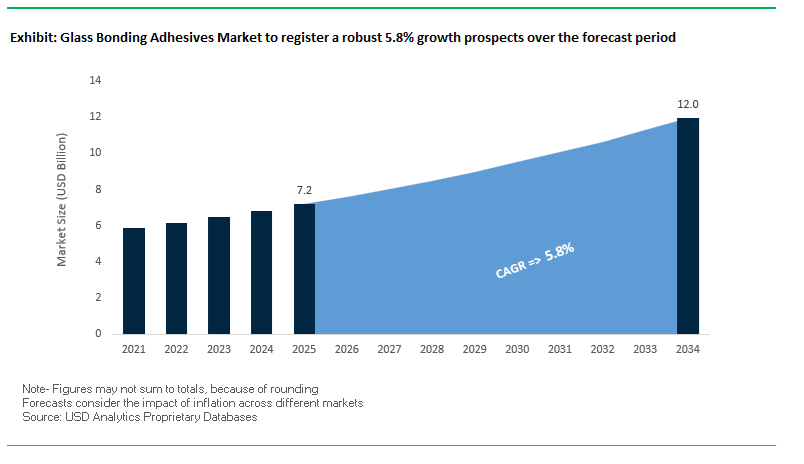

The Global Glass Bonding Adhesives Market is projected to expand from USD 7.2 billion in 2025 to USD 12 billion by 2034, advancing at a CAGR of 5.8%, as glass transitions from a passive enclosure material to a load-bearing, functional design element across automotive, architectural, and electronics applications. Growth is structurally driven by the replacement of mechanical fastening and solvent-based sealants with adhesive-led bonding architectures that deliver optical clarity, stress distribution, and long-term durability while meeting tightening environmental and safety regulations. OEMs are increasingly specifying UV-curable, silicone, and silane-modified polymer (SMP) adhesives to enable thinner glass sections, frameless designs, and multi-material integration—capabilities that fasteners and legacy sealants cannot support without compromising aesthetics or structural integrity.

From a performance and qualification standpoint, manufacturers such as Sika, Dow, Henkel, 3M, and Saint-Gobain are advancing glass bonding systems that combine high tensile strength, controlled elasticity, and rapid curing to meet production and reliability demands. Structural glass adhesives qualified for façade glazing, automotive bonding, and specialty enclosures are achieving tensile strengths approaching 1,200 psi, supporting bonded assemblies exposed to wind load, vibration, and thermal cycling. In parallel, UV-curable acrylic and hybrid systems, optimized for LED curing, are delivering fixture and full-cure times in the 1–30 second range, materially improving takt times in electronics, display assembly, and specialty glazing operations where precision and throughput are critical. These attributes are reinforcing adhesive bonding as a manufacturing enabler rather than a secondary joining choice.

Regulatory and occupational safety considerations are accelerating material substitution within the market. Polyurethane and SMP glass adhesives with less than 0.1% free monomeric diisocyanate are increasingly specified in automotive glazing and architectural bonding to align with REACH and workplace exposure limits, without sacrificing bond strength or long-term elasticity. Silicone-based glass adhesives continue to be favored in curtain wall and structural glazing systems due to their UV stability and movement accommodation, while SMP technologies are gaining traction where paintability, low-VOC profiles, and mixed-substrate adhesion are required.

The global glass bonding adhesives industry is witnessing transformative advancements in curing technology, material chemistry, and sustainability, reshaping competition and expanding high-performance application segments.

In October 2024, Henkel AG & Co. KGaA unveiled a new high-temperature glass adhesive formulation tailored for next-generation automotive and electronics components exposed to severe thermal cycling. This innovation marks Henkel’s push into extreme-environment bonding systems, targeting EV battery modules and smart cockpit assemblies where consistent adhesion under thermal load is critical.

By September 2024, 3M Company strengthened its leadership in UV-curable glass adhesives with a new generation featuring faster curing kinetics and enhanced optical stability under prolonged UV exposure. These adhesives significantly improve throughput in large-scale assembly lines for display panels, touchscreens, and precision optical components.

In August 2024, Dymax Corporation launched its LED-optimized adhesive line, engineered to cure specifically at 385 nm wavelengths, eliminating mercury lamps and aligning with the industry’s environmental goals. The shift toward LED curing technology underscores a broad trend toward low-energy, mercury-free, and precision curing systems that integrate seamlessly into automated production workflows.

Sika AG’s announcement in July 2024 of expanded sustainable building solutions reinforces the use of low-VOC, structural silicone adhesives for façade and glazing applications. Its high-elasticity sealants play a crucial role in architectural glass façades, combining aesthetic transparency with long-term UV and weather resistance.

Dow Inc., in June 2024, launched a new polyurethane system for laminated glass, providing enhanced acoustic insulation and impact resistance—key properties for automotive safety glass and soundproof architectural glazing. This system exemplifies the convergence of functional performance and comfort design in modern glass bonding.

In May 2024, Ashland Inc. emphasized its strategic focus on display assembly adhesives, specifically optically clear adhesives (OCA) and liquid optically clear resins (LOCA) for automotive infotainment and consumer electronics, highlighting the growing dominance of glass-to-display bonding.

H.B. Fuller, through an April 2024 acquisition of a niche industrial adhesives manufacturer, strengthened its position in specialized glass-to-metal bonding—a vital domain for aerospace and industrial equipment.

Meanwhile, Wacker Chemie AG in March 2024 expanded its silicone production footprint, ensuring supply stability for structural glazing adhesives, while Bostik (Arkema) in February 2024 introduced a Silane Modified Polymer (SMP) hybrid adhesive for window and façade bonding, offering high elasticity and superior resistance to environmental stress.

A defining trend in the glass bonding adhesives market is the rapid adoption of high-modulus structural silicones designed for unitized curtain wall systems and large-format glass façades. The demand for sleek, all-glass architectural designs has shifted engineering priorities toward sealants capable of exceptional load transfer, flexibility, and UV stability. According to leading building envelope specifications, structural silicone adhesives used in four-sided glazing must reliably transmit design wind loads up to 2400 Pa and safety loads of 3600 Pa, ensuring the structural integrity of façades subjected to extreme wind and temperature fluctuations.

Major adhesive manufacturers have responded by introducing two-component, fast-curing silicone structural sealants optimized for factory-fabricated curtain wall units. These formulations are tested for a service life exceeding 20 years, maintaining adhesion under harsh conditions—from −40°C cold cycles to prolonged solar UV exposure above 140°C. Their high modulus and excellent elasticity make them indispensable for modern skyscrapers and high-performance building envelopes. In addition, these sealants meet stringent ASTM C1184 and EN ISO 11600 standards, ensuring compliance with global structural glazing codes.

In addition to mechanical performance, durability testing has become a defining competitive factor. Leading structural silicones demonstrate no visible degradation after 1,000 hours of QUV accelerated aging, ensuring stability in extreme climates. The ability of these adhesives to maintain elasticity and structural integrity makes them the backbone of next-generation sustainable, energy-efficient façades, combining aesthetic freedom with long-term reliability for architects and builders.

Another transformative innovation in the glass bonding adhesives market is the proliferation of UV-curing and light-manageable adhesive technologies in electronics assembly, particularly for touch displays, camera modules, and wearable sensors. As manufacturing in consumer electronics accelerates, particularly across Asia-Pacific production hubs, adhesive technologies capable of instantaneous curing, high transparency, and thermal control are redefining production efficiency.

UV-curing adhesives provide instant fixture strength, drastically reducing assembly cycle times while maintaining optical clarity near 100% transmittance—critical for high-definition displays. Recent R&D initiatives have centered on reducing haze levels and refractive index variation to below 0.01, enhancing the brightness and visual quality of bonded glass components. However, as miniaturization advances, light penetration challenges in “shadowed zones” have driven the rise of dual-cure adhesive technologies. These systems combine UV-curing with secondary thermal or moisture-activated curing, ensuring complete polymerization in complex assemblies like camera sensors or micro-speaker modules.

Manufacturers are leveraging UV-LED curing systems that deliver consistent energy with minimal thermal output, extending operational life beyond 20,000 hours and improving process control. The integration of UV-curing glass adhesives has become central to next-generation flexible electronics and optical assemblies, where adhesive precision directly impacts device performance, transparency, and mechanical robustness.

The global automotive sector represents one of the most dynamic opportunities for glass bonding adhesive manufacturers, particularly with the rise of Electric Vehicles (EVs) and advanced glazing systems. The integration of bonded panoramic sunroofs, glued-in windshields, and structural glass panels demands adhesives with exceptional mechanical strength, crash resistance, and long-term stability.

The automotive glazing trend is moving toward adhesives that contribute structurally to vehicle rigidity while ensuring occupant safety during impact. High-performance polyurethane (PU) and modified silane (MS) adhesives are designed to meet or exceed OEM crash-resistance benchmarks. These formulations deliver rapid “green strength” to meet just-in-time (JIT) production cycles—allowing vehicles to proceed to final assembly within hours of bonding. Adhesive formulations with advanced moisture-curing kinetics ensure faster throughput while maintaining strong adhesion on diverse substrates, including glass, aluminum, and polycarbonate.

Additionally, the industry’s shift toward lightweight materials and reduced vehicle weight has heightened the importance of adhesive versatility. Modern structural adhesives eliminate the need for aggressive pretreatment, reducing the risk of stress cracking in polycarbonate glazing systems—especially relevant for EV panoramic roofs and autonomous vehicle sensor housings. As OEMs adopt large-format glass surfaces to enhance aesthetics and aerodynamics, suppliers of high-strength, low-density adhesive systems are strategically positioned to capture long-term growth in the automotive glass bonding segment.

The intersection of smart glass technology and photovoltaic integration is emerging as a transformative growth opportunity for the glass bonding adhesives industry. The expansion of Building-Integrated Photovoltaics (BIPV) and switchable smart glazing systems demands adhesives that combine optical clarity with electrical insulation, UV resistance, and environmental durability.

In BIPV façade applications, adhesives play a crucial role in ensuring long-term performance, glare control, and electrical isolation between laminated glass layers. Recent studies on photovoltaic glass modules show that specialized optically clear adhesives (OCAs) can maintain reflectivity below 0.1% while passing damp heat (85°C, 85% RH for 1,000 hours) and temperature cycling tests (−40°C to 85°C)—confirming resilience under extreme environmental exposure. The ability to retain adhesion and clarity over decades is essential for architectural adoption, particularly in energy-harvesting facades and solar-integrated glazing systems.

For smart windows that integrate liquid crystal (LC) layers or electrochromic films, the adhesive must not interfere with the switching mechanism between transparent and opaque modes. R&D efforts are focused on developing low-ion migration, non-yellowing OCAs with optical transmission rates exceeding 98%, ensuring both functionality and aesthetics in long-term operation. The growing adoption of switchable privacy glass and solar-harvesting façades positions adhesive manufacturers to capitalize on a new frontier—where sustainability, technology, and design converge.

In parallel, global initiatives promoting net-zero buildings are accelerating BIPV adoption, particularly across Europe, China, and North America. Adhesive systems that meet EN 50583 and IEC 61215 certification standards for laminated PV glass are expected to witness exponential demand as smart façades and energy-positive buildings redefine modern construction paradigms.

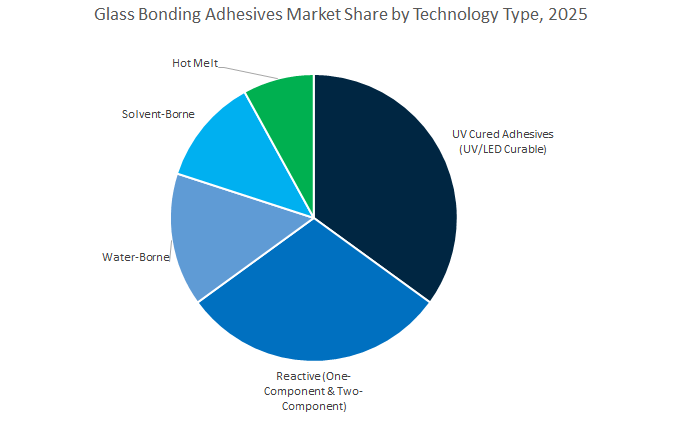

Glass Bonding Adhesives Market Share Insights, 2025-2034

The UV-cured glass bonding adhesives segment holds the leading position with a projected 33.5% market share in 2025, driven by their rapid curing speed, optical clarity, and superior bond strength. These adhesives have become essential in electronics, medical devices, and precision optical applications, where transparency, accuracy, and aesthetics are critical. UV and LED-curable adhesives provide instant polymerization under light exposure, enabling faster production cycles and higher throughput in industries such as smartphone manufacturing, display panels, and decorative glass fixtures. Their ability to form bubble-free, high-strength bonds makes them indispensable in architectural and automotive glass assemblies, particularly for sensors and electronic modules in modern vehicles. The shift toward UV LED curing systems for energy efficiency and low thermal stress further strengthens this segment’s dominance.

Reactive adhesives, including one-component and two-component epoxy, silicone, and polyurethane systems, maintain a robust market share in structural and high-stress bonding applications. Their exceptional mechanical strength, thermal stability, and moisture resistance make them the preferred choice in automotive, construction, and industrial glass installations. In particular, two-component polyurethane adhesives are widely used for windshield bonding, façade glazing, and encapsulated electronic components, where long-term reliability is vital. Meanwhile, water-borne glass adhesives are gaining traction in interior applications and consumer goods due to their eco-friendly formulations and compliance with VOC standards. These systems are increasingly used for mirrors, decorative panels, and indoor glass furnishings, where odor reduction and clean application are valued. Solvent-borne and hot melt adhesives serve niche roles in specialty industrial uses, where rapid drying, high adhesion on metal-glass interfaces, or thermal resistance is critical, such as in automotive lighting assemblies or aerospace components.

The building and construction sector dominates the global glass bonding adhesives market, capturing a projected 32.9% share in 2025, primarily due to the surging adoption of structural glazing, curtain walling, and insulating glass units. The modern architectural trend toward energy-efficient glass façades, daylight-optimized buildings, and aesthetic transparency has elevated the demand for high-performance silicone, polyurethane, and UV-curable adhesives that ensure long-term adhesion and weather resistance. These adhesives are integral to high-rise façades, glass roofs, and solar panels, where mechanical integrity and thermal stability are paramount. In emerging markets such as India, China, and the UAE, urban expansion and smart city projects are significantly contributing to market expansion.

The automotive and transportation sector follows as a major contributor, with adhesive applications in windshields, windows, sunroofs, and headlamp assemblies. Increasing vehicle production, along with trends in lightweighting and electric vehicle design, continues to drive demand for structural glass adhesives that offer vibration damping, UV stability, and impact resistance. Similarly, the electronics segment is growing rapidly, driven by innovations in display technologies, touchscreens, and sensor integration. Glass bonding adhesives are pivotal for achieving optical clarity and precision alignment in smartphones, tablets, and wearable devices.

The furniture and decorative glass segment represents a stable market supported by rising consumer preference for transparent, modern interior designs that rely on secure glass-to-metal and glass-to-wood bonds. Meanwhile, the medical device and industrial assembly segments account for specialized demand where chemical resistance, biocompatibility, and thermal reliability are essential. Adhesives used in medical glassware and laboratory instruments must meet stringent regulatory standards, driving the adoption of low-outgassing, light-curable materials.

The competitive ecosystem of the glass bonding adhesives industry is anchored by five dominant players—Henkel AG & Co. KGaA, Sika AG, Dymax Corporation, Dow Chemical Company, and Ashland Inc.—each leveraging material science innovation and regulatory foresight to sustain leadership in this rapidly evolving market.

Henkel commands one of the world’s largest adhesive portfolios, exceeding 8,000 product variants, spanning UV-curable acrylates, polyurethanes, and silicones. Its flagship Loctite® range sets global standards in optical clarity, tensile strength, and fast curing for automated glass assembly. The company’s global network in over 120 countries provides comprehensive support for electronics and automotive OEMs. Henkel’s innovation trajectory emphasizes high-temperature resistance, shock absorption, and sustainable chemistry—driving its reputation as the leading choice for precision glass bonding across high-value manufacturing sectors.

Sika AG integrates advanced structural silicone and polyurethane adhesives under its renowned Sikasil® and Sikaflex® brands. With over $2.5 billion in annual R&D investment, Sika’s Purform® technology has set the benchmark for low-isocyanate, REACH-compliant formulations, significantly enhancing worker safety and environmental compatibility. The company’s leadership in architectural glazing, insulated glass (IG) units, and structural façades underscores its dominance in the green building adhesives segment.

Dymax distinguishes itself through its integrated curing systems, providing both adhesives and LED curing equipment—a unique combination ensuring fully validated process performance. Its Multi-Cure® adhesives enable primary UV curing followed by secondary moisture cure, resolving the shadow-cure challenge in opaque glass assemblies. With product lines optimized for 385 nm and 405 nm LED wavelengths, Dymax has become the go-to supplier for medical device, electronics, and precision optics manufacturers seeking speed and biocompatibility.

Dow revolutionized architectural bonding with its DOWSIL™ and DOW CORNING® lines, pioneering structural silicone glazing (SSG) technology used globally for high-rise façades and curtain walls. Its silicone adhesives provide superior UV, thermal, and weather resistance, ensuring decades of bond integrity. Recent innovations target electric vehicle (EV) glazing systems, offering adhesives compatible with integrated sensors and antennas. Dow’s OEM certification programs maintain strict compliance and safety across all automotive glass applications.

Ashland leverages its polymer science expertise to enhance adhesive formulations through specialty additives and resins such as Aqualon™ and Purelam™. These technologies are critical in improving optical clarity, adhesion, and rheology control in urethane-acrylic glass bonding systems. The company’s continued innovation in optically clear adhesives (OCA) and liquid optically clear resins (LOCA) supports next-generation display assembly and flexible electronics manufacturing. Ashland’s focus on low-VOC, high-tack polymers underscores its alignment with future sustainability goals.

The United States glass bonding adhesives market is experiencing strong growth fueled by automotive electrification, modern architectural glazing, and sustainability regulations. Companies such as 3M are pioneering Two-Part Structural Adhesives (epoxy and acrylic) that provide superior bonding strength for high-strength steel and aluminum used in electric vehicle (EV) body structures, battery pack enclosures, and lightweight chassis systems. The advanced adhesives play a critical role in achieving weight reduction and improving crash resistance in next-generation vehicles.

In the automotive glass bonding segment, DuPont’s BETASEAL™ systems are setting new standards by supporting integrated antenna and ADAS sensor compatibility, essential for autonomous and connected vehicles. Meanwhile, Dymax Corporation continues to innovate in UV-curable acrylic adhesive technologies, introducing faster-curing, low-shrinkage materials tailored for precision glass-to-metal and glass-to-plastic bonding in consumer electronics and medical devices.

From a regulatory standpoint, the growing enforcement of low-VOC standards across U.S. states has led to increased adoption of waterborne and 100% solids adhesive systems, aligning with EPA and LEED-certified sustainability goals. The architectural glass bonding segment—driven by high-rise construction and energy-efficient façade design—shows robust demand for high-modulus silicone sealants conforming to ASTM and AAMA standards. With heavy investment in automation and digital manufacturing, U.S.-based adhesive producers are optimizing production processes to integrate with OEM robotic assembly lines, boosting efficiency and product consistency in the structural glass adhesives market.

Germany and the broader European Union remain at the forefront of eco-compliant glass bonding adhesives development, driven by stringent environmental and safety regulations such as REACH and EU Green Deal directives. Manufacturers are intensifying their focus on low-VOC, sustainable, and circular adhesives tailored for architectural glazing, public transport, and EV manufacturing applications.

Leading European players like Henkel AG & Co. KGaA and Sika AG are heavily investing in next-generation polyurethane (PU) and modified silane (SMP) systems that provide superior flexibility, adhesion, and fire resistance—critical for structural glazing and façades in energy-efficient buildings. The high-performance adhesives also meet EN 13501 and DIN 4102 fire safety requirements, reflecting the EU’s commitment to green construction.

The rapid electrification of automotive production across Europe is driving the demand for advanced PU adhesives in direct glass glazing for EVs, enabling enhanced body stiffness, faster processing times, and thermal management in lightweight vehicles. Moreover, European R&D centers are pioneering dual-cure UV + moisture adhesive technologies that ensure complete polymerization even in shadowed glass areas, enhancing reliability in complex bonding geometries. With ongoing investment in high-speed rail and green infrastructure, Germany and the EU are solidifying their position as global leaders in sustainable glass bonding adhesive innovation.

China represents the largest global market for glass bonding adhesives, with exponential demand stemming from urbanization, industrial expansion, and electric vehicle production. The 14th Five-Year Plan and the government’s Smart City Initiative have fueled rapid construction of curtain walls, glass façades, and prefab structures, creating immense need for polyurethane and silicone structural adhesives that meet national GB standards for performance and safety.

Global adhesive leaders such as Sika and Henkel are implementing a local-for-local manufacturing strategy, expanding domestic production facilities to reduce lead times and cater to regional humidity and temperature challenges. At the same time, Chinese electronics manufacturers are driving heavy demand for UV-curable acrylic and epoxy adhesives optimized for smartphone, display, and consumer electronics assembly—a sector where precision and curing speed are critical.

The New Energy Vehicle (NEV) sector is a major growth engine, with glass bonding adhesives being vital for battery module assembly, panoramic roofs, and windshields in EVs. Additionally, government initiatives promoting prefabricated and modular construction are expanding the use of high-strength glass bonding systems and weather-resistant sealants for exterior insulation and finish systems (EIFS). The integration of policy support, infrastructure growth, and manufacturing modernization positions China as the world’s most dynamic and high-volume producer of industrial glass adhesives.

Japan and South Korea are leading centers for precision adhesive technology, dominating the consumer electronics, display, and optical glass bonding segments. Their expertise in UV-curable and thermally stable adhesive systems supports cutting-edge applications in flexible OLED screens, AR/VR devices, and ADAS-integrated automotive glass.

Electronics miniaturization trends drive demand for low-outgassing UV adhesives capable of bonding ultra-thin glass layers while maintaining clarity and conductivity. Automotive innovations, led by Japanese OEMs, are fueling R&D in UV-LED curable adhesives for LiDAR sensors and in-glass camera modules, which require excellent heat dissipation and vibration resistance. The emphasis on thermally conductive and transparent adhesives for automotive displays and navigation systems highlights both countries’ leadership in hybrid glass–electronics integration.

Both Japan and South Korea have advanced automated manufacturing systems that utilize adhesives with extremely short cure times (under 10 seconds) to ensure throughput efficiency. Additionally, firms like ThreeBond Holdings Co., Ltd. and LG Chem are expanding portfolios of optical bonding and sealing materials to support semiconductors, displays, and EV component manufacturing. The innovation ecosystem cements Japan and South Korea’s role as pioneers in high-precision, high-performance glass bonding adhesives for global electronics and automotive industries.

India’s glass bonding adhesives industry is expanding rapidly in tandem with its infrastructure and housing boom, supported by large-scale government programs such as the Smart Cities Mission and Pradhan Mantri Awas Yojana (PMAY). Public infrastructure projects—including ring roads, airports, and expressways—have significantly increased demand for polyurethane and silicone-based sealants and adhesives in construction and structural glazing applications.

In a notable move, AIS Glass Solutions Limited acquired Balaji Building Technologies Limited, enhancing its position as a leader in architectural glass solutions and driving local demand for high-strength structural adhesives. The growing adoption of nanotechnology coatings by companies like HeatCure also reflects a trend toward integrating advanced bonding systems in performance glass applications for residential and commercial buildings.

The residential and commercial construction sectors continue to consume large volumes of epoxy and polyurethane adhesives for window systems, façade panels, and glazing, while India’s expanding e-commerce logistics and packaging sectors indirectly sustain adhesive consumption across construction supply chains. With foreign direct investments in glass and adhesives manufacturing, India is rapidly becoming a key regional market for construction-grade and structural glass adhesives, bridging demand between the Middle East and Southeast Asia.

Vietnam stands out as one of the fastest-growing markets in the Asia-Pacific glass bonding adhesives industry, propelled by industrialization, urbanization, and electronics manufacturing expansion. Large-scale infrastructure projects such as the North–South Expressway Phase 2 are fueling demand for PU-based structural adhesives in construction, particularly for glazing and cladding systems in commercial complexes and public infrastructure.

Vietnam’s emergence as a regional electronics hub, hosting major production facilities for Samsung and LG, has spurred growth in high-performance glass bonding adhesives for device assembly and precision component manufacturing. Furthermore, the Power Development Plan 8 (PDP8), aiming to achieve 30.9% renewable energy generation by 2030, is creating demand for adhesives used in solar panel assembly and glass-to-frame bonding within photovoltaic systems.

Global adhesive leaders such as Henkel Vietnam, 3M, and Dow are expanding operations locally, introducing advanced structural silicone and polyurethane adhesive systems tailored for Vietnam’s tropical climate and rapid industrial development. The convergence of foreign investment, electronics sector growth, and renewable energy expansion makes Vietnam a critical node in the ASEAN glass bonding adhesives market.

Glass Bonding Adhesives Market Report Scope

Glass Bonding Adhesives Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$7.2 Billion

|

|

Market Size (2034)

|

$12 Billion

|

|

Market Growth Rate

|

5.8%

|

|

Segments

|

By Resin/Chemistry (Polyurethane, Structural Silicone, Structural Acrylic, UV-Curable Acrylate, Epoxy, Cyanoacrylate, Modified Silanes), By Technology Type (Reactive, UV Cured Adhesives, Water-Borne, Solvent-Borne, Hot Melt), By End-Use Industry (Automotive & Transportation, Building & Construction, Electronics, Furniture & Decorative Glass, Medical Devices, Industrial Assembly), By Substrate (Glass-to-Glass, Glass-to-Metal, Glass-to-Plastic, Glass-to-Composite, Glass-to-Ceramic

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Henkel AG & Co. KGaA, 3M Company, Sika AG, The Dow Chemical Company, H.B. Fuller Company, DuPont, Arkema S.A., Huntsman International LLC, Dymax Corporation, Permabond Engineering Adhesives, Master Bond Inc., Panacol-Elosol GmbH, ThreeBond Holdings Co., Ltd., Ashland Inc., Momentive Performance Materials Inc.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

By Resin/Chemistry

- Polyurethane

- Structural Silicone

- Structural Acrylic

- UV-Curable Acrylate

- Epoxy

- Cyanoacrylate

- Modified Silanes

By Technology Type

- Reactive

- UV Cured Adhesives

- Water-Borne

- Solvent-Borne

- Hot Melt

By End-Use Industry

- Automotive & Transportation

- Building & Construction

- Electronics

- Furniture & Decorative Glass

- Medical Devices

- Industrial Assembly

By Substrate

- Glass-to-Glass

- Glass-to-Metal

- Glass-to-Plastic

- Glass-to-Composite

- Glass-to-Ceramic

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

- Henkel AG & Co. KGaA

- 3M Company

- Sika AG

- The Dow Chemical Company

- H.B. Fuller Company

- DuPont

- Arkema S.A.

- Huntsman International LLC

- Dymax Corporation

- Permabond Engineering Adhesives

- Master Bond Inc.

- Panacol-Elosol GmbH

- ThreeBond Holdings Co., Ltd.

- Ashland Inc.

- Momentive Performance Materials Inc.

*- List not Exhaustive

Research Coverage

Prepared by USDAnalytics, this report investigates performance, processing, and compliance dynamics shaping the Global Glass Bonding Adhesives Market, delivering analysis reviews on demand inflections across structural glazing, automotive glazing, precision electronics, and decorative applications. It highlights breakthroughs in UV-LED fast cure, REACH-aligned low-isocyanate polyurethane, high-modulus structural silicones, and SMP hybrids that unlock stronger, clearer, and more durable glass interfaces while reducing VOCs and energy use. With comparative cure-speed maps, tensile/peel benchmarks, substrate compatibility matrices (glass-to-metal/plastic/composite), and total-installed-cost views, this report is an essential resource for product managers, sourcing leaders, process engineers, and specifiers seeking reliable bonds, shorter cycles, and lifetime optical stability in next-gen façades, vehicles, and devices.

Scope Highlights

Segmentation:

- By Resin/Chemistry: Polyurethane; Structural Silicone; Structural Acrylic; UV-Curable Acrylate; Epoxy; Cyanoacrylate; Modified Silanes.

- By Technology Type: Reactive; UV Cured Adhesives; Water-Borne; Solvent-Borne; Hot Melt.

- By End-Use Industry: Automotive & Transportation; Building & Construction; Electronics; Furniture & Decorative Glass; Medical Devices; Industrial Assembly.

- By Substrate: Glass-to-Glass; Glass-to-Metal; Glass-to-Plastic; Glass-to-Composite; Glass-to-Ceramic.

Geographic Scope: Analysis spans 25+ countries across North America, Europe, Asia Pacific, Latin America, the Middle East & Africa.

Time Frame: Historic data 2021–2024 and forecast data 2025–2034.

Companies: Analysis/profiles of 15+ companies covering portfolios, innovation pipelines, sustainability posture, M&A, and regional strategy.

Deliverables

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.