors. The 2024 launch of Henkel’s Innovation Center in Shanghai exemplifies China’s push toward R&D-driven adhesive solutions, aimed at enhancing product efficiency and compliance with tightening emission standards. National programs like the Blue Sky Protection Campaign continue to reshape production norms, accelerating the shift toward low-VOC and water-based adhesive systems across major provinces.

China’s Electric Vehicle (EV) manufacturing boom—supported by record production levels in 2024—has fueled demand for heat-resistant and fast-setting spray adhesives used in interior trim assembly, soundproofing, and battery bonding applications. Domestic companies are scaling production of synthetic rubber and acrylic spray adhesives tailored for high-temperature performance and flexible substrate bonding. Additionally, the expansion of furniture and packaging sectors underpins strong demand for solvent-free, long-bonding formulations.

Germany – Regulatory Precision and Automotive Innovation Anchor European Spray Adhesives Market

Germany stands as the European hub for high-performance spray adhesives, driven by precision manufacturing, regulatory discipline, and cutting-edge automotive engineering. The nation’s commitment to sustainability—through strict adherence to REACH (Registration, Evaluation, Authorisation and Restriction of Chemicals) regulations—has spurred widespread conversion from traditional solvent-based adhesives to waterborne polyurethane spray systems across industrial and construction sectors.

German adhesive manufacturers are investing heavily in R&D to enhance water-based spray dispersion performance, particularly focusing on improving heat resistance, bond strength, and moisture durability to match solvent-based counterparts. In the automotive sector, OEMs are increasingly relying on fast-cure spray adhesives for lightweight composite bonding and modular interiors, directly supporting the country’s EV transition. Furthermore, Germany remains a major exporter of polyurethane resins and precision adhesive dispensing systems, supplying global markets with the technological backbone for next-generation spray adhesive applications across insulation, packaging, and manufacturing industries.

India – Infrastructure Boom and Domestic Manufacturing Drive Spray Adhesive Consumption

The Indian spray adhesives market is rapidly evolving, propelled by the country’s infrastructure development, manufacturing expansion, and increasing preference for eco-friendly adhesive technologies. The sector benefits from strong domestic initiatives like “Make in India” and large-scale urbanization programs that generate immense demand for flooring, HVAC insulation, and wall-panel bonding solutions. In 2024, Pidilite’s joint venture (ICA Pidilite) introduced UV-curable adhesive technologies, a critical step toward faster curing and industrial-grade spray adhesive adoption.

Multinational chemical giants are strengthening their presence in India’s high-growth market. WACKER Chemie AG’s introduction of two new dispersible polymer powders at PAINTINDIA 2024 marked a significant step toward water-based and solvent-free formulations tailored to local construction needs. With India’s construction and infrastructure investments rising steadily, demand for professional-grade spray adhesives for woodworking, insulation, and furniture assembly is expected to escalate. Moreover, growing consumer awareness of low-emission and sustainable adhesives is driving manufacturers to localize production of eco-friendly spray systems suitable for India’s tropical climate and expanding industrial base.

Canada – Stringent VOC Regulations Redefine the Industrial and Consumer Spray Adhesives Market

The Canadian spray adhesives market is undergoing a major transformation driven by its nationwide VOC reduction mandates. Effective January 2024, the Canadian government implemented stringent VOC concentration limits across 130 product categories, including industrial and consumer adhesives. The regulation is forcing rapid reformulation across the industry, resulting in an accelerated transition toward low-VOC, water-based, and hot-melt spray adhesive systems.

Manufacturers and importers are investing in advanced R&D to maintain high adhesive strength and application speed while adhering to the new compliance thresholds. The introduction of the VOC Compliance Unit Trading System incentivizes innovation, allowing companies to trade emission credits in exchange for developing sub-limit, sustainable adhesive products. The reforms have reshaped product portfolios across commercial construction, furniture, and packaging sectors. Contractors and DIY consumers are adopting next-generation, low-odor spray adhesives for applications like carpet installation, insulation bonding, and decorative paneling, aligning with the nation’s long-term net-zero emissions goals.

United Kingdom (U.K.): Market Consolidation and Product Diversification Strengthen Industry Presence

The United Kingdom spray adhesives industry is witnessing consolidation and vertical integration, with global players expanding their manufacturing and distribution networks to meet rising domestic and European demand. In September 2023, H.B. Fuller Company acquired Sanglier Limited, a leading independent manufacturer of industrial spray adhesives, marking a strategic expansion that broadened its European product range and improved local manufacturing agility. Similarly, Sika AG’s acquisition of Cromar Building Products Ltd. (February 2025) reinforced its presence in the roofing and building envelope segment, incorporating high-strength spray contact adhesives into its solutions portfolio.

The nation’s housing and construction growth, reflected in over 210,000 new dwellings completed by March 2023, continues to fuel high demand for rapid-bonding adhesives in insulation, joinery, and flooring applications. A notable trend is the professional adoption of pre-pressurized spray systems with synthetic rubber-based adhesives that enhance on-site productivity and minimize solvent exposure. The U.K. remains a leader in developing energy-efficient, performance-grade spray adhesives that cater to the region’s growing emphasis on sustainable building practices and productivity optimization.

Spray Adhesives Market Report Scope

Spray Adhesives Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$6.1 Billion

|

|

Market Size (2034)

|

$9.1 Billion

|

|

Market Growth Rate

|

4.5%

|

|

Segments

|

By Product Technology (Water-based, Solvent-based, Hot-Melt, Others), By Resin Type (Synthetic Rubber, Polyurethane, Acrylic, Epoxy, Vinyl Acetate Ethylene, Others), By End-User (Building & Construction, Furniture & Upholstery, Automotive & Transportation, Packaging & Labeling, Textile & Leather, Others

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Henkel AG & Co. KGaA, 3M Company, H.B. Fuller Company, Arkema Group, Sika AG, Dow Inc., BASF SE, Pidilite Industries Limited, Avery Dennison Corporation, Huntsman Corporation, Illinois Tool Works Inc. (ITW), Eastman Chemical Company, Mapei S.p.A., Wacker Chemie AG, Soudal NV

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

By Product Technology

- Water-based

- Solvent-based

- Hot-Melt

- Others

By Resin Type

- Synthetic Rubber

- Polyurethane

- Acrylic

- Epoxy

- Vinyl Acetate Ethylene

- Others

By End-Use Industry

- Building & Construction

- Furniture & Upholstery

- Automotive & Transportation

- Packaging & Labeling

- Textile & Leather

- Others

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in Spray Adhesives Market

- Henkel AG & Co. KGaA

- 3M Company

- H.B. Fuller Company

- Arkema Group

- Sika AG

- Dow Inc.

- BASF SE

- Pidilite Industries Limited

- Avery Dennison Corporation

- Huntsman Corporation

- Illinois Tool Works Inc. (ITW)

- Eastman Chemical Company

- Mapei S.p.A.

- Wacker Chemie AG

- Soudal NV

*- List not Exhaustive

Research Coverage

Prepared by USDAnalytics, this report investigates the global Spray Adhesives Market, mapping how low-VOC reformulations, water-based dispersion platforms, and 2K polyurethane systems are translating lab breakthroughs into line-speed productivity and compliance advantages across construction, automotive, furniture, packaging, and insulation. Our analysis reviews performance envelopes (fast-grab handling, coverage efficiency, temperature tolerance, open time control) alongside sourcing shifts, M&A signals, and regulatory trajectories to isolate where value pools are expanding and which chemistries are gaining OEM specification. It highlights application-ready solutions that cut overspray, raise first-pass yield, and de-risk audits under evolving VOC and propellant norms—linking materials design to real factory KPIs. Crafted for executives, product managers, and manufacturing engineers, this report is an essential resource for prioritizing portfolios, qualifying suppliers, and timing market entry as eco-compliant spray technologies scale globally.

Scope Highlights

Segmentation:

- By Product Technology: Water-based; Solvent-based; Hot-Melt; Others

- By Resin Type: Synthetic Rubber; Polyurethane; Acrylic; Epoxy; Vinyl Acetate Ethylene; Others

- By End-Use Industry: Building & Construction; Furniture & Upholstery; Automotive & Transportation; Packaging & Labeling; Textile & Leather; Others

- By Region: North America; Europe; Asia Pacific; South & Central America; Middle East & Africa

Geographic Scope: Analysis spans 25+ countries across North America, Europe, Asia Pacific, Latin America, the Middle East & Africa.

Time Horizon: Historic data 2021–2024 and forecast data 2025–2034.

Companies: Analysis/profiles of 15+ companies, including Henkel AG & Co. KGaA; 3M Company; H.B. Fuller Company; Arkema Group; Sika AG; Dow Inc.; BASF SE; Pidilite Industries Limited; Avery Dennison Corporation; Huntsman Corporation; Illinois Tool Works Inc. (ITW); Eastman Chemical Company; Mapei S.p.A.; Wacker Chemie AG; Soudal NV.

Deliverables

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.