Market Overview: Structural Adoption and Formulation Advances Cementing Polyurethane Hot Melt Adhesives in Modern Manufacturing

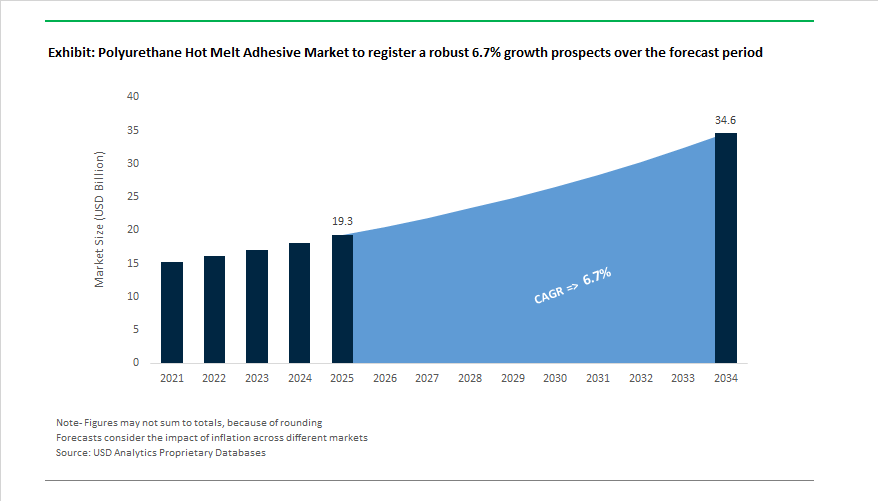

The Global Polyurethane Hot Melt Adhesive (PUR HMA) Market is projected to expand from USD 19.3 billion in 2025 to USD 34.6 billion by 2034, growing at a CAGR of 6.7% as manufacturers increasingly leverage PUR hot melts for end-use reliability, process integration, and sustainability compliance rather than simple bonding. Across automotive, electronics, packaging, and construction, PUR HMAs are supplanting solvent-based systems because they combine reactive crosslinking with thermoplastic processing, delivering bonds that continue to strengthen post-application and resist chemical, thermal, and moisture stresses that many thermoplastics struggle to withstand.

Leading industrial users exploit the reactive chemistry of PUR HMAs—where the adhesive initially solidifies on cooling then continues to crosslink through moisture exposure—to create thermally stable, chemically resistant networks with high cohesive strength, a property that differentiates them from traditional non-reactive hot melts. This characteristic underpins their selection in automotive assembly and engineered wood lamination, where long-term durability and bond integrity are mission-critical, and increasingly in EV battery module encapsulation and advanced electronics assembly, where exposure to thermal cycling and vibration is routine.

Manufacturer practices reflect the breadth of application scope and performance nuances. PUR HMAs are used to bond wood, plastics, fabrics, leather, and engineered panels in wood, furniture, and construction markets thanks to their versatility and wide range of open times and viscosities tailored to specific assembly environments. Industrial adhesive producers also offer 100% solid, solvent-free PUR formulations that align with tightening VOC emission regulations in North America and Europe, reducing environmental impact and occupational health requirements in production facilities.

In packaging, PUR HMAs provide strong, quick bonds with excellent heat resistance and solvent-free profiles, enabling their use in sealing and bonding applications ranging from beverage cartons to rigid transparent packaging structures without the need for solvents. Across apparel and specialty assembly, reactive polyurethane hot melt grades are formulated for quick surface drying and high production efficiency—some grades exhibit surface tack in as little as seconds and full curing over 24–48 hours, reflecting the balance between rapid line throughput and long-term bond development.

The polyurethane hot melt adhesive industry has entered a transformative phase marked by sustainability, digital integration, and regional production expansions. The global chemical and adhesive producers are implementing strategic actions that are reshaping the market’s operational and technological landscape.

In September 2024, Henkel AG & Co. KGaA launched Technomelt Supra 079 Eco Cool, a groundbreaking bio-based PUR HMA that combines 49% renewable feedstock with ISCC-certified raw materials. This innovation cuts CO₂ emissions by 32% while reducing energy consumption, marking a significant milestone in sustainable hot melt manufacturing for packaging and consumer goods. The launch reinforces Henkel’s leadership in low-carbon adhesive solutions and aligns with its global sustainability roadmap.

Similarly, Bostik (Arkema Group) unveiled its Kizen LIME series in September 2024, targeting the packaging and labeling industry with an emphasis on low-carbon, flexible bonding solutions using high-performance PUR technology. These adhesives deliver optimized adhesion on coated papers and biodegradable films, addressing the rapid shift toward eco-friendly, recyclable packaging.

On the industrial side, Dow Inc. completed a tenfold expansion of its VORATRON™ production line in Ahlen, Germany (May 2024), enhancing supply capacity for EV battery adhesives and gap fillers. The project positions Dow as a crucial supplier to Europe’s growing e-mobility value chain, where thermal management, vibration damping, and safety compliance are paramount.

In the construction adhesives segment, Sika AG intensified its regional production capabilities by commissioning a new facility in Ust-Kamenogorsk, Kazakhstan (April 2025). This plant will cater to mortar, concrete admixtures, and PU-based construction adhesives, supporting Sika’s penetration into emerging Central Asian markets. Further expanding its portfolio, Sika acquired Cromar Building Products (March 2025), strengthening its presence in the UK roofing and sealants market.

Sika’s October 2024 investment in Giatec Scientific Inc. highlighted the sector’s digital evolution, as AI-based monitoring systems begin integrating into construction adhesive and sealant applications. Its August 2025 joint venture initiative in Germany, Austria, and Switzerland will further enhance localized supply chains and expand the market for high-performance PUR structural adhesives.

Meanwhile, H.B. Fuller continued its growth trajectory with the acquisition of Sanglier Limited (September 2023), expanding its European engineering adhesives portfolio. Similarly, Henkel’s expansion in Salisbury, North Carolina (December 2022) added a new 10,000-square-foot production unit for Technomelt PUR adhesives, increasing supply reliability for North American customers.

Market Trend 1: Rising Demand for High-Temperature-Resistant Polyurethane HMPURs in Automotive and Electronics Assembly

The surge in electric vehicle (EV) production and miniaturized electronic systems is accelerating the development of high-temperature-resistant polyurethane hot melt adhesives designed to deliver mechanical stability and long-term durability under extreme conditions. Modern EV battery assemblies, electronic control units (ECUs), and sensor modules generate higher thermal loads that traditional thermoplastics and conventional adhesives cannot sustain, positioning reactive polyurethane hot melt adhesives (HMPURs) as indispensable in advanced assembly lines.

Patented innovations—such as the methods detailed in US10781345B1—highlight how polyurethane HMPUR formulations with enhanced heat and cold shock resistance are being tailored for metal-to-plastic bonding and composite assembly in EV systems. These adhesives maintain consistent performance in operating temperature ranges exceeding 120°C, ensuring long-term mechanical integrity in demanding automotive environments.

In electronics manufacturing, where compact assemblies intensify heat concentration, manufacturers like DIC Corporation and H.B. Fuller have introduced reactive PUR hot melts optimized for high-speed, automated component bonding. These products deliver rapid setting times (under 15 seconds) and exceptional mechanical strength, crucial for PCB lamination, connector encapsulation, and optical sensor modules. As electronics miniaturization continues to advance, thermally stable HMPUR systems are becoming a vital enabler for ruggedized consumer electronics and automotive control electronics.

Market Trend 2: Shift Toward Sustainable, Bio-Based, and Low-Monomer Reactive HMPURs in Packaging and Furniture Manufacturing

The global packaging and furniture sectors are undergoing a decisive transformation driven by regulatory mandates such as EU REACH Annex XVII, which restricts monomeric diisocyanate content above 0.1%. The has catalyzed the market’s shift toward micro-emission polyurethane hot melt adhesives and bio-based HMPUR formulations that provide performance parity with traditional solvent systems while significantly improving sustainability credentials.

In response, leading manufacturers including Henkel, Jowat, and Bostik have commercialized new low-VOC, REACH-compliant adhesive lines specifically engineered for furniture lamination, profile wrapping, and paper-based packaging. These systems minimize worker exposure risks, aligning with EU directives that require mandatory safety training for handling high-isocyanate products.

Simultaneously, bio-based polyurethane hot melt adhesives—derived from renewable feedstocks such as bio-based polyols and plant oils—are setting new standards in sustainable manufacturing. Recent product innovations like Henkel’s Technomelt Supra ECO demonstrate that 85% bio-based formulations can achieve fast curing times (1–2 seconds) and maintain thermal resistance up to 98°C, fully degrading within 180 days under industrial composting conditions. These attributes have made bio-HMPURs the adhesive of choice for eco-friendly packaging and circular furniture production, directly contributing to global carbon reduction targets.

Market Opportunity 1: Automation-Driven Adoption in Footwear Manufacturing with Solvent-Free HMPUR Systems

The transition toward automated footwear assembly lines and the elimination of solvent-borne adhesives has unlocked significant growth potential for reactive polyurethane hot melt adhesives in footwear production. HMPURs provide the ideal combination of high flexibility, excellent adhesion, and zero VOC emissions, supporting robotic application systems in modern shoe manufacturing plants.

Research studies confirm that bio-based polyurethane hot melt formulations can achieve bonding strength equivalent to traditional solvent-based cements in sole bonding, insole lamination, and upper attachment applications. For instance, studies evaluating sustainable HMPURs for footwear joints show adhesive tensile strengths exceeding 2.5 MPa, meeting or exceeding the quality benchmarks for commercial use while maintaining full environmental compliance.

The rapid curing, moisture-reactive nature of these adhesives allows seamless integration into automated or semi-robotic assembly lines, reducing production cycle times and manual labor. As footwear brands intensify efforts to reduce carbon footprints and eliminate toxic emissions, solvent-free, bio-based HMPURs are expected to dominate the global footwear adhesive market in the coming decade.

Market Opportunity 2: High-Performance HMPUR Solutions for Composite and Multi-Material Construction Applications

The accelerating adoption of prefabricated composite panels and multi-material structures in the construction and infrastructure sectors is driving demand for structural polyurethane hot melt adhesives that offer superior weather resistance, elasticity, and mechanical durability.

In panel lamination for façades, floors, and transportation interiors, moisture-curing HMPURs are gaining prominence for their dual-phase bonding action—delivering instant high green strength followed by chemical cross-linking that produces a permanently elastic, chemical-resistant joint. Technical application data from leading suppliers such as Bostik and TEX YEAR confirm that these adhesives withstand temperature extremes from -40°C to +120°C, resist water ingress, and bond effectively to diverse substrates, including aluminum, PVC, wood, and fiber-reinforced composites (FRCs).

The performance profile makes reactive HMPURs the adhesive of choice for Structural Insulated Panels (SIPs), curtain walls, and modular construction elements where traditional mechanical fasteners fail to maintain long-term structural integrity. Further, the industry’s shift toward energy-efficient, lightweight building systems positions HMPURs as the go-to solution for composite bonding in high-performance architecture and infrastructure.

Polyurethane Hot Melt Adhesive Market Share Insights, 2025-2034

Market Share by Product Type/Chemistry

The Reactive Polyurethane Hot Melt Adhesives (PUR HMA) segment leads the global polyurethane hot melt adhesive market, accounting for an estimated 69.4% market share in 2025. This dominance is attributed to their exceptional mechanical strength, chemical and heat resistance, and superior durability once cured. Reactive PUR HMAs undergo a secondary curing reaction with ambient moisture, forming thermoset cross-linked structures that provide permanent, high-strength bonding performance across diverse substrates such as metals, plastics, wood, and composites. These characteristics make them indispensable in automotive assembly, furniture manufacturing, packaging, construction, and electronics—industries that demand both processing efficiency and long-term reliability.

Meanwhile, non-reactive polyurethane hot melt adhesives hold a significant yet smaller share, primarily used in applications prioritizing speed, convenience, and strong initial tack over extreme environmental durability. Non-reactive systems are widely adopted in bookbinding, packaging, labeling, and woodworking, where process speed and aesthetics are key. Their instant bond formation, low energy consumption, and recyclability make them valuable in high-speed assembly lines. However, the market trend is increasingly favoring reactive PUR HMAs due to their dual advantage of hot melt processability and thermoset performance, aligning with global demand for high-performance, low-VOC adhesive solutions that meet modern manufacturing standards and sustainability goals.

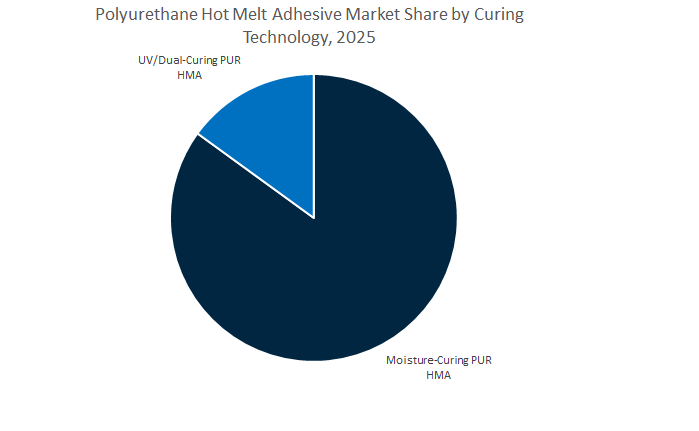

Market Share by Curing Technology

The Moisture-Curing PUR Hot Melt Adhesives segment overwhelmingly dominates the market, projected to capture 82.6% share in 2025, underscoring its position as the industry standard in reactive hot melt adhesive technologies. Moisture-curing systems cure through ambient humidity, enabling controlled cross-linking that enhances bond strength, chemical resistance, and thermal stability. This curing mechanism allows for long open times, facilitating complex assembly processes before achieving permanent adhesion. The simplicity of processing, coupled with high final bond integrity, has made moisture-curing PUR HMAs the preferred choice across automotive, woodworking, textile, furniture, and packaging sectors. Their versatility in bonding porous and non-porous substrates—combined with excellent resistance to heat, solvents, and impact—drives their continued dominance. Moreover, advancements in low-emission and fast-curing moisture-based formulations are reinforcing their role in sustainable manufacturing environments where environmental compliance and production efficiency are paramount.

On the other hand, UV/Dual-Curing PUR HMAs represent a smaller but rapidly expanding segment, primarily focused on precision-driven, high-value applications. These formulations leverage dual-curing mechanisms—using both UV light and moisture or heat activation—to enable instant tack and complete curing control, which is critical in electronics, medical devices, and advanced industrial assembly. The technology allows for automation compatibility, minimal downtime, and exact curing in shadowed or intricate bonding areas. While this segment remains niche, its growth trajectory is strong, reflecting the global shift toward smart manufacturing and precision adhesives. As manufacturers increasingly adopt hybrid production systems and robotics, UV and dual-cure PUR HMAs are expected to gain traction in applications demanding speed, precision, and reliability, positioning them as the next-generation adhesive technology within the polyurethane hot melt ecosystem.

The polyurethane hot melt adhesive market is consolidated among major multinational producers that combine advanced polymer science, regional manufacturing, and sustainability-driven innovation. These key participants are strengthening their competitive position through bio-based chemistry, capacity expansions, and regulatory compliance leadership.

Henkel remains the global market leader in polyurethane hot melt adhesives, generating over EUR 21.6 billion in 2024 sales under its Adhesive Technologies division. Its Technomelt PUR portfolio is globally recognized for applications in bookbinding, furniture lamination, and high-speed packaging. The company’s latest launch, Technomelt Supra 079 Eco Cool, integrates 49% bio-based content, aligning with circular economy initiatives. Henkel’s 2025 strategy focuses on accelerating digital manufacturing, low-VOC innovation, and smart packaging adhesives while maintaining global production network efficiency across 150+ sites.

H.B. Fuller is a key player specializing in Reactive Hot Melt (RHM) and High-Performance PUR adhesives for automotive interiors, packaging, and flexible lamination. Its one- and two-component polyurethane solutions are engineered for superior impact resistance, aging durability, and rapid processing speeds. The company’s 100% solids formulations eliminate solvent carriers, enabling VOC-free operations. With the 2023 acquisition of Sanglier Limited, Fuller expanded its reach across construction and engineering adhesives in Europe, reinforcing its presence in high-value industrial bonding markets.

Bostik, a division of Arkema, leverages material science expertise to develop crystalline and amorphous PUR adhesives suitable for automotive interiors, packaging, and textiles. Its Kizen LIME launch in 2024 highlighted Arkema’s strategy to deliver carbon-neutral, recyclable packaging adhesives. With a portfolio spanning high-temperature crystalline PUR HMAs for structural applications and low-temperature breathable membrane adhesives, Bostik continues to lead in sustainable and intelligent adhesive systems for demanding markets.

Sika continues to innovate with its Purform® polyurethane technology, designed with <0.1% free monomer diisocyanate content, exempting users from REACH-specific training requirements. Its adhesives serve vehicle glazing, roofing, and building envelope sealing, offering superior elasticity and weather durability. Through its 2025 joint venture projects and new Kazakhstan plant, Sika is strengthening its regional manufacturing footprint. Posting 7.4% sales growth in 2024, Sika’s expansion strategy reflects its dominance in sustainable construction adhesives and industrial bonding solutions.

3M’s Scotch-Weld™ and Fastbond™ PUR Hot Melt Adhesives are synonymous with high-strength, precision industrial assembly. Leveraging its material science expertise, 3M develops dual-cure and reactive PUR adhesives for applications requiring impact resistance and dynamic load endurance, such as automotive electronics and transportation components. The company is investing in smart adhesive systems with self-healing capabilities, aimed at extending component lifecycles in medical devices, electronics, and mobility sectors. Its strong R&D orientation (6% of annual sales reinvested) underscores 3M’s leadership in next-generation polyurethane bonding.

Country Analysis: Regional Innovations and Strategic Advancements in the Global Polyurethane Hot Melt Adhesive (PUR HMA) Industry

China: Expanding Global Manufacturing Leadership with Sustainable and High-Speed PUR Hot Melt Production

China remains the largest global manufacturing hub for Polyurethane Hot Melt Adhesives (PUR HMAs), driven by its dominance in automotive, electronics, and construction sectors. The nation’s continued industrial transformation under the “Made in China 2025” initiative has positioned advanced materials, including high-performance reactive adhesives, at the forefront of strategic growth. Major investments are pouring into Non-Isocyanate PUR and bio-based reactive polyurethane formulations, aligning with stricter environmental emission controls and the country’s national sustainability targets. The rapid electrification of transport has made China a major consumer of PUR HMAs for EV battery module bonding, where their superior thermal stability, flexibility, and chemical resistance make them indispensable in lightweight vehicle assembly.

Additionally, China’s booming infrastructure and urbanization wave continues to boost demand for moisture-resistant construction adhesives, particularly for insulation panels, window profile wrapping, and facade applications. Global adhesive manufacturers are expanding local PUR HMA production capacity in central and southern China to ensure shorter lead times and supply consistency for Tier 1 suppliers in automotive, packaging, and electronics manufacturing. In 2024–2025, the surge in robotic dispensing technology adoption has further modernized flat lamination processes in high-gloss kitchen and office furniture production, optimizing precision and output efficiency. Supported by industrial innovation, renewable chemistry, and automation, China stands as the driving force behind next-generation PUR HMA manufacturing in Asia-Pacific.

Germany: European Leader in Low-Emission and Fast-Curing Polyurethane Hot Melt Technologies

Germany continues to define the European premium market for PUR hot melt adhesives, balancing stringent REACH compliance, sustainability, and automotive-grade performance. The Annex XVII restrictions on Di-isocyanates have spurred domestic adhesive manufacturers to pioneer Micro-Emission PUR Hot Melt Adhesives (ME-PUR) containing less than 0.1% free monomers, ensuring worker safety and regulatory compliance. German producers are also global frontrunners in developing Fast-Curing PUR HMAs designed for high-speed, automated assembly lines in luxury automotive interiors, dashboard assembly, and high-end profile wrapping, where aesthetic precision and bond reliability are critical.

A strong emphasis on bio-based polyols derived from renewable resources supports Germany’s broader carbon neutrality objectives. The transition toward lightweight vehicle structures and multi-material designs—integrating composites, aluminum, and thermoplastics—has amplified the role of reactive PUR adhesives in replacing welding and mechanical fastening. Simultaneously, a major European adhesive company announced a significant capacity expansion in Germany to meet the growing demand for low-VOC, solvent-free adhesive systems in packaging, furniture, and construction sectors. Academic collaborations between German technical universities and industrial R&D centers are further advancing moisture-curing kinetic models, ensuring predictable bond performance under varying climatic conditions. As the innovation hub for high-performance PUR systems, Germany remains central to Europe’s sustainable adhesive transformation.

United States: PUR Hot Melts Revolutionizing Packaging, Nonwovens, and Modular Construction

The United States Polyurethane Hot Melt Adhesives (PUR HMA) market is undergoing rapid growth across e-commerce packaging, nonwoven hygiene products, modular construction, and electronics assembly. American adhesive manufacturers are at the forefront of hybrid material innovation, developing UV-curable and hybrid reactive PUR hot melts that enable faster curing, high temperature resistance, and flexible bonding in sensitive electronics and medical device applications. The thriving e-commerce and logistics sector continues to propel demand for PUR-based packaging adhesives, which provide superior bonding strength on recycled corrugated boards—a key challenge in sustainable packaging design.

State-level regulatory tightening, particularly under California’s SCAQMD VOC rules, is accelerating the industry’s shift toward 100% solids, solvent-free PUR adhesive systems. The construction sector is also embracing PUR HMAs in cross-laminated timber (CLT) and prefabricated modular housing, where durability, moisture resistance, and structural integrity are critical. Additionally, R&D initiatives across U.S. adhesive laboratories are exploring reversible polyurethane formulations to enable easy disassembly of multi-layer flexible packaging, advancing the circular economy for polymeric materials. With robust investment, advanced production facilities, and growing sustainability mandates, the U.S. has established itself as a key global center for high-performance PUR adhesive technology innovation.

Japan: Precision PUR Hot Melts for Miniaturized Electronics and Automotive Lightweighting

Japan’s polyurethane hot melt adhesive market exemplifies the fusion of precision manufacturing, electronics innovation, and material science excellence. The country’s electronics sector—known for miniaturized consumer devices like smartphones, wearables, and smart sensors—demands ultra-low-temperature dispensing PUR HMAs to protect delicate components from heat-induced stress during assembly. The advanced formulations deliver high precision, fast wetting, and superior adhesion strength, making them ideal for high-speed robotic dispensing on flexible printed circuit boards (FPCBs) and fine-pitch electronic modules.

In the automotive industry, PUR HMAs are vital for lightweight structural bonding, providing both crash resistance and vibration absorption while ensuring compliance with stringent fuel efficiency and safety standards. Academic institutions in Japan are publishing extensive studies on the viscoelastic and fatigue properties of reactive polyurethane adhesives under thermal cycling, strengthening predictive models for electronic reliability and automotive performance. Japanese factories are also pioneering Industry 4.0-driven production systems, utilizing AI-aided process control and real-time viscosity monitoring to achieve zero-defect bonding. With its unmatched expertise in precision, automation, and advanced polymer chemistry, Japan remains a global hub for premium PUR HMA technologies in electronics and automotive innovation.

Italy: PUR Hot Melts Powering High-End Furniture, Woodworking, and Footwear Excellence

Italy stands as a major European hub for luxury furniture, woodworking, and footwear adhesives, where aesthetic precision and durability are paramount. The country’s prestigious furniture and interior design sectors heavily rely on premium PUR Hot Melts for Edgebanding and Profile Wrapping, enabling seamless, invisible bond lines with superior heat resistance and color stability. Italian manufacturers are also innovating moisture-curing polyurethane formulations specifically engineered for high-gloss laminated panels and curved-edge profiles, meeting the evolving standards of global furniture export markets.

In the footwear and leather goods industries, Italy is leading in the adoption of specialized polyurethane-based adhesives that outperform traditional solvent-based glues in flexibility, adhesion strength, and water resistance. Local adhesive producers are scaling production capacity to meet the rising demand for PUR HMA systems in structural bonding for earthquake-resistant timber construction and engineered wood panels, aligning with Italy’s sustainability and building resilience standards. By combining craftsmanship with chemical innovation, Italy continues to dominate Europe’s aesthetic and performance-driven PUR adhesive markets.

South Korea: Driving Display and Automotive Innovation Through Advanced PUR Adhesive Technologies

South Korea has rapidly become a key Asian hub for advanced display technology and high-performance automotive components, both of which rely heavily on next-generation PUR Hot Melt Adhesives. The country’s leadership in OLED and flexible display manufacturing drives intensive R&D in transparent, flexible optical PUR adhesives, offering high clarity, low shrinkage, and strong adhesion for foldable smartphones, tablets, and thin-film panels. The adhesives are critical for maintaining optical performance and mechanical reliability in ultra-thin displays.

In the automotive sector, Korean OEMs use PUR HMAs extensively for direct glazing applications (windshields), interior lamination, and body reinforcement, contributing to improved vehicle safety, structural stiffness, and acoustic insulation. The convergence of electronics, mobility, and material science innovation positions South Korea as a leading market for high-precision, durable, and versatile PUR adhesives. Supported by continuous investment in advanced polymer chemistry and display technology infrastructure, the country is set to play a pivotal role in shaping the next phase of Polyurethane Hot Melt Adhesive development across Asia-Pacific.

Polyurethane Hot Melt Adhesive Market Report Scope

Polyurethane Hot Melt Adhesive Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$19.3 Billion

|

|

Market Size (2034)

|

$34.6 Billion

|

|

Market Growth Rate

|

6.7%

|

|

Segments

|

By Product Type (Reactive, Non-Reactive), By Curing Technology (Moisture-Curing, UV/Dual-Curing), By Raw Material (Polyether-based, Polyester-based, Bio-Based/Renewable Polyol), By End-User (Woodworking & Furniture, Automotive & Transportation, Packaging & Labeling, Building & Construction, Nonwovens & Hygiene, Electronics & Electrical, Footwear & Leather, Textile & Apparel, Others

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Henkel AG & Co. KGaA, H.B. Fuller Company, Arkema Group (Bostik), Sika AG, 3M Company, Jowat SE, Dow Inc., Wacker Chemie AG, DIC Corporation, Huntsman International LLC, DuPont de Nemours, Inc., BASF SE, Ashland Global Holdings Inc., Klébér Adhésifs (Kleiberit), Tex Year Industries Inc.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

By Product Type/Chemistry

By Curing Technology

- Moisture-Curing

- UV/Dual-Curing

By Raw Material

- Polyether-based

- Polyester-based

- Bio-Based/Renewable Polyol

By End-Use Industry/Industry

- Woodworking & Furniture

- Automotive & Transportation

- Packaging & Labeling

- Building & Construction

- Nonwovens & Hygiene

- Electronics & Electrical

- Footwear & Leather

- Textile & Apparel

- Others

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in Polyurethane Hot Melt Adhesive Market

- Henkel AG & Co. KGaA

- H.B. Fuller Company

- Arkema Group (Bostik)

- Sika AG

- 3M Company

- Jowat SE

- Dow Inc.

- Wacker Chemie AG

- DIC Corporation

- Huntsman International LLC

- DuPont de Nemours, Inc.

- BASF SE

- Ashland Global Holdings Inc.

- Klébér Adhésifs (Kleiberit)

- Tex Year Industries Inc.

*- List not Exhaustive

Research Coverage

Developed by USDAnalytics, this report investigates the Global Polyurethane Hot Melt Adhesive (PUR HMA) Market, delivering analysis reviews on demand inflection points, pricing levers, and technology differentiation across automotive, electronics, packaging, woodworking, and construction supply chains; it highlights breakthroughs in reactive chemistry (HMPUR), low-temperature dispensing, and bio-based/low-monomer systems, benchmarks regulatory impacts on VOC limits and worker safety, and translates specification-level performance (green strength, heat/humidity endurance, dielectric and creep resistance) into sourcing and ROI guidance—making this report an essential resource for executives, product managers, procurement leaders, and application engineers shaping solvent-free, high-throughput bonding strategies.

Scope Highlights

Segmentation:

- By Product Type/Chemistry: Reactive; Non-Reactive.

- By Curing Technology: Moisture-Curing; UV/Dual-Curing.

- By Raw Material: Polyether-based; Polyester-based; Bio-Based/Renewable Polyol.

- By End-Use Industry/Industry: Woodworking & Furniture; Automotive & Transportation; Packaging & Labeling; Building & Construction; Nonwovens & Hygiene; Electronics & Electrical; Footwear & Leather; Textile & Apparel; Others.

- By Region: North America (United States, Canada, Mexico); Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe); Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC); South & Central America (Brazil, Argentina, Rest of SCA); Middle East & Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa).

Geographic Scope: Analysis spans 25+ countries across North America, Europe, Asia Pacific, Latin America, the Middle East & Africa.

Time Horizon: Historic data 2021–2024 and forecast data 2025–2034.

Companies Covered: Analysis / profiles of 15+ companies.

Deliverables

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.