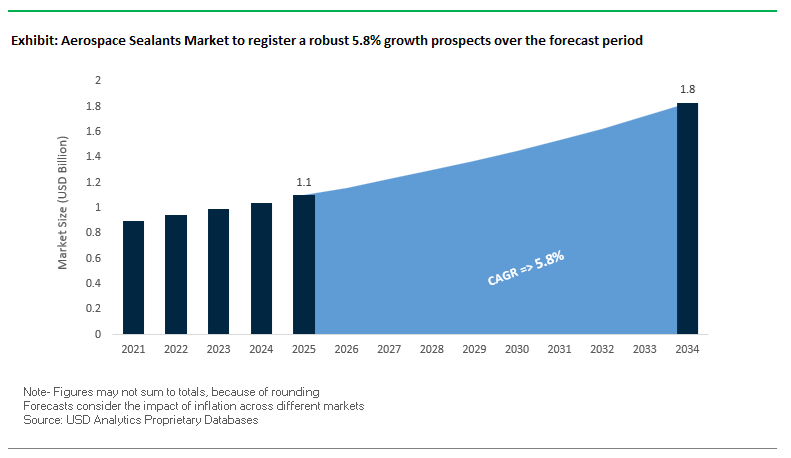

The global aerospace sealants market is projected to grow from $1.1 billion in 2025 to $1.8 billion by 2034, registering a CAGR of 5.8%. The global aerospace sealants market is projected to expand from USD 1.1 billion in 2025 to USD 1.8 billion by 2034, registering a 5.8% CAGR, as aircraft manufacturers and MRO operators intensify their focus on fuel system integrity, long-life airframe sealing, and weight-optimized materials. Aerospace sealants are no longer auxiliary consumables; they are mission-critical materials engineered to ensure leak-free fuel tanks, pressure-resistant fuselage joints, corrosion protection, and environmental sealing across the entire aircraft lifecycle. Leading manufacturers such as PPG Aerospace, Henkel, 3M, H.B. Fuller (Kömmerling), and Parker LORD position sealants as integral to structural reliability rather than maintenance afterthoughts.

Growth is anchored in the continued dominance of polysulfide and polythioether sealants, which remain the industry standard for fuel tank sealing due to their proven resistance to aviation fuels, hydraulic fluids, microbial growth, and cyclic thermal stress. Manufacturer technical data emphasizes compliance with SAE AMS-S-8802 (Rev F) and related specifications requiring reliable performance across −54 °C to +121 °C, with validated service lives exceeding 25,000 flight cycles or 30 years. These performance thresholds directly support airframe life-extension programs pursued by both commercial airlines and defense operators seeking to defer capital expenditure on fleet replacement.

A defining shift in the market is the acceleration of low-density and lightweight sealant formulations, where suppliers are engineering materials that deliver 3–4 lb/gal weight reduction without sacrificing elongation, adhesion, or fuel resistance. OEMs increasingly quantify sealant mass at the aircraft level, as even incremental weight savings translate into measurable fuel burn reduction and CO₂ emissions improvement over long service horizons. In parallel, manufacturers are phasing out chromated systems in favor of chromate-free, low-VOC sealants, responding to REACH compliance, worker safety mandates, and airline sustainability targets.

Operational efficiency is another core growth driver. Rapid-cure aerospace sealants offering tack-free times of 3–6 hours are standard offerings from major suppliers, enabling faster AOG recovery and line-maintenance turnaround without compromising adhesion or chemical resistance. To support process consistency, manufacturers continue to invest in pre-mixed and frozen (PMF) sealants, Semkit® cartridge systems, and controlled-thaw logistics, reducing application variability, material waste, and rework across both OEM assembly lines and global MRO networks.

The global aerospace sealants industry is witnessing a wave of strategic partnerships, product launches, and regulatory reforms, reshaping the competitive and technological landscape. In September 2025, BASF’s Chemetall division and Azelis expanded their distribution partnership to cover Southeast Asia, including the Philippines and Thailand, for the supply of Naftoseal® polysulfide sealants and related surface treatment technologies. This move reflects the increasing regional demand for integral fuel tank sealing systems in the fast-growing Asia-Pacific aerospace market.

In June 2025, PPG Aerospace introduced a polythioether sealant system tailored for next-generation composite bonding applications, offering a non-chromated, low-VOC, and rapid-cure alternative to traditional polysulfide systems. The innovation meets rising environmental regulations while providing high elongation and superior fuel resistance — features essential for composite aircraft fuselage and wing structures. Similarly, in May 2025, 3M Aerospace announced a major product development initiative around its low-density, manganese dioxide cure sealants (AC-380 family), emphasizing fuel resistance, weight savings, and faster application times to support OEMs’ production efficiency targets.

The regulatory landscape evolved significantly in January 2026, when a joint EASA–FAA advisory circular proposed enhanced guidelines for the use of chrome-free corrosion-inhibitive sealants in MRO operations. This update underscores the aerospace industry’s shift toward sustainable chemistry and worker safety compliance, impacting formulations used in legacy aircraft maintenance. Earlier, in March 2025, Henkel Aerospace expanded its footprint by acquiring a European polyurethane sealant manufacturer, broadening its presence in interior sealing and non-structural applications — a strategic move aligning with the company’s sustainable materials roadmap.

The innovation pipeline remains robust across the value chain. In October 2025, a multi-institutional academic consortium announced a breakthrough fluorosilicone sealant formulation capable of maintaining elasticity down to −75°C, opening new possibilities for high-altitude and space-adjacent aerospace applications. Meanwhile, PPG Aerospace continued its expansion momentum by opening a new Application Support Center (ASC) in the Middle East (November 2025), dedicated to servicing regional MRO fleets with PRC® pre-mixed and frozen (PMF) sealants. Additionally, in April 2025, a major sealant packaging partner invested $20 million to expand clean-room facilities for Semkit® cartridge preparation, ensuring uninterrupted supply for high-rate aircraft production programs.

The evolution of propulsion technology—ranging from ultra-efficient high-bypass turbofan engines to Sustainable Aviation Fuel (SAF) and hydrogen-powered concepts—is redefining performance thresholds for aerospace sealants. These systems operate under elevated pressures and temperatures, demanding fuel-resistant, high-temperature sealing solutions capable of maintaining elasticity and adhesion under extreme stress conditions.

Recent advancements, such as PPG’s PR-1770® Class A high-temperature fuel tank sealant, exemplify the technological leap. The formulation withstands temperatures up to +180°C (356°F) while resisting degradation from phosphate ester hydraulic fluids—a key requirement for next-generation nacelles and fuel tanks. The innovation drives the strategic shift toward high-performance polysulfide and polythioether chemistries, optimized for compatibility with hotter-running propulsion systems.

A critical factor accelerating the transition is the chemical composition of Sustainable Aviation Fuels (SAFs). Unlike conventional Jet A fuels, which contain approximately 17% aromatics by volume, many SAF formulations such as HEFA and ATJ are completely aromatic-free. The lack of aromatics affects the elastomer swelling behavior in nitrile O-rings and sealants, creating a compatibility gap that can lead to fuel leakage and premature seal failure. Consequently, OEMs and sealant producers are investing heavily in next-generation elastomeric and polysulfide sealants designed for stable performance in low-aromatic fuel environments.

These advancements are not limited to fuel systems alone; they extend across engine nacelles, hydraulic systems, and propulsion interfaces, where thermal cycling and chemical exposure create complex design challenges. The result is a clear market trajectory toward multifunctional aerospace sealants engineered to provide chemical inertness, temperature resilience, and longevity in SAF and hydrogen propulsion environments.

Aircraft manufacturers and operators continue to prioritize fuel efficiency and weight reduction, making low-density aerospace sealants a cornerstone of sustainable aviation design. Every kilogram saved contributes to measurable efficiency gains—translating into lower operational costs, extended range, and reduced carbon emissions.

Innovative products such as PPG’s PR-1782® Class B Low Density sealant demonstrate up to 30% weight reduction per unit volume compared to traditional formulations, while maintaining the necessary adhesion and flexibility for fuselage and structural fillet sealing. Similarly, 3M’s AC-770 low-density polysulfide sealant family achieves a 25% density reduction, weighing 3–4 lbs. less per gallon than standard alternatives—critical for large-scale airframe applications consuming thousands of gallons per aircraft program.

The measurable weight saving has a profound impact: in a single wide-body aircraft, substituting standard sealants with lightweight versions can result in hundreds of kilograms of mass reduction, directly contributing to lower fuel burn and reduced lifecycle CO₂ emissions.

In addition, the industry is increasingly pairing lightweight sealants with automated robotic dispensing systems for precision application, reducing waste and enhancing bond uniformity. The convergence of material innovation and automation establishes a competitive differentiation for manufacturers supplying next-generation eco-efficient sealants to Airbus, Boeing, and regional jet OEMs.

As the aviation industry pivots toward hydrogen-powered propulsion as a key zero-emission strategy, the demand for cryogenic sealing solutions represents a transformative opportunity. Hydrogen’s physical properties—extremely low temperature and molecular diffusivity—make conventional rubber-elastic sealing solutions ineffective. New materials must endure cryogenic temperatures near −253°C (−423°F) while maintaining gas-tight integrity under pressure cycling and vibration.

Companies like Parker Prädifa are pioneering PTFE and resilient metallic seals (e.g., C-rings) for liquid hydrogen storage systems, establishing a foundation for cryogenic sealing standards in aerospace applications. These materials provide low-temperature flexibility and glass-hard embrittlement resistance, critical to prevent catastrophic leaks or hydrogen embrittlement in aircraft fuel systems.

In addition, hydrogen’s natural permeability through polymer matrices remains a technical barrier to commercialization. Academic studies (2025) on polymeric hydrogen tanks (Type IV and V) highlight that even defect-free composites experience steady-state hydrogen permeation, posing serious safety and efficiency risks. Consequently, next-generation aerospace cryogenic sealants must not only resist extreme temperatures but also minimize hydrogen diffusion through novel barrier coatings or nanocomposite formulations.

The hydrogen economy’s projected growth—bolstered by initiatives like Airbus ZEROe—signals a once-in-a-generation opportunity for material suppliers to capture an emerging high-value niche. The race to develop certified ultra-low-permeation hydrogen sealants for cryogenic fuel systems could redefine the competitive landscape of aerospace materials over the next decade.

The Maintenance, Repair, and Overhaul (MRO) segment is emerging as a consistent and resilient revenue driver for the aerospace sealants market. Global commercial fleet aging and supply chain delays in new aircraft deliveries have extended the operational lifecycles of existing aircraft, leading to a surge in structural maintenance and resealing requirements.

According to Oliver Wyman, the average fleet age has climbed to 13.4 years, up from 12.1 years in the prior year, while annual flight hours are projected to exceed 112 million by 2035. The “super-cycle” in MRO activity is fueling heightened consumption of certified repair-grade sealants for fuel tank resealing, fuselage joints, and pressurized cabin areas.

Sealants designed for the MRO sector—such as quick-cure polysulfides and elastomeric repair compounds—enable faster turnaround during heavy maintenance checks. Additionally, the increasing use of automation and pre-mixed cartridge systems in hangars is improving sealant consistency and reducing application time, addressing the industry’s growing demand for time-efficient repair materials.

Airframe MRO, in particular, represents a core area of aftermarket consumption. The structural resealing of wings, fuselages, and pressure bulkheads remains integral to corrosion prevention and fatigue mitigation, ensuring regulatory compliance with airworthiness directives. As airlines extend fleet lifespans while awaiting new-generation aircraft, demand for MRO-focused sealants will continue to rise—creating a stable, counter-cyclical revenue stream for manufacturers and distributors.

Aerospace Sealants Market Share Insights, 2025-2034

The liquid and paste sealants segment dominates the global aerospace sealants industry, commanding approximately 70% of the total market share in 2025. This dominance is attributed to their exceptional versatility, adaptability, and proven performance across a wide range of applications—from fuel tanks and fuselage joints to pressurized cabin seams and engine nacelles. Liquid and paste formulations, typically based on polysulfide, silicone, and polyurethane chemistries, are the industry’s cornerstone for both OEM assembly lines and MRO operations. Their ability to conform to complex geometries, irregular surfaces, and large bonding areas makes them indispensable for structural and non-structural sealing tasks. Furthermore, these sealants are available in multiple application formats—brushable, extrudable, and sprayable grades—offering flexibility in both manual and automated production environments. In the aerospace sector, liquid/paste sealants are crucial for maintaining aircraft integrity, preventing corrosion, ensuring fuel containment, and reducing aerodynamic drag. The segment’s growth is further driven by the introduction of low-density, chromate-free, and fast-curing sealant formulations that align with sustainability regulations such as REACH, EPA, and FAA environmental standards. As aircraft become increasingly composite-intensive, liquid and paste sealants will remain the backbone of critical bonding and corrosion protection systems, securing their leadership in the global aerospace sealants market.

The tapes and pre-formed seals segment represents a significant and growing niche within the aerospace sealants market, driven by the aerospace industry’s shift toward automation, repeatability, and reduced assembly time. Pre-formed sealants and sealant tapes are indispensable for access panels, avionics bays, door frames, and quick-seal applications, where precision, uniform thickness, and clean installation are paramount. These products enhance manufacturing consistency, particularly in high-throughput OEM production lines, by reducing the variability associated with manual sealant application. Materials like fluoroelastomers, silicone elastomers, and polyurethane foams dominate this segment for their thermal resistance, flexibility, and long-term sealing reliability. Moreover, pre-formed seals are designed to ensure rapid installation and re-sealing during MRO operations, which significantly reduces aircraft downtime and maintenance costs. With advancements in custom-molded and extruded gasket technologies, this segment is expanding into pressurization systems, environmental control ducts, and vibration-damping interfaces. While it remains smaller than liquid/paste sealants by volume, its precision-oriented performance and efficiency advantages make it an essential component of the modern aerospace manufacturing ecosystem.

The film and adhesive sealants segment occupies a high-value position in the aerospace market, reflecting its critical role in composite and hybrid structural assemblies. These sealants combine the properties of both adhesives and sealants, enabling continuous, void-free bonds that provide structural strength, environmental protection, and vibration resistance in one layer. They are extensively used in wing and fuselage assemblies, where metal-to-composite and composite-to-composite joints demand exceptional fatigue resistance and long-term sealing integrity. Epoxy-based film sealants are particularly favored for their chemical stability, durability, and compatibility with autoclave and out-of-autoclave (OOA) curing processes. Their precise thickness and clean application make them ideal for automated production environments in which quality assurance and weight consistency are paramount. The growing adoption of lightweight airframe architectures, electric propulsion systems, and carbon-fiber components has elevated demand for these advanced sealing materials. As the aerospace industry continues to move toward integrated structural bonding and multifunctional materials, film and adhesive sealants are expected to capture increasing value share due to their efficiency, reliability, and role in enhancing aerodynamic performance.

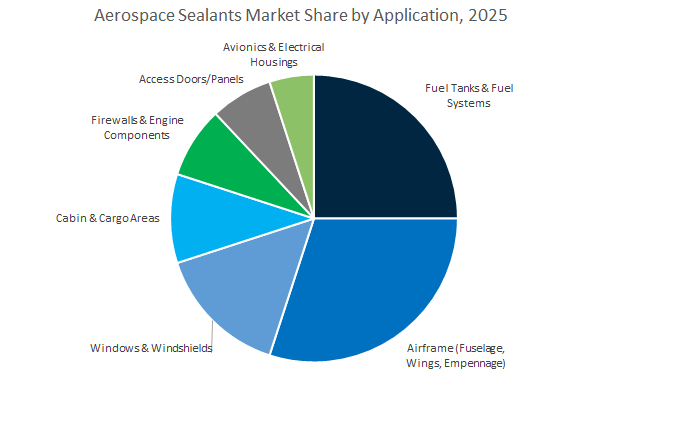

The airframe segment, encompassing fuselage, wings, and empennage assemblies, leads the global aerospace sealants industry with an estimated 30% market share in 2025. This dominance stems from the sheer scale and complexity of the airframe structure, where sealants play a crucial role in corrosion prevention, aerodynamic smoothing, and pressurization. Aerospace-grade sealants are applied along panel joints, lap seams, rivets, and fastener lines to prevent moisture ingress and ensure long-term structural integrity. The segment’s growth is being fueled by the rise of composite airframes—as seen in aircraft like the Boeing 787 and Airbus A350—which require sealants with enhanced flexibility, UV resistance, and chemical compatibility to bond dissimilar materials. Moreover, OEMs are increasingly adopting robotic sealant dispensing systems for precise, repeatable application across large structures, improving both quality and efficiency. Airframe sealants, particularly polysulfide and polyurethane formulations, remain indispensable for maintaining airworthiness, reducing drag, and extending aircraft lifespan, cementing this segment as the backbone of the aerospace sealant market.

The fuel tanks and fuel systems segment, contributing roughly 25% of global market share, represents the most safety-critical and performance-demanding application area for aerospace sealants. These environments require materials capable of withstanding continuous fuel immersion, extreme temperature shifts, and pressure fluctuations. Polysulfide-based sealants dominate this segment due to their exceptional fuel resistance, flexibility, and ability to maintain airtight integrity under stress. They are extensively used in wing fuel tanks, fuselage fuel bays, and integral tank joints to prevent fuel leaks and resist degradation from jet fuels, hydraulic fluids, and de-icing agents. Moreover, low-density, fast-curing variants have gained popularity for reducing weight and improving production efficiency. As modern aircraft designs prioritize fuel efficiency and extended operational range, the demand for next-generation, environmentally compliant fuel tank sealants continues to rise. The integration of self-healing and corrosion-inhibiting technologies in advanced sealant formulations further underscores their importance in ensuring aircraft safety and operational reliability.

The windows and windshields segment represents a specialized, high-value niche within the aerospace sealants market, driven by its stringent optical clarity, adhesion, and environmental durability requirements. Sealants in this category must maintain flexibility and transparency while withstanding UV radiation, temperature fluctuations, and pressurization cycles. Silicone-based and polyurethane sealants dominate due to their elasticity, weather resistance, and strong adhesion to glass, polycarbonate, and metal substrates. In addition to maintaining structural integrity, these sealants play a crucial role in reducing cabin noise and vibration. The ongoing innovation in anti-fog, UV-stable, and low-outgassing formulations has further elevated their role in enhancing passenger comfort and flight safety. As modern aircraft designs incorporate larger panoramic windows and cockpit transparency systems, this segment is poised for continuous growth in both OEM and MRO applications.

The cabin, cargo, and access door applications form a vital segment emphasizing operational safety, passenger comfort, and maintenance efficiency. Cabin sealants are used extensively for pressurization, moisture control, and noise insulation, particularly in joints, seams, and floor structures. Cargo bay and access door sealants—often in tape or pre-formed gasket form—ensure quick installation, re-sealability, and long-term flexibility under repeated mechanical stress. These materials are also critical for preventing corrosion, fluid ingress, and structural fatigue over the aircraft’s operational lifespan. The segment’s expansion is driven by fleet modernization and cabin refurbishment programs, where interior sealing plays a major role in extending aircraft service life.

The aerospace sealants competitive landscape is characterized by the dominance of globally certified manufacturers that combine chemical innovation, regulatory compliance, and process automation. Leading companies such as PPG Industries, 3M, Henkel, BASF (Chemetall), Solvay, and Socomore (Flamemaster) are advancing the performance boundaries of polysulfide, polyurethane, and fluorosilicone chemistries, driving safer, lighter, and more sustainable aerospace sealing solutions.

PPG Aerospace continues to lead the aerospace sealants market through its PRC® and Proseal™ brands, delivering certified solutions for fuel tank integrity and aerodynamic sealing. The company’s product range complies with MIL-SPEC and SAE AMS standards, including the widely used P/S 890® Class A formulations. PPG’s ARE™ 3D-printed sealants have revolutionized the application process by reducing manual labor in complex geometries, while its low-density polysulfide and polythioether sealants improve weight efficiency. The company’s Semkit® and PMF cartridges support MRO and OEM users in minimizing waste and ensuring consistent application during aircraft assembly and repair.

3M Aerospace maintains a strong presence across structural and non-structural sealing applications, supplying AC-380 and AC-770 polysulfide sealants known for superior chemical resistance and flexibility. The company’s latest low-density sealants deliver significant weight reduction without compromising fuel resistance or adhesion strength, aligning with aircraft OEM lightweighting targets. Its adhesion promoters (AC-160) and specialty repair pastes enable rapid MRO operations. Leveraging global materials science capabilities, 3M integrates adhesives, fillers, and surface treatments into a cohesive system supporting the entire aircraft assembly and maintenance lifecycle.

Henkel Aerospace has built a reputation for innovation through its Loctite® and Bonderite® technologies, offering polyurethane and epoxy-based sealant systems for both structural and non-structural aerospace applications. The company’s recent acquisition of a European polyurethane sealant manufacturer enhances its capabilities in interior sealing and vibration damping solutions. Henkel’s focus on low-VOC and solvent-free formulations aligns with emerging global sustainability mandates. Its products are widely used for engine area sealing, heat-resistant bonding, and fuel system applications, where mechanical strength and fatigue resistance are critical.

BASF’s Chemetall division commands a leading position in fuel tank and fuselage sealing with its Naftoseal® line of polysulfide and polythioether sealants, certified by all major aircraft OEMs. The company integrates surface treatment technologies (Ardrox®) with its sealing portfolio to ensure optimal adhesion and corrosion protection. Recent innovations include pre-cast sealing solutions such as Naftoseal® seal caps, which reduce manual variability and assembly time. The 2025 expansion into Southeast Asia with Azelis further strengthens Chemetall’s technical service network and distribution footprint across emerging aerospace hubs.

Solvay continues to push the boundaries of polymer science with specialty polyimide and high-Tg epoxy-based sealants that operate in extreme environments. The company’s solutions cater to primary and secondary aircraft structures, including antenna radomes and electronic housings where dielectric performance is crucial. Solvay’s materials integrate seamlessly with its FM® adhesive film range, ensuring comprehensive composite protection. Its strategic focus on lightweight, high-temperature, and low-outgassing sealants positions Solvay as a technology partner for next-generation aerospace and defense systems.

Socomore, through its Flamemaster brand, specializes in fire-retardant and thermal protection sealants for both civil and military aircraft. Its CS 3205 polysulfide formulations meet FAR 25.853 and MIL-S-8802 specifications, providing exceptional resistance to fire, fuel, and hydraulic fluids. The company’s strong presence in defense aviation stems from its MIL-SPEC-qualified sealants designed for fuel tank repair and high-temperature engine applications. Socomore is actively developing low-toxicity, easy-to-apply sealants that reduce rework time and improve environmental compliance for global OEMs and MRO operators.

The United States aerospace sealants market remains a global leader, supported by major manufacturing investments, strict regulatory oversight, and high-volume OEM demand. In October 2025, PPG Industries announced a $380 million investment to construct a 198,000-square-foot aerospace coatings and sealants plant in Shelby, North Carolina, a move designed to increase domestic capacity and ensure secure supply for both commercial and defense aircraft manufacturers.

The U.S. Environmental Protection Agency’s (EPA) 2025 amendments to National VOC Emission Standards are prompting a sector-wide shift toward low-reactivity, low-VOC polysulfide and polythioether sealant formulations, particularly for aircraft exteriors, fuel tanks, and touch-up applications. Aerospace OEMs, including Boeing and Lockheed Martin, are ramping up sealant procurement as they scale production of next-generation commercial and military platforms.

R&D is intensely focused on fast-curing, robot-compatible sealants that minimize MRO turnaround time and enhance operational efficiency. The emergence of firewall and high-temperature aerospace sealants tailored for hypersonic and advanced defense programs marks a new technological frontier. Furthermore, material science innovation is prioritizing sealant adhesion optimization for composite airframes, ensuring compatibility with new lightweight substrates used in modern aircraft structures.

China’s aerospace sealants industry is witnessing accelerated development as the government enforces stricter environmental standards and supports local manufacturing self-sufficiency. The GB 30981.2-2025 regulation (effective June 2026) mirrors international VOC restrictions, compelling domestic producers to transition toward eco-friendly, solvent-free aerospace sealants.

Massive state-backed investments and joint ventures are expanding production capabilities for aviation-grade polysulfide and silicone sealants, ensuring supply to the country’s major programs like COMAC C919 and regional jet manufacturing initiatives. Additionally, the growth of MRO infrastructure across China is stimulating demand for certified line-repair sealants used in cabin maintenance and structural repair operations.

R&D efforts are intensifying around rapid-cure polythioether formulations with extended shelf life, reducing assembly time and improving productivity. Simultaneously, the government’s self-reliance strategy for aerospace materials is encouraging the indigenous development of high-specification elastomers, minimizing import dependency while meeting international certification benchmarks.

Germany stands as the European epicenter for aerospace sealant innovation, leveraging its engineering precision and environmental leadership to develop next-generation formulations. Major companies such as Henkel AG & Co. KGaA are spearheading R&D into non-chrome and low-VOC aerospace sealants compliant with EU REACH and EASA regulations, maintaining performance integrity in harsh aerospace environments.

The nation’s deep OEM-supplier integration, especially with Airbus, is accelerating the deployment of automated sealant application systems for fuselage joint sealing. The shift enables high-volume, consistent application with minimal material waste. German research institutes are further developing solvent-free and bio-based polyurethane sealants designed for cabin interiors and pressurized window sealing.

Public and private R&D funding continues to drive thermal stability and fire-resistant sealant advancements, particularly for military aircraft operating in high-stress environments. Germany’s technology ecosystem positions it as a global leader in sustainable aerospace sealing solutions aligned with Europe’s carbon neutrality goals.

The United Kingdom aerospace sealants market is rapidly evolving with strong defense sector demand, innovative composite bonding research, and advanced MRO applications. Ongoing defense programs, such as the Tempest Future Combat Air System (FCAS), are driving demand for stealth-compatible, high-durability sealants capable of maintaining structural integrity under extreme operational stress.

The UK’s established MRO hub status supports high-volume consumption of line-repair aerospace sealant kits used across civil and military fleets. Local R&D partnerships between universities and sealant manufacturers are pioneering composite-compatible bonding systems that maintain long-term adhesion between dissimilar materials like carbon fiber, titanium, and thermoplastics.

The nation is also exploring 3D-printable, curable sealant materials for use in additive manufacturing-based repair of non-critical components—a cutting-edge development in maintenance efficiency. Compliance with EASA REACH chemical standards continues to reshape the formulation of existing aerospace sealants toward non-restricted, environmentally responsible chemicals, ensuring both regulatory and operational excellence.

France remains a strategic leader in European aerospace sealant production, deeply tied to Airbus assembly lines and Europe’s expanding defense sector. French manufacturers are prioritizing high-volume, FST-compliant aerospace sealants for wing box sealing, fuselage joints, and fuel containment systems.

Local R&D is intensely focused on rapid-curing polythioether sealants that minimize assembly cycle times while maintaining strong fuel and hydraulic fluid resistance. Moreover, manufacturers are certifying sealant formulations for extreme cold performance and high-altitude stability, ensuring reliability in long-haul commercial and military aircraft.

To mitigate supply chain disruptions, France is securing local production of key precursors such as polysulfide polymers, strengthening resilience against global raw material volatility. In parallel, investments in automated sealing systems for Airbus fuselage manufacturing are streamlining efficiency and precision. A growing innovation focus is on developing SAF (Sustainable Aviation Fuel)-resistant sealants, ensuring long-term performance as aviation transitions to greener fuels.

India’s aerospace sealants market is expanding rapidly under the government’s Aatmanirbhar Bharat (Self-Reliant India) initiative, emphasizing domestic production of certified materials for both civil and defense aviation programs. Increased procurement under HAL’s indigenous fighter and transport aircraft projects has spurred R&D into certified polysulfide and polyurethane aerospace sealants designed for tropical and high-humidity environments.

International investments, such as Sika’s new Pune facility (2025), though primarily automotive-focused, underscore the region’s growing role in specialty sealant production with potential aerospace diversification. Concurrently, rising foreign direct investment in MRO facilities across India is boosting consumption of certified sealant kits for line maintenance and repair operations.

Local producers are pursuing technology transfer partnerships to meet international FAR/EASA certification standards, focusing on long-life, fuel-resistant formulations. The country’s surging domestic air travel, combined with government-backed manufacturing incentives, positions India as an emerging hub for localized aerospace sealant production and maintenance innovation.

Aerospace Sealants Market Report Scope

Aerospace Sealants Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$1.1 Billion

|

|

Market Size (2034)

|

$1.8 Billion

|

|

Market Growth Rate

|

5.8%

|

|

Segments

|

By Chemical Type (Polysulfide Sealants, Polythioether Sealants, Silicone Sealants, Polyurethane Sealants, Fluorosilicone Sealants, Epoxy-based Sealants, Others), By Product Form (Liquid/Paste, Tapes & Pre-formed Seals, Film/Adhesive Sealants), By Aircraft Type (Commercial Aircraft, Military Aircraft, General Aviation, Helicopters), By Technology (Solvent-based Sealants, Water-based Sealants, Two-Component Sealants, UV/Light-Curable Sealants, Non-curing Compounds), By Application (Fuel Tanks & Fuel Systems, Airframe, Windows & Windshields, Firewalls & Engine Components, Avionics & Electrical Housings, Cabin & Cargo Areas, Access Doors/Panels), By End-User (OEM, MRO, Aftermarket

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

PPG Industries Inc., Henkel AG & Co. KGaA, 3M Company, H.B. Fuller Company, Sika AG, Arkema Group, Solvay S.A., Flamemaster Corporation, Master Bond Inc., Momentive Performance Materials Inc., W. L. Gore & Associates, Inc., Permabond LLC, Royal Adhesives & Sealants, LLC, DELO Industrial Adhesives, Dow Inc.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

By Chemical Type

- Polysulfide Sealants

- Polythioether Sealants

- Silicone Sealants

- Polyurethane Sealants

- Fluorosilicone Sealants

- Epoxy-based Sealants

- Others

By Product Form

- Liquid/Paste

- Tapes & Pre-formed Seals

- Film/Adhesive Sealants

By Aircraft Type

- Commercial Aircraft

- Military Aircraft

- General Aviation

- Helicopters

By Technology/Cure

- Solvent-based Sealants

- Water-based Sealants

- Two-Component Sealants

- UV/Light-Curable Sealants

- Non-curing Compounds

By Application

- Fuel Tanks & Fuel Systems

- Airframe

- Windows & Windshields

- Firewalls & Engine Components

- Avionics & Electrical Housings

- Cabin & Cargo Areas

- Access Doors/Panels

By End-User

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

- PPG Industries Inc.

- Henkel AG & Co. KGaA

- 3M Company

- H.B. Fuller Company

- Sika AG

- Arkema Group

- Solvay S.A.

- Flamemaster Corporation

- Master Bond Inc.

- Momentive Performance Materials Inc.

- W. L. Gore & Associates, Inc.

- Permabond LLC

- Royal Adhesives & Sealants, LLC

- DELO Industrial Adhesives

- Dow Inc.

*- List not Exhaustive

Research Coverage

Prepared by USDAnalytics, this report investigates the global Aerospace Sealants market across chemistries, cure technologies, aircraft programs, and applications; our analysis reviews qualification pathways (SAE AMS, MIL, OEM specs), lifecycle performance under thermal/pressure cycling, SAF compatibility, and weight-saving formulations, and highlights rapid-cure, low-density, and chromate-free innovations enabling faster MTAT and lower CO₂. We benchmark leaders on certification breadth, supply resilience, and automation readiness, map MRO versus OEM pull, and size spend by airframe and fuel systems through 2034. Capturing regulatory shifts (VOC/PFAS), packaging advances (PMF/Semkit®), and regional capacity build-outs, this report is an essential resource for materials, maintenance, and procurement teams seeking measurable gains in reliability and throughput. Technical and commercial breakthroughs—from high-temperature fuel-resistant polysulfides/polythioethers to cryogenic-ready solutions—are quantified against fleet age, delivery backlogs, and retrofit cycles to support de-risked sourcing and specification decisions.

Scope Includes

- By Chemical Type: Polysulfide Sealants; Polythioether Sealants; Silicone Sealants; Polyurethane Sealants; Fluorosilicone Sealants; Epoxy-based Sealants; Others

- By Product Form: Liquid/Paste; Tapes & Pre-formed Seals; Film/Adhesive Sealants

- By Aircraft Type: Commercial Aircraft; Military Aircraft; General Aviation; Helicopters

- By Technology/Cure: Solvent-based; Water-based; Two-Component; UV/Light-Curable; Non-curing Compounds

- By Application: Fuel Tanks & Fuel Systems; Airframe; Windows & Windshields; Firewalls & Engine Components; Avionics & Electrical Housings; Cabin & Cargo Areas; Access Doors/Panels

- By End-User: OEM; MRO; Aftermarket

- Geographic Scope: Analysis spans 25+ countries across North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa.

- Time Horizon: Historic 2021–2024 and Forecast 2025–2034.

- Companies: 15+ company analysis/profiles with product coverage, certifications, and strategies.

Deliverables

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.