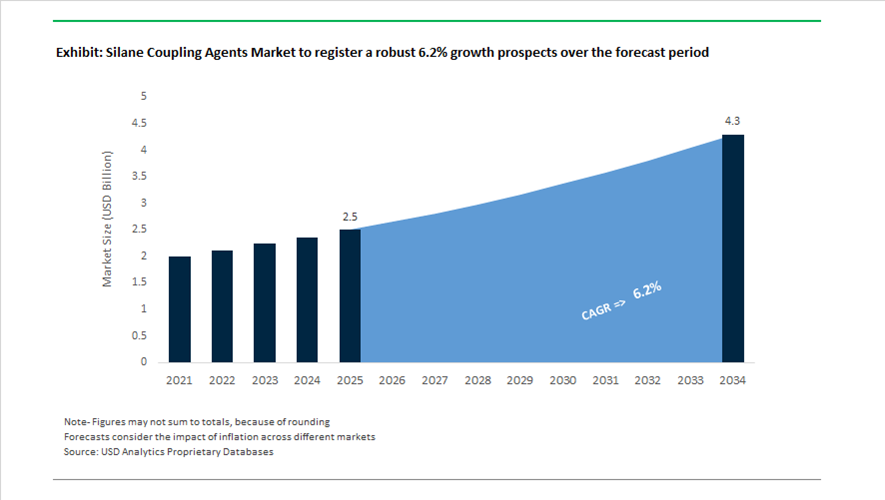

Silane Coupling Agents Market Valuation 2025–2034: $2.5 Billion to $4.3 Billion at 6.2% CAGR Backed by Green Tires, Electronics, and Low-VOC Coatings

The global silane coupling agents market is valued at $2.5 billion in 2025 and is projected to reach $4.3 billion by 2034, registering a CAGR of 6.2%. Growth is driven by expanding demand across rubber reinforcement, green tire manufacturing, high-performance coatings, adhesives and sealants, semiconductor materials, lithium-ion battery coatings, and advanced composite applications. Silane coupling agents play a critical role in improving interfacial bonding between inorganic fillers and organic polymers, enhancing tensile strength, abrasion resistance, moisture resistance, and thermal stability. Rising regulatory pressure on volatile organic compound emissions, increasing adoption of fuel-efficient tires, and growth in new energy vehicle production are structurally reinforcing long-term demand for sulfur silanes, amino silanes, vinyl silanes, and epoxy-functional silanes.

In April 2024, KCC Corporation completed its acquisition of Momentive Performance Materials, consolidating a significant portion of global silane and silicone capabilities under one group. The acquisition strengthened R&D depth in advanced electronics materials and automotive silane technologies. Throughout 2024, Shin-Etsu Chemical expanded its functional materials portfolio with long-chain spacer-type silanes designed to increase hydrophobicity and flexibility in composite filler surface treatments. These developments align with rising demand for lightweight composite materials in automotive and construction applications, where performance optimization at the molecular interface directly influences durability and lifecycle performance.

Capacity expansion and regional localization intensified during 2025. In March 2025, Momentive and Hungpai formed a joint venture to expand silane production capacity in Asia, focusing on high-performance sulfur silanes for green tire applications. In May 2025, Wacker Chemie commissioned new specialty silane production lines at its Zhangjiagang site in China to serve electronics and New Energy Vehicle sectors requiring high-purity silanes. In mid-2025, Shin-Etsu Chemical acquired a specialized European silane manufacturer to establish localized supply for sustainable construction and automotive materials. In October 2025, Evonik inaugurated its Alu5 specialty hub in Yokkaichi, Japan, producing silane-treated surface modifiers essential for lithium-ion battery coatings and semiconductor fabrication. In late 2025, Momentive introduced a new portfolio of low-VOC and eco-friendly silane coupling agents tailored to EU and North American environmental compliance standards.

In January 2026, Evonik launched TEGO® Dispers 695, a hyperdispersant utilizing advanced silane chemistry to optimize pigment wetting in radiation-curing and UV ink systems. The innovation targets high-performance coatings and printing applications where dispersion stability and curing efficiency are critical. In early 2026, Momentive finalized a $30 million expansion at its Leverkusen site in Germany to increase production of NXT silanes used in low rolling resistance tire compounds. These silanes enable tire manufacturers to improve fuel efficiency while maintaining wet grip performance. In January 2026, Dow implemented a global 5%–10% price adjustment across its high-performance building silane portfolio, reflecting higher raw material and environmental compliance costs associated with ultra-high purity silane production. These strategic investments, product innovations, and pricing recalibrations underscore how sustainability mandates, electric mobility growth, semiconductor scaling, and advanced coatings technology are shaping the silane coupling agents market trajectory through 2034.

Key Trends and High-Value Opportunities Shaping the Global Silane Coupling Agents Market

EV-Specific Green Tire Formulations Accelerating Silica–Silane Adoption

The global shift toward electric mobility is redefining tire material science and positioning silane coupling agents as a core performance enabler rather than a formulation additive. Electric vehicles impose fundamentally different mechanical and efficiency requirements on tires, including up to 30% lower rolling resistance to extend driving range and significantly higher torque resistance to manage instant acceleration. These demands have triggered a structural move away from carbon black fillers toward high-dispersion silica systems, where sulfur-functional silane coupling agents are essential to achieve strong rubber–filler interaction and minimize energy loss.

Industry assessments in early 2025 indicate that the EV tire segment is on track to expand from approximately $4.18 billion in 2025 to more than $16.9 billion by 2032, creating a sustained demand pipeline for advanced silanes. Leading tire manufacturers such as Continental and Michelin have accelerated sustainable materials roadmaps targeting over 40% renewable or recycled content by 2030. Achieving these targets while preserving abrasion resistance and tread life relies heavily on optimized silica–silane bonding chemistry. At the regulatory level, EU and APAC tire labeling regimes enforced through 2025 have made Class A fuel efficiency ratings contingent on superior rolling resistance performance, further embedding high-performance sulfur silanes as a baseline requirement rather than a premium upgrade.

Infrastructure Modernization Driving Silane-Enhanced Composite Adoption

Public infrastructure renewal programs are emerging as a parallel demand engine for silane coupling agents, particularly through the adoption of fiber-reinforced polymer composites in bridge rehabilitation and coastal protection. In these applications, silanes function as the mandatory adhesion promoter that stabilizes the interface between hydrophilic fibers and organic resin matrices, preventing delamination under moisture and thermal stress.

In the United States, the U.S. Department of Transportation has allocated more than $27 billion under the Bridge Formula Program by late 2025, targeting repairs across roughly 15,000 bridges. Many of these projects are incorporating FRP rebar and composite wraps, where silane coupling agents create hydrophobic barriers that preserve bond strength in wet and saline environments. A similar policy-driven adoption trend is evident in India under the National Infrastructure Pipeline, where 2025 public works directives increasingly specify silane-modified anti-corrosive coatings for marine and urban assets. These silane-coupled systems improve coating hardness to 4H levels and materially enhance impedance, extending asset life cycles and protecting large-scale public investments.

High-Stability Silanes for AI and HPC Thermal Interface Materials

The rapid expansion of artificial intelligence workloads and high-performance computing is pushing electronic systems toward a thermal ceiling, creating a premium opportunity for advanced silane chemistries in thermal interface materials. Modern GPUs, optical transceivers, and power electronics operate at junction temperatures exceeding 175 degrees Celsius, requiring TIMs with extreme thermal conductivity and long-term stability. In these formulations, silanes are critical for chemically bonding high-load conductive fillers such as alumina and boron nitride into silicone matrices without compromising viscosity or reliability.

In October 2025, Henkel commercialized Loctite TCF 14001, a liquid TIM delivering 14.5 W per meter-kelvin thermal conductivity for 800G and 1.6T AI optical transceivers. This product highlights growing demand for amino and epoxy silanes capable of sustaining high filler loading and thermal cycling. As AI servers and EV power electronics increasingly transition to silicon carbide MOSFETs, the TIM market is projected to approach $14 billion by 2035, creating a substantial addressable market for next-generation, high-temperature silane coupling agents.

Hydrolysis-Resistant Silanes for Advanced Medical Device Coatings

The medical devices sector presents a differentiated opportunity for silane coupling agents engineered for long-term performance in moisture-rich and saline biological environments. Conventional silanes often fail in these conditions due to premature hydrolysis, leading to adhesion loss and device degradation. In response, chemical innovators are advancing long-chain, multifunctional, and dipodal silane architectures that form denser siloxane networks and deliver superior hydrolytic stability.

By late 2025, Shin-Etsu expanded its portfolio of dipodal silanes designed for medical-grade silicone adhesives used in wearable sensors and diagnostic equipment. These formulations are particularly effective on challenging substrates such as polycarbonate and specialty metals common in 3D-printed implants. Studies published in 2025 demonstrate that silane-coupled composite coatings can reduce corrosion current density by several orders of magnitude, positioning hydrolysis-resistant silanes as a critical material enabler for the next generation of implantable and wearable medical electronics.

Silane Coupling Agents Market Share and Segmentation Insights

Sulfur-Containing Silanes Lead Market Demand Driven by Green Tire Manufacturing

Sulfur-containing silanes accounted for 32.80% of the silane coupling agents market in 2025, reflecting their essential role in silica-reinforced rubber compounding used in tire manufacturing. Compounds such as tetrasulfide and disulfide silanes act as coupling agents that chemically bond silica fillers to rubber polymers, improving mechanical strength and energy efficiency in tire tread formulations. This coupling reaction enables the production of low rolling resistance tires, which enhance vehicle fuel efficiency and reduce carbon emissions. A major 2025 industry driver is the continued push for fuel-efficient vehicle technologies and stricter global fuel economy standards, which has accelerated the adoption of silica-filled tire compounds. These formulations rely heavily on sulfur silanes to maintain optimal polymer-silica interaction and tire durability performance.

Rubber & Tires Sector Drives Global Consumption of Silane Coupling Agents

Rubber and tire manufacturing represents the largest end-use industry in the silane coupling agents market, accounting for 38.60% of global consumption in 2025 due to the large-scale production of silica-reinforced tire compounds. Silane coupling agents enhance the bonding between inorganic silica fillers and organic rubber polymers, improving tire durability, wet traction performance, and rolling resistance characteristics. As tire manufacturers continue to adopt silica-based tread formulations, the demand for specialized silane systems continues to increase. A key 2025 industry trend is the growing penetration of silica-filled tire technologies across both passenger and commercial vehicle segments. Advanced silane formulations are being developed for specific polymer systems such as styrene-butadiene rubber and butadiene rubber, enabling optimized tire processing and enhanced overall tire performance.

Silane Coupling Agents Market Competitive Landscape

The 2026 silane coupling agents market is shaped by EV-driven demand, green tire innovation, and semiconductor-grade purity requirements. Industry leaders are advancing sulfur-functional and amino silanes, waterborne VOC-compliant systems, and localized production strategies to support polymer composites, electronics, and sustainable infrastructure applications.

Evonik accelerates PFAS-free silane innovation and EV tire efficiency with sulfur-functional Si 291®

Evonik Industries AG maintains a leadership position in high-performance silane coupling agents through its Dynasylan® and Protectosil® portfolios. The company reported 2025 adjusted EBITDA of €1.874 billion and projects €1.7–€2.0 billion in 2026, reflecting strong specialty additives demand. Its PFAS-free Protectosil ECO-TRETE® ANTIGRAFFITI solution aligns with tightening environmental regulations. The introduction of Si 291®, a sulfur-functional silane, enhances silica dispersion in green tires, reducing rolling resistance and improving EV range. Operational restructuring via SYNEQT separation sharpens focus on specialty silanes and semiconductor chemicals. Strategic alignment with sustainable construction and mobility trends strengthens its market dominance.

Shin-Etsu expands silane capacity and semiconductor-grade integration with long-chain spacer innovation

Shin-Etsu Chemical is strengthening its dominance through a ¥80 billion investment cycle, achieving 1.5x capacity expansion across Japan and Thailand. The company is scaling long-chain spacer silanes that enhance hydrophobicity and flexibility in automotive electronics and PCB coatings. Renewable energy integration in Thailand supports low-carbon silane production for global OEM supply chains. Its vertical integration ensures consistent supply of ultra-high purity silanes for ALD and sub-3nm semiconductor fabrication. Advanced silicone and coupling agent technologies position Shin-Etsu at the core of AI-driven electronics demand. Focus on high-reliability materials reinforces its leadership in electronics-grade silanes.

Dow advances low-VOC waterborne silanes with AI-driven manufacturing and infrastructure applications

Dow Inc. is executing its Transform to Outperform initiative, targeting a $2 billion EBITDA uplift through AI-enabled process optimization. The company is prioritizing low-VOC, waterborne silane coupling agents for sustainable construction and urban infrastructure. Its silanes and siliconates are widely deployed in Sponge City projects, enhancing durability and water repellency. The Shanghai Cooling Science Studio integrates silane-modified materials for advanced thermal management in AI and data center applications. With 2025 sales of approximately $40 billion, Dow leverages global scale to ensure supply reliability. Strategic investments support high-growth coatings, adhesives, and electronics segments.

Momentive strengthens tire and wind energy segments with low-emission NXT™ silanes and amino-functional innovations

Momentive Performance Materials is advancing high-performance silane technologies for tire reinforcement and renewable energy composites. Its NXT Z™ silanes reduce ethanol emissions during tire manufacturing, supporting Euro 7 compliance and green mobility goals. Amino-functional silanes enhance glass fiber bonding in wind turbine blades, improving durability and fatigue resistance. The Nanjing facility serves as a hub for electronic-grade silanes, supporting APAC semiconductor growth. Silquest™ products enable silane-modified polymers that replace isocyanates in construction adhesives. Focus on interface engineering strengthens its role in aerospace, EV, and infrastructure applications.

Wacker leverages integrated silicon-to-silane value chain and GENIOSIL® adhesives for high-performance applications

Wacker Chemie AG maintains a competitive edge through full vertical integration from silicon to silanes, ensuring feedstock security amid trichlorosilane volatility. Its GENIOSIL® STP-E technology leads in high-performance adhesive systems, offering primerless bonding and superior durability. Innovation in silane creams and emulsions enhances penetration for construction and heritage preservation applications. The company is advancing silazanes with >99.9% purity for EUV lithography and semiconductor processes. Stable supply chains and advanced R&D align with EU Chips Act requirements. Wacker’s portfolio supports both construction chemicals and high-end electronics markets.

Gelest drives niche innovation with dipodal silanes and nanotechnology-enabled surface modification solutions

Gelest, part of Mitsubishi Chemical Group, is a key innovator in specialty silane coupling agents for microelectronics and biomedical applications. The company is scaling production of cyclic aza-silanes and azido-silanes for nanoscale surface engineering. Dipodal silanes offer up to 100,000x greater hydrothermal stability, making them critical for medical implants and dental composites. Expanded UV-curable silanes support optical coatings in AR/VR devices, delivering high clarity and scratch resistance. With a portfolio of over 3,000 silicon-based compounds, Gelest enables custom synthesis for advanced R&D. Its focus on high-complexity applications positions it as a leader in next-generation silane technologies.

China: Integrated Scale, Regulatory Push, and Electronics-Led Purity Upgrades

China has consolidated its role as the global volume anchor for silane coupling agents by tightly integrating silicon metal, chlorosilane intermediates, and downstream functional silanes within domestic supply chains. Large producers such as Hubei Jianghan New Materials have expanded amino- and sulfur-functional silanes to serve the country’s fast-growing green tire ecosystem, where silica–silane systems are now standard for rolling-resistance reduction. Technology advancement accelerated in September 2025 at ASE China with the debut of Alpha³ silane technology, enabling rapid moisture curing without tin catalysts. This shift is material for China’s eco-friendly adhesives market, as it simultaneously improves cure speed and aligns with tightening chemical safety expectations.

Policy has been a decisive catalyst. The Ministry of Ecology and Environment has accelerated the phase-out of high-VOC solvent-borne coupling agents, triggering a reported 90% year-on-year rise in R&D investment for water-borne silane sol-gel systems. Parallel investments in Jiangsu and Zhejiang are scaling semiconductor-grade silane precursors to reduce import dependence for encapsulation materials used in 3 nm chip production. Demand is also broadening across energy applications, with methacryloxy silanes increasingly specified for offshore wind turbine blades requiring long-term hydrolytic stability. Targeted subsidies under the “Specialized and Sophisticated” enterprise program are further steering manufacturers toward ultra-high-purity grades for aerospace and advanced electronics.

Germany: Smart Materials Integration and Lifecycle Transparency

Germany’s silane coupling agents market is being reshaped by integration across silica, silanes, and downstream applications, particularly for electric vehicles and infrastructure durability. Effective January 1, 2025, Evonik launched its Smart Effects unit, merging its Silica and Silanes businesses into a 3,500-employee platform focused on molecular-level optimization for battery materials. Product innovation continues to emphasize tin-free systems. At the European Coatings Show 2025, Wacker Chemie presented GENIOSIL STP-E 140 and 340, silane-terminated polymers engineered with alpha and gamma silyl architectures to deliver high elastic recovery in sealants without organotin catalysts.

Sustainability benchmarking has become a competitive differentiator. Environmental Product Declarations introduced for the PROTECTOSIL line in late 2025 have raised expectations for lifecycle transparency in construction chemicals. Regulatory pressure from ECHA scrutiny of epoxy-functional silanes has accelerated adoption of Evonik’s next-generation VPS SIVO adhesion promoters, designed to replace legacy GLYMO chemistries. In parallel, water-borne silane binders such as SIVO 140 are gaining share in marine and bridge coatings by cutting VOC emissions by more than 90% versus solvent systems, aligning performance durability with compliance.

Japan: Precision Chemistry for Batteries, Memory, and Mobility

Japan’s silane coupling agents market is defined by precision manufacturing and cross-industry collaboration. In October 2025, Evonik inaugurated its Alu5 fumed alumina plant in Yokkaichi, optimized for surface-modified alumina produced with advanced silane treatments for lithium-ion battery separators. This investment underscores Japan’s role in supplying high-reliability materials for energy storage. At the same time, Shin-Etsu Chemical expanded its KBM and KBE series with ultra-high-purity epoxy silanes tailored for HBM3e encapsulation, reflecting the tight coupling between silane chemistry and advanced semiconductor packaging yields.

Collaborative development is translating into downstream performance gains. Joint R&D between Japanese tire manufacturers and silane suppliers culminated in the 2026 rollout of ultra-low rolling resistance tires using mercapto-functional silanes, delivering an estimated 5% EV range improvement. Policy is reinforcing sustainability alignment. New 2026 “Circular Chemicals” guidelines from METI favor silanes using bio-based ethanol in alkoxy groups. Market expansion is also evident in transportation infrastructure, with scaled production of p-styryltrimethoxysilane for glass-fiber reinforced plastics used in high-speed rail applications.

United States: Reshoring, Clean Energy Demand, and Compliance-Driven Reformulation

The U.S. silane coupling agents market is undergoing strategic reshoring as suppliers buffer against trade volatility and regulatory change. Following 2025 tariff updates, producers including Momentive and Dow accelerated vertical integration along the Gulf Coast to localize silane production. Momentive’s 2025 integration of acquired silicone assets has strengthened domestic supply of NXT silanes for North America’s green tire programs, reducing exposure to overseas intermediates.

Energy transition priorities are expanding application breadth. The Department of Energy awarded 2025 grants to develop silane-based surface treatments that improve moisture resistance in perovskite solar cells, addressing a core durability barrier for outdoor deployment. Regulatory enforcement under updated TSCA provisions has also favored labeling-free silane adhesion promoters in industrial adhesives, simplifying compliance for formulators. Infrastructure investment remains a stable demand pillar, with Dow expanding DOWSIL and XIAMETER portfolios to include moisture-scavenging silanes engineered for high-performance architectural glazing systems.

India: Infrastructure Pull and Domestic Capability Building

India has emerged as the fastest-growing APAC market for silane coupling agents in 2025, driven by domestic manufacturing policy and infrastructure expansion. The Make in India initiative has stimulated demand across automotive, electronics, and cable sectors, while national highway and bridge programs are lifting consumption of silane-siloxane water repellents used to mitigate chloride-induced corrosion in reinforced concrete. Local production capacity has expanded, with domestic firms initiating vinyl and amino silane manufacturing to supply the XLPE-insulated wire and cable industry, reducing reliance on imports.

Sustainability and skills development are reinforcing long-term adoption. The Indian Rubber Board’s 2026 roadmap emphasizes a transition to silica–silane tire systems to meet upcoming fuel-efficiency labeling norms. To support technical assimilation, “Silane Excellence Centers” established in Pune and Chennai in 2025 are training formulators on advanced coupling agent integration across adhesives, elastomers, and composites. This combination of infrastructure pull, policy alignment, and capability building positions India as a structurally attractive growth market for silane suppliers.

Comparative Snapshot: Silane Coupling Agents by Country

Silane Coupling Agents Market County Level Snapshot

|

Country

|

Primary Demand Driver

|

Technology Focus

|

|

China

|

Integrated manufacturing and regulation

|

Water-borne, UHP, and semiconductor-grade silanes

|

|

Germany

|

EV materials and compliance

|

Tin-free, lifecycle-assessed silanes

|

|

Japan

|

Precision electronics and batteries

|

Ultra-high-purity and functional specialty silanes

|

|

United States

|

Reshoring and clean energy

|

Labeling-free, energy-grade surface treatments

|

|

India

|

Infrastructure and localization

|

Vinyl, amino, and siloxane water repellents

|

Silane Coupling Agents Market Report Scope

Silane Coupling Agents Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$2.5 Billion

|

|

Market Size (2034)

|

$4.3 Billion

|

|

Market Growth Rate

|

6.2%

|

|

Segments

|

By Product Type (Sulfur-Containing Silanes, Amino Silanes, Vinyl Silanes, Epoxy Silanes, Methacryloxy Silanes, Other Functional Silanes), By Form (Liquid, Powder, Water-Borne Sol-Gels), By Function (Coupling Agents, Adhesion Promoters, Surface Modifiers, Moisture Scavengers, Crosslinking Agents), By End-Use Industry (Rubber & Tires, Adhesives & Sealants, Paints & Coatings, Composites, Electrical & Electronics, Other Industrial Applications)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Evonik Industries AG, Shin-Etsu Chemical Co. Ltd., Momentive Performance Materials Inc., Dow Inc., Wacker Chemie AG, Hubei Jianghan New Materials Co. Ltd., Jiangxi Chenguang New Materials Co. Ltd., Gelest Inc., SCA Specialty Chemicals, JNC Corporation, Arkema SA, Hung Pai Chemical Co. Ltd., Nantong Chenguang Chemical, WD Silicone Co. Ltd., KCC Corporation

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Silane Coupling Agents Market Segmentation

By Product Type

- Sulfur-Containing Silanes

- Amino Silanes

- Vinyl Silanes

- Epoxy Silanes

- Methacryloxy Silanes

- Other Functional Silanes

By Form

- Liquid

- Powder

- Water-Borne Sol-Gels

By Function

- Coupling Agents

- Adhesion Promoters

- Surface Modifiers

- Moisture Scavengers

- Crosslinking Agents

By End-Use Industry

- Rubber & Tires

- Adhesives & Sealants

- Paints & Coatings

- Composites

- Electrical & Electronics

- Other Industrial Applications

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in Silane Coupling Agents Industry

- Evonik Industries AG

- Shin-Etsu Chemical Co. Ltd.

- Momentive Performance Materials Inc.

- Dow Inc.

- Wacker Chemie AG

- Hubei Jianghan New Materials Co. Ltd.

- Jiangxi Chenguang New Materials Co. Ltd.

- Gelest Inc.

- SCA Specialty Chemicals

- JNC Corporation

- Arkema SA

- Hung Pai Chemical Co. Ltd.

- Nantong Chenguang Chemical

- WD Silicone Co. Ltd.

- KCC Corporation

*- List not Exhaustive