Market Overview: Polyurethane Sealants Transition from Commodity Fillers to Performance-Critical Systems

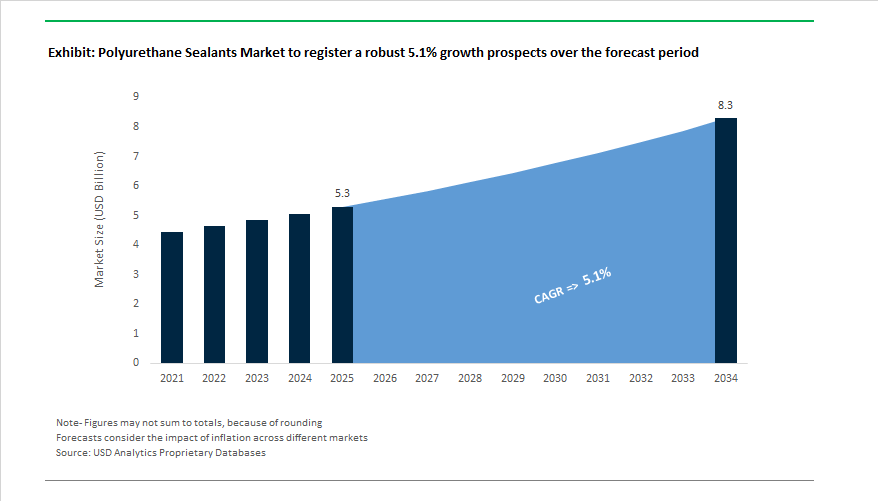

The Global Polyurethane Sealants Market is projected to expand from USD 5.3 billion in 2025 to USD 8.3 billion by 2034, at a CAGR of 5.1%, as polyurethane sealants evolve from basic gap-filling materials into performance-critical systems across construction, transportation, industrial assembly, and renewable energy infrastructure. Demand growth is increasingly shaped by movement capability, long-term durability, and regulatory compliance under real service conditions. In building envelopes, façades, flooring, and glazing, polyurethane sealants are specified because they combine high elastic recovery, strong adhesion to porous and non-porous substrates, and sustained resistance to moisture ingress, outperforming acrylics and many silicones in mechanically stressed joints.

From a formulation and application standpoint, one-component moisture-curing polyurethane sealants dominate global installations, driven by ease of application, predictable curing behavior, and reduced on-site complexity. Manufacturer portfolios such as Sika’s Sikaflex® construction sealants, Henkel’s TEROSON® PU range, and 3M™ polyurethane sealants are engineered to meet ASTM C920 Class 25 and Class 50 movement ratings, enabling reliable performance in expansion joints, curtain walls, and flooring transitions subject to continuous thermal and structural movement. This movement capability—often ±25% to ±50%—is increasingly treated as a baseline requirement rather than a premium feature, particularly in high-rise construction and large commercial assets where joint failure translates directly into water damage and lifecycle cost escalation.

Low-VOC and water-reduced polyurethane sealants are gaining preference in Europe and North America as green building certifications and indoor air quality standards tighten. Major manufacturers have reformulated legacy systems to comply with LEED, A+ indoor air quality labels, and EU construction product regulations, while maintaining adhesion to concrete, metals, coated substrates, and plastics. In transportation and automotive assembly, polyurethane sealants are increasingly used as structural-elastic interfaces rather than auxiliary materials—supporting body-in-white stiffness, corrosion protection, and Noise, Vibration, and Harshness (NVH) control. OEMs increasingly specify PU sealants in lieu of mechanical fasteners in secondary joints to reduce weight and simplify assembly, a trend reinforced by electric vehicle architectures where acoustic comfort and vibration damping are more visible to end users.

The renewable energy segment is emerging as a structurally important demand pillar. Wind turbine manufacturers and offshore infrastructure operators rely on polyurethane sealants for blade joint sealing, tower section interfaces, nacelle assemblies, and cable penetrations, where fatigue resistance under cyclic load and environmental exposure determines asset uptime. Sealant systems used in these applications are qualified for prolonged UV exposure, salt spray, and temperature cycling—requirements that favor polyurethane chemistries over less elastic alternatives.

The polyurethane sealants industry is undergoing dynamic transformation, led by sustainability-driven innovation, capacity expansion in emerging markets, and a rapid pivot toward bio-based and ultra-low monomer formulations.

In October 2025, DuPont expanded its polyurethane foam sealant product line with Great Stuff™ Wide Spray Foam Sealant, designed for large-area sealing and professional construction use. The new formulation emphasizes application speed and energy efficiency, reflecting DuPont’s continued leadership in high-volume, precision-engineered sealing products for the commercial and residential building markets.

Meanwhile, Sika AG took a landmark step in May 2025 with the launch of Sikaflex® Purform®, an ultra-low monomer polyurethane sealant that eliminates the need for specific REACH safety training by maintaining <0.1% monomeric diisocyanate. This product aligns with European occupational safety regulations while ensuring high performance in façade, flooring, and modular construction applications.

Henkel AG & Co. KGaA continued its manufacturing expansion with a major investment in June 2024 at its Kurkumbh, India site, enhancing regional production capacity for advanced PU adhesives and sealants. This facility underscores Henkel’s focus on Asia-Pacific’s booming construction markets, enabling faster delivery and localized R&D support.

In July 2025, H.B. Fuller acquired a specialty adhesives and sealants producer, strengthening its position in transportation and high-performance construction sealing applications. The acquisition reflects a broader strategy of portfolio diversification and market expansion in Asia and Europe.

BASF SE, in March 2025, expanded production of Polyurethane Dispersions (PUDs) at its Spanish facility, supporting the growing need for low-VOC sealant formulations aligned with global sustainability goals. The company also partnered with STOCKMEIER Urethanes USA, Inc. (August 2024) to co-develop eco-friendly surfacing systems, a move signaling BASF’s dedication to sustainable innovation across industrial and recreational infrastructure.

In April 2025, Dow Inc. advanced the circular economy agenda by piloting a recyclable polyurethane adhesive system designed to enhance film layer separation in flexible packaging. This innovation supports recyclability standards in Europe and aligns with multi-layer packaging waste reduction policies.

The 3M Company, in February 2025, rolled out a dual-cure polyurethane-hybrid adhesive system that integrates both moisture and UV curing, a major leap for industrial automation and precision electronic assembly. Similarly, Arkema (via Bostik) completed the acquisition of Dow’s flexible packaging adhesives business (September 2024), expanding its range of solvent-free polyurethane systems tailored for flexible packaging.

Market Trend 1: Shift Toward High-Modulus, Fast-Cure Polyurethane Sealants for Infrastructure and Transportation Joints

The increasing global demand for fast-curing polyurethane sealants in infrastructure projects such as highways, airports, and bridges is transforming industry performance benchmarks. Governments and contractors are prioritizing products that allow rapid return-to-service to minimize downtime and disruption in critical transport infrastructure.

Recent case studies by Sika Group demonstrate the power of the shift. Its Sikaflex®-406 KC system enables full reopening of concrete highways and pavement joints to traffic within 2 to 3 hours of application—a significant leap from traditional polyurethane sealants that require overnight curing. The innovation allows infrastructure projects to meet both tight construction timelines and cost-efficiency targets.

From a technical standpoint, high-modulus polyurethane sealants feature a Shore A hardness of 50 ± 5 and a tensile stretch modulus of ≥1.0 MPa, ensuring that they can absorb moderate movement while withstanding dynamic loads. These performance attributes make them ideal for sealing joints between floors, machinery foundations, and heavy-duty stair structures. As cities expand and demand rapid infrastructure rehabilitation, these high-modulus, accelerated-cure polyurethane systems are becoming indispensable across civil and industrial engineering applications.

Market Trend 2: Emergence of Non-Isocyanate and Low-VOC Polyurethane Sealants for Sustainable Construction

The industry’s pivot toward non-isocyanate and low-VOC polyurethane sealants reflects a decisive movement toward sustainability, worker safety, and compliance with global Indoor Air Quality (IAQ) regulations. Both the EU Industrial Emissions Directive and the U.S. EPA’s VOC guidelines are enforcing stricter emissions standards, compelling manufacturers to develop products with VOC levels below 28 g/L—a prerequisite for LEED and BREEAM green building certifications.

Chemical innovation is at the core of the transformation. Researchers have successfully synthesized non-isocyanate polyhydroxyurethanes (PHUs) using cyclic carbonates and polyamines—a process that utilizes CO₂ as a renewable feedstock and achieves 100% atom economy. The “green chemistry” pathway eliminates toxic isocyanate precursors while maintaining the mechanical and adhesive performance required for interior applications.

Major industry participants, including Dow and BASF, are expanding portfolios of low-VOC, solvent-free polyurethane sealants optimized for interior construction, flooring, and façade sealing. These formulations align with the growing global preference for eco-friendly construction materials, while offering enhanced UV resistance, minimal odor, and improved elastic recovery—features that are standard for high-end commercial and residential buildings.

Market Opportunity 1: Expanding Applications in Electric Vehicle (EV) Battery Enclosure Sealing and Thermal Management

The rise of electric vehicle production is creating a new frontier for polyurethane sealants, particularly in battery enclosure sealing, thermal management, and fire protection. EV batteries require precise bonding and sealing to prevent contamination, manage heat, and ensure mechanical integrity throughout their operational life.

One- and two-part polyurethane battery sealants are being engineered for automated application systems in gigafactory environments. These sealants enable fully robotic dispensing and mixing, providing IP67 and IP69-rated waterproofing—critical for preventing ingress of moisture, dust, and contaminants into battery housings. Leading suppliers such as 3M and Dow Automotive have commercialized formulations that exhibit high elongation, excellent dielectric strength, and adhesion to dissimilar substrates such as aluminum, steel, and engineered plastics.

In addition to sealing, polyurethane-based foams and potting materials are integral to battery pack insulation and safety. Modern all-water polyurethane foams demonstrate thermal conductivities of 0.020–0.035 W/m·K and comply with UL94 V-0 flame retardancy, providing both heat dissipation and fire containment. These materials maintain EV battery operating temperatures within the safe range of 25°C to 40°C, preventing thermal runaway and extending service life. As automakers continue to prioritize safety and lightweight design, EV battery sealants represent one of the fastest-growing niches in the global polyurethane market.

Market Opportunity 2: Marine-Grade Polyurethane Sealants Supporting Offshore Wind Farm Construction

The offshore wind energy boom has become a significant driver of the polyurethane sealants and coatings market, where performance, longevity, and resistance to harsh marine environments are non-negotiable. Offshore wind structures—including turbine towers, foundations, and transition pieces—face constant exposure to saltwater, high winds, and UV radiation, demanding coatings that can sustain structural integrity for over two decades.

A standard corrosion protection system for offshore wind towers, as defined by ISO 12944-5, employs a polyurethane topcoat over an epoxy primer to achieve maximum UV and abrasion resistance in C5-M marine exposure zones. The PPG Protective & Marine Coatings case study at the Utgrunden Offshore Wind Farm in the Baltic Sea demonstrated that a specialized polyurethane topcoat remained effective after 20 years in service, confirming its unparalleled resistance to environmental degradation.

In addition, polyurethane’s versatility—offering Shore hardness options from A10 (soft elastomeric sealants) to D90 (rigid coatings)—allows engineers to tailor the product for joint flexibility, vibration damping, or long-term corrosion protection. As global renewable energy capacity expands beyond 1,000 GW, polyurethane sealants are set to play an essential role in ensuring offshore asset reliability and reduced lifecycle maintenance costs.

Competitive Landscape: Key Companies and Strategic Profiles

The global polyurethane sealants market is moderately consolidated, led by innovation-focused multinationals investing heavily in sustainability, regional expansion, and hybrid chemistry technologies. Each company’s competitive strategy reflects its response to regulatory shifts and evolving end-use requirements in construction, automotive, and industrial assembly.

Sika AG continues to lead the market in construction-grade polyurethane sealants through its renowned Sikaflex® product family. The introduction of Purform® technology demonstrates Sika’s commitment to safety and sustainability, reducing monomeric diisocyanate content below 0.1%. The company’s PU sealants are vital for infrastructure projects, including bridges, tunnels, and airports, where movement tolerance and long-term adhesion are critical. Additionally, Sika is expanding its product portfolio to address modular construction and off-site panel bonding, offering sealants with enhanced elasticity and faster curing characteristics.

Henkel leverages its LOCTITE and TECHNOMELT brands to provide advanced polyurethane-based sealants and adhesives across industrial and consumer segments. Its 2023 introduction of bio-based PU adhesives using renewable polyols reflects a major step toward carbon-neutral product lines. Henkel also integrates advanced automation systems for automotive and electronics applications, combining its engineering services with product expertise to enhance process efficiency. The 2024 expansion of its Indian manufacturing facility further strengthens its Asia-Pacific supply chain and sustainability footprint.

Dow remains at the forefront of polymer innovation, supplying tailored polyurethane systems and precursors for sealant production. Its BETASEAL™ PU system dominates the automotive glazing and bonding market, ensuring safety, vibration control, and thermal stability in both internal combustion and electric vehicles. In April 2025, Dow began pilot testing recyclable polyurethane adhesives for flexible packaging, aligning with global circular economy objectives. Additionally, its VORASIL™ silane-modified polymer hybrids bridge the gap between PU and SMP technologies, delivering primerless adhesion and superior UV resistance.

Bostik, a division of Arkema, benefits from its parent company’s deep materials expertise to develop high-performance polyurethane sealants for construction, mobility, and DIY markets. The company’s Kizen LIME and smart adhesive ranges target sustainable and recyclable applications, while its EV battery assembly adhesives address the next generation of e-mobility solutions. Through continuous R&D investment (2.7% of sales) and dedicated innovation centers in France, China, and the U.S., Bostik is advancing the design of hybrid polyurethane chemistries for high-stress bonding environments.

BASF SE dominates the polyurethane raw materials landscape with an expansive network for MDI and bio-based polyols. Its March 2025 capacity expansion in Spain bolsters the production of Polyurethane Dispersions (PUDs)—key components of low-VOC sealants and coatings. Collaborations such as the STOCKMEIER Urethanes partnership (August 2024) demonstrate BASF’s move toward sustainable surfacing and sports flooring systems. As global regulations tighten on VOC emissions, BASF’s vertically integrated supply chain and focus on bio-feedstocks position it as a long-term leader in sustainable polyurethane chemistry.

H.B. Fuller is a global leader in industrial assembly and construction sealants, offering one- and two-component polyurethane solutions tailored for roofing, fenestration, and automotive bonding. The company’s acquisition strategy, including HS Butyl and other specialty producers, enhances its market coverage in high-performance sealing systems. Fuller’s R&D centers are pioneering automated, reactive PU adhesives compatible with robotic assembly lines, enabling high throughput and minimal downtime. Its products emphasize durability, extreme weather resistance, and compliance with global green building standards.

Country Analysis: Regional Developments and Technological Advancements in the Global Polyurethane Sealants Industry

Germany: Advancing Sustainable and REACH-Compliant Polyurethane Sealants for Automotive and Industrial Sectors

Germany continues to lead the European polyurethane sealants market, driven by advanced chemistry, REACH-compliant innovation, and the rapid transformation of its automotive and industrial ecosystems. The country’s sealant manufacturers are spearheading the shift toward bio-based and low-emission polyurethane formulations, reflecting the EU’s sustainability and circular economy goals. In March 2024, Lanxess introduced its Adiprene Green product line, utilizing renewable raw materials to replace fossil-based inputs, marking a pivotal step in sustainable polyurethane prepolymer development. Concurrently, Henkel AG & Co. KGaA, headquartered in Düsseldorf, has expanded its Adhesive Technologies division, investing heavily in low-VOC and bio-derived polyurethane adhesives and sealants tailored for EV battery housing, lightweight automotive structures, and general industrial applications.

Germany’s robust REACH regulatory framework continues to accelerate the transition to ultra-low-monomer diisocyanate polyurethane sealants, ensuring worker safety and regulatory compliance, particularly in the construction and DIY markets. The surge in domestic EV manufacturing—supported by major OEM investments—has also led to growing consumption of fast-curing, thermally stable polyurethane sealants for battery modules, chassis bonding, and underbody protection. Moreover, the nation’s emphasis on factory automation and precision engineering sustains strong demand for high-performance two-component polyurethane sealants in machinery and robotics. Combining chemistry innovation with stringent sustainability mandates, Germany remains at the forefront of European polyurethane sealant technology and production leadership.

China: Expanding Production Capacity and Infrastructure Demand for Construction-Grade Polyurethane Sealants

China remains the largest global producer and consumer of polyurethane sealants, underpinned by massive infrastructure investments, construction growth, and industrial diversification. In June 2024, Sika inaugurated a state-of-the-art production facility in Northeast China, aimed at meeting the country’s soaring demand for specialty construction chemicals, including high-durability polyurethane sealant systems for commercial and residential construction. Government-led programs—such as the expansion of high-speed rail networks, urban infrastructure, and public utilities—are driving strong demand for expansion joint polyurethane sealants capable of withstanding vibration, temperature extremes, and heavy mechanical loads.

China’s industrial manufacturing base continues to fuel growth in oil- and chemical-resistant polyurethane sealants for machinery and equipment sealing, while rapid urbanization and affordable housing programs stimulate high-volume usage of single-component construction-grade sealants. Major domestic chemical companies like Yantai Wanhua Polyurethanes Co., Ltd. are scaling MDI and polyol production capacity, strengthening the upstream supply chain for polyurethane manufacturing across Asia-Pacific. With its blend of infrastructure-driven consumption, localized raw material production, and foreign investment in manufacturing, China is consolidating its role as the dominant global hub for polyurethane sealants in both construction and industrial sectors.

United States: Advancing Green Building and Structural Bonding through Next-Generation Polyurethane Sealants

The United States polyurethane sealants market is advancing rapidly, driven by green construction codes, automotive lightweighting trends, and federal infrastructure spending. The country’s strong focus on energy-efficient and low-VOC construction materials is reshaping product innovation across the adhesives and sealants sector. With the Infrastructure Investment and Jobs Act (IIJA) allocating billions toward public works, demand for high-flexibility concrete joint and bridge sealants has surged, particularly for roadway expansion joints, tunnels, and water-resistant applications.

In industrial innovation, 3M Company continues to pioneer dual-cure polyurethane adhesive and sealant systems, combining moisture and UV curing for high-precision automotive and electronic assembly applications. Similarly, Dow Inc. is developing temperature- and chemical-resistant polyurethane systems designed for industrial machinery and aerospace components, supporting extreme operational environments. The modular and prefabricated housing sector—a key growth area—heavily utilizes reactive polyurethane adhesives for weatherproof panel bonding, aligning with green building trends. Additionally, tightening VOC regulations in states such as California are pushing manufacturers toward 100% solids and solvent-free polyurethane formulations. The combined forces have positioned the United States as a leader in sustainable, high-performance polyurethane sealants for construction, EVs, and aerospace applications.

Switzerland: Setting Global Benchmarks with PURFORM® Sustainable Polyurethane Technology

Switzerland remains a global hub for premium polyurethane sealant innovation, led by Sika AG, one of the most influential companies in the global construction chemicals industry. In 2024, Sika launched its revolutionary PURFORM® technology, a next-generation polyurethane formulation with ultra-low monomeric diisocyanate content (<0.1%), providing a regulatory-compliant, sustainable alternative ahead of the EU’s new isocyanate handling standards. The technology underpins flagship products such as Sikaflex Pro-3 and Sikaflex 11FC, which are rapidly becoming industry benchmarks for construction-grade polyurethane sealants.

Switzerland also serves as a central R&D hub for developing specialty construction chemicals, with stringent national building codes driving innovation in acoustic and thermal sealant technologies. The country’s advanced laboratory infrastructure supports global testing and formulation of eco-friendly, high-durability polyurethane systems for the industrial, marine, and architectural markets. With sustainability and precision engineering as its foundation, Switzerland continues to lead global efforts in high-performance, regulatory-compliant polyurethane sealant technology, reinforcing its reputation as a pioneer in sustainable chemistry and construction innovation.

Japan: Advancing High-Precision Polyurethane Sealants for Automotive, Marine, and Infrastructure Applications

Japan’s polyurethane sealants market is characterized by its focus on automotive precision engineering, shipbuilding durability, and high-tech manufacturing applications. The nation’s expanding Electric Vehicle (EV) sector has intensified the demand for high-performance polyurethane sealants used in battery pack sealing, vibration damping (NVH), and structural bonding, ensuring vehicle integrity under extreme conditions. In the marine sector, Japan’s prominent shipbuilding industry continues to utilize weather-resistant polyurethane sealants for deck joints, hull protection, and underwater fittings, offering exceptional adhesion and flexibility in harsh environments.

Companies such as Konishi Co. Ltd. are leading the development of specialized industrial-grade polyurethane formulations, catering to high-precision electronics and equipment manufacturing. Furthermore, Japan’s anti-seismic construction standards have created sustained demand for flexible, elastomeric polyurethane sealants used in expansion joints and earthquake-resistant infrastructure projects. Through a combination of technological precision, R&D investment, and commitment to sustainability, Japan continues to shape the Asia-Pacific polyurethane sealant industry, maintaining a reputation for reliability, performance, and innovation in advanced material applications.

India: Infrastructure Expansion and Domestic Manufacturing Driving Polyurethane Sealant Consumption

India’s polyurethane sealants market is expanding at an unprecedented pace, propelled by urban infrastructure development, housing initiatives, and rapid industrialization. The construction boom—fueled by government programs such as “Housing for All” and Smart Cities Mission—is creating immense demand for construction-grade polyurethane sealants, particularly in precast, waterproofing, and expansion joint applications. In July 2024, Henkel expanded its Kurkumbh facility, the company’s largest adhesive and sealant plant in India, to strengthen local production capacity for polyurethane-based solutions targeting construction, packaging, and general industrial markets.

Domestic companies such as Pidilite Industries Ltd. are also scaling their portfolios of PU sealants to serve both professional contractors and DIY markets, leveraging the country’s expanding retail and distribution networks. Meanwhile, India’s automotive manufacturing clusters in Tamil Nadu and Maharashtra are increasing demand for OEM-grade polyurethane sealants for vehicle assembly, glazing, and underbody protection. With its robust policy support, foreign investment inflows, and evolving manufacturing infrastructure, India is rapidly emerging as South Asia’s fastest-growing hub for polyurethane sealant production and application.

Polyurethane Sealants Market Report Scope

Polyurethane Sealants Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$5.3 Billion

|

|

Market Size (2034)

|

$8.3 Billion

|

|

Market Growth Rate

|

5.1%

|

|

Segments

|

By Product Type (One-Component, Two-Component, Hybrid), By Application (Glazing and Fenestration, Expansion and Construction Joints, Flooring and Joining, Sanitary and Kitchen, Submerged and Tank), By End-Use Industry (Building and Construction, Automotive and Transportation, General Industrial, Aerospace and Defense, Others), By Raw Material (Isocyanates, Polyols

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Sika AG, Henkel AG & Co. KGaA, The Dow Chemical Company, BASF SE, Arkema S.A. (Bostik), H.B. Fuller Company, 3M Company, Soudal N.V., Mapei S.p.A., Huntsman Corporation, Wacker Chemie AG, RPM International Inc., Pidilite Industries Limited, ITW Polymers Sealants North America, Konishi Co. Ltd.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

By Product Type/Chemistry

- One-Component

- Two-Component

- Hybrid

By Application

- Glazing and Fenestration

- Expansion and Construction Joints

- Flooring and Joining

- Sanitary and Kitchen

- Submerged and Tank

By End-Use Industry

- Building and Construction

- Automotive and Transportation

- General Industrial

- Aerospace and Defense

- Others

By Raw Material

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in Polyurethane Sealants Market

- Sika AG

- Henkel AG & Co. KGaA

- The Dow Chemical Company

- BASF SE

- Arkema S.A. (Bostik)

- H.B. Fuller Company

- 3M Company

- Soudal N.V.

- Mapei S.p.A.

- Huntsman Corporation

- Wacker Chemie AG

- RPM International Inc.

- Pidilite Industries Limited

- ITW Polymers Sealants North America

- Konishi Co. Ltd.

*- List not Exhaustive

Research Coverage

Developed by USDAnalytics, this report investigates the Global Polyurethane Sealants Market through rigorous analysis reviews of demand drivers, compliance shifts, and technology adoption across construction, transportation, and industrial value chains; it highlights breakthroughs in ultra-low-monomer chemistries, hybrid/fast-cure systems, and water-borne dispersions, translating specification-level performance (movement accommodation, elastic recovery, weatherability, and substrate versatility) into sourcing, cost-in-use, and ROI guidance—making this report an essential resource for executives, engineers, and procurement leaders optimizing sealant selection for green buildings, EV platforms, and long-life infrastructure.

Scope Highlights

Segmentation:

- By Product Type/Chemistry: One-Component; Two-Component; Hybrid.

- By Application: Glazing & Fenestration; Expansion & Construction Joints; Flooring & Joining; Sanitary & Kitchen; Submerged & Tank.

- By End-Use Industry: Building & Construction; Automotive & Transportation; General Industrial; Aerospace & Defense; Others.

- By Raw Material: Isocyanates; Polyols.

- By Region: North America (United States, Canada, Mexico); Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe); Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC); South & Central America (Brazil, Argentina, Rest of SCA); Middle East & Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa).

Geographic Scope: Analysis spans 25+ countries across North America, Europe, Asia Pacific, Latin America, the Middle East & Africa.

Time Horizon: Historic data 2021–2024 and forecast 2025–2034.

Companies Covered: Analysis / profiles of 15+ companies.

Deliverables

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.