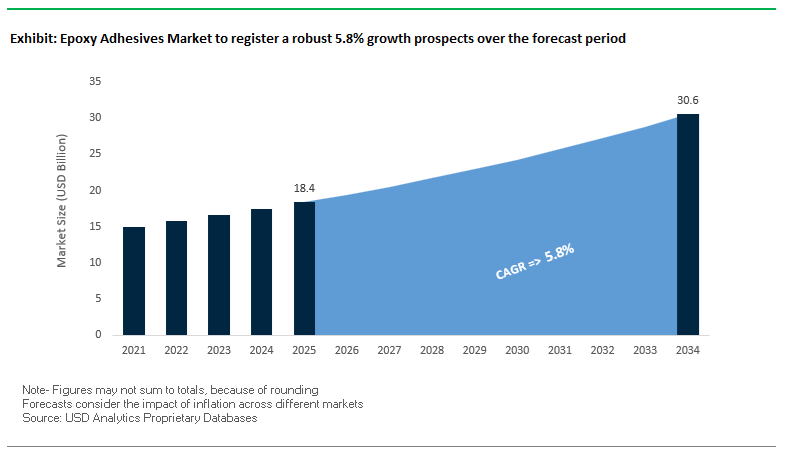

The Global Epoxy Adhesives Market is projected to expand from USD 18.4 billion in 2025 to USD 30.6 billion by 2034, progressing at a CAGR of 5.8%, as epoxy-based bonding systems become structurally indispensable across automotive, aerospace, electronics, construction, and renewable energy manufacturing. This growth is not volume-driven but performance-led: epoxy adhesives are increasingly specified where joints must withstand sustained mechanical loads, wide thermal cycling, chemical exposure, and long service lifetimes. In lightweight vehicle platforms, wind energy structures, and power electronics assemblies, epoxies enable multi-material bonding strategies that replace mechanical fastening and welding, directly supporting OEM objectives around weight reduction, energy efficiency, and modular system design.

From a materials and engineering perspective, epoxy adhesives continue to set the benchmark for strength-to-weight ratio and thermal stability. Structural epoxy systems routinely maintain mechanical integrity from −50°C to above 200°C, allowing reliable bonding in engines, turbines, battery enclosures, and electronic encapsulation environments where thermal excursions are unavoidable. Two-component epoxy formulations achieving lap shear strengths exceeding 20 N/mm² on steel substrates have become standard in load-bearing assemblies, enabling fastener elimination without compromising joint durability. In composite-intensive applications such as wind turbine blades and automotive structural components, epoxy resin systems supporting fiber volume contents up to 65% are critical for efficient load transfer, fatigue resistance, and dimensional stability under cyclic stress.

Ongoing innovation in 1K and 2K epoxy technologies is increasingly shaped by regulatory and system-level constraints rather than incremental performance gains. Thermally conductive epoxy adhesives reaching 1.4 W/m·K are central to EV battery modules and power electronics, where heat dissipation and electrical insulation must be delivered simultaneously within compact architectures. At the same time, tightening environmental and occupational regulations are accelerating the transition toward low-BPA and non-CMR epoxy chemistries, forcing manufacturers to redesign curing agents, resin backbones, and additive packages without sacrificing high-temperature performance or mechanical reliability.

The epoxy adhesives industry is experiencing a phase of transformative innovation characterized by safer formulations, circular material adoption, and advanced aerospace applications. Key developments illustrate how leading producers are realigning their portfolios to address both performance and environmental expectations.

In September 2025, Huntsman Advanced Materials launched a newly reformulated range of ARALDITE® epoxy adhesives, free from Bisphenol A (BPA) and substances classified as Carcinogenic, Mutagenic, or Reprotoxic (CMR). This initiative marks a decisive shift toward sustainable epoxy chemistries, ensuring compliance with evolving EU REACH standards and improving worker safety in industrial manufacturing. Simultaneously, Huntsman introduced Post-Consumer Recycled (PCR) plastic cartridges for selected ARALDITE® products, cutting CO₂ emissions by up to 36% compared to virgin plastics—a significant step toward sustainable packaging in industrial adhesives.

In Q3 2025, 3M Company unveiled its next-generation aerospace structural adhesive film, part of the Scotch-Weld™ portfolio, engineered for bonding composite and metallic aircraft components. This advanced epoxy adhesive film offers superior fracture toughness and consistent bonding performance across a wide temperature range, addressing critical needs in OEM and MRO aerospace markets. Around the same time, Olin Corporation reaffirmed its sustainability roadmap by announcing its goal of achieving carbon neutrality by 2050, emphasizing renewable energy use and process efficiency in its epoxy resin production, which forms the backbone for many adhesive formulations.

The automotive sector, a dominant end-user, continued its transition to 2K epoxy systems throughout 2025, driven by the structural integration of aluminum and carbon fiber composites in next-generation vehicles. These adhesives enable improved crash resistance and rigidity while reducing overall vehicle mass, contributing to EV range optimization. Meanwhile, Henkel’s Loctite hybrid epoxy adhesives, launched in late 2025, blended the properties of structural and instant adhesives—offering fast curing and long-term durability ideal for automotive assembly, electronics encapsulation, and MRO repairs.

Further industry diversification was visible in Hexion’s strategic separation (Q4 2024) into dedicated business entities, one focusing on specialty epoxy resins for wind energy and EV applications. This move strengthened its positioning as a raw material leader for high-performance composites. However, U.S. trade tariffs introduced in early 2025 on specialty chemicals created cost pressures across the epoxy adhesive supply chain, prompting manufacturers to diversify sourcing and prioritize regionalized production strategies to stabilize margins.

The proliferation of wide-bandgap semiconductors (WBG) such as Silicon Carbide (SiC) and Gallium Nitride (GaN) across electric vehicles (EVs), power modules, and renewable energy systems is reshaping adhesive performance standards. These systems generate extreme heat at high switching frequencies, making thermally conductive yet electrically insulating epoxy adhesives indispensable for heat management and long-term device reliability.

Recent Epoxy Resin Composite Dielectrics (ERCD) innovations demonstrate thermal conductivities up to 10 W/m·K and glass transition temperatures (Tg) exceeding 300°C, engineered for double-sided cooled (DSC) SiC power modules. The high thermal stability enables survival under thermal cycling tests from 240°C to 125°C over 3,000 cycles, ensuring durability in demanding EV and industrial inverter applications.

Equally critical are epoxy molding compounds (EMCs) with high Tg (≈205°C) and low Coefficient of Thermal Expansion (CTE ≈10 ppm/°C), optimized to protect semiconductor packages under High-Temperature Reverse Bias (HTRB) testing. Advanced filler technologies, notably Silicon Nitride (Si₃N₄) and Boron Nitride (BN)—have been proven to enhance conductivity fourfold with only a 2 wt% loading, achieving superior heat dissipation and dielectric insulation.

These breakthroughs reflect an industry-wide transition toward high-efficiency thermal management adhesives tailored for EV power electronics, 5G communication modules, and energy storage inverters.

The expanding use of carbon-fiber composites in aerospace, wind energy, and automotive lightweighting is accelerating the demand for toughened epoxy systems that cure efficiently at low to moderate temperatures, reducing production energy costs and minimizing part distortion.

Advanced rubber-toughened thermoset epoxies are designed with secondary thermoplastic phases and elastomeric modifiers that enhance interlaminar fracture toughness, crucial for preventing microcracking under fatigue and impact loading. In aerospace composites, formulations like IM7/8551-7 epoxy systems have shown improved interlaminar shear strength while maintaining structural stiffness, meeting FAA-level damage tolerance criteria.

In carbon-fiber motor casing applications, optimized toughened epoxy matrices achieved interlaminar shear strengths (ILSS) up to 122 MPa with T800 carbon fiber, outperforming standard T300/T700 systems (~90 MPa). Such systems significantly extend fatigue life in rotor housings and fuselage components, particularly in aerospace and electric aviation applications.

These developments are not only technical improvements but also align with sustainability goals—enabling low-temperature curing (<120°C) that lowers energy consumption by up to 30% and supports integration with automated composite manufacturing. The result is a new class of high-toughness, low-energy epoxy formulations that deliver both environmental and performance advantages.

The rapid global expansion of renewable energy infrastructure, particularly offshore wind, is driving massive demand for long-pot-life, high-strength epoxy adhesives engineered for both manufacturing and repair of turbine blades exceeding 80 meters in length.

Next-generation wind blade bonding systems feature controlled pot lives up to 260 minutes, maintaining high fracture toughness and excellent adhesion to composite substrates. These features are essential for the precise assembly of large blade sections, reducing downtime in blade alignment and bonding processes.

With the U.S. federal target of 30 GW of offshore wind capacity by 2030, the demand for high-durability epoxy adhesives in marine and coastal installations is intensifying. The Bureau of Ocean Energy Management (BOEM) has already approved over a dozen offshore wind projects, signaling a robust market for marine-grade structural epoxies that can withstand salt spray, humidity, and long-term water exposure.

Repair-grade epoxy systems are equally vital to reduce maintenance costs. Proven formulations retain lap shear strength of 26 MPa after 1,000 hours in 50°C saltwater at 80% humidity, ensuring longevity and safety in harsh offshore environments. The application space drives the pivotal role of environmentally resistant epoxy systems in maintaining the operational integrity of global wind energy assets.

The global race to commercialize Solid-State Batteries (SSBs) is creating a high-value market for specialized epoxy adhesives that provide hermetic sealing, chemical resistance, and mechanical stability in next-generation EV batteries. These adhesives serve dual functions in cell encapsulation, electrolyte bonding, and thermal protection.

Unlike conventional liquid electrolyte systems, SSBs rely on solid ceramic or glass electrolytes, which require adhesives capable of bonding rigid interfaces while resisting high temperatures (up to 165°C) and exposure to corrosive salts. Epoxy systems are uniquely suited to the challenge, providing high dielectric strength and low ionic permeability, essential for maintaining cell integrity over thousands of charge cycles.

In laboratory-scale SSBs, epoxy encapsulants are preferred for micro-sealing applications due to their chemical inertness and ability to prevent gas leakage. Additionally, structural electrolyte research shows epoxy incorporation can raise the Young’s modulus to 0.65 GPa, improving the mechanical resilience of the solid electrolyte layer.

As major automakers and battery developers—such as Toyota and QuantumScape—move toward SSB commercialization between 2027–2030, the demand for battery-safe epoxy adhesives will surge. These systems must deliver not only mechanical bonding and chemical resistance but also compatibility with automated dispensing and curing systems within gigafactories, cementing their importance in the future of electric mobility manufacturing.

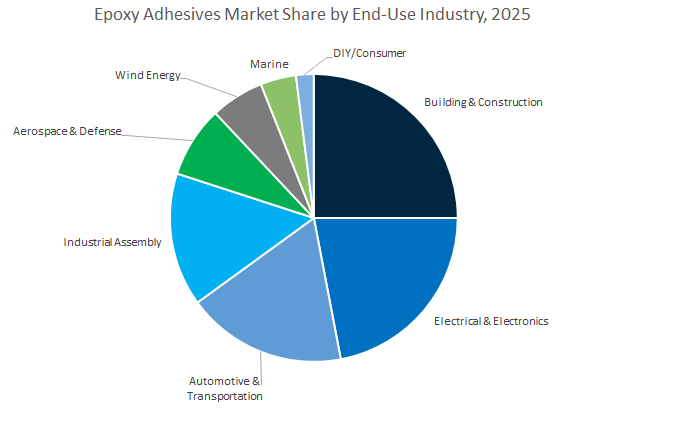

Epoxy Adhesives Market Share Insights, 2025-2034

Two-component epoxy adhesives represent the largest and most versatile segment in the global epoxy adhesives industry, commanding a projected 58.5% market share in 2025. These systems—comprising separate resin and hardener components—provide unmatched flexibility in formulation, enabling control over working time, cure rate, and bond strength. Their superior mechanical properties, chemical resistance, and ability to cure at room temperature make them indispensable in construction, industrial assembly, marine, and energy applications. In infrastructure repair, they are the adhesive of choice for crack injection, concrete anchoring, and steel bonding, while in manufacturing, they are used for equipment assembly and heavy-duty composite joining. The two-part systems are particularly valued for their structural integrity and long-term durability, even under dynamic loads or thermal cycling. Moreover, the expanding use of low-VOC and solvent-free formulations aligns with environmental compliance requirements, further strengthening their adoption across industrialized and emerging markets alike. As industries increasingly shift toward lightweight materials and mixed-substrate bonding, two-component epoxies continue to lead the market due to their ability to bond metals, composites, and plastics with equal efficiency.

The one-component epoxy adhesives segment is gaining rapid traction, driven by the need for process efficiency and consistent quality in automated production lines. Unlike two-component systems, these adhesives are pre-mixed and cure upon exposure to heat, providing a uniform and void-free bond that meets the stringent standards of automotive, aerospace, and electronics manufacturing. They are widely used in structural automotive bonding, electronic encapsulation, and motor assembly, where precision and repeatability are critical. Their thermal curing process ensures predictable performance, enabling high-strength joints with excellent resistance to vibration, fatigue, and temperature extremes. The increasing adoption of electric vehicles (EVs), 5G components, and miniaturized electronics is significantly boosting demand for one-component epoxy formulations that offer fine-line application, high dielectric strength, and strong adhesion to metals and composites. As automation and smart manufacturing expand globally, these heat-curable, single-component systems are emerging as a key enabler of high-throughput, quality-driven production environments.

The building and construction segment holds the largest share of the global epoxy adhesives market, projected at 24.3% by 2025, driven by their extensive use in concrete bonding, structural repair, flooring, and anchoring applications. Epoxy adhesives are indispensable in both new construction and restoration projects, where they are used to bond steel reinforcements, patch cracks, and provide structural integrity to aging infrastructure. Their high tensile strength, chemical resistance, and ability to cure under varying conditions make them essential for civil engineering and architectural applications. Furthermore, the surge in urbanization, modular construction, and smart city initiatives is fueling demand for high-performance adhesives that offer long-term durability and safety. The growing emphasis on sustainable construction materials and VOC-compliant epoxy systems is reinforcing their position as a preferred solution in modern architectural design and infrastructure resilience projects.

The electrical and electronics industry represents one of the most dynamic segments of the epoxy adhesives market, characterized by constant innovation and miniaturization. Epoxy adhesives are critical for semiconductor packaging, printed circuit board (PCB) assembly, potting, and encapsulation, providing both mechanical protection and electrical insulation. Their superior thermal conductivity, dielectric strength, and chemical stability make them indispensable for heat dissipation and component reliability in high-performance electronic devices. As the 5G network rollout, EV electronics integration, and IoT expansion accelerate, the need for high-purity, low-outgassing epoxy formulations is expanding rapidly. These adhesives are also favored for sensitive electronic assemblies where reworkability and precision are required. Manufacturers are increasingly developing low-temperature curing and halogen-free epoxy systems, aligning with both sustainability standards and global electronics safety regulations.

The epoxy adhesives market remains dominated by innovation-led players who combine materials science expertise, sustainability initiatives, and application-specific specialization. Major contributors such as Henkel AG & Co. KGaA, Huntsman Corporation, 3M Company, Olin Corporation, and Hexion Inc. continue to expand their reach across automotive, aerospace, and renewable energy sectors, introducing solutions that meet both technical and environmental performance demands.

Henkel leads the global structural adhesive market under its Loctite brand, offering a wide range of two-part epoxies, thermally conductive systems, and hybrid adhesives. Its LOCTITE® EA 9497, with temperature resistance up to 200°C, is widely used in electronics thermal management. Henkel’s hybrid adhesives combine the benefits of epoxies and cyanoacrylates, reducing curing times to seconds, enhancing manufacturing efficiency. The company’s global R&D footprint of over 60 production and innovation centers allows for localized customization in automotive, aerospace, and industrial repair sectors.

Huntsman’s ARALDITE® range remains synonymous with composite bonding and aerospace durability, supporting critical applications in wind turbine blades and EV composites. Its September 2025 launch of BPA- and CMR-free ARALDITE® products aligns with the EU’s sustainable materials agenda. Huntsman’s advanced simulation tools cut adhesive qualification time by up to 50%, while its resin systems enable fiber volume fractions up to 65%, improving the strength-to-weight ratio in lightweight composite assemblies.

3M dominates the aerospace epoxy adhesives segment through its Scotch-Weld™ product line, supporting structural and honeycomb bonding across aircraft fuselages and interiors. Its latest epoxy adhesive films exhibit service temperature stability up to 177°C (350°F) and superior fracture resistance, ensuring long-term reliability under fluctuating pressure and thermal conditions. Integrated with surface treatment and dispensing systems, 3M provides turnkey bonding solutions for advanced aerospace manufacturing and maintenance.

Olin Corporation, one of the world’s largest producers of epoxy resins and intermediates, plays a critical upstream role in the adhesive value chain. Its vertically integrated operations secure a stable global supply of basic epoxy resin building blocks. The company’s product portfolio targets aerospace coatings, composite adhesives, and electrical encapsulants, and it has pledged to achieve net-zero carbon emissions by 2050. Olin’s innovation strategy centers on renewable feedstocks and energy-efficient resin manufacturing for sustainable epoxy adhesive production.

Hexion Inc. is reinforcing its leadership in specialty epoxy systems for wind energy blades, engineered wood, and automotive electrification following its 2024 business restructuring. Its specialty resins division delivers high-performance adhesives and hardeners optimized for durability and energy efficiency in structural composites. Recognized with 12 Responsible Care® Awards from the American Chemistry Council, Hexion exemplifies safety and sustainability leadership, actively advancing low-VOC, high-durability epoxy innovations for the global renewable energy transition.

The United States epoxy adhesives market continues to lead global innovation, guided by stringent regulatory frameworks, rising environmental accountability, and continuous technological advancements across aerospace, defense, and electronics sectors. The U.S. Environmental Protection Agency (EPA) finalized its 2024 update to the National Emission Standards for Hazardous Air Pollutants (NESHAP) for epoxy resin production, targeting a reduction of approximately 105 tons of hazardous emissions annually, primarily epichlorohydrin. The new compliance requirement compels U.S. manufacturers to adopt cleaner, low-VOC epoxy formulations and reengineer production methods to meet strict emission benchmarks.

Defense and aerospace continue to drive demand for high-strength, fatigue-resistant epoxy adhesives certified for extreme environments. Ongoing Department of Defense (DoD) contracts and new programs for next-generation aircraft are stimulating market growth for high-temperature, structural bonding adhesives designed for carbon-fiber composites. Additionally, the GSA’s 2024 Facilities Standards (P100) mandates the use of low-VOC materials in federal construction projects, further accelerating the transition toward environmentally compliant epoxy bonding agents. The electronics industry adds another growth vector, with U.S. specialty chemical manufacturers launching thermally conductive, fast-curing epoxy adhesives optimized for compact consumer electronics and automotive sensor applications. The combination of regulatory alignment, aerospace investment, and miniaturization trends positions the U.S. as a global benchmark for sustainable, high-performance epoxy adhesive technologies.

China remains the largest producer and consumer in the global epoxy adhesives industry, driven by massive domestic manufacturing capacity, expanding EV production, and rapid growth in the electronics and infrastructure sectors. The launch of new epoxy adhesive grades (CSA6250, CSE6508, CSE6587) in Q4 2024 by a leading local manufacturer highlights China’s commitment to localized innovation for high-reliability applications in electronics and medical devices, with a focus on thermal stability and environmental compliance.

China’s Electric Vehicle (EV) ecosystem is a primary growth catalyst, spurring significant R&D investments in flame-retardant and thermally conductive epoxy encapsulants used in battery packs and electronic modules to enhance safety and energy efficiency. Additionally, rising investment in aerospace-grade composite materials has created a strong need for two-component toughened epoxy adhesives in aircraft assembly and carbon-fiber structures. On the infrastructure side, large-scale high-speed rail, bridge, and dam projects are sustaining strong consumption of epoxy mortars and anti-corrosion repair adhesives, critical for long-term durability. Supported by government policy favoring local material innovation and green manufacturing, China continues to expand its foothold as a global hub for high-performance, industrial-grade epoxy adhesives used across EV, electronics, and heavy infrastructure applications.

Germany’s epoxy adhesives market is evolving rapidly as the nation leads Europe’s transition to lightweight mobility, automation, and Industry 4.0-based manufacturing ecosystems. German automotive OEMs and engineering firms are integrating robotic and automated adhesive dispensing systems, enabling precise, high-throughput bonding operations across vehicle body, powertrain, and electronics assembly lines. Adhesive suppliers are investing in pre-programmed epoxy systems that integrate seamlessly with smart robotic lines, supporting efficiency, consistency, and reduced waste in automotive production.

R&D in low-temperature curing structural epoxy adhesives is advancing quickly to facilitate multi-material bonding, especially between aluminum, composites, and carbon fiber—materials central to the electric vehicle transition. German manufacturers are expanding production capacity for industrial-grade epoxy adhesives to serve the machinery, tooling, and precision engineering sectors, which demand ultra-reliable bonding performance under dynamic stress. The innovations align with Germany’s long-standing reputation for precision engineering, sustainability, and automation excellence, reinforcing its role as Europe’s core center for next-generation industrial epoxy adhesive manufacturing.

India’s epoxy adhesives industry is witnessing rapid expansion, supported by strong government incentives, infrastructure growth, and industrial localization. In Q2 2024, a global adhesive leader inaugurated a new production facility in Kurkumbh, Maharashtra, enhancing the country’s capacity for epoxy and structural adhesives used in automotive, electronics, and construction sectors. The government’s “Make in India” initiative is accelerating local manufacturing of crash-resistant epoxy adhesives for body-in-white (BIW) automotive applications, reducing dependency on imports and supporting supply chain resilience.

Furthermore, India’s growing wind energy sector, both onshore and offshore, is creating substantial demand for epoxy resin systems used in wind turbine blade bonding and composite reinforcement. As the nation expands its renewable energy capacity, epoxy formulations with enhanced fatigue resistance and durability are becoming central to component production. Combined with infrastructure projects in roadways, rail, and housing, India’s domestic consumption of industrial-grade epoxy adhesives is set to increase sharply, positioning the country as a rising manufacturing hub in the global epoxy adhesives market.

Mexico’s strategic proximity to the United States, combined with its rapidly growing automotive and construction industries, is transforming the country into a vital epoxy adhesive production and export base in Latin America. In Q3 2024, a global specialty chemicals manufacturer opened a state-of-the-art production facility in Querétaro, dedicated to expanding regional epoxy adhesive capacity to support automotive manufacturing and large-scale construction projects across North and Central America.

The expansion strengthens cross-border supply chains, enabling shorter lead times and localized support for OEMs requiring high-strength structural bonding adhesives. Mexico’s construction sector also benefits significantly, with epoxy-based sealants and concrete repair systems gaining traction in infrastructure projects such as highways, bridges, and commercial complexes. The country’s growing integration with the U.S. and Canadian markets under the USMCA framework continues to enhance its competitiveness, positioning Mexico as a key player in regional epoxy adhesive production and distribution.

France is playing a leading role in redefining epoxy adhesive sustainability and recyclability through major European initiatives that align with the EU Circular Economy Action Plan. The ZEBRA (Zero wastE Blade ReseArch) project, a groundbreaking French-led consortium, achieved a major milestone in Q4 2024 by successfully demonstrating closed-loop recycling of wind turbine blades using compatible epoxy resin and adhesive systems. The achievement establishes a new benchmark for recyclable composite structures and influences the development of eco-compatible epoxy alternatives for industrial applications.

At the same time, France’s aerospace industry continues to advance its use of high-performance epoxy adhesives. A major European specialty materials company launched AeroPaste 1003 in Q2 2024, a structural epoxy paste adhesive designed for Advanced Air Mobility (AAM), Commercial Aerospace, and Defense applications, offering improved processing flexibility and faster assembly cycles. The developments reflect France’s leadership in both environmental innovation and aerospace technology, placing it at the center of Europe’s evolution toward recyclable, high-strength epoxy bonding systems.

Japan continues to lead the high-precision electronics segment of the global epoxy adhesives market, leveraging its expertise in semiconductor packaging, automotive sensors, and display technologies. Local R&D efforts are heavily focused on ultra-thin, thermally conductive epoxy die-attach adhesives that provide excellent electrical insulation and heat dissipation, supporting next-generation semiconductor miniaturization and high-resolution display assembly.

Japanese chemical manufacturers, in collaboration with Tier 1 automotive suppliers, are developing advanced epoxy encapsulants for ADAS (Advanced Driver-Assistance Systems) sensors and cameras, ensuring long-term reliability in extreme temperature and vibration environments. The adhesives are crucial for the country’s leading automotive brands integrating electronic control systems in EVs. As Japan continues to advance materials engineering and thermal management capabilities, it solidifies its global leadership in high-technology, precision-grade epoxy adhesives for electronics and automotive applications.

Epoxy Adhesives Market Report Scope

Epoxy Adhesives Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$18.4 Billion

|

|

Market Size (2034)

|

$30.6 Billion

|

|

Market Growth Rate

|

5.8%

|

|

Segments

|

By Component Type (One-Component Epoxy Adhesives, Two-Component Epoxy Adhesives, Film Epoxy Adhesives), By Technology (Solvent-Based Epoxy Adhesives, Water-Based Epoxy Adhesives, Hot-Melt Epoxy Adhesives, Reactive Epoxy Adhesives), By Curing Mechanism (Room Temperature Curing, Heat-Curing, UV/LED-Curing, Chemically-Curing), By End-User (Automotive & Transportation, Aerospace & Defense, Building & Construction, Wind Energy, Electrical & Electronics, Marine, Industrial Assembly, DIY/Consumer), By Resin (Bisphenol A Epoxy, Bisphenol F Epoxy, Novolac Epoxy, Aliphatic Epoxy, Other Specialized Epoxies

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Henkel AG & Co. KGaA, 3M Company, Huntsman Corporation, Sika AG, H.B. Fuller Company, Dow Chemical Company, Arkema S.A., DuPont de Nemours, Inc., Mitsubishi Chemical Corporation, Momentive Performance Materials Inc., Ashland Global Holdings Inc., Master Bond Inc., Olin Corporation, PPG Industries, Inc., Permabond LLC

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

By Component Type

- One-Component Epoxy Adhesives

- Two-Component Epoxy Adhesives

- Film Epoxy Adhesives

By Technology/Formulation

- Solvent-Based Epoxy Adhesives

- Water-Based Epoxy Adhesives

- Hot-Melt Epoxy Adhesives

- Reactive Epoxy Adhesives

By Curing Mechanism

- Room Temperature Curing

- Heat-Curing

- UV/LED-Curing

- Chemically-Curing

By End-Use Industry

- Automotive & Transportation

- Aerospace & Defense

- Building & Construction

- Wind Energy

- Electrical & Electronics

- Marine

- Industrial Assembly

- DIY/Consumer

By Chemistry/Resin

- Bisphenol A Epoxy

- Bisphenol F Epoxy

- Novolac Epoxy

- Aliphatic Epoxy

- Other Specialized Epoxies

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

- Henkel AG & Co. KGaA

- 3M Company

- Huntsman Corporation

- Sika AG

- H.B. Fuller Company

- Dow Chemical Company

- Arkema S.A.

- DuPont de Nemours, Inc.

- Mitsubishi Chemical Corporation

- Momentive Performance Materials Inc.

- Ashland Global Holdings Inc.

- Master Bond Inc.

- Olin Corporation

- PPG Industries, Inc.

- Permabond LLC

*- List not Exhaustive

Research Coverage

Prepared by USDAnalytics, this report investigates the Epoxy Adhesives Market end-to-end—delivering analysis reviews on demand catalysts, qualification criteria, and procurement risks while mapping specification shifts in structural, thermal, and electrically insulating epoxy systems. It highlights recent breakthroughs in BPA/CMR-free chemistries, high-toughness/low-temperature cure platforms for composites, and thermally conductive encapsulants for WBG power electronics; compares performance on shear/peel, fracture toughness, Tg/CTE, dielectric strength, and long-term aging; and aligns these with compliance needs across REACH, VOC, and aerospace/automotive OEM standards. With decision frameworks for replacing mechanical fasteners, validated application playbooks (from BiW joints to wind blade bonding and PCB potting), and vendor capability benchmarking, this report is an essential resource for engineering leaders, sourcing teams, and R&D stakeholders seeking faster specification, safer production, and lower total applied cost in high-reliability manufacturing.

Scope Highlights

Segmentation:

- By Component Type: One-Component Epoxy Adhesives; Two-Component Epoxy Adhesives; Film Epoxy Adhesives.

- By Technology/Formulation: Solvent-Based; Water-Based; Hot-Melt; Reactive Epoxy Adhesives.

- By Curing Mechanism: Room-Temperature; Heat-Curing; UV/LED-Curing; Chemically-Curing.

- By End-Use Industry: Automotive & Transportation; Aerospace & Defense; Building & Construction; Wind Energy; Electrical & Electronics; Marine; Industrial Assembly; DIY/Consumer.

- By Chemistry/Resin: Bisphenol A Epoxy; Bisphenol F Epoxy; Novolac Epoxy; Aliphatic Epoxy; Other Specialized Epoxies.

Geographic Scope: Analysis spans 25+ countries across North America, Europe, Asia Pacific, Latin America, the Middle East & Africa.

Time Frame: Historic data 2021–2024 and forecast data 2025–2034.

Companies: Analysis/profiles of 15+ companies including strategic moves, technology focus, certifications, and sustainability roadmaps.

Deliverables

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.