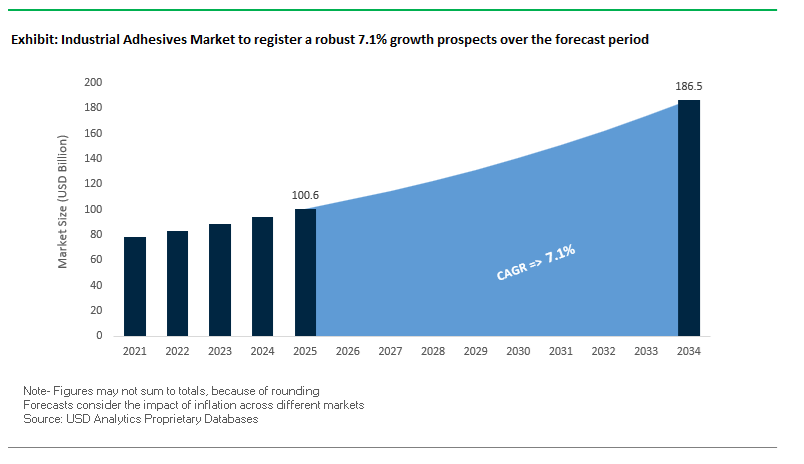

The Global Industrial Adhesives Market is forecasted to grow from USD 100.6 billion in 2025 to USD 186.5 billion by 2034, registering a CAGR of 7.1%. Industrial adhesives are increasingly vital in enabling the transformation of manufacturing processes across sectors such as automotive, aerospace, electronics, construction, packaging, and renewable energy. The surge in EV adoption, lightweighting initiatives, and environmental sustainability targets are fundamentally reshaping adhesive chemistries—from traditional solvent-based systems to bio-based, low-VOC, and high-performance thermosetting adhesives designed for structural reliability and environmental compliance.

The industry’s evolution is driven by three key performance dimensions—mechanical strength, thermal conductivity, and chemical sustainability. In the electric vehicle sector, high thermal conductivity adhesives (≥3 W/m·K) are replacing mechanical fasteners for battery assembly, offering flame retardancy (UL94 V-0) and enhanced thermal management. Similarly, in aerospace manufacturing, structural adhesives enable a 15% reduction in aircraft component weight, enhancing fuel efficiency while joining dissimilar composites and metals. In the construction industry, next-generation Purform® polyurethane adhesives are enhancing airtight sealing performance, contributing to Net Zero Energy Building (NZEB) compliance.

Emerging regulations in North America and Europe are compelling adhesive manufacturers to transition toward low-emission, bio-based, and migration-resistant adhesives for food packaging and hygiene applications. Furthermore, the miniaturization of medical and wearable electronics is expanding demand for IBOA-free, UV-curable adhesives, emphasizing biocompatibility and flexibility. The industrial adhesives ecosystem is, therefore, positioned at the intersection of performance innovation and sustainability leadership, where technological adaptability defines long-term competitiveness.

The industrial adhesives sector is undergoing a transformative phase marked by global investment flows, product innovation, and strategic consolidation aimed at advancing sustainability, performance, and automation.

In September 2025, Henkel AG & Co. KGaA inaugurated its €60 million Inspiration Center for Adhesive Technologies in Shanghai, serving as a key Asia-Pacific hub for R&D collaboration, customer testing, and sustainable materials development. This facility focuses on accelerating low-carbon adhesives, targeting packaging, mobility, and electronics sectors in the region. In July 2025, Applied Adhesives acquired BTmix and HG Adhesive Dispensing, integrating adhesive formulation and precision dispensing technology to strengthen its industrial automation platform. During the same month, Sonoco announced a $30 million capacity expansion across its adhesives and sealants production lines, underscoring the industry's focus on supply chain resilience and production scalability.

In June 2025, Meridian Adhesives Group established its Penang Application Development Center in Malaysia to expand technical expertise in electronics assembly adhesives—an essential step to serve Asia’s fast-growing semiconductor and automotive electronics markets. Similarly, DELO Industrial Adhesives launched two landmark products in May and March 2025, introducing directional conductive adhesives for microLED production and an IBOA-free medical-grade adhesive (PHOTOBOND MG4047) aligned with tightening EU health regulations.

Corporate restructuring remains a recurring theme. Evonik Industries in October 2024 announced plans to streamline its adhesive portfolio, focusing on high-margin specialty materials and exploring partnerships for its polyester division. Meanwhile, Applied Adhesives completed another strategic acquisition—AutomationSupply365—to strengthen its industrial automation and equipment supply chain integration, marking a clear move toward end-to-end adhesive solutions.

Sustainability imperatives are driving a paradigm shift in adhesive manufacturing toward renewable, recyclable, and low-carbon adhesive chemistries. Regulatory frameworks such as the EU Circular Economy Action Plan, coupled with the Packaging and Packaging Waste Regulation (PPWR) and Ecodesign for Sustainable Products Regulation (ESPR), aim to double circularity rates to 24% by 2030, fundamentally reshaping the demand landscape for industrial adhesives. These policies compel manufacturers to design products that are “recyclable by design,” catalyzing an industry-wide migration to bio-based and solvent-free adhesive systems across packaging, construction, and consumer goods sectors.

Technological advances are closing the performance gap between traditional petroleum-based adhesives and bio-based alternatives. For instance, a materials innovator recently commercialized a 100% biobased, water-based adhesive that demonstrated PVA-equivalent bonding strength in ISO T-Peel and Lap Shear tests—proof that sustainability and performance are no longer mutually exclusive. Similarly, BioBond Adhesives Inc. has emerged as a frontrunner by licensing patented biopolymer technologies from multiple universities, developing plant-water-based adhesive systems for packaging and consumer goods applications.

In addition, the shift is being reinforced by large-scale decarbonization initiatives. Leading adhesive producers are adopting ISCC-certified mass-balance accounting and renewable carbon sourcing to achieve verified carbon footprint reductions of up to 25% compared to conventional petroleum-based adhesive systems. As major FMCG and construction brands move toward net-zero material inputs, the demand for high-bio-content, recyclable adhesives is projected to accelerate sharply, establishing a long-term growth frontier in the green adhesives segment of industrial manufacturing.

The integration of Industry 4.0, robotics, and smart manufacturing systems is transforming industrial adhesives from passive bonding agents into active functional materials. Recent R&D breakthroughs have produced adhesive systems with embedded sensing, self-healing, and tunable mechanical properties, enabling intelligent process feedback and adaptive functionality.

Academic research has introduced a magnetorheological smart adhesive that mimics biological muscle tissue behavior—capable of stiffness modulation and microsecond response times to external stimuli. Such materials are proving invaluable in precision robotics and automated handling systems, where millisecond-level attachment and release capabilities are critical. These intelligent adhesives are also being explored in smart packaging, microelectronics assembly, and aerospace maintenance applications, allowing adaptive bonding or debonding based on temperature, light exposure, or electric fields.

In industrial production, functional adhesives with thermal management and sensing capabilities are gaining traction, particularly in battery assembly and power electronics. These systems integrate thermal interface materials (TIMs) that not only dissipate heat but also monitor temperature thresholds in real time, improving safety and system performance. The convergence of adhesive technology and embedded intelligence is reshaping the industrial landscape—transforming adhesives into critical components of predictive maintenance and energy-efficient manufacturing ecosystems.

The global shift toward electrified mobility represents a defining growth vector for the industrial adhesives industry. With global EV production expected to surpass 70 million units by 2035, adhesives are replacing traditional mechanical fasteners in key applications—battery pack assembly, thermal interface management, crash-resistant bonding, and lightweight body structures.

The U.S. Department of Energy (DOE) has allocated $43 million under the Vehicle Technologies Office (VTO) Battery FOA for FY 2024, specifically targeting innovations that enhance EV battery safety and thermal management. Adhesive manufacturers are responding by developing thermally conductive and flame-retardant structural adhesives designed to mitigate thermal runaway risks in lithium-ion battery modules. These formulations enable efficient heat dissipation, enhance crash durability, and improve cell-to-cell insulation, making them essential to next-generation EV architectures.

Further, high-durability polyurethane and epoxy adhesives are facilitating vehicle lightweighting, replacing rivets and welds in aluminum and composite body structures to achieve up to 15–20% weight reduction without compromising strength. As governments and automakers invest in gigafactory-scale EV production, the demand for specialized structural and thermal adhesives in battery, motor, and e-powertrain assembly will remain one of the fastest-growing segments within the industrial adhesives market.

The rise of automated, precision-based manufacturing in electronics, automotive, and packaging sectors is generating strong opportunities for industrial adhesives designed for robotic and high-speed dispensing systems. The demand for adhesives that can maintain rheological consistency, rapid cure kinetics, and precise bead control is expanding, particularly in high-throughput environments such as semiconductor packaging, circuit assembly, and automated carton sealing.

Modern robotic glue dispensers, operating with positioning accuracy as tight as 0.01 mm and speeds up to 5.05 m/s, impose stringent requirements on adhesive formulations. Adhesives must maintain dimensional stability during extrusion, resist dripping or stringing, and cure uniformly under controlled thermal or UV exposure. Consequently, manufacturers are formulating low-viscosity, high-thixotropy adhesive systems optimized for robotic application consistency, enabling superior production yield and automation compatibility.

In advanced electronics manufacturing, dual-cure and UV-activated adhesives are gaining prominence for their ability to support multi-layer PCB assembly, microelectronic encapsulation, and optical sensor bonding at high precision. Additionally, in packaging automation, metallocene-based hot melt adhesives have become integral to achieving reliable, high-speed sealing—capable of maintaining adhesion strength even under challenging conditions such as recycled board substrates and temperature fluctuations.

As the global industrial base embraces Industry 4.0 digitalization, the intersection between adhesive technology and smart robotics is poised to redefine efficiency benchmarks. The convergence will continue to expand the market for machine-compatible, high-performance adhesives, anchoring the industry’s role in the next generation of intelligent manufacturing ecosystems.

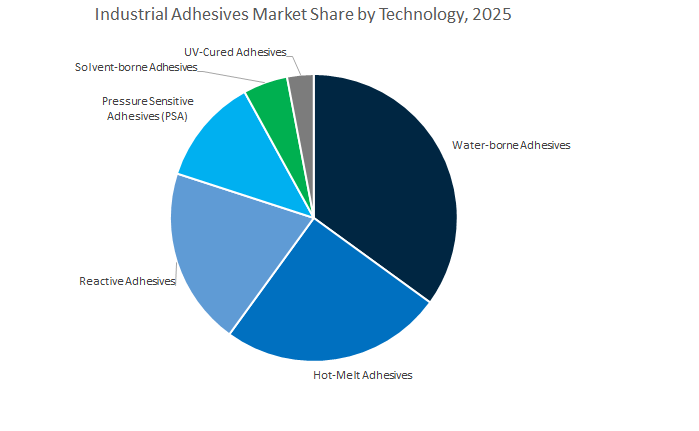

Industrial Adhesives Market Share Insights, 2025-2034

The water-borne adhesives segment dominates the global industrial adhesives market, accounting for a projected 33.9% share in 2025, underscoring its pivotal role in driving sustainable and regulatory-compliant adhesive technologies. This leadership stems from the global shift toward low-VOC, non-toxic, and eco-friendly adhesive formulations aligned with environmental mandates in North America, Europe, and Asia-Pacific. Water-borne adhesives are widely used in packaging, woodworking, and construction, where cost-effectiveness, versatility, and strong adhesion to porous substrates make them the default choice. The advancement of polyvinyl acetate (PVA), acrylic, and polyurethane dispersions has further enhanced their bond strength and water resistance, enabling their adoption in high-humidity environments and diverse industrial applications.

The hot-melt adhesives (HMAs) segment is witnessing rapid growth due to their fast-setting characteristics, thermal stability, and adaptability to automated production lines. Their solvent-free nature and compatibility with a wide range of substrates position them as an attractive alternative for high-speed packaging, nonwovens, and automotive assembly. Particularly, reactive polyurethane (PUR) hot melts are reshaping the market with enhanced bond durability, chemical resistance, and structural performance, allowing their use in interior trim, electronics, and footwear assembly. Reactive adhesives continue to hold a vital position in structural and performance-driven applications such as aerospace, automotive, and construction, where epoxy, silicone, and polyurethane systems provide unmatched mechanical strength and environmental endurance.

Meanwhile, pressure-sensitive adhesives (PSAs) and UV-cured adhesives serve specialized, value-driven markets that demand instant adhesion, optical clarity, and precision curing. PSAs are key in labels, tapes, and medical applications, offering a balance of tack and flexibility, while UV-curable adhesives thrive in electronics, optical devices, and high-precision industrial assemblies due to their rapid curing and low heat generation. On the other hand, solvent-borne adhesives—once the industry standard—are steadily declining as companies move away from VOC-heavy processes toward cleaner technologies. However, they maintain relevance in niche markets where deep penetration and strong substrate bonding are critical, such as footwear and laminating operations.

The packaging industry remains the leading consumer of industrial adhesives, projected to hold a 26.8% share in 2025, reflecting the adhesive’s foundational role in corrugated box sealing, flexible packaging, and labeling. The exponential rise in e-commerce, food delivery services, and FMCG logistics continues to boost adhesive consumption in this sector. Hot-melt and water-borne adhesives dominate packaging lines due to their fast-curing, cost-efficient, and recyclable properties, enabling high-speed operations without compromising bond integrity. As the demand for sustainable and recyclable packaging materials grows, manufacturers are developing compostable and bio-based adhesive formulations compatible with paper, bioplastics, and coated substrates. The packaging segment’s growth is also supported by the integration of smart labeling and tamper-evident solutions, which require pressure-sensitive and UV-curable adhesives for reliability and precision.

The building and construction segment maintains a robust share due to its extensive use of adhesives in flooring, roofing, panels, insulation, and façade bonding. Industrial-grade adhesives have become essential for lightweight and modular construction, providing superior load distribution, weather resistance, and structural durability compared to mechanical fastening systems. In the automotive and transportation sector, adhesives are increasingly deployed for electric vehicle (EV) assembly, battery modules, glass bonding, and composite structures, replacing traditional welding and riveting techniques. The focus on vehicle lightweighting and vibration damping continues to fuel adoption of epoxy, polyurethane, and hybrid adhesives, which enhance energy efficiency and safety performance.

The woodworking and joinery sector represents a stable market for PVA, polyurethane, and melamine-based adhesives, widely used in furniture, cabinetry, and engineered wood components. Growing consumer preference for aesthetic, durable, and eco-certified furniture has increased demand for formaldehyde-free, low-emission adhesive systems. Similarly, the industrial assembly segment encompasses a wide array of applications—from electronics and appliances to machinery and equipment manufacturing—where bonding precision and automation compatibility are critical. Nonwovens and hygiene applications, driven by diaper and sanitary product production, demand adhesives with soft touch, elasticity, and long-term skin compatibility.

The competitive landscape of the industrial adhesives industry is characterized by innovation leadership, regional expansion, and sustainability integration. Major players—Henkel, H.B. Fuller, Sika, 3M, Arkema (Bostik), and Master Bond—are strategically aligning their product portfolios with global trends in lightweighting, decarbonization, and digital manufacturing.

Henkel AG & Co. KGaA: Setting the Global Benchmark in Sustainable Adhesive Technologies

Henkel remains the undisputed leader in industrial adhesives, driving innovations across mobility, packaging, and electronics. Through its “Respect the Planet, Rethink Design” initiative, Henkel integrates sustainable chemistry and circular design principles into all major adhesive lines. The company’s Technomelt and Loctite structural adhesives support up to 15% carbon footprint reduction in automotive assemblies via lightweight bonding. With a newly opened Shanghai Innovation Center (Sept 2025) and a regional automotive hub in Pune (Jul 2025), Henkel continues to lead in low-energy curing systems and thermal management materials for EV battery integration.

H.B. Fuller Company: Expanding High-Performance Adhesive Solutions Across Diverse Markets

H.B. Fuller has built a diversified portfolio across hygiene, packaging, and industrial bonding. The company’s acquisition of ND Industries (May 2024) added the Vibra-Tite brand, strengthening its presence in threadlockers and structural sealants. Its Full-Care® 7000 series enhances performance in disposable hygiene manufacturing, while its bio-based adhesive line targets the circular economy. With investments in reactive hot melts and functional coatings, Fuller focuses on sustainability, supply chain security, and technical partnerships with global OEMs.

Sika AG: Leading Innovations in Polyurethane and Structural Bonding Technologies

Sika AG dominates the industrial adhesives space through its Purform® polyurethane and SikaPower® epoxy technologies. The Purform® series features ultra-low monomeric diisocyanate content, ensuring compliance with REACH and improving workplace safety. Its SmartCore® epoxy adhesives deliver crash-durable performance for transportation, wind turbine, and construction applications. Recent acquisitions—Gulf Additive Factory LLC (Qatar) and Cromar Building Products (UK)—in 2025 have reinforced its presence in industrial assembly and sustainable construction.

3M Company: Advancing Pressure-Sensitive and Electrically Conductive Adhesive Technologies

3M continues to pioneer pressure-sensitive adhesives (PSAs) and high-performance epoxy systems for electronics and transportation. Its Scotch-Mount PSA 4998, launched in January 2024, provides exceptional heat resistance and strong bonding under vibration stress, vital for automotive interiors and EV applications. The company’s R&D focus on conductive adhesives for sensor and display integration further positions 3M at the forefront of smart material interfaces in industrial design.

Arkema S.A. (Bostik): Advancing Bio-Based Adhesives for Circular Industry Applications

Through its Bostik brand, Arkema continues to lead in high-performance, low-VOC adhesives for construction, hygiene, and nonwovens. Its collaboration with INRAE is accelerating the development of bio-based adhesive chemistries sourced from renewable feedstocks. Arkema’s SMP (Silyl Modified Polymer) technology provides high adhesion and elasticity for industrial assemblies without solvents. The company’s regional expansions and colocation production strategy enable faster time-to-market and reduced carbon footprint.

Master Bond Inc.: Specialized Epoxies for Extreme Industrial and Aerospace Conditions

Master Bond specializes in custom epoxy, sealant, and potting formulations engineered for high temperature, vibration, and chemical resistance. Its graphene-filled EP30NG epoxy offers superior electrical and thermal conductivity, while EP21TCHT-1 maintains stability after 1,000 hours at 85°C/85% RH. With NASA-certified low-outgassing materials and >3 W/m·K thermally conductive systems (EP5TC-80), Master Bond is a key supplier to aerospace, defense, and EV manufacturers requiring long-term durability in extreme environments.

The United States Industrial Adhesives Market remains a global benchmark for advanced adhesive technology, particularly in aerospace bonding, electric vehicles (EVs), and medical-grade applications. The country’s strategic focus on domestic production incentives under federal initiatives like the Inflation Reduction Act (IRA) and Bipartisan Infrastructure Law (BIL) has spurred investment in next-generation adhesive formulations designed for lightweight, durable, and energy-efficient applications.

Bostik (Arkema Group) recently invested $27 million in its Middleton, Massachusetts facility, enhancing capacity for high molecular weight polyester adhesives and reinforcing its sustainability-oriented production strategy. Meanwhile, Sika AG’s acquisition of Kwik Bond Polymers (KBP) strengthened its U.S. infrastructure adhesives portfolio, targeting concrete repair and structural bonding applications. The automotive industry, particularly the surge in EV manufacturing, remains a key demand driver for structural acrylics and epoxy adhesives, enabling lightweighting and improved crash resistance.

In addition, regulatory pressure from California’s Air Resources Board (CARB) is accelerating the adoption of low-VOC and water-borne adhesives across furniture, construction, and automotive manufacturing. On the technology front, companies such as 3M and Dymax are pioneering biocompatible, 28-day wear medical-grade silicone adhesives for wearables, while electronics manufacturers are integrating directional conductive adhesives (DCAs) as reliable non-solder bonding alternatives for micro-LED and flexible display assembly. The U.S. continues to lead the global market in sustainable and precision-engineered adhesive systems across high-growth industrial verticals.

China holds the position of the largest consumer and producer in the global industrial adhesives market, fueled by rapid industrialization, e-commerce logistics, and automotive innovation. Major international and domestic players continue to expand capacity to serve the fast-growing market for high-speed packaging, electronics assembly, and construction adhesives.

A major development was Sika’s acquisition of Crevo-Hengxin, a strategic move that strengthened its specialty silicone sealant and industrial adhesives portfolio across Asia Pacific. Domestic companies are advancing high-temperature and chemical-resistant epoxy systems to serve China’s automotive, electronics, and industrial machinery markets. The country’s massive e-commerce ecosystem—a cornerstone of its economy—drives demand for EVA and metallocene hot-melt adhesives in automated carton-sealing and tamper-evident packaging applications.

In alignment with China’s 14th Five-Year Plan, industrial policies prioritize green and low-carbon manufacturing, pushing adhesive producers to develop eco-friendly, solvent-free technologies that meet tightening environmental standards. The expansion of R&D hubs in Shanghai and Shenzhen is fostering innovation in photoanionic curing systems and pressure-sensitive adhesives (PSAs) capable of fast UV curing for semiconductor and electronic device applications. As a result, China’s strategic blend of manufacturing scale, technological advancement, and environmental policy compliance solidifies its role as a global center for next-generation industrial adhesives.

Germany serves as the epicenter of industrial adhesives innovation in Europe, combining advanced R&D, regulatory compliance, and precision manufacturing. German automotive OEMs and Tier-1 suppliers are integrating high-performance polyurethane (PU), modified acrylate, and epoxy adhesives into vehicle assembly to achieve lightweighting and improved crash safety—critical for meeting Euro 7 emission targets.

Leading companies like Henkel AG & Co. KGaA and its Loctite brand are driving global sustainability efforts through REACH-compliant adhesives that support circular material use and recyclability. Products such as Loctite EA 9365FST, designed for aircraft interiors, exemplify the industry’s shift toward low-VOC, high-durability bonding solutions for thermoplastic and thermoset composites. Concurrently, ALTANA’s ELANTAS division continues to invest in low-VOC impregnating and electrical resin systems, ensuring compliance with evolving European Green Deal regulations.

Germany’s industrial automation ecosystem—spanning robotics, machinery, and electronics—relies on precision adhesives for consistent, fatigue-resistant bonds in high-load environments. As sustainability becomes a central pillar, German chemical companies are leading in water-based, bio-derived adhesive technologies and digital material validation platforms, making Germany the model for sustainable industrial adhesives innovation in the European market.

India is rapidly evolving into one of the fastest-growing industrial adhesives markets, propelled by its expansive infrastructure development and manufacturing sector growth under the ‘Make in India’ and Production Linked Incentive (PLI) programs. Mega projects such as Bharatmala highways and Dedicated Freight Corridors are driving demand for high-strength polyurethane and epoxy adhesives used in bridge construction, tunnel sealing, and concrete rehabilitation.

Global leaders are strengthening their footprint in India — for instance, Henkel’s new electronics adhesives facility in Kurkumbh, Maharashtra, enhances domestic supply capabilities for the electronics manufacturing industry. Meanwhile, Pidilite Industries, the country’s largest adhesives manufacturer, is expanding its industrial segment portfolio with high-performance epoxy, polyurethane, and hybrid adhesives to meet the growing needs of construction and automotive clients.

The surge in EV and battery manufacturing, supported by India’s ambition to become an EV export hub, is further driving the use of thermal management encapsulants and structural adhesives for power electronics and battery packs. Additionally, partnerships like Avery Dennison’s collaboration with Dow to develop recyclable hot-melt label adhesives reflect the industry’s sustainability-driven transformation. India’s growing synergy between policy, domestic manufacturing, and sustainability initiatives positions it as a key emerging market for industrial adhesives.

Japan continues to lead in high-precision and high-reliability adhesive systems, catering to industries that demand miniaturization, optical clarity, and long-term durability. Japanese manufacturers, including Nitto Denko Corporation, Sekisui Chemical, and Toyo-Morton (Toyo Ink Group), are advancing UV-curing and cyanoacrylate adhesives that offer exceptional purity, heat resistance, and electrical insulation for semiconductors, display modules, and optical sensors.

Sika’s acquisition of Hamatite (2021) further solidified its presence in Japan’s automotive sector, emphasizing sealing and bonding solutions for lightweight EV and hybrid vehicle architectures. The construction industry is also a significant contributor, where MS polymer and silicone-based sealants are increasingly used in earthquake-resistant infrastructure due to their flexibility, high tensile strength, and durability.

Japan’s R&D focus on thermal and dielectric adhesives for high-frequency electronics and precision components underscores its leadership in next-generation electronic encapsulation and micro-assembly. The country’s commitment to innovation, reliability, and material purity continues to define its role as a global hub for industrial adhesive technology advancement.

The European Union (EU) is at the forefront of sustainable adhesive manufacturing, propelled by regulatory frameworks such as REACH, the European Green Deal, and VOC emission directives. The transition toward bio-based, solvent-free adhesives is reshaping industrial production across packaging, construction, and transportation sectors.

Arkema’s Bostik division exemplifies The shift, securing an eight-year biomethane supply agreement with ENGIE to decarbonize multiple European manufacturing sites. Furthermore, the launch of Bostik Fast Glue Ultra+, which contains 60% bio-based materials, marks a milestone in integrating renewable resources into industrial adhesive formulations. Similarly, Henkel and Jowat SE are expanding portfolios of recyclable, low-carbon adhesives that align with Europe’s Circular Economy Action Plan.

Infrastructure programs such as the Connecting Europe Facility (CEF), focused on modernizing continental transport networks, are generating strong demand for high-strength, weather-resistant structural adhesives in civil engineering and energy applications. The EU’s regulatory momentum is making Europe a global leader in sustainable adhesive innovation, balancing industrial performance with environmental responsibility.

Industrial Adhesives Market Report Scope

Industrial Adhesives Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$100.6 Billion

|

|

Market Size (2034)

|

$186.5 Billion

|

|

Market Growth Rate

|

7.1%

|

|

Segments

|

By Chemistry (Acrylic Adhesives, Polyurethane Adhesives, Epoxy Adhesives, Silicone Adhesives, Cyanoacrylate Adhesives, VAE/EVA Adhesives, Styrenic Block Copolymers, Rubber-based Adhesives, Phenolic and Vinyl Adhesives, Other Specialty Polymers), By Technology (Water-borne Adhesives, Hot-Melt Adhesives, Reactive Adhesives, Solvent-borne Adhesives, UV-Cured Adhesives, Pressure Sensitive Adhesives), By End-Use Industry (Packaging, Automotive & Transportation, Building & Construction, Woodworking & Joinery, Consumer Goods & DIY, Assembly, Footwear & Leather, Medical & Healthcare, Aerospace & Defense, Nonwovens & Hygiene), By Application Function (Structural Bonding, Non-Structural Bonding, Sealing & Caulking, Lamination, Tapes & Labels, Encapsulation & Potting, Coating), By Form (Liquid, Paste, Film, Tape, Pellets, Powder

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Henkel AG & Co. KGaA, Sika AG, H.B. Fuller Company, Arkema Group, 3M Company, Dow Inc., Huntsman Corporation, Wacker Chemie AG, Avery Dennison Corporation, Ashland Global Holdings Inc., DELO Industrial Adhesives, Covestro AG, Pidilite Industries Ltd., Mitsubishi Chemical Corporation, Dymax Corporation

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

By Chemistry

- Acrylic Adhesives

- Polyurethane Adhesives

- Epoxy Adhesives

- Silicone Adhesives

- Cyanoacrylate Adhesives

- VAE/EVA Adhesives

- Styrenic Block Copolymers

- Rubber-based Adhesives

- Phenolic and Vinyl Adhesives

- Other Specialty Polymers

By Technology

- Water-borne Adhesives

- Hot-Melt Adhesives

- Reactive Adhesives

- Solvent-borne Adhesives

- UV-Cured Adhesives

- Pressure Sensitive Adhesives

By End-Use Industry

- Packaging

- Automotive & Transportation

- Building & Construction

- Woodworking & Joinery

- Consumer Goods & DIY

- Assembly

- Footwear & Leather

- Medical & Healthcare

- Aerospace & Defense

- Nonwovens & Hygiene

By Application Function

- Structural Bonding

- Non-Structural Bonding

- Sealing & Caulking

- Lamination

- Tapes & Labels

- Encapsulation & Potting

- Coating

By Form

- Liquid

- Paste

- Film

- Tape

- Pellets

- Powder

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

- Henkel AG & Co. KGaA

- Sika AG

- H.B. Fuller Company

- Arkema Group

- 3M Company

- Dow Inc.

- Huntsman Corporation

- Wacker Chemie AG

- Avery Dennison Corporation

- Ashland Global Holdings Inc.

- DELO Industrial Adhesives

- Covestro AG

- Pidilite Industries Ltd.

- Mitsubishi Chemical Corporation

- Dymax Corporation

*- List not Exhaustive

Research Coverage

Purpose-built for strategy, sourcing, and engineering leaders, the USDAnalytics study on the Industrial Adhesives Market synthesizes performance, compliance, and cost-in-use into one decision-grade narrative: this report investigates how structural strength, thermal management, and low-emission chemistry are converging across mobility, aerospace, electronics, construction, and packaging; tracks regulatory and supply-chain inflections shaping specifications and pricing; surfaces commercialization breakthroughs in reactive systems, UV/IBOA-free grades, and circular-ready platforms; analysis reviews M&A, capacity moves, and automation-led dispensing that reset productivity benchmarks; and highlights the procurement levers—process compatibility, cure kinetics, and durability KPIs—that de-risk adoption at scale. With scenario-led forecasts and benchmark metrics mapped to end-use workflows, this report is an essential resource for OEMs, converters, formulators, and investors seeking defensible choices on portfolio design, plant retrofits, and ESG outcomes, etc……

Scope Highlights

Segmentation

- By Chemistry: Acrylic Adhesives; Polyurethane Adhesives; Epoxy Adhesives; Silicone Adhesives; Cyanoacrylate Adhesives; VAE/EVA Adhesives; Styrenic Block Copolymers; Rubber-based Adhesives; Phenolic & Vinyl Adhesives; Other Specialty Polymers

- By Technology: Water-borne; Hot-Melt; Reactive; Solvent-borne; UV-Cured; Pressure-Sensitive Adhesives

- By End-Use Industry: Packaging; Automotive & Transportation; Building & Construction; Woodworking & Joinery; Consumer Goods & DIY; Assembly; Footwear & Leather; Medical & Healthcare; Aerospace & Defense; Nonwovens & Hygiene

- By Application Function: Structural Bonding; Non-Structural Bonding; Sealing & Caulking; Lamination; Tapes & Labels; Encapsulation & Potting; Coating

- By Form: Liquid; Paste; Film; Tape; Pellets; Powder

- By Region: North America (United States, Canada, Mexico); Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe); Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC); South & Central America (Brazil, Argentina, Rest of SCA); Middle East & Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Geographic Scope: Analysis spans 25+ countries across North America, Europe, Asia Pacific, Latin America, the Middle East & Africa.

Time Horizon: Historic data 2021–2024 and forecasts 2025–2034.

Companies: 15+ company analyses/profiles (list not exhaustive).

Deliverables

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.