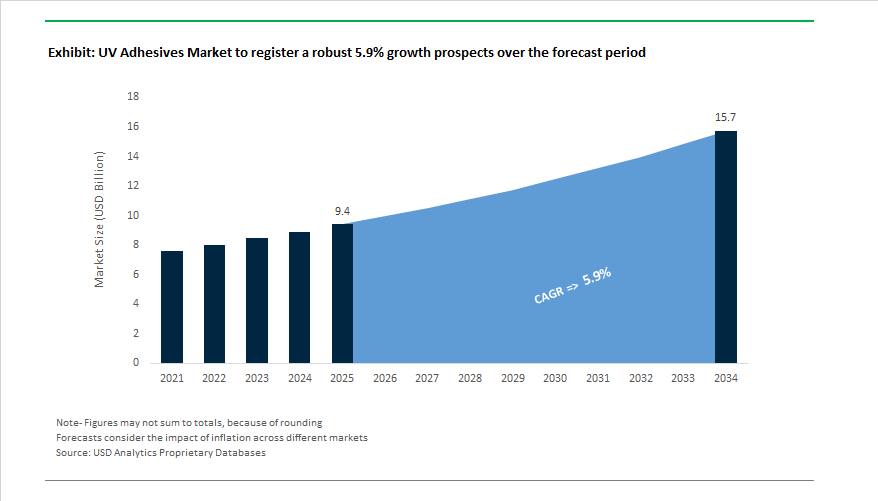

The Global UV Adhesives Market is projected to rise from USD 9.4 billion in 2025 to USD 15.7 billion by 2034, at a CAGR of 5.9%, as ultraviolet (UV) and UV-LED curable chemistries become essential materials in high-precision manufacturing environments that demand instant cure, low thermal impact, and low-VOC performance. UV adhesives are increasingly specified not as secondary bonding agents, but as production-critical materials in sectors where productivity, thermal control, and regulatory alignment matter — most notably electronics, medical devices, automotive assembly, optics, and advanced packaging.

Market expansion is anchored in rapid adoption of UV-LED curing equipment and chemistry synergies, which offer lower heat input and precise energy delivery to initiate polymerization across UV-reactive resin systems such as acrylics, epoxies, and silicones. LED-optimized UV adhesives mitigate substrate heat sensitivity and expand substrate compatibility, enabling bonding on plastics, glass, metals, and composites without damage to electronic or optical components — a capability emphasized by UV adhesive portfolios from major suppliers including 3M, Henkel, H.B. Fuller, Dymax, and DELO Industrial Adhesives that pair resin systems with matched curing parameters.

Electronics manufacturing remains the largest end-use driver, accounting for roughly 40% of UV adhesive deployment as assembly moves toward smaller form factors, tighter tolerances, and higher throughput. UV-curable systems are widely used in display bonding, sensor encapsulation, and PCB lamination where instant curing under controlled wavelengths improves yield and minimizes thermal stress on sensitive substrates. Photoinitiator and polymer advances — such as those available in specialized resin lines — have enhanced adhesion strength, chemical resistance, and cure depth, which are prerequisites for long-term reliability in high-density electronic assemblies.

Market Analysis: LED-Optimized UV Chemistries, Medical Compliance, and Yield-Critical Semiconductor Applications

The UV adhesives market is increasingly defined by process control, regulatory alignment, and yield sensitivity, rather than cure speed alone. In October 2025, DELO’s UV process breakthrough for Fan-Out Wafer-Level Packaging (FOWLP) underscored this shift by demonstrating that curing profiles and light-engine design are now yield-critical variables. By addressing wafer warpage and die shift through tightly controlled UV exposure, DELO effectively linked adhesive formulation, photoinitiator response, and irradiation hardware to semiconductor manufacturing outcomes—positioning UV adhesives as process-enabling materials in advanced packaging rather than interchangeable bonding agents. This development reflects broader industry recognition that UV systems must be co-optimized with equipment to meet sub-micron alignment and thermal distortion constraints.

Medical device manufacturing is reinforcing a parallel, regulation-driven evolution. In September 2025, Henkel (Loctite) introduced LED-curable flexible and rigid UV adhesive grades (AA 3951 and AA 3953) explicitly designed for smaller, safer medical devices, aligning formulation choices with tightening biocompatibility and device safety expectations. This followed January 2025 launches of AA 3952 and SI 5057, which addressed a persistent industry bottleneck: reliable bonding of difficult thermoplastic elastomers (TPEs) under EU MDR requirements.

Capacity investment and portfolio consolidation further illustrate how manufacturers are positioning for scale and resilience. 3M’s expansion of its Valley, Nebraska facility in May 2025, while publicly centered on personal safety products, reflects the type of upstream capacity reinforcement that supports high-volume UV-cured acrylic tapes and industrial adhesive supply across multiple end markets. At the same time, portfolio breadth and M&A activity are reshaping competitive positioning. The November 2024 acquisition of Coatings & Adhesives Corporation by INX Group, forming INX International Coatings & Adhesives, strengthened UV-curable inks and coatings capabilities for packaging—tightening integration between adhesives, coatings, and print technologies. On the product innovation front, Permabond’s May 2024 launch of UV643—capable of sub-second curing on rigid plastics and plastic-to-metal assemblies—highlighted continued demand for ultra-fast cycle times in automated manufacturing.

Market Trend 1: Widespread Adoption of Dual-Cure and Shadow-Cure Formulations for Complex Electronics and Automotive Applications

The increasing intricacy of electronic assemblies—from ADAS sensors in automotive systems to wearable medical devices and miniaturized sensors—is propelling the market toward dual-cure UV adhesives. These advanced materials combine UV light curing with a secondary thermal or moisture cure, ensuring complete polymerization even in shadowed or opaque areas where UV light penetration is limited.

A significant milestone in the domain came in November 2023, when Master Bond introduced a dual-cure epoxy capable of achieving a UV-cure in just 20–30 seconds, followed by a secondary heat cure to ensure total crosslinking. The innovation enables manufacturers to achieve 100% bond-line reliability in complex multi-layered electronic devices, including camera modules, micro-lenses, and circuit assemblies.

In the automotive sector, the proliferation of Advanced Driver-Assistance Systems (ADAS) and in-vehicle display systems is accelerating demand for dual-cure UV silicones, offering both rapid fixture time and exceptional thermal and chemical resistance. These adhesives ensure high-strength bonding in under-hood environments, combining speed, durability, and environmental sealing performance.

The trend is reinforced by advances in multi-wavelength UV LED curing systems—like Permabond’s UV643 (launched in May 2024)—that operate across 365–420 nm, enabling reliable curing through UV-stabilized plastics and thick substrates. The integration of dual-cure processes and multi-wavelength curing technologies allows manufacturers to reduce cycle time and enhance throughput, especially in high-density electronic assemblies and optical modules.

Market Trend 2: Surge in Low-Migration, Biocompatible UV Adhesives for Medical Device Manufacturing

With the tightening of ISO 10993 and USP Class VI regulatory standards, the UV adhesives market is rapidly advancing toward biocompatible, low-leachable formulations tailored for medical and healthcare applications. These adhesives are integral to the assembly of syringes, catheters, diagnostic equipment, and wearable sensors, where patient safety and device sterilization compatibility are paramount.

Leading producers of medical-grade UV-curable acrylates provide USP Class VI-certified formulations, affirming the absence of cytotoxicity and ensuring compliance for Class II and III medical devices. These adhesives feature ultra-low residual monomer and photoinitiator content—typically below 0.01 mg/kg for aromatic amines—significantly reducing leachables that could compromise patient safety.

The market gained momentum in January 2025, when Henkel introduced advanced UV adhesives designed specifically for flexible medical devices and wearable biosensors, ensuring strong adhesion under repeated motion while being compatible with ethylene oxide and gamma sterilization.

Further, UV-curing adhesives are revolutionizing needle bonding in disposable medical products, offering instant curing in seconds and enabling continuous high-speed manufacturing of syringes and infusion sets. The evolution not only enhances production efficiency but also aligns with global healthcare manufacturing automation trends.

Market Opportunity 1: Development of High-Refractive-Index UV Adhesives for Optical, LiDAR, and AR/VR Systems

The rapid growth of autonomous vehicles, augmented reality (AR), and virtual reality (VR) is creating an expanding high-value market for optically clear adhesives (OCAs) with high refractive index (RI) properties. These specialized UV adhesives are essential for precision bonding in LiDAR modules, optical sensors, and display lenses, where light transmission efficiency is mission-critical.

Technical advancements allow UV-curable optical adhesives to achieve refractive indices ranging from 1.5 to over 1.9, effectively minimizing light scattering and reflection losses. Such performance is indispensable for maintaining optical clarity in AR/VR waveguides, micro-displays, and advanced camera lenses.

For automotive LiDAR systems, high-RI UV adhesives ensure precise optical alignment, preventing signal loss and maintaining sub-millimeter detection accuracy—critical for autonomous navigation and collision avoidance technologies.

In AR/VR device assembly, manufacturers demand adhesives that deliver >99% visible light transmission post-cure while maintaining micro-level bond-line thickness (BLT). The implementation of fast-curing UV adhesives in these optical systems enables high-precision alignment and reduced cycle times, paving the way for mass-market scalability of immersive technologies.

Market Opportunity 2: Expansion of Sustainable and Bio-Based UV Adhesives for Circular Packaging and Consumer Goods

As global industries pivot toward sustainable manufacturing and Extended Producer Responsibility (EPR) compliance, the UV adhesives sector is witnessing a new frontier in bio-based and recyclable adhesive systems. These eco-conscious formulations enable manufacturers to meet Net-Zero carbon goals while maintaining the performance reliability expected from industrial-grade UV-curable adhesives.

In November 2024, a leading manufacturer introduced a bio-based instant adhesive with 60% renewable content, derived from natural raw materials. The milestone represents the transition from petroleum-based chemistry to renewable polymer backbones, supporting sustainable manufacturing in consumer packaging and labeling.

Additionally, bio-based hot-melt UV adhesives tailored for the packaging sector have achieved over 60% CO₂ emission reductions, as documented in life-cycle assessments (LCA), showcasing their direct contribution to corporate carbon footprint reduction and ESG compliance.

Regulatory frameworks like EPR and EU Green Deal mandates further drive demand for recyclable adhesive systems compatible with mono-material packaging—particularly HDPE and PET substrates. Recent product launches in 2024 feature certified organic contents exceeding 45%, mineral oil-free formulations, and high bonding strength, enabling brand owners to align with circular economy goals while maintaining packaging performance.

UV Adhesives Market Share Insights, 2025-2034

Market Share by End-Use Industry

The Electronics sector represents the dominant share of the global UV adhesives industry, accounting for a projected 38.6% market share in 2025. This leadership is driven by the increasing demand for fast-curing, high-precision bonding technologies across modern electronic applications such as display assembly, camera modules, PCB potting, and lens alignment. The continuing trend toward miniaturization, thinner displays, and multi-layered circuit designs amplifies the need for low-heat curing and optically clear adhesives, both hallmark advantages of UV-curable formulations. In the electronics manufacturing ecosystem, where speed, thermal sensitivity, and precision are paramount, UV adhesives offer unmatched curing speed, eliminating the need for extended heating processes and reducing cycle time. Their use has expanded from smartphones and tablets to 5G infrastructure, wearables, and automotive electronics, supported by the rising automation of assembly lines and demand for adhesives that cure on-demand for controlled production.

Beyond electronics, Medical Devices and Automotive stand out as the most dynamic growth sectors in the UV adhesives market. The medical industry’s adoption of UV-curable adhesives stems from their biocompatibility, transparency, and ability to form sterile, solvent-free bonds, meeting stringent regulatory and safety requirements for catheters, syringes, diagnostic devices, and wearable biosensors. The Automotive sector, meanwhile, is undergoing a technological revolution driven by electrification, advanced sensors, and LED lighting systems, all of which require high-performance UV adhesives with superior resistance to vibration, temperature fluctuations, and long-term environmental exposure. In particular, electric vehicle (EV) assembly and autonomous driving systems are pushing manufacturers toward precision bonding technologies that enable lightweight designs and electronic integration. Additional sectors such as Industrial Assembly, Packaging, and Aerospace contribute specialized, high-performance demand. In industrial assembly, UV adhesives are valued for rapid throughput and automation compatibility in line production. Packaging applications leverage UV-curable coatings and laminations for durable, high-gloss finishes and protective barriers, while the aerospace industry uses them for composite bonding, optical components, and display panels, where lightweight and precision-engineered materials are critical.

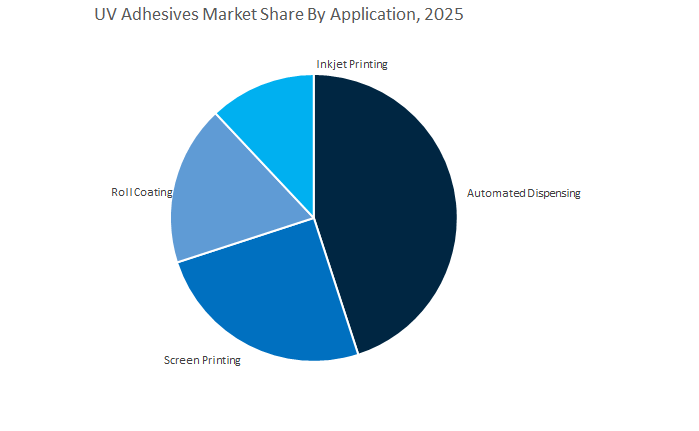

Market Share by Application Method

The Automated Dispensing segment holds the largest share of the global UV adhesives market, commanding a projected 44.9% share in 2025. This dominance reflects the increasing automation and precision required in advanced manufacturing processes—particularly in electronics, automotive, and medical device production—where UV adhesives are applied in micro-precise patterns under controlled conditions. Automated dispensing systems deliver consistent volume control, repeatability, and minimal waste, making them indispensable for large-scale manufacturing lines that prioritize speed, accuracy, and reliability. The integration of automated UV-curing equipment further enhances production efficiency, allowing for instant curing and reduced downtime, which is critical for continuous operations in high-output industries. As production systems transition toward Industry 4.0 standards, automated dispensing continues to lead adoption due to its compatibility with robotic assembly, vision-based alignment, and smart curing systems, particularly in microelectronics and electric vehicle component assembly.

Meanwhile, Screen Printing and Roll Coating methods retain substantial market presence, particularly in flat-surface bonding, decorative coatings, and flexible packaging applications. Screen printing remains a cornerstone for touch panel lamination, membrane switches, and optical films, where uniform adhesive layers and precision control are necessary for clarity and adhesion consistency. Roll coating, on the other hand, is central to high-speed continuous processes such as laminated film production, UV varnish coatings, and flexible circuit manufacturing, offering excellent scalability and surface uniformity. These conventional application techniques maintain strong relevance due to their mature technology base and cost-effectiveness in large-scale manufacturing environments. The Inkjet Printing segment, though currently the smallest, is emerging as the fastest-growing application method in the UV adhesives industry. It aligns perfectly with the industry’s shift toward digital manufacturing, customization, and additive processing. Inkjet-based UV adhesive application enables variable patterning, minimal waste, and localized deposition, making it ideal for prototyping, on-demand production, and micro-scale device assembly.

Competition centers on LED-first formulations, dual/secondary cure for shadowed joints, biocompatibility and MDR readiness, and application equipment ecosystems (dispensing, optics, motion). Vendors that pair materials + process hardware + validation data are winning specifications in electronics and med-tech while expanding into automotive semi-structural and UV-cured tapes/laminates.

Henkel offers 40+ ISO 10993-tested UV/light-cure products for medical, plus new LED-curables (Sep 2025) enabling smaller, safer device designs. The AA 3952 / SI 5057 launch (Jan 2025) targets TPE bonding under EU MDR. Beyond chemistry, Henkel supplies Loctite dispensing/curing/motion systems for process-capable lines, reducing validation time and variability in electronics and medical assembly.

Dymax’s light-curing leadership spans UV/Visible/LED materials, with patents like See-Cure™ (visual cure confirmation) and shadow-area strategies. It supplies halogen-free, RoHS-compliant conformal coatings/encapsulants with low ionic/outgassing for semiconductor & micro-assembly, validated against MIL-STD-883 / ASTM-E595—ideal for optics, sensors, and aerospace electronics.

3M leverages screen-printable UV-curing PSAs (e.g., SP7202) for fine-line graphics/displays and UV-cured acrylic foam tapes delivering high shear & heat resistance in automotive trim and BIW attachments. Capacity moves like the May 2025 Valley, NE expansion support high-volume supply. Focus on 100%-solids, solvent-free UV systems aligns with sustainability and line-speed targets.

DELO invests >15% of sales in R&D, pioneering DELO-DUALBOND (light-fix + secondary cure) for shadowed geometries. Its Oct 2025 fan-out packaging breakthrough mitigates warpage/die shift, signaling deep process-materials co-design with OSATs and IDMs. Sustainability efforts include low-energy UV bonding and bio-based raw-material pilots.

H.B. Fuller supplies acrylic-based UV adhesives across appliance, medical, and general industrial, with dual-cure options (secondary moisture/heat/anaerobic) to finish cures in shadowed bonds. The portfolio spans variable viscosities for jetting, needle, or film methods, targeting high-speed automation with thermal-cycling durability and impact resistance.

Master Bond focuses on high-T_g UV epoxies (e.g., T_g > 180 °C) for automotive electronics and industrial automation, USP Class VI-capable grades for demanding medical, and nanosilica-filled dual-cure systems (e.g., LED422DC90) for deep-section “side-bonding” and abrasion resistance. Strengths include chemical/solvent resistance for process-chemical exposure and harsh environments.

Country Analysis: Regional Developments Shaping the Global UV Adhesives Industry

United States – Pioneering UV Adhesive Innovation in Advanced Manufacturing and Electronics

The United States UV adhesives market is witnessing rapid innovation, driven by its dominance in electronics assembly, medical devices, and aerospace manufacturing. Companies like Dymax Corporation are spearheading sustainability initiatives—its May 2025 launch of TPO-free light-curable adhesives responds to the tightening environmental and regulatory landscape for photoinitiators and monomers. Master Bond’s dual-cure epoxy UV23FLDC-80TK, introduced in late 2023, showcases hybrid curing efficiency by enabling both rapid UV curing (within 30 seconds) and secondary heat curing for shadowed regions, particularly vital in complex electronics and sensor encapsulation.

Industry leaders such as 3M and Epoxy Technology, Inc. are expanding their portfolios in high-reliability UV-curable acrylics and epoxies tailored for wearable medical devices, aerospace electronics, and automotive sensors. Meanwhile, Permabond’s UV6357 adhesive, launched in July 2025, demonstrates innovation for cold-temperature industrial bonding, such as refrigeration assembly. Academic institutions and agencies like NIST are pushing the frontier in next-generation photoinitiator chemistry, optimizing cure depth and speed for thick-film and structural applications. The synergy between private-sector R&D and federal research programs keeps the U.S. at the forefront of UV-curable adhesive technology for advanced manufacturing.

Germany – European Powerhouse for High-Performance and VOC-Free UV Adhesives

Germany’s UV adhesives industry stands as a benchmark for precision manufacturing, sustainability, and VOC compliance. The country leads the European UV-curable adhesives market, supported by Henkel AG & Co. KGaA’s strategic expansion of its medical-grade UV adhesive portfolio. In January 2025, Henkel introduced Loctite AA 3952 and SI 5057, both ISO 10993 biocompatible adhesives for flexible and wearable medical devices, aligning with EU medical device regulations.

DELO Industrial Adhesives, another key German innovator, continues to dominate automotive and industrial electronics with ultra-fast-curing, low-shrinkage UV epoxies. Concurrently, Panacol-Elosol GmbH is driving advances in UV-curable jetting materials and 3D printing adhesives, complementing the nation’s rapid transition to automated UV LED curing systems. The Federal Ministry for Economic Affairs and Climate Action (BMWK) actively supports solvent-free UV resin R&D, reducing VOC emissions while enhancing crosslinking efficiency. In addition, German research universities are developing TPO-free photoinitiators to preempt EU restrictions, solidifying Germany’s role as the epicenter of sustainable UV-curing adhesive technology in Europe.

China – Mass Production and Localization in Electronics and EV Adhesive Systems

China dominates the Asia-Pacific UV-curable adhesives market, underpinned by its expansive consumer electronics manufacturing ecosystem and EV production scale. The assembly of smartphones, displays, and camera modules drives enormous consumption of UV-curable acrylics and optical adhesives, while government policies supporting the EV industry have catalyzed demand for UV-curable structural and encapsulating adhesives used in battery modules, inverters, and power electronics.

China’s localization strategy has intensified, with major investment directed toward domestic production of photoinitiators, resins, and raw materials to ensure self-sufficiency amid global supply chain disruptions. Companies like DeepMaterial Co., Ltd. are pioneering cost-effective UV-curable encapsulants and potting compounds for LED lighting and industrial electronics, addressing both cost and performance optimization. Furthermore, the expansion of high-speed digital printing across China has created massive demand for UV-curable inks, varnishes, and coatings. Industrial parks in China’s key provinces are increasingly mandating low-VOC operational frameworks, fostering the widespread shift toward 100% solids UV adhesive formulations.

Japan – Precision UV Adhesive Formulations for Optics, Displays, and Space Applications

Japan’s UV adhesive market is defined by high-precision engineering and deep integration in optical devices, display panels, and aerospace electronics. Manufacturers like ThreeBond International and SEKISUI CHEMICAL CO., LTD. are pioneering high-clarity UV-curing adhesives essential for optical lens bonding and display assembly, addressing the demands of OLED and Micro-LED fabrication. The automotive and electronics sectors increasingly rely on low-outgassing, thermally stable UV adhesives suited for vacuum environments and high-temperature bonding, particularly in satellite components and autonomous sensor modules.

Denka Co., Ltd. remains central to UV-curable silicone adhesive innovation, delivering flexible, low-modulus materials ideal for flexible electronics and sensors. Japan’s automotive manufacturers also employ UV-curing adhesives for surface repair and small-part assembly, ensuring fast turnaround and high clarity. Ongoing R&D in non-yellowing and moisture-resistant UV formulations for optical displays strengthens Japan’s leadership in premium UV-curing chemistry across advanced manufacturing applications.

United Kingdom – Expanding Medical and Industrial UV Adhesive Applications

The United Kingdom UV adhesives market is growing steadily, driven by its strong medical device manufacturing base and niche industrial assembly sectors. Medical applications are a key focus, with manufacturers emphasizing ISO 10993-certified UV adhesives for catheters, respiratory systems, and diagnostic equipment. Local firms such as Cartell UK Ltd. and high-tech distributors play a vital role in supporting custom UV-curing systems and material supply across low-volume, high-precision assembly lines.

The UK’s industrial and renewable energy sectors are increasingly adopting UV-curable cyanoacrylates and hybrid adhesives for rapid curing, flexibility, and weather resistance. The materials are critical for solar panel bonding, architectural glass facades, and outdoor installations requiring long-term UV stability. The shift toward sustainable, VOC-free UV-curing materials aligns with the UK’s broader net-zero manufacturing goals, positioning the nation as a key European hub for medical-grade and high-performance industrial UV adhesives.

South Korea – UV Adhesive Leadership in Semiconductor and Display Technologies

South Korea has positioned itself as a global leader in UV-curable adhesives through its dominance in semiconductors, displays, and flexible electronics. Major conglomerates are advancing the use of optically clear adhesives (OCA) in foldable, rollable, and flexible OLED displays, requiring exceptional transparency and elasticity. The semiconductor packaging sector extensively uses thixotropic UV-curable underfills and glob-top coatings, ensuring thermal stability and mechanical resilience in high-density integrated circuits.

Government-backed Industry 4.0 initiatives are driving the integration of automated UV LED curing and precision dispensing systems into high-speed electronics assembly. The technological advancements have enabled significant yield improvement and cost efficiency in South Korea’s electronics export industry. With expanding investments in EV battery, display, and microelectronics manufacturing, South Korea continues to set global benchmarks for UV-curable adhesive technologies in precision, scalability, and automation.

India – Emerging Market for Automotive, Electronics, and Construction UV Adhesives

India’s UV adhesives market is expanding rapidly, supported by the ‘Make in India’ initiative and the country’s rising manufacturing capabilities in automotive, electronics, and packaging sectors. Domestic suppliers are increasingly adopting UV-curing systems to accelerate production throughput and reduce energy consumption. The automotive components industry, in particular, benefits from fast-curing UV bonding solutions for glass, dashboard assemblies, and headlamp sealing.

The packaging industry is also embracing UV-curable laminating adhesives and printing inks, especially in flexible packaging for premium consumer goods. Rising investments in commercial construction have further boosted the adoption of UV-curable sealants and glass bonding adhesives for modern façade and architectural glazing applications, emphasizing clarity, strength, and weather resistance. As UV adhesive technology becomes integral to India’s industrial modernization, the country is positioned as a key emerging hub for UV curing and advanced photopolymer chemistry.

UV Adhesives Market Report Scope

UV Adhesives Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$9.4 Billion

|

|

Market Size (2034)

|

$15.7 Billion

|

|

Market Growth Rate

|

5.9%

|

|

Segments

|

By Resin Type (UV-Curable Acrylic, UV Epoxy, UV Cyanoacrylate, UV Silicone), By End-Use Industry (Electronics, Medical, Automotive, Industrial, Aerospace, Packaging), By Application Method (Automated, Screen Printing, Inkjet, Roll Coating), By Curing Method (UV Light, LED Light, Dual Cure), By Performance Characteristic (Optical Clear, Flexible, Thermal Management, Structural

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Henkel AG & Co. KGaA, 3M Company, Dymax Corporation, H.B. Fuller Company, DELO Industrial Adhesives, Sika AG, Master Bond Inc., Permabond LLC, Panacol-Elosol GmbH, Epoxy Technology, Inc., Dow Inc., ThreeBond International, Inc., SEKISUI CHEMICAL CO., LTD., BASF SE, Heraeus Holding GmbH

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

By Resin Type

- UV-Curable Acrylic

- UV Epoxy

- UV Cyanoacrylate

- UV Silicone

By End-Use Industry

- Electronics

- Medical

- Automotive

- Industrial

- Aerospace

- Packaging

By Application Method

- Automated

- Screen Printing

- Inkjet

- Roll Coating

By Curing Method

- UV Light

- LED Light

- Dual Cure

By Performance Characteristic

- Optical Clear

- Flexible

- Thermal Management

- Structural

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in UV Adhesives Market-

- Henkel AG & Co. KGaA

- 3M Company

- Dymax Corporation

- H.B. Fuller Company

- DELO Industrial Adhesives

- Sika AG

- Master Bond Inc.

- Permabond LLC

- Panacol-Elosol GmbH

- Epoxy Technology, Inc.

- Dow Inc.

- ThreeBond International, Inc.

- SEKISUI CHEMICAL CO., LTD.

- BASF SE

- Heraeus Holding GmbH

*- List not Exhaustive

Research Coverage

Prepared by USDAnalytics, this report investigates the global UV Adhesives Market through the lens of LED-first curing, electronics miniaturization, med-device compliance, automotive integration, and packaging automation; our analysis reviews supply chain readiness, material platforms (acrylate, epoxy, cyanoacrylate, silicone), and the production economics of instant, low-heat cures that compress takt times while meeting low-VOC expectations; it synthesizes recent breakthroughs in dual/secondary cure strategies, shadow-cure reliability, and high-refractive-index optical bonding, and highlights how standards (e.g., ISO 10993/MDR) and LED light-engine advances are reshaping qualification and yield—making this report an essential resource for engineering, sourcing, and operations leaders who must balance throughput, reliability, and regulatory conformance, etc……

Scope Highlights

Segmentation:

- By Resin Type: UV-Curable Acrylic; UV Epoxy; UV Cyanoacrylate; UV Silicone

- By End-Use Industry: Electronics; Medical; Automotive; Industrial; Aerospace; Packaging

- By Application Method: Automated; Screen Printing; Inkjet; Roll Coating

- By Curing Method: UV Light; LED Light; Dual Cure

- By Performance Characteristic: Optical Clear; Flexible; Thermal Management; Structural

- By Region: North America (United States, Canada, Mexico); Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe); Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC); South & Central America (Brazil, Argentina, Rest of SCA); Middle East & Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Geographic Scope: Analysis spans 25+ countries across North America, Europe, Asia Pacific, Latin America, the Middle East & Africa.

Time Horizon: Historic data 2021–2024 and forecast data 2025–2034.

Companies Covered (analysis/profiles of 15+): Henkel AG & Co. KGaA; 3M Company; Dymax Corporation; H.B. Fuller Company; DELO Industrial Adhesives; Sika AG; Master Bond Inc.; Permabond LLC; Panacol-Elosol GmbH; Epoxy Technology, Inc.; Dow Inc.; ThreeBond International, Inc.; SEKISUI CHEMICAL CO., LTD.; BASF SE; Heraeus Holding GmbH.

Deliverables

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.