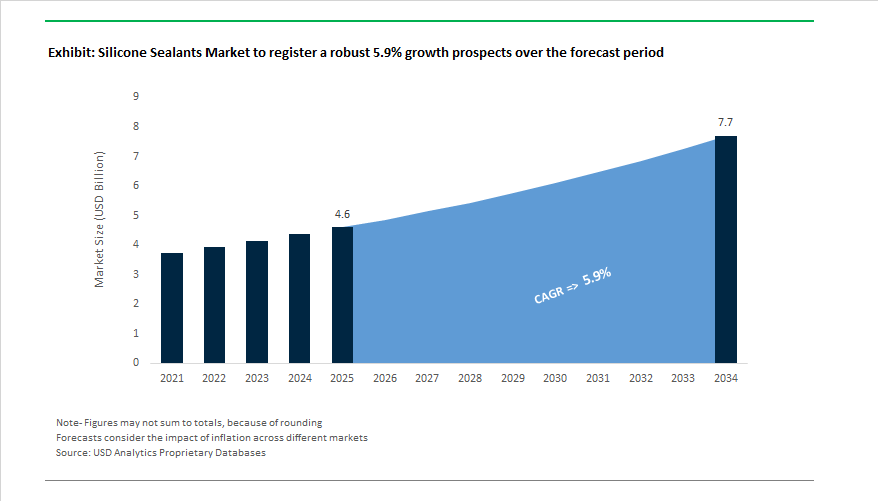

The Global Silicone Sealants Market is projected to grow from $4.6 billion in 2025 to $7.7 billion by 2034, expanding at a CAGR of 5.9%. The market’s robust performance stems from the material’s unmatched combination of elasticity, UV resistance, weather durability, and long-term structural reliability, making it indispensable for construction, automotive, electronics, and renewable energy applications.

Silicone sealants play a pivotal role in modern structural glazing, façade engineering, and modular construction, where they replace mechanical joints to deliver flexible yet durable bonding capable of withstanding dynamic loads. Products such as DOWSIL™ 795 Structural Glazing Sealant—rated for ±50% movement per ASTM C719—demonstrate how silicone formulations outperform traditional sealants in accommodating façade movement while maintaining adhesion integrity. Similarly, two-component (2K) systems like DOWSIL™ 983 provide dual-function performance (structural + weatherseal) with 20-year durability guarantees under accelerated weathering tests.

From an energy efficiency standpoint, silicone-based façade coatings and sealants have been shown to reduce building heat loss by up to 40% and water absorption by 80%, directly supporting compliance with global energy efficiency standards and green building codes such as LEED and BREEAM. Furthermore, neutral-cure silicone formulations are increasingly preferred due to their non-corrosive cure byproducts, enabling unprimed adhesion to coated glass, anodized aluminum, and powder-coated surfaces—materials that dominate modern curtainwall architecture.

Key Industry Insights

- Market Value: $4.6 billion (2025) → $7.7 billion (2034); CAGR: 5.9%.

- High-Movement Capability: ASTM C719 compliant sealants offer ±50% joint flexibility for seismic and façade applications.

- Sustainability Trend: Biomethanol-based and carbon-neutral silicone sealants are gaining regulatory preference under EU REACH and low-VOC mandates.

- Industrial Shift: Two-part (2K) factory glazing sealants provide ≥20-year service life, outlasting conventional organic sealants.

- Growth Verticals: Rapid expansion in EV assembly, modular construction, and fire-rated sealants is driving diversification.

- Future Outlook: Industry leaders are developing low-embodied-carbon silicone sealants with verified PAS 2060 carbon neutrality certifications for global façade projects.

The silicone sealants market is witnessing accelerated innovation, driven by the global shift toward sustainability, fire safety, and energy-efficient construction. Major producers are investing heavily in R&D and regional production hubs to meet growing demand in Asia, the Middle East, and North America.

In September 2025, Stabond launched its Firewall 2K silicone sealant, a breakthrough high-temperature two-component formulation engineered for fire safety applications. The product provides exceptional resistance to heat, smoke, and gas penetration, addressing the needs of commercial and industrial fire-rated assemblies. This innovation aligns with the global trend of adopting fire-blocking and smoke-sealing technologies that meet evolving building safety codes.

WACKER Chemie AG, in March 2025, introduced a biomethanol-derived natural stone silicone sealant at the European Coatings Show 2025, reinforcing the movement toward renewable raw material sourcing and low-VOC sealant formulations. The company simultaneously expanded specialty silicone production capacity in Japan and South Korea (January 2025) to meet the surging regional demand for automotive-grade and construction-grade silicones—a strategic move enhancing Wacker’s position in the Asia-Pacific market.

Henkel Adhesive Technologies, in October 2025, announced the release of multiple Environmental Product Declarations (EPDs) for its Ceresit and Loctite sealant portfolios. This initiative underscores the company’s commitment to green building transparency by providing environmental data across over 38 sustainability indicators. The EPD expansion aids developers seeking compliance with LEED, WELL, and BREEAM standards, solidifying Henkel’s reputation as a leader in sustainable construction materials.

Dow Inc. continues to lead in low-carbon innovation. The company’s DOWSIL™ 991 High Performance Sealant, launched under its Carbon-Neutral Silicone Service in February 2024, provides an externally verified PAS 2060 certificate, enabling building projects to achieve measurable reductions in embodied carbon. Furthermore, Dow’s energy-efficient multi-pane glazing solutions, announced the same year, showcase how silicone technology supports operational carbon reduction in next-generation façades.

Meanwhile, Momentive Performance Materials and Shin-Etsu Chemical Co., Ltd. are advancing performance boundaries through R&D investments in weather durability and smart infrastructure integration. Momentive’s RapidStrength™ cold-applied silicone sealant, developed for factory glazing, cuts production time significantly, while Shin-Etsu’s durable construction sealants continue to set benchmarks in UV, ozone, and moisture resistance, making them indispensable for long-life infrastructure projects in diverse climates.

The market also faces regulatory headwinds: ongoing EU REACH restrictions on cyclic siloxanes (D4, D5, D6) have forced global reformulations to maintain ≤0.1% w/w thresholds. This reformulation wave is reshaping supply chains while encouraging producers to adopt safer cyclic-free silicone chemistries for the next generation of environmentally compliant sealants.

Market Trend 1: Accelerated Reformulation to Eliminate Plasticizers and Hazardous Additives

A fundamental transformation is underway in the Silicone Sealants Industry, driven by global regulations and end-user demand for non-toxic, phthalate-free formulations. Manufacturers are responding to stricter environmental mandates and corporate ESG goals by phasing out phthalate plasticizers and hazardous additives, particularly in consumer, construction, and packaging applications.

Leading companies like Henkel Adhesive Technologies (2024) have announced next-generation silicone and PVC-based sealants completely free from phthalate plasticizers, aligning with EU REACH and U.S. FDA safety mandates. The transition not only improves environmental credentials but also eliminates substances classified as carcinogenic, mutagenic, or toxic to reproduction (CMR). Such proactive measures underscore the industry's shift toward sustainable sealant chemistry that meets upcoming global safety standards.

In the U.S., the FDA’s 2024 regulatory updates—revoking authorization for 23 phthalates—further emphasize the tightening control over plasticizer use, influencing sealant raw material supply chains. Academic research also reports that phthalate-free plasticizers grew from 12% to 35% of the global plasticizer market between 2005 and 2017, a clear indicator of large-scale industry re-engineering.

The ripple effect of these regulatory changes is profound: manufacturers are innovating alternative additives, such as bio-based esters, citrate compounds, and polymeric plasticizers, to preserve flexibility while ensuring compliance. These non-toxic, high-purity silicone sealants are becoming the new benchmark for indoor construction, glazing, and consumer packaging—solidifying the market’s commitment to health-conscious and environmentally sustainable innovation.

Market Trend 2: Proliferation of Hybrid Silicone-Organic Polymer Systems for Multi-Substrate Compatibility

The demand for multi-performance sealants—combining flexibility, adhesion, and paintability—has led to the rapid growth of hybrid silicone-organic polymer technologies, particularly MS Polymer and SPUR-based sealants. These systems merge the elasticity and UV stability of silicones with the paintability and mechanical strength of polyurethanes, catering to modern construction and industrial needs.

Technically, MS Polymer-based sealants exhibit superior mechanical properties, including Shore A hardness of 20–40, elongation at break of 500–800%, and tensile strength of 1–3 MPa, striking the optimal balance between flexibility and strength. Their low-VOC, solvent- and isocyanate-free composition positions them as an environmentally superior alternative to polyurethanes—particularly critical for LEED- and BREEAM-certified projects where indoor air quality compliance is mandatory.

Another key advantage is paintability and primerless adhesion across a diverse range of substrates—metals, wood, plastics, and concrete—making these hybrid sealants ideal for façade glazing, curtain wall joints, and interior finishing. Their UV and weathering resistance ensures exceptional durability under outdoor exposure, overcoming the long-standing discoloration and cracking issues of organic polymers.

The Hybrid Silicone-Organic Polymer trend marks a structural redefinition of sealant performance, where versatility, compliance, and longevity converge—setting a new global standard for sustainable, high-performance construction sealing systems.

Market Opportunity 1: Engineering of Fire-Rated Intumescent Silicone Sealants for Mass Timber Construction

The rise of mass timber construction (MTC)—especially Cross-Laminated Timber (CLT)—is creating an urgent need for fire-rated silicone sealants capable of ensuring both smoke containment and movement accommodation at structural joints. With global building codes permitting timber skyscrapers up to 18 stories, fire-resilient sealing technologies are at the core of next-generation sustainable architecture.

Fire-rated silicone sealants are already certified to maintain up to 240 minutes (4 hours) of integrity and insulation, as per BS EN 1366-4 standards for linear joint seals. However, innovation opportunities lie in integrating intumescent technology—allowing the sealant to expand 5–10x during fire exposure, sealing gaps and blocking smoke propagation. While intumescence is common in acrylic systems (e.g., 3M’s IC 15WB+), embedding such behavior into high-elastic silicone matrices remains an untapped frontier.

Further, silicone sealants in timber structures must accommodate ±25% joint movement, bridging gaps between flexible timber panels and rigid substrates without losing adhesion even after thermal exposure. The integration of intumescent additives within flexible silicone networks would represent a paradigm shift—delivering fire, acoustic, and weather performance in a single product. The advancement aligns with the expanding mass timber construction codes in Europe, North America, and Japan, signaling a multi-billion-dollar material innovation opportunity.

Market Opportunity 2: Formulation of Conductive and EMI Shielding Silicone Sealants for Advanced Electronics and EV Systems

The explosion of 5G infrastructure, IoT devices, and EV electronics is creating a lucrative frontier for conductive and EMI-shielding silicone sealants, which combine electrical performance with environmental sealing. These advanced sealants play a pivotal role in electronic enclosures, base stations, and control modules, where both signal integrity and protection from harsh environments are critical.

The global conductive plastics and EMI shielding materials market, valued at USD 1.35 billion in 2024, highlights the scale of the opportunity. Conductive silicone sealants, filled with metallic (silver, nickel, copper) or carbon-based fillers, can achieve EMI attenuation up to 70 dB while maintaining IP-rated watertight sealing. The dual functionality positions silicone as a high-value solution for 5G antennas, radar housings, and high-frequency electronics.

In automotive e-mobility, conductive and thermally conductive silicones are increasingly used for battery enclosures and control units (ECUs), where sealing performance must withstand operating temperatures up to 150°C while ensuring electrical grounding and EMI shielding. Companies like Dow and Wacker are leveraging cross-sector expertise from photovoltaic and aerospace silicone systems to engineer these next-generation conductive sealants.

By combining environmental durability, electrical conductivity, and electromagnetic compatibility (EMC), conductive silicone sealants are emerging as an enabling material for the next phase of electronics miniaturization and EV reliability.

Silicone Sealants Market Share Insights, 2025-2034

Market Share by Formulation

One-Part Silicone Sealants dominate the global silicone sealants market, accounting for an estimated 77.2% share by 2025. Their market leadership stems from unmatched ease of application, minimal preparation requirements, and broad compatibility across substrates, making them indispensable in construction, automotive repair, and general maintenance. These moisture-curing formulations eliminate the need for on-site mixing, thereby reducing labor time and ensuring consistent performance in variable conditions. They are extensively used for structural glazing, weatherproofing, joint sealing, and window installation, owing to their strong adhesion, flexibility, and UV resistance. As the global construction sector emphasizes productivity, sustainability, and simplified installation, single-component sealants have become the preferred choice for contractors and manufacturers seeking efficiency without compromising durability. The adoption of low-VOC and neutral-cure formulations further accelerates their use in both indoor and outdoor environments, supporting the sustainability goals of green building initiatives.

On the other hand, Two-Part Silicone Sealants represent a specialized but vital segment of the market. These formulations are primarily used in industrial, structural, and high-precision manufacturing environments that demand deep-section curing, controlled application, and superior mechanical strength. Two-part systems are favored in curtain wall assembly, insulating glass units, and aerospace applications, where rapid curing and consistent performance under extreme stress are essential. They offer enhanced bonding uniformity and chemical stability, making them particularly valuable in automated production lines and factory-controlled settings.

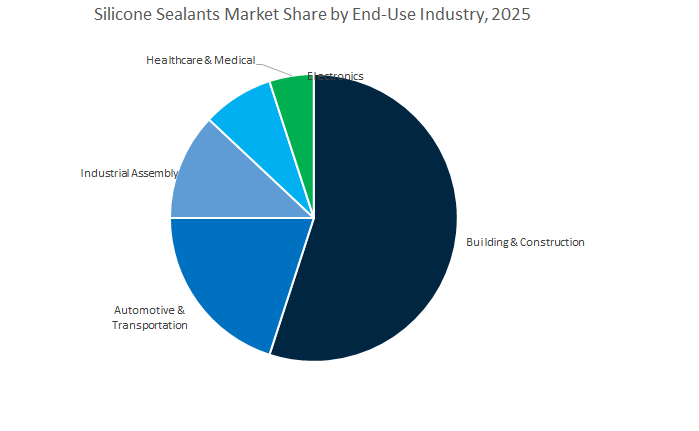

Market Share by End-Use Industry

The Building & Construction sector is the dominant consumer of silicone sealants, commanding approximately 54.1% of the global market share in 2025. This dominance is anchored in the material’s unmatched performance in weatherproofing, structural glazing, expansion joint sealing, and sanitary applications across both new builds and renovations. Silicone sealants are a cornerstone of modern architecture due to their superior UV stability, elasticity, and resistance to moisture and temperature extremes. They are extensively used in high-rise façades, glass curtain walls, and prefabricated structures, where structural integrity and long-term durability are critical. With growing global investments in urban infrastructure, smart cities, and sustainable buildings, demand for high-performance silicone sealants continues to surge. Furthermore, the shift toward energy-efficient buildings has reinforced the use of silicone sealants in thermal insulation, air-tight sealing, and solar panel installations, strengthening their strategic role in sustainable construction.

The Automotive & Transportation segment ranks as the second-largest contributor, utilizing silicone sealants in vehicle assembly, glass bonding, seam sealing, and gasketing applications. Their flexibility, resistance to vibration, and ability to maintain adhesion under harsh environmental conditions make them vital in both traditional and electric vehicles (EVs). Silicone sealants are increasingly used for EV battery module sealing, lightweight composite bonding, and aerodynamic component assembly, reflecting the industry’s transition toward electrification and material innovation. The Industrial Assembly sector also holds a substantial market share, leveraging silicone sealants for equipment assembly, HVAC systems, appliance manufacturing, and heavy machinery. Their temperature resistance and long service life make them suitable for environments involving thermal cycling, mechanical stress, or chemical exposure.

Beyond industrial and automotive sectors, Electronics and Healthcare applications represent niche but rapidly growing areas. In electronics, silicone sealants are valued for potting, conformal coating, and LED encapsulation, protecting sensitive components from moisture and heat. In the healthcare sector, medical-grade silicone sealants are essential in device assembly, prosthetics, and surgical equipment manufacturing, meeting stringent biocompatibility and sterilization requirements.

The Global Silicone Sealants Industry remains moderately consolidated, with five global leaders—Dow, Wacker Chemie, Henkel, Momentive, and Shin-Etsu—commanding over 75% of market share. Their competitive advantage lies in technological depth, R&D scalability, and material sustainability.

Dow’s DOWSIL™ 995 Structural Sealant offers ±50% movement and unprimed adhesion across substrates including reflective glass and anodized aluminum, making it the industry benchmark for high-performance glazing and curtainwall bonding. The company’s Carbon-Neutral Silicone Service, verified to PAS 2060, positions Dow as a pioneer in low-embodied-carbon façade materials. With innovations like DOWSIL™ 983 two-part glazing sealant, warranted for 20+ years, and DOWSIL™ 1200 OS low-VOC primer, Dow delivers unmatched system integration, durability, and sustainability for the global façade and infrastructure markets.

Wacker’s ELASTOSIL® eco line replaces 100% of fossil feedstocks with biomass-certified sources, significantly cutting the carbon footprint of building materials. With new plants in Japan and South Korea (January 2025), Wacker is meeting escalating demand from the Asian automotive and construction markets. Its advanced formulations—neutral-curing, alkoxy-terminated polymers, and tailored additives—offer superior flame retardance, non-staining properties for natural stone, and compliance for food-contact sealing, reinforcing Wacker’s status as a sustainability leader in specialty silicones.

Henkel’s construction adhesives business emphasizes sustainability transparency, with over 50 EPDs released for Ceresit® and Loctite® sealant brands. Their UL 746C-certified silicones, rated up to 230°C, ensure superior thermal cycling and mechanical stability for HVAC and appliance applications. Henkel’s Industry 4.0-enabled plant in Pune, India, drives high-volume manufacturing efficiency, supporting rapid growth across mobility, electronics, and construction sealant markets.

Momentive’s UltraGlaze™ structural glazing sealants are precision-engineered for impact-resistant and high-load façade systems, widely adopted in architectural and transportation infrastructure. Its RapidStrength™ cold-applied silicone accelerates factory glazing production, while the SilPruf™ weatherseal series is backed by a 40-year Miami weathering study, proving unmatched UV and environmental stability. The company’s Elemax™ barrier coatings further highlight its ability to deliver air- and water-resistant silicone systems for large-scale modular and smart construction projects.

Shin-Etsu offers high-durability construction sealants designed to withstand UV, ozone, and temperature extremes, maintaining elasticity and adhesion across diverse climates. Its functional sealant portfolio spans flame-retardant, cleanroom, and mold-resistant applications. Backed by its leadership in semiconductor-grade silicone and Crystal Film Bonding (CFB) technologies, Shin-Etsu transfers high-tech process innovations into building-grade silicone performance, providing a scientifically engineered, globally reliable sealant platform.

Country Analysis: Key Drivers of Innovation and Adoption in the Global Silicone Sealants Market

China: Infrastructure Expansion and E-Mobility Lead Asia-Pacific Silicone Sealant Growth

China remains the epicenter of global silicone sealant demand, propelled by large-scale infrastructure development, expanding manufacturing capacity, and rapid adoption of green building materials. The government’s ongoing Belt and Road Initiative continues to stimulate extensive construction across bridges, transportation hubs, and high-speed rail networks—driving robust consumption of structural glazing and weatherproof silicone sealants. With over CNY 4 trillion allocated for “hidden infrastructure” modernization through 2030, silicone-based materials are increasingly preferred over acrylics due to their superior UV resistance and long-term elasticity.

The nation recorded an 8.9% increase in chemical manufacturing investment in 2024, strengthening the domestic supply chain for silicone resins and specialty polymers. At the same time, China’s dominance in Electric Vehicle (EV) manufacturing has led to surging adoption of thermally conductive silicone adhesives, gap fillers, and potting compounds for high-performance battery systems and power electronics. Global leaders such as Sika AG have expanded their manufacturing footprint in Northeast China (2024) to meet the escalating demand for industrial and construction-grade silicone sealants.

United States: Infrastructure Revitalization and High-Tech Manufacturing Drive Silicone Sealant Demand

The United States silicone sealants market is experiencing strong expansion fueled by infrastructure spending, green building initiatives, and advancements in electronics and aerospace engineering. Under the Infrastructure Investment and Jobs Act (IIJA), over $550 billion in federal funding for transportation and public works projects is generating heightened demand for durable expansion joint sealants, waterproof coatings, and highway bridge protection materials. Stricter state and federal energy-efficiency building codes, aligned with LEED and BREEAM certifications, are reinforcing the shift toward low-VOC, neutral-cure silicone sealants that reduce environmental impact without compromising performance.

In the high-tech sector, the revitalization of semiconductor fabrication has led to increased reliance on ultra-pure silicone encapsulants and potting materials used for microelectronics assembly and chip packaging. Moreover, the U.S. aerospace and defense industries—key contributors to advanced material innovation—demand flame-retardant, temperature-stable silicone sealants for critical thermal protection in aircraft and satellite systems. In the architectural sector, the ongoing boom in commercial high-rise glazing supports consistent growth in structural silicone glazing (SSG) sealants, which ensure long-lasting adhesion and weather resistance. With its robust R&D ecosystem and industrial resilience, the U.S. remains a global leader in premium and specialized silicone sealant technologies.

Germany: European Center for High-Performance Silicone Sealant R&D and Sustainability

Germany stands at the forefront of European silicone sealant innovation, with a strong emphasis on energy efficiency, e-mobility, and sustainable production. The EU’s Renovation Wave Strategy—aimed at improving energy performance in millions of older buildings—has boosted nationwide demand for high-insulation, weatherproof silicone sealants in energy retrofits and façade refurbishments. German engineering precision and regulatory rigor continue to shape the market, as manufacturers develop oxime-free, REACH-compliant silicone formulations that combine performance with environmental safety.

The country’s dominant automotive industry, home to premium OEMs like BMW, Volkswagen, and Mercedes-Benz, is driving R&D investment in lightweight silicone adhesives for bonding dissimilar substrates and protecting EV battery modules. Leading producers such as Wacker Chemie AG and Henkel AG & Co. KGaA are spearheading developments in bio-based silicone sealants and low-carbon manufacturing technologies, ensuring alignment with the EU’s sustainability roadmap. With its advanced R&D infrastructure and adherence to strict material standards, Germany continues to act as Europe’s technological nucleus for high-durability and eco-friendly silicone sealant solutions.

India: Infrastructure Acceleration and Localization Boost Silicone Sealant Manufacturing

India’s silicone sealants market is rapidly scaling due to a combination of infrastructure development, affordable housing programs, and domestic manufacturing expansion. The government’s PM Gati Shakti National Master Plan and Smart Cities Mission have accelerated construction activity across highways, airports, and urban housing, stimulating widespread adoption of glazing, expansion-joint, and waterproofing silicone sealants. In addition, initiatives like the Pradhan Mantri Awas Yojana (PMAY) have created significant demand for general-purpose and moisture-resistant silicone products across Tier-2 and Tier-3 cities.

Partnerships such as Saugaat Inc. and Elkem India’s collaboration (November 2023) underscore a trend toward localized production and supply chain strengthening for structural glazing silicone sealants used in architectural façades and high-rise buildings. The automotive OEM sector is another growth catalyst, with EV manufacturers increasing their use of high-temperature silicone sealants for battery safety and thermal insulation applications. Supported by industrial investments, skilled labor, and a booming construction market, India is rapidly becoming a key emerging hub for silicone sealant manufacturing in the Asia-Pacific region.

Japan: Advanced Silicone Materials and Seismic Resilience Shape Market Demand

Japan continues to be a technological frontrunner in high-performance silicone sealants, emphasizing precision, purity, and durability. Industry giants such as Shin-Etsu Chemical Co., Ltd. dominate production with extensive portfolios of industrial-grade and high-purity silicone sealants used across electronics, semiconductors, and advanced displays. In the construction sector, Japan’s unique focus on seismic resilience drives strong demand for high-elongation, flexible silicone sealants capable of withstanding significant joint movement and vibrations during earthquakes.

In early 2025, Soudal Group acquired a majority stake in Sharp Chemicals, signaling increased international collaboration and investment to meet Japan’s growing appetite for high-performance and DIY-oriented sealant solutions. The Japanese market also leads in next-generation insulating and structural glazing silicone sealants for energy-efficient façade systems. With its combination of high technical standards, R&D innovation, and reliability in performance, Japan remains a global benchmark for premium-grade silicone sealant technology.

Saudi Arabia: Vision 2030 Mega Projects Fuel Silicone Sealant Boom in the Middle East

Saudi Arabia’s construction and infrastructure renaissance under Vision 2030 has transformed the nation into the largest structural sealant market in the Middle East. Massive megaprojects—such as NEOM, The Line, and the Red Sea Development—are generating record-breaking demand for weather-resistant silicone sealants and glazing systems engineered to withstand extreme temperature fluctuations ranging from -40°C to +150°C. The projects prioritize long-lifecycle, UV-stable, and sand-resistant silicone sealants, ideal for the region’s harsh environmental conditions.

Contractors and developers increasingly specify neutral-cure, low-VOC silicone grades with 20-year weathering warranties, reflecting a move away from traditional acrylic and polysulfide alternatives. Simultaneously, Saudi Arabia’s growing adoption of green building practices and sustainable design frameworks is accelerating the uptake of energy-efficient, high-performance silicone sealants for superior air and moisture barrier integrity. Backed by large-scale investments and a rapidly diversifying construction ecosystem, Saudi Arabia is emerging as the Middle East’s structural silicone sealant powerhouse.

Silicone Sealants Market Report Scope

Silicone Sealants Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$4.6 Billion

|

|

Market Size (2034)

|

$7.7 Billion

|

|

Market Growth Rate

|

5.9%

|

|

Segments

|

By Curing System (Neutral, Acetoxy, Heat-Cure, Pressure Sensitive, Radiation Cured), By Formulation (One-Part/Single-Component, Two-Part/multi-component), By Product Type, Construction, Structural Glazing, Automotive & Transportation, Electronic, High-Temperature, Marine, Insulating Glass, DIY/Consumer), By End-User (Building & Construction, Automotive & Transportation, Electronics, Industrial Assembly, Healthcare & Medical

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Dow Inc., Wacker Chemie AG, Shin-Etsu Chemical Co., Ltd., Henkel AG & Co. KGaA, Sika AG, Momentive Performance Materials Inc., H.B. Fuller Company, Soudal Group, 3M Company, BASF SE, PPG Industries Inc., RPM International Inc., Arkema Group (Bostik), Kömmerling Chemische Fabrik GmbH, Pidilite Industries Ltd.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

By Curing System/Technology

- Neutral

- Acetoxy

- Heat-Cure

- Pressure Sensitive

- Radiation Cured

By Formulation

- One-Part/Single-Component

- Two-Part/Multi-Component

By Product Type/End-Use Grade

- Construction

- Structural Glazing

- Automotive & Transportation

- Electronic

- High-Temperature

- Marine

- Insulating Glass

- DIY/Consumer

By End-Use Industry

- Building & Construction

- Automotive & Transportation

- Electronics

- Industrial Assembly

- Healthcare & Medical

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in Silicone Sealants Market

- Dow Inc.

- Wacker Chemie AG

- Shin-Etsu Chemical Co., Ltd.

- Henkel AG & Co. KGaA

- Sika AG

- Momentive Performance Materials Inc.

- H.B. Fuller Company

- Soudal Group

- 3M Company

- BASF SE

- PPG Industries Inc.

- RPM International Inc.

- Arkema Group (Bostik)

- Kömmerling Chemische Fabrik GmbH

- Pidilite Industries Ltd.

*- List not Exhaustive

Research Coverage

Prepared by USDAnalytics, this report investigates the Global Silicone Sealants Market through the lens of performance engineering, sustainability, and code compliance—tracking how chemistry breakthroughs (neutral-cure, heat-cure, radiation-cured, and PSA systems), factory-glazing workflows, and carbon-accounted product lines are reshaping façade, mobility, and electronics sealing; our analysis reviews specification trends (movement capability, durability, VOC/REACH conformity), capex footprints, and route-to-market shifts, and highlights where one-part versus two-part systems win on productivity, lifetime elasticity, and substrate range—making this report an essential resource for architects, façade consultants, OEM engineers, sourcing leaders, and investors requiring decision-grade forecasts, standards mapping, and competitor positioning through 2034.

Scope Highlights

Segmentation:

- By Curing System/Technology: Neutral; Acetoxy; Heat-Cure; Pressure Sensitive; Radiation Cured.

- By Formulation: One-Part/Single-Component; Two-Part/Multi-Component.

- By Product Type/End-Use Grade: Construction; Structural Glazing; Automotive & Transportation; Electronic; High-Temperature; Marine; Insulating Glass; DIY/Consumer.

- By End-Use Industry: Building & Construction; Automotive & Transportation; Electronics; Industrial Assembly; Healthcare & Medical.

- By Region: North America (United States, Canada, Mexico); Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe); Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC); South & Central America (Brazil, Argentina, Rest of SCA); Middle East & Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa).

Geographic Scope: Analysis spans 25+ countries across North America, Europe, Asia Pacific, Latin America, the Middle East & Africa.

Timeframe: Historic data 2021–2024 and forecasts 2025–2034.

Companies: Analysis/profiles of 15+ companies.

Deliverables

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.