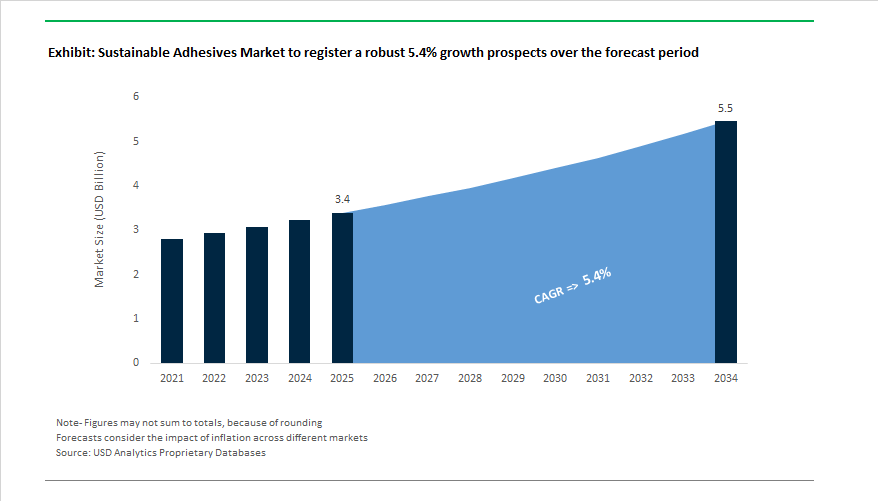

The Global Sustainable Adhesives Market is expected to expand from USD 3.4 billion in 2025 to USD 5.5 billion by 2034, advancing at a 5.4% CAGR, as sustainability shifts from a compliance topic to a core product-design and procurement criterion. What distinguishes this market is not volume substitution alone, but a structural re-engineering of adhesive chemistry, sourcing, and manufacturing footprints in response to Scope 1–3 emission targets, product carbon footprint disclosure, and tightening VOC and hazardous-substance regulations across major end markets.

Leading adhesive manufacturers are moving beyond incremental reformulation toward feedstock-level innovation, including mass-balanced bio-based polyols, renewable acrylic monomers, lignin-derived tackifiers, and solvent-free reactive systems. Several global suppliers now commercialize adhesive portfolios with 30–70% bio-carbon content, while maintaining performance parity in shear strength, heat resistance, and durability—a threshold that previously limited adoption in structural, electronics, and automotive applications. At the same time, low-VOC and zero-solvent systems are becoming standard in packaging, hygiene, and construction, driven by REACH, EPA, and regional indoor air quality frameworks.

From an industrial perspective, sustainable adhesives are increasingly evaluated on total lifecycle impact rather than formulation alone. Manufacturers are integrating lower-temperature curing chemistries, reduced coat-weight technologies, and energy-efficient hot-melt and UV-curing processes to cut downstream energy use at converter and OEM facilities. In parallel, design-for-recycling requirements—particularly in flexible packaging and labels—are pushing adhesive developers to engineer systems that enable clean separation, repulpability, or compatibility with mono-material recycling streams, without sacrificing line speed or bond reliability.

The sustainable adhesives landscape is defined by strategic partnerships, breakthrough launches, and capacity expansions focused on carbon reduction and regulatory alignment. Leading chemical and adhesive manufacturers are re-engineering formulations to comply with VOC emission limits, green building standards, and automotive sustainability directives. This period witnessed the emergence of new product categories and corporate investments that signal the sector’s strategic pivot toward eco-efficiency and responsible innovation.

In October 2025, Henkel and Dow expanded their longstanding collaboration to integrate low-carbon raw materials and renewable electricity into hot melt adhesive production, achieving measurable PCF reductions in packaging applications. Earlier, in June 2025, H.B. Fuller introduced Millennium PG-1 EF ECO2, a first-of-its-kind commercial roofing adhesive utilizing atmospheric gases instead of high-GWP blowing agents—a key milestone for sustainable construction materials. Similarly, Henkel’s €60 million Shanghai Inspiration Center, inaugurated in January 2025, serves as a regional hub for sustainable co-innovation, emphasizing Asia-Pacific’s growing demand for eco-efficient bonding solutions.

Late 2024 marked significant moves from competitors as well: Ashland launched a water-based adhesive series designed for automotive interiors, aligning with stringent low-VOC emission standards, while Dow inaugurated an automotive-focused innovation center in Wiesbaden, Germany in Q3 2024, dedicated to developing next-generation adhesives for lightweighting and EV battery assembly. Arkema’s Bostik also unveiled bio-based adhesives tailored for EV battery thermal management in Q3 2024, reinforcing the material shift toward renewable chemistries.

In parallel, H.B. Fuller secured a multi-year EV adhesives supply agreement in Q3 2024, strengthening its role in the electric mobility value chain, while Henkel’s enhanced Environmental Product Declarations (EPDs) initiative in H1 2025 further advanced sustainability transparency across its construction adhesives portfolio. The 2024 acquisition of Polytec PT by Arkema’s Bostik division expanded its footprint in engineering adhesives (particularly for electronics and EV sectors) and highlighted the industry’s drive toward comprehensive, sustainable, and performance-driven adhesive ecosystems.

Market Trend 1: Strategic Shift to Bio-Based Polyurethane Raw Materials to Decarbonize Supply Chains

The global movement toward carbon-neutral and renewable manufacturing has accelerated the replacement of fossil-based polyols with bio-attributed and waste-derived feedstocks, fundamentally transforming polyurethane adhesive chemistry. Major chemical producers are scaling innovations that directly reduce the carbon intensity of adhesive production, aligning with net-zero goals across construction, automotive, and consumer goods sectors.

In late 2023, Covestro AG and Selena announced the launch of bio-attributed polyurethane (PU) foams developed using renewable polyols derived from plant oils and biomass residues. The initiative demonstrates how supply chain decarbonization is becoming embedded in high-volume adhesive formulations for construction insulation and sealants, segments traditionally reliant on petroleum-derived inputs.

Similarly, Mitsubishi Chemical Group’s BioPTMG, a plant-based polyether polyol, introduced in October 2024, exemplifies the transition toward bio-synthetic PU precursors. These raw materials not only lower fossil fuel dependency but also deliver mechanical and chemical performance comparable to their petroleum-based counterparts, ensuring seamless adoption across automotive interiors, coatings, and flexible packaging adhesives.

With the building and construction sector expected to account for over 33% of the total bio-based polyurethane demand by 2024, the technical maturity and commercial traction of bio-based polyols are beyond the experimental stage. The increasing alignment of major brands with ESG benchmarks and Science-Based Targets (SBTi) further ensures that renewable polyurethane adhesives will anchor the industry's long-term decarbonization strategy.

Market Trend 2: Reformulation for Monomaterial Packaging to Enable High-Quality Recycling

Under growing Extended Producer Responsibility (EPR) regulations, adhesive innovation in flexible packaging and labeling has become a cornerstone of the circular economy. The focus has shifted toward monomaterial packaging adhesives that maintain bond integrity during use but separate cleanly during recycling, ensuring high-quality polymer recovery.

In a milestone development, Bostik introduced SF10M, a recyclable laminating adhesive certified by RecyClass for PE and PP monomaterial packaging. The product not only meets stringent design-for-recycling standards but also enhances the mechanical and optical properties of recycled films, making it a benchmark for compliance under EPR-driven sustainability goals.

Governments are reinforcing the trend through modulated fee structures under EPR schemes in regions such as California and the European Union, offering reduced fees for highly recyclable packaging. The directly incentivizes brand owners to transition toward wash-off adhesives and recyclable laminating systems, stimulating industry-wide reformulation.

Technical standards issued by organizations like APR (Association of Plastic Recyclers) and RecyClass stipulate that alkali wash-off adhesives for HDPE and PP packaging must operate effectively between 60–85°C without leaving residue. The establishes a stringent performance benchmark for new adhesive chemistries that combine operational robustness with recycling efficiency.

Market Opportunity 1: Development of Carbon-Negative Adhesives from Captured CO₂ and Methane

A defining breakthrough for the sustainable adhesives industry lies in the use of captured greenhouse gases (GHGs)—specifically CO₂ and methane—as feedstocks for adhesive polymer production. The carbon capture and utilization (CCU) model enables the creation of adhesives with net-negative carbon footprints, directly linking industrial decarbonization with circular carbon economics.

A flagship project by Celanese Corporation exemplifies the transition. The company’s CCU methanol plant, capable of capturing 180,000 metric tons of CO₂ annually, produces low-carbon methanol, a precursor to vinyl acetate monomer (VAM)—a key input for water-based adhesive polymers. The vertically integrated carbon recycling pathway reduces both scope 1 and 3 emissions while embedding sustainability into the adhesive manufacturing value chain.

Likewise, Covestro and Aramco Performance Materials have successfully commercialized CO₂-based polycarbonate polyols (under the “Converge” brand), containing up to 40% captured CO₂. These are already in use across coatings, foams, and adhesives, demonstrating scalability and compatibility with existing production infrastructure.

By replacing petrochemical intermediates with CO₂-derived building blocks, manufacturers can deliver high-performance adhesive products while closing the carbon loop. The commercial success of such initiatives signals a near-future market where carbon-negative adhesives become a standard across packaging, automotive, and construction industries.

Market Opportunity 2: Engineering of Reversible Adhesives for a Circular Built Environment

As the global construction industry grapples with the fact that it generates one-third of all waste worldwide, the introduction of reversible or debondable adhesives represents a transformative leap toward a circular built environment. These adhesives are specifically designed for design-for-disassembly (DfD) applications, enabling the non-destructive separation and reuse of high-value materials such as cross-laminated timber (CLT), façade panels, and composite assemblies.

Academic research into thermally reversible polymer systems has demonstrated adhesives that can bond and unbond via heat activation, regaining their structural integrity upon cooling. Such systems allow modular building elements to be deconstructed without damage, facilitating the reuse of valuable components while minimizing landfill waste and resource depletion.

The innovation aligns with growing global sustainability certifications and green construction directives, which increasingly mandate circular construction practices. By allowing easy separation of bonded layers, reversible adhesives reduce waste generation and support high-value material recovery, significantly enhancing lifecycle efficiency.

The push toward net-zero construction and closed-loop material systems ensures strong commercial interest in reversible adhesives from architectural, civil, and modular construction sectors. As urban regeneration and prefabrication accelerate, such adhesives will underpin a new standard of sustainable architectural design, blending mechanical performance with circular functionality.

Sustainable Adhesives Market Share Insights, 2025-2034

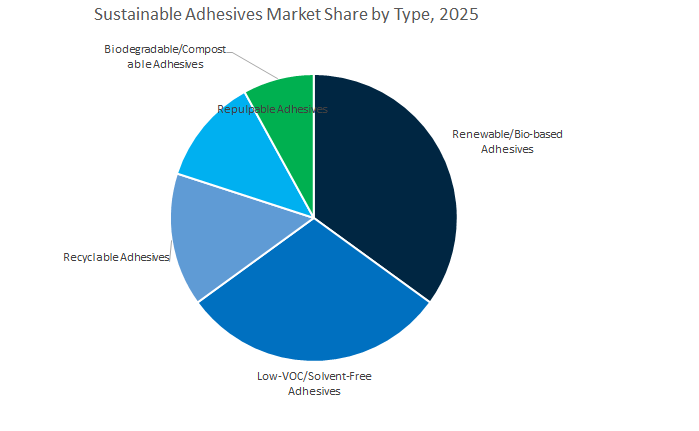

Market Share by Type

The renewable and bio-based adhesives segment dominates the global sustainable adhesives market, accounting for 34.1% of total demand in 2025, driven by the accelerating shift toward bio-renewable materials derived from starch, soy, lignin, and natural resins. These adhesives are increasingly preferred by manufacturers seeking to reduce carbon footprints and comply with sustainability targets set by global brands and environmental regulations. Their compatibility with paper, wood, and biodegradable substrates makes them highly relevant to the packaging, woodworking, and consumer goods industries. Low-VOC and solvent-free adhesives maintain a strong share, propelled by stringent air quality regulations in North America and Europe and growing awareness about occupational health in manufacturing. These formulations offer high performance without the emissions associated with conventional solvent-based systems, making them a preferred choice for construction, automotive, and textile applications. Meanwhile, recyclable and repulpable adhesives play a vital role in supporting circular economy goals, particularly in paperboard packaging and labeling where adhesive removability and fiber recovery are key. The biodegradable and compostable adhesives segment, though still emerging, shows robust growth potential aligned with the global surge in compostable packaging, bioplastics, and single-use consumer products.

Market Share by End-Use Industry

The packaging industry remains the largest end-use sector for sustainable adhesives, commanding an estimated 39.4% market share in 2025, supported by rapid growth in eco-friendly flexible packaging, carton sealing, and labeling applications. Regulatory frameworks such as the EU Packaging and Packaging Waste Directive and Extended Producer Responsibility (EPR) programs are driving brand owners to adopt biodegradable, compostable, and recyclable adhesive systems compatible with sustainable substrates. Construction and building applications form the second-largest segment, fueled by the growing emphasis on LEED-certified and green building practices, where low-emission and non-toxic adhesive formulations are favored for flooring, panel lamination, and insulation. The woodworking and furniture industry continues to rely on sustainable adhesives for formaldehyde-free panels, veneers, and cabinetry, while the automotive and transportation sector integrates bio-based bonding solutions to support lightweighting, recyclability, and interior air quality improvement. The medical and hygiene segment represents a fast-growing niche, with sustainable adhesives gaining traction in biocompatible wound dressings, wearable sensors, and hygiene products.

The competitive dynamics of the sustainable adhesives market are anchored by major players including Henkel AG & Co. KGaA, H.B. Fuller Company, Dow Inc., Arkema S.A. (Bostik), and Ashland LLC. These companies are driving sustainability transformations through bio-based innovation, carbon-neutral manufacturing, and circular economy initiatives. Their collective strategies reveal a global shift from short-term compliance to long-term regenerative chemistry and material responsibility.

Henkel continues to strengthen its dominance in adhesive technologies through sustainability-first innovations. In January 2025, it inaugurated a €60 million Inspiration Center in Shanghai, serving as a global innovation hub for co-developing sustainable adhesive formulations with customers. Henkel’s partnership with Dow (October 2025) focuses on low-carbon feedstocks and renewable electricity integration to reduce emissions in hot melt production. The company’s adoption of Environmental Product Declarations (EPDs) across its construction adhesive lines sets an industry benchmark for ESG transparency. Henkel’s roadmap emphasizes scope 3 decarbonization, digital traceability, and end-of-life recyclability for adhesives used in packaging, electronics, and mobility sectors.

As the world’s largest pureplay adhesives manufacturer, H.B. Fuller is pioneering eco-engineered bonding solutions. In June 2025, the company introduced Millennium PG-1 EF ECO2, a revolutionary roofing adhesive leveraging ECO2 Driven™ technology that eliminates harmful chemical blowing agents. Nearly 60% of its R&D projects target sustainable innovation, focusing on recyclable and bio-based adhesive systems. Furthermore, its multi-year EV adhesives supply agreement (Q3 2024) reinforces the company’s presence in the sustainable mobility ecosystem, supplying critical bonding and sealing materials for battery assembly and body structures in electric vehicles.

Dow remains a cornerstone of the sustainable adhesives ecosystem, blending material science expertise with green innovation. Its Wiesbaden Innovation Center (Q3 2024) is focused on lightweight automotive adhesives and EV battery technologies, advancing sustainability across transportation sectors. Collaborating with Henkel (October 2025), Dow is a critical enabler of low-carbon adhesive production, leveraging its polymer and monomer expertise to reduce scope 3 emissions. The company’s strategy centers on developing waterborne systems, low-VOC solutions, and reactive chemistries that meet global environmental regulations without compromising adhesive performance.

Through its Bostik subsidiary, Arkema is redefining performance and sustainability in specialty adhesives. Its 2024 acquisition of Polytec PT expanded its reach into engineering adhesives—notably thermally and electrically conductive materials for electronics and EV battery assembly. Bostik also introduced bio-based hot melt polyamide resins under the Thermelt® brand for automotive and renewable energy applications. Arkema’s innovation strategy integrates renewable raw materials, functionalized polymers, and bio-based chemistries to deliver performance with a lower carbon impact across automotive, medical, and construction sectors.

Ashland continues to invest in sustainable adhesive solutions built on bio-based polymers and cellulose derivatives. Its Q4 2024 launch of low-VOC, water-based adhesives for automotive interiors marks a critical step toward eco-compliant industrial bonding. The company’s ongoing research into biodegradable and multifunctional starch-based platforms supports next-generation adhesive formulations with minimal environmental impact. By focusing on low-VOC neutralizers and high-efficiency systems, Ashland positions itself as a sustainability-forward competitor serving niche, high-value markets requiring superior adhesion with a reduced carbon footprint.

Country Analysis: Global Footprint of Sustainable Adhesives Development

United States – Expanding Bio-Based Feedstocks and Advanced Green Adhesive Applications

The United States sustainable adhesives market is advancing rapidly, driven by public-sector R&D investments and corporate sustainability commitments across automotive, construction, and packaging industries. The Department of Energy (DOE) allocated over $15 million in 2025 toward the development of lignin- and cellulose-derived structural bio-adhesives, aimed at high-strength applications in cross-laminated timber (CLT) and lightweight composites. Concurrently, Ingredion’s 2024 launch of plant-based starch adhesives for paper and corrugated packaging is transforming the sustainable packaging value chain by improving repulpability and recyclability of fiber-based substrates.

In the commercial sector, H.B. Fuller Company introduced a hot-melt adhesive series containing up to 70% renewable raw materials, setting a benchmark for circular adhesive design. The 3M Company’s new reactive hot melt system for consumer electronics and sensor encapsulation exemplifies the market shift toward solvent-free chemistries with superior heat and mechanical resistance. Moreover, AIAG’s updated EV material guidelines are driving automotive manufacturers to adopt low-VOC, solvent-free polyurethane and epoxy systems for interior air quality compliance. Construction adhesives are undergoing a green revolution as manufacturers transition entire product lines toward low-emission, water-based formulations, aligned with LEED and Green Globes certification standards. The evolving landscape cements the U.S. as a leader in high-performance, low-emission, and bio-derived adhesive technologies.

Germany – Innovation Hub for Bio-Based Industrial Adhesives and Circular Manufacturing

Germany continues to lead Europe in sustainable adhesives R&D, driven by EU environmental directives, industrial precision, and world-class polymer innovation. Henkel AG & Co. KGaA expanded its Technomelt low-temperature hot-melt adhesives line in early 2025, designed for recycling-compatible flexible packaging and energy-efficient production. The German Federal Ministry for Economic Affairs and Climate Action (BMWK) is supporting the industrial scalability of lignin-based wood adhesives, advancing the replacement of traditional phenol-resorcinol-formaldehyde (PRF) resins used in mass timber construction.

BASF SE strengthened its sustainable adhesive portfolio through capacity expansion of the Acronal water-based polymer dispersion line in Ludwigshafen, supporting low-VOC coatings and PSAs for European packaging and construction markets. Meanwhile, Jowat SE unveiled a PUR hot-melt adhesive with 50% bio-based content for furniture and edge banding applications, balancing renewable sourcing with superior thermal stability. Automotive clusters across southern Germany are also testing recyclable polyurethane (PU) adhesives that enable detachable bonding in EV battery casings, aligning with EU’s circular economy strategy. The advances position Germany as a pioneer in bio-based adhesive chemistry and sustainable industrial bonding technologies.

China – Green Manufacturing Policies Fuel Eco-Friendly Adhesives Production

China is emerging as a high-growth market for sustainable adhesive systems, propelled by new environmental regulations, EV industry expansion, and green manufacturing mandates. The Ministry of Ecology and Environment’s 2025 national VOC standard tightened emission limits across adhesive categories, accelerating the transition to water-based and solvent-free formulations in footwear, furniture, and architectural applications. Concurrently, Chinese chemical producers are investing in bio-fermentation technology to produce acrylic acid from renewable feedstocks, securing domestic supply for sustainable acrylic adhesives and PSAs.

In the EV manufacturing segment, leading Chinese automakers are mandating low-halogen, lightweight epoxy adhesives for safer, more sustainable battery module assembly. Industrial parks in the Yangtze River Delta are offering tax incentives for non-isocyanate polyurethane (NIPU) adhesive production lines, driving localization of green adhesive technologies. Additionally, expanding solar and wind manufacturing facilities are stimulating demand for environmentally resilient bonding solutions in renewable energy systems. China’s combined industrial capacity, regulatory momentum, and R&D focus make it a critical pillar in the global transition to eco-friendly adhesive manufacturing.

France – Leader in Bio-Polymers and Recyclable Adhesive Solutions

France is at the forefront of sustainable polymer chemistry, emphasizing bio-sourced adhesives and advanced circular packaging solutions. Arkema, through its Bostik brand, launched bio-based polyamide hot-melt adhesives in 2024, with up to 90% renewable castor oil content, catering to automotive textiles and footwear bonding applications. The French Environment and Energy Management Agency (ADEME) continues to fund projects developing reversible adhesive chemistries to meet the EU’s 2030 packaging recyclability targets, an area of growing strategic importance.

Additionally, a domestic French manufacturer introduced a water-based pressure-sensitive adhesive (PSA) certified by European paper mills for 100% repulpability, addressing a major sustainability challenge in paper label recycling. France’s R&D efforts align strongly with the EU Green Deal, emphasizing renewable raw materials, closed-loop recycling, and low-carbon adhesive technologies. The nation’s chemical ecosystem is thus solidifying its role as an innovation hub for advanced sustainable adhesive formulations and circular packaging materials.

India – Local Manufacturing and Policy Push Drive Green Adhesive Adoption

India’s sustainable adhesives market is scaling rapidly, supported by government policy, infrastructure expansion, and local manufacturing initiatives. Pidilite Industries announced in 2025 a major capacity expansion for water-based polymer emulsions used in construction and woodworking adhesives, aligning with growing demand for low-VOC products under India’s Smart Cities and Green Building missions. The Bureau of Indian Standards (BIS) is updating its packaging adhesive standards to support multi-layer film recyclability, signaling a shift toward solvent-free, recycling-compatible formulations.

The Ministry of Housing and Urban Affairs now encourages the use of eco-friendly adhesives in affordable housing programs, promoting locally produced, humidity-resistant sealants for tropical climates. Research at the Indian Institutes of Technology (IITs) is converting agricultural waste like cashew nut shell liquid (CNSL) into bio-based epoxy and phenolic adhesives, showcasing India’s potential in sustainable materials R&D. With accelerating construction, FMCG, and packaging sector growth, India is emerging as a regional leader in scalable, cost-effective, and low-emission adhesive technologies.

Japan – Precision Sustainability in Electronics and Automotive Adhesives

Japan’s sustainable adhesives ecosystem emphasizes precision, performance, and safety, driven by electronics miniaturization and EV innovation. DIC Corporation recently launched a solvent-free polyurethane laminating adhesive for food packaging, offering high heat resistance and minimal monomer migration, ensuring compliance with Japan’s food safety standards. Meanwhile, major automotive OEMs are adopting silane-modified polymer (SMP) adhesives and sealants that are isocyanate-free, delivering long-term flexibility and structural integrity in EV battery enclosures.

The Ministry of Economy, Trade and Industry (METI) supports cutting-edge research into reversible structural adhesives, enabling heat- or chemical-triggered debonding for efficient repair and recycling of electronics and vehicles. Japan’s high-precision manufacturing sector also utilizes biocompatible and bio-derived adhesive systems for wearables and medical devices, blending innovation with environmental responsibility. The nation’s commitment to renewable materials, zero-waste manufacturing, and high-tech bonding performance ensures its continued dominance in precision sustainable adhesive technologies.

Sustainable Adhesives Market Report Scope

Sustainable Adhesives Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$3.4 Billion

|

|

Market Size (2034)

|

$5.5 Billion

|

|

Market Growth Rate

|

5.4%

|

|

Segments

|

By Sustainability Type (Recyclable Adhesives, Water-Based Adhesives, Bio-Based/Renewable Adhesives, Biodegradable), By Raw Material (Water-Based, Plant-Based/Natural, Acrylic-Based, EVA (Ethylene Vinyl Acetate)-Based), By End-Use Industry (Packaging, Building & Construction, Automotive & Transportation, Woodworking & Furniture, Consumer/DIY

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Henkel AG & Co. KGaA, H.B. Fuller Company, 3M Company, Arkema S.A. (Bostik), Dow Inc., Sika AG, BASF SE, Avery Dennison Corporation, Jowat SE

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

By Sustainability Type

- Recyclable Adhesives

- Water-Based Adhesives

- Bio-Based/Renewable Adhesives

- Biodegradable

By Raw Material

- Water-Based

- Plant-Based/Natural

- Acrylic-Based

- EVA (Ethylene Vinyl Acetate)-Based

By End-Use Industry

- Packaging

- Building & Construction

- Automotive & Transportation

- Woodworking & Furniture

- Consumer/DIY

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in Sustainable Adhesives Market

- Henkel AG & Co. KGaA

- H.B. Fuller Company

- 3M Company

- Arkema S.A. (Bostik)

- Dow Inc.

- Sika AG

- BASF SE

- Avery Dennison Corporation

- Jowat SE

*- List not Exhaustive

Research Coverage

Prepared by USDAnalytics, this report investigates how sustainability-led chemistry and decarbonized manufacturing are reshaping industrial bonding, translating bio-based, water-borne, recyclable, and low-VOC platforms into measurable performance at scale; it captures breakthroughs in renewable feedstocks, CCU-derived intermediates, monomaterial packaging laminants, and reversible/debond-on-demand systems, while our analysis reviews specification shifts, compliance trajectories, and total-cost impacts across packaging, mobility, construction, electronics, and woodworking. It also highlights technology roadmaps, ecosystem partnerships, and design-for-circularity practices that move sustainable adhesives from niche to default in high-throughput production—equipping R&D, procurement, and operations leaders to align portfolios with net-zero and EPR outcomes. Built for decision-makers seeking credible, action-ready intelligence, this report is an essential resource for prioritizing investments, qualifying suppliers, and accelerating low-carbon product transitions, etc……

Scope Highlights

Segmentation:

- By Sustainability Type: Recyclable Adhesives; Water-Based Adhesives; Bio-Based/Renewable Adhesives; Biodegradable

- By Raw Material: Water-Based; Plant-Based/Natural; Acrylic-Based; EVA (Ethylene-Vinyl Acetate)-Based

- By End-Use Industry: Packaging; Building & Construction; Automotive & Transportation; Woodworking & Furniture; Consumer/DIY

- By Region: North America; Europe; Asia Pacific; South & Central America; Middle East & Africa

Geographic Scope: Analysis spans 25+ countries across North America, Europe, Asia Pacific, Latin America, the Middle East & Africa.

Time Horizon: Historic data 2021–2024 and forecast data 2025–2034.

Companies: Analysis/profiles of 15+ companies (including Henkel AG & Co. KGaA; H.B. Fuller Company; 3M Company; Arkema S.A. (Bostik); Dow Inc.; Sika AG; BASF SE; Avery Dennison Corporation; Jowat SE).

Deliverables

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.