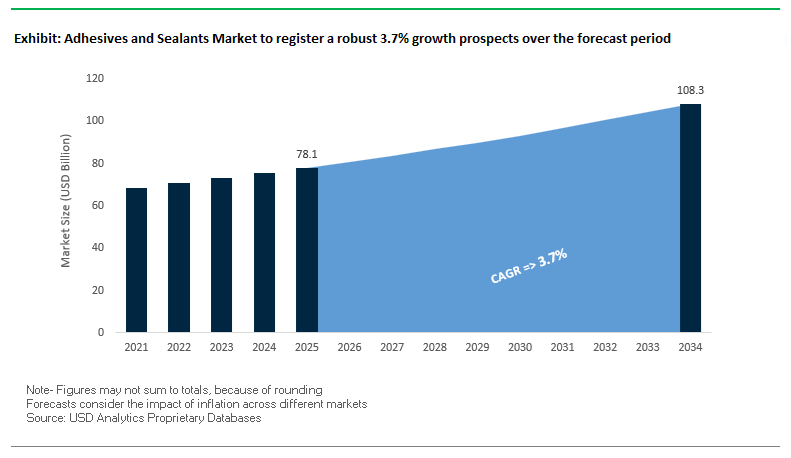

The global adhesives and sealants market is valued at $78.1 billion in 2025 and is expected to reach $108.4 billion by 2034, expanding at a CAGR of 3.7%. The market’s growth trajectory is underpinned by rising demand across construction, automotive, packaging, and electronics sectors, coupled with the transition toward low-VOC, water-based, and sustainable adhesive technologies. The market is also characterized by the increasing penetration of bio-based formulations, stricter environmental regulations, and digital transformation in adhesive manufacturing. For manufacturers and end-users, the focus is shifting from cost competitiveness to performance longevity, carbon reduction, and recyclability—key priorities for global sustainability mandates.

Demand is expanding beyond conventional building envelopes into automotive insulated glass, where OEMs are using advanced IG sealants to improve thermal comfort, acoustic damping, condensation resistance, and vehicle energy efficiency, particularly in EV platforms. At the same time, façade engineers and glass fabricators are specifying sealant systems that comply with low-VOC regulations, embodied-carbon targets, and long-term certification standards (EN 1279, ASTM E2190, ISO 9001/14001), accelerating innovation in sustainable silicone and hybrid chemistries.

Regionally, Asia-Pacific is emerging as the fastest-scaling market, driven by high-rise construction, climate-adaptive façade design, and infrastructure investment, while Europe and North America continue to lead in code-driven retrofits, warm-edge adoption, and premium IG performance standards. As a result, manufacturers with integrated portfolios spanning spacers, coatings, sealants, and façade systems are gaining strategic advantage by offering glass processors complete, validated IG solutions rather than standalone products.

The global adhesives and sealants industry is experiencing rapid strategic realignments, driven by decarbonization goals, portfolio optimization, and global expansion efforts. In October 2025, Henkel and Dow expanded their strategic partnership to accelerate decarbonization across the adhesive portfolio—targeting low-carbon feedstocks, renewable electricity, and hot-melt adhesive innovation for sustainable packaging applications. This collaboration represents a significant milestone in the industry’s transition toward low-carbon adhesives and net-zero production ecosystems.

In the same month (October 2025), Sika AG expanded its European footprint through the acquisition of Marlon Tørmørtel A/S, a Danish mortar manufacturer. This acquisition strengthens Sika’s position in the Nordic construction market, enabling cross-selling between mortar, sealant, and waterproofing product lines. Meanwhile, H.B. Fuller reported Q2 2025 Adjusted EBITDA of $166 million, up 5% year-over-year, supported by its portfolio shift toward high-margin adhesives and sustained cost management.

Geographically, major players continue to strengthen production networks across Asia-Pacific and the Middle East. In June 2025, Sika AG finalized the acquisition of a construction chemicals company in Qatar, expanding its presence in the Middle East’s booming infrastructure sector. Similarly, in April 2025, Sika opened a new plant in Kazakhstan for concrete admixtures and mortars, further boosting its Central Asian capacity.

Corporate realignments are reshaping strategic focus areas—H.B. Fuller’s launch of the Building Adhesive Solutions (BAS) global business unit in January 2025 marked a decisive step to strengthen its construction adhesives portfolio. Simultaneously, Sika AG’s new manufacturing sites in Singapore and China (Xi’an and Suzhou) reinforce its commitment to Asia-Pacific expansion and supply chain proximity.

Despite headwinds in the automotive and construction sectors, Wacker Chemie AG (March 2025) demonstrated strong financial resilience, maintaining stable sales through its Silicones and Polymers divisions. In the UK, Sika’s acquisition of Cromar Building Products (March 2025) added a well-established roofing systems portfolio, enhancing its building envelope and waterproofing solutions. These developments underline the ongoing consolidation trend, where leading companies are merging capacity, R&D, and sustainability to maintain competitiveness in a tightening regulatory landscape.

A defining trend in the global adhesives and sealants industry is the accelerated shift from petrochemical-based raw materials to bio-circular and renewable feedstocks, driven by corporate sustainability goals, lifecycle emissions regulations, and end-user demand for eco-compliant materials. The transformation is not only environmental but also economic—signaling a complete reorientation of the supply chain toward low-carbon, circular adhesive solutions.

In early 2024, Bostik (Arkema Group) exemplified the movement by introducing Kizen LIME, a bio-circular hotmelt adhesive formulated with over 80% renewable ingredients, fully certified under recognized bio-based material standards. Collaborating with partners like Dow, Arkema achieved a near 100% carbon footprint avoidance, including biogenic carbon uptake, establishing a new performance and sustainability benchmark for high-volume packaging adhesives.

At a regulatory level, frameworks such as REACH (EU) and the US EPA’s Safer Choice program are exerting unprecedented pressure on traditional formulations, compelling manufacturers to reformulate adhesives using low-VOC, non-toxic, and recyclable raw materials. In the U.S., Safer Choice certification is a recognized differentiator in construction, consumer goods, and green building materials procurement.

In 2025, one leading Asian adhesive manufacturer reported that 86% of its adhesive revenue originated from eco-certified green materials, underscoring the rapid commercial viability of sustainable chemistry. The adoption of bio-based hot melts and bio-polymers across packaging, construction, and assembly applications signals a clear industry pivot toward carbon neutrality and next-generation circular adhesive technologies.

The next wave of innovation in the adhesives and sealants market is centered around smart and functional adhesives that extend beyond bonding — providing added functionalities like conductivity, heat dissipation, debonding, and sensing. These advancements are enabling circular product design, modular electronics, and high-value component recovery, particularly in electronics and automotive manufacturing.

A prime example is Apple’s integration of electrically released adhesives in its latest smartphone models, which allow for non-destructive disassembly of batteries and critical components. The adhesive maintains high initial strength yet releases completely upon application of a low electrical voltage (9–12V) for under a minute—aligning with global “Right to Repair” and electronics recycling mandates. The innovation marks a paradigm shift in electronics repairability and sustainability, reducing waste and enabling efficient end-of-life material recovery.

Similarly, industry leaders like Henkel and tesa SE are accelerating the rollout of debonding-on-demand adhesives in alignment with upcoming EU EV battery passport regulations and recycling quotas. These adhesives enable controlled separation of critical battery pack components, directly supporting EV circularity, remanufacturing, and recycling systems. As electric vehicle batteries can account for nearly 50% of a vehicle’s total cost, debonding adhesive technologies are becoming pivotal in next-generation battery lifecycle management.

The integration of smart adhesives, particularly in thermal, electrical, and mechanical management systems, represents the convergence of material science and intelligent manufacturing, creating a new frontier for multi-functional bonding materials that enhance both performance and sustainability.

The transition toward a hydrogen-based clean energy system is creating one of the most technically demanding markets for sealants and adhesive systems. Hydrogen’s molecular size and high diffusion capability require ultra-dense sealing materials that can resist permeation, rapid gas decompression (RGD), and hydrogen embrittlement under extreme operating conditions.

Hydrogen fuel storage and transportation systems operate at pressures up to 700 bar (10,000 psi)—an environment where even minor sealing failures can lead to catastrophic energy losses. The demand for low-permeability elastomers and advanced polymer sealants has therefore surged across electrolyzers, fuel cells, and cryogenic hydrogen tanks.

Specialized adhesive and sealant manufacturers are partnering with original equipment manufacturers (OEMs) across the hydrogen value chain to develop proprietary materials for bipolar plate sealing, gasket bonding, and cryogenic containment applications. These co-engineered materials exhibit high elasticity, thermal resistance, and long-term chemical stability, supporting the scalability of hydrogen mobility infrastructure.

The hydrogen economy—driven by global decarbonization policies, net-zero targets, and government incentives—presents a lucrative frontier for high-performance adhesives. Companies capable of delivering hydrogen-compatible sealants and composite interface bonding systems are poised to dominate a market that will underpin fuel cell manufacturing and clean energy logistics in the coming decade.

As the global automotive industry undergoes a seismic shift toward electrification and lightweighting, structural adhesives are replacing traditional mechanical fasteners as the primary enabler of multi-material bonding. The use of aluminum, carbon fiber, composites, and high-strength steels in EV design demands versatile adhesive systems that can handle dissimilar material bonding, vibration damping, and thermal expansion without compromising safety or rigidity.

In Body-in-White (BIW) assembly, epoxy and polyurethane structural adhesives are increasingly replacing spot welds to create continuous load transfer surfaces, improving torsional stiffness and crash resistance by over 30%. Unlike welds or rivets, adhesives distribute stress evenly, enhancing both structural performance and energy absorption during impact—key to meeting EV crash safety standards.

In addition, adhesives are critical for preventing galvanic corrosion between dissimilar metals such as steel and aluminum. The innovation allows OEMs to design lightweight, corrosion-resistant vehicle bodies while extending battery range and efficiency. As automakers continue to scale EV production, the demand for high-performance structural adhesives, battery encapsulants, and lightweight bonding solutions is expected to rise exponentially through 2030.

The integration of adhesives into automated manufacturing processes further drives their central role in the next generation of electric vehicles, bridging performance engineering with sustainability objectives.

Adhesives and Sealants Market Share Insights, 2025-2034

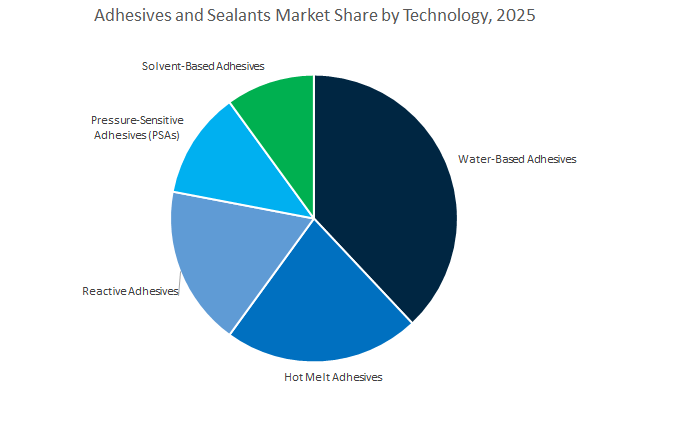

The water-based adhesives segment dominates the global adhesives and sealants industry, accounting for an estimated 38% of total market share in 2025. This leadership stems from its widespread acceptance as the most environmentally compliant and cost-effective bonding solution across multiple industries. Water-based adhesives have become the preferred choice for packaging, paper converting, woodworking, and construction applications due to their low VOC emissions, user-friendly formulations, and ease of cleanup. The transition toward sustainable and safer adhesive systems, driven by stringent environmental regulations such as REACH and EPA standards, continues to accelerate this segment’s growth. Furthermore, ongoing innovations in polyvinyl acetate (PVA), ethylene-vinyl acetate (EVA), and acrylic polymer emulsions are improving adhesive strength, drying time, and substrate versatility, making water-based technologies increasingly suitable for automated and high-speed production environments. As industries prioritize sustainability and regulatory compliance, water-based adhesives will remain the default technology for large-volume manufacturing and eco-friendly operations.

The hot melt adhesives segment, accounting for 22% of the global market, is one of the fastest-growing categories due to its solvent-free, instant-bonding formulations that support high-speed production in packaging, hygiene products, electronics, and automotive applications, with growth further reinforced by e-commerce expansion and increased use of EVA, polyamide, and polyolefin chemistries, as well as the rising adoption of reactive hot melts for furniture, textiles, and automotive interiors. In contrast, the reactive adhesives segment represents the high-value, performance-driven core of the industry, with epoxy, PUR, silicone, and anaerobic systems delivering structural strength, durability, and chemical resistance required in aerospace, automotive, wind energy, and electronics. Demand continues to accelerate with the use of lightweight composites, EV battery systems, and advanced electronic assemblies, while innovations in UV-curable and hybrid reactive technologies enable faster curing and greater precision in automated manufacturing, solidifying reactive adhesives as essential for high-performance engineering applications.

The pressure-sensitive adhesives segment occupies a strong and specialized role in the global adhesives market, serving as a critical technology for tapes, labels, graphic films, medical products, electronics, and automotive applications where peel adhesion, tack, and repositionability are essential. Its growth is being accelerated by rising demand for smart labels, wearable devices, and flexible electronics, along with advancements in UV-stable, low-outgassing, and optically clear PSAs formulated with water-based and solvent-free systems that support sustainability goals. In contrast, the solvent-based adhesives segment, remains technically relevant in applications such as footwear, flexible laminates, and specialty automotive components due to its strong adhesion to low-surface-energy substrates and excellent water resistance. Although regulatory pressure is driving a shift toward low-VOC and solvent-free alternatives, solvent-based systems continue to hold meaningful market share in regions with less stringent environmental standards or where performance under humid, high-temperature conditions is prioritized.

The packaging segment holds the leading position in the global adhesives and sealants market, commanding approximately 32% of the total market share in 2025. This dominance is driven by the global boom in e-commerce, FMCG, and flexible packaging industries, which require high-speed bonding, durability, and sustainability. Adhesives are vital for carton sealing, labeling, case forming, and flexible film lamination, ensuring product integrity and visual appeal. Water-based and hot melt adhesives dominate this segment due to their cost efficiency, fast-curing capability, and environmental compliance. As brands increasingly shift toward recyclable and biodegradable packaging materials, adhesive manufacturers are developing bio-based, repulpable, and compostable formulations. The integration of smart packaging technologies—such as tamper-evident seals and RFID-enabled labels—is also expanding adhesive functionality beyond bonding. With consumer packaging innovation accelerating globally, the packaging segment continues to serve as the volume and innovation powerhouse of the adhesives market.

The building and construction segment, holding around 26% of total market share, represents one of the most robust and consistent application areas. Adhesives and sealants are extensively used for flooring, tiling, panel installation, waterproofing, insulation bonding, and structural glazing. Their role in enhancing energy efficiency, acoustic insulation, and weather resistance makes them indispensable to modern architecture. The demand for low-VOC, high-strength, and fire-resistant adhesive systems has surged with the rise of green building certifications (LEED, BREEAM) and urban infrastructure expansion. Silicone and polyurethane-based sealants dominate this space, while water-based and hybrid adhesives are gaining popularity due to their sustainability profile and ease of application. As megacities continue to expand and smart building technologies evolve, the construction sector remains a key revenue pillar for the global adhesives and sealants industry, supported by both renovation cycles and new project developments.

The automotive and transportation sector has become a high-growth pillar of the adhesives and sealants market, relying on advanced bonding technologies to support lightweighting, safety, and the rapid shift to electric mobility, where structural adhesives, thermal conductive materials, and flame-retardant solutions are critical for chassis assembly, battery systems, and vibration control. Sealants further enhance vehicle durability through glass bonding, weatherproofing, and corrosion protection, with automation and environmental regulations accelerating the adoption of reactive and hybrid chemistries. In parallel, the electronics segment continues to advance as a precision-focused, high-performance market in which adhesives enable semiconductor packaging, display assembly, component protection, and thermal management. Rising demand for optically clear adhesives, conductive epoxies, and silicone encapsulants reflects the proliferation of 5G, flexible electronics, EV electronics, and miniaturized devices. With performance and reliability at the core of value creation, this segment remains a leading center of innovation for UV-curable, nano-engineered, and next-generation adhesive technologies.

The competitive landscape of the global adhesives and sealants market is defined by technological leadership, sustainability-driven innovation, and global manufacturing integration. Leading companies are investing in low-VOC materials, carbon-neutral manufacturing, and high-performance bonding systems to meet rising environmental and performance standards. The market is moderately consolidated, with major players such as Henkel, Sika AG, H.B. Fuller, Dow, 3M, and Wacker Chemie AG commanding substantial shares through advanced R&D, vertical integration, and strategic acquisitions.

Henkel AG & Co. KGaA remains the world’s largest adhesive solutions provider, with industry-leading brands like Loctite and Teroson dominating structural bonding, packaging, and consumer adhesive markets. The company expects organic sales growth of 2–4% in fiscal 2025, following €10.97 billion in Adhesive Technologies sales in 2024. Henkel’s innovation strategy centers on digital printing adhesives, sustainable hot-melt technologies, and industrial bonding systems designed for lightweighting and circular economy applications.

Sika AG is a dominant force in specialty construction chemicals, particularly in polyurethane, epoxy, and silicone sealants. The company achieved 1.6% growth in local currencies in H1 2025 and is integrating the MBCC Group with synergy targets set for completion by end of 2026. Sika’s strength lies in roofing, waterproofing, and concrete admixtures, with new plants across China, Singapore, and Central Asia positioning it for long-term growth in emerging construction markets.

H.B. Fuller stands as the largest pure-play adhesive manufacturer, specializing in hot-melt, pressure-sensitive, and structural adhesives for sectors such as electronics, packaging, and medical devices. Targeting an Adjusted EBITDA of $615–630 million for fiscal 2025, the company continues to prioritize portfolio optimization and medical adhesive innovations. In October 2025, it appointed a MedTech industry veteran to its board, strengthening its strategic focus on medical-grade bonding solutions and advanced assembly adhesives.

Dow Inc. is a global materials science powerhouse providing industrial sealants, silicone adhesives, and acrylic systems. The company is investing $1.2 billion in 2024 towards expanding sustainable materials and decarbonization initiatives, targeting a reduction of 5 million metric tons in annual CO₂ emissions by 2030. Its high-performance silicone sealants cater to demanding construction, automotive, and energy applications, reinforcing Dow’s position in carbon-neutral materials innovation.

3M Company leverages its diversified technology portfolio to lead in structural adhesives, VHB™ tapes, and aerospace sealants. With over 450 adhesive and sealant products, 3M continues to drive automotive lightweighting and high-strength bonding solutions. Its water-based adhesion promoters for VHB™ tape enhance sustainability while maintaining performance across aerospace, transport, and electronics sectors—solidifying its leadership in high-performance bonding systems.

Wacker Chemie AG dominates the silicone sealants and specialty chemicals segment, serving the construction, automotive, and electronics industries. The company expects Silicones division sales to grow by 10% in 2025, with total group revenue projected at €6.1–6.4 billion. Wacker’s expertise in high-performance elastomers and polysilicon materials underpins its position as a technological leader in sustainable and long-life sealant systems.

China remains the largest consumer and producer in the Asia-Pacific adhesives and sealants industry, powered by its dominant automotive, construction, and electronics manufacturing base. The country’s strategic focus on lightweight automotive design and Electric Vehicle (EV) production continues to accelerate the adoption of advanced structural adhesives over traditional mechanical fastening methods. With strong policy support under the “Made in China 2025” initiative, local manufacturers are rapidly expanding capacity for high-specification epoxy and polyurethane adhesives, significantly reducing reliance on imported specialty materials.

The electronics sector represents another powerful growth driver. China’s massive consumer electronics and display manufacturing clusters are spurring innovation in conductive adhesives, die-attach materials, and optical clear adhesives (OCAs) used in smartphones, flexible displays, and semiconductors. Simultaneously, the country’s aggressive infrastructure and urbanization drive—including high-speed rail, smart city, and housing megaprojects—is fueling continuous demand for construction sealants, waterproofing membranes, and façade bonding adhesives. The combination of industrial integration, domestic innovation, and government investment cements China’s leadership position as a global manufacturing and export hub for next-generation adhesive technologies.

The United States adhesives and sealants market is advancing through a blend of sustainability mandates, precision engineering, and innovation in specialty chemistry. The Infrastructure Investment and Jobs Act has stimulated broad activity across bridge, tunnel, and commercial building projects, fueling steady demand for hybrid and silicone-based sealants offering superior weatherproofing and durability. The U.S. also leads in bio-based adhesive R&D, as environmental standards such as Green Seal and EPA VOC reduction policies push manufacturers to reformulate toward low-emission and solvent-free adhesives.

The aerospace and defense sectors are major innovation engines, requiring high-performance structural adhesives capable of enduring thermal expansion, vibration, and extreme mechanical loads. Simultaneously, 3D printing and additive manufacturing technologies are opening new frontiers for customizable, high-strength adhesive materials designed for prototyping and end-use parts. As R&D intensity continues to rise, U.S. companies are also strengthening their domestic distribution networks and regional production facilities to mitigate supply chain vulnerabilities. The result is a highly dynamic, innovation-centric market that is reshaping the global standard for bio-based, high-durability adhesive and sealant solutions.

Germany continues to define the European adhesives and sealants landscape, underpinned by world-class automotive engineering and environmental compliance. The EU Green Deal and updated REACH regulatory framework are accelerating the shift from solvent-based to water-borne and hot-melt adhesives, particularly in packaging, furniture, and woodworking industries. Major German chemical companies are spearheading R&D in solvent-free polymer systems, aligning with carbon neutrality goals while maintaining superior performance standards.

The German automotive sector remains the largest single application area, with OEMs and Tier 1 suppliers adopting high-modulus Modified Silane Polymer (SMP) and polyurethane adhesives for multi-material bonding and body-in-white (BIW) assembly. Parallelly, chemical majors such as BASF and Henkel are investing heavily in carbon capture utilization (CCU) to produce sustainable polymer feedstocks for adhesive manufacturing. With precision-driven production, digitalization of coating systems, and strong export capabilities, Germany stands as Europe’s innovation hub for high-performance, low-carbon adhesive technologies.

India’s adhesives and sealants industry is entering a period of explosive expansion, driven by urbanization, infrastructure development, and government-led manufacturing initiatives. Under the ‘Make in India’ campaign, domestic production across automotive, electronics, and packaging sectors is accelerating, fueling demand for industrial-grade adhesives. The ongoing construction boom—encompassing housing, roads, airports, and metro projects—is creating sustained consumption of tile adhesives, flooring compounds, and weather-resistant construction sealants.

The packaging and e-commerce industries are key growth pillars, requiring specialized hot-melt adhesives designed for high-speed automated packaging lines and corrugated box sealing. Additionally, the rise in modular furniture and organized woodworking is driving adoption of polyvinyl acetate (PVA) and hot-melt polyurethane (HMPUR) adhesives for decorative laminates and furniture assembly. Supported by favorable government policy, rising disposable incomes, and expanding export opportunities, India is rapidly positioning itself as a regional adhesives manufacturing and distribution powerhouse across South Asia.

Japan’s adhesives and sealants industry is defined by high-precision manufacturing and continuous R&D leadership in specialty materials. The country’s dominance in electronics and semiconductor assembly drives robust demand for cyanoacrylate, UV-curable, and conductive die-attach adhesives used in microelectronics, displays, and sensors. Japanese manufacturers are renowned for developing low-outgassing, high-purity adhesives tailored for cleanroom and optoelectronic environments.

In the automotive sector, Japan continues to set the benchmark in body-in-white structural adhesives, glazing sealants, and crash-resistant bonding systems. The nation’s leadership in fiber-optic communication infrastructure has also fueled the development of optical fiber bonding materials, supporting the global rollout of 5G and advanced telecom networks. With a strong focus on miniaturization, high-temperature performance, and low environmental impact, Japan remains a global technology leader in high-performance adhesive systems for advanced industrial applications.

South Korea is a global front-runner in display, battery, and electronics adhesive innovation, driven by its leadership in OLED, QLED, and lithium-ion battery manufacturing. The country’s EV expansion is generating unprecedented demand for thermally conductive and flame-retardant structural adhesives, critical for battery pack bonding, module assembly, and safety insulation.

In parallel, the display industry’s evolution toward flexible and foldable screens is spurring intensive R&D into optically clear adhesives (OCAs) and pressure-sensitive adhesives (PSAs) optimized for high-clarity, bendable surfaces. Government-backed funding for semiconductor and materials innovation continues to strengthen the domestic supply of epoxy-based die-attach and encapsulation adhesives for microelectronics and high-performance chip packaging. With sustained investments in material science and automation, South Korea is cementing its position as a global hub for next-generation adhesive technology across EV, display, and semiconductor ecosystems.

Brazil remains the largest adhesives and sealants market in Latin America, supported by robust construction activity, automotive assembly, and growing packaging demand. The country’s residential and commercial construction boom continues to sustain high consumption of acrylic, silicone, and polyurethane sealants, particularly for waterproofing, joint sealing, and façade applications.

The automotive and aftermarket sectors are key consumers of polyurethane and epoxy adhesives, supporting vehicle assembly, maintenance, and part replacement. Meanwhile, the flexible packaging and food processing industries are accelerating demand for lamination adhesives and food-safe bonding formulations. Increasing emphasis on local manufacturing and supply chain self-reliance is attracting global chemical players to establish production partnerships in Brazil, positioning it as the regional adhesives manufacturing and distribution hub for Latin America’s growing industrial base.

Adhesives and Sealants Market Report Scope

Adhesives and Sealants Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$78.1 Billion

|

|

Market Size (2034)

|

$108.4 Billion

|

|

Market Growth Rate

|

3.7%

|

|

Segments

|

By Technology (Water-Based Adhesives, Solvent-Based Adhesives, Hot Melt Adhesives, Reactive Adhesives, Pressure-Sensitive Adhesives (PSAs)), By Adhesives Resin (Acrylic, Polyurethane (PU), Epoxy, Vinyl Acetate Emulsion (VAE)/EVA, Styrenic Block Copolymers (SBC), Silicone, Natural/Bio-based), By Adhesives Application (Packaging, Building & Construction, Automotive & Transportation, Woodworking & Furniture, Electronics, Medical, Consumer/DIY), By Sealants Resin Type (Silicone, Polyurethane (PU), Hybrid (MS Polymer/SMP), Acrylic, Polysulfide, Butyl), By Sealants Application (Building & Construction, Automotive & Transportation, Industrial Assembly, Consumer/DIY

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Henkel AG & Co. KGaA, Sika AG, H.B. Fuller Company, 3M Company, Arkema S.A. (Bostik), The Dow Chemical Company, Wacker Chemie AG, Huntsman Corporation, Avery Dennison Corporation, RPM International Inc., Ashland Global Holdings Inc., Lord Corporation, Pidilite Industries Ltd., DuPont de Nemours, Inc., BASF SE

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

By Technology

- Water-Based Adhesives

- Solvent-Based Adhesives

- Hot Melt Adhesives

- Reactive Adhesives

- Pressure-Sensitive Adhesives (PSAs)

By Adhesives Resin

- Acrylic

- Polyurethane (PU)

- Epoxy

- Vinyl Acetate Emulsion (VAE)/EVA

- Styrenic Block Copolymers (SBC)

- Silicone

- Natural/Bio-based

By Adhesives End-Use Industry

- Packaging

- Building & Construction

- Automotive & Transportation

- Woodworking & Furniture

- Electronics

- Medical

- Consumer/DIY

By Sealants Resin Type

- Silicone

- Polyurethane (PU)

- Hybrid (MS Polymer/SMP)

- Acrylic

- Polysulfide

- Butyl

By Sealants End-Use Industry

- Building & Construction

- Automotive & Transportation

- Industrial Assembly

- Consumer/DIY

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

- Henkel AG & Co. KGaA

- Sika AG

- H.B. Fuller Company

- 3M Company

- Arkema S.A. (Bostik)

- The Dow Chemical Company

- Wacker Chemie AG

- Huntsman Corporation

- Avery Dennison Corporation

- RPM International Inc.

- Ashland Global Holdings Inc.

- Lord Corporation

- Pidilite Industries Ltd.

- DuPont de Nemours, Inc.

- BASF SE

*- List not Exhaustive

Research Coverage

This report investigates how sustainability mandates, electrification, and high-throughput packaging are reshaping the global adhesives and sealants landscape, quantifying profit pools across chemistries and applications while mapping regulatory, cost, and technology inflection points. Produced by USDAnalytics, the study’s analysis reviews decarbonized feedstocks, water-borne platforms, smart/debondable systems, and automation-ready dispensing as adoption catalysts; it surfaces breakthroughs in bio-circular hot melts, reactive hybrids, and repairability-focused designs, and highlights supply-side moves (expansions, portfolio realignments) that alter regional competitiveness. With risk-tested scenarios to 2034 and decision tools for pricing, sourcing, and specification control, this report is an essential resource for executives and engineers seeking durable performance, lower embodied carbon, and recyclable end-states without sacrificing throughput or total cost.

Scope Highlights

- By Technology: Water-Based; Solvent-Based; Hot Melt; Reactive; Pressure-Sensitive (PSA).

- By Adhesives Resin: Acrylic; Polyurethane (PU); Epoxy; VAE/EVA; SBC; Silicone; Natural/Bio-based.

- By Adhesives End-Use: Packaging; Building & Construction; Automotive & Transportation; Woodworking & Furniture; Electronics; Medical; Consumer/DIY.

- By Sealants Resin: Silicone; Polyurethane (PU); Hybrid (MS Polymer/SMP); Acrylic; Polysulfide; Butyl.

- By Sealants End-Use: Building & Construction; Automotive & Transportation; Industrial Assembly; Consumer/DIY.

- Geographic Scope: Analysis spans 25+ countries across North America, Europe, Asia Pacific, Latin America, the Middle East & Africa.

- Timeframe: Historic 2021–2024 and Forecast 2025–2034.

- Companies: 15+ company analyses/profiles.

Deliverables

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.