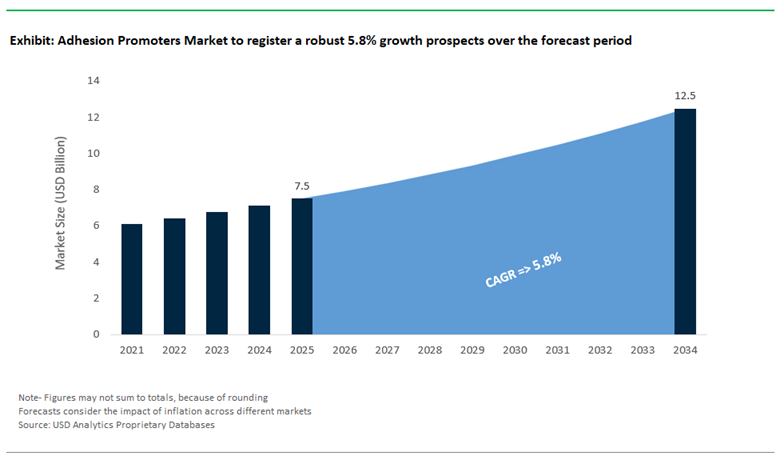

The Global Adhesion Promoters Market, valued at USD 7.5 billion in 2025 and projected to reach USD 12.5 billion by 2034 at a CAGR of 5.8%, plays a foundational role in modern material engineering by enabling durable bonding between otherwise incompatible substrates. Across automotive, industrial coatings, flexible packaging, electronics, and construction, adhesion promoters are no longer optional additives—they are process-critical materials that directly determine coating lifetime, laminate integrity, corrosion resistance, and long-term mechanical reliability. Leading manufacturers position adhesion promoters as interfacial engineering solutions, designed to chemically bridge polymers with metals, glass, ceramics, fillers, and treated plastics under increasingly aggressive service environments.

From a formulation standpoint, the market is anchored by silane coupling agents, maleic-anhydride-grafted polymers, chlorinated polyolefins (CPOs), and functional polymer dispersions, each optimized for specific substrate combinations and processing routes. Silane-based adhesion promoters remain the industry benchmark due to their ability to form covalent bonds across organic–inorganic interfaces, making them indispensable in coatings, electronics encapsulation, fiberglass composites, and corrosion-protective systems. In parallel, CPO-based promoters are essential for bonding low-surface-energy plastics such as polypropylene and TPOs in automotive exterior coatings, while MAH-grafted polyolefins dominate composite compounding, multilayer packaging, and glass-fiber-reinforced plastics.

Manufacturers are increasingly engineering adhesion promoters to meet simultaneous performance, regulatory, and sustainability targets. Automotive OEMs and Tier-1 suppliers demand promoters compatible with waterborne coatings, low-bake processes, and multi-material lightweight structures, particularly for EV battery packs, composite body panels, and structural adhesives. In response, suppliers are scaling low-VOC, solvent-free, and bio-attributed adhesion technologies that preserve bond strength, hydrolytic stability, and thermal resistance while complying with REACH, EPA, and regional emissions standards. This sustainability shift is not cosmetic; it reflects real process changes on OEM coating lines, packaging lamination plants, and electronics assembly floors.

Across downstream industries, adhesion promoters are increasingly specified at the design and qualification stage, not added post-hoc. Packaging converters rely on them to ensure ink adhesion, metallized film bonding, and barrier layer integrity under thermal cycling and food-contact conditions. Electronics manufacturers use ultra-pure silanes to improve dielectric adhesion, moisture resistance, and signal reliability in PCBs and semiconductor packaging. Meanwhile, industrial coatings producers integrate adhesion promoters into primers and topcoats to extend corrosion protection lifetimes in marine, infrastructure, and energy assets.

The Global Adhesion Promoters Market is undergoing a pivotal transition characterized by innovation in sustainable chemistry, advanced bonding technologies, and cross-industry adoption. Over the past two years, a clear movement toward environmentally responsible and high-performance formulations has reshaped product development pipelines.

In January 2023, BASF SE introduced a bio-based adhesion promoter, underscoring the global shift toward eco-friendly raw materials and reduced carbon footprint manufacturing. Similarly, Dow Chemical (May 2023) invested heavily in next-generation adhesion technology R&D to meet performance standards in high-demand industries like automotive and infrastructure. This momentum was mirrored by Eastman Chemical Company’s launch of its Advantis product line (July 2023), offering regulatory-compliant alternatives to restricted materials, a move that highlights the increasing importance of safety and sustainability in industrial formulations.

The automotive and packaging industries remain key growth anchors. 3M’s October 2023 product launch introduced high-performance adhesion promoters for automotive structural parts, targeting durable bonding under thermal and mechanical stress. Meanwhile, Nippon Paper Group (November 2023) expanded its portfolio with advanced adhesion promoters for e-commerce and flexible packaging applications, optimizing bonding for diverse substrates. On the sustainability front, a March 2025 innovation by Vantage unveiled the iSAP 311 Inhibited Surface Adhesion Promoter, a non-chromated pretreatment designed for aerospace — signaling a definitive shift away from harmful heavy-metal-based chemistries.

The market is witnessing an accelerated shift toward silane-based adhesion promoters, driven by the need for longer-lasting infrastructure coatings, superior metal protection, and reliable bonding between dissimilar materials. Silane coupling agents are becoming the preferred solution due to their ability to form covalent bonds, ensuring exceptional adhesion and corrosion resistance even under extreme environmental conditions.

Eastman’s 2023 launch of Advantis adhesion promoters exemplifies the evolution, delivering enhanced adhesion and corrosion protection for multi-layered paint systems — a key demand in infrastructure and marine coatings. Similarly, Dow’s DOWSIL™ SH 6040 Silane has proven indispensable for polymer-to-metal and polymer-to-glass bonding applications, expanding its utility in industrial construction and protective coating formulations. The industry is also transitioning away from toxic chromate-based systems, with Vantage’s 2024 iSAP 311 non-chromated adhesion promoter setting a benchmark for eco-friendly, high-strength metal pretreatments.

As sustainability and performance become inseparable market drivers, silanes have emerged as the chemical backbone for next-generation adhesion technologies. The dominance of silanes across market share statistics reinforces their versatility in high-demand sectors, including automotive composites, wind energy, and protective coatings, ensuring long-term structural integrity and surface performance.

Sustainability regulations are redefining adhesive and coating chemistry, leading to a decisive industry-wide shift toward low-VOC, solvent-free, and waterborne adhesion promoters. As global environmental frameworks like the U.S. EPA’s VOC Emission Standards tighten, manufacturers are accelerating R&D to match solvent-based performance with eco-friendly formulations.

PPG Industries has documented that its new generation of waterborne resin systems achieves performance parity with solvent-based products in corrosion resistance and durability, bridging the historical gap in adhesion strength and weatherability. Henkel’s 2023 sustainability strategy reinforces the transition, prioritizing resource-efficient, water-based adhesive additives to meet its carbon-neutral product goals by 2030. Likewise, BASF’s additive portfolio is expanding with solvent-free adhesion technologies designed for automotive and industrial coatings that demand long-term adhesion and environmental compliance.

The move toward 100% solids and waterborne systems marks a pivotal phase in the industry's green chemistry evolution, reducing hazardous emissions while ensuring long-lasting adhesion performance across substrates.

As automakers aggressively pursue vehicle lightweighting to improve fuel efficiency and meet global emissions standards, the use of polyolefins (TPOs, PP) in exteriors and interiors is rapidly expanding. However, these low-surface-energy plastics pose significant adhesion challenges — creating a major opportunity for next-generation adhesion promoters capable of forming strong, durable bonds between polyolefins and coatings, paints, or adhesives.

BASF Coatings emphasizes the criticality of adhesion promoters in ensuring optimal surface bonding for polyolefin-based automotive interiors and exterior coatings. The I-CAR (Inter-Industry Conference on Auto Collision Repair) highlights adhesion promoters as mandatory materials in TPO repair, underscoring their essential role in automotive refinishing and crash repair applications. Similarly, Pro Form’s TPO Adhesion Promoter targets complex thermoplastic substrates, reinforcing the rise of product specialization tailored for automotive manufacturing needs.

In addition, silane coupling agents are expanding their role in the automotive composites sector by modifying the surface chemistry of plastics and fiber-reinforced materials, making them more receptive to coatings. The capability directly supports automakers’ growing reliance on lightweight composites and recyclable polymers, paving the way for sustainable mobility solutions. As automotive OEMs increasingly standardize TPO-compatible adhesion systems, the opportunity is expected to accelerate, driving innovation in both primerless and surface-activated adhesion technologies.

The proliferation of flexible hybrid electronics (FHE), wearable devices, and printed sensors is creating a lucrative growth opportunity for high-performance adhesion promoters tailored for flexible substrates like PET, polyimide (PI), and textile films. The demand for robust bonding between conductive inks, films, and polymer substrates is surging as flexible electronics become central to next-generation devices and 5G-enabled infrastructure.

DuPont’s conductive ink platforms are prime examples, requiring ASTM D3359-certified adhesion ratings to maintain reliable performance under mechanical stress. A 2023 study published in MDPI confirmed that bending cycle reliability in multilayer flexible electronics is directly correlated to adhesion promoter quality, solidifying their role in electronics durability and long-term reliability. Henkel’s R&D has similarly shifted focus toward low-temperature-curing conductive inks and adhesive systems compatible with flexible substrates, advancing printed electronics manufacturing efficiency.

Further, DuPont Electronics & Industrial’s transparent conductive ink technology for OLED displays and PV cells relies heavily on optically clear, high-durability adhesion promoters to preserve optical transmittance and electrical integrity. As the boundaries between mechanical flexibility and electronic performance continue to blur, adhesion promoters are becoming the invisible yet indispensable enablers of modern electronics — creating high-margin, innovation-driven opportunities in the global market.

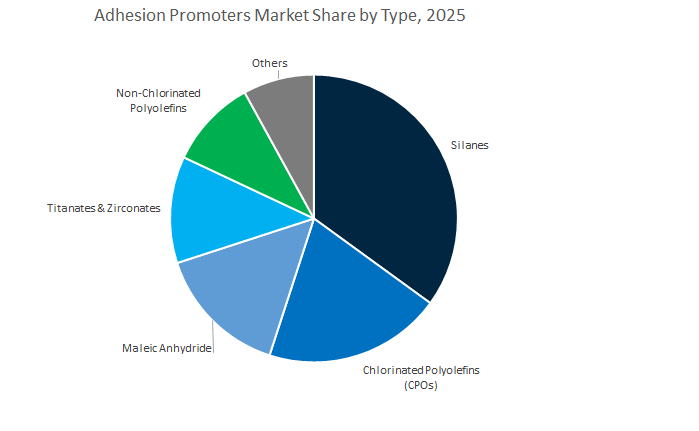

Adhesion Promoters Market Share Insights, 2025-2034

The silane-based adhesion promoters segment dominates the global adhesion promoters industry, accounting for approximately 35% of the market share in 2025. This dominance is primarily due to silanes’ exceptional versatility and chemical functionality across a broad spectrum of substrates, including glass, metals, ceramics, and mineral fillers. Their ability to form robust siloxane linkages enables durable interfacial bonding, significantly enhancing the mechanical strength, corrosion resistance, and moisture durability of coatings, composites, and adhesives. Silanes are heavily used in automotive coatings, construction sealants, and fiber-reinforced composites, reflecting their integral role in modern materials engineering. Furthermore, the ongoing shift toward high-performance and eco-friendly coatings has further elevated silane adoption, as they improve adhesion while maintaining low-VOC formulations. Continuous innovation in functional silane chemistries (such as amino, epoxy, methacryloxy, and vinyl silanes) is also broadening their utility across hybrid materials and next-generation manufacturing applications, securing their leading position in the market.

The chlorinated polyolefins (CPOs) segment captures around 20% market share, driven by its indispensable use in promoting adhesion to non-polar substrates like polypropylene (PP), polyethylene (PE), and thermoplastic olefins (TPOs). These materials dominate automotive interiors, bumpers, flexible packaging films, and other applications where achieving strong adhesion remains technically challenging. CPOs act as primer coatings that improve interfacial bonding between organic coatings or adhesives and polyolefin surfaces, which otherwise resist conventional adhesion methods. Their cost-effectiveness, ease of formulation, and proven compatibility with various coating systems have made them the workhorse solution for plastic adhesion. However, environmental regulations on halogenated compounds are beginning to restrain long-term growth, encouraging R&D investment toward non-chlorinated alternatives that maintain similar performance without ecological drawbacks.

The maleic anhydride-grafted polymer segment plays a crucial role in the evolving landscape of polymer modification and compatibilization, particularly in recycled plastics and bio-composite applications. These adhesion promoters act as coupling agents, improving the dispersion of fillers and reinforcing fibers within polymer matrices. They are widely adopted in automotive lightweighting, packaging, and industrial composites, where strong interfacial bonding between dissimilar materials (such as polyamide, polyethylene, and glass fibers) is essential. Their rising importance in polymer circularity and mechanical recycling underscores their growing strategic value. The segment’s share is expected to expand steadily as manufacturers aim to enhance mechanical integrity and sustainability in multi-material systems.

The paints and coatings segment dominates the global adhesion promoters market, representing approximately 40% of the total share in 2025. Adhesion promoters are fundamental to the durability, corrosion protection, and performance of coatings used in automotive OEM, industrial maintenance, construction, and marine applications. They enhance adhesion to a wide range of substrates from metals and plastics to wood and glass and improve resistance to humidity, abrasion, and UV exposure. The growth in automotive refinishing, protective coatings, and high-performance architectural paints has significantly boosted demand for silane-based and titanate-based adhesion promoters. Moreover, the global shift toward waterborne and low-VOC coatings has amplified reliance on adhesion promoters that ensure performance parity with solvent-based systems. As sustainability and material compatibility continue to define modern coating technologies, adhesion promoters have become indispensable for achieving durability and aesthetic consistency across eco-friendly formulations.

The adhesives and sealants segment, holding around 22% of market share, represents one of the most dynamic and innovation-driven areas of growth. Adhesion promoters are integral to the formulation of high-strength structural adhesives and elastomeric sealants, particularly in industries like automotive, aerospace, and construction, where diverse substrates must be bonded under extreme environmental conditions. The rising adoption of lightweight materials, composites, and plastic assemblies has increased the need for advanced coupling agents (particularly silanes and maleic anhydride-based systems) to ensure mechanical integrity and chemical compatibility. Additionally, the transition from solvent-based adhesives to waterborne and hybrid chemistries further amplifies the demand for adhesion promoters that provide strong bonding performance even under reduced surface energy. As industrial automation and product miniaturization continue, the segment is expected to remain a strategic growth frontier for the adhesion promoters industry.

The plastics modification segment represents another critical area of expansion, driven by the surge in recycled plastics, biopolymers, and performance composites. Adhesion promoters are increasingly employed to compatibilize polymer blends, improve filler dispersion, and strengthen fiber-matrix interfaces, enhancing both processing stability and end-product performance. The transition toward circular economy models in packaging, automotive, and consumer goods manufacturing is accelerating the use of maleic anhydride and non-chlorinated coupling agents in recycled polyolefin systems. Similarly, innovations in bio-based and biodegradable polymer formulations are creating fresh opportunities for new-generation adhesion promoters designed to improve interfacial bonding in eco-friendly materials.

The competitive environment of the Adhesion Promoters Market is defined by a blend of chemical innovation, global integration, and sustainability-driven differentiation. Leading players such as Momentive Performance Materials, Evonik Industries, Dow Inc., BASF SE, Eastman Chemical Company, and Wacker Chemie AG are emphasizing both technological leadership and circular economy principles. These companies are expanding portfolios through strategic R&D, product line diversification, and regional production optimization to meet specialized end-user demands across automotive, packaging, and high-performance coatings.

Momentive Performance Materials remains the undisputed leader in the silane-based adhesion promoters segment. Its Silquest™ brand exemplifies high-reliability silane technologies used across electronics, automotive, and construction coatings. The company’s ongoing investments in high-purity organo-functional silanes are directly aligned with the miniaturization trend in semiconductor and electronics applications, reinforcing its reputation as a frontrunner in molecular bonding performance.

Evonik Industries AG leverages its expansive specialty chemical portfolio to deliver organo-functional silanes and chlorinated polyolefins (CPOs) tailored for difficult-to-bond substrates such as plastics and composites. The company’s strategy of offering complete formulation systems—combining adhesion promoters, catalysts, and additives—gives it a competitive edge in high-end paints, coatings, and adhesives markets. Its focus on system integration rather than stand-alone products enhances efficiency for industrial coating manufacturers globally.

Dow Inc. combines extensive global manufacturing scale with advanced silane coupling agent innovations under its DOWSIL™ brand. The company’s recent expansion into adhesion solutions for green building materials and infrastructure projects demonstrates its proactive stance in sustainable construction chemistry. Through sustained R&D and collaborative projects, Dow is fortifying its presence in automotive lightweighting and EV material bonding, positioning itself as a catalyst for sustainable infrastructure innovation.

BASF SE integrates adhesion promoter development into its vast chemical manufacturing ecosystem, allowing seamless synergy with coatings, automotive OEMs, and industrial adhesive producers. Its bio-based adhesion promoter launched in January 2023 underscores a strategic commitment to carbon reduction and circular chemistry. BASF’s innovation pipeline continues to focus on maleic anhydride and hybrid chemistries optimized for next-generation coatings and polymer systems used in high-performance environments.

Eastman Chemical Company maintains a strong niche in rosin-based and hydrocarbon-resin-derived adhesion solutions, particularly suited for pressure-sensitive adhesives (PSAs) and protective coatings. The Advantis product line (July 2023) was specifically designed to mitigate materials of concern, offering compliant alternatives amid tightening global chemical regulations. This strategic positioning highlights Eastman’s role in delivering safe, reliable, and performance-driven adhesive solutions for critical industrial applications.

Wacker Chemie AG continues to expand its presence in silicone and silane-based adhesion systems, notably under the WACKER Geniosil™ brand. The company’s focus on electric vehicle (EV) battery assemblies, sealants, and thermal interface adhesives aligns with growing global demand for durable and moisture-resistant materials. With investments targeting EV supply chains and renewable energy applications, Wacker is solidifying its position as a technological partner in next-generation structural bonding.

China continues to dominate the global adhesion promoters industry, leveraging its large-scale industrial base, policy-driven infrastructure development, and technological innovation in EV, construction, and packaging sectors. The government’s push for urbanization and electric vehicle infrastructure is driving exponential demand for high-performance construction sealants and silane-based adhesion systems, vital for advanced building materials and automotive composites.

The country’s chemical manufacturing ecosystem is rapidly expanding its amino-functional silane capacity, supporting the domestic shift toward silica-reinforced “green tires” and sustainable adhesives. Parallel to The, China’s EV battery Gigafactories, supported by state funding, are adopting high-purity photoresist adhesion promoters for cell-to-pack bonding, heat management, and electrode coating stability. Additionally, provincial innovation parks are incentivizing R&D partnerships for non-halogenated adhesion promoters—aligning with new national safety and environmental standards in wire and cable manufacturing.

Emerging industries such as digital printing and flexible packaging are spurring demand for titanate and zirconate-based adhesion promoters that enhance ink compatibility on complex polymer films. Furthermore, leading multinational specialty chemical firms are localizing production to strengthen their supply chain for automotive Tier 1 suppliers, improving response times and reducing dependency on imports. The strategic advancements position China as a self-sufficient, innovation-led hub for global adhesion promoter production, balancing industrial scale with sustainability priorities.

The United States adhesion promoters market is undergoing a structural transformation toward bio-based and low-VOC formulations, driven by tightening environmental standards and innovation in high-value sectors such as aerospace, automotive, and semiconductors. Companies like Eastman Chemical are leading The transition, introducing next-generation bio-based adhesion promoters that comply with emerging regulatory frameworks and corporate sustainability goals.

The aerospace industry remains a prime consumer, where thermosetting adhesion promoters are being developed for carbon fiber reinforced polymers (CFRPs)—critical in achieving lightweight, durable, and fuel-efficient aircraft structures. Similarly, the CHIPS Act has revitalized semiconductor manufacturing, creating new demand for high-purity photoresist adhesion promoters used in advanced lithography, packaging, and wafer bonding applications.

In the automotive sector, U.S. manufacturers are innovating epoxy-silane systems to strengthen mixed-material joints between aluminum and composites in EV architectures, while VOC reduction mandates are accelerating the adoption of waterborne adhesion promoters in coatings. Furthermore, 3D printing research collaborations are advancing liquid adhesion promoters for improved interlayer strength and substrate bonding in additive manufacturing. Combined, The developments illustrate the U.S. leadership in sustainable chemistry, advanced materials engineering, and localized production—cornerstones of future adhesion technologies.

Germany stands at the forefront of sustainable adhesion promoter innovation, fueled by stringent EU chemical policies and deep industrial expertise. Industry leaders such as Evonik Industries AG, Wacker Chemie AG, and BASF SE are spearheading efforts to eliminate environmentally harmful materials by commercializing non-chlorinated polyolefins (CPOs) and PFAS-free adhesion solutions, fully aligned with the European Green Deal.

Germany’s strong automotive industry is leveraging silane-modified adhesion promoters tailored for E-coat and primer-less automotive coatings, ensuring enhanced durability on recycled or composite substrates. Additionally, public-private research programs are channeling significant funding into molecular surface engineering and nanomaterial-based adhesion interfaces, setting new performance benchmarks in chemical bonding efficiency.

The wind energy sector is emerging as a key growth driver, with rising demand for high-durability, weather-resistant adhesion promoters used in turbine blade bonding and repair. Meanwhile, specialty silane producers like Wacker Chemie are optimizing production consistency for rubber and sealant markets, strengthening Europe’s supply security. Through its combination of innovation, policy alignment, and industrial precision, Germany remains the anchor of Europe’s high-performance and sustainable adhesion promoter ecosystem.

Japan’s adhesion promoters market is characterized by unparalleled precision, purity, and performance, supporting critical applications in electronics, semiconductors, and automotive manufacturing. Industry giants such as Shin-Etsu Chemical Co., Ltd. and Nippon Shokubai Co., Ltd. lead global innovation in ultra-high-performance adhesion promoters for display panels, flexible printed circuits, and semiconductor encapsulation.

The nation’s advanced elastomer and composites industry relies on specialized bonding agents designed for high-temperature seals and vibration damping, essential in high-performance machinery. Japan’s automotive sector continues to pioneer lightweight and high-strength bonding technologies, integrating adhesion promoters that enhance durability in aluminum and composite vehicle structures.

Significant growth is also evident in water treatment infrastructure, where chemical- and microbe-resistant adhesion systems improve coating performance for pipelines and storage facilities. Additionally, Japanese firms are developing specialized adhesion promoters for optical fibers, ensuring moisture resistance and mechanical durability in telecommunications. Japan’s strategic R&D investments and global supply chain resilience underpin its leadership in smart, high-purity adhesion systems.

South Korea remains a global hub for high-tech adhesion promoter development, fueled by its leadership in OLED, micro-LED, and advanced display production. The country’s display manufacturers depend on photoresist adhesion promoters and ultra-clean surface modifiers to achieve superior resolution and color precision in next-generation panels.

The EV and energy storage industries are rapidly expanding, driving adoption of adhesion promoters engineered for electrode bonding and thermal interface stability within lithium-ion batteries and ESS modules. The nation’s strong flexible packaging industry is equally reliant on customized adhesion systems that ensure barrier integrity and mechanical performance under extreme stress.

Supported by government R&D initiatives, South Korea is actively developing hydrophobic adhesion promoters for marine coatings and external construction materials—enhancing durability in humid and saline environments. Furthermore, the country’s ongoing autonomous vehicle advancements have created niche applications for precision adhesion in sensors and radar systems, reflecting its deep integration of adhesives in smart mobility innovation.

India’s adhesion promoters industry is accelerating in response to massive infrastructure expansion, industrialization, and policy-driven localization. With billions invested in roads, bridges, and commercial projects, demand for high-performance silane and epoxy adhesion systems is rising, particularly for construction sealants and concrete admixtures.

The automotive manufacturing sector, one of India’s fastest-growing export industries, increasingly depends on adhesion promoters for coatings, rubber bonding, and tire formulations, ensuring enhanced durability under extreme conditions. The government’s ‘Make in India’ initiative has also attracted foreign chemical investments, resulting in local production and R&D centers that reduce reliance on imported specialty chemicals.

In the energy sector, rural electrification and grid expansion have created new opportunities for protective coating adhesion promoters in transformers and power cables. Simultaneously, India’s modern packaging industry, supported by FMCG growth, requires advanced acrylic and polyurethane adhesion solutions for multilayer films and laminates.

France plays a strategic role in Europe’s advanced adhesion promoters landscape, focusing on high-specification aerospace applications and eco-friendly coating technologies. The country’s aerospace and defense leaders are driving R&D into high-temperature-resistant adhesion systems suitable for metal-to-composite bonding in critical structural aircraft components.

French specialty chemical firms, led by Arkema SA, are pioneering thermoplastic composite adhesion technologies, essential for next-generation mobility and recyclability objectives. In parallel, France’s coatings and construction industries are transitioning toward bio-sourced, solvent-free adhesion formulations, complying with stringent EU environmental mandates.

With sustained investment in building renovation and insulation upgrades, France is also witnessing increased consumption of durable, weather-resistant adhesion promoters for high-performance sealants and insulation systems. The strategic directions affirm France’s position as a European leader in sustainable, aerospace-grade, and composite-compatible adhesion promoter solutions.

Adhesion Promoters Market Report Scope

Adhesion Promoters Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$7.5 Billion

|

|

Market Size (2034)

|

$12.5 Billion

|

|

Market Growth Rate

|

5.8%

|

|

Segments

|

By Type (Silanes, Chlorinated Polyolefins (CPOs), Maleic Anhydride, Titanates & Zirconates, Non-Chlorinated Polyolefins, Others), By Substrate (Metals, Plastics & Composites, Glass & Ceramics, Rubber & Elastomers, Wood & Cellulosic Materials, Concrete & Stone), By Application (Paints & Coatings, Adhesives & Sealants, Rubber Compounding, Plastics Modification, Printing Inks, Tapes & Labels), By End-Use Industry (Automotive & Transportation, Construction & Infrastructure, Electrical & Electronics, Packaging, Aerospace & Defense, Consumer Goods & Appliances

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Dow Inc., Evonik Industries AG, Wacker Chemie AG, BASF SE, Momentive Performance Materials Inc., Eastman Chemical Company, Shin-Etsu Chemical Co., Ltd., Arkema SA, NIPPON SHOKUBAI CO., LTD., PPG Industries, Inc., 3M Company, Nouryon, DIC Corporation, Sika AG, Altana AG

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

By Type

- Silanes

- Chlorinated Polyolefins (CPOs)

- Maleic Anhydride

- Titanates & Zirconates

- Non-Chlorinated Polyolefins

- Others

By Substrate

- Metals

- Plastics & Composites

- Glass & Ceramics

- Rubber & Elastomers

- Wood & Cellulosic Materials

- Concrete & Stone

By Application

- Paints & Coatings

- Adhesives & Sealants

- Rubber Compounding

- Plastics Modification

- Printing Inks

- Tapes & Labels

By End-Use Industry

- Automotive & Transportation

- Construction & Infrastructure

- Electrical & Electronics

- Packaging

- Aerospace & Defense

- Consumer Goods & Appliances

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

- Dow Inc.

- Evonik Industries AG

- Wacker Chemie AG

- BASF SE

- Momentive Performance Materials Inc.

- Eastman Chemical Company

- Shin-Etsu Chemical Co., Ltd.

- Arkema SA

- NIPPON SHOKUBAI CO., LTD.

- PPG Industries, Inc.

- 3M Company

- Nouryon

- DIC Corporation

- Sika AG

- Altana AG

*- List not Exhaustive

Research Coverage

This report investigates how adhesion promoters unlock durable bonding between dissimilar materials and accelerate sustainability in coatings, automotive, packaging, and electronics; it consolidates breakthroughs in silane coupling, maleic-anhydride compatibilization, and non-chlorinated polyolefin platforms into decision-ready intelligence. Produced by USDAnalytics, the study delivers analysis reviews of regulatory catalysts, performance trade-offs (corrosion protection, humidity/UV resistance, LSE substrate anchorage), and value-chain moves (capacity shifts, spec-in strategies, cost curves). It highlights emerging green-chemistry formulations and primerless systems that raise conversion efficiency and lifetime TCO, mapping where buyers gain measurable gains in adhesion strength and compliance. By translating lab results into plant-floor outcomes, this report is an essential resource for executives, R&D chemists, sourcing leaders, and application engineers aligning product roadmaps with low-VOC mandates and multi-material manufacturing.

Scope of the study includes-

- By Type: Silanes; Chlorinated Polyolefins (CPOs); Maleic Anhydride; Titanates & Zirconates; Non-Chlorinated Polyolefins; Others.

- By Substrate: Metals; Plastics & Composites; Glass & Ceramics; Rubber & Elastomers; Wood & Cellulosic; Concrete & Stone.

- By Application: Paints & Coatings; Adhesives & Sealants; Rubber Compounding; Plastics Modification; Printing Inks; Tapes & Labels.

- By End-Use: Automotive & Transportation; Construction & Infrastructure; Electrical & Electronics; Packaging; Aerospace & Defense; Consumer Goods & Appliances.

- Geographic Scope: Analysis spans 25+ countries across North America, Europe, Asia Pacific, Latin America, the Middle East & Africa.

- Time Frame: Historic data 2021–2024 and forecasts 2025–2034.

- Companies: Analysis/profiles of 15+ companies.

Deliverables

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.