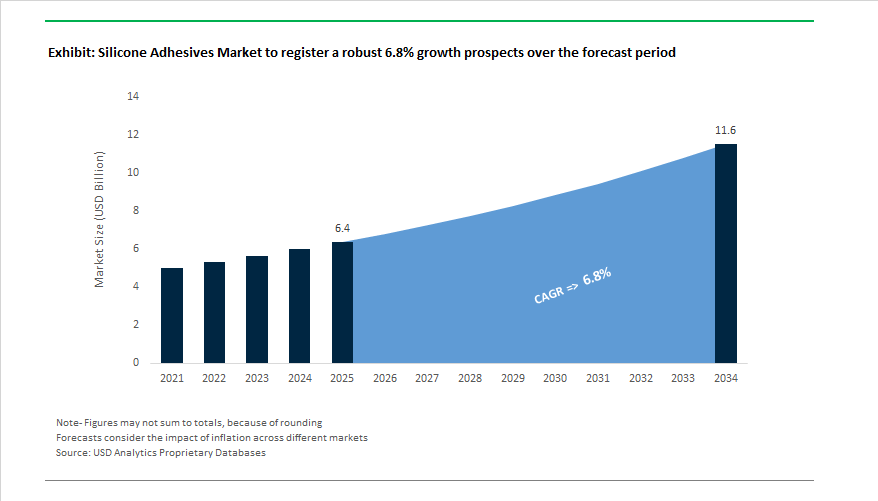

The Global Silicone Adhesives Market is projected to grow from $6.4 billion in 2025 to $11.6 billion by 2034, exhibiting a compound annual growth rate (CAGR) of 6.8%. This steady expansion is driven by the increasing use of high-performance silicone bonding systems across industries that demand durability, flexibility, dielectric strength, and extreme temperature stability — from electric vehicles (EVs) and aerospace propulsion systems to semiconductor protection and medical device assembly.

Silicone adhesives outperform conventional organic polymers due to their exceptional resistance to heat, UV radiation, ozone, and chemical degradation, ensuring reliability under the harshest environmental conditions. In automotive applications, two-component (2K) high-temperature silicone adhesives maintain cohesive strength from −60°C to over 300°C, supporting gasketing and bonding in engine compartments, exhaust assemblies, and EV power modules. Meanwhile, in electronics, silicone-based conformal coatings and encapsulants with dielectric strengths exceeding 15 kV/mm are critical for sensor protection, PCB insulation, and semiconductor packaging—all essential for miniaturized and high-power-density electronic designs.

In EV battery technology, the adoption of thermally conductive silicone adhesives capable of 5.0 W/(m·K) heat transfer has become pivotal for maintaining safe operating temperatures in lithium-ion cells, reducing thermal runaway risk, and extending battery service life. The aerospace and composites segment further relies on aerospace-grade silicone adhesives with joint movement tolerances exceeding ±50%, designed for aircraft windows, fuel tanks, and composite structural assemblies, ensuring over a decade of field durability.

The past 18 months have marked a critical period for transformation in the silicone adhesives industry, with manufacturers prioritizing sustainable chemistry, high-temperature resistance, and electronics integration.

In October 2025, Wacker Chemie AG introduced a biomethanol-based silicone sealant for natural stone, marking a major milestone in sustainable adhesive manufacturing. This new range reduces fossil feedstock dependency while maintaining the high elasticity and low-bleed properties required for architectural and façade sealing applications. Earlier, in March 2025, Wacker debuted a low-volatile (LV) epoxy-polysiloxane hardener system designed for metal coatings and structural adhesives, aligning with stricter EU VOC emission limits in construction and manufacturing.

Dow Inc. has strengthened its automotive materials leadership, announcing in September 2025 the expansion of its DOWSIL™ thermally conductive silicone compounds portfolio for next-generation automotive control units (ECUs) and power electronics. These formulations deliver enhanced vibration resistance and superior thermal cycling performance, addressing the critical durability demands of electric vehicles. Similarly, in February 2025, Dow launched its low-VOC DOWSIL™ 991 Sealant—a non-staining silicone engineered for porous substrates such as natural stone—tailored for sustainable architecture and building envelope applications.

In the electronics domain, Shin-Etsu Chemical Co., Ltd. introduced a new high-performance silicone coating material line in May 2025, offering thermal stability, moisture protection, and low internal stress, ideal for semiconductor packaging and high-density power devices. This complements the growing demand for dielectric silicone coatings used in 5G, semiconductor, and EV inverter systems.

Momentive Performance Materials Inc., in June 2025, expanded its fully-fluorinated silicone rubber (FFSL) product line, enhancing fuel, oil, and solvent resistance in complex automotive sealing applications. The firm also reported new Liquid Silicone Rubber (LSR) applications specified by leading automotive suppliers for ADAS optical systems, validating the role of transparent silicone adhesives in advanced optical bonding.

Meanwhile, Henkel AG & Co. KGaA, in August 2025, reaffirmed its strategic direction by prioritizing Mobility & Electronics through significant R&D and digitalization investments. The company continues to optimize Loctite® and Technomelt® silicone adhesive solutions for thermal management, sealing, and electronics assembly, emphasizing low-curing-time products suited for high-volume production environments.

Market Trend 1: Accelerated Adoption of UV and Light-Cure Silicone Adhesives for High-Speed Electronics Manufacturing

The global trend toward rapid, automated, and high-precision manufacturing in sectors such as consumer electronics, EV battery assembly, and micro-optics is driving a surge in demand for UV and light-cure silicone adhesives. These formulations represent a breakthrough over conventional moisture- or heat-curing systems by delivering exceptional curing speed, minimal heat exposure, and high process control.

Leading manufacturers report that UV-cure silicone systems can achieve initial cure in just 10 to 40 seconds under UV-LED irradiation conditions of 100–300 mW/cm² at 365 nm, dramatically improving throughput on fast-moving assembly lines. The capability has made light-cure silicone adhesives a cornerstone for Printed Circuit Board (PCB) bonding, flexible displays, optical sensors, and microelectronic assemblies, where precision and repeatability are paramount.

A key technical advantage of light-cure silicones lies in their low thermal stress, eliminating the risk of heat-related component degradation that often accompanies oven-based or hot-cure systems. Their uncured stability until exposure enables exact dispensing and jetting automation, essential for miniaturized and optical assemblies in smartphones, wearables, and automotive infotainment displays. Further, UV-cure silicone adhesives align perfectly with green manufacturing standards, as their formulations are typically solvent-free and VOC-compliant, enabling sustainability compliance under EPA, REACH, and RoHS frameworks.

Market Trend 2: Reformulation to Eliminate Platinum Catalysts for Chemical and Thermal Stability in Harsh Environments

The reliance on platinum-catalyzed addition-cure silicones—long the industry standard for premium bonding—has come under scrutiny due to cure inhibition issues and cost volatility. Industrial applications in automotive, aerospace, and chemical processing environments often involve exposure to inhibitors such as amines, sulfides, and tin salts, which can deactivate platinum catalysts and compromise adhesion integrity.

The has catalyzed a global reformulation shift toward non-platinum neutral-cure chemistries, including oxime-cure and alkoxy-cure silicone systems. These condensation-based technologies are inherently resistant to chemical poisoning, ensuring consistent cure performance even in contaminated or mixed-material environments. For instance, oxime-cure silicones exhibit stable adhesion on corrosion-prone metals like chrome, copper, and steel, while maintaining reliable sealing and elasticity across a temperature range of −40°C to +150°C—making them ideal for under-the-hood automotive and industrial applications.

Additionally, regulatory efforts to restrict hazardous volatile byproducts—such as MEKO (Methyl Ethyl Ketoxime)—are driving innovation toward non-oxime neutral-cure silanes and low-emission condensation systems. These new catalysts achieve high performance while meeting indoor air quality (IAQ) and REACH Annex XVII compliance.

As industries demand greater chemical resilience, mechanical integrity, and environmental safety, non-platinum silicone adhesives are emerging as the new standard in hostile or contamination-prone operating environments.

Market Opportunity 1: Development of Thermally Conductive, Electrically Insulating Silicone Adhesives for EV Power Electronics

The electrification of the global automotive sector is fueling innovation in thermally conductive yet electrically insulating silicone adhesives—a critical technology for ensuring efficient heat management and electrical isolation in high-voltage power electronics.

Advanced thermally conductive silicone potting and gap-filling materials achieve thermal conductivities up to 2.3 W/m·K, allowing superior heat dissipation in EV inverters, DC/DC converters, and onboard chargers. Simultaneously, they maintain dielectric strengths ≥20 kV/mm, ensuring insulation integrity for components operating between 400–800V. The dual-functionality—heat conduction without electrical compromise—is vital to preventing short circuits and extending the lifespan of high-power modules.

These high-performance silicones also exhibit remarkable thermal endurance, maintaining stable hardness and tensile properties even after thousands of operating hours at 150°C. The durability minimizes mechanical fatigue and supports the reliability of EV electronics under constant vibration and heat exposure.

Economically, thermally conductive adhesives enable manufacturers to replace traditional mechanical fasteners and complex housings, simplifying assembly and reducing overall production costs. As automakers accelerate toward mass electrification, the integration of thermal, electrical, and mechanical performance within a single adhesive material represents a defining opportunity for market differentiation and scalability.

Market Opportunity 2: Development of High-Refractive-Index Optical Silicone Adhesives for AR Waveguide Displays

The emergence of Augmented Reality (AR), Mixed Reality (MR), and wearable optical systems is creating a high-value niche for high-refractive-index (HRI) silicone adhesives capable of bonding precision optical components such as waveguide combiners, micro-displays, and lens assemblies. These adhesives play a critical role in maximizing light transmission efficiency and visual fidelity across multi-layer optical interfaces.

In optical engineering, precise refractive index (RI) matching is essential to minimize Fresnel reflection losses. While standard silicones possess RI values around 1.4, cutting-edge HRI silicones are being engineered to achieve refractive indices as high as 1.47, offering improved optical coupling and light throughput for next-generation AR devices. These adhesives exhibit optical transmittance ≥90% at 1 mm thickness and haze values ≤1, ensuring ultra-clear bonding without distortion or light scattering.

Additionally, ultra-low shrinkage during curing prevents birefringence and misalignment in sensitive optical stacks, safeguarding image precision in thin, multi-layer AR assemblies. Their moisture resistance, elasticity, and long-term clarity ensure stability under thermal cycling and daily consumer use, aligning with the durability standards of wearable electronics.

Silicone Adhesives Market Share Insights, 2025-2034

Market Share by Product Type

One-Component Silicone Adhesives dominate the global silicone adhesives market, accounting for an estimated 68.4% market share by 2025. Their leadership is attributed to exceptional ease of use, single-package convenience, and broad applicability across construction, transportation, and general industrial sectors. These systems cure under ambient moisture without requiring mixing, enabling faster processing and reduced labor in both field and factory environments. One-component silicone adhesives are extensively used for structural glazing, sealing, and general-purpose bonding due to their ability to maintain elasticity, adhesion, and mechanical integrity across extreme temperatures and environmental conditions. Moreover, the global shift toward low-maintenance and high-performance bonding materials has strengthened demand for these formulations, particularly in infrastructure, automotive, and electronics assembly where reliability and weatherability are critical. Their compatibility with a wide range of substrates such as glass, metals, plastics, and composites further enhances their adoption in diverse end-use industries.

On the other hand, Two-Component Silicone Adhesives maintain an important niche in the high-performance and precision bonding segment. These systems are specifically designed for applications requiring rapid curing, thick bond line formation, or precise process control, such as in electronics encapsulation, aerospace composites, and solar energy module assembly. Two-component systems offer greater flexibility in curing profiles and improved performance in environments where moisture cure is inadequate, making them preferred for controlled manufacturing conditions and automated assembly lines. As manufacturers move toward miniaturization and high-precision bonding, demand for two-component silicone adhesives is expected to grow steadily, particularly in electric vehicles, advanced electronics, and medical device assembly.

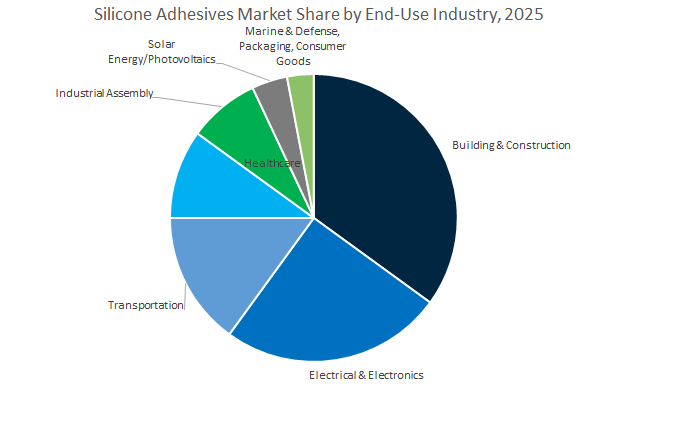

Market Share by End-Use Industry

The Building & Construction sector leads the global silicone adhesives market, representing 34.6% of the total market share in 2025, underpinned by rapid urbanization, infrastructure development, and increasing adoption of high-performance sealing materials in both residential and commercial projects. Silicone adhesives are indispensable in structural glazing, curtain wall bonding, window and door sealing, and waterproofing applications, offering unmatched UV resistance, thermal stability, and elasticity. The material’s ability to maintain performance under severe weather conditions makes it the preferred choice for façade engineering, green buildings, and prefabricated modular construction. Growing emphasis on energy efficiency and sustainable building practices further drives demand for silicone adhesives with low-VOC formulations and enhanced thermal insulation compatibility. In both new construction and retrofit projects, silicone’s versatility in bonding dissimilar materials ensures its continued dominance in this sector.

The Electrical & Electronics industry represents a rapidly expanding segment, fueled by the global proliferation of smart devices, 5G infrastructure, and electric vehicles (EVs). Silicone adhesives play a vital role in potting, encapsulation, and component bonding, ensuring superior electrical insulation and protection against moisture, dust, and thermal stress. Their dielectric properties and thermal management capabilities make them indispensable in semiconductor packaging, LED assembly, and sensor integration. The Transportation sector also contributes significantly to market growth, as silicone adhesives are increasingly adopted in vehicle body assembly, glass bonding, and vibration-dampening applications for both traditional and electric vehicles. In aerospace and rail transport, they deliver lightweighting benefits, durability, and long-term fatigue resistance.

Healthcare emerges as a high-value niche within the silicone adhesives market, driven by applications in medical devices, wearables, and prosthetics. Biocompatible silicone adhesives are essential for implantable devices, wound dressings, and transdermal patches, owing to their flexibility, hypoallergenic nature, and sterilization resistance. The Industrial Assembly and Solar Energy/Photovoltaics sectors follow closely, using silicone adhesives for assembly operations, component sealing, and panel encapsulation to improve efficiency and durability. Meanwhile, Marine, Defense, Packaging, and Consumer Goods applications represent specialized but steady demand streams where silicone adhesives are valued for moisture resistance, corrosion protection, and long service life.

The Global Silicone Adhesives Market remains consolidated, with the top five companies—Dow Inc., Henkel AG & Co. KGaA, Wacker Chemie AG, Shin-Etsu Chemical Co., Ltd., and Momentive Performance Materials Inc.—collectively accounting for over 70% of global production capacity. Each company leverages vertical integration, sustainability strategies, and advanced polymer R&D to sustain competitiveness.

Dow operates one of the world’s most advanced silicone value chains, offering the DOWSIL™ range of 1K and 2K RTV silicone adhesives and sealants designed for temperature extremes (−70°C to 350°C) and elongation capabilities exceeding 800%. Dow’s core strength lies in its thermally conductive silicone technologies for EV batteries and inverters, and its low-VOC construction sealants for façade and glazing applications. The company’s continuous investment in bio-based silicone systems and smart formulation design reinforces its position as the leader in high-performance silicone adhesive technologies.

Henkel leads the global adhesive technologies segment, offering one-component silicone adhesives under its Loctite® line that achieve tack-free times under 10 minutes, enabling rapid assembly line throughput. Its Technomelt® and Loctite® solutions are integral to thermal management and powertrain sealing in electric mobility. Henkel’s 2025 investments in AI-driven R&D platforms and regional production hubs (e.g., India and China) have strengthened its supply agility and market responsiveness. Its medical-grade adhesives also comply with ISO 10993 and USP Class VI, serving as benchmarks for biocompatibility.

Wacker Chemie AG has established itself as a leader in bio-based and silane-modified polymer (SMP) silicone systems, focusing on hybrid formulations that offer tear resistance exceeding 30 N/mm and improved adhesion to diverse substrates. Its α³ Technology Platform and DEHESIVE® PSAs provide superior performance in high-temperature tapes and release liners. In 2025, Wacker expanded its biomethanol-based silicone product line, confirming its status as a pioneer in sustainable silicone chemistry for both industrial and consumer applications.

Shin-Etsu continues to dominate the high-purity silicone market with specialized electronic-grade materials offering enhanced dielectric insulation and low moisture permeability. Its advanced silicone coatings for semiconductors provide heat stability and stress relief critical for power electronics and sensor modules. The company’s optical encapsulant materials and thermal interface silicones are widely used in LED, EV, and semiconductor manufacturing, reflecting its precision-engineering legacy in functional silicone materials.

Momentive is a global leader in automotive-grade LSR and RTV silicone adhesives, specializing in products capable of curing at 150°C or above for rapid manufacturing cycles. Its silicone materials, such as the TSE and SilCool™ series, are designed to ensure thermal conductivity and low modulus properties ideal for ADAS sensors, EV cameras, and power electronics. Momentive’s high-transparency silicone elastomers for optical systems and fuel-resistant fluorosilicones for mobility applications highlight its depth in next-generation material performance.

Country Analysis: Active Developments Defining the Global Silicone Adhesives Industry

China: Expanding Production and Construction Drive Silicone Adhesive Growth Across Asia-Pacific

China remains the undisputed powerhouse in the global silicone adhesives market, driven by its strong manufacturing infrastructure, rapid industrialization, and aggressive investment in green construction and electric mobility. In 2024, chemical manufacturing investment surged by 8.9%, reinforcing domestic supply chains for high-performance silicone elastomers and resins essential to building, automotive, and electronics applications. Multinational giants like Dow and Wacker Chemie AG have increased their local R&D presence and introduced carbon-neutral silicone adhesive formulations tailored for the country’s massive construction and façade sealing projects, supporting China’s decarbonization and sustainable urbanization goals.

The construction sector continues to be a dominant demand driver, with new floor area expected to reach 14.2 billion square feet by 2027, creating strong consumption for structural silicone sealants in curtainwall, glazing, and high-rise infrastructure. Furthermore, China’s leading role in electric vehicle (EV) manufacturing — producing nearly 60% of global EV batteries — is accelerating the adoption of heat-cure and thermally conductive silicone adhesives for battery encapsulation, power module bonding, and thermal management systems. As both domestic and international firms scale up localized production, China solidifies its position as the largest and fastest-growing market for industrial and construction-grade silicone adhesives in the Asia-Pacific region.

United States: Medical-Grade Innovation and Sustainable Building Sealants Define Market Momentum

The United States silicone adhesives industry is advancing rapidly through innovation in medical-grade adhesives, energy-efficient construction materials, and high-performance electronics applications. A key highlight came in February 2023, when 3M Company introduced a medical-grade silicone adhesive capable of adhering to skin for up to 28 days, revolutionizing long-term medical wearable applications and doubling the previous industry benchmark. The advancement aligns with a broader U.S. trend toward biocompatible, skin-safe, and breathable silicone formulations in the growing medical device and life sciences sectors.

Simultaneously, the U.S. construction sector is witnessing surging demand for low-VOC, neutral-cure silicone sealants, driven by stricter LEED-certified green building standards and new energy-efficiency codes. Manufacturers are also increasing R&D in UV-cured silicone adhesives to improve assembly speeds for electronics, EVs, and semiconductor packaging. The acquisition of U.S.-based silicone-coated healthcare product manufacturers by companies such as Wacker Chemie AG (May 2024) demonstrates a strategic effort to consolidate the healthcare silicone segment. Supported by regulatory incentives for energy retrofit programs and an expanding medical-grade silicone adhesive ecosystem, the U.S. market continues to be a global center of high-innovation and sustainable silicone technologies.

Germany: E-Mobility and Regulatory Compliance Fuel Advanced Silicone Adhesive Engineering

Germany remains a European leader in silicone adhesive manufacturing, with a strong focus on automotive electrification, sustainability, and precision industrial applications. Industry giants like Henkel AG & Co. KGaA and Wacker Chemie AG dominate the market, driving innovation in high-temperature, low-emission silicone bonding solutions for EVs and high-performance machinery. The introduction of EU REACH restrictions on specific cyclic siloxanes has accelerated the transition toward compliant, eco-friendly silicone formulations that maintain strength, elasticity, and long-term stability in demanding environments.

Germany’s automotive sector, which represents over 20% of the country’s manufacturing output, increasingly relies on silicone adhesives for battery sealing, heat dissipation, and lightweight structural assembly. In parallel, major R&D investments in digitalized specialty chemical laboratories, particularly at facilities like BYK-Chemie (Altana Group, 2024), are improving the efficiency and traceability of silicone product development. Germany’s integration of automated production technologies, low-VOC innovations, and renewable energy utilization underpins its role as a benchmark for sustainable, high-performance silicone adhesive engineering in Europe.

India: Infrastructure Growth and Domestic Manufacturing Propel Silicone Adhesive Demand

India’s silicone adhesives market is experiencing exponential growth, driven by rapid infrastructure expansion, housing development programs, and local manufacturing advancements. Government-backed initiatives like the Smart Cities Mission and Pradhan Mantri Awas Yojana (PMAY) continue to generate vast demand for elastic silicone sealants in waterproofing, curtainwall systems, and glass façades. In addition, India’s manufacturing value surpassed USD 461 billion in 2024, boosting consumption of industrial-grade silicone adhesives across machinery assembly, electronics, and automotive manufacturing.

Local and multinational players, including Pidilite Industries, Sika India, and McCoy Soudal, are investing in regional R&D and distribution partnerships to enhance market reach and tailor products for India’s hot, humid climate conditions. The domestic focus on ISO-10993-certified silicone adhesives for medical and semiconductor packaging further underscores the country’s pivot toward higher-value, precision-based manufacturing. Supported by government incentives for local production and sustainable building technologies, India is emerging as a key growth engine in the global silicone adhesives landscape, bridging Asia-Pacific’s industrial expansion and global supply chain diversification.

South Korea: Specialty Silicone Expansion Anchored in Electronics and Automotive Innovation

South Korea has established itself as a critical hub for high-purity silicone adhesives catering to electronics, semiconductors, and automotive engineering. In January 2025, Wacker Chemie AG inaugurated a new specialty silicones production facility in the country, reinforcing its regional capacity to meet the rising demand for construction, automotive, and high-tech manufacturing sectors. The nation’s leadership in semiconductor fabrication drives heavy reliance on silicone encapsulants, potting compounds, and bonding agents that offer excellent dielectric properties and reliability for miniaturized devices.

In the automotive sector, South Korea’s rapid adoption of electric mobility fuels the need for high-temperature silicone adhesives used in battery modules, EV charging components, and powertrain insulation. The developments are supported by collaborations between domestic manufacturers and global chemical companies, ensuring steady innovation in thermally conductive and low-outgassing silicone formulations. South Korea’s synergy of cutting-edge materials science, high-tech manufacturing infrastructure, and export-driven industrial strategy ensures its continued prominence in the Asia-Pacific silicone adhesives supply chain.

United Kingdom: Regulatory Compliance and Aerospace Applications Drive Advanced Silicone Demand

The United Kingdom’s silicone adhesives industry is evolving under strong regulatory and sustainability pressures, especially amid the nation’s Net-Zero 2050 commitments and the EU-wide Renovation Wave Policy. The initiatives are boosting adoption of high-insulation, low-carbon silicone sealants for energy-efficient retrofits and large-scale residential and commercial renovations. The government’s energy-saving targets have made silicone adhesives a critical enabler for air-tight, weatherproof building envelopes and long-lasting waterproof sealing solutions.

Simultaneously, the UK’s aerospace and defense sectors maintain significant demand for flame-retardant, high-strength silicone structural adhesives that comply with strict international safety certifications. Companies such as Henkel (Loctite) and Momentive are expanding their portfolios with high-temperature-resistant silicone formulations for aerospace-grade bonding, vibration damping, and maintenance repair operations (MRO). Investments in low-carbon manufacturing technologies and sustainable raw material sourcing further reinforce the UK’s trajectory as a leader in high-performance silicone adhesives for advanced engineering and construction applications.

Silicone Adhesives Market Report Scope

Silicone Adhesives Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$6.4 Billion

|

|

Market Size (2034)

|

$11.6 Billion

|

|

Market Growth Rate

|

6.8%

|

|

Segments

|

By Product Type (One-Component, Two-Component), By Technology (Room Temperature Vulcanizing, Heat Cured, Liquid Silicone Rubber, Pressure-Sensitive Adhesives, UV-Cured), By End-Use Industry (Building & Construction, Transportation, Electrical & Electronics, Healthcare, Packaging, Consumer Goods, Industrial Assembly, Solar Energy/Photovoltaics, Marine & Defense), By Curing Mechanism (Condensation, Addition

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Henkel AG & Co. KGaA, Dow Inc., Wacker Chemie AG, Shin-Etsu Chemical Co., Ltd., 3M Company, Sika AG, Momentive Performance Materials Inc., Arkema Group (Bostik), H.B. Fuller Company, Huntsman Corporation, KCC Silicone Corporation, Elkem ASA, Evonik Industries AG, Illinois Tool Works Inc. (ITW), Pidilite Industries Ltd.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

By Product Type

- One-Component

- Two-Component

By Chemistry/Technology

- Room Temperature Vulcanizing

- Heat Cured

- Liquid Silicone Rubber

- Pressure-Sensitive Adhesives

- UV-Cured

By End-Use Industry

- Building & Construction

- Transportation

- Electrical & Electronics

- Healthcare

- Packaging

- Consumer Goods

- Industrial Assembly

- Solar Energy/Photovoltaics

- Marine & Defense

By Curing Mechanism

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in Silicone Adhesives Market

- Henkel AG & Co. KGaA

- Dow Inc.

- Wacker Chemie AG

- Shin-Etsu Chemical Co., Ltd.

- 3M Company

- Sika AG

- Momentive Performance Materials Inc.

- Arkema Group (Bostik)

- H.B. Fuller Company

- Huntsman Corporation

- KCC Silicone Corporation

- Elkem ASA

- Evonik Industries AG

- Illinois Tool Works Inc. (ITW)

- Pidilite Industries Ltd.

*- List not Exhaustive

Research Coverage

Prepared by USDAnalytics, this report investigates the Global Silicone Adhesives Market at the intersection of electrification, lightweighting, and micro-electronics, mapping how chemistry breakthroughs—from UV/light-cure systems to thermally conductive, electrically insulating grades—are accelerating adoption in EV power electronics, aerospace composites, and high-reliability semiconductor packaging; our analysis reviews capacity moves, feedstock dynamics, standards compliance, and OEM specification trends, and highlights performance deltas versus organic polymers in extreme temperature, vibration, and dielectric environments—making this report an essential resource for product managers, sourcing leaders, application engineers, and investors seeking defensible forecasts, technology roadmaps, and competitor positioning through 2034.

Scope Highlights

Segmentation:

- By Product Type: One-Component; Two-Component.

- By Chemistry/Technology: Room Temperature Vulcanizing; Heat Cured; Liquid Silicone Rubber; Pressure-Sensitive Adhesives; UV-Cured.

- By End-Use Industry: Building & Construction; Transportation; Electrical & Electronics; Healthcare; Packaging; Consumer Goods; Industrial Assembly; Solar Energy/Photovoltaics; Marine & Defense.

- By Curing Mechanism: Condensation; Addition.

- By Region: North America (United States, Canada, Mexico); Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe); Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC); South & Central America (Brazil, Argentina, Rest of SCA); Middle East & Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa).

Geographic Scope: Analysis spans 25+ countries across North America, Europe, Asia Pacific, Latin America, the Middle East & Africa.

Timeframe: Historic data 2021–2024 and forecast data 2025–2034.

Companies Covered: Analysis / profiles of 15+ companies.

Deliverables

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.