Semiconductor Chemical Market Valuation 2025–2034: $47 Billion to $148.1 Billion at 13.6% CAGR Fueled by AI, EUV Lithography, and Regional Fab Investments

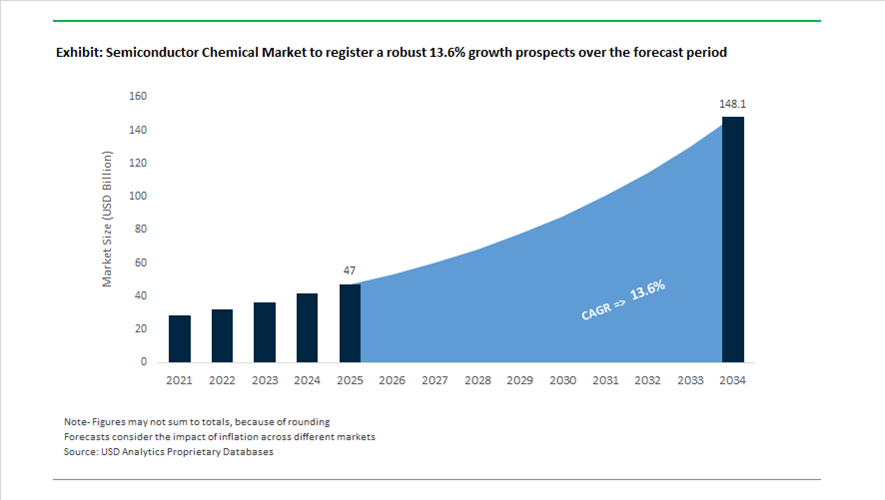

The global semiconductor chemical market is valued at $47 billion in 2025 and is projected to reach $148.1 billion by 2034, expanding at a robust CAGR of 13.6%. This acceleration reflects structural demand from advanced logic, memory scaling below 5nm nodes, high-bandwidth memory (HBM), chiplet integration, silicon carbide (SiC) power devices, and AI data center infrastructure. Semiconductor chemicals including CMP slurries, photoresists, specialty gases, wet chemicals, advanced dielectric materials, wafer cleaning agents, and electronic-grade polymers are becoming increasingly performance-critical as device architectures shift toward EUV lithography, gate-all-around (GAA) transistors, and heterogeneous packaging.

In June 2024, Shin-Etsu Chemical introduced an excimer laser-based dual damascene manufacturing method for semiconductor package substrates. This technology eliminates photoresist in back-end processing, reducing material consumption and lowering chiplet assembly costs. In August 2024, ON Semiconductor announced a $2 billion investment in a new Czech Republic plant while expanding capacity in South Korea, with a strategic focus on silicon carbide chemicals and power modules. These developments reflect rising capital expenditure in compound semiconductor materials aligned with EV power electronics and energy-efficient data centers.

Throughout 2025, structural portfolio realignments and capacity expansions reshaped competitive positioning. In April 2025, the MAVNU consortium acquired hubergroup and later announced a production realignment to expand high-value semiconductor chemical output for European and Asian markets. In July 2025, Air Liquide committed €250 million to build ultra-pure nitrogen, hydrogen, and argon production units in Dresden, Germany under the Silicon Saxony cluster. The facility, operational by 2027, directly supports advanced node wafer fabrication requiring ultra-high purity electronic gases. In November 2025, DuPont completed the separation of its electronics division into Qnity Electronics, Inc., enabling focused investment in CMP pads, slurries, advanced dielectric materials, and semiconductor process chemistries. The same month, Entegris opened a 135,000-square-foot Center of Excellence in Colorado Springs, supported by $75 million in CHIPS Act funding, restoring domestic FOUP manufacturing and expanding advanced liquid filtration systems for sub-5nm fabrication.

In December 2025, Merck KGaA inaugurated its €500 million Semiconductor Solutions megasite in Kaohsiung, Taiwan, covering 150,000 m² and scheduled for mass production of thin-film materials and specialty gases in 2026. In November 2025, Fujifilm completed a 13 billion yen expansion at its Shizuoka facility, deploying AI-driven particle inspection systems tailored for EUV and PFAS-free photoresists. At Semicon India 2025, Fujifilm also announced plans to establish its first semiconductor materials plant in Gujarat, signaling supply chain diversification beyond East Asia. In February 2026, Henkel announced a $2.5 billion acquisition of Stahl Holdings to enhance its advanced adhesives and high-performance polymer portfolio targeting semiconductor assembly. The same month, Sumitomo Chemical revised its financial outlook upward due to strong semiconductor processing material shipments within its ICT & Mobility segment, supported by AI data center expansion. These developments collectively reinforce vertical integration, regional localization, advanced materials innovation, and supply chain resilience as central growth pillars driving the semiconductor chemical market toward $148.1 billion by 2034.

High-Impact Trends and Strategic Opportunities in the Global Semiconductor Chemical Market

Concentration of Capital Expenditure on Ultrapure Chemistries for Sub-3nm and EUV Manufacturing

The semiconductor chemical market is entering a decisive inflection point as device architectures transition toward sub-3nm nodes and EUV-enabled patterning. At these geometries, chemical impurity tolerances have tightened from parts-per-billion to parts-per-trillion levels, fundamentally reshaping supplier qualification criteria and capital allocation priorities. Leading fabs are no longer sourcing commoditized wet chemicals but are locking in long-term partnerships for proprietary ultrapure acids, solvents, CMP slurries, photoresist ancillaries, and atomic-layer deposition precursors that can preserve yield at atomic-scale feature sizes.

In December 2025, KPPC Advanced Chemicals, part of the Kanto Chemical group, initiated construction of a $500 million ultrapure chemical campus in Arizona, with Phase 1 alone representing a $120 million investment. The facility is explicitly designed to supply ppt-grade chemistries to TSMC, Intel, and Micron. This aligns with forecasts from SEMI, which project 7nm-and-below capacity expanding at roughly 16% annually through 2025, adding more than 300,000 wafers per month. The result is a structural demand pull for next-generation etchants, selective cleans, and functional fluids that can operate reliably in EUV and atomic-layer process windows.

Policy-Driven Onshoring of Mature Node Capacity and Localization of Bulk Chemical Supply

While advanced logic dominates industry narratives, public policy is simultaneously catalyzing a resurgence of mature node manufacturing above 28nm to secure supply chains for automotive, industrial, aerospace, and defense applications. This dual-track expansion is creating stable, long-duration demand for bulk semiconductor chemicals, particularly localized blending, purification, and distribution capabilities near fabs.

In the United States, the U.S. Department of Commerce finalized more than $36 billion in CHIPS Act awards by November 2025, with a growing share directed toward supply chain adjacency projects rather than fabs alone. Funding allocations to Hemlock Semiconductor for polysilicon and to Corning for EUV and DUV materials underscore a policy mandate to anchor the full semiconductor chemical ecosystem domestically. A similar pattern is emerging in India, where the India Semiconductor Mission has approved ten major projects across six states, exceeding ₹1.6 trillion in committed investment. Flagship initiatives involving Tata–PSMC and CG–Renesas are actively drawing global chemical suppliers to establish domestic purification and formulation units, reinforcing long-term demand visibility as India targets a $109 billion semiconductor market by 2030.

Closed-Loop Recycling and Abatement Services for High-GWP Semiconductor Gases

Environmental compliance is rapidly evolving from a cost center into a strategic opportunity within the semiconductor chemical market. Heightened scrutiny of perfluorocarbons, NF3, and SF6 emissions is pushing fabs to demand integrated chemical management services rather than standalone material supply. In early 2025, the global semiconductor gas abatement systems market reached approximately $1.52 billion, reflecting rising adoption of plasma-wet and catalytic destruction technologies with higher destruction removal efficiency. Major manufacturers such as Renesas have disclosed that PFC emissions can account for more than 5% of total Scope 1–3 greenhouse gas footprints, intensifying procurement pressure for effective abatement.

Beyond emissions control, circular recovery systems represent a compelling cost and ESG lever. Leading fabs are now targeting recovery rates of up to 90% for select wet chemicals, including SPM mixtures, translating into 15 to 20% reductions in total chemical operating costs. Suppliers capable of integrating recovery, purification, and reuse into closed-loop service contracts are positioned to secure higher-margin, stickier relationships.

Specialized Chemistries for Advanced Packaging, Chiplets, and CoWoS Architectures

The rapid rise of AI and high-performance computing is accelerating the industry’s shift toward heterogeneous integration, fundamentally altering chemical demand profiles. Advanced packaging technologies now account for roughly 35% of total semiconductor chemical consumption, up from 25% five years ago, driven by chiplets, 3D-ICs, and CoWoS platforms. High-performance AI accelerators, including those in Nvidia’s Blackwell generation, rely on CoWoS architectures that require specialized temporary bonding and debonding agents, ultra-fine pitch plating chemistries, and advanced dielectric materials.

By 2026, TSMC plans to scale CoWoS capacity to approximately 88,000 wafers per month to meet AI demand. This expansion creates a substantial opportunity for suppliers developing thermal interface materials and through-silicon via plating solutions capable of managing power densities above 40 W per square centimeter, thresholds at which conventional packaging chemistries fail. As back-end complexity increases, semiconductor chemicals are becoming a core enabler of performance scaling, not merely a supporting input.

Semiconductor Chemical Market Share and Segmentation Insights

Electronic Gases Lead Semiconductor Chemical Demand as Advanced Wafer Fabrication Expands

Electronic gases accounted for 32.80% of the semiconductor chemical market in 2025, reflecting their critical role in semiconductor manufacturing processes. High-purity gases such as fluorinated etch gases, deposition gases, and carrier gases are essential for advanced processes including plasma etching, chemical vapor deposition, and ion implantation. As semiconductor fabrication continues to move toward advanced technology nodes and higher wafer start volumes, the consumption of ultra-high-purity electronic gases continues to rise across global semiconductor fabs. A major 2025 industry development is the expansion of localized electronic gas production and purification facilities near semiconductor fabrication plants. This localization strategy strengthens semiconductor supply chain security, ensuring reliable gas supply and consistent quality for new fabrication facilities being developed in major semiconductor manufacturing regions.

Consumer Electronics Drive Semiconductor Chemical Consumption Across Device Manufacturing

Consumer electronics represent the largest end-user segment in the semiconductor chemical market, accounting for 38.60% of total demand in 2025 due to the massive production scale of electronic devices worldwide. Semiconductor components used in smartphones, laptops, tablets, wearable electronics, and home entertainment systems require advanced fabrication processes supported by specialized semiconductor chemicals. These chemicals are essential for photolithography, wafer cleaning, deposition, and planarization steps in integrated circuit manufacturing. A major 2025 industry trend is the continued expansion of high-performance consumer electronics incorporating advanced processors, memory chips, and power management devices, which increases demand for high-purity semiconductor chemicals capable of supporting smaller transistor geometries and higher wafer processing precision.

Semiconductor Chemical Market Competitive Landscape

The 2026 semiconductor chemicals market is driven by ultra-high purity specialty chemicals, AI-led chip demand, and localized supply chains under CHIPS Act policies. Growth is fueled by PFAS-free photoresists, low-GWP gases, and advanced wafer fabrication chemicals for sub-5nm and AI accelerator production.

BASF expands semiconductor-grade chemical capacity with ammonium hydroxide and sulfuric acid investments

BASF SE is strengthening its semiconductor chemicals position through localized production and Verbund integration. Construction of an electronic-grade ammonium hydroxide plant in Ludwigshafen supports advanced node semiconductor manufacturing. A parallel sulfuric acid facility addresses rising demand for wafer cleaning and etching chemicals. Startup of the Zhanjiang steam cracker enhances feedstock integration for electronic materials in Asia. The company reported €6.6 billion EBITDA in 2025 and is maintaining €13 billion capex through 2029. Focus on bulk and specialty electronic chemicals supports regional semiconductor ecosystem growth.

Merck accelerates semiconductor materials leadership with Taiwan megasite and AI-driven thin-film innovation

Merck KGaA is advancing its semiconductor chemicals portfolio through large-scale infrastructure and high-performance materials innovation. The €500 million Kaohsiung megasite enables full-scale production of specialty gases and thin-film materials for AI chips. Record performance in thin films supports atomic layer deposition and advanced chip architectures. 2025 net sales reached €21.1 billion with strong EBITDA growth driven by electronics materials. Digital twin integration enhances manufacturing precision and operational efficiency. Renewable energy adoption targets 50% power usage at the new facility.

Air Liquide strengthens ultra-high purity gas dominance with strategic acquisitions and semiconductor supply expansion

Air Liquide is reinforcing leadership in semiconductor specialty gases through targeted acquisitions and infrastructure investments. The €3 billion acquisition of DIG Airgas expands its footprint in South Korea’s semiconductor market. Investments in Singapore support production of ultra-high purity nitrogen for advanced fabrication plants. The company reported operating margins above 20% and net profit exceeding €3.5 billion in 2025. Expansion into India through NovaAir acquisition supports emerging semiconductor manufacturing hubs. Focus on long-term supply contracts ensures stability for high-volume fab operations.

Shin-Etsu capitalizes on AI-driven wafer demand and photoresist growth for advanced lithography processes

Shin-Etsu Chemical Co., Ltd. is leveraging its dominance in silicon wafers and photoresists to capture AI-driven semiconductor demand. Growth in 300 mm wafer shipments reflects rising requirements from memory and logic manufacturers. Formation of the μ-Material Machine Business Unit enhances integration of materials and advanced packaging technologies. Fiscal 2026 revenue is projected at ¥2.4 trillion with strong operating income driven by electronics materials. Photoresist demand is increasing with expansion of EUV lithography capacity. Focus on advanced substrates supports next-generation chip manufacturing.

Entegris advances extreme purity solutions with US investments and next-generation contamination control technologies

Entegris, Inc. is strengthening its semiconductor chemical solutions through investments in extreme purity and contamination control. A $700 million investment in the United States supports R&D and manufacturing expansion for advanced materials. New technology centers in the U.S. and Korea enhance localized support for semiconductor customers. Innovations in fluid management systems reduce electrostatic contamination risks in sub-3nm node production. Leadership transition supports scaling of global operations and supply chain resilience. Focus on advanced purity solutions aligns with increasing yield requirements in advanced chip fabrication.

DuPont repositions semiconductor chemicals through electronics spin-off and focus on advanced packaging materials

DuPont is restructuring its semiconductor chemicals business through the spin-off of its electronics division into an independent entity. The new company focuses on metallization chemistries, dielectrics, and advanced packaging solutions. Post-spin-off, DuPont reported 2025 net sales of $6.849 billion and improved market valuation. Strategic emphasis on heterogeneous integration supports next-generation data center and AI hardware requirements. Capital restructuring initiatives enhance financial flexibility for future investments. Focus on high-performance materials strengthens positioning in semiconductor interconnect technologies.

India: Policy-Led Scale-Up of Domestic Semiconductor Chemical Ecosystems

India is transitioning from an import-dependent semiconductor chemicals consumer to a policy-driven manufacturing and formulation hub. As of August 2025, the India Semiconductor Mission had approved ten projects with cumulative investment commitments of approximately INR 1.6 trillion across six states, creating an immediate downstream requirement for ultra-high-purity wet chemicals, specialty gases, and on-site chemical distribution systems. Government-backed Specialty Chemical Zones in Gujarat and Odisha are being positioned as anchor supply bases for the Micron ATMP facility and the Tata–PSMC fab, reducing logistics risk for acids, CMP slurries, and advanced cleaning chemistries. The Modified Scheme for Semiconductor Fabs, which offers up to 50% fiscal support, explicitly covers chemical handling infrastructure, accelerating the localization of UHP sulfuric acid, hydrogen peroxide, and solvent blending units.

Demand is also being pulled by design-led innovation. The commissioning of 3nm chip design facilities in Noida and Bengaluru during 2025 has triggered early-stage consumption of EUV photoresist developers, residue removers, and defect-control surfactants that were previously limited to East Asian ecosystems. Multinational alignment reinforces this trajectory. In November 2025, Sumitomo Chemical announced the acquisition of a Taiwan-based process chemicals firm to serve as a bridgehead for its Indian manufacturing expansion, specifically targeting the OSAT segment. Complementing infrastructure and corporate investment, a national skilling initiative launched in late 2025 aims to train 85,000 engineers in semiconductor-grade chemical handling and cleanroom protocols, addressing one of the most critical execution risks for chemical reliability and yield consistency.

South Korea: R&D Consolidation and Packaging-Centric Chemical Innovation

South Korea’s semiconductor chemical landscape is increasingly defined by R&D consolidation around memory and advanced packaging. In 2025, BASF completed the relocation and expansion of its Electronic Materials R&D Center to Ansan, focusing on next-generation CMP slurries and post-CMP cleaning agents optimized for sub-5nm logic and advanced DRAM nodes. Quality assurance has become equally strategic. Tokyo Ohka Kogyo inaugurated a state-of-the-art inspection facility at its Incheon plant to strengthen purity control for photoresists supplied to Samsung and SK Hynix, reducing defectivity risks at scale.

Technology roadmaps are reshaping chemical demand profiles. With High Bandwidth Memory accounting for roughly 20% of DRAM revenues by late 2025, local chemical suppliers have pivoted toward epoxy molding compounds tailored for 3D TSV packaging and thermal management. The 2025 joint venture between JSR Corporation and FLOSFIA to mass-produce iridium-based deposition precursors represents a structural shift toward power semiconductor materials. Policy alignment amplifies these trends. The updated K-Semiconductor Belt strategy targets USD 450 billion in cumulative investment by 2030 and introduces a specific mandate to domesticate 70% of critical etching gases, directly benefiting domestic gas purification and precursor suppliers.

United States: Node Shrink, Regulatory Pressure, and Material Security

The United States semiconductor chemical market is expanding rapidly under the combined weight of fab construction, node migration, and regulatory change. CHIPS Act implementation has translated into material-specific grants from the Department of Commerce, supporting new UHP sulfuric acid and hydrogen peroxide plants by suppliers such as Chemours and Solvay in Arizona and Texas. In 2025 alone, four major fab construction projects broke ground simultaneously, driving unprecedented demand for on-site chemical manufacturing, gas cabinets, and bulk delivery systems designed to minimize contamination risk.

Technology inflection points are redefining formulation requirements. The transition to 2nm and Angstrom-class nodes, including Intel 18A, has introduced backside power delivery architectures that require novel cleans, adhesion promoters, and ruthenium-based interconnect precursors. Regulatory dynamics further complicate the landscape. The EPA’s 2025 update on PFAS regulations has triggered a broad R&D pivot toward PFAS-free surfactants and photoresists, forcing reformulation across multiple wet-process steps. At the same time, federal investment in silicon carbide precursor chemistry is strengthening supply chains for EV power semiconductors concentrated in the U.S. Battery Belt, reinforcing the strategic importance of domestic chemical capacity.

Japan: Materials Supremacy and Integrated Chemical Platforms

Japan continues to anchor the global semiconductor chemical value chain through materials dominance and integrated manufacturing strategies. Domestic firms control over 90% of the high-end photoresist market, with Shin-Etsu Chemical and Sumitomo Chemical announcing capacity expansions in late 2025 for ArF and EUV grades. Structural consolidation is underway. In December 2025, Sumitomo Chemical, Mitsui Chemicals, and Idemitsu Kosan finalized an agreement to integrate their domestic polyolefin and specialty chemical businesses, streamlining semiconductor-grade plastics used in fabs and packaging lines.

Japan is also regaining momentum in fab construction. A 2025 SEMI assessment identified the country as a global leader in new fab starts, particularly for automotive and imaging sensors, driving localized demand for dopants, organometallic precursors, and specialty gases. Strategic R&D initiatives reinforce this position. The Rapidus project in Hokkaido has attracted a dense cluster of chemical suppliers, including JSR and Fujifilm, to co-develop 2nm-ready chemical delivery systems targeted for deployment by early 2027, tightly coupling materials innovation with manufacturing roadmaps.

Taiwan: Foundry-Centric Chemical Demand and Sustainability Enforcement

Taiwan remains the epicenter of advanced semiconductor chemical consumption due to foundry concentration and aggressive packaging expansion. In 2025, TSMC expanded its CoWoS capacity to approximately 75,000 wafers per month, creating a structurally large and localized market for advanced packaging chemicals, underfill materials, and low-k dielectrics. Proximity has become a strategic imperative. Global chemical suppliers are acquiring niche Taiwanese firms to embed capabilities near giga-fabs, a trend highlighted by Sumitomo Chemical’s late-2025 M&A activity.

Sustainability has emerged as a non-negotiable operating condition. The Taiwanese government’s 2025 Green Manufacturing initiative mandates closed-loop solvent recycling across all 300mm wafer facilities, forcing chemical suppliers to redesign formulations and recovery systems simultaneously. This regulatory stance is accelerating innovation in low-loss solvents, reclaimable developers, and extended-life cleaning chemistries, reinforcing Taiwan’s role as both a volume and technology driver in the global semiconductor chemical industry.

Comparative Snapshot: Country-Level Strategic Positioning

Semiconductor Chemical Market County Level Snapshot

|

Country

|

Primary Strategic Lever

|

Chemical Demand Driver

|

|

India

|

Policy incentives and localization

|

Wet chemicals, EUV cleans, OSAT materials

|

|

South Korea

|

R&D consolidation and HBM growth

|

CMP slurries, EMCs, deposition precursors

|

|

United States

|

CHIPS Act and node migration

|

UHP acids, PFAS-free chemistries, SiC precursors

|

|

Japan

|

Materials dominance and integration

|

Photoresists, dopants, organometallics

|

|

Taiwan

|

Foundry and packaging scale

|

Advanced packaging chemicals, solvent recovery

|

Semiconductor Chemical Market Report Scope

Semiconductor Chemical Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$47 Billion

|

|

Market Size (2034)

|

$148.1 Billion

|

|

Market Growth Rate

|

13.6%

|

|

Segments

|

By Product Type (Wet Chemicals, Photolithography Chemicals, Deposition Materials, CMP Materials, Electronic Gases, Cleaning & Surface Preparation Chemicals), By Process Step (Wafer Fabrication, Photolithography, Etching & Ashing, Deposition, CMP & Planarization, Assembly & Packaging), By End-User Application (Consumer Electronics, Automotive Electronics, Telecommunications, Data Centers, Industrial & Medical Electronics)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

BASF SE, Merck KGaA, Tokyo Ohka Kogyo Co. Ltd., JSR Corporation, Sumitomo Chemical Co. Ltd., Shin-Etsu Chemical Co. Ltd., FUJIFILM Holdings Corporation, Dow Inc., DuPont de Nemours Inc., Honeywell International Inc., Entegris Inc., Air Liquide SA, Linde plc, Kanto Chemical Co. Inc., Solvay SA

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Semiconductor Chemical Market Segmentation

By Product Type

- Wet Chemicals

- Photolithography Chemicals

- Deposition Materials

- CMP Materials

- Electronic Gases

- Cleaning & Surface Preparation Chemicals

By Process Step

- Wafer Fabrication

- Photolithography

- Etching & Ashing

- Deposition

- CMP & Planarization

- Assembly & Packaging

By End-User Application

- Consumer Electronics

- Automotive Electronics

- Telecommunications

- Data Centers

- Industrial & Medical Electronics

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in Semiconductor Chemical Industry

- BASF SE

- Merck KGaA

- Tokyo Ohka Kogyo Co. Ltd.

- JSR Corporation

- Sumitomo Chemical Co. Ltd.

- Shin-Etsu Chemical Co. Ltd.

- FUJIFILM Holdings Corporation

- Dow Inc.

- DuPont de Nemours Inc.

- Honeywell International Inc.

- Entegris Inc.

- Air Liquide SA

- Linde plc

- Kanto Chemical Co. Inc.

- Solvay SA

*- List not Exhaustive