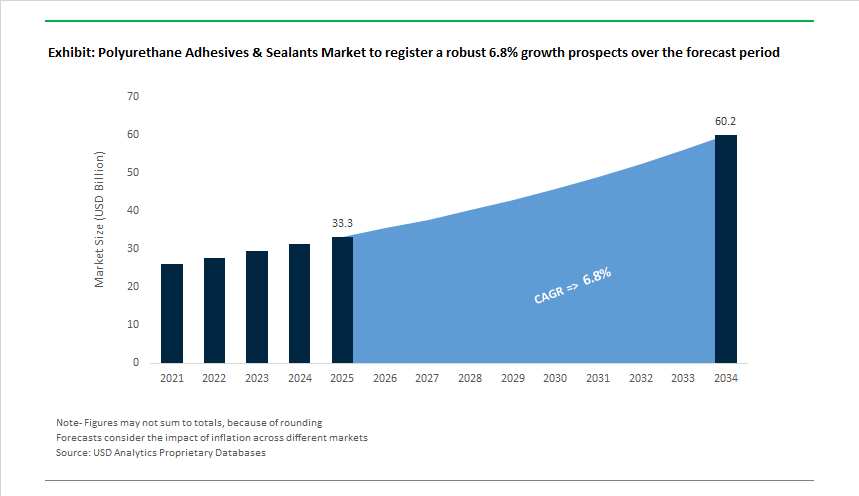

The Global Polyurethane Adhesives and Sealants Market is projected to grow from USD 33.3 billion in 2025 to USD 60.2 billion by 2034, advancing at a CAGR of 6.8%, reflecting polyurethane’s enduring role as the default elastic bonding and sealing chemistry across construction, mobility, packaging, and electronics. Unlike specialty adhesives that compete on narrow performance niches, polyurethane continues to scale because it uniquely balances elastic recovery, adhesion across heterogeneous substrates, moisture tolerance, and long-term durability—attributes that remain difficult to replicate simultaneously with alternative chemistries.

Polyurethane adhesives and sealants are increasingly specified not as interchangeable consumables, but as risk-mitigation materials in applications exposed to thermal cycling, vibration, and environmental ingress. In construction and infrastructure, PU sealants underpin façade glazing, expansion joints, waterproofing, and thermal insulation systems where movement accommodation and weather resistance directly affect asset lifespan. In automotive and EV manufacturing, PU systems are integral to battery pack bonding, vibration damping, and mixed-material assemblies, where elastic stress distribution is essential to prevent fatigue and cracking over long duty cycles.

Within the market, value is shifting decisively toward reactive and hot-melt polyurethane systems, reflecting both regulatory pressure and manufacturing economics. Reactive PU adhesives, which cure via moisture or latent crosslinking mechanisms, continue to dominate applications requiring long-term mechanical integrity under dynamic stress, such as structural panels, sandwich composites, and transportation assemblies. At the same time, hot-melt polyurethane (HMPUR) adhesives—now accounting for over one-third of global demand—are gaining ground in woodworking, packaging, and industrial assembly, where fast set times, solvent-free processing, and high green strength support automated, high-throughput production lines.

The polyurethane adhesives and sealants industry has experienced a period of rapid transformation, characterized by major investments, new product innovations, and regulatory alignment toward sustainability.

In March 2025, Henkel AG & Co. KGaA projected 2–4% organic sales growth for its Adhesive Technologies business, fueled by demand in Mobility & Electronics and industrial manufacturing segments. This announcement followed a series of strategic expansions, including a USD 23 million modernization of its Bopfingen, Germany facility (October 2023–2025)—a site pivotal to Henkel’s global polyurethane adhesives production network. The company’s proactive investment signals a long-term strategy to reinforce its leadership in reactive hot-melt and structural polyurethane adhesives for next-generation electric vehicles and electronics.

Meanwhile, Lubrizol Corporation entered the spotlight in May 2024 with the launch of Pearlbond ECO 590 HMS TPU, expanding its bio-based thermoplastic polyurethane (TPU) portfolio. This development is significant for the hot melt adhesives (HMA) market, offering sustainable, high-performance bonding solutions for footwear, automotive, and flexible packaging. The same month, Bostik (Arkema) announced a $27 million investment in its Middleton, Massachusetts plant, aimed at expanding manufacturing capacity for low-VOC, sustainable polyurethane adhesives, reinforcing its North American market leadership.

In Late 2024, Mitsui Chemicals revealed a major capacity expansion for polyurethane dispersions (PUDs) in response to growing European demand for sustainable packaging solutions, doubling its production by 2025. This expansion strengthens supply chains for water-based PU systems and underlines a marketwide pivot toward eco-friendly adhesive technologies. Similarly, Sika AG continued to roll out its Purform® technology, introduced in January 2022, which sets the benchmark for ultra-low monomer polyurethane adhesives with less than 0.1% diisocyanate content, aligning with Europe’s REACH compliance.

In October 2023, Dow Thailand Group introduced the DIAMONDLOCK polyurethane flooring adhesive, designed for low-VOC, flexible, and non-flammable performance in the construction sector—a crucial development for Asia’s green infrastructure drive. On the innovation front, H.B. Fuller’s 2025 Customer Innovation Awards (September 2025) recognized breakthroughs such as triple-insulating glass units (IGUs), showcasing PU adhesive integration for superior thermal efficiency in sustainable building designs.

Market Trend 1: Accelerated Shift Towards Waterborne and Reactive Hot-Melt Polyurethane (HMPUR) Systems

The polyurethane adhesives and sealants market is rapidly embracing waterborne dispersions and HMPUR technologies to meet global environmental standards while enhancing productivity and safety. With tightening VOC (Volatile Organic Compound) and isocyanate exposure limits, industries such as automotive, construction, and consumer goods are transitioning from solvent-based formulations to reactive and zero-emission systems.

In the United States, stringent VOC regulations—such as those in the District of Columbia, which cap VOC levels for certain polyurethane adhesives at below 70 g/L—have compelled adhesive formulators to innovate. Similarly, in Europe, the Industrial Emissions Directive (IED) and consumer-driven sustainability expectations have accelerated the adoption of low monol DMC-based polyols, which reduce VOC emissions by over 95% during polyurethane production.

Automotive OEMs, especially those operating high-speed assembly lines, are at the forefront of the shift. The rise of reactive HMPUR adhesives, which feature open times as short as 30 seconds and require no external curing agents, has optimized manufacturing efficiency while eliminating harmful solvent residues. Their moisture-curing mechanism delivers superior durability, bonding strength, and flexibility—key attributes for interior trim, dashboard lamination, and lightweight assembly applications.

Market Trend 2: Development of High-Performance Polyurethane Systems for Electric Vehicle Battery Pack Assembly

The emergence of electric vehicles (EVs) has created a new frontier for the polyurethane adhesives and sealants industry. The integration of structural bonding, vibration dampening, and thermal management within battery modules and electric drivetrains demands advanced polyurethane chemistries capable of multifunctional performance.

Leading material innovators such as DuPont and 3M have developed Thermally Conductive Structural Adhesives (TCSAs) and compressible polyurethane insulators that enable crash-durable, thermally stable, and fire-resistant bonding within battery packs. These materials not only secure dissimilar substrates—such as aluminum, steel, and polymer housings—but also regulate heat transfer to mitigate thermal runaway risks.

The need for high dielectric strength, low outgassing, and moisture-resistant sealing has positioned polyurethane systems as indispensable for EVs. Their role extends from cell-to-cell gap fillers and busbar potting to pack sealing for ingress protection under extreme environmental conditions.

In Asia-Pacific, particularly China, where over 9.5 million new-energy vehicles were sold in a single year, the scaling of EV battery production lines has created record demand for specialized polyurethane adhesives that combine thermal conductivity and flexibility. The high-specification demand is driving ongoing R&D investment in advanced polyurethane formulations for EV manufacturing ecosystems, solidifying their role in the electromobility supply chain.

Market Opportunity 1: Capitalizing on the Industrialization of Wood-Based Construction and Mass Timber

The rise of engineered wood construction, including Cross-Laminated Timber (CLT) and Glue-Laminated Timber (GLT), has opened substantial growth avenues for high-strength polyurethane structural adhesives. These systems are valued for their superior bond integrity, long open times, and resistance to humidity and temperature fluctuations, making them ideal for mass timber panel lamination and on-site bonding.

A recent Linnaeus University research initiative, supported by Södra’s research foundation, is spearheading the development of bio-based polyurethane adhesives derived from liquefied biomass and technical kraft lignin, aimed at reducing dependency on petrochemical polyols. The aligns with the construction industry’s push toward low-carbon building materials and ESG-aligned procurement.

Academic studies further confirm polyurethane’s superior bond line shear strength, particularly in hardwood CLT panels made from red oak and yellow poplar, outperforming traditional phenol-formaldehyde adhesives. These results establish polyurethane as the preferred bonding solution for both softwood and hardwood mass timber assemblies, delivering enhanced load-bearing and seismic resilience.

Notably, one-component (1K) moisture-curing polyurethane systems account for approximately 52% of total construction adhesive usage, underscoring their pivotal role in the industrialized and modular construction sectors. The ability to deliver structural-grade performance with easy application makes polyurethane adhesives central to the global expansion of prefabricated and engineered timber buildings.

Market Opportunity 2: Servicing the Offshore Wind Energy Sector with High-Durability Marine Sealants

The global offshore wind energy boom is creating long-term, high-margin opportunities for polyurethane sealants and coatings engineered for marine and corrosive environments. With wind turbine installations expanding rapidly across Europe, Asia, and North America, durable polyurethane protection systems are in high demand for towers, transition pieces, and foundations exposed to saltwater and extreme weather.

For C5-M corrosivity zones (as classified under ISO 12944-5), offshore structures typically rely on a multi-layer coating system that includes a zinc epoxy primer, intermediate epoxy layer, and polyurethane topcoat, achieving a total dry film thickness (DFT) of approximately 320 μm. The polyurethane layer serves as the UV-resistant, color-stable finish that ensures long-term gloss retention and protection from mechanical erosion.

Product innovation is also being driven by stricter worker safety and REACH compliance mandates. Sikaflex® Purform sealants, for example, feature monomeric diisocyanate levels below 0.1%, offering high durability, chemical resistance, and safety compliance under the EU’s latest Occupational Exposure Limits (OEL).

In addition, polyurethane’s tunable Shore hardness range (A10–D90+) allows its use across diverse offshore applications—from vibration-dampening seals and blade edge fillers to rigid tower coatings—providing unparalleled mechanical adaptability. As global offshore wind capacity is expected to triple by 2030, polyurethane-based sealants and coatings are set to become a cornerstone of long-life, corrosion-resistant marine infrastructure.

Polyurethane Adhesives & Sealants Market Share Insights, 2025-2034

Market Share by Product Type

The polyurethane adhesives segment dominates the global polyurethane adhesives and sealants market, capturing an estimated 58.6% share in 2025. This leadership stems from polyurethane adhesives’ exceptional mechanical strength, flexibility, and adhesion versatility, which make them indispensable across diverse industries such as automotive, construction, electronics, and footwear. Their superior bonding ability on a wide range of substrates — including metals, plastics, composites, and wood — has positioned them as a material of choice for structural and semi-structural bonding applications. The automotive sector, in particular, relies heavily on polyurethane adhesives for panel bonding, glass installation, and lightweight composite assembly, supporting the shift toward fuel efficiency and electric vehicle (EV) designs. Additionally, their high chemical resistance, moisture tolerance, and temperature stability drive usage in industrial manufacturing and product assembly.

Conversely, polyurethane sealants hold a strong and stable market position, serving as the cornerstone of construction and infrastructure sealing applications. Their elasticity, UV stability, and weatherproofing capabilities make them ideal for expansion joints, glazing, and façade sealing, where long-term environmental exposure is a key concern. Sealants are also critical in transportation, shipbuilding, and heavy machinery, where they prevent leakage, vibration, and corrosion. As the construction industry accelerates its focus on durable, energy-efficient building materials, the demand for low-VOC, moisture-curing polyurethane sealants continues to rise.

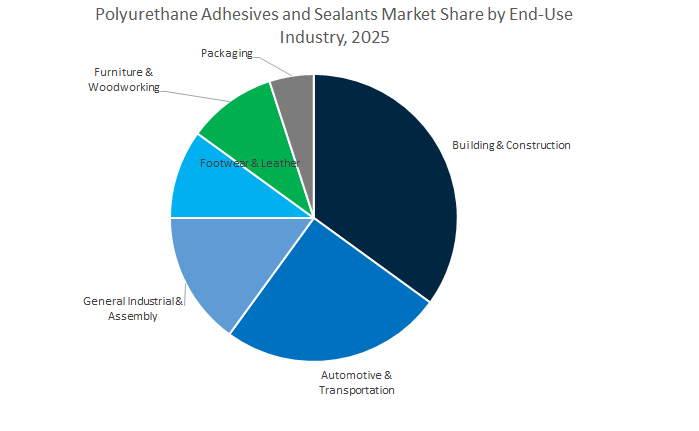

Market Share by End-Use Industry

The building and construction sector leads the global polyurethane adhesives and sealants market, commanding a projected 34.3% share in 2025. This dominance is attributed to polyurethane’s unmatched performance in structural glazing, flooring, roofing, insulation, and concrete repair applications. The industry’s preference for low-VOC, high-durability sealants and adhesives aligns with modern construction standards emphasizing energy efficiency, sustainability, and longevity. Polyurethane formulations are essential for facade bonding, window installations, and waterproofing systems, where their superior elasticity accommodates movement while maintaining adhesion under thermal and environmental stress. Additionally, the growing demand for pre-fabricated and modular construction techniques has boosted the adoption of fast-curing PU adhesives, which enhance production speed and assembly precision.

The automotive and transportation segment represents one of the fastest-growing application areas, driven by the global shift toward electric vehicles (EVs) and lightweighting strategies. Polyurethane adhesives are increasingly used in battery module encapsulation, panel assembly, and glass bonding, offering vibration damping, chemical resistance, and long-term durability. The general industrial and assembly sector remains a major consumer, employing PU adhesives for bonding, coating, and sealing in machinery, appliances, and product manufacturing that require structural integrity under dynamic loads. Footwear and leather applications continue to rely on polyurethane adhesives for sole bonding and material lamination, where flexibility and comfort are critical differentiators. In furniture and woodworking, polyurethane formulations enable strong, moisture-resistant joints, supporting aesthetic design and durability.

While the packaging industry accounts for a smaller portion of the market, its role is growing due to the adoption of polyurethane-based laminating adhesives in flexible and specialty packaging. These adhesives deliver superior chemical resistance, adhesion to films, and compliance with food safety regulations, making them indispensable in high-performance packaging applications.

The competitive landscape of the polyurethane adhesives and sealants market is shaped by a combination of technological innovation, sustainability commitments, and geographic expansion. Major players—including Henkel, Sika, H.B. Fuller, Bostik (Arkema), and Dow—are reinforcing their global production capacities, focusing on bio-based chemistry, ultra-low monomer formulations, and high-performance applications spanning from EV battery assembly to construction waterproofing systems.

Henkel maintains a commanding position in polyurethane adhesives and sealants, driven by its Loctite and Teroson product lines. The company’s Bopfingen plant expansion (2024–2025), worth approximately USD 23 million, underscores its strategy to optimize global adhesive production networks. Henkel’s reactive polyurethane hot melts (PUR HMAs) are central to automotive, packaging, and electronics markets, where precision and durability are essential. The company’s focus on Mobility & Electronics aligns with the surging demand for PU-based solutions in EV battery bonding and advanced industrial sealing applications.

Sika AG has cemented its position as a global technology leader in the construction and automotive sectors through its flagship Sikaflex® and SikaTack® product lines. The introduction of Purform® technology in 2022—featuring ultra-low monomeric diisocyanate content (<0.1%)—set a new benchmark for health and environmental safety compliance in polyurethane adhesives and sealants. Sika’s R&D is heavily aligned with global trends in green building certification and automotive lightweighting, providing comprehensive systems for joint sealing, direct glazing, and weatherproofing. Its global deployment of Purform products demonstrates commitment to next-generation, low-emission construction materials.

As one of the world’s largest pure-play adhesive companies, H.B. Fuller offers a diverse range of one- and two-component polyurethane systems engineered for high mechanical strength and extreme environmental performance. In 2025, the company gained recognition for its Customer Innovation Awards, particularly for triple-insulating glass unit (IGU) applications that enhance energy-efficient window performance. With a portfolio exceeding 20,000 adhesive products and 700+ patents, H.B. Fuller combines technological expertise with co-innovation partnerships, reinforcing its role in the energy-efficient construction and industrial assembly sectors.

Bostik, under Arkema, continues to expand its specialty polyurethane adhesive and sealant portfolio with a strong focus on sustainability and process efficiency. Its $27 million expansion in Massachusetts (2024) strengthens capacity for low-VOC and solvent-free polyurethane systems, aligning with customer sustainability targets. Leveraging Arkema’s expertise in specialty polymers such as PVDF, Bostik delivers innovative solutions for construction, industrial filtration, and personal care applications. Through synergistic R&D with Arkema, Bostik’s 2KPU® adhesives have gained prominence in ultra-filtration cartridge and water treatment solutions—a growing sustainability frontier.

Dow combines material science leadership with deep integration across polyols and isocyanates, enabling the design of custom polyurethane systems for adhesives and sealants. Its DIAMONDLOCK polyurethane flooring adhesive (launched in 2023 in Thailand) showcases the company’s strategic move toward low-VOC, non-flammable construction adhesives that meet the region’s sustainable building codes. Dow’s ongoing innovation in reactive polyurethane polymers positions it as a foundational supplier to adhesive manufacturers, particularly in the construction, insulation, and automotive assembly markets.

Country Analysis: Regional Market Dynamics and Strategic Developments in the Global Polyurethane Adhesives and Sealants Industry

United States: Infrastructure Expansion and Automotive Electrification Driving Polyurethane Adhesives Innovation

The United States Polyurethane Adhesives and Sealants market is undergoing rapid growth, propelled by large-scale infrastructure investments, the transition to electric mobility, and a strong push toward sustainable adhesive technologies. The Infrastructure Investment and Jobs Act (IIJA) has significantly boosted demand for high-durability polyurethane sealants used in bridge joints, highway repair, and civil construction, where flexibility and environmental resistance are essential. Parallelly, the surge in modular and prefabricated construction is stimulating adoption of low-isocyanate, ultra-flexible polyurethane adhesives, like those launched by Sika AG, to improve bonding precision and extend open time for off-site panel assembly.

The automotive and transportation sectors represent a major growth avenue, with EV manufacturers increasingly turning to dual-cure polyurethane adhesives, such as the UV and moisture-cured systems developed by 3M Company, for battery modules, sensors, and interior laminations. Innovation in recyclable polyurethane adhesives, pioneered by Dow Inc., is revolutionizing the flexible packaging market, offering sustainable solutions for major consumer packaged goods (CPG) brands. Meanwhile, Lubrizol Corporation expanded its bio-based TPU range for hot melt adhesives, reinforcing its focus on carbon footprint reduction. Belzona Inc. introduced new two-part polyurethane bonding systems for erosion and corrosion repair in industrial equipment, aligning with the growing maintenance and repair demand. Overall, the U.S. market is increasingly defined by sustainability, electrification, and infrastructure resilience, making it a global innovation leader in polyurethane adhesive systems.

Germany: Electrification and Low-VOC Technologies Anchoring Europe’s Polyurethane Leadership

Germany remains the European epicenter of polyurethane adhesives and sealants innovation, driven by automotive electrification, sustainable chemistry, and regulatory pressure. In 2024, Henkel AG & Co. KGaA announced a €21.5 million investment in expanding its Bopfingen adhesives plant, a critical global site for polyurethane adhesive production. Similarly, Dow’s tenfold expansion of its VORATRON™ thermal management adhesives in Ahlen underscores the country’s central role in meeting EV battery assembly requirements, where heat dissipation and bonding integrity are vital.

Germany’s Green Building movement and EU VOC regulations are accelerating the adoption of water-borne and low-emission polyurethane adhesives, especially in flooring, wood bonding, and insulation applications. Henkel’s TECHNOMELT bio-based PUR adhesives exemplify The transition toward eco-friendly manufacturing, catering to the furniture and electronics sectors. Meanwhile, BASF SE’s 2024 expansion of its PUD (Polyurethane Dispersion) capacity in Spain supports Europe’s growing demand for low-VOC laminating adhesives, particularly in packaging and textiles. Additionally, the German government’s recyclability targets for household packaging by 2025 are driving R&D toward recyclable and solvent-free PUR adhesives. With global OEMs and top-tier R&D centers like Fraunhofer leading advancements, Germany continues to define Europe’s polyurethane sustainability roadmap through material innovation, precision engineering, and circularity compliance.

China: Expanding Production Base and Infrastructure Development Strengthening Global Polyurethane Demand

China stands as the largest consumer and fastest-growing production hub in the global Polyurethane Adhesives and Sealants market, supported by massive industrial, automotive, and construction expansion. The nation’s 2024 milestone came with Beijing Gaomeng New Materials’ capacity expansion project, enhancing domestic production of composite and water-based polyurethane adhesives. The development aligns with China’s policy focus on energy-efficient, solvent-free adhesive technologies under its Green Manufacturing initiatives.

Robust infrastructure investment, particularly in high-speed rail and urban transit systems, continues to drive demand for two-component (2C) structural polyurethane adhesives, known for high bonding strength and vibration resistance. The construction envelope market—encompassing curtain walls, insulation, and glazing—is also seeing increased polyurethane usage due to national energy efficiency mandates. Sika AG’s acquisition of Crevo-Hengxin, a Chinese sealant manufacturer, has strengthened its Asia-Pacific polyurethane sealant portfolio, enhancing local distribution and production capabilities. Additionally, automotive OEMs, including China’s rapidly growing EV segment, are heavily adopting fast-curing, lightweight polyurethane adhesives to improve bonding between composite, metal, and plastic parts. China’s footwear manufacturing base further drives significant demand for solvent-free and water-based polyurethane adhesives, cementing the country’s position as a global hub for both volume production and sustainable polyurethane innovation.

India: Infrastructure Modernization and Local Manufacturing Accelerating Polyurethane Adhesive Adoption

India’s Polyurethane Adhesives and Sealants market is entering a phase of rapid industrialization and modernization, propelled by government-led initiatives such as the “Smart Cities Mission” and “Housing for All” programs. The projects are driving massive demand for high-performance polyurethane sealants used in infrastructure, commercial real estate, and waterproofing applications. The rise of prefabricated construction and transportation projects is also fueling growth in structural and flexible polyurethane bonding solutions.

Domestic adhesive leader Pidilite Industries Ltd. is expanding its industrial polyurethane portfolio for construction, lamination, and waterproofing, responding to a growing appetite for durable, fast-curing solutions. India’s rapidly expanding e-commerce and packaging industry is further driving consumption of solvent-free polyurethane laminating adhesives, meeting global food-contact safety standards. The automotive sector, spurred by the Make in India initiative, is increasingly utilizing lightweight polyurethane adhesives to improve NVH (Noise, Vibration, and Harshness) performance in vehicle assembly. Additionally, industrial flooring and furniture manufacturing are seeing a major transition toward Hot-Melt Polyurethane (HMPUR) adhesives, prized for their moisture resistance and quick bonding speed. Supported by government infrastructure spending, rising disposable incomes, and localized adhesive production, India is rapidly emerging as South Asia’s strategic growth hub for polyurethane technologies.

Brazil: Infrastructure Expansion and Automotive Growth Driving Latin American Polyurethane Market Development

Brazil dominates the Latin American polyurethane adhesives and sealants market, driven by strong construction activity, industrial expansion, and automotive output. Major urban infrastructure and pre-salt oil and gas projects are key growth engines for weather-resistant polyurethane sealants, particularly for concrete joint sealing and waterproofing. The residential construction boom, coupled with Brazil’s expanding energy-efficient housing initiatives, is supporting adoption of polyurethane foams and sealants for insulation and air sealing within building envelopes.

The automotive sector continues to be a significant consumer, using polyurethane adhesives for windshield bonding and structural assembly, aligning with global safety and performance standards. The furniture and woodworking industries are progressively adopting low-VOC, water-borne polyurethane adhesives, replacing solvent-heavy alternatives in compliance with evolving environmental regulations. In parallel, Brazil’s packaging and footwear sectors, both major export industries, are driving demand for flexible, high-performance PUR adhesives for lamination and sole bonding. Additionally, Sika’s acquisition of a Peruvian family-owned adhesives business in 2023 has expanded its distribution footprint across Latin America, positioning Brazil as a regional hub for polyurethane construction and industrial solutions. The country’s steady industrial recovery and sustainability push make it a key emerging player in the global polyurethane adhesives landscape.

Polyurethane Adhesives & Sealants Market Report Scope

Polyurethane Adhesives & Sealants Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$33.3 Billion

|

|

Market Size (2034)

|

$60.2 Billion

|

|

Market Growth Rate

|

6.8%

|

|

Segments

|

By Product Type (Polyurethane Adhesives, Polyurethane Sealants), By Raw Material Type (Polyols, Isocyanates, Prepolymers), By Technology - Adhesives (Solvent-Borne, Water-Borne, 100% Solids, Two-Component, Hybrid), By Technology - Sealants (One-Component, Two-Component), By End-User (Building & Construction, Automotive & Transportation, Packaging, Footwear & Leather, Furniture & Woodworking, General Industrial & Assembly

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Henkel AG & Co. KGaA, Sika AG, H.B. Fuller Company, Dow Inc., Arkema S.A. (Bostik), Huntsman Corporation, BASF SE, 3M Company, Wacker Chemie AG, Covestro AG, Illinois Tool Works Inc. (ITW), Jowat SE, MAPEI S.p.A., Pidilite Industries Ltd., RPM International Inc.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

By Product Type

- Polyurethane Adhesives

- Polyurethane Sealants

By Raw Material Type

- Polyols

- Isocyanates

- Prepolymers

By Chemistry/Technology - Adhesives

- Solvent-Borne

- Water-Borne

- 100% Solids

- Two-Component

- Hybrid

By Chemistry/Technology - Sealants

- One-Component

- Two-Component

By End-Use Industry

- Building & Construction

- Automotive & Transportation

- Packaging

- Footwear & Leather

- Furniture & Woodworking

- General Industrial & Assembly

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in Polyurethane Adhesives and Sealants Market

- Henkel AG & Co. KGaA

- Sika AG

- H.B. Fuller Company

- Dow Inc.

- Arkema S.A. (Bostik)

- Huntsman Corporation

- BASF SE

- 3M Company

- Wacker Chemie AG

- Covestro AG

- Illinois Tool Works Inc. (ITW)

- Jowat SE

- MAPEI S.p.A.

- Pidilite Industries Ltd.

- RPM International Inc.

*- List not Exhaustive

Research Coverage

This report investigates the Global Polyurethane Adhesives and Sealants Market, delivering analysis reviews on demand shifts, regulatory momentum, technology upgrades, and cost-to-serve dynamics; it highlights the rapid adoption of water-borne, 100% solids, and reactive systems; quantifies end-use penetration across construction, mobility, packaging, and electronics; and maps supplier innovation from ultra-low-monomer PUR to thermally conductive and fast-cycle HMPUR. Built by USDAnalytics, the study connects capacity moves, feedstock trends, and application engineering metrics to purchasing decisions, showcases breakthroughs in EV battery pack bonding and mass-timber structural adhesion, and stress-tests scenarios under VOC/REACH compliance and EHS constraints—making this report an essential resource for procurement leaders, converters, and OEM design teams seeking durable, flexible, and sustainable polyurethane bonding and sealing solutions at scale.

Scope Highlights

Segmentation:

- By Product Type: Polyurethane Adhesives; Polyurethane Sealants.

- By Raw Material Type: Polyols; Isocyanates; Prepolymers.

- By Chemistry/Technology – Adhesives: Solvent-Borne; Water-Borne; 100% Solids; Two-Component; Hybrid.

- By Chemistry/Technology – Sealants: One-Component; Two-Component.

- By End-Use Industry: Building & Construction; Automotive & Transportation; Packaging; Footwear & Leather; Furniture & Woodworking; General Industrial & Assembly.

- By Region: North America (United States, Canada, Mexico); Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe); Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC); South & Central America (Brazil, Argentina, Rest of SCA); Middle East & Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa).

Geographic Scope: Analysis spans 25+ countries across North America, Europe, Asia Pacific, Latin America, the Middle East & Africa.

Time Horizon: Historic data 2021–2024 and forecasts 2025–2034.

Companies Covered: Analysis / profiles of 15+ companies.

Deliverables

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.