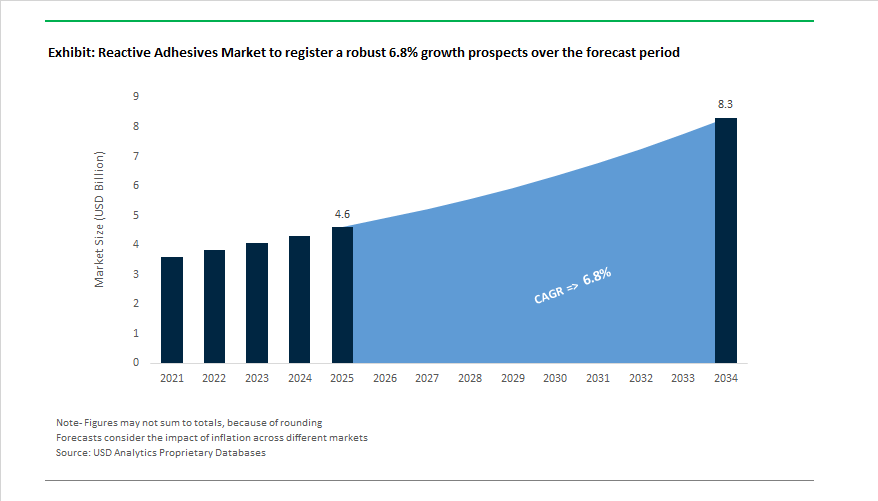

The Global Reactive Adhesives Market is projected to expand from USD 4.6 billion in 2025 to USD 8.3 billion by 2034, growing at a CAGR of 6.8%, as reactive chemistries become structurally embedded in lightweighting, electrification, and precision manufacturing strategies. Growth is being driven less by substitution of legacy glues and more by the system-level redesign of assemblies, where epoxies, polyurethanes, cyanoacrylates, and hybrid reactive systems replace mechanical fastening, welding, and solvent-based bonding in load-bearing and safety-critical applications.

In automotive and e-mobility manufacturing, reactive adhesives are now specified as primary structural elements rather than secondary joining aids. OEMs are increasingly relying on crash-resistant epoxy and polyurethane systems for body-in-white reinforcement, mixed-material joints, and battery pack assembly, where adhesives must deliver shear strength, fatigue resistance, and durability under thermal cycling. Vehicle production volumes exceeding 90 million units annually have amplified the impact of adhesive-driven lightweighting, as even marginal weight reductions translate directly into range extension, emissions compliance, and platform standardization across ICE and EV architectures. Suppliers such as Henkel (LOCTITE structural epoxies), Sika (crash-resistant PU and epoxy systems), and Arkema (Bostik MMA and epoxy technologies) are aligning product development with OEM requirements for automated dispensing, controlled cure profiles, and low-monomer formulations.

The construction and prefabrication ecosystem represents the second major demand pillar, where reactive adhesives are enabling modular, off-site fabrication and high-load glazing systems. Polyurethane and epoxy adhesives are increasingly used in sandwich panels, structural glazing, and façade elements because they combine elastic load transfer with long-term environmental resistance, outperforming mechanical anchoring in both durability and thermal efficiency. As modular construction scales globally, contractors and fabricators are prioritizing one-component, moisture-curing systems that simplify application while meeting stringent movement and adhesion requirements across concrete, metals, and engineered composites.

Electronics and medical device manufacturing are reshaping the performance envelope of reactive adhesives through curing innovation. Fast-curing cyanoacrylates, snap-cure epoxies, and light-activated hybrids are being adopted to support miniaturized assemblies, high-density interconnects, and biocompatible device construction. Directional and electrically conductive reactive adhesives—commercialized by electronics-focused material suppliers—are gaining relevance in miniLED, microLED, and advanced sensor modules, where precise conductivity paths and controlled cure kinetics are critical to yield and reliability. These applications are shifting procurement focus toward process compatibility and functional integration, rather than bond strength alone.

The Global Reactive Adhesives Industry is witnessing a remarkable wave of sustainability partnerships, product innovations, and capacity expansions. Key manufacturers are recalibrating their portfolios to align with carbon neutrality targets, circular production models, and specialized End-Use Industrys across electronics, construction, and automotive manufacturing.

In October 2025, Henkel and Dow deepened their sustainability collaboration, introducing low-carbon feedstocks and renewable electricity in adhesive production. This partnership aims to reduce Product Carbon Footprints (PCF) by 20–40% across selected hot melt lines in Europe — a milestone aligning with the EU Green Deal and corporate decarbonization goals. Similarly, DELO Industrial Adhesives achieved a major breakthrough in September 2025 with the successful validation of directional conductive adhesives, proving their reliability as an alternative to solder for miniLED and microLED assembly, thereby revolutionizing the future of high-density electronics.

In July 2025, H.B. Fuller launched its Millennium PG-1 EF ECO2 roofing adhesive, leveraging patented ECO2 Driven™ technology that replaces high-GWP blowing agents with natural gases — a strong stride in sustainable construction adhesives. That same month, APPLIED Adhesives expanded its market reach through the acquisition of BTmix, reinforcing its position as a custom reactive adhesive solutions leader in North America.

Strategic investments have also been central to expansion plans. Bostik (Arkema) announced a $27 million investment (May 2025) in its Middleton, Massachusetts facility to ramp up production of high molecular weight polyester — a crucial raw material for high-performance reactive adhesives in industrial and automotive sectors. Sika AG, in April 2025, inaugurated a major production facility in Kazakhstan, strengthening its Central Asian footprint and production capacity for mortars and admixtures.

Earlier, DELO (March 2025) introduced an IBOA-free light-curing adhesive engineered for medical wearables and glucose monitoring sensors, meeting rising demand for biocompatible, non-toxic adhesives. H.B. Fuller’s January 2025 restructuring created the Building Adhesive Solutions (BAS) division to consolidate high-margin, performance-driven adhesive operations, while Sika’s new facilities in Singapore and Xi’an (January 2025) further reinforced regional responsiveness.

Market Trend 1: Rising Adoption of Silane-Terminated Polymer (STP) Reactive Adhesives for Sustainable Construction

The construction industry’s pivot toward low-emission, isocyanate-free adhesives has firmly positioned Silane-Terminated Polymers (STPs) at the center of the sustainable materials revolution. STP adhesives—particularly silyl-terminated polyethers (STPE) and silyl-terminated polyurethanes (STPU)—are replacing traditional solvent-based and polyurethane systems in flooring, façade bonding, and sealing applications due to their superior UV stability, elasticity, and environmental compliance.

Under tightening regional regulations such as Germany’s ABG certification and the French VOC Label system, construction adhesives must meet the A+ VOC classification, allowing a maximum TVOC emission level of less than 100 µg/m³. STP systems easily comply without using isocyanates or phthalates, aligning with LEED and BREEAM green building standards.

Performance advancements have eliminated previous mechanical limitations of STPs. New-generation α-silane-terminated polyethers demonstrate tensile lap-shear strengths exceeding 10 N/mm² and a Shore D hardness of up to 80, making them comparable to polyurethane-based structural adhesives. Further, their UV and weather resistance ensure longer maintenance cycles, reducing lifecycle costs for infrastructure and façade projects.

Manufacturers such as Sika, Wacker, and Henkel are expanding their portfolios of isocyanate-free hybrid sealants, promoting health and safety advantages by eliminating REACH training requirements associated with traditional polyurethane use. The ongoing regulatory and technological convergence firmly positions STPs as the future backbone of sustainable, high-performance construction bonding systems.

Market Trend 2: Integration of Reactive Adhesives in Electric Vehicle (EV) Battery Systems

The rapid growth of the electric vehicle (EV) sector has created an advanced material frontier for reactive adhesives in battery module assembly, structural bonding, and thermal management. These adhesives provide both mechanical stability and electrical safety, critical for maintaining energy efficiency and crash resilience.

Modern EV battery packs integrate two-component (2K) epoxy and polyurethane adhesives for bonding dissimilar materials such as aluminum, carbon fiber composites, and thermoplastics. These solutions meet global safety standards like UNECE R100 Rev. 3, enhancing crashworthiness while reducing structural weight by up to 15% compared to mechanical fasteners.

Thermally conductive reactive adhesives (TCAs), formulated with ceramic or aluminum oxide fillers, achieve conductivity levels of 1.5–3.0 W/m·K, effectively dissipating localized heat and minimizing the risk of thermal runaway. Their dual-function design allows simultaneous bonding and thermal control, an essential characteristic in battery cooling plate interfaces and cell-to-cell bonding.

In addition, the rise of automated EV manufacturing favors fast-curing two-component SMP (Silyl-Modified Polymer) and acrylic adhesives, which provide precise viscosity control and quick fixture times suitable for robotic dispensing. These innovations reduce production cycle times and eliminate complex surface preparation processes typical of older epoxies, enabling scalable, high-volume EV production.

Market Opportunity 1: Commercialization of Debonding-on-Demand Adhesives for Recycling and Repairable Electronics

The emergence of right-to-repair regulations and circular economy mandates is driving R&D into debonding-on-demand reactive adhesives—materials designed for controlled disassembly in electronics, EV batteries, and complex assemblies.

Chemical innovators are exploring fluoride-ion degradable and Diels–Alder reversible systems that can depolymerize on thermal or chemical activation, allowing clean separation of substrates such as aluminum, glass, and polymer composites. These systems enable efficient recovery of valuable materials while reducing electronic waste, aligning with EU Circular Economy Action Plan and WEEE directives.

In consumer electronics, manufacturers are adopting thermally debondable PSAs and expandable microsphere systems, which expand by up to 100 times their initial volume under localized heat, breaking adhesive bonds without damaging sensitive PCB components. Laboratory tests demonstrate debonding completion in under 30 seconds using magnetic field-triggered heating of iron oxide nanoparticle-filled adhesives, showcasing the potential for high-speed recycling processes.

Hybrid adhesive systems using dual-stimuli activation—combining imine linkages (acid-sensitive) and thermal triggers—offer additional control. These systems ensure strong bonding during normal product use but allow precise, safe disassembly through mild thermal or chemical exposure, paving the way for modular electronics repair and closed-loop material recovery.

Market Opportunity 2: Advanced Reactive Hotmelts for Lightweight Automotive Interior Assembly

As automotive manufacturers pursue lightweighting and design efficiency, reactive polyurethane hot melt adhesives (PUR-HM) are emerging as indispensable materials for interior assembly, trim bonding, and semi-structural components. Their unique dual-cure mechanism—instant physical solidification followed by moisture-driven crosslinking—combines high green strength with permanent elasticity, optimizing production cycle times for high-speed automated assembly.

In applications such as headliners, dashboards, and door panels, reactive PUR-HMs demonstrate significantly shorter open times (30–60 seconds) compared to two-part systems, accelerating throughput while maintaining strong, flexible bonds. To further enhance performance and sustainability, recent formulations integrate hollow polymeric microspheres (density <0.04 g/cm³), reducing adhesive density by up to 40%, contributing directly to overall vehicle mass reduction and improved EV range efficiency.

In addition, these reactive hotmelts exhibit superior vibration absorption and acoustic dampening—key benefits for EV interiors that require low noise, vibration, and harshness (NVH) levels. Their elastomeric nature provides multi-functional performance, offering thermal insulation, stress dispersion, and adhesion to diverse substrates like composites and plastics used in modular automotive design.

The combination of lightweight formulation, multi-functionality, and automation compatibility positions advanced reactive PUR-HMs as the preferred material class for next-generation EV interior manufacturing, delivering cost-effective production and long-term structural reliability.

Reactive Adhesives Market Share Insights, 2025-2034

Market Share by Component

Two-Component (2K) Reactive Adhesives dominate the global market, accounting for an estimated 61.6% share in 2025, owing to their superior mechanical strength, durability, and chemical resistance. These systems are designed for high-performance structural bonding applications where long-term stability, temperature resistance, and impact strength are critical. Industries such as automotive, aerospace, and renewable energy rely heavily on 2K reactive adhesives for their ability to form strong, permanent bonds between metals, composites, and plastics—especially as lightweighting trends and multi-material assemblies continue to accelerate. The dual-component chemistry allows precise control of curing kinetics and bond strength, making it indispensable for EV battery assembly, aircraft interiors, and industrial machinery manufacturing. Furthermore, advancements in dispensing technologies and automated mixing systems have enhanced 2K adhesives’ process efficiency, supporting their widespread adoption in modern manufacturing.

On the other hand, One-Component (1K) Reactive Adhesives maintain a strong market presence, particularly in construction, do-it-yourself (DIY), and assembly applications, where ease of use, minimal equipment requirements, and ambient curing offer clear advantages. Their popularity in on-site applications such as flooring installation, sealing, and modular construction is attributed to their ability to cure under ambient moisture, providing a balance between flexibility and strength. However, 2K systems continue to outpace 1K formulations in terms of industrial demand due to their faster curing and higher load-bearing capabilities. The segmentation trend underscores a clear divide: 2K systems dominate performance-driven sectors, while 1K adhesives cater to convenience-oriented applications, reflecting the dual dynamics of performance optimization and process simplicity in the global reactive adhesives market.

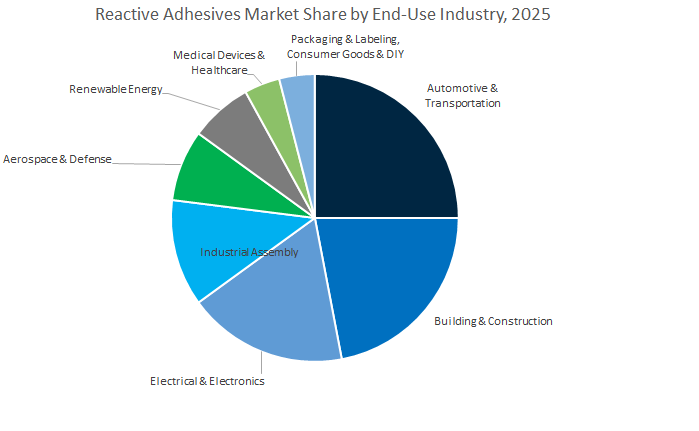

Market Share by End-Use Industry

The automotive and transportation sector holds the largest share of the global reactive adhesives market, estimated at 24.3% in 2025, driven by rapid electrification, lightweighting initiatives, and the replacement of mechanical fasteners with structural bonding. Reactive adhesives have become integral to EV battery module bonding, composite panel assembly, and crash-resistant structural joints, where strength and temperature stability are critical. The move toward electric vehicles (EVs) has particularly accelerated adoption due to the adhesives’ ability to provide thermal management, vibration damping, and long-term durability under extreme conditions.

The building and construction industry follows closely, utilizing reactive adhesives in structural glazing, curtain walls, flooring, and modular construction. The ability to deliver strong, moisture-resistant bonds makes them ideal for both residential and commercial infrastructure projects. Electrical and electronics represent a fast-growing segment as miniaturization and automation demand precise bonding solutions for encapsulation, conformal coatings, and advanced display assembly. In industrial assembly, reactive adhesives are replacing traditional joining techniques across sectors such as appliance, machinery, and renewable energy manufacturing.

The competitive landscape of the Global Reactive Adhesives Market is characterized by strategic manufacturing expansions, ESG-driven innovation, and specialized product diversification. Leading companies including Sika AG, H.B. Fuller, Arkema (Bostik), Henkel AG & Co. KGaA, and 3M Company are focusing on sustainability, fast-curing technologies, and high-value applications to capture emerging demand in automotive, construction, and electronics sectors.

Sika AG remains a frontrunner in construction chemicals and polyurethane systems, renowned for its Sikaflex® and SikaTack® series. The company’s proprietary i-Cure® and PowerCure® technologies enable rapid, moisture-independent curing, ideal for modular construction and automotive lightweighting. In 2025, Sika expanded aggressively, opening new plants in Ust-Kamenogorsk (Kazakhstan) and Quito (Ecuador) to strengthen local supply chains. Its low-isocyanate and high-flexibility adhesives are widely used in infrastructure repair and modular buildings, aligning with the growing demand for smart and sustainable construction materials.

H.B. Fuller continues to expand its presence across industrial, packaging, and construction sectors, emphasizing sustainability and performance efficiency. Its Millennium PG-1 EF ECO2 adhesive (July 2025) integrates ECO2 Driven™ technology, significantly reducing environmental impact in commercial roofing. The company’s 2025 restructuring into the Building Adhesive Solutions (BAS) unit underscores its focus on high-margin markets like structural adhesives. With its portfolio of reactive hot melts, epoxies, and acrylics, H.B. Fuller leads in flexible packaging, insulation glass, and durable industrial bonding solutions.

Bostik, a division of Arkema, is leveraging backward integration and material science to pioneer engineering and elastic bonding solutions. In May 2025, Bostik announced a $27 million investment in its Massachusetts manufacturing plant to boost polyester capacity, enhancing sustainability and reliability for reactive adhesive applications. Its Born2Bond™ precision adhesives and Polytec PT conductive systems cater to aerospace, automotive, and electronics markets requiring high-strength and thermally stable bonding. Bostik’s focus on bio-based and conductive adhesive innovation reinforces its competitive edge in energy-efficient assembly and microelectronic bonding.

Henkel remains a technological powerhouse with industry-leading brands like Technomelt®, Loctite®, and Teroson®. The company’s October 2025 partnership with Dow represents a pivotal sustainability milestone, introducing renewable electricity and low-carbon feedstocks to reduce PCF by up to 40%. Henkel’s reactive polyurethane hot melts and epoxies are widely adopted in industrial assembly, electronics, and MRO applications. With an ongoing transition toward bio-based polyurethane adhesives and high-performance bonding systems, Henkel continues to solidify its position as a climate-positive adhesives manufacturer.

3M Company continues to dominate the high-performance adhesives landscape with its dual-cure polyurethane and structural acrylic technologies. Its dual-cure PU adhesive (late 2023) merges UV and moisture curing, accelerating production cycles in automotive electronics and industrial assembly. 3M’s expertise in Optically Clear Adhesives (OCA) also supports display and medical wearable applications, while its investment in additive manufacturing-compatible adhesives showcases its leadership in digital bonding innovation. Through its deep material science capabilities, 3M continues to redefine reactive adhesive efficiency and processing speed for advanced manufacturing.

Country Analysis: Strategic Developments and Regional Dynamics in the Global Reactive Adhesives Industry

United States: Advanced Aerospace Formulations and Automotive Electrification Fuel Reactive Adhesives Demand

The United States reactive adhesives market is witnessing rapid technological transformation driven by innovation in aerospace, electric vehicles (EVs), and modular construction. In late 2023, 3M Company launched a next-generation Reactive Hot Melt Adhesive engineered for electronic devices and wearables, offering superior thermal resistance, moisture protection, and substrate versatility, positioning it as a preferred solution for miniaturized electronics. The U.S. Department of Energy identified the automotive sector as a major end-user, contributing nearly 25% of global adhesive consumption in 2022, driven by the transition to lightweight materials, composite bonding, and thermal management adhesives for EVs.

Leading players such as Dow Inc. are piloting recyclable polyurethane adhesive systems to strengthen circular economy efforts across flexible packaging applications. In the aerospace sector, manufacturers are investing heavily in modified acrylic (MMA) and epoxy formulations tailored to meet FAA-certified performance standards, critical for composite bonding, fuel system sealing, and structural reinforcement. Similarly, H.B. Fuller’s expansion in North America enhances regional capacity for reactive polyurethane and silane-modified polymer (SMP) adhesives, aligning with the rise in off-site prefabrication and modular construction. The growing synergy between sustainability regulations and performance demands has positioned the United States as a hub for high-performance, low-emission reactive adhesive technology focused on automotive electrification and industrial innovation.

China: Dominating High-Volume Reactive Adhesive Production for Automotive and Electronics Manufacturing

China remains the largest producer and consumer of reactive adhesives in the Asia-Pacific region, accounting for over 50% of the region’s total adhesives and sealants market share. The dominance is underpinned by its industrial scale, strong electronics manufacturing ecosystem, and massive automotive production capacity. Major global companies such as 3M and Dow have increased local investments, expanding reactive adhesive production facilities to strengthen supply chain resilience and meet surging domestic demand. The expansions directly support China’s rapidly evolving EV industry, where thermally conductive polyurethane gap fillers, epoxy potting compounds, and flame-retardant adhesives are essential for battery cell assembly and thermal interface management.

The Chinese government’s advanced materials development programs—aligned with its “Made in China 2025” strategy—are fostering the creation of bio-based and solvent-free adhesive technologies, reducing import dependency and environmental impact. The booming electronics manufacturing segment, producing smartphones, displays, and EV control systems, further drives demand for precision epoxy systems and flexible polyurethane encapsulants. Simultaneously, national eco-packaging standards are mandating the use of low-VOC, water-based adhesive formulations in e-commerce packaging and FMCG labeling. With rising domestic innovation and foreign investment convergence, China stands as the global epicenter for high-performance reactive adhesive formulation and large-scale production efficiency.

Germany: REACH-Compliant Innovation and Automotive Engineering Excellence Propel Reactive Adhesives Market Growth

Germany is at the forefront of reactive adhesive formulation and sustainable chemistry, particularly within automotive engineering, industrial assembly, and construction sectors. In early 2024, Henkel AG & Co. KGaA expanded its specialty portfolio by acquiring Seal for Life Group, bolstering its expertise in sealing, corrosion prevention, and reactive bonding solutions. The German automotive sector remains a leading demand generator for multi-substrate epoxy and polyurethane systems that support lightweight body assembly, crash resistance, and battery protection in EVs.

Environmental compliance is a major driver of product innovation. Adhering to the EU REACH framework, manufacturers are investing in bio-based polyurethane and low-VOC adhesives, exemplified by Henkel’s Technomelt bio-based PUR line launched in 2023. The transition toward sustainable industrial bonding is further reinforced by EU Green Deal mandates emphasizing circular materials. In parallel, reactive epoxy and polyurethane adhesive systems are gaining traction in green building applications, meeting both performance and emissions standards. With its combination of chemical innovation, regulatory alignment, and precision engineering, Germany continues to define the European benchmark for sustainable and high-durability reactive adhesive systems.

Switzerland: Pioneering Low-Isocyanate Reactive Adhesives for Sustainable Construction and Industrial Applications

Switzerland remains a cornerstone of global adhesive innovation, primarily through Sika AG’s leadership in polyurethane and hybrid sealant technologies. In 2024, the company launched its low-isocyanate, ultra-flexible polyurethane adhesive, specifically designed for modular and prefabricated construction applications. The new technology allows for faster installation and superior weather durability, addressing the needs of high-efficiency, off-site manufacturing projects. Furthermore, the company’s proprietary Purform® polyurethane technology, deployed in its Sikaflex® product range, features ultra-low monomeric diisocyanate content (<0.1%), enabling compliance with the EU’s 2023 industrial safety regulations while maintaining mechanical performance.

In late 2023, Sika expanded its North American production capacity by acquiring a regional adhesive manufacturer to reinforce its supply chain for reactive sealants and adhesives in infrastructure and civil construction. Switzerland’s emphasis on R&D excellence and industrial durability ensures its position as a global hub for next-generation reactive polyurethane technologies, combining performance, worker safety, and environmental responsibility in construction-grade and high-performance industrial applications.

Japan: Leading Precision Manufacturing through Advanced Reactive Adhesive R&D and EV Integration

Japan’s reactive adhesives industry is defined by precision engineering, electronics miniaturization, and electric mobility innovation. Local manufacturers such as ThreeBond have developed high-durability, silyl-based reactive sealants like ThreeBond 1160, optimized for EV battery housing, thermal sealing, and vibration protection in automotive electronics. The country’s leadership in epoxy and cyanoacrylate formulations caters to consumer electronics and semiconductor packaging, where micro-bonding precision, fast-curing cycles, and dielectric stability are critical performance factors.

R&D initiatives are focused on high-temperature and humidity-resistant adhesives, addressing Japan’s unique manufacturing needs in power electronics, robotics, and automotive component assembly. Japanese firms are also pioneering magnet bonding technologies, introducing liquid and sheet-type reactive adhesives for rotor core assembly in electric drivetrains, which improve motor efficiency and thermal stability. With its deep integration of chemical innovation, miniaturized bonding applications, and sustainable EV solutions, Japan remains a global technology leader in precision-grade reactive adhesives for high-performance industrial ecosystems.

India: Expanding Reactive Adhesive Market Supported by Infrastructure and Automotive Growth

India is rapidly emerging as one of the fastest-growing markets for reactive adhesives, underpinned by urban infrastructure expansion, industrial manufacturing, and a booming automotive sector. Government initiatives like “Make in India” and large-scale infrastructure projects are catalyzing foreign and domestic investments in reactive polyurethane and epoxy adhesive technologies to support the country’s evolving construction and engineering landscape.

The automotive manufacturing boom, coupled with rising EV adoption, has accelerated demand for high-strength structural adhesives used in vehicle chassis bonding, panel lamination, and thermal management systems. Leading chemical firms have established regional application laboratories to develop cost-optimized, climate-adapted reactive adhesives suitable for India’s unique industrial requirements. Additionally, the construction sector’s focus on precast concrete systems, wall panel bonding, and flooring adhesives is driving the uptake of reactive systems for long-term durability and flexibility. As India’s industrial output and infrastructure projects grow, its market is evolving into a regional hub for reactive adhesive production and technology localization, catering to both domestic and export-oriented manufacturing.

Reactive Adhesives Market Report Scope

Reactive Adhesives Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$4.6 Billion

|

|

Market Size (2034)

|

$8.3 Billion

|

|

Market Growth Rate

|

6.8%

|

|

Segments

|

By Resin Type (Polyurethane, Epoxy, Modified Acrylic, Cyanoacrylate, Silicone, Anaerobic, Silane-Modified Polymers, Others), By Technology (Reactive Hot Melt, UV/LED Curable, Moisture-Curing, Pressure-Sensitive Reactive, Dual-Cure Systems), By Component (One-Component, Two-Component), By End-Use Industry (Automotive & Transportation, Building & Construction, Electrical & Electronics, Aerospace & Defense, Renewable Energy, Consumer Goods & DIY, Medical Devices & Healthcare, Packaging & Labeling, Industrial Assembly), By Application Type (Structural Bonding, Gasketing, Sealing, Laminating, Potting and Encapsulation, Gap Filling

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Henkel AG & Co. KGaA, 3M Company, Sika AG, H.B. Fuller Company, Arkema Group, Dow Inc., Huntsman International LLC, Wacker Chemie AG, Jowat SE, Avery Dennison Corporation, Covestro AG, Master Bond Inc., DELO Industrial Adhesives, ThreeBond Holdings Co., Ltd., Evonik Industries AG

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

By Resin Type

- Polyurethane

- Epoxy

- Modified Acrylic

- Cyanoacrylate

- Silicone

- Anaerobic

- Silane-Modified Polymers

- Others

By Technology

- Reactive Hot Melt

- UV/LED Curable

- Moisture-Curing

- Pressure-Sensitive Reactive

- Dual-Cure Systems

By Component

- One-Component

- Two-Component

By End-Use Industry

- Automotive & Transportation

- Building & Construction

- Electrical & Electronics

- Aerospace & Defense

- Renewable Energy

- Consumer Goods & DIY

- Medical Devices & Healthcare

- Packaging & Labeling

- Industrial Assembly

By Application Type

- Structural Bonding

- Gasketing

- Sealing

- Laminating

- Potting and Encapsulation

- Gap Filling

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in Reactive Adhesives Market

- Henkel AG & Co. KGaA

- 3M Company

- Sika AG

- H.B. Fuller Company

- Arkema Group

- Dow Inc.

- Huntsman International LLC

- Wacker Chemie AG

- Jowat SE

- Avery Dennison Corporation

- Covestro AG

- Master Bond Inc.

- DELO Industrial Adhesives

- ThreeBond Holdings Co., Ltd.

- Evonik Industries AG

*- List not Exhaustive

Research Coverage

Produced by USDAnalytics, this report investigates the Reactive Adhesives Market end-to-end, connecting demand catalysts in lightweight vehicles, sustainable construction, precision electronics, and modular manufacturing with the performance economics of epoxy, polyurethane, cyanoacrylate, modified acrylic, silicone, anaerobic, and silane-modified systems; it delivers analysis reviews on curing speed, bond durability, substrate range, and automation readiness; it highlights breakthroughs in low-VOC one-component systems, UV/LED dual-cure platforms, thermally conductive formulations for EV batteries, and debond-on-demand chemistries for repairability and recycling—making this report an essential resource for procurement, R&D, application engineers, and strategy teams that need defensible forecasts, competitive moves, and specification-level insights across automotive, building, electronics, aerospace, renewable energy, medical devices, and industrial assembly.

Scope Highlights

Segmentation:

- By Resin Type: Polyurethane; Epoxy; Modified Acrylic; Cyanoacrylate; Silicone; Anaerobic; Silane-Modified Polymers; Others.

- By Technology: Reactive Hot Melt; UV/LED Curable; Moisture-Curing; Pressure-Sensitive Reactive; Dual-Cure Systems.

- By Component: One-Component; Two-Component.

- By End-Use Industry: Automotive & Transportation; Building & Construction; Electrical & Electronics; Aerospace & Defense; Renewable Energy; Consumer Goods & DIY; Medical Devices & Healthcare; Packaging & Labeling; Industrial Assembly.

- By Application Type: Structural Bonding; Gasketing; Sealing; Laminating; Potting & Encapsulation; Gap Filling.

- By Region: North America (United States, Canada, Mexico); Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe); Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC); South & Central America (Brazil, Argentina, Rest of SCA); Middle East & Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa).

Geographic Scope: Analysis spans 25+ countries across North America, Europe, Asia Pacific, Latin America, the Middle East & Africa.

Time Horizon: Historic data 2021–2024 and forecast 2025–2034.

Companies: Analysis/profiles of 15+ companies.

Deliverables

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.