Coupling Agents Market Outlook 2025–2034: $2.7 Billion to $4.6 Billion at 6% CAGR Driven by Silane Innovation, Green Adhesives, and EV Battery Applications

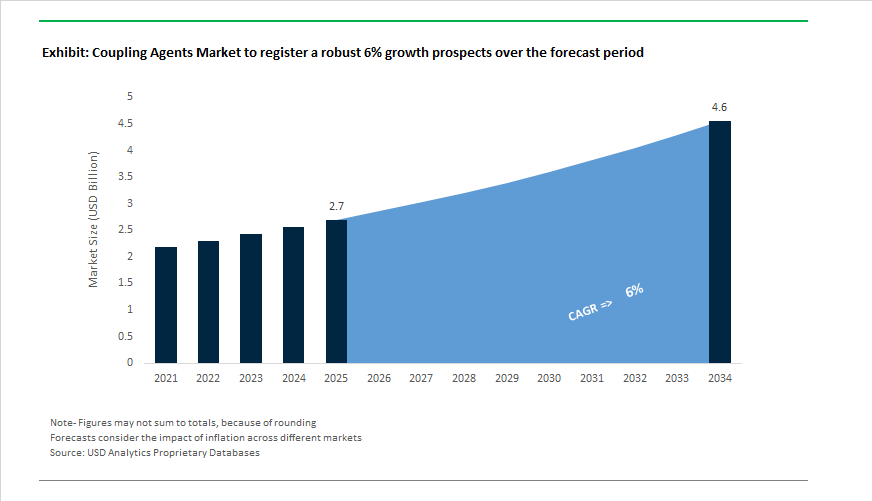

The global Coupling Agents Market is projected to expand from $2.7 billion in 2025 to $4.6 billion by 2034, registering a CAGR of 6%. Market growth is supported by rising demand for silane coupling agents, titanates, zirconates, and multifunctional surface modifiers across automotive composites, electronics encapsulation, EV battery systems, adhesives and sealants, marine coatings, and advanced ceramics. Increasing regulatory pressure to reduce VOC emissions and Scope 3 carbon intensity is accelerating the adoption of eco-friendly silane chemistry and low-carbon production platforms. Integration of coupling agents into high-performance filler systems such as spherical silica, alumina, glass fibers, and battery separator coatings is strengthening their role in structural reinforcement and adhesion optimization.

Strategic consolidation and capacity expansion reshaped competitive positioning during 2024 and 2025. In May 2024, KCC Corporation completed its acquisition of Momentive Performance Materials, strengthening its global presence in silanes and silicones and consolidating R&D efforts for next-generation coupling agents in automotive and electronics markets. In October 2024, Momentive Technologies acquired Sibelco’s spherical alumina and silica business, enhancing its ability to supply surface-treated fillers that require specialized coupling chemistry for dispersion and thermal management applications. In December 2024, Arkema finalized the acquisition of Dow’s laminating adhesives business, integrating advanced coupling agent technologies into its Bostik segment for flexible packaging and industrial bonding. In March 2025, Momentive and Hungpai formed a joint venture to expand high-purity silane production in Asia-Pacific, targeting the regional tire and green-energy sectors. Shin-Etsu announced a $21.3 million expansion at its Akron, Ohio facility in July 2025, part of a broader multi-year investment plan to increase specialty silane capacity.

Product innovation and sustainability initiatives accelerated across adhesives, coatings, and battery systems. In late 2024, Dow launched a new eco-friendly silane portfolio designed to reduce VOC content in adhesive and sealant formulations while maintaining bond durability under REACH and EPA standards. During the same period, Momentive introduced a multifunctional marine silane that integrates corrosion protection within the coupling molecule, simplifying marine coating formulations for high-salinity environments. In October 2025, Arkema highlighted water-based separator coating systems for lithium-ion batteries at K 2025, technologies that rely on advanced coupling agents to maintain mechanical stability and thermal safety. In March 2025, Shin-Etsu transitioned its Rayong, Thailand silane production to biomass-derived renewable energy, responding to global demand for low-carbon Green Silane solutions.

Operational restructuring and distribution optimization defined the 2026 outlook. Wacker Chemie launched its PACE restructuring program in January 2026, targeting €300 million in annual savings while maintaining focus on silicones and silane-based additives for semiconductor and EV applications. Evonik expanded its hydroxyl-terminated polybutadiene production in Marl during 2024 and established a Shanghai facility in 2025, supporting high-performance adhesive systems that incorporate coupling agents for aerospace and advanced composites. In February 2026, Evonik streamlined its North American distribution network, appointing regional specialists to strengthen supply continuity and technical support for coupling agents and coating additives. These developments reflect sustained investment in silane surface modification technologies, renewable production models, adhesive innovation, and EV-driven composite material integration across global industrial value chains.

Trends and Opportunities in the Global Coupling Agents Market

Rapid Shift Toward Functional and Specialty Silanes for High-Performance Composites

- High-temperature and structurally demanding applications are driving a clear shift away from generic silane coupling agents toward aromatic-backbone and secondary amino-functional silanes engineered for thermal stability and controlled cure behavior. In December 2025, Wacker Chemie and SICO Performance Material inaugurated a 2,300 square meter technology center in China dedicated to specialty silane development. The center focuses on organofunctional silanes designed to act as molecular binders in hybrid polymer systems used in electromobility, power engineering, and aerospace structures where standard coupling agents degrade under cyclic thermal stress.

- Parallel advances are visible in secondary amino-functional silanes. Evonik has scaled production of its Dynasylan® 1122 and 1124 grades, which feature symmetric silicon atoms and precisely tuned reactivity. These properties are critical in airframe and advanced composite bonding, where cure kinetics must align with differential thermal expansion between substrates. Such silanes are increasingly specified for applications requiring bond stability at temperatures approaching 250 degrees Celsius for decorative elements and even higher thresholds for structural composite components.

Coupling Agents Tailored for Nanofillers in Electronics and 6G Packaging

- As electronics miniaturization accelerates, coupling agents are playing a decisive role in enabling the dispersion and stabilization of nanoscale fillers used for thermal management and signal integrity. Technical findings reported in August 2025 highlighted polaritonic coupling effects between graphene and boron nitride nanotubes, drawing attention to the need for interfacial chemistries capable of supporting energy transfer at the nanoscale. This has intensified research into coupling agents that can prevent agglomeration while maintaining functional alignment within polymer matrices used in 5G and emerging 6G device packaging, where circuit dimensions are approaching 20 to 30 nanometers.

- In parallel, manufacturers of thermal interface materials are increasingly adopting cationic silane coupling agents to surface-treat high dielectric constant ceramic powders and boron nitride fillers. These agents enable uniform dispersion within polymer matrices, supporting efficient heat dissipation in high-density AI server racks and advanced computing hardware. Importantly, they also preserve electrical insulation properties, a critical requirement as power densities rise and component spacing shrinks in next-generation electronics.

Coupling Agents Enabling Circular and Bio-Based Composite Materials

- Regulatory mandates to increase recycled content in automotive and consumer products are creating strong demand for coupling agents that can compatibilize degraded or chemically heterogeneous materials. In October 2025, BASF demonstrated advanced recycling pathways for Polyamide 6 recovered from end-of-life vehicles. During re-polymerization, specialized coupling agents are applied to restore interfacial bonding and mechanical integrity, enabling recycled polymers to meet the stringent safety and performance requirements specified for Mercedes-Benz chassis components.

- Bio-based composites represent a parallel opportunity. Research published in March 2025 showed that treating natural fibers such as jute and kenaf with maleic anhydride coupling agents increased tensile strength by approximately 35%. The reaction between MAH groups and the cellulose backbone forms fiber cellulose esters, significantly improving adhesion in polylactic acid matrices. This performance uplift is accelerating adoption of bio-composites in sustainable automotive interior panels and lightweight structural components.

Adhesion Promoters for Solid-State Battery Interfaces

- The transition toward solid-state batteries is creating a high-value niche for coupling agents capable of stabilizing interfaces between ceramic electrolytes and lithium-based electrodes. Industry guidelines released in late 2025 emphasized the importance of engineered electrode and electrolyte tandems to reduce interfacial resistance and prevent delamination during repeated charge and discharge cycles. Coupling agents are increasingly incorporated into wet-chemical processing routes to enhance adhesion and mechanical compatibility within oxide-based solid-state battery architectures.

- Functional material leaders such as Shin-Etsu Chemical have developed proprietary surface treatment methods for silicon monoxide anode materials. By using specialty silane coupling agents as interfacial bridges, these processes bond inorganic active particles to polymer binders more effectively. The result is lower internal resistance and reduced mechanical failure during lithiation, supporting higher energy density and longer cycle life in next-generation electric vehicle batteries.

Coupling Agents Market Share and Segmentation Insights

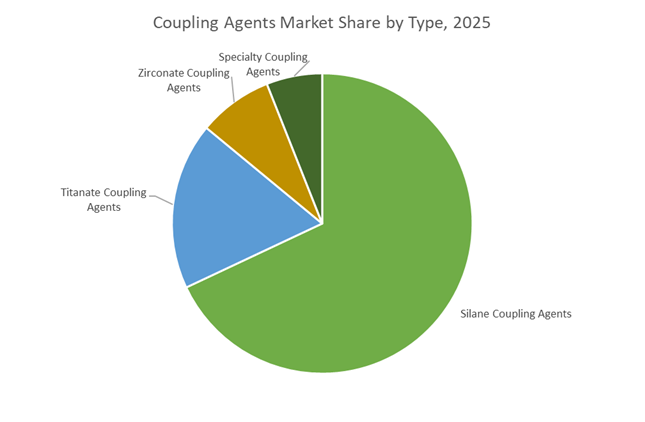

Type-Based Segmentation: Silane Coupling Agents Dominate While Specialty Chemistries Support High-Performance Systems

Silane coupling agents command 68% of global market share in 2025, reflecting unmatched versatility in bonding inorganic fillers to organic polymers across fiberglass composites, tire manufacturing, and adhesive formulations. Their role in enhancing silica-rubber interaction is critical for fuel-efficient tires and lightweight automotive components. Titanate coupling agents hold a meaningful share, valued for improving filler dispersion and reducing viscosity in highly filled plastics, magnetic media, and cable compounds. Zirconate coupling agents address high-temperature applications, offering superior thermal stability in aerospace composites and advanced coatings where silanes may degrade. Specialty coupling agents, including amino- and methacrylate-functional variants, serve niche but growing applications in dental materials, medical devices, and electronic packaging, where tailored interfacial chemistry enables performance gains in miniaturized and high-reliability systems.

End-Use Industry Breakdown: Automotive Leads as Renewables and Electronics Accelerate Adoption

Automotive and transportation account for 32% of coupling agent demand, driven by tire compounding, composite body panels, and under-hood components requiring strong interfacial bonding and heat resistance. Building and construction represent a major secondary segment, utilizing coupling agents in fiber-reinforced concrete, polymer composites, and weather-resistant sealants to enhance durability under environmental exposure. Electrical and electronics applications depend on coupling agents for printed circuit boards, encapsulants, and conductive adhesives, supporting device miniaturization and reliability. Energy and renewable power is a fast-growing market, with coupling agents enabling structural integrity in wind turbine blades, solar modules, and battery systems. Healthcare and medical devices complete the landscape, demanding biocompatible coupling chemistries for dental composites, orthopedic implants, and diagnostic components where material bonding directly impacts patient safety.

Competitive Landscape of the Coupling Agents Market

The Coupling Agents Market is characterized by intense innovation in organofunctional silanes, bio-attributed chemistries, and electronic-grade surface modifiers, with leading players competing on purity, tire performance, adhesives compliance, and EV-driven composites demand.

Momentive leads green tire silane innovation with NXT™, FXP™, and NRX™ technologies

Momentive Performance Materials Inc. is widely recognized as a global leader in silane coupling agents, particularly within automotive rubber and high-performance tire applications. Its NXT™ and FXP™ silane series are industry benchmarks for reducing rolling resistance in green tires, directly supporting fuel efficiency and EV range extension. In February 2025, Momentive formed a strategic joint venture with Jiangxi Hungpai New Material, combining proprietary silane technology with large-scale Asian production capacity. During 2025–2026, it introduced the NRX™ silane range engineered for natural rubber-based truck tires, enhancing durability and wet grip. Strategically, the company divested consumer sealants to prioritize specialty silicones and high-value electronic materials.

Evonik strengthens bio-attributed Dynasylan® portfolio for adhesives and coatings

Evonik Industries AG commands a strong European position in organofunctional silanes through its Dynasylan® brand, widely used as adhesion promoters and surface modifiers in coatings, inks, and composites. A market leader in solvent-free, REACH-compliant silane-modified polymers (SMP), Evonik plays a critical role in the adhesives and sealants sector. In early 2026, the company streamlined its North American distribution network, effective May 2026, to enhance technical responsiveness. Evonik is also accelerating investment in bio-attributed silanes using a mass-balance approach to align with EU 2026 carbon neutrality targets, reinforcing its positioning in sustainable coupling agent chemistry.

Shin-Etsu dominates electronic-grade silanes for 5G and semiconductor packaging

Shin-Etsu Chemical Co., Ltd. differentiates itself through ultra-high-purity electronic-grade silanes essential for advanced semiconductor packaging, 5G infrastructure, and AI-driven microelectronics. Leveraging deep vertical integration from raw silicon to finished coupling agents, Shin-Etsu ensures unmatched batch consistency and contamination control. Its KBM and KBE grades span vinyl, epoxy, and styryl functional silanes tailored for resin modification and specialty medical device applications. With a strategic focus on quality-driven differentiation, the company prioritizes niche high-end segments where chemical stability and reproducibility are mandatory for safety and regulatory compliance.

Dow accelerates organofunctional silane capacity for EV and infrastructure growth

Dow Inc. remains a global titan in coupling agents, particularly for glass-fiber reinforced polymers used in sustainable infrastructure and building applications. Under its 2026 Transform to Outperform initiative, Dow is deploying AI to optimize specialty chemical supply chains and reduce time-to-market for advanced composite binders. In late 2025, it introduced siloxane-alkyd and siloxane-epoxy chemistries delivering superior UV and corrosion resistance in marine and architectural coatings. The company is also expanding organofunctional silane capacity across APAC to support rising EV production, reinforcing its dominance in high-volume industrial coupling agent applications.

Gelest drives niche innovation in life science and aerospace coupling agents

Gelest, Inc., part of Mitsubishi Chemical Group, operates as an innovation-focused specialist in complex silane and metal-organic chemistry. Its SIVATE™ functional silane blends enable advanced surface modification for micro-particles, specialty acrylates, and biomaterials. In early 2026, Gelest digitized its technical library into interactive selection guides, enhancing molecule-specific precision for researchers. The company holds a strong position in life science tools, supplying coupling agents for DNA array technology, medical devices, and contact lens monomers. Acting as an R&D partner for aerospace and microelectronics firms, Gelest excels in custom, proprietary coupling agent development.

United States: Supply Chain Consolidation and EV-Focused Coupling Innovation

The United States coupling agents industry in 2025 is undergoing a structural reset driven by consolidation, trade policy, and rapid electrification of transport. Evonik Industries announced the phased closure of its silica production facilities in New York and Maryland, scheduled for mid-2025 and mid-2026. This decision reflects a deliberate shift toward scale efficiency and tighter integration with high-growth downstream partners in tires, adhesives, and advanced composites. Rather than capacity contraction, the move signals capital redeployment toward higher-margin silane coupling systems that deliver superior interfacial bonding and durability in performance-critical applications. Parallel to this, tariff measures introduced through 2025, with effective rates reaching 25 to 30% on imported chemical precursors, have materially altered procurement strategies. U.S. manufacturers are accelerating vertical integration and localized sourcing of silicon-derived inputs to stabilize margins and reduce exposure to import volatility.

Technology-led differentiation is most visible in electric vehicle platforms. At The Battery Show North America 2025, Wacker Chemical Corporation showcased silane-terminated polyether based thermally conductive adhesive systems engineered for cell-to-pack and cell-to-chassis architectures. These coupling-enabled systems improve adhesion between dissimilar substrates while maintaining thermal conductivity and vibration resistance. Regulatory pressure is reinforcing sustainable reformulation. In response to tighter U.S. EPA proposals on hazardous substances, Evonik Industries introduced PFAS-free TEGO® PPA processing additives for food-contact and packaging polymers. At the R&D level, leading U.S. firms are embedding AI-driven digital twin modeling into 2026 development pipelines, allowing predictive selection of coupling agent chemistries for polymer nanocomposites without exhaustive physical trials. Sustainability credentials are becoming procurement-critical, with Hexion and Polynt securing ISCC PLUS certification in late 2025, validating the use of bio-circular raw materials across coupling agent and resin production.

China: Volume Leadership and Advanced Offshore Coupling Systems

China remains the global epicenter for silica-silane coupling agent consumption and production, underpinned by scale-driven industrial policy and infrastructure expansion. As of 2025, the national Green Tire initiative continues to mandate low rolling resistance and high energy efficiency for commercial vehicle fleets, reinforcing China’s dominance in silica-silane coupling agents used in tire reinforcement. This policy-driven demand sustains large-volume production while pushing incremental improvements in coupling efficiency and abrasion resistance. Beyond tires, offshore and renewable infrastructure is emerging as a high-value application frontier. In September 2025, Shanghai Electric launched Ulstein-designed Service Operation Vessels equipped with advanced coupling-agent-enabled polymer systems engineered to withstand C5-M marine corrosion environments.

Material innovation is also accelerating through cross-sector collaboration. PETRONAS, working with Chinese research partners, commercialized ProShield+, a graphene-silane hybrid coating that addresses micro-cracking and delamination in offshore oil and gas assets. This reflects a broader trend toward hybrid coupling chemistries that combine silane bonding efficiency with nanomaterial reinforcement. Capacity expansion remains aggressive. Throughout 2025, INEOS Composites and AOC expanded manufacturing footprints in China to support rising demand for silane-enabled adhesives, moisture barriers, and encapsulation systems in semiconductors and advanced electronics. China’s coupling agent ecosystem is therefore evolving from pure volume leadership toward multifunctional, high-reliability interfacial technologies.

India: Infrastructure Durability and Process-Driven Demand

India’s coupling agents industry is increasingly shaped by regulatory reform, infrastructure longevity goals, and industrial water management challenges. A notable policy development in July 2025 came from the Central Electricity Regulatory Commission, which issued a directive for phased implementation of Market Coupling in the power sector, with the Day-Ahead Market scheduled for rollout in January 2026. While focused on electricity markets, this reform is indirectly stimulating grid-scale infrastructure upgrades, increasing demand for silane-modified sealants, coatings, and composite interfaces used in substations and transmission assets.

Environmental compliance is a direct driver of coupling chemistry adoption. In 2025, the Central Pollution Control Board enforced stricter Zero Liquid Discharge mandates across pharmaceutical and textile clusters. This has sharply increased demand for coupling agents that remain stable under high total dissolved solids conditions, particularly in membrane filtration systems and industrial coatings exposed to aggressive effluents. Infrastructure policy further reinforces long-term demand. The 2025 update of the PM Gatishakti National Master Plan explicitly prioritized silane-modified sealants and Migrating Corrosion Inhibitor systems in coastal bridge projects to achieve 100-year service life targets. Collectively, these factors position coupling agents as critical enablers of durability, compliance, and lifecycle performance across India’s infrastructure and process industries.

Germany: Circular Plastics and Cost-Driven Industrial Restructuring

Germany’s coupling agents market is defined by circular economy mandates and structural cost optimization. At K 2025, Evonik Industries presented its circular plastics roadmap through the TEGO® CYCLE additive portfolio. These coupling-agent-based systems are designed to compatibilize contaminated and mixed plastic waste streams, enabling the production of high-quality recyclates suitable for demanding applications. This approach reflects Germany’s broader policy emphasis on material recovery, polymer compatibility, and closed-loop value chains, where coupling agents play a pivotal role in restoring mechanical integrity to recycled polymers.

At the same time, cost pressures from sustained high energy prices are forcing operational restructuring. In late 2025, Wacker Chemie AG launched a comprehensive cost-efficiency program targeting production and administrative processes, with full implementation expected by Q1 2026. The initiative is designed to preserve competitiveness in silane and coupling agent production while continuing to invest in high-performance and sustainable chemistries. Germany’s market trajectory therefore combines aggressive circularity goals with disciplined cost management, reinforcing its position as a technology-driven, regulation-aligned hub for advanced coupling agents.

Comparative Snapshot: Country-Level Strategic Orientation in the Coupling Agents Industry

Coupling Agents Market County Level Snapshot

|

Country

|

Primary Strategic Driver

|

Key Application Areas

|

Direction of Coupling Agent Innovation

|

|

United States

|

Tariffs and EV electrification

|

EV batteries, packaging, nanocomposites

|

PFAS-free, AI-optimized, bio-circular

|

|

China

|

Green Tire policy and offshore scale

|

Tires, offshore wind, electronics

|

Silane hybrids, graphene-silane systems

|

|

India

|

Infrastructure durability and ZLD

|

Bridges, membranes, industrial coatings

|

High-TDS-stable, silane-modified systems

|

|

Germany

|

Circular economy and cost control

|

Recycled plastics, industrial polymers

|

Compatibilizers for recyclates, energy-efficient production

|

Coupling Agents Market Report Scope

Coupling Agents Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$2.7 Billion

|

|

Market Size (2034)

|

$4.6 Billion

|

|

Market Growth Rate

|

6%

|

|

Segments

|

By Type (Silane Coupling Agents, Titanate Coupling Agents, Zirconate Coupling Agents, Specialty Coupling Agents), By Technology (Solvent-Based, Water-Borne, 100 Percent Solids and Powder), By Application (Rubber and Plastics, Adhesives and Sealants, Paints and Coatings, Fiberglass and Composites, Electronics and Semiconductors), By End-Use Industry (Automotive and Transportation, Building and Construction, Electrical and Electronics, Healthcare and Medical Devices, Energy and Renewable Power)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Evonik Industries AG, Dow Inc., Wacker Chemie AG, Shin-Etsu Chemical Co. Ltd., Momentive Performance Materials Inc., Arkema S.A., 3M Company, Huntsman Corporation, Gelest Inc., Jingzhou Jianghan Fine Chemical Co. Ltd., Nouryon Chemicals Holding B.V., Kenrich Petrochemicals Inc., WD Silicone Co. Ltd., Hubei Bluesky New Material Inc., Sika AG

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Coupling Agents Market Segmentation

By Type

- Silane Coupling Agents

- Titanate Coupling Agents

- Zirconate Coupling Agents

- Specialty Coupling Agents

By Technology

- Solvent-Based

- Water-Borne

- 100% Solids and Powder

By Application

- Rubber and Plastics

- Adhesives and Sealants

- Paints and Coatings

- Fiberglass and Composites

- Electronics and Semiconductors

By End-Use Industry

- Automotive and Transportation

- Building and Construction

- Electrical and Electronics

- Healthcare and Medical Devices

- Energy and Renewable Power

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in Coupling Agents Industry

- Evonik Industries AG

- Dow Inc.

- Wacker Chemie AG

- Shin-Etsu Chemical Co. Ltd.

- Momentive Performance Materials Inc.

- Arkema S.A.

- 3M Company

- Huntsman Corporation

- Gelest Inc.

- Jingzhou Jianghan Fine Chemical Co. Ltd.

- Nouryon Chemicals Holding B.V.

- Kenrich Petrochemicals Inc.

- WD Silicone Co. Ltd.

- Hubei Bluesky New Material Inc.

- Sika AG

*- List not Exhaustive