Market Overview: Structural, Thermally Functional, and Low-Monomer Adhesives Redefining Performance-Critical Manufacturing

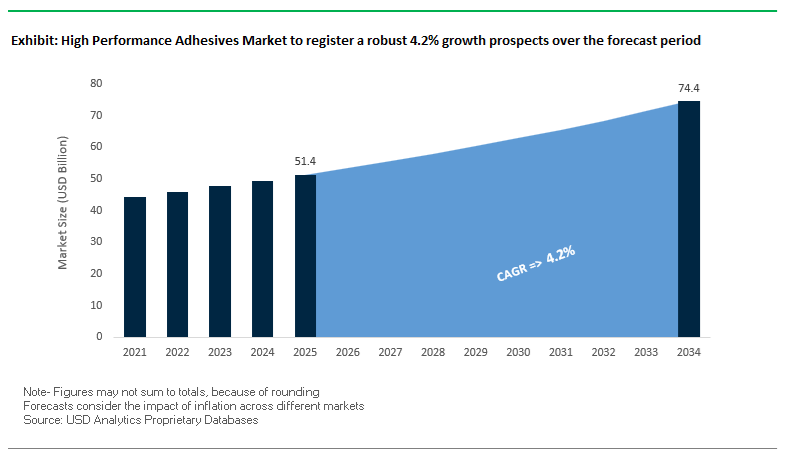

The Global High-Performance Adhesives Market is projected to expand from USD 51.4 billion in 2025 to USD 74.4 billion by 2034, advancing at a CAGR of 4.2%, as adhesives move decisively into the role of primary structural and functional materials across aerospace, automotive lightweighting, electronics, EV battery systems, and advanced construction. Growth is not volume-led; it is driven by OEM-level redesign of assemblies where adhesives replace welding, riveting, and mechanical fastening to enable weight reduction, thermal control, vibration damping, and multi-material integration. High-performance epoxies, polyimides, and reactive polyurethane (PUR) systems dominate this transition because they deliver predictable mechanical performance under sustained load, thermal cycling, and chemical exposure—conditions where conventional joining methods introduce stress concentrations and long-term reliability risks.

From a materials and compliance standpoint, the market is being reshaped by regulatory pressure and process engineering constraints rather than incremental performance gains. Major manufacturers such as Henkel, 3M, Sika, H.B. Fuller, Arkema (Bostik), Dow, and Huntsman have restructured portfolios around low-monomer, low-VOC, and waterborne technologies to align with REACH and global occupational safety requirements without sacrificing bond integrity. Next-generation PUR hot-melt systems with <0.1% free monomeric diisocyanate are being specified across automotive interiors, panel bonding, and modular construction, eliminating mandatory user safety certification while retaining elasticity and long-term durability. In parallel, aerospace-qualified epoxy and polyimide adhesives continue to set the upper boundary of performance, with continuous service capability around 200°C and specialized grades tolerating up to 260°C, supporting composite airframes, propulsion-adjacent structures, and space-grade assemblies.

Thermal functionality and electrification are adding a second structural demand layer. In EV battery packs, power electronics, and high-density semiconductor modules, adhesives are increasingly required to function as thermal management interfaces, not just mechanical bonds. Leading suppliers have commercialized thermally conductive adhesive (TCA) systems delivering approximately 1.4–3.1 W/mK, enabling heat dissipation while maintaining electrical insulation and vibration resistance in multi-cell lithium-ion architectures. At the same time, modified structural epoxies achieving shear strengths around 3,140 psi on metal-to-metal joints have crossed the threshold at which adhesives are engineered as credible substitutes for welding in lightweight automotive and transport structures.

In March 2025, Henkel AG & Co. KGaA announced projected organic sales growth of 2–4% for its Adhesive Technologies division, emphasizing E-Mobility and 5G infrastructure applications. Its strategic investments in battery safety adhesives, conductive materials, and high-thermal stability systems reinforce Henkel’s leadership in energy-efficient transportation and next-gen electronics.

By Q1 2025, H.B. Fuller expanded its Specialty Transportation Adhesives division, launching new formulations for commercial vehicles, rail, and aviation, integrating acoustic and thermal control properties. These customized adhesives improve manufacturing automation and noise damping — two critical parameters for smart mobility design.

In Q4 2024–Early 2025, Sika AG extended its Purform® technology across its polyurethane glass adhesives portfolio (Sikaflex®, SikaTack®), meeting new EHS and REACH standards by reducing monomeric diisocyanate levels below 0.1%, eliminating special safety training while enhancing end-user protection.

In September 2025, an academic collaboration unveiled Dq622JD-136, an aerospace-grade epoxy adhesive achieving superior mode-II fracture toughness and exceptional elastic modulus on aluminum substrates, marking a major leap in Thermal Protection Systems (TPS) for spacecraft and high-temperature aircraft bonding.

By mid-2025, Henkel further expanded its Global E-Mobility Center, investing in R&D for battery recycling, fire-retardant adhesives, and thermal gap fillers. This center also focuses on adhesive-enabled lightweight structures, enabling manufacturers to reduce battery weight while maintaining structural safety.

Throughout 2025, the market also saw a rising trend in bio-based raw material integration, particularly renewable polyols used in polyurethane adhesives to reduce the carbon footprint. Major adhesive producers began issuing Life Cycle Assessment (LCA) transparency reports, ensuring traceable ESG compliance.

Additionally, a shift toward digital manufacturing and AI-driven formulation design accelerated in 2025. Adhesive producers are deploying machine learning tools to simulate bond strength, aging behavior, and curing performance — cutting R&D cycles by 20–30%.

By late 2024, the demand for waterborne high-performance adhesives surged due to VOC legislation tightening across the U.S. and Europe. The transition has been particularly evident in durable goods, insulation, and flooring adhesives, where traditional solvent-based systems are being phased out.

One of the most transformative developments in the high-performance adhesives market is the emergence of thermally conductive yet electrically insulating adhesives designed for SiC- and GaN-based power electronics in electric vehicles, renewable energy systems, and high-power computing. As wide-bandgap semiconductors become standard in EV inverters and on-board chargers, traditional bonding and gap-filling materials are reaching their performance limits—especially in heat dissipation and insulation reliability.

To address the challenge, manufacturers are introducing silicone and epoxy-based thermally conductive gap fillers that combine superior dielectric strength with high thermal conductivity values—reaching up to 3.5 W/m·K. These formulations effectively manage localized heat flux while preventing dielectric breakdowns, ensuring long-term reliability in EV battery packs and power modules operating at high voltages.

A significant leap in high-temperature compatibility has also been achieved. Traditional conductive adhesives degrade near 200°C, limiting SiC’s full potential. In contrast, new die-attach polymer systems have been validated to operate reliably above 200°C, enabling advanced double-side cooled power modules capable of supporting higher switching frequencies and greater power density.

At the research frontier, scientists are developing polycarbosilane-derived bonding materials, which, upon thermal treatment, convert into ceramic-like structures with low coefficients of thermal expansion (CTE). The innovation directly mitigates thermal fatigue between dissimilar materials such as copper and aluminum, which differ significantly in CTE (~17 ppm/°C vs 23 ppm/°C). These material breakthroughs are redefining the standards for adhesive reliability, electrical insulation, and thermal management in next-generation EV and power electronics manufacturing.

The drive toward miniaturized electronics and high-speed automated manufacturing is fueling a rapid transition to low-temperature and ultrafast-curing adhesive technologies that enhance process efficiency without compromising component integrity. The trend is particularly strong in semiconductor packaging, MEMS sensors, and advanced optoelectronic assemblies, where adhesives must provide high bonding strength while minimizing thermal exposure.

Innovations in UV-curable epoxy systems are transforming the assembly landscape. Advanced formulations can achieve full polymerization within seconds under LED-UV light, drastically reducing cycle times and enabling precision placement of micro-scale components. In semiconductor manufacturing, where throughput is paramount, the represents a competitive advantage by boosting productivity and yield without requiring high-heat oven curing.

To accommodate delicate components, such as micro-electromechanical systems (MEMS), sensors, and optoelectronic devices, next-generation dual-cure adhesives are being adopted. These systems combine UV-curing for rapid surface fixation with secondary thermal or moisture cure mechanisms to ensure full cross-linking even in shadowed regions. By maintaining process temperatures below 80°C, they prevent thermal damage to sensitive components while ensuring mechanical robustness.

As manufacturing scales toward greater automation, the integration of fast-curing, precision-controlled adhesive systems is becoming critical. The not only shortens production cycles but also enhances product quality, making low-temperature, rapid-cure adhesives an essential enabler for advanced electronics, automotive sensors, and high-speed industrial assembly lines.

The next evolution in semiconductor packaging—Heterogeneous Integration (HI) and Chiplet-Based Architectures—is revolutionizing the demand profile for high-performance adhesives. As the industry surpasses the physical scaling limits of Moore’s Law, packaging innovation has become central to maintaining performance growth in AI, 5G, and high-performance computing (HPC).

Modern chip packages integrate multiple functional dies (logic, memory, I/O) within a single structure, relying heavily on non-conductive adhesives, underfills, and die-attach films to manage thermal and mechanical stresses. These adhesives must maintain dimensional stability, low CTE, and high modulus strength to support fine-pitch interconnections in 2.5D and 3D stacking architectures.

Leading semiconductor assembly companies report that advanced underfill and die-attach materials have cut design cycle times by nearly 50% (e.g., from 90 days to 45 days) in Fan-Out Chip-on-Substrate (FOCoS) manufacturing. The acceleration is achieved through superior gap-filling and flow properties that accommodate ultra-thin die and narrow bondline control, enabling more compact, thermally optimized designs.

The rise of AI accelerators and HPC processors—which can generate intense localized heat—further heightens the demand for adhesives with high modulus (2–4 GPa) and extremely low moisture absorption. The performance profile is critical for preventing warpage, delamination, and reliability loss under repeated thermal cycling. As Heterogeneous Integration becomes the cornerstone of semiconductor advancement, adhesive innovation is emerging as a strategic bottleneck and high-margin growth frontier in advanced electronics packaging.

The global race to commercialize Solid-State Batteries (SSBs)—touted as the future of electric mobility—is generating a surge in demand for specialized high-performance adhesives that can ensure hermetic sealing, structural integrity, and interfacial stability within solid electrolyte systems. As automotive OEMs and battery manufacturers ramp up gigafactory investments, adhesives are playing a pivotal role in enabling scalable, defect-free SSB assembly.

Recent research breakthroughs have focused on iodine ion-based adhesive materials that enhance interfacial contact between solid electrolytes and electrodes, minimizing internal resistance and improving cycle life. These “ionic bonding adhesives” are engineered for electrochemical stability and adhesion to ceramic and polymer electrolyte layers, demonstrating the growing role of adhesive chemistry in electrochemical performance optimization.

In mass manufacturing, specialized adhesives are being used in cell encapsulation, lamination, and protective coating processes to ensure long-term safety and mechanical durability. Production facilities are increasingly integrating laser-assisted surface activation before adhesive deposition to achieve perfect wetting and adhesion uniformity, vital for the long lifespan of SSB modules.

The emerging segment offers vast commercial potential as EV manufacturers demand lightweight, flame-retardant, and thermally stable adhesives compatible with solid electrolytes. Adhesive technologies capable of surviving high voltages, wide thermal ranges, and extreme vibration conditions are poised to become indispensable to the next generation of electric vehicles, grid storage systems, and aerospace-grade energy modules.

High Performance Adhesives Market Share Insights, 2025-2034

Reactive systems (1K/2K epoxies and polyurethanes) lead with a projected 32.6% share in 2025, reflecting their role as the structural backbone in automotive, aerospace, and construction where load-bearing strength, thermal/chemical resistance, and long-term durability are non-negotiable. Radiation-cured (UV/LED) adhesives are the fastest risers as electronics, medical devices, and precision assembly favor on-demand curing, tight takt times, and minimal thermal stress, improving throughput and first-pass yield. Hot-melt technologies—including reactive PUR HMAs—expand with lines that need instant green strength plus high final strength, bridging the gap between speed and structural performance for appliances, furniture, and e-mobility modules. Water-borne and advanced PSAs sustain significant shares where low VOCs, compliance, and flexible bonding dominate (panels, laminates, protective films), while solvent-borne chemistries recede into niche, legacy applications that demand specific wetting kinetics or extreme environments.

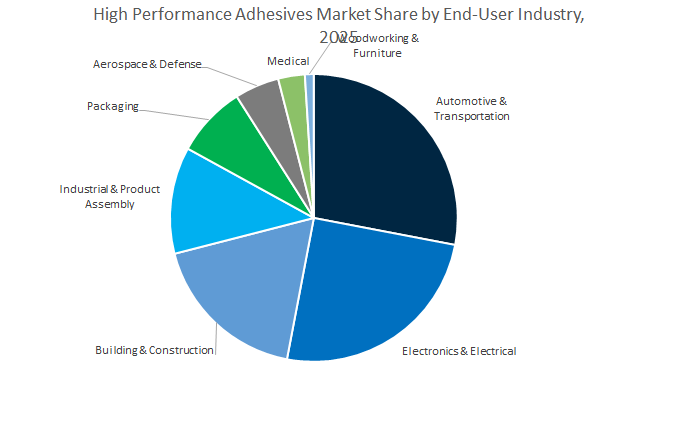

Automotive & transportation tops the market with a projected 28.9% share in 2025, underpinned by EV battery pack assembly, body-in-white reinforcement, NVH damping, and glazing—all of which trade welds/rivets for multi-material bonding to cut weight and enhance crash energy management. Electronics & electrical follows with robust growth: semiconductor packaging, camera modules, displays, and 5G infrastructure require die attach, underfills, and optically clear bonds that cure fast and survive heat/humidity cycles. Building & construction maintains a large, steady base—structural glazing, façades, composite panels, and high-performance flooring—where adhesives enable air/water tightness and long design lives. Industrial & product assembly and packaging provide substantial volumes focused on cycle time, automated dispensing, and adhesion to low-energy plastics. Aerospace & defense, medical, and woodworking remain specialized but high-value segments demanding certified, extreme-performance bonding (flame/smoke/tox, bio-compatibility, fatigue resistance).

The global high-performance adhesives ecosystem is anchored by Henkel AG & Co. KGaA, Sika AG, H.B. Fuller, 3M Company, and Arkema (Bostik) — each leveraging technological differentiation, sustainability initiatives, and global production scale.

Henkel’s Adhesive Technologies unit generated €10.97 billion in 2024, solidifying its global dominance in industrial bonding and structural adhesives. Its Mobility & Electronics segment leads innovations in EV battery, powertrain, and semiconductor bonding. Henkel’s LOCTITE® and BONDERITE® brands deliver UV-curing acrylics and heat-curing epoxies with proven reliability under extreme conditions. The company’s 61 R&D labs across 30 countries enable localized formulation adaptation for OEMs.

Sika AG remains the global authority in polyurethane and epoxy adhesives, notably through Sikaflex®, SikaPower®, and Sikadur® product lines. Its Purform® polyurethane platform achieves <0.1% monomer content, pre-empting future EHS regulations. The Sika SmartCore® technology enhances epoxy toughness for crash-resistant bonding in automotive and industrial structures. Sika’s adhesives also support composite reinforcement and façade structural glazing in construction.

H.B. Fuller is a pioneer in Engineering Adhesives (EA) for durable goods, vehicles, and electronics. Its portfolio spans PUR, epoxy, and cyanoacrylate systems, including Weld Mount™ fastening adhesives and powertrain flange sealants used in over 5 million engines annually. The company’s ongoing R&D investments target bio-based and low-monomer chemistries, supporting global sustainability mandates while maintaining high mechanical integrity under heat and vibration.

3M Company continues to dominate through its VHB™ Tapes and Scotch-Weld™ epoxy adhesive series, known for aerospace-grade reliability. It is also a leader in thermal management materials, integrating adhesives, films, and thermal interface solutions into one cohesive bonding system. 3M’s expertise in surface energy optimization enables superior adhesion to LSE plastics and composites, making it a key supplier for electronics and lightweight automotive components.

Arkema’s Bostik division specializes in polyamide, polyester, and methyl methacrylate (MMA) adhesives, delivering fast-curing, high-strength structural solutions. Its low-VOC and solvent-free adhesives cater to construction, packaging, and high-performance assembly markets. Arkema’s innovation pipeline focuses on one-component reactive systems and automated production efficiency. Bostik’s MVR™ adhesives are key to demanding flooring and high-durability construction projects.

The United States remains a powerhouse in the high-performance adhesives market, driven by its dominance in aerospace, electric vehicles, renewable energy infrastructure, and advanced manufacturing. The country is prioritizing R&D for next-generation structural adhesives, self-healing polymers, and battery thermal interface materials (TIMs)—key components in achieving lightweighting and safety compliance for EVs and defense-grade applications.

Leading U.S. chemical manufacturers are driving large-scale expansions and product launches to serve high-demand verticals. Dow Inc., for instance, expanded its VORATRON™ adhesive and gap filler production line to meet surging EV battery assembly demand across North America. Similarly, Sika AG’s Powerflex™ technology blends flexibility with high structural integrity, making it ideal for composite vehicle bodies and high-load applications in EV manufacturing.

Innovation is also shifting toward adaptive and self-healing polyurethane adhesives, pioneered by companies like 3M and H.B. Fuller, designed to withstand fatigue and improve the long-term reliability of components in electric drivetrains. Henkel Corporation’s $30 million expansion in South Dakota enhances the company’s North American supply of advanced thermal management adhesives and electronic encapsulants, catering to EV and semiconductor industries.

The market’s evolution aligns with sustainability and VOC reduction trends, with firms like Ashland Inc. emphasizing durable, eco-efficient products such as Pliogrip™ structural adhesives. The U.S. focus on EV supply chain independence, aerospace innovation, and advanced MRO applications is expected to consolidate its leadership in the global high-performance adhesives landscape.

China is aggressively scaling up its high-performance adhesives production to support domestic semiconductor, electronics, and EV industries, propelled by government-backed initiatives under the Made in China 2025 strategy. The nation’s emphasis on electronic-grade conductive adhesives, thermal interface materials, and polyurethane structural bonding agents reflects its ambition to achieve supply chain autonomy.

The rapid deployment of 5G technology, smart devices, and New Energy Vehicles (NEVs) has accelerated demand for electrically conductive adhesives (ECAs) and high-purity epoxy systems for flexible PCBs, optical components, and high-speed data modules. Local manufacturers, such as Hubei Huitian New Materials Co., Ltd., are emerging as key players in supplying polyurethane and silicone-based adhesives for automotive and infrastructure applications.

To reduce dependency on imports, China is localizing the production of advanced polymer systems and specialty resins for structural adhesives used in automotive bonding, aerospace composites, and lithium battery assembly. The government’s dual circulation policy and environmental protection laws are further driving the shift toward low-VOC, solvent-free adhesive systems.

China’s combined focus on sustainability, high-volume manufacturing, and advanced materials R&D positions it as the largest consumer and one of the fastest-growing producers of high-performance adhesives globally.

Germany continues to dominate the European high-performance adhesives industry, setting global benchmarks for regulatory compliance, polyurethane innovation, and structural bonding excellence. The country’s automotive and construction sectors remain primary growth drivers, demanding superior performance adhesives that meet stringent REACH and EU sustainability mandates.

Sika AG leads the market with its Purform™ Technology, a next-generation polyurethane adhesive platform designed with ultra-low monomeric diisocyanate content, ensuring compliance with evolving health and safety standards. The innovation aligns with Europe’s push for low-emission, high-durability adhesives across automotive and industrial segments.

Henkel AG & Co. KGaA continues to advance TECHNOMELT® SUPRA hot melt adhesives, enhancing processing efficiency and environmental performance in automated packaging lines. Meanwhile, Dow Inc.’s renewable energy-powered facility in Ahlen underlines the country’s commitment to sustainable, high-performance production for global adhesive demand.

Jowat SE’s Jowapur® line of polyurethane hot-melt adhesives caters to specialized industries such as woodworking, textiles, and high-precision furniture manufacturing, reinforcing Germany’s leadership in technical material formulation. The nation’s emphasis on environmentally responsible innovation, advanced polymer engineering, and precision manufacturing keeps it at the forefront of the European adhesives ecosystem.

Japan is a global frontrunner in ultra-high-purity adhesives tailored for semiconductor, microelectronics, and precision assembly applications. The government’s heavy investment in the Rapidus consortium, supporting the production of 2 nm semiconductor nodes, is driving an ecosystem-wide demand for high-performance temporary bonding and die-attach adhesives.

Nissan Chemical Corporation and Tokyo Electron (TEL) are leading R&D for temporary bonding adhesives that secure wafers during chemical mechanical polishing (CMP) and multi-layer stacking—critical processes for next-generation 3D integrated chip packaging. The collaboration between TEL and local technology partners is advancing the world’s first 300 mm wafer stacking operations, requiring precision adhesives with low dielectric constants and high heat resistance.

Shin-Etsu Chemical and Sumitomo Chemical contribute to the supply of photoresist and encapsulant materials, essential for high-resolution lithography and chip-level packaging. With Japan’s emphasis on semiconductor sovereignty, nanotechnology integration, and materials science excellence, the country remains indispensable in the global high-performance adhesives supply chain—particularly for electronics miniaturization and advanced chip packaging.

South Korea’s high-performance adhesives industry is deeply integrated into its EV battery manufacturing and semiconductor ecosystem. The nation’s major conglomerates, including SK Inc. and LG Chem, are leading large-scale investments in high-purity materials and specialty chemical production, vital for adhesive formulation and electronic encapsulation.

SKC Co., Ltd., a subsidiary of SK Inc., supplies precision-engineered semiconductor chemicals and base materials for high-performance adhesive applications in chip packaging and cleanroom assembly. Simultaneously, domestic EV battery producers are scaling the use of thermally conductive adhesives and structural gap fillers to enhance module integrity and fire resistance in lithium-ion battery packs.

The consumer electronics segment—particularly smartphones, displays, and wearables—continues to rely on UV-curable and cyanoacrylate adhesives that ensure rapid curing and minimal VOC emissions. With the government’s support for carbon neutrality and advanced materials R&D, South Korea is emerging as a regional innovation hub for high-strength, heat-resistant, and conductive adhesives used across next-generation technologies.

India’s high-performance adhesives market is entering a major expansion phase, driven by rapid industrialization, semiconductor policy incentives, and domestic infrastructure development. The Semicon India Programme (SIP), launched by the Ministry of Electronics and Information Technology (MeitY), is stimulating the local ecosystem for die-attach, encapsulation, and circuit assembly adhesives required in domestic electronics manufacturing.

Global adhesive producers, including Henkel and H.B. Fuller, are increasing supply partnerships with Indian manufacturers, while Pidilite Industries Ltd. expands its portfolio to include moisture-resistant polyurethane adhesives for infrastructure, construction, and automotive segments. The rise of local smartphone and telecom equipment production, combined with India’s PLI scheme, is catalyzing adoption of high-performance structural adhesives and electronic encapsulants.

India’s dual demand—from infrastructure adhesives for large-scale projects and specialty adhesives for electronic assembly—positions it as a key emerging market. Government-backed import substitution policies and quality standardization (BIS certification) are fostering the growth of a self-reliant, high-performance adhesive manufacturing ecosystem across the subcontinent.

France is establishing itself as a European leader in sustainable and high-performance adhesive innovation, with a strong industrial base in aerospace, packaging, and advanced materials engineering. French chemical giants are focusing on bio-based and recyclable adhesive chemistries, aligned with EU Green Deal objectives.

Significant R&D efforts are dedicated to developing lightweight, temperature-resistant adhesives for aerospace composites and specialty packaging. France’s industrial collaboration between Safran, Arkema, and Airbus suppliers is driving innovation in epoxy and polyurethane systems that meet fire, smoke, and toxicity (FST) standards for aircraft interiors.

The nation’s chemical sector is equally focused on recyclable adhesives compatible with circular economy frameworks, serving both aerospace and consumer packaging industries. With its high emphasis on sustainability, innovation funding, and advanced materials research, France is consolidating its position as a key European hub for high-performance, eco-efficient adhesives.

High Performance Adhesives Market Report Scope

High Performance Adhesives Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$51.4 Billion

|

|

Market Size (2034)

|

$74.4 Billion

|

|

Market Growth Rate

|

4.2%

|

|

Segments

|

By Chemistry (Epoxy, Polyurethane, Acrylic, Cyanoacrylate, Silicone, Vinyl Acetate Ethylene, Polyamide, Others), By Technology (Water-Borne, Solvent-Borne, Hot Melt, Reactive, Radiation-Cured, Pressure-Sensitive Adhesives), By End-User Industry (Automotive & Transportation, Electronics & Electrical, Building & Construction, Packaging, Aerospace & Defense, Medical, Industrial & Product Assembly, Woodworking & Furniture), By Application (Structural Bonding, Non-Structural/Elastic Bonding, Sealing & Gasketing, Thermal Management, Encapsulation & Potting, Die Attach, Flexible Film Lamination, Tapes & Labels), By Substrate (Composites, Metals, Plastics, Glass, Wood, Rubber, Ceramic

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Henkel AG & Co. KGaA, 3M Company, H.B. Fuller Company, Sika AG, Arkema S.A., Dow Inc., Huntsman Corporation, Illinois Tool Works Inc., Jowat SE, BASF SE, Ashland Inc., Mapei S.p.A., Avery Dennison Corporation, Master Bond Inc., Pidilite Industries Ltd.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

By Chemistry

- Epoxy

- Polyurethane

- Acrylic

- Cyanoacrylate

- Silicone

- Vinyl Acetate Ethylene

- Polyamide

- Others

By Technology

- Water-Borne

- Solvent-Borne

- Hot Melt

- Reactive

- Radiation-Cured

- Pressure-Sensitive Adhesives

By End-User Industry

- Automotive & Transportation

- Electronics & Electrical

- Building & Construction

- Packaging

- Aerospace & Defense

- Medical

- Industrial & Product Assembly

- Woodworking & Furniture

By Application

- Structural Bonding

- Non-Structural/Elastic Bonding

- Sealing & Gasketing

- Thermal Management

- Encapsulation & Potting

- Die Attach

- Flexible Film Lamination

- Tapes & Labels

By Substrate

- Composites

- Metals

- Plastics

- Glass

- Wood

- Rubber

- Ceramic

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

- Henkel AG & Co. KGaA

- 3M Company

- H.B. Fuller Company

- Sika AG

- Arkema S.A.

- Dow Inc.

- Huntsman Corporation

- Illinois Tool Works Inc.

- Jowat SE

- BASF SE

- Ashland Inc.

- Mapei S.p.A.

- Avery Dennison Corporation

- Master Bond Inc.

- Pidilite Industries Ltd.

*- List not Exhaustive

Research Coverage

This High Performance Adhesives study from USDAnalytics delivers decision-grade coverage and technical buyers alike—this report investigates demand shifts from structural bonding to thermally conductive assemblies, tracks breakthroughs in low-monomer PUR and high-temperature epoxies, and consolidates OEM adoption signals across automotive, aerospace, electronics, construction, and specialty packaging. Our editorial analysis reviews product pipelines, compliance pivots (REACH/VOC), and digital formulation advances, and highlights how adhesives are displacing welds/fasteners in lightweight structures while enabling thermal management in EVs and power electronics. Built to support strategy, sourcing, and engineering roadmaps, this report is an essential resource for executives, product managers, application engineers, and procurement teams seeking evidence-backed perspectives on chemistry innovation, processing speed, reliability under heat/vibration, and ESG-aligned materials transitions.

Scope Highlights

Segmentation (as covered in this study):

- By Chemistry: Epoxy; Polyurethane; Acrylic; Cyanoacrylate; Silicone; Vinyl Acetate Ethylene; Polyamide; Others

- By Technology: Water-Borne; Solvent-Borne; Hot Melt; Reactive; Radiation-Cured; Pressure-Sensitive Adhesives

- By End-User Industry: Automotive & Transportation; Electronics & Electrical; Building & Construction; Packaging; Aerospace & Defense; Medical; Industrial & Product Assembly; Woodworking & Furniture

- By Application: Structural Bonding; Non-Structural/Elastic Bonding; Sealing & Gasketing; Thermal Management; Encapsulation & Potting; Die Attach; Flexible Film Lamination; Tapes & Labels

- By Substrate: Composites; Metals; Plastics; Glass; Wood; Rubber; Ceramic

- Geographic Scope: Analysis spans 25+ countries across North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa.

- Time Horizon: Historic data (2021–2024) and forecast outlook (2025–2034) with annual updates.

- Companies: Deep-dive analysis/profiles of 15+ leading players including Henkel, 3M, H.B. Fuller, Sika, Arkema (Bostik), Dow, Huntsman, Illinois Tool Works, Jowat, BASF, Ashland, Mapei, Avery Dennison, Master Bond, and Pidilite (list not exhaustive).

Deliverables

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.