Market Overview: Elastomeric Sealants as Critical Enablers of Asset Longevity, Energy Efficiency, and OEM Risk Management

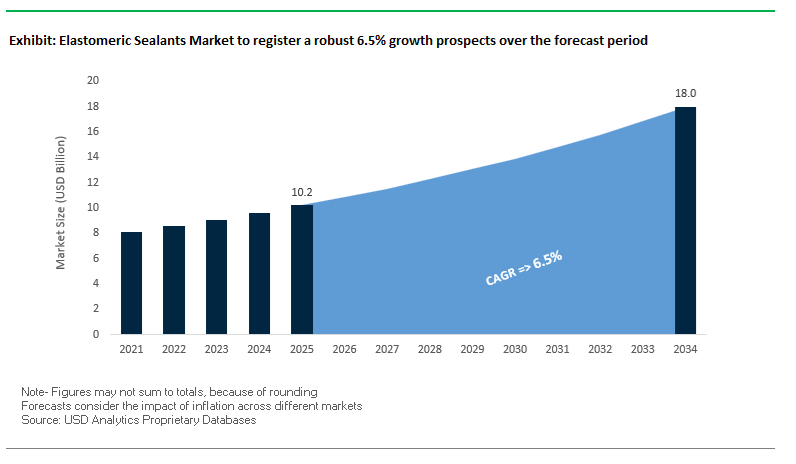

The Global Elastomeric Sealants Market is projected to grow from $10.2 billion in 2025 to $18 billion by 2034, registering a compound annual growth rate (CAGR) of 6.5%. The steady market growth is fueled by technological advancements in silicone, The elastomeric sealants market has entered a structurally more important phase, driven less by construction cycles and more by their role in protecting asset performance over long service lives. For manufacturers and OEM-facing suppliers, elastomeric sealants are no longer treated as ancillary materials; they are increasingly specified as performance-critical inputs that influence façade thermal ratings, infrastructure maintenance intervals, and EV system reliability. Silicone, polyurethane (PU), and silane-modified polymer (SMP) chemistries sit at the center of this shift due to their ability to combine elastic recovery, long-term adhesion, and regulatory compliance within a single formulation.

Demand is being reshaped by how sealants are qualified and embedded into system-level designs. In architectural glazing, structural silicone sealants for insulated glass units are engineered to limit argon gas loss to below 1% annually, enabling 25-year-plus façade performance warranties and making sealant choice a determinant of whole-building energy outcomes rather than a downstream procurement decision. In civil infrastructure, high-modulus PU sealants are specified to accommodate ±25% joint movement under repeated thermal cycling without cohesive or adhesive failure, directly linking sealant performance to bridge and highway lifecycle costs. These requirements are driving consolidation toward fewer, highly validated products that can meet multiple standards and reduce technical risk for specifiers, contractors, and owners.

At the same time, substitution toward higher-value formulations is accelerating. Low-VOC and solvent-free SMP sealants are replacing solvent-borne elastomers in North America and Europe as green building codes and contractor liability standards tighten, shifting volume toward premium chemistries with predictable cure behavior and broad substrate compatibility. In automotive and electric vehicle manufacturing, elastomeric adhesive-sealants are displacing discrete gaskets and secondary sealing operations in battery pack assemblies, where they combine environmental sealing with thermal stability at continuous operating temperatures up to 150 °C and tensile strengths above 5 MPa. For manufacturers, these performance thresholds translate into tangible business outcomes: deeper OEM integration, higher value per application, reduced price sensitivity, and longer qualification cycles that protect margins. Over the next decade, competitive advantage will hinge on the ability to industrialize these formulations at scale, align them with evolving standards, and support customers with application-level validation rather than incremental chemistry differentiation.

The global elastomeric sealants industry is undergoing rapid transformation driven by sustainability commitments, renewable energy adoption, and advanced polymer R&D. Recent developments highlight strong momentum across product innovation, capacity investments, and regulatory compliance.

In September 2025, TYPAR launched its Liquid Flashing sealant, a primer-free elastomeric formulation designed for seamless air and water sealing in building envelopes. Integrated into the TYPAR Weather Protection System, the product streamlines installation and enhances long-term waterproofing performance in both residential and commercial projects. Earlier, in February 2025, Wacker Chemie AG unveiled ELASTOSIL® eco 7770 P, a sustainable, low-emission silicone sealant tailored for natural stone applications. It offers enhanced mold resistance and reduced environmental impact, aligning with the growing demand for eco-certified construction materials.

The renewable energy market continues to drive innovation. In March 2023, Dow Inc. expanded its silicone sealant line with the launch of the DOWSIL™ PV series, engineered for photovoltaic (PV) module assembly, addressing long-term durability needs in solar installations. This aligns with the global shift toward renewable energy infrastructure, where reliable sealing is critical for weatherproofing and electrical insulation. Similarly, Sika AG’s Purform® technology, an ongoing innovation, represents a regulatory breakthrough with <0.1% free monomeric diisocyanate content, ensuring compliance with European REACH regulations while maintaining mechanical excellence in its Sikaflex® polyurethane sealants.

In August 2023, Covestro strengthened its presence in Asia with a new polyurethane elastomer plant in Shanghai, addressing the rising demand for automotive and industrial-grade PU systems. Meanwhile, the emergence of self-healing elastomers in mid-2024, based on poly(vinyl alcohol) research, introduced the potential for self-repairing sealant formulations—a development that could redefine maintenance expectations in the long term. Finally, Avery Dennison’s acquisition of Meridian Adhesives Group’s flooring business (2024–2025) underscores ongoing industry consolidation aimed at enhancing vertical integration and product diversification across adhesives and elastomeric sealing systems.

Architectural innovation and the growing use of large prefabricated façade elements have intensified the demand for high-movement, low-modulus elastomeric sealants capable of absorbing substantial structural and thermal shifts without joint failure. Modern high-rise glass and metal façade systems rely heavily on sealants that combine flexibility with robust adhesion under dynamic stress conditions.

According to ASTM C920 (Class 100/50) standards, premium ultra-low modulus silicone formulations are engineered to accommodate joint movement capabilities up to +100%/−50%, making them indispensable for curtain wall applications and insulating glass units (IGUs). Their tensile stress at 100% elongation—often around 0.24 MPa (35 psi)—demonstrates minimal stress on delicate substrates like natural stone, high-performance concrete, and anodized aluminum panels.

A leading industry trend involves non-staining silicone sealants, specifically formulated to maintain clean finishes on porous substrates while offering ±50% movement capability. The addresses one of the biggest concerns in architectural glazing and façade weatherproofing—the preservation of visual and structural integrity over decades of thermal cycling. Such low-modulus, high-recovery formulations (often achieving ≥80% elastic recovery after 28 days) ensure sustained façade resilience, particularly in high-rise buildings where mechanical fasteners alone are no longer viable.

As sustainability mandates reshape the global construction landscape, the elastomeric sealants industry is undergoing a rapid transition to eco-friendly, bio-based, and low-VOC formulations that comply with LEED, BREEAM, and other green building frameworks. These sustainable formulations integrate renewable raw materials, minimize hazardous emissions, and meet evolving health and environmental performance benchmarks.

A significant leap in material science comes from the replacement of traditional phthalate plasticizers with bio-derived alternatives, such as diacetyl epoxidized vegetable-oleic acid glyceride, derived from vegetable oils. These plasticizers retain the flexibility, softness, and adhesion required for high-performance sealants while offering biodegradability and non-toxicity. Parallel developments in polymer chemistry include bio-based acrylic and styrene-acrylic dispersions, verified to contain up to 50% renewable content using mass balance certification methods.

Regulatory pressure—particularly in the U.S. and European Union—continues to accelerate the trend. Standards such as EMICODE® EC1+ and Indoor Air Comfort Gold (IACG) certifications act as benchmarks for low-VOC and phthalate-free elastomeric sealants. These policies are pushing manufacturers to redesign entire product lines around carbon footprint reduction, renewable input sourcing, and superior indoor air quality performance, creating a decisive competitive advantage for sustainability-driven brands.

The ongoing global electrification wave presents a major growth frontier for elastomeric sealants designed for EV battery manufacturing, sealing, and thermal protection. These sealants must deliver exceptional heat resistance, dielectric strength, and fire-retardant performance under extreme operational environments—making them mission-critical for EV safety and performance optimization.

Modern flame-retardant silicone-based elastomers are achieving compliance with UL 94 V-0 vertical burn standards, self-extinguishing within 10 seconds without flaming drips—an essential benchmark for thermal runaway mitigation. Additionally, silicone-based gap fillers and Thermal Interface Materials (TIMs) feature thermal conductivities exceeding 3.0 W/m·K, ensuring optimal heat transfer between battery cells and cooling plates while maintaining system flexibility.

Gigafactories across Europe, North America, and Asia-Pacific are investing heavily in automated dispensing systems capable of applying these advanced sealants at scale. Each EV battery enclosure requires a combination of environmental sealing, vibration damping, and fireproof bonding, driving unprecedented demand for custom-formulated, high-volume elastomeric sealing compounds. These materials directly contribute to vehicle range enhancement, structural stability, and recyclability, aligning with automakers’ circular economy strategies.

The global adoption of mass timber construction—especially Cross-Laminated Timber (CLT) and Glulam—is redefining the use of elastomeric sealants in sustainable architecture. These wooden structures experience considerable dimensional movement due to moisture variations, necessitating high-flexibility, moisture-resistant sealants to ensure long-term air and weather barrier integrity.

Studies report that wood moisture content in mass timber can increase from 12–14% during fabrication to over 20% in exposed construction phases, often exceeding 30% in localized wetting zones. Such fluctuations can cause cracks, checks, and joint separations if sealants lack sufficient elasticity. Sealants with movement accommodation up to 25% of joint width have become essential for maintaining joint integrity and preventing air leakage in high-performance timber façades.

Modern building codes also emphasize airtightness and fire resistance. Specialized elastomeric sealants are being specified at mass timber intersections and rated joints to enhance fire-stop performance and energy efficiency. In tandem, the rapid growth of prefabricated CLT panel systems—which reduce on-site labor by up to 50%—has expanded demand for factory-applied and field-applied durable joint sealants that maintain flexibility and adhesion through transportation, installation, and long-term environmental exposure.

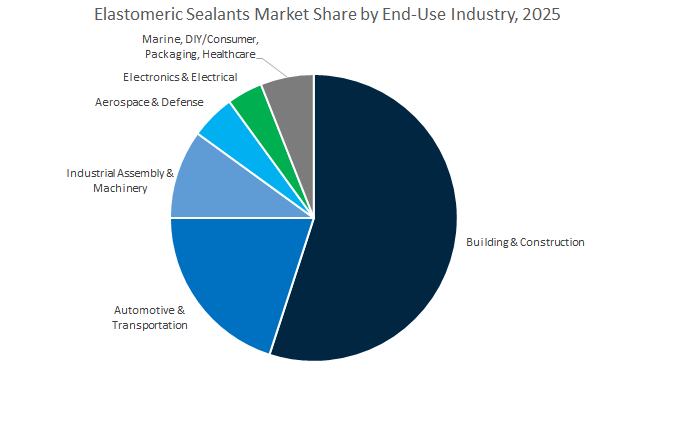

Elastomeric Sealants Market Share Insights, 2025-2034

The building and construction industry is the dominant consumer of elastomeric sealants, accounting for over half of the global market share. These sealants are indispensable in both residential and commercial construction, providing long-term flexibility, weatherproofing, and adhesion in critical applications such as expansion joints, curtain walls, glazing, façades, and roofing systems. Their superior movement capability enables structures to withstand thermal expansion, contraction, and seismic activity without cracking or losing adhesion. The segment’s dominance is underpinned by global trends in urbanization, infrastructure modernization, and sustainable building design, where energy efficiency and air-tightness are key performance criteria. Silicone, polyurethane (PU), and hybrid MS polymer-based elastomeric sealants are increasingly used to meet low-VOC, green building standards, particularly in North America, Europe, and rapidly industrializing Asia-Pacific markets. In addition, the increasing emphasis on retrofit and renovation projects across mature economies continues to boost demand for sealants used in re-caulking, waterproofing, and façade refurbishment. With smart cities and sustainable construction at the forefront, building & construction applications will remain the backbone of global elastomeric sealant demand, supported by ongoing innovations in UV-resistant, paintable, and fast-curing formulations.

The automotive and transportation industry represents a major pillar of the global elastomeric sealants market, fueled by growing vehicle production, electrification, and lightweight design trends. Sealants in this sector are critical for sealing body seams, bonding glass, encapsulating electrical components, and dampening noise and vibration (NVH). They must withstand extreme conditions including high temperatures, fuel exposure, and continuous mechanical stress, which has led to the widespread use of silicone and hybrid polyurethane systems. In electric vehicles (EVs), elastomeric sealants play an increasingly important role in battery pack sealing, insulation, and thermal management, ensuring safety and long-term performance. Moreover, the automotive aftermarket and maintenance segment continues to drive consistent demand for repair and resealing applications. The growing complexity of modern vehicles and increased reliance on automated and robotic assembly have also encouraged adoption of advanced, fast-curing formulations compatible with automated dispensing. With OEMs emphasizing lightweighting and structural integrity, elastomeric sealants are integral to both design and manufacturing—positioning this segment as a strategic growth engine within the global market.

Moisture-curing elastomeric sealants hold the largest share of the global market, driven by their exceptional balance of flexibility, adhesion, and weather resistance. These systems—based largely on polyurethane, silicone, and hybrid polymer technologies—cure upon exposure to ambient humidity, forming robust elastomeric joints capable of withstanding decades of environmental stress. Their versatility spans construction, automotive, marine, and industrial applications, where they are used for expansion joints, glazing, and panel bonding. Moisture-cure sealants are favored for their excellent movement capability, UV resistance, and adhesion to diverse substrates including concrete, metal, and plastics. As green building regulations tighten globally, manufacturers are increasingly developing low-VOC, isocyanate-free, and solvent-free formulations, reinforcing their sustainability profile. The ongoing shift toward hybrid silane-modified polymers (SMPs) is further enhancing this segment’s share, offering the benefits of both silicones and polyurethanes without their respective limitations. As infrastructure projects and building envelope designs become more sophisticated, moisture-curing elastomeric sealants will remain the industry’s performance benchmark.

Water-based elastomeric sealants represent a significant share of the global market, driven by their low environmental impact, ease of application, and cost-effectiveness. These formulations, often acrylic- or latex-based, are preferred for interior sealing, painting preparation, and DIY applications, where exposure to extreme weather or chemicals is minimal. The segment benefits from increasing regulatory restrictions on solvent-based formulations, particularly in North America and Europe, pushing both professional and consumer markets toward low-VOC, odor-free alternatives. Water-based elastomeric sealants are especially popular for perimeter sealing, caulking around windows and doors, and joint sealing in residential buildings. They are also compatible with paintable surfaces, enhancing their appeal in interior finishing and remodeling. Technological advancements have improved their adhesion, flexibility, and durability, enabling broader use in light commercial construction. As sustainability continues to guide formulation development, next-generation water-based sealants featuring bio-based polymers and enhanced moisture resistance are expected to expand this segment’s reach globally.

The global elastomeric sealants market is characterized by high technical specialization and consolidation among major players, including Dow Inc., Sika AG, H.B. Fuller, Wacker Chemie AG, and PPG Industries. These companies are leveraging innovation in silicone, polyurethane, and silane-modified polymer chemistry, coupled with digitalization and sustainability strategies, to capture long-term market leadership.

Dow Inc. maintains a global leadership position through its DOWSIL™ brand, delivering advanced silicone elastomers and thermally conductive sealants for EV battery assemblies, solar modules, and façade glazing. The 2023 launch of the DOWSIL™ PV series reinforced Dow’s presence in photovoltaic module sealing, ensuring long-term resistance to UV, heat, and weather exposure. The company’s carbon-neutral silicone initiative represents a major sustainability milestone, while its integrated global supply chain enables localized delivery for high-volume infrastructure and e-mobility projects.

Sika AG remains a front-runner in polyurethane and hybrid SMP sealant technology. Its proprietary Purform® chemistry sets new safety and compliance standards, eliminating health training requirements under REACH while enhancing mechanical strength and adhesion. The Sikaflex® range remains globally dominant in civil engineering joints and building envelope sealing, renowned for its chemical resistance and >25% movement capability. Sika’s infrastructure solutions, including tunneling and waterproofing sealants, continue to be integral to megaprojects worldwide.

H.B. Fuller focuses on flexible packaging, hygiene, and electronics with its Advantra® and Swift® elastomeric product lines. These offer low-temperature bonding and high elasticity, improving energy efficiency and production throughput. The company’s R&D centers emphasize bio-based adhesives and high-purity elastomeric formulations for medical and hygiene markets, where purity and elasticity are critical. Fuller’s strategic push toward sustainable packaging adhesives aligns with global initiatives for recyclable and circular economy materials.

Wacker Chemie AG is a major innovator in silicone-based elastomeric sealants, leveraging its vertically integrated production model to ensure cost stability and quality control. Its ELASTOSIL® eco 7770 P exemplifies next-generation sustainable silicone technology, offering low emissions and resistance to mold and mildew for architectural and natural stone applications. With growing investments in Asian R&D and manufacturing facilities, Wacker is targeting the green construction and façade restoration markets with a full portfolio of RTV silicones and hybrid polymers.

PPG Industries integrates its coatings and sealant expertise to offer durable elastomeric systems for architectural, industrial, and aerospace applications. Its polyurethane and acrylic sealants are widely used in façade restoration and infrastructure rehabilitation, benefiting from PPG’s strong distribution network. In aerospace, PPG develops high-temperature, chemical-resistant sealants meeting FAA and defense-grade standards, reinforcing its position in high-specification markets. The company’s global presence ensures seamless delivery and cross-market product adoption.

The United States elastomeric sealants market remains at the forefront of product innovation and environmental compliance, with a strong emphasis on low-VOC polyurethane and silicone elastomeric formulations. In January 2025, DuPont launched its Great Stuff Wide Spray Foam Sealant, engineered for superior air sealing and insulation performance in both commercial and residential construction. The product’s focus on energy efficiency and low emissions reflects growing alignment with U.S. green building certifications such as LEED and WELL.

Additionally, Balco’s introduction of its Elastomeric Expansion Seal System (ESS) in late 2024 represents a significant leap in the durability and waterproofing of high-traffic structures, including parking decks and open-air arenas. Regulatory enforcement by the EPA and state environmental agencies continues to drive market preference toward low-emission, high-flexibility sealants. The regulations have accelerated innovation in sustainable polyurethane and SMP-based elastomeric sealants, particularly for civil infrastructure upgrades under the Bipartisan Infrastructure Law.

Germany maintains its position as a European powerhouse in the automotive-grade and sustainable construction sealant markets. The country’s automotive industry, accounting for roughly 23% of the global premium car segment, has fueled a surge in demand for thermal-resistant silicone sealants and polyurethane-based elastomeric adhesives used in EV battery assembly and lightweight vehicle bonding. German manufacturers are prioritizing low-VOC, high-strength materials that enhance noise, vibration, and harshness (NVH) reduction while ensuring mechanical flexibility under thermal cycling.

The Energy Saving Ordinance (EnEV) further compels the adoption of high-durability, weatherproof elastomeric sealants to improve building energy performance. Leading companies such as Henkel and Wacker Chemie AG are heavily investing in R&D for silyl-modified polymer (SMP) and hybrid polymer sealants, optimizing adhesion, flexibility, and sustainability. The advancements support Germany’s commitment to the EU Green Deal and net-zero building standards, consolidating its leadership in the European elastomeric sealant technology sector.

China remains the largest global consumer of elastomeric sealants, driven by massive state-led infrastructure projects and the rapid scale-up of EV and electronics production. The nation’s aggressive urbanization initiatives and transportation infrastructure programs have created unprecedented demand for construction-grade polyurethane and silicone elastomeric sealants for bridges, high-rises, and smart city projects. The ongoing shift toward high-performance and weather-resistant formulations aligns with China’s Five-Year Plan for Sustainable Urban Development.

In a strategic move, Sika AG’s acquisition of Shenzhen Landun Holding has enhanced the company’s access to China’s booming construction and waterproofing markets, strengthening its regional presence in elastic waterproofing systems. Simultaneously, the rapid expansion of electronic manufacturing and EV assembly lines is spurring demand for specialty electronic-grade elastomeric sealants used in thermal management, insulation, and moisture barrier applications. The government’s push for self-sufficiency in advanced materials ensures continued local innovation and production expansion in high-durability silicone and polyurethane systems.

The India elastomeric sealants market is accelerating due to massive public infrastructure projects under initiatives such as ‘Housing for All’ and the National Infrastructure Pipeline (NIP). Rapid growth in transportation, residential, and commercial construction is fueling consistent demand for polyurethane and acrylic elastomeric sealants that provide durability, UV resistance, and flexibility under diverse climatic conditions. The construction sector’s preference for cost-efficient yet reliable materials positions elastomeric sealants as a core component in India’s urban development roadmap.

Domestic leaders like Pidilite Industries Ltd. are significantly expanding manufacturing capacity and supply chains to meet the fragmented yet growing demand for sealants across Tier II and Tier III cities. Additionally, rising adoption of green building certifications such as IGBC and GRIHA is increasing market interest in low-VOC and bio-based elastomeric sealants, particularly for premium commercial real estate projects. The focus on local production and eco-compliant formulations aligns with India’s Make in India strategy to promote sustainable industrial growth.

Japan stands as a global hub for specialty silicone elastomeric sealant innovation, characterized by its focus on precision engineering and high-performance materials. In May 2025, Shin-Etsu Chemical introduced new high-functionality silicone elastomeric products, extending applications beyond industrial sealing to include personal care and specialty coatings, reflecting Japan’s leadership in multi-market polymer technology.

Given Japan’s seismic vulnerability, building codes mandate ultra-flexible, high-elongation elastomeric sealants for facade glazing, expansion joints, and seismic dampening systems, ensuring long-term safety and resilience. Furthermore, the country’s robust electronics and automotive manufacturing base continues to drive demand for precision-applied, high-thermal-stability elastomeric sealants for component encapsulation and vibration control. The cross-sector synergy has made Japan a critical supplier of premium-grade, high-durability sealants in the global market.

South Korea is rapidly emerging as a technological leader in elastomeric silicone sealants, particularly within the battery manufacturing and electronics sectors. During Inter-Battery 2025, Elkem showcased advanced silicone-based thermal management sealants engineered to mitigate vibration, heat, and moisture exposure in high-energy-density EV batteries. The innovation aligns with South Korea’s strategy to reinforce its global leadership in lithium-ion battery technology and EV component manufacturing.

In parallel, KCC Silicone’s Harmonie™ NatuVel Gel received the Gold Award at In-Cosmetics Korea 2025, showcasing its excellence in advanced silicone chemistry—an innovation with potential industrial applications in marine, construction, and specialty sealant markets. South Korea’s shipbuilding and automotive exports, governed by strict performance and safety standards, continue to generate demand for marine-grade polysulfide and automotive elastomeric sealants capable of withstanding extreme conditions and chemical exposure.

The European Union remains a central hub for sustainability-driven transformation in the elastomeric sealants industry, influenced by stringent EU Green Deal, REACH, and Circular Economy Action Plan policies. The initiatives compel manufacturers to transition toward bio-based, ultra-low-VOC, and recyclable elastomeric formulations, minimizing environmental impact without compromising performance. The European Adhesive & Sealant Industry Association (FEICA) continues to lead R&D efforts on recyclable packaging, green formulations, and end-of-life recycling frameworks for sealant applications.

Market consolidation is another defining trend, highlighted by Soudal’s acquisition of Sharp Chemicals, expanding its regional footprint in industrial and construction-grade elastomeric sealants. European manufacturers are prioritizing sustainable SMP (Silyl-Modified Polymer) and solvent-free hybrid systems, optimized for building envelopes, window sealing, and energy-efficient construction across the region. The sustainability-led shifts are positioning Europe as the benchmark for environmentally compliant elastomeric sealant production.

Elastomeric Sealants Market Report Scope

Elastomeric Sealants Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$10.2 Billion

|

|

Market Size (2034)

|

$18 Billion

|

|

Market Growth Rate

|

6.5%

|

|

Segments

|

By Resin Type (Silicone, Polyurethane, Polysulfide, Silyl Modified Polymers, Acrylic, Butyl, Styrenic Block Copolymer, Polybutadiene, Other), By End-Use Industry (Building & Construction, Automotive & Transportation, Aerospace & Defense, Marine, Electronics & Electrical, Industrial Assembly & Machinery, Packaging, Healthcare & Medical, DIY/Consumer), By Functionality (Moisture-Cure, Solvent-Based, Water-Based, Hot-Melt, UV/Radiation-Cure, Two-Component Systems, One-Component Systems), By Application Type (Glazing, Joint Sealing, Weatherproofing, Roofing, Façade Sealing, Firestopping, Water/Thermal Barrier, Floor Sealing, Panel Bonding), By Packaging (Cartridges, Tubes, Pails/Drums, Sachets/Foils, Aerosol Cans, Bulk Containers

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Henkel AG & Co. KGaA, 3M Company, Sika AG, The Dow Chemical Company, H.B. Fuller Company, Arkema Group, RPM International Inc., Wacker Chemie AG, Pidilite Industries Ltd., Shin-Etsu Chemical Co., Ltd., PPG Industries, Inc., Sherwin-Williams Company, MAPEI S.p.A., DuPont de Nemours, Inc., KCC Corporation

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

By Resin Type

- Silicone

- Polyurethane

- Polysulfide

- Silyl Modified Polymers

- Acrylic

- Butyl

- Styrenic Block Copolymer

- Polybutadiene

- Other

By End-Use Industry

- Building & Construction

- Automotive & Transportation

- Aerospace & Defense

- Marine

- Electronics & Electrical

- Industrial Assembly & Machinery

- Packaging

- Healthcare & Medical

- DIY/Consumer

By Functionality/Curing

- Moisture-Cure

- Solvent-Based

- Water-Based

- Hot-Melt

- UV/Radiation-Cure

- Two-Component Systems

- One-Component Systems

By Application Type

- Glazing

- Joint Sealing

- Weatherproofing

- Roofing

- Façade Sealing

- Firestopping

- Water/Thermal Barrier

- Floor Sealing

- Panel Bonding

By Packaging

- Cartridges

- Tubes

- Pails/Drums

- Sachets/Foils

- Aerosol Cans

- Bulk Containers

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

- Henkel AG & Co. KGaA

- 3M Company

- Sika AG

- The Dow Chemical Company

- H.B. Fuller Company

- Arkema Group

- RPM International Inc.

- Wacker Chemie AG

- Pidilite Industries Ltd.

- Shin-Etsu Chemical Co., Ltd.

- PPG Industries, Inc.

- Sherwin-Williams Company

- MAPEI S.p.A.

- DuPont de Nemours, Inc.

- KCC Corporation

*- List not Exhaustive

Research Coverage

Prepared by USDAnalytics, this report investigates the Elastomeric Sealants Market, delivering analysis reviews of demand drivers, technology roadmaps, pricing and capacity shifts, and regulatory tailwinds shaping adoption across construction, transportation, energy, electronics, and marine. It highlights breakthroughs in ultra-low-VOC SMP systems, high-movement silicone façade weatherseals, REACH-aligned low-monomer PU chemistries, and EV-grade thermal/FR sealing compounds, while mapping how specification trends and nearshoring are reshaping converter economics and OEM qualification cycles. With granular country views and comparative performance benchmarking, this report is an essential resource for materials strategists, R&D and application engineers, sourcing leaders, and investment teams seeking decision-ready insights on elastic sealing technologies, end-use mix shifts, and 2025–2034 growth scenarios.

Scope Highlights

Segmentation:

- By Resin Type: Silicone; Polyurethane; Polysulfide; Silyl-Modified Polymers; Acrylic; Butyl; Styrenic Block Copolymer; Polybutadiene; Other.

- By End-Use Industry: Building & Construction; Automotive & Transportation; Aerospace & Defense; Marine; Electronics & Electrical; Industrial Assembly & Machinery; Packaging; Healthcare & Medical; DIY/Consumer.

- By Functionality/Curing: Moisture-Cure; Solvent-Based; Water-Based; Hot-Melt; UV/Radiation-Cure; Two-Component Systems; One-Component Systems.

- By Application Type: Glazing; Joint Sealing; Weatherproofing; Roofing; Façade Sealing; Firestopping; Water/Thermal Barrier; Floor Sealing; Panel Bonding.

- By Packaging: Cartridges; Tubes; Pails/Drums; Sachets/Foils; Aerosol Cans; Bulk Containers.

Geographic Scope: Analysis spans 25+ countries across North America, Europe, Asia Pacific, Latin America, the Middle East & Africa.

Time Frame: Historic data 2021–2024 and forecast data 2025–2034.

Companies: 15+ company analyses/profiles covering portfolios, innovations, sustainability pathways, and go-to-market strategies.

Deliverables

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.