High Purity Gas Market to Reach $118.1 Billion by 2034 Driven by Semiconductor Manufacturing and Advanced Electronics Demand

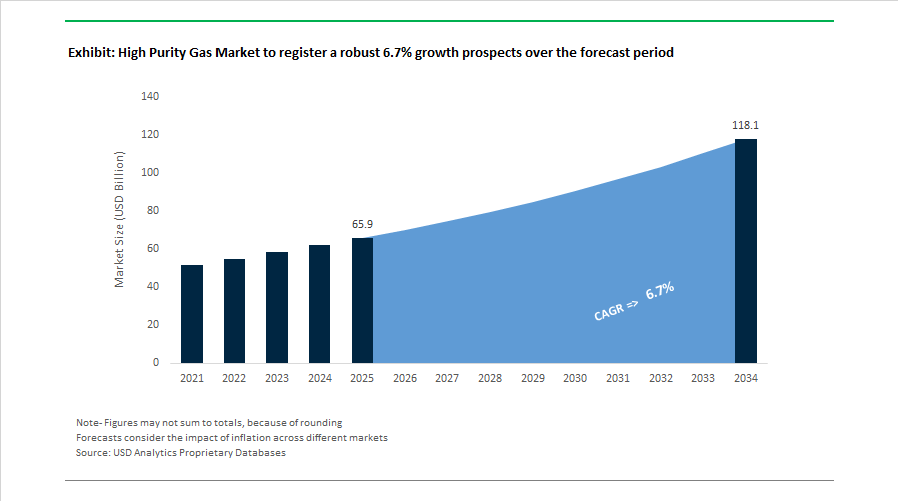

The Global High Purity Gas Market is experiencing sustained growth due to the rapid expansion of semiconductor manufacturing, advanced electronics production, aerospace applications, and medical technologies. The market is projected to grow from $65.9 billion in 2025 to $118.1 billion by 2034, registering a CAGR of 6.7% during the forecast period. Rising investments in AI-driven semiconductor fabrication plants, electric vehicle battery production, and high-performance electronics manufacturing are significantly increasing demand for ultra-high purity industrial gases such as nitrogen, argon, helium, neon, krypton, xenon, and hydrogen. These gases are essential for wafer processing, etching, lithography, inerting, and cooling applications across advanced manufacturing ecosystems.

The technical and operational landscape of the high purity specialty gases industry is rapidly evolving as semiconductor manufacturing advances toward sub-3nm nodes, requiring higher gas purity standards. Semiconductor fabrication facilities are increasingly shifting from 99.999% (5N) to 99.9999% (6N) purity levels for gases such as nitrogen and argon, as even parts-per-billion contamination can significantly reduce wafer yields. At the same time, geopolitical factors have reshaped supply chains, particularly for neon, with approximately 40% to 50% of global high-purity neon production secured through long-term take-or-pay contracts with lithography equipment manufacturers to ensure supply stability.

On the production side, energy efficiency has become a key competitive benchmark since Cryogenic Air Separation Units account for roughly 70% to 80% of operational costs, prompting new 2025-generation facilities to target 5% to 8% improvements in specific power consumption through digital twin optimization and advanced automation. The industry is also strengthening sustainability initiatives, including helium recycling systems that now achieve over 90% recovery compared to the previous 30% standard, while tightening environmental regulations for fluorinated gases in semiconductor etching processes are pushing manufacturers to implement gas abatement systems capable of more than 98% destruction removal efficiency.

Market Analysis: Strategic Industry Developments Accelerating the High Purity Gas Ecosystem (2024–2026)

The High Purity Gas industry is currently shaped by large-scale infrastructure investments aligned with the global AI semiconductor boom, advanced electronics manufacturing, and regional supply chain security initiatives. One of the most significant developments occurred in February 2026, when Air Liquide published its Pre-FY 2025 results communication, highlighting a strategic shift toward electronics-grade high purity gases as a primary growth engine for its operations across Asia and North America, particularly to support semiconductor fabrication facilities and advanced microelectronics manufacturing.

In January 2026, Air Liquide completed the €2.85 billion acquisition of DIG Airgas in South Korea, significantly strengthening its footprint in one of the world’s most concentrated semiconductor manufacturing clusters and securing long-term supply relationships with major memory chip fabrication companies. During the same month, Air Products commissioned a new high purity nitrogen production facility in Dortmund, Germany, specifically designed to supply ultra-pure inert gases for aerospace and defense applications, further expanding Europe’s specialized gas infrastructure.

Several major investments and partnerships throughout 2025 also reinforced the growth trajectory of the ultra-high purity industrial gases market. In December 2025, Southern Industrial Gas (SIG) signed a Memorandum of Understanding for a new helium extraction and purification facility in Malaysia, aimed at decentralizing helium supply chains and reducing reliance on geopolitically sensitive production regions. Earlier in October 2025, Linde plc secured a long-term supply agreement with a U.S.-based electric vehicle battery manufacturer to provide ultra-high purity hydrogen and nitrogen used in advanced electrode drying and battery manufacturing processes. In July 2025, Taiyo Nippon Sanso Corporation announced the full operational deployment of new krypton and xenon gas manufacturing equipment at its Fukuyama Plant in Japan, targeting increasing demand from satellite propulsion systems and specialized high-intensity lighting technologies.

Emerging regional investments are also strengthening domestic supply capabilities. In April 2025, Inox Air Products inaugurated India’s first ultra-high purity nitrous oxide production facility in Chennai, capable of producing 99.9999% (6N) purity gas for semiconductor manufacturing and medical electronics industries. Meanwhile, in January 2025, the U.S. Department of Energy released a policy document outlining modular technologies for extracting helium from flare gases, enabling independent producers to expand helium supply and mitigate the ongoing Helium 4.0 shortage crisis affecting multiple high-tech industries. These strategic investments, policy developments, and technological advancements are collectively reinforcing the global supply chain for high purity industrial gases, positioning the market for sustained growth across semiconductor, aerospace, electronics, and advanced manufacturing sectors.

High Purity Gas Market Trends and Opportunities

Capital Shift Toward On-Site Gas-as-a-Service Models for Semiconductor Fabs

The high purity gas market is experiencing a structural capital realignment as semiconductor manufacturers prioritize supply security, purity assurance, and long-term cost stability. Instead of relying on merchant delivery of liquid gases, fabs are increasingly adopting on-site gas-as-a-service models, anchored by dedicated air separation units and ultra-high-purity purification plants. These assets are typically financed through long-duration take-or-pay contracts spanning 15 to 20 years, effectively transforming industrial gases from a variable operating expense into a strategic infrastructure investment.

This trend is particularly visible in the United States, where fab construction is accelerating. In July 2025, Air Liquide announced an investment exceeding $50 million to design, build, and operate an advanced gas production facility for a leading semiconductor manufacturer in the Southeastern U.S. The plant is engineered to supply ultra-high-purity nitrogen and oxygen directly at the point of use, with operations scheduled for late 2027. According to SEMI’s January 2025 World Fab Forecast, construction is expected to begin on 18 new fabs globally in 2025, including fifteen 300 mm facilities. Each fab requires fully integrated high purity gas infrastructure to support advanced logic nodes below 7 nm, which are projected to record around 16% year-on-year capacity growth during 2025.

The model is also gaining traction in emerging manufacturing hubs. In November 2024, INOX Air Products secured a long-term supply contract with Tata Group’s TP Solar for its Tirunelveli facility, following a greenfield investment exceeding INR 2,000 crore. These developments highlight how on-site gas generation is becoming a prerequisite for semiconductor and adjacent high-tech manufacturing competitiveness.

Global Scramble for Diversified Grade 5 Helium Supply

The helium segment of the high purity gas market is undergoing a profound supply-side reset. The depletion of the U.S. Federal Helium Reserve, combined with sanctions-related disruptions to Russian exports, has triggered a global scramble to secure diversified, long-term sources of Grade 5 helium. Demand is being driven by mission-critical applications, including extreme ultraviolet lithography in semiconductor fabs and high-uptime magnetic resonance imaging networks in healthcare.

Europe has moved aggressively to lock in alternative supply routes. In December 2025, Uniper signed a 15-year sales and purchase agreement with QatarEnergy for liquid helium sourced from Ras Laffan. The agreement secures approximately 70 million standard cubic feet per year of high purity helium, providing long-term insulation from spot market volatility. In parallel, the European Union’s sanctions package effective September 2024 permanently banned helium imports from Russia, accelerating the pivot toward Canadian and Middle Eastern supply chains.

In the United States, privatization of federal helium assets is stimulating new domestic production. Following the June 2024 asset transfer, Helium One Global commissioned its Pinon Canyon facility in Colorado in December 2025, with commercial sales expected from January 2026. These investments are taking place in a pricing environment where Grade A helium has reached estimated base levels of $390 to $500 per thousand cubic feet, reinforcing the strategic importance of supply diversification.

Ultra-High-Purity Hydrogen Infrastructure for GaN and SiC Semiconductor Manufacturing

The rapid adoption of gallium nitride and silicon carbide devices for electric vehicles, renewable energy inverters, and 5G infrastructure is creating a high-margin opportunity for suppliers of ultra-high-purity hydrogen. These compound semiconductors require hydrogen with oxygen and moisture impurities below 1 part per billion to ensure defect-free epitaxial growth during metal organic chemical vapor deposition processes.

The MOCVD equipment market reached an estimated value of $1.5 billion by late 2024, driven by the deployment of multi-wafer reactors that consume large volumes of carrier gases. This has opened a pathway for gas suppliers to deploy on-site palladium membrane purifiers capable of delivering hydrogen at 9.0-grade purity levels. Public funding initiatives are reinforcing this trend. Under the U.S. CHIPS Act and India’s National Green Hydrogen Mission, targeted incentives are being directed toward gas purification and delivery technologies that reduce cost per wafer by minimizing yield losses caused by trace contamination.

Demand growth is closely linked to electrification. Silicon carbide power devices enable 800-volt electric vehicle architectures that support ultra-fast charging cycles of around 15 minutes. As EV adoption accelerates, gas suppliers delivering ultra-high-purity hydrogen to SiC fabs are seeing a direct and sustained increase in contracted gas volumes.

High-Precision Specialty Gas Mixtures for CCUS Measurement and Verification

As carbon capture, utilization, and storage projects transition from pilot scale to commercial deployment, a new demand segment is emerging for specialty calibration gases and tracer mixtures used in measurement, reporting, and verification frameworks. These high-precision mixtures are essential for validating sensor accuracy, detecting micro-leakage, and ensuring regulatory compliance across the CCUS value chain.

In December 2025, carbon standard bodies including Verra released updated CCUS methodology modules that require operators to use ISO 17025 certified calibration gases. This requirement is driving demand for highly stable, multi-component gas mixtures capable of maintaining compositional integrity under high-pressure storage and injection conditions. Tracer gases such as perfluorocarbons are increasingly being deployed to detect minute leaks in underground geological storage formations, creating a specialized blending opportunity for industrial gas providers.

Regulatory momentum is reinforcing this opportunity. The European Union Emissions Trading System is moving toward stricter verification of captured and stored carbon dioxide, compelling industrial emitters to upgrade analytical and monitoring systems. As a result, the calibration gas and specialty mixture segment, already valued at over $600 million, is projected to expand steadily through 2030, positioning high purity gas suppliers at the core of the global decarbonization measurement infrastructure.

High Purity Gas Market Share and Segmentation Insights

Specialty and Electronic Gases Lead the High Purity Gas Market in Semiconductor Manufacturing

Specialty and Electronic Gases accounted for 42.80% of the High Purity Gas Market share in 2025, making them the largest product category within advanced gas supply chains. These gases include highly purified process chemicals such as silane, ammonia, tungsten hexafluoride, hydrogen chloride, nitrous oxide, and specialized organometallic compounds, all of which are critical for modern semiconductor fabrication and electronic component manufacturing. Specialty gases are used in processes including chemical vapor deposition, plasma etching, doping, and wafer cleaning, where extremely high purity levels are required to prevent contamination and ensure precise microelectronic structures. The rapid expansion of semiconductor fabrication plants, flat panel display manufacturing, LED production, and photovoltaic cell fabrication has significantly increased demand for these gases. In 2025, the segment is strongly influenced by the localization of semiconductor supply chains driven by government initiatives such as semiconductor manufacturing incentives and regional fabrication investments. As new semiconductor fabs are established in North America and Europe, specialty gas producers are building local purification and distribution facilities to ensure consistent supply and maintain strict quality control for advanced semiconductor manufacturing processes.

Electronics and Semiconductors Drive the Largest Demand for High Purity Gases

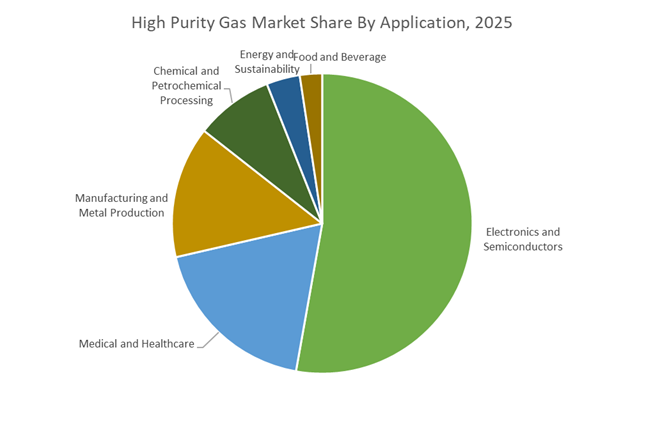

Electronics and Semiconductors represented 52.80% of the High Purity Gas Market share in 2025, making it the dominant application sector for ultra-high purity gas technologies. Semiconductor manufacturing relies heavily on high purity gases to support thin film deposition, plasma etching, doping, oxidation, and wafer surface cleaning processes used in integrated circuit fabrication. Even trace contaminants in process gases can disrupt semiconductor manufacturing, requiring gas purity levels exceeding 99.999% or higher depending on process requirements. As global demand for advanced electronics including smartphones, cloud computing infrastructure, artificial intelligence processors, and electric vehicle electronics continues to expand, semiconductor fabrication volumes are increasing correspondingly. In 2025, demand for high purity gases is further accelerated by the shift toward advanced three-dimensional chip architectures, including 3D NAND memory structures and gate-all-around transistor technologies. These next-generation chip designs require deep trench etching and multiple stacked deposition layers, significantly increasing the amount of process gas consumed per wafer. As a result, gas consumption growth is being driven not only by higher wafer production but also by increasing process complexity in advanced semiconductor nodes.

Competitive Landscape in High Purity Gas Market

Air Liquide Strengthens Semiconductor Dominance Through Strategic Acquisitions

Air Liquide continues to consolidate its leadership in electronic grade gases and ultra-high purity gas supply for semiconductor manufacturing. Under its ADVANCE strategic plan, the company balances operating margin expansion with decarbonization commitments. In January 2026, Air Liquide completed the €3 billion acquisition of DIG Airgas in South Korea, doubling its workforce in a critical semiconductor cluster and reinforcing its position in advanced chip fabrication ecosystems. The company also committed over €250 million to new gas production units in Silicon Saxony, Germany, and an additional $50 million ultra-pure gas plant in the United States. With FY 2025 sales of €26.94 billion and Gas & Services contributing 97% of revenue, Air Liquide remains a benchmark supplier for high purity nitrogen, hydrogen, and specialty gas mixtures used in CVD and etching processes.

Linde plc Expands High Purity Hydrogen and EUV Gas Leadership

Linde plc maintains its position as the world’s largest industrial gas producer by revenue, reporting $34 billion in full-year 2025 sales and extending its dividend growth streak to 33 consecutive years. The company is prioritizing high purity hydrogen, carbon capture integration, and EUV lithography gas supply chains essential for sub-5nm semiconductor manufacturing. Linde remains a key supplier of ultra-high purity neon and helium mixtures required for advanced photolithography systems. With approximately $4 billion in planned capital expenditure for 2026, Linde is expanding capacity to support aerospace propulsion, energy transition projects, and semiconductor mega fabs. Its disciplined capital allocation and global pipeline infrastructure provide competitive advantages in long-term supply agreements for specialty and electronic grade gases.

Air Products Focuses on Hydrogen Megaprojects and Operational Reset

Air Products and Chemicals, Inc. is executing a strategic reset following significant 2025 asset restructuring charges of approximately $3.7 billion. Entering 2026, the company is concentrating on high-return industrial gas projects and operational efficiency improvements. As the world’s largest hydrogen producer, Air Products manages a backlog of multi-billion-dollar megaprojects including the NEOM Green Hydrogen initiative. The company expects roughly $4 billion in capital expenditure in FY 2026 and has issued adjusted EPS guidance between $12.85 and $13.15, signaling financial recovery. With $12 billion in 2025 sales and a 30% operating margin in Asia, Air Products remains a critical supplier of high purity hydrogen, LNG process gases, and merchant nitrogen and oxygen across more than 50 countries.

Taiyo Nippon Sanso Advances 6N Gas Purification and Semiconductor Infrastructure

Taiyo Nippon Sanso Corporation, part of Mitsubishi Chemical Group, is recognized globally for high purity gas purification systems capable of achieving 99.9999% purity levels. The company is a leading manufacturer of purification hardware for nitrogen, oxygen, hydrogen, argon, helium, and ammonia, supporting semiconductor fabrication plants worldwide. In 2026, TNSC is emphasizing membrane-based separation technologies that improve energy efficiency in on-site high purity argon and nitrogen generation. Its specialty gas piping systems and detoxification units are critical for CVD and plasma etching processes in chip manufacturing. The company is also scaling liquid helium logistics using advanced ultra-low temperature vacuum transport systems, reinforcing its presence in global electronics and aerospace markets.

Messer Group Expands Renewable Hydrogen and Specialty Gas Footprint

Messer Group remains the largest privately held industrial gas specialist, positioning itself as an agile competitor in high purity hydrogen and specialty gas supply. In January 2026, Messer’s hydrogen filling station in Kerpen set a record by dispensing 456 kilograms of hydrogen in a single day, demonstrating technical capability in mobility-grade H2 infrastructure. The company is preparing to launch a 25 MW renewable hydrogen plant in Belgium under the Hyoffgreen project, expected to reduce CO2 emissions by 25,000 tons annually. Messer Americas continues to expand operations across the United States, Canada, and Brazil, focusing on healthcare gases and semiconductor-grade specialty mixtures. Through academic partnerships such as its cooperation with the University of Pécs, Messer is strengthening long-term expertise in hydrogen engineering and high purity gas systems.

United States: Semiconductor Localization, Hydrogen Scale-Up, and Supply Security

The United States high purity gas industry is undergoing a structural expansion anchored in semiconductor reshoring, hydrogen decarbonization, and critical gas supply security. Under the CHIPS Act, the U.S. Department of Commerce finalized more than USD 39 billion in direct grants by early 2026, catalyzing the construction of over 15 advanced semiconductor fabrication plants. This wave of capacity has necessitated localized supply of ultra-high purity nitrogen, argon, and hydrogen, particularly for sub-5nm process nodes where contamination tolerances are measured in parts per trillion.

Industrial gas majors are aligning capacity with fab geography. Air Liquide announced a USD 50+ million investment in July 2025 for a dedicated production plant in the Southeastern United States to supply ultra-high purity nitrogen and oxygen to a leading semiconductor manufacturer, with operations scheduled for late 2027. In parallel, Air Liquide committed more than USD 250 million to a new Idaho unit supplying Micron Technology with electronic-grade gases for memory fabrication, reflecting demand growth driven by AI hardware. Air Products expanded its Texas ultra-high purity hydrogen facility in March 2025 to meet 6N purity requirements for 3nm and 2nm nodes. Beyond electronics, the hydrogen economy is scaling. Air Products is advancing an USD 8–9 billion low-carbon energy complex in Louisiana, with agreements finalized in late 2025 to supply Yara with high purity low-carbon hydrogen for ammonia, targeting FID by mid-2026. Supply resilience is also improving. Following helium price volatility flagged by the U.S. Geological Survey in 2024, the United States prioritized domestic helium refinement and recycling, establishing new strategic reserves by 2026 to mitigate global outage risks.

South Korea: On-Site Gas Generation and Strategic Localization of Electronic Gases

South Korea’s high purity gas ecosystem is tightly coupled with its memory semiconductor leadership and national technology policy. The government unveiled a EUR 18.6 billion support package in 2024 for the semiconductor sector, with EUR 3.6 billion allocated for 2025–2027 to accelerate R&D in specialty electronic gases and workforce development. This policy backdrop is reinforcing localization of 6N-grade noble gases and high purity hydrogen under the Strategic Technology Master Plan administered by the Ministry of Science and ICT, which offers tax incentives for domestic suppliers achieving verified purity thresholds.

Operational models are shifting toward resilience. By 2026, Samsung Electronics and SK Hynix expanded gas-on-site generation across mega-fabs to reduce transport risk associated with hazardous electronic-grade chemicals such as chlorine and fluorine blends. International integration continues. The SEMICON Korea 2026 business mission scheduled for February 2026 aims to connect European SMEs to Korean supply chains, focusing on advanced etching gases and sustainable gas manufacturing technologies, reinforcing South Korea’s role as a global node for specialty electronic gases.

China: Electronic Special Gas Localization and Noble Gas Recovery

China’s high purity gas industry is being reshaped by localization mandates and upstream feedstock security. In 2025, the Ministry of Industry and Information Technology issued directives under the 15th Five-Year Plan prioritizing domestic production of electronic special gases compatible with 5nm processes, targeting reduced reliance on imports by 2030. Decarbonization is integrated into capacity expansion. In December 2025, Air Liquide expanded and electrified its Shaanxi oxygen facility, lowering the carbon intensity of high purity oxygen used in electronics and chemical processing.

Feedstock stability is strengthening. The National Energy Administration projected natural gas production to reach 260 billion cubic meters in 2025, underpinning stable refinement of high purity atmospheric and carbon gases. Noble gas self-sufficiency is also advancing. Large air separation units in the Shandong chemical cluster integrated krypton and xenon recovery systems in late 2025, targeting a 20% increase in domestic supply by 2026 for aerospace and advanced lighting applications.

Germany: Chips Act Response and Industrial Decarbonization with Oxygen

Germany’s high purity gas market is expanding in response to semiconductor investment and industrial decarbonization. In April 2025, Linde inaugurated a new high purity gas unit designed to serve the growing fab ecosystem in the Silicon Saxony region, directly aligned with the European Chips Act. This facility supplies ultra-high purity nitrogen, argon, and hydrogen required for advanced lithography and deposition.

Energy efficiency and emissions reduction are central themes. Air Liquide invested approximately EUR 40 million in 2025 to modernize its Stade site, improving efficiency and lowering CO2 emissions under a long-term agreement with Dow. Adoption of HeatOx technology is accelerating across heavy industry. By 2025–2026, German manufacturers integrated high purity oxygen into combustion systems to improve efficiency and decarbonize glass and cement operations, reinforcing oxygen’s role as a transition enabler.

Japan: AI-Driven Purity Control and Biocarbon Integration

Japan’s high purity gas industry is distinguished by precision control and integration with low-carbon industrial processes. In January 2025, Taiyo Nippon Sanso launched an AI-based purity monitoring system capable of detecting contaminants at parts-per-trillion levels, a critical capability for sub-7nm wafer fabrication and advanced packaging.

Industrial decarbonization is extending gas demand beyond electronics. From early 2026, Idemitsu and Aisin Takaoka scaled biocoke and torrefied biomass projects that rely on high purity gases for controlled processing. In steelmaking, Kobe Steel and Mitsubishi Ube Cement are preparing a 2026 joint venture that uses high purity industrial gases to enable biocarbon co-firing, reducing reliance on coking coal.

Singapore: Ultra-Pure Nitrogen and Regional Distribution Hub

Singapore has consolidated its position as Southeast Asia’s logistics and production hub for high purity gases. In 2025, Air Liquide invested more than EUR 50 million to build an ultra-pure nitrogen unit supplying GlobalFoundries, emphasizing energy-efficient delivery for high-volume fabs. Regulatory reforms introduced for 2026 have streamlined transit of hazardous electronic-grade chemicals, strengthening Singapore’s role as the preferred regional distribution node for specialty gases.

Summary Table: Country-Level Strategic Signals in the High Purity Gas Industry

High Purity Gas Market County Level Snapshot

|

Country

|

Strategic Driver

|

Primary Gas Focus

|

Structural Implication

|

|

United States

|

CHIPS Act, hydrogen decarbonization

|

UHP nitrogen, hydrogen, helium

|

Localized supply chains and resilience

|

|

South Korea

|

Semiconductor policy, on-site generation

|

6N noble gases, electronic gases

|

Supply security and localization

|

|

China

|

ESG localization, noble gas recovery

|

Electronic special gases, oxygen

|

Import substitution and feedstock stability

|

|

Germany

|

European Chips Act, HeatOx adoption

|

UHP gases, oxygen

|

Fab support and industrial decarbonization

|

|

Japan

|

AI purity control, biocarbon

|

Ultra-clean gases

|

Precision manufacturing leadership

|

|

Singapore

|

Fab supply and logistics reform

|

Ultra-pure nitrogen

|

Regional hub consolidation

|

High Purity Gas Market Report Scope

High Purity Gas Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$65.9 Billion

|

|

Market Size (2034)

|

$118.1 Billion

|

|

Market Growth Rate

|

6.7%

|

|

Segments

|

By Product Type (Atmospheric Gases, Noble Gases, Carbon Gases, Specialty and Electronic Gases), By Purity Level (Four-N Purity, Five-N Purity, Six-N and Above Purity), By Application (Electronics and Semiconductors, Medical and Healthcare, Manufacturing and Metal Production, Chemical and Petrochemical Processing, Energy and Sustainability, Food and Beverage)

|

|

Study Period

|

2019- 2025 and 2026-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Linde plc, Air Liquide S.A., Air Products and Chemicals, Inc., Taiyo Nippon Sanso Corporation, Messer Group GmbH, Iwatani Corporation, Merck KGaA, Resonac Holdings Corporation, SK Materials Co., Ltd., Gulf Cryo, Matheson Tri-Gas, Inc., SOL Group, Electronic Fluorocarbons, Entegris, Inc., Advanced Specialty Gases

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

High Purity Gas Market Segmentation

By Product Type

- Atmospheric Gases

- Noble Gases

- Carbon Gases

- Specialty and Electronic Gases

By Purity Level

- Four-N Purity

- Five-N Purity

- Six-N and Above Purity

By Application

- Electronics and Semiconductors

- Medical and Healthcare

- Manufacturing and Metal Production

- Chemical and Petrochemical Processing

- Energy and Sustainability

- Food and Beverage

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in the High Purity Gas Industry

- Linde plc

- Air Liquide S.A.

- Air Products and Chemicals, Inc.

- Taiyo Nippon Sanso Corporation

- Messer Group GmbH

- Iwatani Corporation

- Merck KGaA

- Resonac Holdings Corporation

- SK Materials Co., Ltd.

- Gulf Cryo

- Matheson Tri-Gas, Inc.

- SOL Group

- Electronic Fluorocarbons

- Entegris, Inc.

- Advanced Specialty Gases

*- List not Exhaustive