Market Overview: High-Efficiency Hot Melt Adhesives Becoming Core Enablers of Automated, Low-Emission Manufacturing

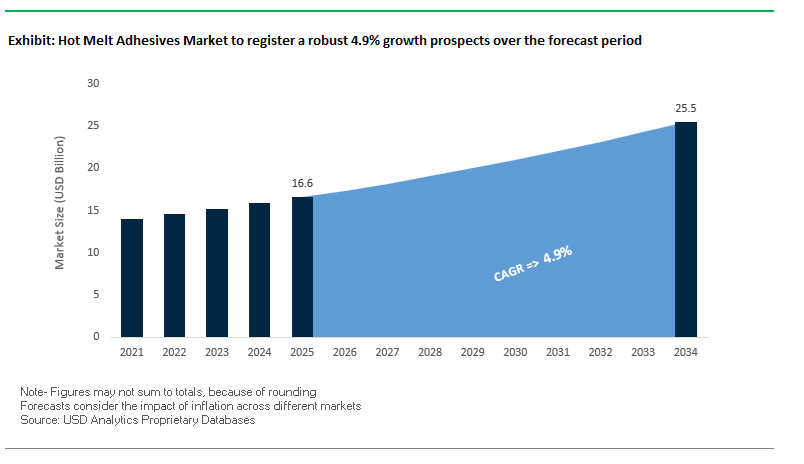

The Global Hot Melt Adhesives (HMA) Market is projected to expand from USD 16.6 billion in 2025 to USD 25.5 billion by 2034, advancing at a CAGR of 4.9%, as HMAs consolidate their role as the default bonding technology in high-speed, energy-efficient industrial production. Growth is structurally driven by the replacement of solvent-based and waterborne systems with 100% solid hot melt chemistries that eliminate drying steps, reduce energy consumption, and support increasingly automated manufacturing lines. Across packaging, automotive, woodworking, hygiene, and electronics, adhesive selection is closely tied to line speed, coat-weight efficiency, and sustainability compliance, positioning HMAs as process-critical materials rather than interchangeable consumables.

Further, manufacturers such as Henkel, H.B. Fuller, Arkema (Bostik), Dow, Jowat, and 3M are expanding portfolios centered on metallocene polyolefin (mPO), EVA, APAO, polyamide, and reactive hot melt (RHM) platforms to address differentiated performance needs. Metallocene polyolefin HMAs are gaining strong traction in packaging and hygiene applications due to their lower density and controlled molecular architecture, enabling up to 40% adhesive consumption reduction through thinner, more uniform coat weights while maintaining thermal stability and adhesion consistency on high-speed lines. In contrast, polyamide-based HMAs are increasingly specified in automotive and electronics assemblies where resistance to oils, fuels, and aggressive thermal cycling—typically from −40°C up to +185°C—is non-negotiable, particularly for wire harness fixation, sensor mounting, and under-the-hood components.

A key structural shift within the market is the growing penetration of reactive hot melt adhesives, which bridge the gap between thermoplastics and thermosets. RHM systems deliver fast initial set typical of conventional HMAs, followed by post-application crosslinking that imparts long-term heat and moisture resistance required in woodworking, automotive interiors, and textile lamination. At the same time, standard thermoplastic HMAs continue to dominate environments where handling strength in under 10 seconds is essential to eliminate clamping, maximize throughput, and reduce factory footprint.

The Hot Melt Adhesives (HMA) industry is undergoing notable transformation marked by sustainability-driven innovation, strategic M&A, and capacity expansions.

In October 2025, Meridian Adhesives Group announced the divestment of its flooring adhesives business (Taylor Adhesives) to Avery Dennison, sharpening its focus on industrial, electronics, and hot melt technologies. This portfolio realignment underscores a strategic industry trend toward specialization in high-performance adhesives for electronics and industrial bonding. Similarly, in August 2025, Sika AG launched a series of high-strength HMAs designed for automotive lightweighting, enhancing structural integrity and aligning with electric vehicle (EV) assembly trends. During the same month, Epoxy Technology (Meridian Group) introduced EPO-TEK® 353NDP, reflecting the increasing crossover between electronics-grade encapsulants and HMA-style potting materials in next-gen connectivity systems.

In May 2025, sustainability took center stage as 3M and Nitto Denko launched bio-based HMAs for automotive applications, targeting global OEMs pursuing carbon footprint reduction and recyclable adhesive systems. Shortly thereafter, H.B. Fuller (April 2025) revealed a major investment in U.S. HMA manufacturing capacity, supporting surging demand in automotive assembly and packaging automation. The same month, Arsenal Capital Partners completed the sale of Applied Adhesives to Bertram Capital, reinforcing consolidation trends that enhance equipment integration and specialty formulation capability within the industrial adhesives market.

Meridian Adhesives Group expanded further in March 2025 with its Penang Application Development Center in Asia, strengthening regional R&D for electronics manufacturing adhesives. Earlier, its December 2024 acquisition of PAS Bangkok Co., Ltd. fortified its supply chain presence in Southeast Asia’s industrial manufacturing belt. In parallel, Henkel Japan expanded its Technomelt HMA portfolio (November 2024) for automotive applications, engineered to meet rigorous durability and performance standards.

A defining trend across the hot melt adhesives market is the transition from conventional petroleum-based polymers such as EVA and polyolefins to bio-based and renewable feedstock-derived adhesives. The shift is propelled by stringent sustainability mandates, corporate carbon reduction targets, and the rising consumer preference for eco-friendly packaging solutions. Adhesive manufacturers are strategically investing in renewable raw materials to minimize environmental impact while maintaining industrial-grade performance.

One of the most prominent breakthroughs in the area was achieved by a global adhesives manufacturer that successfully commercialized a new bio-based hot melt adhesive for consumer packaging. The formulation utilizes 49% direct bio-based raw materials and an additional 30% ISCC-certified mass-balanced feedstock, setting a new benchmark in the development of renewable-content adhesives for folding carton, tray, and wrap-around packaging. According to cradle-to-gate lifecycle assessments, the bio-based formulation delivers up to a 25% reduction in CO₂ emissions compared to conventional EVA-based hot melts.

In addition, bio-based innovation is expanding toward compostable adhesives for paper packaging. A recent independent study confirmed that next-generation 85% bio-based hot melt adhesives could fully degrade within 180 days under industrial composting conditions, aligning with EN 13432 compostability standards. The development supports the circular economy model by offering adhesives that do not compromise the recyclability or biodegradability of packaging materials. The integration of renewable inputs, such as plant-derived polyols and resins, thus represents a fundamental transformation in the green adhesive value chain, reinforcing the industry's path toward net-zero manufacturing and sustainable packaging ecosystems.

Energy efficiency and the need for safer bonding of heat-sensitive substrates are accelerating the adoption of low-temperature hot melt adhesive systems. Manufacturers are focusing on developing high-strength HMAs that deliver optimal performance while operating at significantly reduced application temperatures. The trend not only minimizes energy consumption but also reduces thermal degradation of substrates and equipment, contributing directly to operational cost savings and Scope 2 emission reductions for end users.

Advanced formulations allow stable adhesive performance at 110°C to 120°C, compared to traditional application ranges exceeding 150°C. The 40°C temperature reduction translates into substantial energy savings across industrial packaging lines. Notably, major global adhesive producers are combining low-temperature application capabilities with bio-based content, delivering dual sustainability benefits by reducing both raw material emissions and processing energy. For example, a newly launched bio-based low-temperature adhesive demonstrated 40°C lower application heat requirements while maintaining the same bonding strength as conventional EVA-based hot melts, reflecting a strong technological synergy between sustainability and performance engineering.

The trend also resonates across industries such as automotive interiors, woodworking, and electronics, where thermal stress sensitivity and substrate protection are critical. As industries align with eco-efficient production models, low-temperature HMAs are expected to dominate adhesive selection for high-speed automation and precision bonding—cementing their role as a cornerstone of sustainable industrial innovation.

The global e-commerce boom is fueling an unprecedented demand for hot melt adhesives tailored to automated packaging lines. As fulfillment centers scale up and robotics take over carton sealing, taping, and case erecting, adhesive manufacturers are reengineering product formulations for high-speed application, fast cure cycles, and system compatibility.

Recent innovations have achieved curing times as fast as 1–2 seconds, perfectly suited for automated carton-closing systems operating in fulfillment centers worldwide. These formulations ensure strong adhesion, rapid set time, and minimal downtime, critical for maintaining the pace of logistics operations. Additionally, adhesive technologies are evolving to support the integration of self-adhesive tear tapes and tamper-evident packaging, which rely heavily on advanced hot melt and pressure-sensitive adhesive layers to ensure secure yet easy-opening designs.

Investments in e-commerce packaging infrastructure are also driving the adoption of high-shear, temperature-stable HMAs that can withstand varied transportation environments—from sub-zero cold-chain logistics to humid tropical conditions. Leading brands are collaborating with adhesive suppliers to co-develop tailored formulations for automated robotic application, addressing key challenges such as adhesive stringing, residue formation, and nozzle clogging at high line speeds. As global parcel volumes surge, hot melt adhesives engineered for automation-ready performance represent one of the most lucrative opportunities for manufacturers aiming to expand in the packaging and logistics segment.

The global packaging industry’s transition toward recyclable mono-material structures presents a transformative opportunity for the Hot Melt Adhesives Market, particularly in the development of repulpable, recyclable, and easy-separation adhesive systems. These adhesives are engineered to ensure compatibility with paper and polymer recycling streams while preserving material recovery efficiency.

Recent advancements in repulpable HMAs have demonstrated exceptional recyclability performance, achieving a RejectScore of 93 out of 100 in independent repulping tests. The score confirms that the adhesive is cleanly separated as a compact mass, ensuring high fiber recovery yield and maintaining the quality of recycled paper pulp. Such superior performance aligns with the European Paper Recycling Council (EPRC) guidelines, which outline critical parameters such as minimum adhesive softening point (68°C Ring & Ball) and layer thickness (≥120 μm) for ensuring adhesive compatibility with large-scale recycling operations.

Beyond the paper segment, polyethylene-compatible HMAs are being developed to support the recyclability of mono-material flexible packaging, particularly in stand-up pouches and food wraps. These specialized adhesives are designed to blend seamlessly into polyethylene recycling streams, avoiding contamination and preserving mechanical integrity. As brands adopt circular packaging designs, adhesive manufacturers that provide certified recyclable, compostable, and low-carbon bonding solutions will capture growing partnerships with FMCG and packaging converters striving for 2030 sustainability targets.

Hot Melt Adhesives Market Share Insights, 2025-2034

The packaging segment holds the dominant share of the global hot melt adhesives (HMA) market, accounting for a projected 36.8% in 2025, underscoring its central role in case and carton sealing, labeling, and flexible packaging operations across consumer goods, food, beverage, and e-commerce logistics. The unparalleled rise of online retail and fast-moving consumer goods (FMCG) industries has intensified demand for HMAs that deliver instant bonding strength, clean processing, and long-term adhesion on various substrates such as corrugated fiberboard, paper, foil, and plastics. Hot melt adhesives enable high-speed, automated packaging lines while maintaining thermal stability and reactivation properties, which are critical for maintaining seal integrity during storage and transit. Additionally, brand owners are shifting toward bio-based and low-odor formulations to comply with food-contact safety standards and sustainability goals, strengthening the segment’s dominance.

The nonwoven hygiene products segment represents one of the largest high-volume consumers of HMAs, driven by the production of baby diapers, feminine hygiene pads, and adult incontinence products, where consistent adhesion and skin-safe properties are vital. Manufacturers rely on pressure-sensitive and polyolefin-based HMAs for elastic attachment, core stabilization, and backsheet lamination due to their low viscosity, odor neutrality, and heat stability in continuous, high-speed manufacturing lines. Growth in this segment is bolstered by rising global hygiene awareness, population growth, and premiumization trends favoring soft, breathable, and comfortable products.

In the automotive industry, HMAs are increasingly adopted for interior trim bonding, headliners, seat assembly, and electronic module encapsulation, where lightweighting, vibration damping, and energy efficiency are critical. The surge in electric vehicle (EV) production has further accelerated the use of HMAs for battery pack assembly, insulation fixation, and cable management, offering both structural reliability and processing efficiency. The construction and furniture sectors contribute steady demand through applications in flooring, insulation panels, and cabinetry assembly, leveraging the fast-setting and gap-filling capabilities of HMAs to enhance productivity. Similarly, the electronics, bookbinding, printing, and footwear segments continue to diversify adhesive usage—ranging from circuit encapsulation and textile lamination to spine bonding and shoe sole assembly—highlighting the versatility and adaptability of hot melt adhesives across end-use verticals.

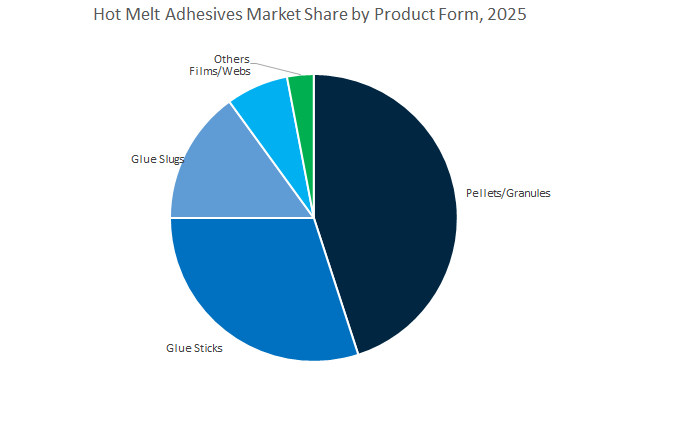

The pellets and granules form dominates the global hot melt adhesives market, capturing an estimated 44.1% share in 2025, largely due to its widespread adoption in industrial-scale packaging, woodworking, and product assembly applications. These solid, free-flowing forms enable automated feeding, metered melting, and consistent dispensing, making them ideal for high-speed production environments. Pellets and granules provide superior shelf stability, easy handling, and minimal waste, allowing manufacturers to streamline inventory management and operational throughput. In addition, pelletized HMAs are compatible with bulk melt units, extrusion systems, and robotic applicators, aligning with the industry’s increasing shift toward automation and smart manufacturing. As companies pursue eco-efficient and bio-based feedstocks, pellets have also become the preferred delivery form for renewable polyolefin and EVA formulations, supporting sustainability initiatives without compromising adhesive performance.

Glue sticks maintain a substantial market share due to their accessibility and versatility across small- and medium-scale applications, including crafts, packaging repair, and manual bonding operations. Their simplicity, portability, and compatibility with handheld glue guns make them indispensable in DIY, stationery, and prototyping markets. Glue slugs serve industrial applications requiring pre-measured, uniform adhesive dosing, particularly in furniture manufacturing, appliance assembly, and automotive trim work, where consistency and efficiency are paramount.

The Global Hot Melt Adhesives Market is led by a combination of diversified chemical giants and specialized adhesive manufacturers. Key players—Henkel AG & Co. KGaA, H.B. Fuller Company, Bostik (Arkema Group), 3M Company, and Jowat SE—shape the market through advanced polymer technology, strategic expansions, and product innovation in industrial automation, automotive bonding, and packaging sustainability.

Henkel dominates the global HMA market through its Technomelt brand, known for superior cost-in-use efficiency, sustainability, and performance. Its Technomelt 2557 EVA adhesive offers exceptional sift-proof sealing and perfume resistance, ideal for consumer goods and carton sealing. In Japan (Nov 2024), Henkel launched a new automotive-grade HMA line, engineered for durability under thermal and mechanical stress. The company’s bio-based formulations and renewable-content adhesives position it at the forefront of ESG-aligned manufacturing, while its high-speed processing HMAs reduce energy and material consumption.

H.B. Fuller Company: Leadership in Reactive Hot Melt and Hygiene Adhesives

H.B. Fuller continues to pioneer sustainable and high-performance hot melt systems across nonwovens, automotive, and assembly applications. Its Full-Care® HMA series delivers up to 70% bio-content, supporting circular economy goals in hygiene product manufacturing. The company’s April 2025 U.S. expansion enhances supply reliability for industrial clients. Its Full-Care 8000 series provides delayed crystallization for thin and soft nonwoven designs, while reactive hot melts (RHMs) enable crosslinked durability on TPO, glass, and metal substrates in challenging environmental conditions.

Bostik (Arkema Group): Advanced mPO and APAO Hot Melt Systems for Packaging and Construction

Bostik leverages Arkema’s polymer chemistry expertise to deliver next-generation low-VOC, high-efficiency EVA and mPO-based HMAs. The company’s Kizen® platform is widely adopted in case and carton sealing, offering clean running and high-speed compatibility. Its THERMOGRIP® 43298 adhesive is compostable, supporting eco-packaging mandates. With a strong focus on APAO (Amorphous Poly-Alpha-Olefins) HMAs, Bostik addresses automotive and construction bonding needs requiring UV stability and heat resistance. The Bostik ACADEMY enhances customer efficiency through technical process training and application optimization.

3M Company: Advanced Hot Melt Systems for Electronics and Automotive Integration

3M specializes in industrial-grade hot melt systems that combine ease of use, precision, and performance. The 3M™ Hot Melt Adhesive 3797 is a low-viscosity solution for electrical potting and printed circuit board assembly, providing high flow and heat resistance up to 77°C. Its bio-based HMA (May 2025) launch aligns with the automotive industry’s lightweighting and environmental objectives. The Scotch-Weld™ and 3748 series offer high-strength bonding (>100 psi) for foams, fabrics, and plastics, reducing the reliance on mechanical fasteners.

Jowat SE: Specialized Hot Melt Systems for Woodworking, Furniture, and Industrial Assembly

Jowat SE is a leader in industrial-grade reactive hot melt technology, with applications across woodworking, furniture manufacturing, textiles, and packaging. Its adhesives offer exceptional heat and moisture resistance, ensuring long-term stability in edge banding and profile wrapping. The company’s customized HMA solutions integrate diverse polymer bases, including polyolefin and EVA, optimized for automated, high-speed assembly. Additionally, its pressure-sensitive hot melts (PSA) are designed for labeling and flexible substrates, offering robust adhesion and recyclability.

China continues to dominate the global hot melt adhesives industry through large-scale capacity expansion, accelerated industrialization, and technological breakthroughs in pressure-sensitive adhesive (PSA) development. The country’s vast packaging, textile, and electronics manufacturing bases are fueling exponential growth in EVA, polyester, and metallocene polyolefin HMAs across industrial and consumer applications.

In September 2025, Zhuhai Yongsheng, a subsidiary of Dongjiang Environmental, expanded its daily hot melt adhesive pellet processing capacity from 3–5 tons to 15–18 tons, marking a major step toward high-volume, cost-competitive production for both domestic and global markets. The expansion supports China’s dual demand for industrial-strength adhesives and eco-friendly packaging solutions amid surging e-commerce activity. Moreover, researchers have developed a photoanionic curing PSA technology that fully cures under UV light in approximately two hours, enabling high-temperature endurance up to 220°C—a critical advantage for semiconductor and flexible electronics assembly.

The government’s environmental regulations continue to promote low-VOC, solvent-free adhesive systems, aligning with its broader industrial sustainability goals. Simultaneously, the hygiene products sector—especially diapers and adult care items—has emerged as a major demand driver for SIS/SBS-based HMAs, valued for their flexibility and durability. Overall, China’s manufacturing infrastructure, domestic innovation ecosystem, and favorable regulatory framework reinforce its position as the world’s largest and most technologically dynamic HMA producer.

The United States remains a global leader in high-performance and sustainable hot melt adhesive innovation, leveraging its R&D strength and advanced material science to serve diverse sectors like automotive, electronics, and packaging. With a strong focus on bio-based feedstocks and reactive adhesive chemistries, the country is transitioning toward greener, more efficient adhesive manufacturing models.

Companies such as Dow Inc. are spearheading The transition through ISCC+ certified AFFINITY™ RE Bio-based Polyolefin Elastomers, derived from renewable Tall Oil feedstocks, significantly reducing carbon footprints across packaging and hygiene applications. Similarly, 3M introduced reactive hot melt adhesives (RHMA) with enhanced heat and moisture resistance for use in smartphones and wearables—addressing the reliability requirements of modern consumer electronics.

Meanwhile, Sika Corporation has strengthened its market presence with 22 facilities across the U.S., leveraging HMA technologies for high-stress construction applications such as window and façade bonding. H.B. Fuller continues its leadership in RHMAs designed for automotive lightweighting and durable electronic bonding, while Beardow Adams Inc. invested over $5.1 million in a new North Carolina facility to bolster local production capacity.

Germany stands as Europe’s innovation hub for high-performance polyurethane (PUR) and polyolefin (PO) hot melt adhesives, backed by its engineering expertise, rigorous regulatory framework, and sustainability-first manufacturing ethos. Major players such as Henkel, BASF, and Jowat SE are driving advancements in low-emission, recyclable, and bio-based adhesive systems that meet the European Union’s environmental mandates.

In a landmark innovation, Jowat SE introduced Jowatherm-Reaktant MR 604.90, the world’s first PUR hot melt adhesive with reduced monomer content, addressing occupational safety while maintaining superior adhesion performance—particularly for furniture and textile applications. Henkel has also launched Technomelt EM 335 RE, a recycling-optimized HMA that enables label separation from PET bottles, supporting closed-loop packaging systems within the circular economy.

Germany’s Packaging Law compliance has prompted adhesive manufacturers to adopt renewable materials, such as Jowatherm GROW bio-based adhesives, aligning with the EU Green Deal and the CEFLEX recyclability framework. Combined with its expertise in automation and industrial bonding, Germany remains the benchmark for eco-efficient hot melt adhesive production across Europe, driving the transition toward non-isocyanate, low-VOC, and recyclable adhesive technologies.

India’s hot melt adhesives market is rapidly scaling due to industrial expansion, FMCG growth, and increased infrastructure investment. The nation is emerging as a regional HMA production hub, supported by favorable policy frameworks and multinational investment inflows.

In February 2024, Henkel Adhesive Technologies India Pvt. Ltd. announced a major capacity investment in Udhamsingh Nagar, Uttarakhand, with a production capacity of 5,010 metric tons per year, aimed at strengthening India’s domestic adhesives supply chain. Similarly, Avery Dennison Corporation, in collaboration with Dow, launched a recyclable hot melt label adhesive in April 2023, improving packaging circularity and aligning with India’s growing sustainability focus.

The footwear, consumer goods, and packaging industries represent key growth sectors. Henkel showcased sustainable HMA portfolios at the India International Footwear Fair (July 2023), highlighting efficient bonding solutions for athleisure and leather alternatives. With India’s e-commerce and FMCG sectors expanding by double digits annually, demand for EVA-based and metallocene HMAs for high-speed case sealing and packaging automation is surging. India’s manufacturing ecosystem, combined with strategic foreign investment, ensures that the country will become a regional production and innovation center for hot melt adhesives by 2030.

Brazil’s hot melt adhesive market is undergoing transformation, driven by its bio-based resource advantage and resurgent construction and packaging sectors. The nation’s agriculture-derived feedstocks, such as soy-based and sugarcane-based polymers, are enabling the development of sustainable hot melt formulations tailored to regional demand for recyclability and reduced carbon emissions.

Collaborative R&D programs between international chemical firms and Brazilian packaging manufacturers are fostering recyclable, bio-based hot melt adhesives compatible with recycled substrates and flexible packaging materials. The construction industry’s rebound, fueled by large-scale infrastructure projects and urban housing initiatives, is also driving the consumption of HMAs in insulation bonding and precast component assembly.

Moreover, Brazil’s footwear and hygiene industries—among the largest in Latin America—require flexible, high-adhesion HMAs for durable, elastic bonding in both textiles and nonwoven applications. Supported by local material sourcing and industrial modernization, Brazil is emerging as the key South American hub for green adhesive innovation and regional exports.

France plays a pivotal role in the European hot melt adhesives market, driven by its expertise in specialty chemicals and global adhesive brands. Arkema Group, through its Bostik division, leads the country’s innovation trajectory in industrial, hygiene, and packaging HMAs.

A strategic milestone was achieved in July 2020, when Arkema acquired Fixatti, a specialist in high-performance thermobonding adhesive powders, enhancing its product portfolio for automotive and textile applications. The Bostik brand remains a global frontrunner in industrial-grade HMAs, particularly in food packaging, hygiene disposables, and construction solutions, aligning with international safety and sustainability standards.

France’s strong industrial ecosystem and commitment to green chemistry ensure continued growth in specialty adhesive applications. With a focus on lightweight materials, clean labeling, and industrial circularity, France continues to be a strategic hub for HMA innovation within the European adhesive value chain.

Hot Melt Adhesives Market Report Scope

Hot Melt Adhesives Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$16.6 Billion

|

|

Market Size (2034)

|

$25.5 Billion

|

|

Market Growth Rate

|

4.9%

|

|

Segments

|

By Resin Type (Ethylene-Vinyl Acetate, Styrenic Block Copolymers, Metallocene Polyolefin, Polyurethane, Polyamide, Amorphous Poly-Alpha-Olefin, Others), By Application (Packaging, Nonwoven Hygiene Products, Automotive, Construction, Furniture & Woodworking, Electronics, Bookbinding & Printing, Footwear), By Product Form (Glue Sticks, Glue Slugs, Pellets/Granules, Films/Webs, Others), By End-Use Industry (Packaging, Nonwoven Hygiene, Automotive & Transportation, Building & Construction, Furniture & Woodworking, Electronics, Textile, Others), By Technology (Thermoplastic Hot Melt Adhesives, Reactive Hot Melt Adhesives

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Henkel AG & Co. KGaA, H.B. Fuller Company, 3M Company, Arkema Group, Sika AG, The Dow Chemical Company, Jowat SE, BASF SE, ExxonMobil Corporation, Avery Dennison Corporation, Mapei S.p.A., Beardow Adams, Pidilite Industries Ltd., Huntsman Corporation, LyondellBasell Industries

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

By Resin Type

- Ethylene-Vinyl Acetate

- Styrenic Block Copolymers

- Metallocene Polyolefin

- Polyurethane

- Polyamide

- Amorphous Poly-Alpha-Olefin

- Others

By Application

- Packaging

- Nonwoven Hygiene Products

- Automotive

- Construction

- Furniture & Woodworking

- Electronics

- Bookbinding & Printing

- Footwear

By Product Form

- Glue Sticks

- Glue Slugs

- Pellets/Granules

- Films/Webs

- Others

By End-Use Industry

- Packaging

- Nonwoven Hygiene

- Automotive & Transportation

- Building & Construction

- Furniture & Woodworking

- Electronics

- Textile

- Others

By Technology

- Thermoplastic Hot Melt Adhesives

- Reactive Hot Melt Adhesives

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

- Henkel AG & Co. KGaA

- H.B. Fuller Company

- 3M Company

- Arkema Group

- Sika AG

- The Dow Chemical Company

- Jowat SE

- BASF SE

- ExxonMobil Corporation

- Avery Dennison Corporation

- Mapei S.p.A.

- Beardow Adams

- Pidilite Industries Ltd.

- Huntsman Corporation

- LyondellBasell Industries

*- List not Exhaustive

Research Coverage

Purpose-built for packaging, hygiene, automotive, woodworking, and electronics stakeholders, the USDAnalytics study on the Hot Melt Adhesives (HMA) Market connects material choice with plant performance and circularity outcomes—this report investigates how EVA, mPO, APAO, polyurethane, polyamide and related chemistries translate into fast set, line uptime, and durable bonds in high-speed automation; maps breakthroughs in low-temperature application grades, bio-based/mass-balance feedstocks, and reactive hot melts that deliver thermoset-level durability; analysis reviews capacity moves, portfolio realignments, and compliance shifts shaping low-VOC, 100% solids adoption; and highlights productivity levers (thin coat weights, <10-second handling strength), energy savings, and recyclability-ready designs that de-risk specifications across packaging, nonwovens, and e-mobility assemblies. Built for strategy, sourcing, and engineering roadmaps, this report is an essential resource for executives, product managers, process engineers, and procurement leaders seeking evidence-backed guidance on reliability, cost-in-use, and ESG alignment, etc……

Scope Highlights

Segmentation

- By Resin Type: Ethylene-Vinyl Acetate; Styrenic Block Copolymers; Metallocene Polyolefin; Polyurethane; Polyamide; Amorphous Poly-Alpha-Olefin; Others

- By Application: Packaging; Nonwoven Hygiene Products; Automotive; Construction; Furniture & Woodworking; Electronics; Bookbinding & Printing; Footwear

- By Product Form: Glue Sticks; Glue Slugs; Pellets/Granules; Films/Webs; Others

- By End-Use Industry: Packaging; Nonwoven Hygiene; Automotive & Transportation; Building & Construction; Furniture & Woodworking; Electronics; Textile; Others

- By Technology: Thermoplastic Hot Melt Adhesives; Reactive Hot Melt Adhesives

- By Region: North America (United States, Canada, Mexico); Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe); Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC); South & Central America (Brazil, Argentina, Rest of SCA); Middle East & Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Geographic Scope: Analysis spans 25+ countries across North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa.

Time Horizon: Historic data 2021–2024 and forecast data 2025–2034.

Companies: Analysis/profiles of 15+ companies (list not exhaustive).

Deliverables

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.