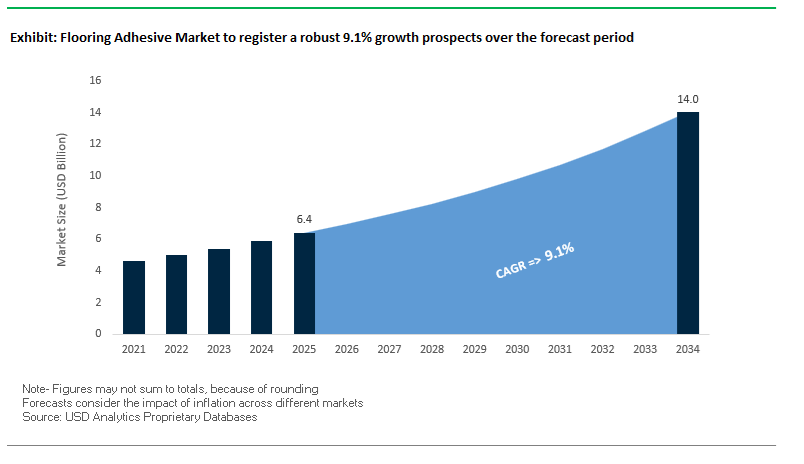

The Global Flooring Adhesive Market is projected to expand from USD 6.4 billion in 2025 to USD 14 billion by 2034, advancing at a CAGR of 9.1%, as flooring installation becomes a time-, emissions-, and risk-sensitive construction activity rather than a finishing trade. Growth is structurally anchored in accelerated urban construction, large-scale renovation cycles, and stricter indoor air quality mandates across commercial, healthcare, hospitality, and residential buildings. Flooring adhesives are specified not only for bond strength, but for moisture tolerance, installation speed, rework flexibility, and regulatory compliance, forcing a clear shift away from legacy solvent-based systems toward pressure-sensitive, silane-modified, and water-based polymer technologies.

From a manufacturer and installer perspective, formulation priorities are being reshaped by real-world site conditions rather than laboratory benchmarks. Leading producers such as Bostik, Mapei, Sika, Henkel, and H.B. Fuller have expanded portfolios of single-application moisture-tolerant adhesives capable of bonding directly to concrete substrates with up to 90% in-situ Relative Humidity (RH)—a critical capability as fast-track projects increasingly bypass extended slab drying schedules. At the same time, the rapid global adoption of Luxury Vinyl Tile (LVT), Luxury Vinyl Plank (LVP), and engineered wood flooring has elevated demand for pressure-sensitive adhesives (PSAs) that offer strong initial tack combined with repositionability. Premium PSA systems deliver working times of up to six hours, allowing large-format commercial installations to proceed without adhesive skinning or bond inconsistency, directly improving labor productivity and reducing installation errors.

Silane-modified polymer (SMP) flooring adhesives are increasingly replacing traditional polyurethane systems. SMP adhesives deliver low-VOC profiles, elastic bonding behavior, and moisture tolerance without isocyanates, aligning with LEED and BREEAM requirements while maintaining performance across wood, vinyl, rubber, and mixed substrates. In parallel, manufacturers are integrating rapid-curing subfloor leveling compounds and fast-track adhesive systems that enable full flooring installation and return-to-service in as little as 4–6 hours, a capability routinely specified in hospitals, retail refurbishments, and transport infrastructure.

The flooring adhesives industry is experiencing a series of strategic movements encompassing acquisitions, product innovations, regulatory reforms, and sustainability-led transformations that redefine competitive priorities.

In March 2024, Bostik (Arkema Group) announced the acquisition of Arc Building Products, expanding its product range and geographic reach within Oceania’s construction adhesives market. This acquisition strengthens Bostik’s position in resilient and textile flooring adhesives, while diversifying its portfolio across solvent-free acrylics and pressure-sensitive adhesives (PSA) used in LVT applications. The move aligns with Bostik’s long-term strategy to enhance its global sustainable construction footprint through innovative, low-emission technologies.

In December 2024, H.B. Fuller Company completed the divestiture of its Flooring business to Pacific Avenue Capital Partners for USD 80 million, a strategic step toward focusing on high-margin specialty adhesive applications in industrial assembly, infrastructure, and building envelope solutions. This divestment reflects the broader trend among global chemical players to streamline portfolios and concentrate on performance-driven adhesive technologies with long-term profitability potential.

By Q1 2025, MAPEI Corporation unveiled an integrated Luxury Vinyl Tile (LVT) installation system for wet environments, combining waterproofing, sound-reduction, and resilient adhesive technologies tailored for hospitals, commercial kitchens, and high-humidity facilities. The product demonstrates the growing integration between flooring adhesives and system-based solutions, ensuring performance consistency and compliance under moisture-prone conditions.

In Q2 2025, Sika AG introduced its next-generation wood floor bonding adhesives featuring ultra-low monomer content, building upon its Purform® technology platform. This innovation directly addresses European REACH regulations, promoting worker safety and sustainable adhesive chemistry without compromising strength or flexibility. Meanwhile, ARDEX Group demonstrated the industry’s rapid-cure leadership through its RAPIDRY FORMULA, successfully applied in a major commercial flooring project (Q3 2025) that achieved subfloor readiness in under 24 hours — a benchmark for fast-track construction practices.

Additionally, BASF SE expanded its ACRONAL binder range for low-VOC water-based adhesives, optimizing shear and peel resistance in carpet and resilient flooring applications, while maintaining environmental compliance. In parallel, an Asia-Pacific manufacturer initiated a flooring adhesive plant expansion in China (Q4 2024), targeting the booming regional infrastructure and residential sectors with high-demand water-based and hot-melt adhesives.

From a regulatory standpoint, North America’s early 2025 VOC directives have accelerated the industry-wide migration toward SMP and water-based formulations, positioning these chemistries as the preferred standard in LEED and Green Building-certified projects. Furthermore, digital integration has gained momentum, as seen in Q2 2025, when a major industrial chemicals firm partnered with a construction tech startup to develop digital adhesive tracking and moisture-testing systems, improving installation validation in large-scale commercial flooring projects.

Lastly, Avery Dennison (Mid-2025) launched high-shear PSA film technology designed for factory-applied adhesives on premium LVT and LVP surfaces, marking a significant advancement in modular flooring installation efficiency.

Regulatory Transformation, Moisture-Resilient Chemistry & Smart-Building Integration

Trend 1: Regulatory-Driven Elimination of Hazardous Additives Reshaping Flooring Adhesive Formulations

Global chemical regulations—particularly the EU REACH Annex XIV restrictions—are accelerating the removal of hazardous plasticizers such as DEHP, DBP, DIBP, and BBP from flooring adhesive formulations. Since these phthalates have been largely banned in Europe since 2015, adhesive manufacturers have had to reformulate products using safer alternatives such as terephthalates, citrates, and polymeric plasticizers, especially for PVC and vinyl flooring. However, studies show that recycled PVC flooring often contains legacy contaminants exceeding the legal limit of 0.1 wt%, creating pressure on adhesive suppliers to guarantee contamination-free formulations to protect circular economy streams. Parallel to these regulatory mandates, the broader flooring industry’s successful phase-out of cadmium and lead stabilizers by 2015 sets a precedent for adhesive manufacturers to voluntarily eliminate all hazardous components to maintain compliance, worker safety, and long-term environmental integrity.

Trend 2: Demand Surge for Low-VOC, Moisture-Tolerant Adhesives for LVT, LVP & Large-Format Tile Installations

The growth of Luxury Vinyl Tile (LVT), rigid-core flooring, and large-format ceramics is driving innovation in low-VOC, moisture-resistant adhesive technologies capable of addressing chronic challenges such as high slab moisture and fast-paced commercial construction timelines. Next-generation polyurethane and silane-modified polymers allow installations on concrete with moisture levels as high as 99% RH, reducing or eliminating the need for costly moisture mitigation systems. Fast-curing, ready-to-use adhesives approved for concrete as young as 28 days enable immediate foot traffic, dramatically shortening project schedules. Meanwhile, “all-in-one” silane-based adhesives—offering built-in moisture control and acoustic damping—allow installers to replace multi-layer systems with a single adhesive step, improving efficiency and ensuring superior performance in modern high-volume construction settings.

Opportunities Aligned With Circularity & Smart Infrastructure

Opportunity 1: Adhesive Technologies Enabling Circular Flooring Systems and Reversible Installation

The construction industry’s shift toward circularity is generating strong demand for reversible and debondable adhesive systems that support flooring recovery, reuse, and recycling, rather than demolition. Breakthrough “Debonding-on-Demand” technologies—activated by controlled triggers such as heat or electrical current—allow tiles and modular flooring to be removed intact for reuse, significantly reducing lifecycle emissions associated with new ceramic production. Economic modeling shows adhesive-free reversible fixing systems can reduce lifetime installation costs by up to 40%, due to simplified subfloor preparation, cleaner removal, and the ability to reuse flooring multiple times. As green building certifications and circular construction policies expand, flooring adhesives that support disassembly rather than destruction will become a mainstream requirement.

Opportunity 2: Growth of Electrically Conductive & Static-Dissipative Adhesives for Smart Buildings and ESD Environments

The rise of data centers, semiconductor production, hospitals, and precision manufacturing is creating a high-value market for conductive and static-dissipative flooring adhesives. These adhesives form a critical part of Electrostatic Discharge (ESD) flooring systems designed to protect sensitive electronics, which can be damaged by static charges as low as 250 volts—far below the threshold humans can perceive. Advanced formulations enhanced with conductive fillers such as carbon fibers, exemplified by products like Bostik STIX A970 ELECTRO, ensure reliable grounding paths and consistent conductivity across large commercial spaces. As smart buildings integrate more electronics, sensors, and autonomous systems, demand for these specialized adhesives will escalate, positioning ESD-compatible solutions as a strategic growth segment within the flooring adhesives market.

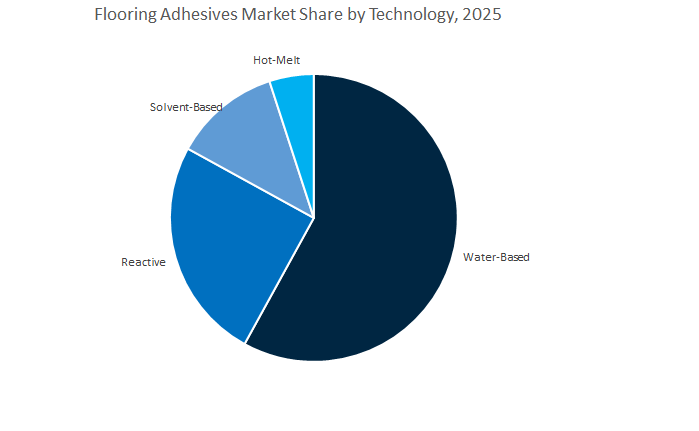

Flooring Adhesive Market Share Insights, 2025-2034

Water-based floor adhesives command approximately 58% of the global market share, reflecting the rapid transition toward environmentally compliant, low-VOC adhesive systems across the flooring industry. Their dominance stems from the growing emphasis on sustainable building materials, as architects and contractors seek formulations that align with LEED certification and regional air-quality regulations. These adhesives provide robust bonding strength across a wide range of substrates, including wood, vinyl, and tile, while simplifying cleanup and reducing odor emissions during installation. The increasing construction of green commercial buildings and eco-labeled residential projects—particularly in North America and Europe—continues to anchor demand. Furthermore, advancements in polymer chemistry have significantly enhanced their shear strength, moisture resistance, and curing characteristics, allowing water-based technologies to replace solvent-based alternatives in most standard flooring applications. Their adaptability in both residential renovations and large commercial installations ensures sustained share retention in 2025 and beyond, positioning water-based adhesives as the industry’s cornerstone technology.

Reactive floor adhesives are witnessing accelerated adoption within industrial, commercial, and moisture-sensitive environments, where long-term durability and chemical resistance are critical. These systems—primarily polyurethane and epoxy-based formulations—provide superior adhesion to dense substrates and perform exceptionally under thermal stress and high traffic. Their expanding use in healthcare, airports, logistics facilities, and sports arenas reflects an industry preference for permanent bonding strength and dimensional stability in challenging conditions. Reactive adhesives also align with the construction sector’s shift toward moisture-tolerant and flexible flooring systems, as their cross-linking chemistries ensure enhanced performance on concrete subfloors and underfloor heating systems. Manufacturers are investing in low-isocyanate and rapid-curing variants to address evolving regulatory and operational demands, enhancing productivity for professional installers.

The global flooring adhesives market is shifting toward water-based and reactive systems but solvent-based adhesives maintain a modest but stable share in certain high-performance and specialty applications. Their fast-setting nature and superior wet-bond properties make them suitable for substrates requiring immediate adhesion or installations in cold environments where water-based systems may underperform. However, tightening VOC regulations and health concerns are steadily constraining growth in this category, pushing manufacturers toward reformulation or phase-out strategies.

The global flooring adhesive industry is highly consolidated among chemical giants and construction solution providers leveraging hybrid chemistries, sustainability-driven R&D, and system-based offerings. Competitive strength depends on the ability to balance technical performance with environmental compliance and application efficiency.

Sika AG remains a frontrunner in polyurethane and silane-modified polymer (SMP) flooring adhesives, renowned for its SikaBond® wood adhesive range and Sikafloor® subfloor systems. The company’s innovation is anchored in elastic floor bonding technology, allowing compensation for wood movement and vibration reduction in modern flooring assemblies. With a focus on low-VOC formulations and regulatory-ready chemistry, Sika’s R&D investments are directed toward next-generation sustainable adhesives. Its integrated system—from primers to finishing varnishes—offers unmatched performance for modular and sustainable construction projects.

MAPEI continues to lead with a comprehensive flooring installation portfolio, particularly in moisture control, self-leveling, and resilient flooring adhesives. The company invests 5% of annual revenue in R&D, with the majority focused on eco-sustainable and fast-drying solutions. Products like Ultraplan HFL (High Flow Leveler) and 3-in-1 wood adhesives combine moisture control, sound insulation, and strong bonding in a single application, catering to high-performance commercial and luxury residential flooring projects.

Bostik is a recognized leader in solvent-free acrylic and pressure-sensitive adhesive (PSA) technologies for resilient and textile flooring. Its STIX A600 EVOLUTION exemplifies next-generation low-VOC performance, offering superior bonding for high-traffic LVT installations. Following the Arc Building Products acquisition (March 2024), Bostik has enhanced its presence in Asia-Pacific and Oceania, consolidating its leadership in sustainable flooring adhesives. The company continues to invest in Green Label Plus-certified systems, driving innovation across LVT, carpet tile, and textile flooring applications.

ARDEX Group dominates the fast-track construction space through its proprietary RAPIDRY FORMULA®, which enables subfloor installations to receive coverings within 4 to 24 hours. Its ARDEX AF adhesives and HENRY brand products are widely specified in airports, healthcare facilities, and high-traffic environments. The company’s system-based approach offers warrantied compatibility across self-leveling compounds and adhesives, ensuring consistency and reduced installation risk.

Following its December 2024 divestiture of the general flooring business, H.B. Fuller has concentrated on Building Adhesive Solutions (BAS GBU), targeting high-performance construction and infrastructure applications. The company continues to develop specialty adhesive chemistries with strong resistance to environmental and thermal stress, supporting critical applications across energy, utilities, and commercial structures. Its pivot away from commodity flooring adhesives strengthens its position in high-value, custom-engineered bonding solutions.

The United States floor adhesives market is rapidly evolving, driven by surging demand for resilient flooring, LVT/LVP installations, and green building initiatives that favor low-VOC, water-based, and moisture-mitigating adhesive systems. In August 2025, Avery Dennison Corporation announced the acquisition of the U.S. flooring adhesives business of Meridian Adhesives Group, including Taylor Adhesives, marking a major step toward vertical integration and diversification into high-performance and solvent-free adhesive manufacturing. The acquisition allows Avery Dennison to leverage its advanced materials science expertise to strengthen its position in construction and industrial adhesive solutions.

Companies such as Sika, Custom Building Products, and TotalWorx launched new acrylic and pressure-sensitive floor adhesives in mid-2025 that can withstand up to 99% relative humidity (RH) and high Moisture Vapor Emission Rates (MVER) — addressing performance requirements in commercial and institutional flooring. Meanwhile, Tarkett North America’s Johnsonite brand has renewed focus on U.S.-made low-VOC flooring adhesives, certified under Cradle to Cradle and other IAQ-compliant frameworks, underscoring domestic sustainability leadership.

Federal funding under the Biden Administration’s Infrastructure Plan, especially targeting education, healthcare, and transport facilities, continues to elevate market growth for durable and high-bond floor adhesives. The trends highlight the U.S. as a center for technological advancement and environmental compliance, shaping the future of moisture-resistant and sustainable resilient flooring adhesives in commercial and industrial applications.

China’s floor adhesives market is expanding on the back of urban renewal programs, green building standards, and prefabrication initiatives, positioning the country as the largest consumer and producer of eco-friendly construction adhesives. In 2024, the government allocated approximately CNY 2.9 trillion for 60,000+ urban renewal projects, boosting demand for flooring adhesives across residential, commercial, and public infrastructure developments.

The implementation of the GB 18584-2024 standard (effective July 2025) sets strict VOC emission caps for interior decoration materials, compelling local manufacturers to develop water-borne, low-odor adhesive systems that comply with next-generation air quality regulations. The GB 18584 update complements China’s 14th Five-Year Plan, which prioritizes cleaner production and industrial sustainability.

The rapid adoption of prefabricated construction methods, projected to account for 30% of all new buildings by 2025, further propels demand for fast-curing polyurethane and epoxy-based adhesives used in floor panels, modular interiors, and composite substrates. Moreover, water-borne adhesives already hold ~40% market share, underscoring the nation’s decisive move toward low-emission, high-performance flooring adhesive technologies. China’s dual focus on industrial expansion and ecological compliance makes it a pivotal global hub for sustainable adhesive manufacturing and export-driven innovation.

Germany remains the European nucleus for high-performance polyurethane (PU) and epoxy flooring adhesives, driven by industrial flooring innovation, environmental regulation, and a sophisticated R&D infrastructure. As part of Europe’s transition toward climate-neutral construction, German manufacturers are leading advancements in self-healing, flexible, and bio-based flooring materials that extend lifecycle durability in commercial and industrial environments.

The domestic demand for PU and epoxy adhesives is growing within high-traffic sectors such as data centers, hospitals, and logistics facilities, where chemical resistance, elasticity, and temperature tolerance are essential. Companies like Henkel AG & Co. KGaA are advancing formaldehyde-free, bio-based adhesive technologies, aligning with EU Green Deal directives and future Construction Products Regulation (CPR) updates.

Furthermore, Henkel and other major European players are increasing transparency through Environmental Product Declarations (EPDs) across their Ceresit and Loctite product lines, ensuring compliance with EU ecolabel certifications. The focus on sustainable manufacturing and regulatory transparency reinforces Germany’s leadership in environmentally responsible, high-durability adhesive systems. The integration of digital process control and smart R&D centers positions Germany as a driving force behind the next generation of high-performance, low-emission floor adhesives in Europe.

Japan’s floor adhesives industry is defined by resilient construction, urban redevelopment, and technological innovation, particularly ahead of the 2025 World Expo in Osaka. The Japanese government’s public infrastructure modernization projects continue to drive demand for high-strength and vibration-tolerant adhesives designed for earthquake-resistant flooring and structural bonding applications.

Local manufacturers are emphasizing high-durability and weather-resistant adhesive systems capable of maintaining performance under seismic stress. The solutions are increasingly applied in public buildings, airports, and high-density residential complexes, supporting the country’s national Green Growth Strategy. The strong presence of wood-based housing further sustains domestic demand for advanced wood adhesives used in residential flooring and renovation projects.

Moreover, Japan’s R&D investments are heavily directed toward low-VOC and bio-based adhesive solutions that complement its sustainability goals and energy-efficient building designs. As a result, manufacturers are focusing on hybrid technologies that merge polyurethane flexibility with epoxy strength, delivering adhesives that meet both structural performance and environmental certification requirements. Supported by policy reforms and export-oriented innovation, Japan is solidifying its position as a leader in eco-smart, high-performance flooring adhesive solutions across Asia-Pacific.

Flooring Adhesive Market Report Scope

Flooring Adhesive Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$6.4 Billion

|

|

Market Size (2034)

|

$14 Billion

|

|

Market Growth Rate

|

9.1%

|

|

Segments

|

By Resin Type (Acrylic Adhesives, Polyurethane Adhesives, Epoxy Adhesives, Vinyl Adhesives, Cementitious Adhesives, Others), By Technology (Water-Based, Solvent-Based, Reactive, Hot-Melt), By Application (Resilient Flooring Adhesives, Wood Flooring Adhesives, Tile & Stone Adhesives, Carpet Flooring Adhesives, Laminate Flooring Adhesives), By End-Use Industry (Residential, Commercial, Industrial, Institutional

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Henkel AG & Co. KGaA, H.B. Fuller Company, Sika AG, Arkema S.A., DOW Inc., Wacker Chemie AG, Mapei S.p.A., LATICRETE International, Inc., Forbo Holding AG, Pidilite Industries Limited, 3M Company, Franklin International, DuPont de Nemours, Inc., KCC Corporation, BASF SE

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

By Chemistry/Resin Type

- Acrylic Adhesives

- Polyurethane Adhesives

- Epoxy Adhesives

- Vinyl Adhesives

- Cementitious Adhesives

- Others

By Technology

- Water-Based

- Solvent-Based

- Reactive

- Hot-Melt

By Application/Flooring Type

- Resilient Flooring Adhesives

- Wood Flooring Adhesives

- Tile & Stone Adhesives

- Carpet Flooring Adhesives

- Laminate Flooring Adhesives

By End-Use Industry

- Residential

- Commercial

- Industrial

- Institutional

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

- Henkel AG & Co. KGaA

- H.B. Fuller Company

- Sika AG

- Arkema S.A.

- DOW Inc.

- Wacker Chemie AG

- Mapei S.p.A.

- LATICRETE International, Inc.

- Forbo Holding AG

- Pidilite Industries Limited

- 3M Company

- Franklin International

- DuPont de Nemours, Inc.

- KCC Corporation

- BASF SE

*- List not Exhaustive

Research Coverage

Prepared by USDAnalytics, this report investigates the Global Flooring Adhesive Market with decision-grade depth, weaving together technology roadmaps, regulatory pivots, and end-use economics to guide specification and sourcing. It delivers analysis reviews of demand across resilient, wood, tile & stone, carpet, and laminate systems; highlights breakthroughs in water-based, SMP/reactive, rapid-cure leveling/mitigation, and low-VOC chemistries; benchmarks moisture/RH tolerances, working/open times, and bond durability under high traffic; and translates code updates and green-building criteria into product selection filters and total installation cost impacts. With granular vendor mapping, channel dynamics, and price–performance corridors by substrate and climate zone, this report is an essential resource for architects, contractors, facility owners, and procurement teams seeking faster installs, higher reliability on high-moisture slabs, and verifiable sustainability outcomes across commercial, industrial, and residential projects.

Scope Highlights

Segmentation:

- By Chemistry/Resin Type: Acrylic; Polyurethane; Epoxy; Vinyl; Cementitious; Others.

- By Technology: Water-Based; Solvent-Based; Reactive; Hot-Melt.

- By Application/Flooring Type: Resilient Flooring Adhesives; Wood Flooring Adhesives; Tile & Stone Adhesives; Carpet Flooring Adhesives; Laminate Flooring Adhesives.

- By End-Use Industry: Residential; Commercial; Industrial; Institutional.

Geographic Scope: Analysis spans 25+ countries across North America, Europe, Asia Pacific, Latin America, the Middle East & Africa.

Time Frame: Historic data 2021–2024 and forecast data 2025–2034.

Companies: Analysis/profiles of 15+ companies covering strategy, portfolios, ESG, M&A, and recent launches.

Deliverables

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.