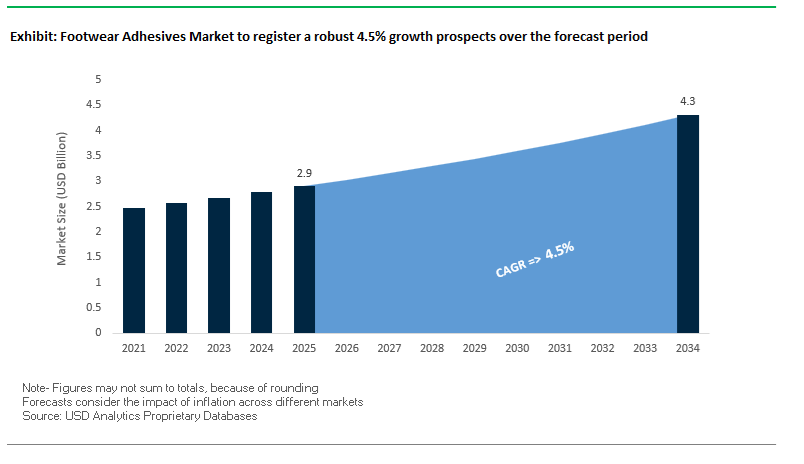

The Global Footwear Adhesives Market is projected to grow from USD 2.9 billion in 2025 to USD 4.3 billion by 2034, advancing at a CAGR of 4.5%, as footwear manufacturing undergoes a structural reset driven by sustainability mandates, automation, and lightweight product design. Adhesives are no longer treated as auxiliary consumables; they are increasingly specified as process-critical materials that directly influence line speed, worker safety, recyclability, and long-term product durability. Global brands and OEMs are pushing suppliers to eliminate solvent-based systems in favor of waterborne polyurethane (WBPU), hot-melt, and reactive polyurethane chemistries, aligning adhesive selection with broader decarbonization, VOC reduction, and labor safety objectives embedded in corporate sourcing standards.

From a manufacturing and supplier perspective, this transition is most pronounced in Asia-Pacific, which accounts for over 60% of global footwear production and serves as the primary implementation ground for new adhesive technologies. Leading adhesive producers such as Henkel, H.B. Fuller, Sika, Bostik, and Dow have expanded WBPU and hot-melt portfolios specifically tailored for athletic, casual, safety, and outdoor footwear, with formulations designed to meet EU REACH, U.S. EPA, and ASEAN chemical compliance requirements. Waterborne systems with VOC levels below 5 g/L are increasingly specified by major athletic and fashion brands, not only to meet regulatory thresholds but to enable safer factory environments and reduce ventilation and energy costs. In parallel, reactive polyurethane and hot-melt adhesives delivering peel strengths exceeding 4 N/mm are being adopted in heavy-duty applications such as military, industrial, and safety footwear, where bond failure directly impacts product liability.

Automation is emerging as a decisive market-shaping force. Footwear OEMs are rapidly deploying automated dispensing, robotic bonding, and digitally monitored curing systems to improve consistency and throughput across high-volume assembly lines. This is driving demand for adhesive formulations with controlled open times and setting times below 60 seconds, enabling precise placement and rapid handling without compromising bond integrity. At the same time, sustainability-driven product design is influencing chemistry choices: single-polymer adhesive systems, including liquid thermoplastic polyurethane (LTPU), are gaining traction as they enable material compatibility between uppers, midsoles, and outsoles, supporting mechanical recyclability and circular footwear models.

The global footwear adhesives market is defined by strategic investments, regulatory tightening, material innovation, and accelerated sustainability initiatives across leading manufacturing hubs.

In September 2025, a major European specialty chemicals company announced a $40 million investment to expand polyurethane dispersion capacity in its Shanghai facility, strengthening the supply of waterborne polyurethane (WBPU) adhesives in the Asia-Pacific region. This investment addresses the surging demand from footwear manufacturing clusters in China, Vietnam, and Indonesia, where footwear OEMs are aggressively transitioning to solvent-free adhesive systems that align with global brand sustainability mandates.

In August 2025, a global adhesives manufacturer commercialized a new range of reactive polyurethane hot-melt adhesives (HMPURs) containing over 30% bio-based polyols, marking a milestone in bio-feedstock integration. These advanced adhesives are engineered for hiking and performance footwear, combining high initial tack with long-term flexibility, while reducing the carbon footprint compared to petroleum-based alternatives.

In July 2025, the footwear adhesives sector witnessed a strong push toward digital manufacturing integration. A key supplier to the sports footwear industry introduced an AI-driven advisory platform that provides real-time monitoring, predictive maintenance, and precision control for automated adhesive application lines—transforming productivity and consistency in high-volume sneaker production.

In June 2025, a Southeast Asian government introduced new labor safety standards banning the use of high-VOC solvent adhesives, compelling local factories to adopt water-based or solvent-free systems. This policy change is expected to reshape the supply chain dynamics in major export markets like Vietnam, Thailand, and Indonesia, driving significant demand for compliant WBPU and EVA adhesives.

In April 2025, an academic breakthrough reported the creation of a fast-crystallizing thermoplastic elastomer (TPE) adhesive, capable of achieving full bonding in under 10 seconds for sole-to-upper attachment on TPE-based substrates—an innovation with potential to revolutionize fast-cycle footwear production.

From a supply chain perspective, February 2025 saw a merger between a South American natural rubber producer and a European chemical firm, ensuring consistent access to natural latex feedstocks for eco-friendly adhesive production. Similarly, in December 2024, a major adhesives company opened a Footwear Innovation Center in Vietnam, focusing on cold-bonding adhesive technologies to minimize energy use and enhance process efficiency in shoe assembly.

The industry is also being reshaped by brand-driven commitments—such as a November 2024 initiative by a leading global footwear brand to ensure that, by 2026, all adhesives used in its shoes will support end-of-life reprocessing and recyclability. Meanwhile, in October 2024, a North American safety footwear manufacturer adopted proprietary reactive hot-melt adhesives that improved bond performance under thermal stress by 40%, underscoring the continued importance of performance adhesives in high-durability footwear segments.

The footwear adhesives market is rapidly transitioning away from traditional solvent-based polyurethane systems to water-based, solvent-free, and reactive hot melt adhesives, under the dual pressure of environmental regulations and brand sustainability commitments. Regulations limiting Volatile Organic Compounds (VOCs) have become the industry’s defining transformation driver, compelling major footwear manufacturers to adopt water-based polyurethane (PU) and non-toxic formulations. Industry bodies such as SATRA have identified the adoption of water-based systems as a “quick sustainability win,” citing their ability to drastically cut atmospheric emissions while maintaining equivalent peel strength and bond integrity to solvent-based systems.

Leading footwear brands are embedding sustainability into their material sourcing strategies. Nike’s “Move to Zero” campaign, for example, sets a 2025 target for achieving zero carbon and zero waste manufacturing. The goal directly impacts the adhesive supply chain, pushing suppliers to develop low-VOC, high-solid PU adhesives that meet Restricted Substances List (RSL) requirements while maintaining mechanical performance across a range of substrates, including synthetic leather and knit uppers. Parallel innovations in non-isocyanate polyurethane systems and encapsulated cross-linking agents are addressing the toxicity challenge of traditional 2K PU systems, improving both worker safety and long-term product compliance.

As sustainability becomes a procurement prerequisite, manufacturers that can deliver low-toxicity, solvent-free adhesives with superior reactivation performance and long open times are emerging as preferred partners for global brands. The transition is not only reducing the industry’s environmental footprint but also establishing water-based systems as the global benchmark for eco-friendly footwear production.

The surge in demand for performance, outdoor, and winter footwear is fueling a wave of innovation in high-flexibility, low-temperature-resistant adhesives capable of maintaining bond strength under extreme temperature fluctuations and mechanical stress. Modern athletic footwear combines complex materials—lightweight thermoplastic polyurethanes, engineered meshes, and foam-based midsoles—that require adhesives capable of bonding dissimilar substrates without compromising elasticity or durability.

Hot melt adhesives, particularly reactive polyurethane (PUR) hot melts, are emerging as the preferred choice due to their superior flexibility, dynamic-load endurance, and strong adhesion at temperatures as low as −30°C. Specialized adhesive formulations designed for high-performance footwear applications feature softer films and low reactivation temperatures (~50°C), ensuring compatibility with temperature-sensitive materials like cup soles and synthetic uppers. The innovation minimizes the risk of substrate deformation while maintaining production speed and adhesive penetration.

Manufacturers are investing in next-generation polyester and EVA-based hot melts, which combine high mechanical strength with chemical resistance, crucial for outdoor and sports footwear exposed to moisture and temperature extremes. As global athletic and performance footwear markets expand, these innovations are setting a new standard for adhesive resilience, flexibility, and process efficiency across climate-sensitive and high-stress product categories.

The rising momentum toward circular economy principles in footwear manufacturing presents one of the most promising growth opportunities for adhesive producers. Brands are moving toward design-for-disassembly concepts, where adhesives play a central role in enabling recyclability by allowing clean material separation at end-of-life. The challenge is to balance strong, long-term adhesion during use with controllable debonding mechanisms that facilitate recovery of components like soles, midsoles, and uppers.

Global sustainability pioneers are setting the benchmark. Adidas, for instance, launched the first fully recyclable running shoe constructed using a single recyclable material, eliminating conventional glue altogether. The move drives a broader industry trend toward reversible adhesives that respond to specific triggers—heat, light, or solvents—to safely dissolve without residue. Research in thermo-reversible and bio-based adhesives derived from starches, proteins, and natural oils is accelerating, offering biodegradable, non-toxic solutions that complement the footwear sector’s shift away from petrochemical-based materials.

From a market standpoint, the next frontier lies in commercializing biodegradable and bio-based hot melts designed for footwear assembly lines, combining strong adhesion, fast curing, and recyclability. The integration of eco-adhesive chemistry with circular design principles positions the sector at the forefront of the footwear industry’s sustainable transformation, creating long-term commercial potential for environmentally responsible adhesive systems.

The global push toward automated and robotic footwear production is revolutionizing adhesive formulation and application methods. As manufacturers deploy robotic cementing and extrusion systems, adhesives must meet precise rheological, viscosity, and curing parameters compatible with automated application. Studies on robotic adhesive systems show that even deposition and continuous flow control are essential to maintain production speeds of up to 200mm/s while ensuring strong, uniform bonding across complex three-dimensional shoe geometries.

Modern automation in footwear manufacturing, inspired by robotic path optimization and AI-driven process control, relies heavily on adhesives engineered with high flow consistency and rapid set times. Robotic extrusion methods—similar to 3D printing—demand adhesive filaments or cartridge-based hot melts capable of melting, dispensing, and curing almost instantaneously. Manufacturers are also developing precision spray adhesives optimized for robotic spray paths that can handle irregular surfaces without clogging or over-application.

The integration of smart adhesive systems compatible with robotics is transforming factory layouts and enabling scalability for high-volume footwear production. As the footwear industry moves toward Industry 4.0, the adhesives sector stands to gain substantially by supplying robotic-compatible, high-speed curing formulations that enhance automation efficiency while maintaining premium bonding performance. The alignment between material innovation and advanced manufacturing automation represents one of the most transformative opportunities for the footwear adhesives market through 2030.

Footwear Adhesives Market Share Insights, 2025-2034

The water-borne footwear adhesives segment commands the largest market share at 42.6% in 2025, driven by the industry’s accelerating transition toward sustainable, eco-compliant, and low-emission adhesive technologies. This dominance is reinforced by global regulations restricting VOC emissions and the footwear industry’s move toward greener production processes, especially among major brands such as Nike, Adidas, and Puma, which have adopted water-borne systems in large-scale manufacturing. These adhesives offer excellent bond strength, improved flexibility, and compatibility with leather, EVA, rubber, and fabric materials, making them suitable for both sports and fashion footwear production. Additionally, advancements in polyurethane dispersion (PUD) and acrylic polymer formulations have closed the performance gap between water-borne and solvent-based systems, leading to widespread adoption in both athletic and lifestyle footwear lines. Their rising use across Asia-Pacific’s large-scale shoe manufacturing hubs — particularly in China, Vietnam, and Indonesia — has consolidated their leadership in global production networks.

Solvent-borne adhesives, while retaining a notable share, are gradually declining due to tightening environmental regulations in Europe and North America. However, they remain indispensable in applications requiring superior tack strength, faster setting times, and high resistance to moisture and temperature extremes. Solvent-based polyurethane and chloroprene formulations continue to find strong demand in work boots, outdoor shoes, and heavy-duty footwear, where mechanical performance outweighs sustainability priorities. In parallel, the hot melt adhesives segment is expanding rapidly, driven by automation in footwear manufacturing. Their instant bonding capability and solvent-free composition make them ideal for thermoplastic and rubber component assembly, especially in midsoles, insoles, and foam attachments. Moreover, their efficiency in automated production lines enhances throughput while reducing process variability. Other technologies, including reactive polyurethane and hybrid adhesives, are carving niche applications in specialty footwear and performance-grade shoes requiring exceptional elasticity and long-term durability.

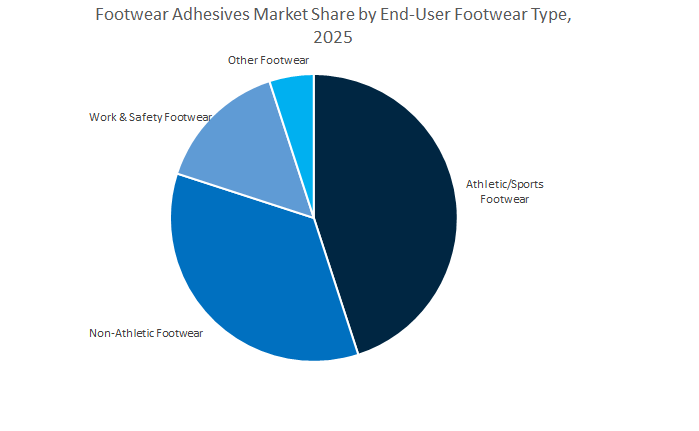

The athletic and sports footwear segment dominates the global footwear adhesives market, with a projected 45.4% share in 2025, reflecting the industry’s reliance on multi-material bonding technologies to support high-performance shoe construction. Sports footwear manufacturing demands strong, flexible, and lightweight adhesive systems that can bond EVA, mesh, rubber, and TPU substrates while withstanding repetitive stress, flexing, and moisture exposure. The surge in global fitness culture, along with the expansion of athleisure and performance-driven footwear lines, continues to boost adhesive demand. Leading global brands are prioritizing water-borne and reactive polyurethane adhesives for enhanced sustainability and product durability. Additionally, the rise of automated, precision-based manufacturing in Asia-Pacific is encouraging wider use of hot melt and reactive adhesives for faster cycle times and reduced defect rates. As innovations in midsole foams, cushioning systems, and breathable fabrics expand, the need for advanced adhesives with specific elasticity and heat resistance profiles continues to grow.

The non-athletic footwear segment maintains a significant market position, driven by demand for casual, formal, and fashion footwear that requires reliable bonding solutions for diverse upper and sole materials, including leather, synthetic textiles, and polyurethane soles. This category benefits from the resurgence of handcrafted and premium shoe lines in both Western and Asian markets, where artisans and manufacturers prefer adhesives offering aesthetic precision and long-lasting flexibility. The growing influence of fast-fashion retail and premium footwear brands has prompted adhesive producers to deliver low-odor, quick-bonding, and non-yellowing formulations, particularly in dress shoes and lifestyle products.

Work and safety footwear forms another critical end-use segment characterized by rigorous performance, mechanical strength, and resistance requirements. Adhesives in this segment must withstand high temperatures, chemical exposure, and mechanical stress, making reactive polyurethane and solvent-based systems particularly relevant. The global industrial workforce expansion and rising construction and manufacturing activity are further stimulating this segment’s adhesive demand. Meanwhile, other footwear categories, including medical, orthotic, and specialty designs, represent niche but steadily expanding markets. These applications often require hypoallergenic, flexible, and lightweight adhesive solutions tailored for comfort, precision, and extended wear.

The competitive landscape of the global footwear adhesives industry is defined by the interplay between chemical innovation, digitalization, and sustainability leadership. Major players such as Henkel, Bostik (Arkema Group), Huntsman, and H.B. Fuller are prioritizing bio-based content, low-VOC waterborne technologies, and automated process integration to meet the evolving needs of global footwear manufacturers and brands.

Henkel leads the market with a focus on automated adhesive application systems and sustainable footwear bonding solutions. Its new-generation water-based polyurethane (PU) adhesives are designed for precision robotic dispensing with minimal waste. Henkel’s R&D centers in Germany and Asia collaborate closely with global sports and fashion brands to co-develop solvent-free, high-strength bonding systems. A key innovation includes “disassembly-on-demand” adhesives, engineered to release bonds safely for material recovery—aligning perfectly with the circular footwear economy.

Bostik maintains a leadership position through its hot-melt and thermoplastic adhesive portfolio, powered by proprietary Platamid® copolyamide and copolyester (CoPA/CoPES) technologies. These adhesives are solvent-free and ideal for toe and heel lasting, foam lamination, and upper reinforcement in sports and fashion footwear. Its Asia-Pacific expansion strategy ensures regional supply resilience and technical support for mass manufacturers. By offering plasticizer-free hot-melt adhesives, Bostik supports both energy-efficient and VOC-free production goals.

Huntsman stands at the forefront of circular footwear materials, driven by its revolutionary SMARTLITE® O Liquid Thermoplastic Polyurethane (LTPU) system. The LTPU allows direct casting of midsoles with ≥50% rebound performance, removing the need for traditional molding methods. This innovation facilitates material recyclability, enabling used soles to be reground and reused in new footwear production. In partnership with framas Group, Huntsman is scaling up LTPU production to support millions of soling units annually—integrating sustainability with scalability.

H.B. Fuller combines high-performance adhesive technology with sustainability. Its polyolefin- and rubber-based hot-melt adhesives offer superior initial tack and temperature resistance, vital for sole-to-upper bonding in extreme environments. The company has expanded its reactive hot-melt polyurethane (HMPUR) line to deliver cross-linked durability and long-term adhesion. Fuller’s next-generation water-based polychloroprene adhesives provide solvent-free alternatives that maintain comparable performance levels, supporting safer, more sustainable manufacturing practices across industrial, protective, and sports footwear applications.

The United States footwear adhesives market is evolving through sustained innovation in bio-based, waterborne, and thermoplastic polyurethane (TPU) adhesives, particularly for athletic and performance footwear. Companies such as Covestro are pioneering Desmomelt® U adhesive systems, enabling automated, 2D digital printing applications that optimize precision and efficiency in sneaker sole bonding. The innovation aligns with broader trends in Industry 4.0 manufacturing, allowing adhesive application to integrate seamlessly with robotic and digital production lines in footwear assembly.

The U.S. market’s sustainability focus has led to a surge in vegan synthetic coating systems and non-toxic TPU materials, supporting a transition to eco-friendly non-leather footwear. Covestro’s Platilon® H2 CQ EC film, a partially bio-based hot melt adhesive, demonstrates equivalent heat resistance and bonding strength compared to conventional grades, meeting growing demand for sustainable high-end footwear adhesives. Furthermore, initiatives like the BOOTS Act, mandating domestically made combat boots for military use, are driving investment in durable, structural bonding solutions that meet defense-grade specifications.

The U.S. Footwear Manufacturers Association (USFMA) has expanded its membership to include advanced machinery and adhesive material companies, signifying a concerted push to strengthen domestic production capacity. Research into smart footwear adhesives — capable of integrating bio-sensors and printed circuits on TPU films — reflects the growing crossover between adhesive science and wearable electronics, positioning the U.S. as a global leader in functional and sustainable adhesive development for the footwear industry.

China remains the largest global hub for footwear adhesive production and consumption, driven by its unmatched manufacturing scale and rapidly evolving green chemistry regulations. The government’s “2025 Action Plan for Stabilizing Foreign Investment” actively supports foreign manufacturers in sectors such as polyurethane, hot melt, and reactive adhesive technologies, facilitating collaborations that strengthen the domestic supply chain.

China’s tightening environmental laws and emissions standards have accelerated the market shift from solvent-based to low-VOC, waterborne, and solvent-free adhesives. The enforcement of national policies like GB 18584-2024 (for emission caps on interior materials) and broader pollution-control frameworks increases the operational cost of legacy adhesive systems, compelling companies to pivot toward compliant eco-friendly formulations.

The country’s urbanization and infrastructure megaprojects, coupled with continued growth in the textile, apparel, and footwear export sectors, sustain massive baseline demand for polyurethane-based adhesives. Domestic producers are rapidly localizing advanced polymer and polyurethane reactive (PUR) technologies, ensuring cost-effective production for both global and regional footwear brands. The booming e-commerce and fast fashion industries have also intensified the need for rapid curing adhesives, enabling faster, automated production lines to meet real-time consumer demand. Overall, China’s combination of scale, compliance, and technological adaptation keeps it at the core of global footwear adhesive supply and innovation.

Vietnam continues to expand its role as one of the world’s largest footwear exporters, attracting Foreign Direct Investment (FDI) from global brands and adhesive manufacturers seeking low-cost, high-efficiency production environments. The market’s growing sophistication, supported by mega-factory investments from companies such as Pou Chen Group and Hong Fu Group, directly correlates with increased procurement of premium footwear adhesives suitable for synthetic, athletic, and lifestyle footwear.

Recent Free Trade Agreements (FTAs) — including the EU-Vietnam Free Trade Agreement (EVFTA), Comprehensive and Progressive Agreement for Trans-Pacific Partnership (CPTPP), and Regional Comprehensive Economic Partnership (RCEP) — have elevated compliance expectations, driving the adoption of certified low-VOC and REACH-compliant adhesives. Vietnam’s Law on Environmental Protection (2020) mandates sustainable production standards, pushing local factories to substitute solvent-based adhesives with PUR and water-based alternatives that meet EU environmental export criteria.

A growing skilled workforce, combined with enhanced automation and dispensing system infrastructure, supports consistent application of hot melt and reactive adhesives in industrial-scale footwear production. As global brands increasingly view Vietnam as a resilient manufacturing base, demand for advanced adhesive chemistries — balancing performance, speed, and sustainability — is expected to surge, reinforcing the country’s reputation as an export-oriented footwear adhesives powerhouse in Asia-Pacific.

Germany, at the center of Europe’s advanced adhesives and specialty chemical innovation, leads the transition toward sustainable, solvent-free, and recyclable adhesive systems for footwear applications. Stricter EU VOC and chemical emissions regulations are compelling manufacturers to develop formulations that comply with Ecolabel and REACH standards, setting the tone for eco-certified footwear adhesive production across the region.

Major European players such as Henkel AG & Co. KGaA have reinforced The transition through their AQUENCE line of water-based adhesives, designed to replace solvent-based alternatives in high-volume footwear manufacturing. Similarly, Jowat SE’s introduction of GROW bio-based hot melt adhesive technology expands the use of renewable materials in textile and leather bonding, reducing fossil fuel dependence. German innovation also extends into adhesive recyclability — developing materials compatible with circular economy practices that enable the disassembly and recycling of footwear components.

Collaborations between machinery manufacturers and adhesive formulators are resulting in the design of automated adhesive dispensing systems, improving precision and process efficiency. Germany’s high-end textile and bluesign®-certified material manufacturing sectors also drive the need for premium polyurethane and reactive adhesives that maintain flexibility and visual clarity in luxury and athletic footwear. The synergy of sustainability, automation, and high precision positions Germany as the benchmark for environmentally advanced adhesive innovation in the European footwear adhesives market.

Italy stands as the epicenter of luxury footwear adhesives innovation, catering to the needs of premium leather and fashion brands that demand aesthetics, durability, and material compatibility. Italian manufacturers specialize in non-staining polyurethane, EVA, and hot melt adhesive systems engineered for bonding sensitive natural leathers and synthetics without compromising softness or finish quality.

The Italian adhesives market benefits from a highly collaborative R&D environment, with partnerships between global chemical companies and specialized SMEs focusing on the customization of hybrid resins and flexible adhesive formulations for high-end shoes. The VAE/EVA adhesives segment has recorded steady growth, favored for its strong adhesion, lightweight properties, and adaptability across diverse footwear types.

Sustainability is becoming a defining element of the Italian luxury adhesive supply chain. Brands increasingly demand low-carbon, non-toxic adhesive systems aligned with ESG principles, reflecting consumer preferences for eco-conscious premium goods. With ongoing innovation in high-clarity polyurethane bonding and advanced finishing chemistries, Italy remains a leader in luxury-grade adhesive performance and environmental responsibility.

India has rapidly emerged as the second-largest global footwear producer, driven by favorable government policies and large-scale private investments. The announcement of ₹2,302 crores investment by Taiwan’s Pou Chen Group in Tamil Nadu (2024) exemplifies the growing international confidence in India’s manufacturing capacity, directly fueling the demand for high-quality footwear adhesives.

Initiatives such as ‘Make in India’, the Indian Footwear and Leather Development Programme (IFLDP), and 100% FDI allowance in footwear manufacturing are catalyzing local adhesive production and supply chain development. Regulatory moves by the Bureau of Indian Standards (BIS) aim to standardize adhesive performance and safety, aligning India with global export standards.

The non-leather footwear segment, accounting for over 90% of the domestic market, predominantly relies on synthetic, rubber, and technical fabric adhesives, driving demand for polyurethane and EVA-based adhesives. Fiscal reforms like GST rationalization on adhesives and footwear inputs are improving manufacturer margins, encouraging the adoption of premium, high-performance adhesive systems.

As infrastructure and technical manufacturing ecosystems expand, India’s focus on sustainability, cost-efficiency, and domestic innovation is transforming it into a major global supplier of footwear adhesive solutions tailored to both mass-market and premium export segments.

Footwear Adhesives Market Report Scope

Footwear Adhesives Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$2.9 Billion

|

|

Market Size (2034)

|

$4.3 Billion

|

|

Market Growth Rate

|

4.5%

|

|

Segments

|

By Resin Type (Polyurethane Adhesives, Solvent-Based Adhesives, Water-Based Adhesives, Hot Melt Adhesives, Reactive Adhesives, Other Adhesives), By Technology (Solvent-Borne, Water-Borne, Hot Melt, Other Technologies), By Footwear Application (Shoe Manufacturing, Shoe Repair/Aftermarket, Orthopedic Insole/Footwear, Athletic Shoe Bonding), By Material (Leather, Rubber, Fabric & Textile, Synthetic Materials, Plastics), By End-User Footwear Type (Athletic/Sports Footwear, Non-Athletic Footwear, Work & Safety Footwear, Other Footwear

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Henkel AG & Co. KGaA, H.B. Fuller Company, Sika AG, 3M Company, Dow Inc., Arkema S.A., Covestro AG, Huntsman Corporation, Jowat SE, Wacker Chemie AG, DuPont de Nemours, Inc., Pidilite Industries Ltd., BASF SE, Mitsubishi Chemical Holdings Corporation, Worthen Industries

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

By Chemistry / Resin Type

- Polyurethane Adhesives

- Solvent-Based Adhesives

- Water-Based Adhesives

- Hot Melt Adhesives

- Reactive Adhesives

- Other Adhesives

By Technology

- Solvent-Borne

- Water-Borne

- Hot Melt

- Other Technologies

By Footwear Application

- Shoe Manufacturing

- Shoe Repair/Aftermarket

- Orthopedic Insole/Footwear

- Athletic Shoe Bonding

By Material/Substrate

- Leather

- Rubber

- Fabric & Textile

- Synthetic Materials

- Plastics

By End-User Footwear Type

- Athletic/Sports Footwear

- Non-Athletic Footwear

- Work & Safety Footwear

- Other Footwear

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

- Henkel AG & Co. KGaA

- H.B. Fuller Company

- Sika AG

- 3M Company

- Dow Inc.

- Arkema S.A.

- Covestro AG

- Huntsman Corporation

- Jowat SE

- Wacker Chemie AG

- DuPont de Nemours, Inc.

- Pidilite Industries Ltd.

- BASF SE

- Mitsubishi Chemical Holdings Corporation

- Worthen Industries

*- List not Exhaustive

Research Coverage

Prepared by USDAnalytics, this report investigates the Global Footwear Adhesives Market with a rigorous focus on performance chemistry, sustainability compliance, and factory automation. It delivers analysis reviews of demand inflection across sports, fashion, and work/safety lines; highlights breakthroughs in low-VOC waterborne polyurethane (WBPU), reactive hot-melt (HMPUR), circular/recyclable bonding, and automation-ready rheologies (fast set, controlled open time); and decodes how brand RSLs, REACH/EPA rules, and factory digitalization are reshaping specification shortlists and total cost of ownership. With vendor benchmarking, price–performance corridors, and substrate compatibility playbooks (leather, EVA, TPU, meshes, foams), this report is an essential resource for materials managers, process engineers, and sourcing leaders seeking durable bonds, lower emissions, and higher line throughput in next-gen footwear manufacturing.

Scope Highlights

Segmentation:

- By Chemistry / Resin Type: Polyurethane Adhesives; Solvent-Based Adhesives; Water-Based Adhesives; Hot Melt Adhesives; Reactive Adhesives; Other Adhesives.

- By Technology: Solvent-Borne; Water-Borne; Hot Melt; Other Technologies.

- By Footwear Application: Shoe Manufacturing; Shoe Repair/Aftermarket; Orthopedic Insole/Footwear; Athletic Shoe Bonding.

- By Material/Substrate: Leather; Rubber; Fabric & Textile; Synthetic Materials; Plastics.

- By End-User Footwear Type: Athletic/Sports Footwear; Non-Athletic Footwear; Work & Safety Footwear; Other Footwear.

Geographic Scope: Analysis spans 25+ countries across North America, Europe, Asia Pacific, Latin America, the Middle East & Africa.

Time Frame: Historic data 2021–2024 and forecast data 2025–2034.

Companies: Analysis/profiles of 15+ companies (strategies, product roadmaps, sustainability posture, and recent moves).

Deliverables

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.