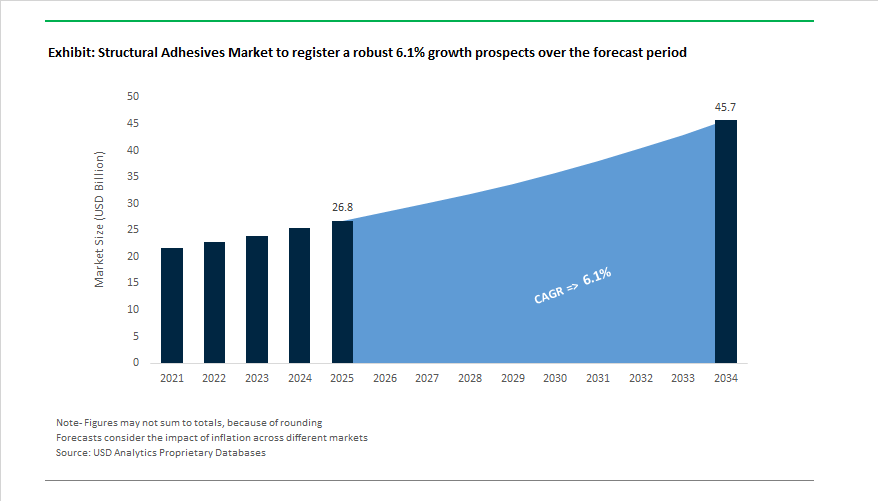

With a market size of USD 26.8 billion in 2025, the Structural Adhesives Market is on track to reach USD 45.7 billion by 2034, reflecting sustained growth at a 6.1% CAGR. The Global Structural Adhesives Market is scaling as a core engineering material category as OEMs redesign products around adhesive-enabled load paths rather than mechanical joints. Across automotive, aerospace, wind energy, rail, and heavy industrial equipment, structural adhesives are now specified at the concept and CAE stage, reflecting their direct impact on stiffness, fatigue life, crash performance, and manufacturability.

From a performance standpoint, leading manufacturers are pushing toughened epoxy systems to deliver lap shear strengths exceeding 25–35 MPa on steel and aluminum, with fracture toughness values (G₁c) that allow bonded joints to outperform spot-welded assemblies under cyclic loading. In parallel, second- and third-generation MMA structural acrylics are increasingly specified where fast fixture times (3–10 minutes) and tolerance to lightly prepared or oily substrates are required—particularly in rail car shells, truck bodies, and composite panel bonding. Further, OEM platforms routinely combine aluminum extrusions, high-strength steel, carbon fiber, SMC, and thermoplastics in a single structure. Structural adhesives are uniquely capable of managing CTE mismatch (often >30–50 µm/m·°C differentials) without inducing stress risers. As a result, adhesive-bonded joints are increasingly replacing rivet-bonded or weld-bonded hybrids, particularly in EV body-in-white architectures and battery enclosure frames.

The market is evolving into a high-specification, high-switching-cost segment, characterized by long OEM qualification cycles, deep application engineering involvement, and strong differentiation based on mechanical performance, processing latitude, and durability assurance. Growth through 2034 will be defined less by incremental volume and more by the continued displacement of welding, riveting, and bolting in load-bearing assemblies, firmly embedding structural adhesives as foundational materials in next-generation manufacturing and lightweight engineering strategies.

The competitive tempo centers on decarbonized feedstocks, regional capacity additions, and next-gen curing agents that sustain structural performance while compressing production cycles. In October 2025, Henkel and Dow expanded their strategic partnership to accelerate decarbonization in adhesives manufacturing by introducing low-carbon feedstocks and renewable electricity into hot-melt production—targeting 20–40% product carbon-footprint cuts for selected lines. Also in October 2025, PPG announced a $380 million aerospace coatings & sealants facility in Shelby, North Carolina (198,000 sq ft) to meet robust demand in aerospace structural bonding.

Earlier in the year, Sika advanced its M&A and footprint strategy: it completed an acquisition in Qatar (June 2025) to deepen access to infrastructure/construction adhesives; it launched a sustainable epoxy hardener with BASF (March 2025) for durable construction structural applications; and it acquired a U.S. building-finishing company (March 2025) to extend distribution for repair and bonding agents. Reinforcing supply resilience, Sika also expanded plants in Singapore and China (January 2025) for adhesives/sealants tied to high-growth construction and industrial demand.

Portfolio focus and market adjacencies remained active. Henkel introduced a medical-grade light-cure adhesive (November 2024) formulated without IBOA or known skin-sensitizers for wearable devices. PPG pursued sharper specialization by divesting its Silicas Products business (September 2024) to concentrate on coatings, sealants, and engineered materials serving aerospace and automotive structural use cases. In a healthcare-relevant adhesive milestone, H.B. Fuller launched Swift Melt 1515-I (January 2024), a bio-compatible hot-melt compliant across India, the Middle East, and Africa for microporous medical tapes requiring robust skin-contact integrity.

Market Trend 1: Accelerated Adoption of Toughened Epoxies and Acrylics for Electric Vehicle Battery Pack Assembly and Lightweighting

The electrification of transportation is radically reshaping the adhesives landscape. As automotive OEMs seek to reduce vehicle weight and enhance energy efficiency, toughened epoxy and acrylic structural adhesives are emerging as critical enablers of multi-material bonding and structural reinforcement.

In the Body-in-White (BIW) stage, advanced adhesives are replacing spot welds and rivets, achieving a mass reduction of up to 10 kg per structure and total weight savings of up to 17 kg—directly correlating to reduced CO₂ emissions and extended EV range. Their ability to create continuous, stress-distributing joints not only reduces fatigue but also improves crash energy absorption, a vital safety consideration in lightweight vehicle architectures.

A defining advantage of these adhesives lies in their compatibility with dissimilar materials, such as aluminum, ultra-high-strength steel, and carbon-fiber composites—a necessity for Cell-to-Body (CTB) battery systems and modular EV platforms. Unlike mechanical fasteners, structural adhesives create hermetic seals that contribute to thermal control and vibration damping, enhancing both safety and performance.

For instance, ThreeBond’s two-component epoxy resin (2.1 W/m·K) exemplifies the fusion of mechanical strength, thermal conductivity, and UL94 V-0 flame retardancy, ensuring safe battery operation while allowing room-temperature curing at 25°C within 24 hours, thus accelerating EV assembly throughput. The marks a clear industrial pivot toward smart structural adhesives that combine functionality, manufacturability, and energy efficiency.

Market Trend 2: Proliferation of Rapid-Curing, Low-Temperature Formulations for Off-Site Construction and Mass Timber

The rise of off-site modular construction and mass timber engineering has redefined adhesive performance expectations. The market is increasingly favoring rapid-curing structural adhesives that function effectively at ambient or low temperatures, supporting continuous production in controlled factory environments and extending usability across climates.

Research into low-temperature epoxy curing demonstrates that curing times can be halved with every 10°C increase above 5°C, emphasizing the demand for systems that maintain mechanical performance without heat acceleration. Advanced modified epoxy resins for timber bonding achieve superior mechanical metrics—up to 9.6 MPa shear strength and 5.18x higher elongation than conventional adhesives—while curing efficiently at room temperature, enabling precision-engineered wood assemblies in cold or variable environments.

Manufacturers are also aligning innovation with sustainability and regulatory compliance. For instance, Henkel’s LOCTITE PURBOND® adhesives, developed for lamination and finger jointing in engineered wood and CLT structures, contain no added formaldehyde and deliver low-VOC performance, aligning with LEED and green building standards.

As prefabrication and sustainable architecture gain momentum globally, these adhesives are becoming integral to achieving lightweight, low-emission, and high-strength building envelopes, particularly in mass timber high-rises where flexibility, strength, and environmental certification intersect.

Market Opportunity 1: Development of Debondable/Reversible Adhesives for Electronics Repair and Component Recycling

As right-to-repair policies and circular economy frameworks gain regulatory traction, manufacturers are investing in debondable structural adhesives to enable non-destructive disassembly and high-value material recovery. The marks a paradigm shift in adhesive technology—from permanence to precision-controlled reversibility.

Academic breakthroughs in electrically detachable structural adhesives have demonstrated ≥90% debonding within one minute under low-voltage activation, enabling safe and residue-free separation of bonded components. The capability is particularly transformative for electronics, automotive modules, and wind turbine blades, where traditional adhesives complicate end-of-life recycling.

In a significant R&D case, vitrimer-based printed circuit boards (vPCBs) utilizing cleavable epoxy resins achieved 98% polymer recovery and 100% fiber recovery after multiple cycles, demonstrating the economic and environmental potential of reversible adhesives.

Regulatory drivers amplify the momentum—the EU’s Right-to-Repair Directive mandates design for repairability, compelling OEMs to adopt debond-on-demand solutions. Companies like Henkel are already pioneering trigger-activated debondable adhesives for EV battery modules, leveraging heat or electrical signals to safely release bonds up to 12 MPa, significantly simplifying repair and recycling processes.

Market Opportunity 2: Engineering of High-Thermal-Conductivity, Electrically Insulating Adhesives for Power Electronics

The transition to wide-bandgap semiconductors (SiC and GaN) in power electronics, 5G infrastructure, and renewable energy systems is driving demand for adhesives that combine structural strength, thermal conductivity, and dielectric insulation. These multifunctional materials are critical to managing heat and maintaining electrical safety in power-dense architectures.

As a benchmark, Toshiba’s SiC module design achieved a 21% reduction in thermal resistance, enabling a 61% reduction in cooling system size, underscoring the transformative role of thermally optimized bonding materials in next-generation inverters.

Commercially, high-performance structural adhesives exhibit thermal conductivity ranging from 0.5 W/m·K to 5 W/m·K, with exceptional dielectric breakdown strength—meeting the demands of battery modules, EV motor assemblies, and renewable inverters. These adhesives ensure long-term mechanical reliability under vibration, temperature cycling, and high voltage.

A prime example is epoxy adhesives with thermal conductivity around 2.1 W/m·K, offering dual functionality as both heat spreaders and structural bonders, allowing design simplification and reduced part count in electric drivetrains and high-frequency electronics.

With miniaturization, higher switching frequencies, and thermal density defining the future of power electronics, high-thermal-conductivity, electrically insulating structural adhesives are poised to become essential materials for EVs, renewable systems, and compact energy storage applications.

Competitive Landscape: Leaders in Structural Epoxies, Toughened PUs, and Fast-Cure Acrylics

The structural adhesives arena is led by diversified materials players combining deep chemistry portfolios, application engineering, and global operations. The five profiled companies below set the pace in strength-to-weight performance, rapid processing, and sustainability.

Henkel’s Loctite (epoxy, MMA) and Technomelt (hot-melt) platforms anchor a broad portfolio spanning Mobility & Electronics, medical, and industrial applications. With 61 labs in 30 countries, Henkel scales innovation into production rapidly. In October 2025, it expanded its partnership with Dow to embed low-carbon feedstocks/renewables into hot-melt manufacturing, targeting 20–40% CO₂e cuts on selected products. Henkel also advances AI-assisted formulation to speed development cycles and is aligned to Scope 3 reduction goals (30% by 2030), while servicing EV assembly and ADAS with high-reliability structural solutions.

Sika delivers polyurethane, epoxy, and silane-terminated polymer (STP) structural solutions under SikaPower®/SikaForce® and one-component Sikaflex®. Its SmartCore® technology toughens 2K cold-curing epoxies for impact-resistant structures, and Purform® reduces free monomeric diisocyanate for REACH compliance. In 2025, Sika opened new plants in Singapore and China to back regional growth, acquired in Qatar (June 2025) to reinforce GCC presence, and executed U.S. distribution expansion (March 2025)—broadening access to structural bonding and reinforcement (e.g., Sikadur® for bridges, CFRP systems).

H.B. Fuller focuses on aerospace, electronics, and new energy with a portfolio covering structural epoxy, PU, and MMA. It emphasizes battery structural adhesives and sealants engineered for IP67+ sealing and mechanical robustness in EV packs. The company advances three innovation streams—new product creation, product enhancement, and process innovation—and deploys FIP/CIP gasket technologies for complex assemblies. Its Technical Center of Excellence accelerates high-performance solutions in construction glazing/IG and energy-efficient envelopes.

Dow supplies acrylic, polyurethane, and silicone systems (e.g., DOWSIL™) for construction, electronics, and mobility with a focus on environmental resistance, vibration damping, and thermal stability. In October 2025, Dow partnered with Henkel to supply low-carbon feedstocks and renewable energy pathways for decarbonizing the hot-melt value chain. Dow’s material science enables lighter, stronger, energy-efficient designs—supporting glazing, façade, and fire-protection assemblies as well as EV bonding and gasketing.

PPG brings coatings, sealants, and engineered materials with deep aerospace credentials, including SEMKIT® packaging for precise 2-component mixing. In October 2025, PPG announced a $380M aerospace coatings & sealants facility in North Carolina to expand structural capabilities. Portfolio focus continued with the September 2024 silicas divestiture, freeing capital for high-margin aerospace/automotive structural solutions, including composite bonding resins (e.g., from Cuming Microwave) for advanced airframe integration.

Structural Adhesives Market Report Scope

Structural Adhesives Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$26.8 Billion

|

|

Market Size (2034)

|

$45.7 Billion

|

|

Market Growth Rate

|

6.1%

|

|

Segments

|

By Resin Type (Epoxy, Polyurethane (PU), Acrylic, Cyanoacrylate, Others), By End-Use Industry (Building & Construction, Automotive & Transportation, Aerospace & Defense, Wind Energy, Marine, Electronics), By Technology (Water-Based, Solvent-Based, Reactive (1K & 2K)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Henkel AG & Co. KGaA, 3M Company, Sika AG, H.B. Fuller Company, Arkema S.A. (Bostik), DuPont, Huntsman Corporation, Dow Inc., Illinois Tool Works Inc. (ITW)

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

By Resin Type (Chemistry)

- Epoxy

- Polyurethane (PU)

- Acrylic

- Cyanoacrylate

- Others

By End-Use Industry

- Building & Construction

- Automotive & Transportation

- Aerospace & Defense

- Wind Energy

- Marine

- Electronics

By Technology/Product Type

- Water-Based

- Solvent-Based

- Reactive (1K & 2K)

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in Structural Adhesives Market

- Henkel AG & Co. KGaA

- 3M Company

- Sika AG

- H.B. Fuller Company

- Arkema S.A. (Bostik)

- DuPont

- Huntsman Corporation

- Dow Inc.

- Illinois Tool Works Inc. (ITW)

*- List not Exhaustive

Research Coverage

Prepared by USDAnalytics, this report investigates the Structural Adhesives Market through the lens of end-use performance, manufacturability, and compliance—connecting chemistry advances in epoxies, PUs, and (meth)acrylates to measurable gains in lightweighting, fatigue life, corrosion resistance, and takt time. It captures breakthroughs in fast-cure systems, thermal/electrical functionality, and debond-on-demand platforms; our analysis reviews OEM specification shifts, multi-material joining strategies (BIW, CTB/CTC), and durability envelopes across transportation, wind, marine, construction, and electronics. It highlights the cost, energy, and sustainability implications of migrating from welds/rivets to structural bonding—covering supply security, low-carbon feedstocks, and factory integration—so engineering, procurement, and operations leaders can benchmark options with confidence; this report is an essential resource for portfolio planning, supplier qualification, and risk-managed adoption of next-generation structural adhesives, etc……

Scope Highlights

Segmentation:

- By Resin Type (Chemistry): Epoxy; Polyurethane (PU); Acrylic; Cyanoacrylate; Others

- By End-Use Industry: Building & Construction; Automotive & Transportation; Aerospace & Defense; Wind Energy; Marine; Electronics

- By Technology/Product Type: Water-Based; Solvent-Based; Reactive (1K & 2K)

- By Region: North America; Europe; Asia Pacific; South & Central America; Middle East & Africa

Geographic Scope: Analysis spans 25+ countries across North America, Europe, Asia Pacific, Latin America, the Middle East & Africa.

Time Horizon: Historic data 2021–2024 and forecast data 2025–2034.

Companies: Analysis/profiles of 15+ companies, including Henkel AG & Co. KGaA; 3M Company; Sika AG; H.B. Fuller Company; Arkema S.A. (Bostik); DuPont; Huntsman Corporation; Dow Inc.; Illinois Tool Works Inc. (ITW) — list not exhaustive.

Deliverables

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.