Market Overview: Electrical and Electronics Adhesives as Enablers of Reliability, Thermal Control, and Manufacturing Yield

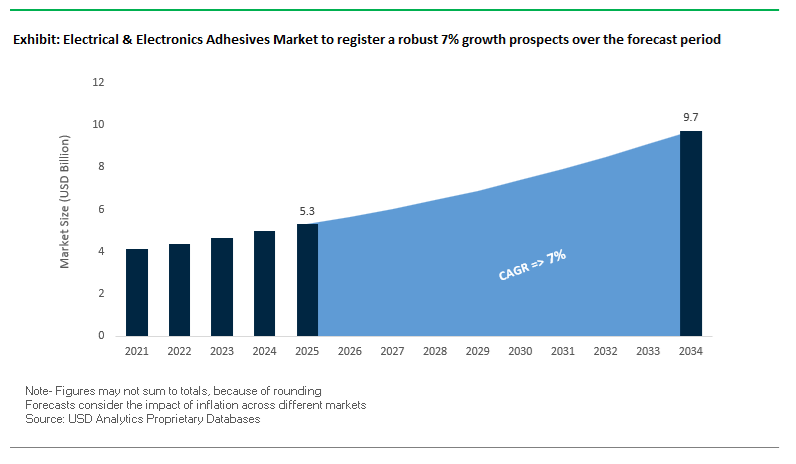

The Global Electrical and Electronics Adhesives Market is projected to grow from USD 5.3 billion in 2025 to USD 9.7 billion by 2034, exhibiting a steady CAGR of 7%. This growth trajectory is fueled by the accelerating adoption of electric vehicles (EVs), 5G infrastructure, semiconductor miniaturization, and advanced consumer electronics that demand enhanced reliability, thermal management, and sustainability. Electrical and electronics adhesives play a central role in bonding, sealing, and encapsulating critical components, ensuring high electrical insulation, heat dissipation, and vibration resistance across complex assemblies.

The core structural shift reshaping demand is the move toward multifunctional, production-compatible formulations aligned with automated electronics manufacturing. OEMs and tier suppliers are prioritizing adhesives that simultaneously deliver controlled thermal conductivity, high dielectric strength, and flame retardancy, while supporting fast cure cycles and precision dispensing on high-throughput lines. The growing use of thermally conductive gap fillers in power electronics and battery control units reflects the need to manage localized heat without adding mechanical complexity, while UV and moisture dual-cure adhesives are increasingly specified to ensure complete cure in shadowed or complex geometries common in electronic modules. This pivot reflects tighter process windows, higher yield expectations, and the need to reduce rework in advanced packaging and module assembly.

With continuous advancements in thermal interface materials (TIMs), electrically conductive adhesives (ECAs), and encapsulation compounds, the market is witnessing a technological shift toward high-performance, reliability-driven bonding solutions that underpin the next era of smart and sustainable electronics manufacturing.

In September 2025, WACKER Chemie AG introduced a new generation of thermally conductive gap fillers engineered for next-generation EV battery modules. These formulations boast enhanced pumpability for automated dispensing systems, addressing the rising demand for scalable solutions in electric mobility assembly lines. This innovation directly supports the surge in high-energy-density battery production, where maintaining uniform heat dissipation is critical for performance and safety.

By August 2025, sustainability became a core R&D focus as a global adhesives manufacturer announced significant investment in developing bio-based and low-VOC structural adhesives. This shift aligns with tightening environmental and occupational health regulations affecting the consumer electronics assembly sector. Companies are actively seeking sustainable adhesives that retain strength, flexibility, and compatibility with existing SMT and lamination processes, signaling a new era of green chemistry adoption in the electronics industry.

In July 2025, a U.S.-based conglomerate completed a new production facility in Southeast Asia dedicated to semiconductor encapsulants and die-attach films (DAFs). This expansion enhances supply chain resilience and meets regional demand for advanced packaging driven by AI chips and microelectronics manufacturing growth. Similarly, June 2025 saw the launch of innovative UV/moisture dual-cure adhesives optimized for complex, multilayer assemblies like OLED panels and 3D sensors, offering both rapid tack and deep-section curing capability.

The May 2025 landscape was marked by a joint development agreement between an automotive Tier 1 supplier and an adhesive manufacturer to produce vibration-damping potting materials for autonomous vehicle sensors and ADAS control units, enhancing reliability under real-world driving conditions. Another significant update came in May 2025 when a national regulatory body mandated higher dielectric strength and thermal stability standards for adhesives used in 5G telecom infrastructure and EV charging stations — emphasizing the growing role of adhesives in ensuring public infrastructure safety and performance.

Earlier, in April 2025, a global materials company acquired a European firm specializing in electrically conductive inks and pastes, integrating this expertise into its flexible electronics and PCB assembly portfolio. The acquisition enhanced vertical integration and innovation capability in printed circuit adhesives, strengthening its market leadership. In March 2025, the introduction of a low-outgassing epoxy adhesive specifically designed for optical bonding in LiDAR sensors and camera modules showcased the precision engineering direction of modern adhesive technology for autonomous navigation systems.

The push for compact, high-efficiency electronic systems—especially in electric vehicles (EVs), 5G infrastructure, data centers, and power semiconductor packaging—has spurred the development of thermally conductive adhesives (TCAs) that effectively dissipate heat while ensuring electrical insulation. The dual-function capability is crucial for extending device life and preventing overheating in high-power-density applications.

Manufacturers are achieving record-breaking thermal performance benchmarks, with silicone-based TCAs offering thermal conductivities of 3.0 W/m·K or greater and thermal resistance below 0.3°C·cm²/W. These materials maintain electrical insulation strength and stability at temperatures exceeding 300°C, making them ideal for Energy Storage Systems (ESS), inverters, and automotive control modules.

The increasing complexity of 400 GbE data transmission in data centers has also accelerated the need for micro-thermal interface coatings designed for pluggable optical modules (POMs) and network line cards. Companies like Henkel have introduced specialized micro-gap fillers and thermally conductive coatings optimized for rapid heat dissipation in compact networking architectures, ensuring consistent signal integrity under heavy workloads.

The global shift toward flexible hybrid electronics (FHE), wearables, and sensor integration has necessitated adhesives that can cure rapidly at low temperatures without compromising bond strength or substrate integrity. As device architectures integrate sensitive polymers, thin films, and delicate semiconductors, low-thermal-stress adhesives have become a linchpin for achieving high-yield, automated production.

Recent product innovations showcase single-component epoxies capable of full cure within 5–10 minutes at 80°C, or extended curing at 60°C for one hour, striking a balance between process flexibility and efficiency. These materials are particularly suitable for multimedia cards (MMCs), image sensors, and micro-electromechanical systems (MEMS) assemblies, where thermal load minimization is essential.

Further, the adoption of UV-LED curing adhesives—especially cationic-curing epoxy systems—has revolutionized throughput in electronic assembly lines. With LED light sources offering lifespans exceeding 20,000 hours and significantly lower thermal radiation compared to traditional mercury lamps, manufacturers can achieve instant polymerization even on shadowed substrates. The advancement is particularly relevant for fine-pitch bonding, FHE circuit encapsulation, and optical component sealing, where ultra-fast, low-energy curing enhances both yield rates and energy efficiency.

The semiconductor industry’s paradigm shift from monolithic system-on-chip (SoC) designs to heterogeneous integration (HI) and chiplet-based architectures has created a massive opportunity for high-reliability die-attach adhesives and electrically conductive bonding materials. These advanced adhesives play a pivotal role in System-in-Package (SiP) and 3D integration processes, where multiple functional dies are interconnected through fine-pitch interposers and micro-vias.

In chiplet packaging, interposer vias—ranging from 50 to 250 μm in diameter—are increasingly filled with conductive adhesive pastes, enabling robust electrical and mechanical interconnections. These adhesives exhibit superior creep resistance, low void content, and enhanced aging stability, essential for long-term reliability in high-performance computing (HPC) and automotive ECUs.

For instance, a thixotropic epoxy adhesive designed for ultra-fine die-attach applications demonstrated 47 N adhesion strength on FR4 substrates and 62 N on gold after seven days at 85°C/85% RH, proving resilience against thermal cycling and humidity exposure—key stress factors in advanced automotive and AI chip assemblies.

As chiplet integration scales, the demand for precision adhesive deposition technologies (e.g., jet-dispensing, micro-stenciling) will further amplify the market for electrically conductive and thermally stable die-attach adhesives critical to enabling next-generation microelectronics.

The rapid commercialization of solid-state batteries (SSBs) represents one of the most transformative growth frontiers for electrical and electronics adhesives. Unlike conventional liquid electrolyte batteries, SSBs require adhesives that can handle high operating temperatures, mechanical stresses, and chemical inertness associated with solid electrolytes and lithium metal interfaces.

In 2024, the Chinese government announced a USD 830 million investment to accelerate SSB industrialization across six major domestic manufacturers, highlighting the scale of opportunity for sealants and encapsulants tailored for these advanced chemistries. Leading companies are commercializing non-silicone, silyl-modified sealants that can operate continuously at temperatures up to 165°C while resisting electrolyte corrosion and thermal expansion mismatches.

These specialized adhesives are engineered to ensure airtight, long-life cell sealing under aggressive cycling conditions and are essential for battery module assembly, anode encapsulation, and pack edge sealing in next-generation EV systems. Their role extends beyond bonding—they act as thermal interface materials, mechanical dampers, and chemical barriers simultaneously, reflecting the multifunctional integration trend in e-mobility manufacturing.

With gigafactory expansions accelerating globally, suppliers of thermal conductive adhesives, solid-state-compatible encapsulants, and dielectric sealants are well-positioned to capture long-term growth in the next-generation battery ecosystem.

Electrical & Electronics Adhesives Market Share Insights, 2025-2034

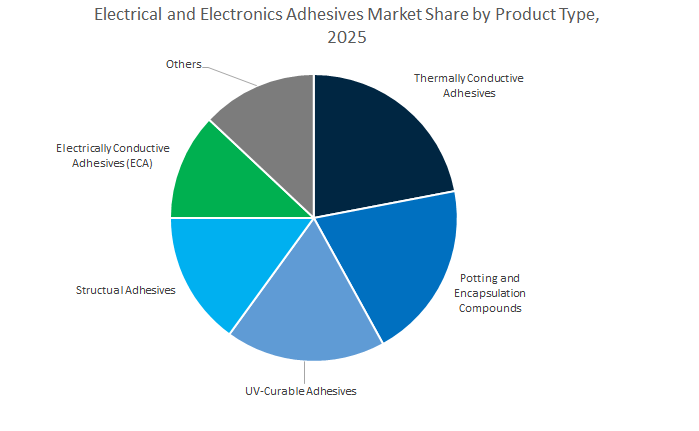

Thermally conductive adhesives hold the largest share of the global electrical and electronics adhesives market, primarily due to their indispensable role in thermal management of high-power electronic components. As electronic devices become smaller yet more powerful, efficient heat dissipation has become a defining design challenge. These adhesives, formulated with ceramic or metal oxide fillers, enable rapid heat transfer from components such as LEDs, power transistors, and EV battery packs to heat sinks or chassis, ensuring operational stability and extending component life. In the EV and 5G infrastructure sectors, thermal runaway prevention is paramount, and the adhesives’ dual functionality—structural bonding and heat conduction—makes them essential. Additionally, the growing deployment of miniaturized and high-density integrated circuits in smartphones, consumer devices, and electric vehicles further cements the dominance of this category. With rising global demand for energy-efficient electronics and high-power computing systems, thermally conductive adhesives are forecast to remain the industry’s cornerstone material for next-generation device reliability.

Potting and encapsulation compounds account for a significant portion of the electronics adhesives market, as the need for protecting sensitive electronic components from moisture, vibration, and thermal cycling continues to escalate. These materials act as environmental shields, encapsulating circuitry to prevent corrosion, dielectric breakdown, or mechanical stress damage. They are indispensable in automotive electronics, industrial control systems, and outdoor communication modules, where durability and insulation are key to system longevity. The transition to electric vehicles (EVs) has further amplified demand, as power electronics, sensors, and battery management systems must operate under extreme conditions. Formulations such as epoxy, polyurethane, and silicone encapsulants offer varying degrees of flexibility, thermal resistance, and electrical insulation—allowing OEMs to customize performance based on application needs. In addition, the integration of potting materials with low-halogen, flame-retardant, and reworkable chemistries aligns with environmental and recyclability goals. As electronics penetrate deeper into harsh-environment and safety-critical domains, potting and encapsulation compounds will remain indispensable for electronic system reliability and long-term protection.

UV-curable adhesives are a rapidly expanding segment within the market, driven by the increasing automation of electronics manufacturing. These adhesives enable instant, on-demand curing under ultraviolet light, offering unparalleled precision and throughput in production processes such as display bonding, touch panel lamination, camera module assembly, and lens mounting. The demand for high-transparency, low-outgassing, and non-yellowing formulations is growing, particularly in consumer electronics and optoelectronics manufacturing. In parallel, electrically conductive adhesives (ECAs) are gaining traction as a solder alternative in miniaturized and flexible electronics. They are critical for interconnecting delicate components, such as in printed circuit boards (PCBs), RFID tags, and flexible displays, where traditional soldering would cause heat damage. ECAs, including isotropic (ICAs) and anisotropic (ACAs) types, combine high conductivity with fine-pitch bonding capability, making them essential for next-generation semiconductor packaging and wearable electronics.

The consumer electronics and automotive & transportation industries drive the majority of global demand for electrical and electronics adhesives. In consumer electronics, adhesives play a critical role in smartphone assembly, flexible displays, wearable devices, and miniaturized sensors, where thin bond lines, transparency, and reworkability are essential for modern designs. The increasing adoption of foldable displays and 3D-structured surfaces has expanded the need for flexible, low-modulus adhesives that maintain durability under bending stress. Meanwhile, the automotive and EV sector represents the fastest-growing market, with adhesives indispensable for battery cell bonding, thermal interface management, and electronic module sealing. As vehicles transition toward electrification, manufacturers require adhesives that can withstand thermal cycling, vibration, and chemical exposure while maintaining electrical insulation. The integration of ADAS systems, radar sensors, and infotainment electronics further expands adhesive use across vehicle systems.

The computers and semiconductor segments are foundational to the global electronics adhesives market, contributing 14.4% and 11.8% of market share respectively. In the computers segment, adhesives are critical for component attachment, heat dissipation, and insulation in laptops, servers, and high-performance data centers. As cloud computing and artificial intelligence workloads intensify, demand for thermal interface materials (TIMs) and encapsulants that ensure stability under continuous load is rising rapidly. In the semiconductors and integrated circuits (IC) industry, adhesives are essential for die-attach, underfill, and packaging applications that ensure precision alignment and long-term electrical reliability. These processes require ultra-pure, low-ionic, high-performance materials that can handle the stresses of miniaturization and power density increases. The proliferation of advanced packaging technologies such as flip-chip, fan-out wafer-level packaging (FOWLP), and system-in-package (SiP) is further driving innovation in adhesive performance. As semiconductor fabrication advances toward sub-5nm nodes and 3D integration, high-purity, thermally conductive, and low-stress adhesives will become increasingly vital to ensure device reliability and yield.

The expansion of 5G communications, industrial automation, and medical electronics is opening new frontiers for high-performance adhesives. In communications, the deployment of 5G base stations and antenna systems requires adhesives with excellent dielectric properties, weatherability, and heat resistance to maintain signal stability and structural integrity under outdoor conditions. In the industrial sector, adhesives are essential for control units, power drives, and electric motors, where they must endure continuous operation in harsh environments involving heat, oil, and vibration. Meanwhile, the medical devices and wearables segment is growing rapidly, demanding biocompatible, skin-friendly, and sterilization-resistant adhesives for sensors, diagnostic equipment, and implantable electronics. These applications emphasize the need for precision dispensing, low-outgassing, and long-term reliability, aligning with regulatory and patient safety requirements.

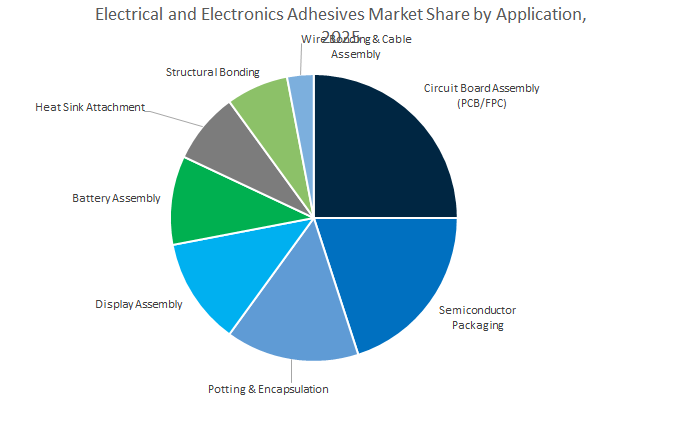

Market Share by Application

The competitive environment in the electrical and electronics adhesives market is characterized by strong innovation, strategic expansion, and sustainability-focused R&D across major multinational players. Companies such as 3M, Henkel, Dow, H.B. Fuller, Momentive, and Heraeus Group are continuously advancing adhesive technologies to support applications in semiconductors, EVs, 5G electronics, and wearable devices. These players are leveraging chemistry innovation — from silicone to epoxy and conductive polymers — to deliver superior thermal, dielectric, and structural performance across global manufacturing networks.

3M’s dominance stems from its vast technology portfolio in optical films, microreplication, and advanced materials science. Its Optically Clear Adhesives (OCA) remain indispensable for display components and flexible electronics. The company’s offerings, including Boron Nitride Cooling Fillers and Novec fluids, reinforce 3M’s leadership in thermal management adhesives for high-heat electronic components. Recently, 3M has intensified its focus on automated dispensing-compatible adhesives that accelerate production for contract manufacturers, particularly in smartphone and automotive display assembly.

Henkel, under its Loctite and Ablestik brands, leads in structural bonding for consumer electronics, enabling sleek, screw-free device designs. Its die-attach adhesives and electrically conductive films cater to IC and LED packaging, ensuring performance reliability. Henkel’s innovation is anchored in low-VOC and bio-based adhesive chemistry, meeting global sustainability mandates. Its thermal interface materials (TIMs) further enhance performance in automotive electronics and data center components, solidifying its integrated materials ecosystem.

Dow’s DOWSIL™ and SYLGARD™ product lines exemplify its expertise in high-performance silicones tailored for dielectric insulation, vibration resistance, and environmental sealing. The company has strengthened its footprint in e-mobility and automotive electronics, offering fast-cure RTV and heat-cure silicones for production throughput optimization. Dow continues to innovate in low-volatility silicones for sensor assemblies and display sealing, delivering durable protection for next-generation electronics.

H.B. Fuller is strategically investing in thermal management and high-reliability adhesives for EV batteries and industrial electronics. Its diverse chemistry portfolio — epoxy, polyurethane, and acrylic systems — supports structural bonding and sealing for high-performance enclosures. The company’s recent expansion of localized manufacturing enhances supply chain resilience, catering to global OEMs demanding fast delivery and technical support. Fuller’s expertise in substrate adhesion across metals, plastics, and ceramics ensures strong market differentiation.

Momentive specializes in RTV silicone sealants, conformal coatings, and silicone elastomers designed for PCB protection and electronic module sealing. The company’s materials offer high dielectric strength and temperature resistance, serving critical roles in power conversion and automotive electronics. Its solutions improve device reliability under shock, vibration, and environmental stress, cementing Momentive’s position as a key enabler of durable and efficient electronic systems.

Heraeus focuses on high-purity electrically conductive adhesives and die-attach pastes vital for semiconductor packaging and microelectronics. Its thermo-setting, solvent-free epoxy systems meet stringent lead-free compliance for advanced semiconductor applications. The company’s high-green-strength SMT adhesives enable high-speed placement in Surface Mount Technology (SMT) lines, preventing component shift and improving yield. By addressing 5G and data center demands through conductive polymers, Heraeus strengthens its position in high-frequency interconnects and precision electronics.

China remains the epicenter of global electronics manufacturing and assembly, accounting for a dominant share in semiconductor, PCB, and consumer electronics production. The country’s introduction of mandatory national standards for hazardous substance control in electronics, effective August 1, 2027, underscores its commitment to sustainability. The regulations mandate the reduction of heavy metals and persistent organic compounds (POCs) in adhesives, compelling local and foreign manufacturers to reformulate high-purity, RoHS-compliant adhesive chemistries.

With integrated circuit exports growing by 11.6%, demand for potting, encapsulation, and thermally conductive electronic adhesives continues to surge. China’s government-driven investments in 5G infrastructure, AI, and smart manufacturing are fostering large-scale adoption of UV-curable, low-outgassing adhesives that ensure reliable thermal and electrical performance in compact electronic devices. Additionally, the “Made in China” procurement policy favors domestic suppliers, prompting multinational firms to expand local production capabilities to maintain competitiveness.

The United States electrical and electronics adhesives market is driven by aerospace innovation, 5G expansion, and advanced manufacturing technologies. Major North American electronics manufacturers and defense contractors are emphasizing temperature-resistant and signal-preserving adhesives for mission-critical applications in satellites, radar, and next-generation communication systems. The rise of 5G network deployment and the rapid integration of Internet of Things (IoT) devices are significantly boosting the need for electrically conductive adhesives (ECA), which provide superior reliability in miniaturized circuit assemblies.

Key players such as 3M Company continue to expand their partnerships and R&D to meet the escalating demand for complex adhesive formulations across semiconductor, medical, and defense sectors. The U.S. also leads in eco-friendly electronic adhesive development, spurred by stringent EPA regulations promoting low-VOC, waterborne, and bio-based adhesive systems. With continuous growth in aerospace, automotive electronics, and medical devices, the U.S. remains a global hub for next-generation high-reliability adhesive technologies.

Germany is establishing itself as a pioneer in smart adhesive technologies and sustainable manufacturing innovation within the European electronics adhesives market. Henkel, headquartered in Düsseldorf, has successfully deployed AI-driven modeling through its partnership with Citrine Informatics, cutting R&D cycles in half for next-generation EV battery adhesives. The digital transformation accelerates the development of thermally stable, electrically insulating, and recyclable adhesive solutions optimized for high-performance electronic components.

German automotive leaders such as BMW and Volkswagen are applying structural and elastomeric adhesives to bond carbon fiber-reinforced plastics (CFRP) with aluminum, improving durability and noise-vibration-harshness (NVH) resistance in EVs and hybrid systems. Meanwhile, the EUR 50 billion investment by global semiconductor giants including TSMC, Intel, and Infineon in domestic chip fabrication is catalyzing massive demand for semiconductor-grade epoxy and silicone adhesives. The Industrieverband Klebstoffe (IVK) further supports eco-innovation by promoting recyclable adhesive formulations aligned with DIN/TS 54405 standards for circular design in electronics.

South Korea continues to dominate the global electronics adhesives market as a hub for semiconductor fabrication, smartphone production, and EV electronics. Its highly integrated ecosystem—anchored by companies like Samsung Electronics, LG Chem, and SK Innovation—fuels exceptional demand for high-precision, UV-cured, and thermally conductive adhesives used in chip packaging, printed circuit boards (PCBs), and micro-displays. The trend toward miniaturization in consumer devices has accelerated the adoption of low-viscosity, rapid curing adhesives that support compact, high-density assemblies.

The automotive electronics sector, driven by the national pivot toward electric mobility, is increasingly adopting reactive and moisture-curing adhesives to enhance battery module adhesion and electronic control unit (ECU) reliability. Additionally, UV-cured adhesives have carved out a niche in the medical device and display industries for precision bonding with minimal residue and rapid processing times. South Korea’s emphasis on innovation, automation, and export compliance ensures its continuous leadership in the Asia-Pacific electrical and electronics adhesives landscape.

Japan remains a key technological contributor to the global electrical and electronics adhesives industry, underpinned by large-scale investments in semiconductor and EV component production. Major foreign investments—such as TSMC’s second fab in Kumamoto and Micron Technology’s plant in Hiroshima—are rapidly scaling domestic manufacturing capacity, boosting demand for ultra-pure, high-thermal-conductivity adhesives essential for wafer bonding and chip packaging. Government policies promoting local production of semiconductors and EV components through tax incentives have further reinforced Japan’s adhesive ecosystem.

The automotive electronics segment continues to dominate the market as manufacturers integrate driver-assistance systems (ADAS) and advanced electronic modules, requiring adhesives that ensure vibration resistance, conductivity, and thermal management. Additionally, the growth of IoT applications has expanded the need for microelectronic-grade adhesives in sensors and communication devices. Japan’s precision manufacturing capabilities and leadership in functional monomer development solidify its reputation as a global benchmark for high-performance electronics adhesive production.

India’s electrical and electronics adhesives market is entering a high-growth phase, driven by domestic manufacturing expansion, EV adoption, and digital industrialization. In July 2024, Henkel Adhesive Technologies India completed Phase III expansion of its Kurkumbh facility, significantly increasing local production capacity for thermal management adhesives and assembly bonding materials. The aligns with the government’s Make in India and PLI (Production-Linked Incentive) schemes, which are drawing global electronics manufacturers to establish local supply chains.

The electric vehicle boom, with over 1.17 million units sold in FY2023, is propelling demand for advanced bonding and potting adhesives in battery packs, wiring harnesses, and electronic control systems. The adoption of Industry 4.0 technologies, including AI-driven monitoring and automated dispensing systems, is enhancing production precision and efficiency. Furthermore, India’s fast-growing electronics assembly sector requires heat-dissipating and electrically insulating adhesives for semiconductor packaging and PCB protection—marking the country as a rising manufacturing powerhouse in Asia.

Electrical & Electronics Adhesives Market Report Scope

Electrical & Electronics Adhesives Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$5.3 Billion

|

|

Market Size (2034)

|

$9.7 Billion

|

|

Market Growth Rate

|

7%

|

|

Segments

|

By Resin Type (Epoxy, Silicone, Polyurethane, Acrylic, Cyanoacrylate, Others), By Product Type (Electrically Conductive Adhesives, Thermally Conductive Adhesives, UV-Curable Adhesives, Potting and Encapsulation Compounds, Structual Adhesives, Others), By End-Use Industry (Computers, Communications, Consumer Electronics, Industrial, Medical Devices & Wearables, Transportation, Semiconductors & Integrated Circuits, Others), By Application (Surface-Mount Devices, Circuit Board Assembly, Wire Bonding & Cable Assembly, Potting & Encapsulation, Display Assembly, Battery Assembly, Heat Sink Attachment, Structural Bonding), By Form (Liquid, Paste, Film & Tape, Solid

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Henkel AG & Co. KGaA, 3M Company, Dow Inc., Sika AG, H.B. Fuller Company, Arkema Group, Huntsman International LLC, Wacker Chemie AG, DELO Industrial Adhesives, Avery Dennison Corporation, Pidilite Industries Ltd., DuPont, NANPAO RESINS CHEMICAL GROUP, Shin-Etsu Chemical Co., Ltd.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

By Resin Type

- Epoxy

- Silicone

- Polyurethane

- Acrylic

- Cyanoacrylate

- Others

By Product Type

- Electrically Conductive Adhesives

- Thermally Conductive Adhesives

- UV-Curable Adhesives

- Potting and Encapsulation Compounds

- Structual Adhesives

- Others

By End-Use Industry

- Computers

- Communications

- Consumer Electronics

- Industrial

- Medical Devices & Wearables

- Transportation

- Semiconductors & Integrated Circuits

- Others

By Application

- Surface-Mount Devices

- Circuit Board Assembly

- Wire Bonding & Cable Assembly

- Potting & Encapsulation

- Display Assembly

- Battery Assembly

- Heat Sink Attachment

- Structural Bonding

By Form

- Liquid

- Paste

- Film & Tape

- Solid

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

- Henkel AG & Co. KGaA

- 3M Company

- Dow Inc.

- Sika AG

- H.B. Fuller Company

- Arkema Group

- Huntsman International LLC

- Wacker Chemie AG

- DELO Industrial Adhesives

- Avery Dennison Corporation

- Pidilite Industries Ltd.

- DuPont

- NANPAO RESINS CHEMICAL GROUP

- Shin-Etsu Chemical Co., Ltd.

*- List not Exhaustive

Research Coverage

Prepared by USDAnalytics, this report investigates the Electrical and Electronics Adhesives Market, delivering analysis reviews on demand inflection points across EVs, 5G infrastructure, data-center hardware, and advanced packaging while mapping material selection to throughput, reliability, and compliance needs. It highlights breakthroughs in thermally conductive yet electrically insulating systems, low-outgassing optics-grade epoxies, UV/moisture dual-cure formulations for automated lines, and UL94 V-0 flame-retardant encapsulants that safeguard high-power, miniaturized assemblies. By aligning performance benchmarks (thermal conductivity, dielectric strength, Tg, CTE, MTTF) with cost-to-serve and localization trends, this report is an essential resource for materials leaders, process engineers, sourcing heads, and strategy teams seeking defensible choices for next-generation electronics manufacturing.

Scope Highlights

Segmentation:

- By Resin Type: Epoxy; Silicone; Polyurethane; Acrylic; Cyanoacrylate; Others.

- By Product Type: Electrically Conductive Adhesives; Thermally Conductive Adhesives; UV-Curable Adhesives; Potting & Encapsulation Compounds; Structural Adhesives; Others.

- By End-Use Industry: Computers; Communications; Consumer Electronics; Industrial; Medical Devices & Wearables; Transportation; Semiconductors & Integrated Circuits; Others.

- By Application: Surface-Mount Devices; Circuit Board Assembly; Wire Bonding & Cable Assembly; Potting & Encapsulation; Display Assembly; Battery Assembly; Heat Sink Attachment; Structural Bonding.

- By Form: Liquid; Paste; Film & Tape; Solid.

Geographic Scope: Analysis spans 25+ countries across North America, Europe, Asia Pacific, Latin America, the Middle East & Africa.

Time Frame: Historic data 2021–2024 and forecasts 2025–2034.

Companies: 15+ company analyses/profiles covering portfolios, capacity moves, partnerships, and innovation pipelines.

Deliverables

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.