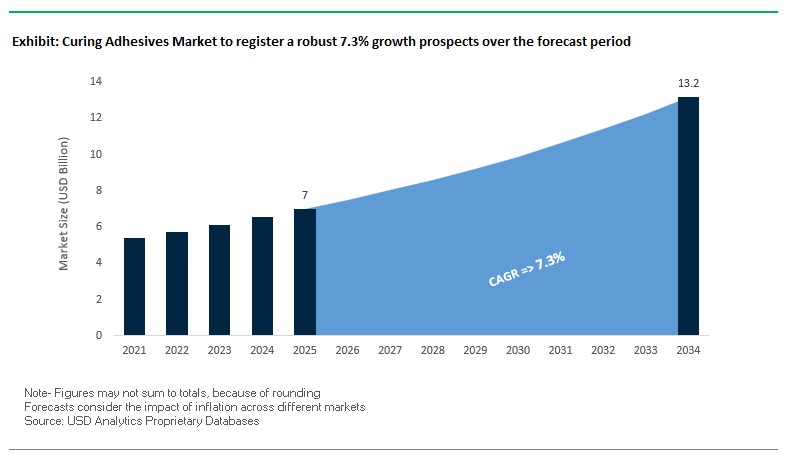

The curing adhesives market is estimated to expand from USD 7.0 billion in 2025 to USD 13.2 billion by 2034, reflecting a 7.3% CAGR as manufacturers standardize adhesive bonding within validated production architectures rather than treating it as an auxiliary process. The curing adhesives market has moved from a secondary joining solution to a core enabler of modern industrial manufacturing, driven by OEM requirements for lighter assemblies, higher structural integrity, and tighter process control. Across automotive, electronics, construction, and aerospace production lines, curing adhesives underpin critical load-bearing, sealing, and encapsulation functions where mechanical fastening and welding impose penalties on weight, design freedom, and cycle time. Epoxy, polyurethane, silicone, and acrylic systems have become integral to structural design because they enable predictable stress distribution, multi-material bonding, and durability under thermal and environmental cycling that legacy joining methods struggle to achieve at scale.

Demand is being structurally reshaped by OEM migration toward fast-cure, automation-compatible adhesive chemistries aligned with high-volume manufacturing and regulatory compliance. Two-component epoxy structural adhesives remain the reference standard for load-critical applications, delivering shear strengths in the 18–35 MPa range and peel strengths reaching 200 N/25 mm, which are routinely specified for aerospace fuselage bonding and automotive body-in-white and chassis assemblies. In parallel, UV- and LED-curing adhesives are redefining electronics manufacturing economics by reducing fixture times to under 10 seconds and achieving full cure within 60 seconds, directly supporting takt-time reduction in display assembly, sensor integration, and semiconductor packaging. These performance characteristics are not incremental; they enable line-speed increases, lower work-in-process inventory, and improved dimensional consistency in miniaturized and high-density electronic components.

Material substitution is accelerating as curing adhesives displace mechanical fasteners, solvent-based sealants, and high-temperature welding in applications where weight reduction, corrosion resistance, and process efficiency translate directly into cost and uptime advantages. Silane-terminated polymer and low-monomer polyurethane systems are gaining adoption as manufacturers respond to REACH and EPA requirements, reducing diisocyanate exposure while maintaining elastic recovery, adhesion durability, and long-term weathering performance. In electric vehicle manufacturing, curing adhesives are no longer optional—they are specified for battery module encapsulation, cell-to-pack bonding, and thermal interface management, maintaining functional integrity across operating ranges from –40 °C to 180 °C. Over the forecast period, manufacturing strategies will increasingly center on securing compliant raw material supply, qualifying faster-curing and automation-ready formulations, and aligning adhesive selection with OEM validation protocols to ensure scalability, regulatory alignment, and long-term production resilience.

The curing adhesives market is witnessing accelerated innovation and consolidation as major chemical and adhesive manufacturers invest in bio-safe formulations, LED-curable systems, and structural performance optimization.

In November 2025, INX Group Limited completed its acquisition of Coatings & Adhesives Corporation, forming INX International Coatings and Adhesives. The merger expands its product line into specialty curing adhesives for the packaging sector, combining coating expertise with high-performance bonding technologies to enhance sustainability and versatility.

A month earlier, in October 2025, H.B. Fuller Company announced the acquisition of GEM S.r.l. and Medifill Ltd., reinforcing its Medical Adhesive Technologies (MAT) portfolio. These acquisitions strengthen Fuller’s presence in cyanoacrylate chemistry and the healthcare adhesives market—particularly in tissue bonding and transdermal patch applications—where biocompatibility and precision curing are critical.

Meanwhile, Permabond launched UV6357 (September 2025), a cold-resistant UV-curable adhesive engineered for refrigeration and freezer applications, showcasing the increasing demand for adhesives with humidity and temperature resilience. In the same period, the German government (July 2025) implemented tighter handling regulations for polyurethane and epoxy systems, prompting industry leaders like Sika AG and Henkel to accelerate their shift to low-monomer and REACH-compliant formulations.

In May 2025, 3M Company extended its low-odor acrylic adhesive line with non-flammable, high-impact formulations aimed at transportation and industrial assembly. Similarly, Sika AG introduced its Purform® technology (March 2025)—a revolutionary polymer backbone that reduces free monomeric diisocyanate content while improving environmental and occupational safety compliance.

Dow Inc. (January 2025) expanded its silicone-based thermally conductive adhesive portfolio, scaling manufacturing of high-performance gap fillers (3.3 W/mK) for EV battery and power electronics thermal management. Finally, Henkel AG (November 2024) deepened its automotive collaboration pipeline by co-developing heat-curing epoxy adhesives with a major European Tier-1 OEM to improve multi-material bonding in EV body structures.

The demand for low-temperature curing adhesives has surged as industries prioritize energy-efficient, fast-curing, and substrate-protective bonding technologies. The transition is particularly pronounced in sectors like electronics assembly, optics, and biomedical devices, where thermal damage or prolonged curing cycles can compromise product integrity and manufacturing efficiency.

Data shows that Vinyl Acetate Ethylene (VAE) systems enhanced with Polyvinyl Alcohol (PVA) enable accelerated polymerization at reduced temperatures—cutting energy use and enabling faster line speeds. These low-temperature curing adhesives are fundamental to sustainable production models, where every kilowatt-hour saved translates to measurable reductions in operating cost and carbon footprint.

In electronics manufacturing, dual-cure adhesives combining UV and moisture or UV and thermal mechanisms have become the benchmark for precision bonding. They allow for instantaneous “snap-cure” fixation under UV light, followed by a secondary thermal or ambient cure that ensures complete polymerization in shaded regions—critical for assembling Printed Circuit Boards (PCBs), LEDs, and sensor arrays. The dual-curing innovation ensures consistent bond integrity while preventing warping or delamination in miniaturized, heat-sensitive assemblies.

The healthcare and biomedical device sector is witnessing similar momentum. Manufacturers are developing ISO 10993-tested, light-curable adhesives for biocompatible bonding of Thermoplastic Elastomers (TPEs), medical-grade plastics, and flexible substrates. These formulations not only ensure non-cytotoxic adhesion and long-term biostability but also comply with EU Medical Device Regulation (MDR) standards—cementing their role in critical applications such as wearable sensors, diagnostic cartridges, and catheter assemblies.

As sustainability becomes a global business imperative, the curing adhesives market is pivoting decisively toward bio-based raw materials, low-VOC formulations, and circular material sourcing. Stringent EPA and REACH regulations have accelerated the shift from solvent-heavy systems to environmentally safe curing adhesives that meet or exceed the performance of traditional petrochemical-based formulations.

Manufacturers are investing heavily in bio-based epoxy and polyurethane chemistries, which achieve mechanical and thermal performance comparable to conventional thermoset systems. These eco-friendly adhesives offer exceptional chemical resistance, high shear strength, and solvent durability, enabling adoption in automotive, electronics, and green construction. The performance parity is a pivotal breakthrough, proving that sustainability and performance are no longer mutually exclusive.

An emerging innovation frontier lies in industrial by-product utilization. Researchers are engineering formaldehyde-free adhesive systems derived from tannins, proteins, saccharides, and lignocellulosic biomass, effectively converting waste into value-added crosslinking feedstocks. The circular approach not only lowers the environmental footprint but also insulates manufacturers from fossil-derived raw material price volatility.

With growing demand from LEED-certified construction projects and sustainable packaging markets, the move toward low-carbon and renewable curing adhesives represents both a regulatory necessity and a competitive advantage.

The rapid commercialization of Flexible Hybrid Electronics (FHE) and wearable medical devices has created a critical niche for curing adhesives that combine mechanical flexibility, strong adhesion, and low curing temperatures. These adhesives are essential for applications where traditional soldering or thermal bonding could damage flexible substrates or micro-components.

Isotropic Conductive Adhesives (ICAs)—especially silver-epoxy formulations—are becoming the standard for roll-to-roll production of flexible circuits. Their ability to cure efficiently under low heat ensures compatibility with polymer films such as PET, PEN, and TPU, enabling continuous, automated fabrication of smart patches, OLED displays, and soft robotics.

Reliability under environmental stress remains a key performance metric. Thermal cycling experiments between −40°C and +125°C have demonstrated that Anisotropic Conductive Adhesives (ACAs) maintain electrical conductivity and mechanical adhesion over thousands of cycles, validating their robustness for harsh operating environments.

Manufacturers are also investing in polyurethane-based dual-cure systems with elongation-at-break values reaching 90% or more, allowing devices to bend, flex, and stretch without electrical discontinuity. These flexible curing systems are unlocking new possibilities for biomedical sensors, foldable displays, and next-generation IoT devices, where structural adaptability is a design imperative.

The explosive growth of electric vehicle (EV) production has created an equally large demand for advanced curing adhesives used in battery assembly, structural bonding, and thermal management systems. Adhesives in the segment must deliver exceptional thermal conductivity, vibration damping, and chemical stability while curing rapidly under high-volume production conditions.

In EV battery packs, Thermally Conductive Adhesives (TCAs) and gap fillers serve a dual role—providing mechanical stability and efficient heat transfer from cells to cooling structures. Commercial-grade polyurethane-based gap fillers achieve thermal conductivity values up to 3.1 W/m·K while maintaining low squeeze forces (<120 N), reducing stress on battery cells and improving process uniformity in automated dispensing systems.

Mechanical durability is equally critical. Two-part epoxy and polyurethane curing systems demonstrate cross-tensile strengths exceeding 10 MPa on aluminum substrates, ensuring long-term adhesion under severe vibration, impact, and thermal cycling conditions. The resilience directly enhances battery module integrity and extends service life in high-demand EV platforms.

Process efficiency represents another vital growth lever. Fast-curing silicone and hybrid adhesive systems that reach operational strength within 4–7 hours at room temperature are revolutionizing EV module manufacturing throughput. In addition, the introduction of low-abrasion filler technologies minimizes equipment wear in automated dispensing systems, reducing maintenance downtime—a major cost factor for mass-scale EV manufacturers.

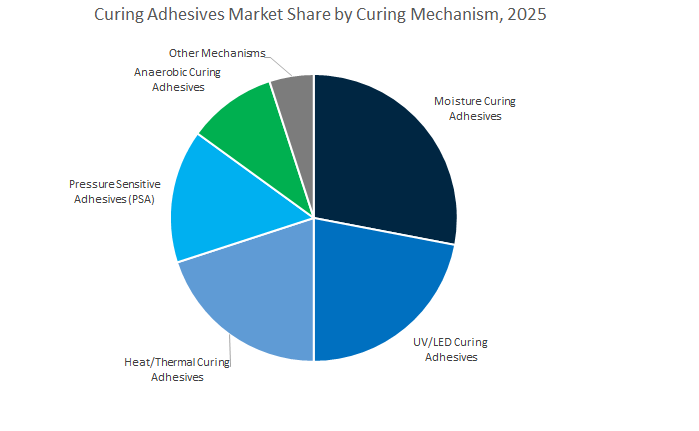

Curing Adhesives Market Share Insights, 2025-2034

Moisture-curing adhesives represent the largest segment in the global curing adhesives market, accounting for an estimated 28.9% share in 2025. Their dominance stems from their broad industrial applicability, excellent adhesion to dissimilar substrates, and environmental curing capability that eliminates the need for heat or light activation. Polyurethane- and silicone-based formulations are widely used across construction, automotive, and general industrial assembly, where they provide flexibility, gap-filling strength, and durability under varying humidity and temperature conditions. In construction, moisture-curing adhesives are indispensable for sealing joints, bonding panels, and waterproofing in both residential and infrastructure projects. Meanwhile, in automotive manufacturing, they are extensively employed in glass bonding, interior assembly, and EV battery sealing, where vibration resistance and long-term elasticity are critical. Their ability to form strong, weather-resistant bonds without additional curing equipment makes them a preferred choice for professionals seeking efficiency, reliability, and cost-effectiveness. The ongoing shift toward solvent-free and low-VOC moisture-cure formulations also aligns with tightening environmental regulations, further solidifying their market leadership.

UV/LED-Curing Adhesives Emerge as the Fastest-Growing Segment in Precision Manufacturing and Electronics

The UV/LED-curing adhesives segment holds a rapidly expanding share, projected at 22.5% in 2025, driven by its unmatched curing speed, accuracy, and adaptability to automated production lines. These adhesives are primarily used in electronics, optical components, and medical device assembly, where instant curing under light exposure allows for high throughput and minimal waste. Their single-component, solvent-free nature makes them highly desirable for cleanroom and microelectronic manufacturing environments, offering superior process control and environmental compliance. In electronics, they are vital for bonding glass, displays, and sensors, while in medical applications, they enable the assembly of catheters, syringes, and wearable devices under low-stress curing conditions that preserve material integrity. The rise of LED-curing systems—which offer energy efficiency and safer operation compared to traditional UV lamps—is accelerating adoption in precision industries. Additionally, the expansion of UV-cure adhesives compatible with flexible substrates and 3D-printed components is expanding their use into advanced manufacturing sectors, including photonics, semiconductors, and electric mobility systems.

Thermal-Curing and Anaerobic Systems Retain High-Performance Niches in Structural and Mechanical Applications

Thermal-curing adhesives, including epoxies, phenolics, and acrylics, hold a strong position in aerospace, automotive, and industrial electronics, where high temperature stability and mechanical strength are non-negotiable. They dominate structural bonding tasks such as metal-to-metal joining, composite assembly, and electronic potting, where superior chemical resistance and load-bearing capabilities are required. Thermal-cure systems are integral to Body-in-White (BIW) automotive structures, aerospace fuselage bonding, and semiconductor encapsulation, offering the performance necessary for extreme service conditions. Anaerobic adhesives, On the other hand, are specialized in mechanical assembly applications like threadlocking, retaining, and sealing in the automotive, machinery, and energy sectors. They cure in the absence of air and in the presence of metal ions, creating durable bonds that resist vibration, temperature fluctuation, and corrosion. These segments, though smaller in volume, represent high-value, mission-critical applications that demand precision-engineered chemistry for structural reliability and longevity.

Pressure-Sensitive Adhesives (PSAs) Maintain Vital Roles in Instant-Bonding Applications Across Industries

Pressure-sensitive adhesives form a distinct category within the curing adhesives market, providing instant adhesion without external curing. PSAs are foundational to the tape, label, and film industries, where immediate tack, removability, and conformability are key. They are widely used in construction masking, electronics assembly, packaging, and medical products, including wound dressings and wearable sensors. The shift toward acrylic and silicone-based PSAs with improved heat and UV resistance is expanding their functionality into demanding industrial applications. Their ease of use, low waste generation, and reworkability make PSAs a cornerstone of modern adhesive applications, especially in high-speed manufacturing lines that require reliability and productivity.

The electronics and electrical sector dominates the curing adhesives market, accounting for 25.6% of global share in 2025. Rapid technological evolution in consumer electronics, semiconductors, and advanced packaging has created a sustained demand for adhesives with precise curing control, high thermal conductivity, and dielectric stability. UV/LED and thermal-curing adhesives are critical for bonding delicate components like IC chips, PCBs, sensors, and displays, where traditional soldering is unsuitable. The miniaturization of devices and the rise of 5G, IoT, and wearable technologies have pushed manufacturers to adopt low-temperature, fast-curing adhesives that ensure high reliability and electrical performance. Furthermore, the proliferation of electric vehicles (EVs) and battery systems has amplified the need for conductive, thermally stable adhesives capable of withstanding harsh environmental conditions. This sector’s innovation-driven nature makes it a cornerstone of technological advancement within the curing adhesives market.

Automotive and Construction Segments Represent Major Pillars of Demand Across Structural and Sealing Applications

The automotive and transportation industry represents one of the largest and most diversified end-use sectors, utilizing almost every curing mechanism—heat-cure for structural bonding, moisture-cure for glass and trim assembly, and anaerobic for fasteners and mechanical retention. Adhesives are essential to modern vehicle design, enabling lightweighting, noise reduction, and electric powertrain efficiency. The transition to electric mobility further boosts demand for adhesives that can withstand thermal shock, vibration, and electrical load, particularly in battery module assembly and EV chassis bonding. In parallel, the construction and infrastructure industry is a major volume driver, heavily relying on moisture-curing and polyurethane-based adhesives for panel bonding, flooring, tiling, and waterproofing applications. The global emphasis on energy-efficient, green building materials and low-VOC formulations continues to accelerate adoption in this sector, particularly in renovation and retrofitting projects.

The curing adhesives market is highly consolidated, dominated by global leaders including Henkel AG, Sika AG, H.B. Fuller, 3M Company, and Dow Inc., each leveraging material innovation, sustainability focus, and strategic acquisitions to secure long-term leadership.

Henkel, through its Loctite® and Teroson® brands, leads the curing adhesives industry with advanced epoxy, polyurethane, and silicone solutions for aerospace, automotive, and electronics. Its two-component epoxy systems ensure unmatched shear strength and fatigue resistance in structural joints, while thermally conductive adhesives support ADAS and under-hood electronics. Henkel’s innovations in metal pretreatment have reduced automotive manufacturing steps from seven to four, cutting costs and enhancing sustainability. The company’s ongoing R&D emphasizes lightweighting, electrification, and sustainability in line with global EV trends.

Sika remains a technology leader in polyurethane and STP curing adhesives, widely adopted under its Sikaflex® and SikaTack® brands for construction and automotive applications. Its Purform® technology represents a major advancement in low-monomer chemistry, delivering both superior mechanical performance and REACH compliance. Sika also dominates in segmental bridge bonding and composite structures, using Sikadur® epoxy and SikaPower® crash-durable adhesives. The company’s expansion of STP-based sealants offers enhanced adhesion, paintability, and moisture-curing flexibility for diverse substrates.

H.B. Fuller is investing aggressively in UV and light-cure technologies, positioning itself as a key player in medical and electronics bonding applications. Through the acquisition of GEM S.r.l. and Medifill Ltd., it reinforced its Medical Adhesive Technologies (MAT) business, targeting suture alternatives and medical device assembly. Fuller’s diverse product portfolio includes cyanoacrylates, reactive hot melts, and polyurethane adhesives, catering to fast-curing, low-temperature applications. Its innovation in miniaturized electronics bonding provides competitive advantages in precision assembly and production efficiency.

3M is a global leader in structural acrylic and multi-material bonding adhesives. Its Scotch-Weld™ portfolio provides high shear and peel strength for transportation and metal fabrication, reducing the need for welding or riveting. 3M’s low-odor, non-flammable formulations are ideal for cold-temperature assembly and worker-safe environments. The company also offers specialized plastic adhesives (DP8010) for low-surface energy (LSE) materials, enhancing design flexibility for automotive and industrial OEMs.

Dow Inc., under its DOWSIL™ brand, is a global pioneer in silicone-based curing adhesives, emphasizing thermal management, flexibility, and reliability in extreme environments. Its thermally conductive adhesives and gap fillers (up to 3.3 W/mK) are vital for EV batteries and power electronics. Dow’s one- and two-part neutral-cure silicone adhesives also support Formed-in-Place Gaskets (FIPG) and structural glazing applications. With railway-approved products like DOWSIL™ 7091, the company continues to dominate high-temperature, vibration-prone, and safety-critical sectors.

The United States curing adhesives market continues to dominate the global landscape, supported by technological innovation, large-scale industrial automation, and an increasing shift toward sustainable adhesive chemistries. Wacker Chemical Corporation’s introduction of hybrid thermally conductive adhesives (TCA) at The Battery Show North America 2025 underscores the market’s focus on EV battery efficiency and heat management. The Adhesives and Sealants Council (ASC) reports that manufacturers are integrating AI-driven 3D vision systems capable of inspecting micro-beads on assembly lines, ensuring precision in automated bonding operations.

Henkel’s facility expansion in South Dakota (2025) marks a major investment in high-performance structural adhesives catering to automotive and aerospace customers demanding fast-curing, high-strength bonding for automated processes. Simultaneously, 3M Company continues to push innovation boundaries with next-generation structural adhesives engineered to meet aerospace-grade thermal and mechanical requirements. The innovations align with the U.S. market’s preference for rapid-curing, durable, and lightweight solutions, ideal for both electric vehicle manufacturing and defense applications.

Germany remains a pivotal hub in the European curing adhesives market, leveraging its leadership in precision engineering, chemical formulation, and regulatory compliance. Henkel AG & Co. KGaA expanded its medical adhesive portfolio in 2025 with the launch of Loctite AA 3952 and Loctite SI 5057, light-curable adhesives tailored for flexible medical device assembly, supporting the global trend toward wearable medical electronics.

The EU diisocyanate restriction (August 2023) continues to reshape the regional adhesive ecosystem, prompting the transition toward zero-isocyanate, UV-curable, and waterborne adhesive systems. German manufacturer DELO Industrie Klebstoffe GmbH & Co. KGaA has introduced dual-curing UV adhesives for complex electronics, offering both primary UV and secondary thermal curing to improve bonding in shadowed microstructures. Investment in carbon-neutral production and digital supply chain optimization further reinforces Germany’s standing as a sustainability benchmark within the curing adhesives industry.

China’s curing adhesives industry is expanding at record speed, supported by rapid industrialization, EV market leadership, and government-backed R&D initiatives. The Ministry of Industry and Information Technology (MIIT) has prioritized high-performance adhesives for new energy vehicles (NEVs) and advanced electronics, prompting both domestic and multinational producers to increase R&D and manufacturing capacity.

International chemical companies are scaling up UV-curable and epoxy resin adhesive production to meet growing demand from electronics and packaging manufacturers, while government-funded infrastructure projects continue to drive consumption of moisture-curing structural adhesives in civil construction and exterior cladding. Local firms are innovating to reduce dependency on imports by producing high-strength, heat-resistant adhesives tailored for EVs, smart devices, and energy systems. The localization push supports China’s broader aim of achieving chemical self-reliance and green industrial growth.

Japan’s curing adhesives market remains at the forefront of precision bonding solutions, particularly for microelectronics, automotive, and industrial machinery. Leading firms such as Three Bond Co. Ltd. are innovating high-temperature-resistant curing adhesives designed for demanding environments like automotive engines and heavy industrial equipment.

R&D initiatives are emphasizing miniaturized, low-outgassing adhesives for display panels, semiconductors, and optical sensors, aligning with Japan’s global leadership in high-end electronics. Despite The technological prowess, Japanese manufacturers maintain a pragmatic approach to adoption, balancing cost and performance by favoring proven mid-range formulations over untested high-cost alternatives. Additionally, growing emphasis on humidity-stable packaging and storage solutions ensures consistent adhesive performance under Japan’s diverse climatic conditions.

South Korea’s curing adhesives industry is expanding rapidly, driven by its world-class battery, semiconductor, and display manufacturing sectors. Major domestic producers are investing in thermally conductive and epoxy-based adhesives to improve battery safety and longevity amid the nation’s aggressive EV transition strategy. R&D efforts are increasingly centered on adhesives compatible with flexible electronics, wearables, and OLED displays, where ultra-thin, heat-dissipative bonding materials are critical.

Industrial players are also prioritizing cost optimization through bulk purchasing and long-term supply agreements, given tight margins in consumer electronics assembly. The Korean government is actively supporting collaborative R&D initiatives between academia and industry to develop next-generation silicone and epoxy curing systems optimized for EV batteries and hydrogen fuel cell components.

India’s curing adhesives market is entering a phase of accelerated growth, powered by industrialization, infrastructure investment, and domestic manufacturing incentives. The ‘Make in India’ initiative and related production-linked incentives (PLI) are encouraging multinational adhesive manufacturers to localize production and expand R&D centers in the country.

The rise in automotive and packaging production is boosting demand for UV-curable coatings and adhesives, which deliver fast curing and energy efficiency—critical in India’s high-volume manufacturing environment. Simultaneously, construction and infrastructure development projects across metropolitan areas are driving the adoption of weather-resistant, moisture-curing adhesives for residential, commercial, and industrial applications. With increasing consumer awareness and environmental regulation, manufacturers are prioritizing low-VOC, sustainable adhesive solutions that align with India’s evolving green building standards.

Curing Adhesives Market Report Scope

Curing Adhesives Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$7 Billion

|

|

Market Size (2034)

|

$13.2 Billion

|

|

Market Growth Rate

|

7.3%

|

|

Segments

|

By Curing Mechanism (UV/LED Curing Adhesives, Moisture Curing Adhesives, Heat/Thermal Curing Adhesives, Anaerobic Curing Adhesives, Pressure Sensitive Adhesives), By Resin Type (Epoxy, Polyurethane, Acrylate, Silicone, Cyanoacrylate), By End-User (Electronics & Electrical, Automotive & Transportation, Medical Devices & Healthcare, Construction & Infrastructure, Aerospace & Defense, Woodworking & Furniture), By Formulation (Solvent-based, Water-based, 100% Solids

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Henkel AG & Co. KGaA, 3M Company, H.B. Fuller Company, Sika AG, The Dow Chemical Company, Wacker Chemie AG, Dymax Corporation, DELO Industrie Klebstoffe GmbH & Co. KGaA, Bostik, Master Bond Inc., Permabond Engineering Adhesives, Three Bond Co. Ltd., Ashland Global Holdings Inc., Shin-Etsu Chemical Co., Ltd., Huntsman Corporation

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

By Curing Mechanism

- UV/LED Curing Adhesives

- Moisture Curing Adhesives

- Heat/Thermal Curing Adhesives

- Anaerobic Curing Adhesives

- Pressure Sensitive Adhesives

By Resin Type

- Epoxy

- Polyurethane

- Acrylate

- Silicone

- Cyanoacrylate

By End-Use Industry

- Electronics & Electrical

- Automotive & Transportation

- Medical Devices & Healthcare

- Construction & Infrastructure

- Aerospace & Defense

- Woodworking & Furniture

By Formulation

- Solvent-based

- Water-based

- 100% Solids

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

- Henkel AG & Co. KGaA

- 3M Company

- H.B. Fuller Company

- Sika AG

- The Dow Chemical Company

- Wacker Chemie AG

- Dymax Corporation

- DELO Industrie Klebstoffe GmbH & Co. KGaA

- Bostik

- Master Bond Inc.

- Permabond Engineering Adhesives

- Three Bond Co. Ltd.

- Ashland Global Holdings Inc.

- Shin-Etsu Chemical Co., Ltd.

- Huntsman Corporation

*- List not Exhaustive

Research Coverage

Prepared by USDAnalytics, this report investigates the Global Curing Adhesives Market, connecting chemistry, curing physics, and manufacturing productivity to real-world outcomes in automotive, electronics, construction, medical, and aerospace value chains. It delivers analysis reviews on strength-to-weight gains, fixture-time reductions, dielectric/thermal reliability, and end-use qualification, surfaces breakthroughs in dual-cure (UV+moisture/thermal) systems, low-monomer polyurethane and STP platforms, and thermally conductive silicone gap-fillers, and highlights regulatory-ready pathways (REACH/EPA/VOC) that de-risk scale-up. Marrying technical scorecards with cost-in-use analytics and competitive positioning, this report is an essential resource for CTOs, R&D formulators, process engineers, sourcing leaders, and investors seeking evidence-based strategies for structural bonding, fast-cure electronics assembly, and sustainable, high-throughput manufacturing.

Scope Highlights

Segmentation:

- By Curing Mechanism: UV/LED Curing Adhesives; Moisture Curing Adhesives; Heat/Thermal Curing Adhesives; Anaerobic Curing Adhesives; Pressure Sensitive Adhesives.

- By Resin Type: Epoxy; Polyurethane; Acrylate; Silicone; Cyanoacrylate.

- By End-Use Industry: Electronics & Electrical; Automotive & Transportation; Medical Devices & Healthcare; Construction & Infrastructure; Aerospace & Defense; Woodworking & Furniture.

- By Formulation: Solvent-based; Water-based; 100% Solids.

Geographic Scope: Analysis spans 25+ countries across North America, Europe, Asia Pacific, Latin America, the Middle East & Africa.

Time Frame: Historic data 2021–2024 and forecast data 2025–2034.

Companies: Analysis/profiles of 15+ companies covering portfolios, M&A, regional capacity, and innovation pipelines.

Deliverables

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.