Market Overview: Silicone and Hybrid Sealants Anchor Durability, Movement Control, and Low-Emission Compliance in Modern Construction

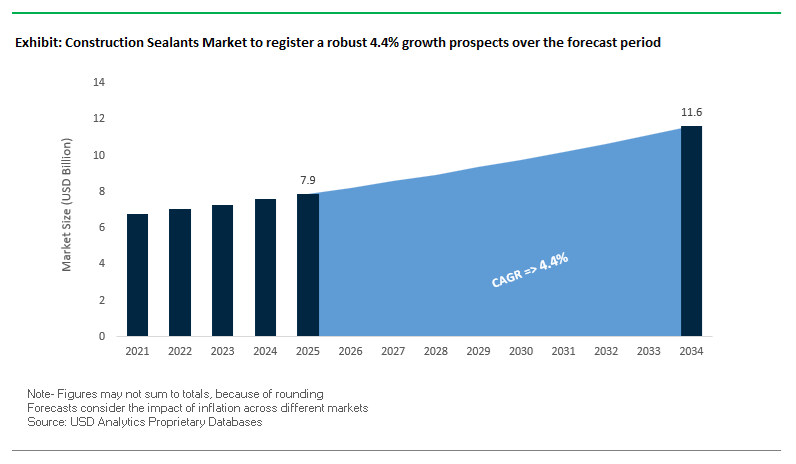

Construction sealants have become structurally consequential materials as building envelopes grow taller, lighter, and more movement-sensitive under modern design codes. The global construction sealants market, expanding from USD 7.9 billion in 2025 to USD 11.6 billion by 2034 at a CAGR of 4.4%, reflects this shift from cosmetic joint filling to performance-critical sealing systems. For façade engineers, glazing contractors, and infrastructure owners, sealants directly determine long-term weather tightness, joint durability, and building energy performance rather than serving as secondary consumables.

The core demand shift is driven by the replacement of traditional oil-based and low-performance mastics with silicone, polyurethane, and silane-modified polymer (SMP) sealants engineered for high movement capability, UV stability, and decades-long service life. Silicone sealants continue to command the largest resin share because manufacturers qualify them for structural glazing and façade joints exposed to sustained thermal cycling, moisture ingress, and ultraviolet radiation, with operational temperature resistance extending from –50 °C to +150 °C. In parallel, hybrid SMP sealants are increasingly specified where contractors require paintability, low shrinkage, and adhesion to mixed substrates without primers—particularly in modular construction and prefabricated façade assemblies. These materials are systematically displacing legacy acrylics and bituminous sealants that fail under long-term joint movement or environmental exposure.

Performance metrics increasingly translate directly into lifecycle economics. Low-modulus formulations with high elastic recovery reduce joint failure and façade maintenance cycles, while neutral-cure and water-based polyurethane systems support compliance with LEED, BREEAM, and WELL requirements by meeting EMICODE EC1+, ISO 16000, and GREENGUARD indoor air quality standards. Manufacturers are scaling low-VOC, low-odor chemistries to align with urban construction mandates and public-building specifications, particularly in high-growth markets such as India, Indonesia, and Brazil. Over the forecast period, competitive positioning in the construction sealants market will depend on manufacturers’ ability to deliver certified durability, movement accommodation, and emission compliance at scale, while supporting faster installation and long-term envelope performance across increasingly complex building designs.

The global construction sealants industry is witnessing a series of strategic developments, highlighting an industry-wide push toward fire safety, regional manufacturing capacity, and sustainable chemistry.

In September 2025, Dow Inc. introduced the DOWSIL™ Fire Protection Sealant, a new formulation engineered to prevent smoke and flame spread across structural penetrations such as cable ducts and pipe chases. This launch directly addresses the rising adoption of fire-rated joint sealing solutions amid stricter building codes in North America and Europe. Around the same time, Wacker Chemie AG broke ground on a new silicone specialty production site in Karlovy Vary, Czech Republic, with production of room-temperature curing silicones expected by the end of 2025. This major investment strengthens Europe’s supply base for high-performance façade and structural sealants, responding to regional demand for energy-efficient, durable building materials.

Earlier in May 2025, Henkel AG & Co. KGaA opened its 70,000 sq. ft. Technology Center in New Jersey, a global innovation hub designed for direct collaboration with customers on sealants, adhesives, and functional coatings. The center enhances Henkel’s capability to co-develop low-emission and elastomeric sealant technologies tailored for construction, automotive, and industrial infrastructure. Similarly, in March 2025, Clariant and Omya jointly announced the launch of AddWorks IBC 760, a stabilizer designed to prevent yellowing in Silane-Modified Polymer (SMP) sealants, ensuring long-term aesthetic and mechanical stability—key concerns for architects and façade engineers.

Regional capacity expansion has become a defining theme. In June 2024, Sika AG inaugurated a major new facility in Kharagpur, India, focused on mortar and concrete admixtures alongside construction sealants, strengthening supply in India’s rapidly growing infrastructure market. Likewise, Wacker Chemie AG expanded its Nünchritz plant in Germany to boost alkoxy silicone sealant production, targeting low-odor, neutral-cure products for sustainable indoor environments. In March 2024, Arkema’s Bostik division announced a distribution partnership with DGE, covering Europe, the Middle East, and Africa (EMEA)—broadening access to industrial and construction-grade sealants for flooring, waterproofing, and façade bonding.

Industry-wide, R&D efforts intensified in hybrid sealant formulations throughout 2024, driven by the need for strong adhesion, paintability, and weather resistance. The adoption of SMP and hybrid polymer technologies continues to grow as professionals seek to replace traditional polyurethane systems with solvent-free, high-durability alternatives aligned with global environmental regulations.

One of the most transformative trends in the construction sealants market is the industry-wide shift toward low-VOC, solvent-free, and high-solids formulations driven by the convergence of environmental regulation, occupational safety, and green building design mandates. Regional standards such as California’s SCAQMD Rule 1168, the EU’s REACH and Deco-Paint Directive, and LEED v4.1 Low-Emitting Materials criteria have made low-VOC sealants a non-negotiable requirement for both commercial and institutional projects globally.

In the U.S., SCAQMD Rule 1168 sets a stringent limit of 250 g/L VOC for most sealant types, with a “Super Compliant” benchmark at <25 g/L, effectively phasing out traditional solvent-based systems. The regulatory benchmark has accelerated R&D investments toward high-solids reactive and waterborne chemistries capable of delivering both compliance and high performance. Concurrently, the European Union’s REACH regulation and the Deco-Paint Directive (2004/42/EC) have harmonized even stricter VOC caps, making solvent-free sealants the market standard across the EU—a region leading global adoption.

Multinational chemical companies such as Dow, Sika, and Tremco are publicly aligning their portfolios with LEED, WELL, and CDPH emissions testing standards, ensuring their weatherproofing and structural sealants qualify for green building credits. The strategic shift toward eco-compliant product portfolios is enabling contractors and developers to meet indoor air quality (IAQ) targets without compromising adhesion or elasticity. Further, solvent-free innovations are reducing on-site health hazards, simplifying environmental audits, and offering builders measurable sustainability advantages—a major differentiator in today’s environmentally certified construction market.

A second defining trend transforming the construction sealants industry is the rapid adoption of hybrid polymer sealants such as MS polymers (Modified Silane) and SPUR (Silyl-Terminated Polyurethanes). These next-generation hybrids combine the durability and UV resistance of silicones with the paintability and adhesion strength of polyurethanes, creating a universal class of high-performance sealants optimized for both structural and decorative applications.

Major manufacturers including Sika (Sikaflex®) and Henkel (Loctite®) have significantly expanded their hybrid product portfolios, introducing solvent-free, isocyanate-free formulations that deliver excellent adhesion strength (≥1 MPa) on diverse substrates such as concrete, glass, aluminum, and stone—often without the need for primers. Laboratory and field evaluations show that MS Polymer sealants can achieve elastic recovery rates exceeding 70% and joint movement capacities of ±25%, placing them in the premium performance category suitable for façade systems, curtain wall assemblies, and high-mobility expansion joints.

The growing versatility of hybrid sealants extends beyond conventional construction. They are being deployed in renewable energy applications, such as solar panel installations and wind turbine components, where extreme UV exposure, thermal cycling, and vibration resistance are critical. In addition, advancements in non-staining hybrid formulations have addressed a major limitation of silicone and polyurethane sealants—chemical migration and substrate discoloration. These non-staining hybrid polymer sealants enable secure, long-term sealing on porous architectural materials like marble and limestone, making them ideal for high-end architectural and restoration projects.

The global push toward building energy decarbonization and retrofit modernization is creating a high-growth, long-term market for air barrier and weatherproofing sealants. National policies in North America and Europe are driving large-scale retrofitting programs that rely on high-performance sealing materials to reduce building envelope leakage, improve insulation, and enhance overall thermal efficiency.

In the United States, the Department of Energy’s Weatherization Assistance Program (WAP) and Inflation Reduction Act (IRA) incentives allocate multi-billion-dollar investments to upgrade energy performance in residential and commercial buildings. Air sealing is one of the most cost-effective measures under these programs, often accounting for up to 40% of total energy savings. As a result, the demand for specialized, durable air-sealing and vapor barrier sealants has skyrocketed—particularly those that retain flexibility and adhesion under continuous thermal cycling and moisture exposure.

The European Union’s “Renovation Wave” strategy, targeting a carbon-neutral building stock by 2050, further amplifies demand for airtight, long-life sealants used in energy-efficient retrofits. Millions of existing buildings across Europe will require comprehensive sealing and insulation upgrades, creating a persistent, high-volume opportunity for manufacturers offering EN- and ASTM-compliant sealant systems certified for building envelope applications. In addition, the integration of robotics and automated dispensing technologies in air sealing—funded under the DOE’s Advanced Building Construction (ABC) initiative—is driving innovation toward precision-engineered sealant chemistries suitable for machine-applied, consistent, and automated deployment.

For sealant producers, aligning product innovation with energy retrofit standards (LEED, Passive House, and NZEB) will be pivotal for capturing share in the policy-backed growth segment. Products that demonstrate measurable airtightness improvements, low shrinkage, and verified VOC compliance are becoming the gold standard in retrofit-grade sealing systems.

The global rise of mass timber construction, particularly in Cross-Laminated Timber (CLT) and Glue-Laminated Timber (Glulam) structures, represents one of the most promising opportunities for construction sealant manufacturers. The structural shift toward renewable materials demands specialized fire-rated, elastic, and non-staining sealants capable of managing hygrothermal movement while maintaining airtightness and aesthetic integrity.

Under the U.S. and International Building Codes (IBC) for mass timber construction types IV-A, IV-B, and IV-C, fire-resistance-rated joints explicitly require sealants meeting ASTM C920 standards to prevent hot gas and smoke transfer. The code-level requirement ensures sustained demand for fire-stop and joint sealants specifically engineered for CLT connections, reinforcing their critical role in mass timber safety design.

From a performance perspective, CLT panels experience natural expansion and contraction due to moisture absorption—a phenomenon that can compromise airtightness and visual finish if inappropriate sealants are used. Thus, manufacturers are developing highly flexible, moisture-tolerant sealants that maintain adhesion even after multiple swelling-drying cycles. These sealants often exhibit elongation capabilities above 600%, ensuring resilience in both interior and exterior timber joints.

Aesthetic considerations are equally crucial. As architects increasingly specify exposed timber surfaces for biophilic and minimalist designs, the demand for UV-stable, non-staining sealants is surging. Products that preserve the natural appearance of wood while providing long-term weather resistance and color stability are commanding premium pricing in the CLT market. Consequently, sealants compatible with timber surfaces are evolving into a distinct, high-value product category that merges fire safety, structural performance, and design aesthetics—positioning manufacturers to capture growth in the sustainable mass timber construction ecosystem.

Construction Sealants Market Share Insights, 2025-2034

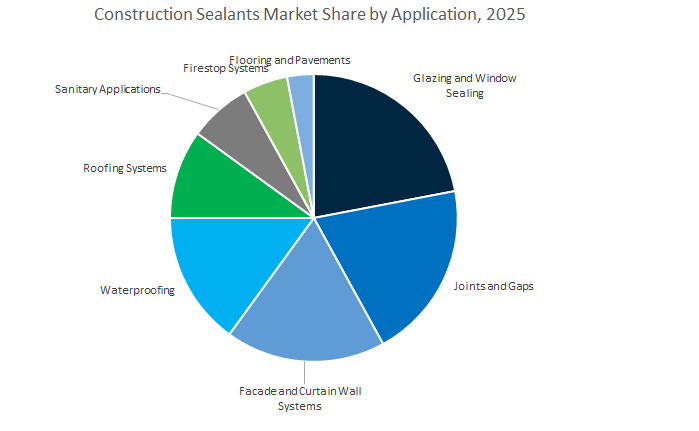

Glazing and Joint Sealing Lead the Global Construction Sealants Market with Over 40% Share

The Glazing and Window Sealing segment dominates the global construction sealants market with a projected 22.9% share in 2025, closely followed by Joints and Gaps at 19.4%. Glazing sealants are indispensable for bonding and weatherproofing glass elements in both residential and commercial buildings, particularly in modern curtain wall and structural glazing systems, which require long-lasting adhesion, UV resistance, and elasticity. High-performance silicone and polyurethane sealants are the backbone of this segment due to their durability and resistance to temperature and moisture extremes.

Joint and gap sealing applications are equally critical, ensuring air and water tightness in expansion joints, precast concrete interfaces, and façade panels. The rising adoption of energy-efficient building envelopes and airtight construction in compliance with green certification programs (LEED, BREEAM) is driving additional growth. These segments are also benefiting from urban infrastructure development and high-rise construction across Asia-Pacific, North America, and the Middle East, where silicone, hybrid polymer, and MS-based sealants are preferred for their high movement capability and weatherability. The demand here reflects the market’s shift from purely functional products to multi-performance sealants that combine structural, acoustic, and thermal benefits.

Facade, Waterproofing, and Roofing Systems Drive High-Performance Sealant Demand

The Facade and Curtain Wall Systems and Waterproofing segments represent a high-value portion of the construction sealants market, emphasizing technical performance over volume. Structural and weather-sealing applications in modern facades demand ultra-durable silicone sealants that can maintain adhesion for 20–30 years under severe environmental stress. This segment benefits from the surge in glass-intensive architecture, especially in commercial skyscrapers and institutional buildings. Waterproofing applications, including below-grade structures, basements, and wet areas, require flexible, hydrolysis-resistant sealants capable of withstanding hydrostatic pressure and cyclic movement. Polyurethane, polysulfide, and hybrid polymer sealants dominate here due to their superior adhesion to concrete, metals, and membranes.

Roofing Systems also represent a strong growth area for UV- and weather-resistant sealants, primarily silicone and butyl-based types used in flashings, joints, and penetrations. Their ability to create seamless, watertight barriers in roof assemblies is critical for extending roof service life and reducing maintenance costs. With the growing adoption of cool roof and green roof technologies, demand for sealants that resist temperature cycling, ponding water, and reflective coatings is rising sharply.

Residential Construction Holds the Largest Share with 33.6% of the Global Market

The Residential Construction sector represents the largest end-use segment, accounting for 33.6% of the global construction sealants market in 2025. This dominance is driven by robust housing demand, rapid urbanization, and renovation trends worldwide. Sealants are integral to nearly every stage of homebuilding—from window and door installation to kitchen and bathroom sealing, perimeter caulking, and waterproofing. The growing emphasis on energy efficiency, air sealing, and green housing codes continues to elevate the use of high-performance silicone and hybrid sealants that enhance insulation and durability. In addition, the DIY and home improvement market is a strong contributor, particularly in developed economies, where homeowners use acrylic and water-based sealants for maintenance and aesthetic repairs. The combination of rising disposable income, consumer awareness, and stricter building standards ensures steady, recurring demand from this sector.

Commercial Construction Drives High-Performance and Architectural Sealant Demand

The Commercial Construction segment, including office buildings, retail complexes, hospitals, and educational facilities, is a key driver of high-value sealant consumption. This sector relies heavily on advanced silicone, polyurethane, and hybrid polymer formulations for façade sealing, structural glazing, and curtain wall systems that must perform under continuous environmental stress. Commercial structures are often designed with glass-dominant exteriors, creating significant demand for UV-stable, long-life sealants capable of withstanding structural load transfer, thermal expansion, and air leakage control. Additionally, indoor air quality and LEED certification requirements favor low-VOC, solvent-free sealants. With global investments in smart buildings and commercial infrastructure rebounding post-pandemic, this segment is expected to sustain strong growth, led by the Asia-Pacific and Middle East regions, where mega-projects and high-rise developments are proliferating.

The construction sealants market is defined by innovation-driven global players that emphasize silicone chemistry leadership, hybrid technology evolution, and safety-compliant performance. Companies like Sika AG, Dow, Henkel, Wacker Chemie, and Arkema (Bostik) dominate the competitive landscape through robust R&D investments, capacity expansion, and customer-centric product development.

Sika AG remains the global pioneer in structural glazing adhesives and construction sealant technologies. Its Sikasil® SG range allows up to 55% smaller joint dimensions without compromising strength—an engineering advantage in high-rise glazing projects. The company’s SikaSeal® range meets stringent low-emission and indoor air quality standards, while its Sika Joint Calculator helps architects design optimal joints that can reduce CO₂ emissions by over 100 tons in major façade projects. With localized production in India (2024 expansion) and R&D focus on low-monomer PU technologies, Sika is setting new benchmarks for sustainability and performance in façade and infrastructure sealant applications.

Dow Inc. dominates the silicone sealant segment, providing high-performance formulations under its DOWSIL™ brand for glazing, cladding, and fire-stopping applications. Its September 2025 launch of DOWSIL™ Fire Protection Sealant highlights the firm’s commitment to safety compliance amid increasing demand for fire-rated structural joints. Dow’s sealants are valued for UV resistance, thermal stability, and substrate versatility, offering durable adhesion to glass, concrete, and metal façades. The company continues to expand its R&D focus on silicone hybrid technologies for enhanced performance in extreme environmental conditions.

Henkel combines broad elastomeric sealant expertise with a sustainability-driven product pipeline under its LOCTITE® and TEROSON® brands. Its Bridgewater Technology Center (May 2025) enables joint R&D efforts with construction and infrastructure partners. Henkel’s low-VOC formulations align with green building and occupational health standards, making them preferred solutions for both industrial and residential construction. Its pre-applied adhesive solutions also streamline on-site installation, improving productivity and consistency in sealing applications.

Wacker Chemie AG is a cornerstone of the European construction sealant market, specializing in neutral-cure alkoxy silicones that offer low odor, strong adhesion, and interior air quality compliance. With major investments in Czech Republic and Germany, Wacker aims to expand cartridge filling capacity by 30 million units annually by 2025. Its ELASTOSIL® eco product line, based on biomethanol feedstocks, reinforces its sustainability credentials by lowering carbon intensity across the sealant value chain. These initiatives underscore Wacker’s commitment to renewable chemistry and large-scale supply reliability.

Through its Bostik subsidiary, Arkema is a frontrunner in Silane-Modified Polymer (SMP) and hybrid sealant technologies. These solvent-free formulations combine excellent adhesion and paintability with enhanced weather and UV resistance, catering to roofing, flooring, and façade sealing needs. In March 2024, Bostik signed a distribution partnership with DGE to expand across EMEA, reinforcing its supply chain for industrial and construction adhesives. Its portfolio emphasizes contractor safety, low hazard labeling, and eco-friendly chemistries, positioning it as a preferred choice in next-generation sustainable sealing systems.

China dominates the global construction sealants industry as the largest consumer and manufacturing base, fueled by an unprecedented scale of infrastructure and high-rise construction. The government’s focus on green building initiatives and energy-efficient architecture continues to accelerate demand for high-performance silicone, polyurethane, and hybrid polymer sealants across commercial, residential, and industrial applications.

In late 2024, a major global chemicals company inaugurated a state-of-the-art R&D and production facility in Xi’an, Northwest China, to develop advanced waterproofing sealants and tile adhesives, strategically addressing inland market growth. Similarly, in 2025, a leading specialty chemicals manufacturer expanded its Suzhou plant capacity to meet surging demand for premium silicone sealants used in façade glazing and flooring systems.

China’s Five-Year Plan mandates stricter indoor air quality standards, driving a nationwide transition from solvent-based sealants to low-VOC, water-based, and MS polymer chemistries. Massive infrastructure projects—such as high-speed rail networks, transportation hubs, and coastal megaprojects—are further increasing adoption of long-life polyurethane and hybrid expansion joint sealants capable of withstanding vibration and temperature extremes.

Meanwhile, domestic innovation in cost-effective PVA and acrylic emulsion formulations caters to the mid-market residential sector, balancing affordability with performance. With the government promoting prefabricated and modular construction, demand for rapid-curing hybrid adhesives is expected to rise exponentially, reinforcing China’s leadership in construction sealant manufacturing and application technology.

The U.S. construction sealants market is entering a period of accelerated transformation, driven by energy efficiency mandates, infrastructure funding, and ESG-focused construction practices. The country’s non-residential sector—particularly in data centers, healthcare facilities, and commercial towers—is witnessing robust adoption of high-durability waterproofing and fire-resistant sealants.

In early 2025, a major global adhesives manufacturer expanded its U.S. footprint through a strategic acquisition of a building materials company specializing in EIFS (Exterior Insulation and Finish Systems) and joint-sealing technologies—both of which represent major sealant-intensive applications. Simultaneously, compliance with state-level energy standards like California’s Title 24 is propelling the use of carbon-neutral silicone glazing sealants designed to minimize heat loss and enhance façade performance.

Manufacturers are leveraging digital product carbon footprint (PCF) assessment platforms to align with green procurement policies. The technology-driven transparency enables architects and developers to select low-emission sealants that meet LEED and WELL certifications. In parallel, data center construction booms are fueling demand for high-performance firestop sealant systems, crucial for meeting stringent operational safety standards.

R&D investments are increasingly directed at AI-enhanced formulation design, improving material curing predictability and adhesion performance across diverse substrates. Overall, the U.S. remains a global pioneer in sustainable sealant innovation, balancing durability, compliance, and energy efficiency.

Germany continues to lead the European construction sealants industry, driven by EU Green Deal directives, REACH chemical compliance, and stringent building efficiency mandates. National initiatives focused on energy renovation of buildings and low-emission public infrastructure are accelerating demand for acrylic, polyurethane, and hybrid polymer sealants that combine environmental compliance with mechanical durability.

In early 2025, a collaboration between a leading German manufacturer and a Swiss counterpart resulted in the introduction of sustainable epoxy hardeners, optimizing performance in construction-grade sealants. The country’s push for circular economy goals is fostering innovation in de-bondable and recyclable adhesives, aligning with the EU’s 2030 resource-efficiency objectives.

German manufacturers are pioneering silylated polymer (SPUR) and MS polymer sealant chemistries, known for being isocyanate-free, paintable, and high-performance. The solutions are increasingly specified in façade systems and prefabricated panels for their balance of elasticity, adhesion, and sustainability. Additionally, advancements in dual-component power dispensing tools are revolutionizing the application process by improving precision and reducing installation time for two-component polyurethane and silicone systems.

India’s construction sealants industry is expanding rapidly, powered by urbanization, infrastructure modernization, and the government’s housing and industrial growth policies. Programs like Pradhan Mantri Awas Yojana (PMAY) and Smart Cities Mission have created immense demand for weatherproof silicone and polyurethane sealants used in affordable and mid-range housing.

The monsoon climate presents unique performance challenges, pushing manufacturers to develop UV-stable and high-moisture-resistant formulations for façades, glazing, and roofing applications. Domestic leaders such as Pidilite Industries and international players are increasing production capacity through new local facilities, reducing dependency on imports and ensuring a consistent supply of acrylic and hybrid sealants for high-volume residential construction.

The commercial building boom—driven by modern curtain-wall designs and glass façades—is stimulating demand for structural glazing sealants compliant with ASTM and ISO standards. Simultaneously, corporate acquisitions in 2024 have diversified product portfolios across high-performance bonding and waterproofing solutions.

With rising emphasis on BIS product certification and low-VOC compliance, India is emerging as a major global hub for sustainable and cost-effective construction sealant production catering to both domestic and export markets.

The UK construction sealants market is being redefined by net-zero building targets, post-Brexit sustainability policies, and tightened fire safety regulations. The retrofit and renovation wave sweeping across the country is fueling demand for high-elasticity air-tight window and door sealing products that enhance both energy and acoustic insulation.

In early 2025, a major construction chemical manufacturer strengthened its UK presence through the acquisition of a roofing systems specialist, expanding its portfolio to include advanced roofing sealants and hybrid bonding technologies. Sustainability remains central to procurement strategies, with low-VOC hybrid polymer formulations gaining preference for their compliance with carbon reduction goals and local supply assurance.

The Grenfell Tower tragedy continues to shape regulatory focus, mandating the integration of flame-retardant and certified firestop sealants in high-rise and public buildings. Moreover, energy performance mandates are driving widespread use of sealants that contribute to airtight building envelopes and reduced operational carbon.

The UK market stands as a leading European example of safety-driven, regulation-compliant innovation, ensuring alignment between energy efficiency, sustainability, and performance durability in construction sealant applications.

Qatar’s construction sealants industry is witnessing robust growth, underpinned by post-World Cup infrastructure investment, commercial real estate expansion, and climate-adaptive building design. The country’s extreme desert temperatures and humidity fluctuations create high-performance requirements for UV-stable, flexible, and high-temperature-resistant sealants.

In mid-2025, a global chemical leader completed the acquisition of a renowned Qatari construction materials manufacturer, strengthening local expertise across concrete admixtures, waterproofing membranes, and façade systems. The strategic expansion directly supports the rising demand for high-performance polyurethane and silicone sealants in Qatar’s luxury residential, hospitality, and public infrastructure sectors.

Ongoing energy-efficiency initiatives—including “cool house” programs and sustainable building design—are catalyzing the market for airtight, low-VOC hybrid polymer sealants that maintain performance under harsh environmental conditions.

As Qatar’s construction landscape evolves toward resilient and thermally efficient design, manufacturers and suppliers are prioritizing region-specific formulations capable of withstanding extreme heat, UV radiation, and sand abrasion—making the nation a regional leader in advanced construction sealant technologies.

Construction Sealants Market Report Scope

Construction Sealants Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$7.9 Billion

|

|

Market Size (2034)

|

$11.6 Billion

|

|

Market Growth Rate

|

4.4%

|

|

Segments

|

By Resin Type (Silicone-based, Polyurethane-based, Hybrid Polymers, Acrylic, Polysulfide, Butyle-based), By Application (Glazing and Window Sealing, Joints and Gaps, Facade and Curtain Wall Systems, Waterproofing, Flooring and Pavements, Roofing Systems, Firestop Systems, Sanitary Applications), By End-User (Commercial Construction, Residential Construction, Infrastructure, Industrial, Repair & Renovation/Aftermarket), By Modulus Type (Low-Modulus, Medium-Modulus, High-Modulus), By Formulation (One-Component Sealants, Two-Component Sealants

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Sika AG, Henkel AG & Co. KGaA, Dow Inc., Arkema Group, H.B. Fuller Company, 3M Company, Wacker Chemie AG, RPM International Inc., Huntsman Corporation, Soudal Group, MAPEI S.p.A., Illinois Tool Works Inc., Pidilite Industries Ltd., DuPont, BASF SE

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

By Resin/Chemical Type

- Silicone-based

- Polyurethane-based

- Hybrid Polymers

- Acrylic

- Polysulfide

- Butyle-based

By Application

- Glazing and Window Sealing

- Joints and Gaps

- Facade and Curtain Wall Systems

- Waterproofing

- Flooring and Pavements

- Roofing Systems

- Firestop Systems

- Sanitary Applications

By End-Use Sector

- Commercial Construction

- Residential Construction

- Infrastructure

- Industrial

- Repair & Renovation/Aftermarket

By Modulus Type

- Low-Modulus

- Medium-Modulus

- High-Modulus

By Formulation/Curing Type

- One-Component Sealants

- Two-Component Sealants

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

- Sika AG

- Henkel AG & Co. KGaA

- Dow Inc.

- Arkema Group

- H.B. Fuller Company

- 3M Company

- Wacker Chemie AG

- RPM International Inc.

- Huntsman Corporation

- Soudal Group

- MAPEI S.p.A.

- Illinois Tool Works Inc.

- Pidilite Industries Ltd.

- DuPont

- BASF SE

*- List not Exhaustive

Research Coverage

Prepared by USDAnalytics, this report investigates the Construction Sealants Market through the lens of performance, compliance, and application productivity—delivering analysis reviews on demand drivers, pricing/mix shifts, and code-aligned specifications; it highlights material advances across silicone, polyurethane, and hybrid SMP platforms that raise joint durability, façade integrity, and lifecycle value; and tracks breakthroughs in fire-safe, low-VOC, and high-movement systems that underpin modern envelopes, glazing, and waterproofing. By connecting curing profiles, modulus behavior, weather/UV stability, and IAQ credentials to real-world installation outcomes and total cost of ownership, this report is an essential resource for architects, façade engineers, contractors, OEM fabricators, and procurement leaders prioritizing safe, energy-efficient, and regulation-ready sealing solutions at scale.

Scope Highlights

Segmentation:

- By Resin/Chemical Type: Silicone-based; Polyurethane-based; Hybrid Polymers; Acrylic; Polysulfide; Butyl-based.

- By Application: Glazing & Window Sealing; Joints & Gaps; Facade & Curtain Wall Systems; Waterproofing; Flooring & Pavements; Roofing Systems; Firestop Systems; Sanitary Applications.

- By End-Use Sector: Commercial Construction; Residential Construction; Infrastructure; Industrial; Repair & Renovation/Aftermarket.

- By Modulus Type: Low-Modulus; Medium-Modulus; High-Modulus.

- By Formulation/Curing Type: One-Component Sealants; Two-Component Sealants.

- Geographic Scope: Analysis spans 25+ countries across North America, Europe, Asia Pacific, Latin America, the Middle East & Africa.

- Time Frame: Historic data (2021–2024) and forecast data (2025–2034).

- Companies: Analysis/profiles of 15+ companies covering strategy, innovation pipelines, capacity moves, and product benchmarking.

Deliverables

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.