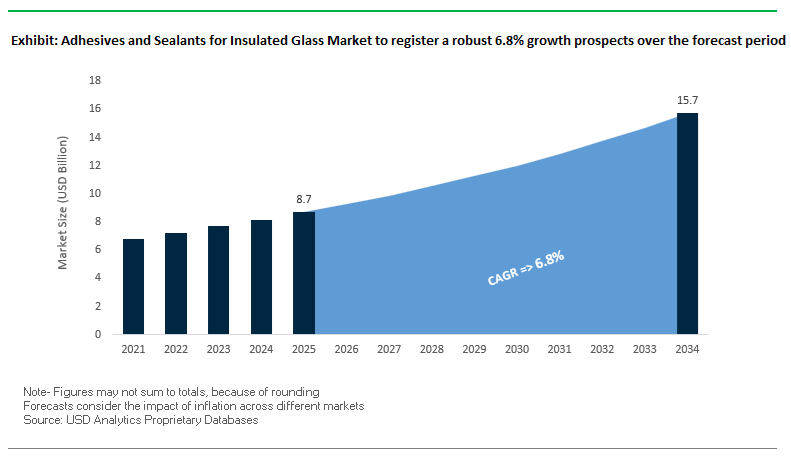

The global adhesives and sealants for insulated glass market is projected to reach $15.7 billion by 2034, growing from $8.7 billion in 2025 at a robust CAGR of 6.8%. This growth is driven by the surging demand for energy-efficient building materials, high-performance façade systems, and next-generation glazing units used in both residential and commercial construction. The market’s trajectory is closely tied to evolving global energy codes, sustainability certifications, and the shift toward low-VOC, long-life silicone and polyurethane sealant systems.

Industry professionals are focusing on advanced sealant formulations that maintain gas retention, UV stability, and long-term adhesion, particularly for structural glazing applications. Meanwhile, automotive manufacturers are rapidly adopting insulated glass (IG) adhesives to enhance passenger comfort, acoustic insulation, and vehicle efficiency. Distributors and manufacturers are addressing the growing regional variations in standards, especially across the APAC, European, and North American markets, where energy performance mandates are accelerating innovation in IG materials and sealant chemistry.

- Energy Efficiency Leadership: Building and construction applications account for nearly $2.1 billion of the total market, driven by stringent global insulation standards and sustainability initiatives.

- Silicone Sealants Lead Performance: Silicone-based adhesives dominate the market for insulated glass units (IGUs), offering unmatched UV resistance, flexibility, and long-term durability in structural applications.

- Automotive IG Integration: The automotive insulated glass segment, valued at around $0.7 billion in 2023, is witnessing fast growth due to the demand for lightweight and thermally efficient glazing systems.

- R&D and Sustainability as Growth Catalysts: Over half of competitive differentiation stems from R&D investment in smart, eco-friendly formulations that comply with LEED and BREEAM green building standards.

- APAC Expansion: The Asia-Pacific market is witnessing rapid adoption in high-rise and infrastructure projects that depend on durable, climate-adapted IG sealant technologies.

The global insulated glass adhesives and sealants industry is undergoing rapid transformation, marked by consolidation, regional capacity expansion, and the launch of sustainable product lines. In July 2025, MAPEI Group expanded its global footprint by acquiring Wecal (Netherlands) and Wykamol (UK)—two major players in insulation and waterproofing systems—strengthening its integrated building envelope offerings and ensuring greater distribution reach for IG installation products. Similarly, Saint-Gobain announced significant capital and R&D investments in March 2025, aligned with its carbon reduction roadmap. These investments are set to influence the downstream supply of eco-friendly IG materials and adhesive systems that meet the next generation of energy-efficient building codes.

In January 2025, Fenzi Group strategically acquired Johnson Matthey’s Advanced Glass Technologies (AGT) business, broadening its solutions portfolio to encompass glass enamels and functional coatings. This vertical integration gives Fenzi greater leverage in providing comprehensive solutions to glass fabricators and IG producers. Regulatory developments have further reinforced the market’s growth: the 2024 IECC energy code revisions (Q4 2024) impose tighter U-factor and SHGC limits, compelling builders to specify advanced gas-retentive IG sealants for compliance.

From a product innovation perspective, Dow Performance Silicones highlighted its low embodied carbon DOWSIL™ Silicones in late 2024, which come with third-party PAS 2060 certification—a major appeal for green-certified façade projects. Around the same time, Sika AG showcased its flagship Sikasil® IG-25 HM Plus, designed for 30+ years of gas retention and superior mechanical strength. H.B. Fuller’s Kömmerling division continued to lead with its KÖDISPACE 4SG spacer system (Q3 2024), a next-gen solution that eliminates metal thermal bridges and enhances IGU thermal efficiency. Meanwhile, sustained urban infrastructure investments across China and the broader APAC region in H1 2024 continue to drive unprecedented demand for locally produced, high-durability IG adhesives and sealants.

The accelerating global drive toward low-energy and passive building designs has spurred the replacement of traditional aluminum spacers in insulated glass units (IGUs) with warm-edge materials such as stainless steel, thermoplastics, and polymeric foams. These advanced spacer systems drastically reduce heat transfer across the window edge, driving the need for next-generation hybrid sealant formulations that can maintain adhesion, flexibility, and gas retention under varying thermal and mechanical stresses.

The thermal conductivity of modern warm-edge spacers—as low as 0.16 W/m²K—represents a more than 1,000x improvement compared to conventional aluminum spacers, which reach up to 160 W/m²K. The quantum leap in thermal insulation is a key enabler for high-efficiency glazing systems meeting Passive House and Zero-Energy Building standards. Research further indicates that warm-edge spacer integration improves overall window U-values by 5–18%, depending on configuration, delivering measurable energy savings and compliance with evolving building codes in the EU, U.S., and Asia-Pacific.

To support these new spacer materials, manufacturers are rapidly deploying hybrid sealant systems that combine foam and stainless steel components, optimizing both thermal performance and mechanical resilience. However, the inclusion of flexible warm-edge components presents fresh challenges for sealant design. Sealants must exhibit higher elastic recovery, lower gas and moisture vapor transmission rates (MVTR), and enhanced adhesion to low-energy substrates—capabilities that are driving research into hybrid silicone-polysulfide and thermoplastic formulations tailored for modern fenestration systems.

The architectural trend toward expansive, high-span glass façades and curved glazing is reshaping demand for structural-grade adhesives and sealants capable of withstanding extreme mechanical stress, thermal cycling, and UV exposure over extended service lives. Modern jumbo insulated glass units (IGUs)—frequently exceeding 7 m² in surface area—require sealants that combine exceptional modulus, adhesion strength, and weatherability while accommodating large-scale deflections under environmental loads.

For example, under a 40 psf wind load, a 72x144-inch IGU can experience a center deflection of over 1.4 inches, placing significant strain on edge seals. In such applications, conventional polysulfide and polyurethane systems fail to maintain integrity over time, leading to gas leakage and edge seal fatigue. Comparative field data report that IGUs using polyisobutylene (PIB) primary seals combined with silicone secondary seals show a cumulative field failure rate of only 1% after 20 years, compared to over 9% failure within 15 years for conventional dual polysulfide systems.

The superior durability is primarily attributed to the temperature-independent permeability stability of silicone sealants, which exhibit minimal degradation in high-UV or thermally dynamic environments. As a result, leading glass fabricators are standardizing high-modulus silicone and modified polymer sealants for structural glazing, large façade units, and curved glass applications, where elasticity and structural adhesion are both critical to long-term performance.

The shift toward advanced silicone-based and hybrid sealants is redefining the competitive landscape, emphasizing performance longevity, weather resistance, and regulatory compliance—particularly in large-scale architectural and energy-efficient façade applications.

Market Opportunity 1: Retrofitting Wave Driven by Energy Efficiency Legislation and Renovation Programs

The global building retrofitting boom presents one of the largest growth avenues for the adhesives and sealants for insulated glass industry. Regulatory frameworks such as the EU Energy Performance of Buildings Directive (EPBD), targeting climate neutrality by 2050, are compelling large-scale window replacement and energy retrofits. The building sector—responsible for roughly 40% of Europe’s total energy consumption and 36% of CO₂ emissions—is under direct pressure to transition toward high-performance IGUs that meet the latest thermal and emission benchmarks.

The shift is creating immense aftermarket demand for retrofit-compatible insulated glass adhesives that facilitate on-site refurbishment, resealing, and reassembly of existing glazing units. The Empire State Building retrofit project serves as a benchmark example: its transformation from double IGUs to triple-glazed, warm-edge, low-E units resulted in 1,150 tons of CO₂ reduction annually, validating both the sustainability and financial viability of retrofit programs.

Further data indicate that replacing outdated double-glazed units (U-value ≈ 2.7 W/m²K) with modern triple-glazed IGUs (U-value ≈ 0.5 W/m²K) can deliver up to 80% improvement in thermal efficiency, driving unprecedented growth in retrofit sealant systems. Distributors and manufacturers offering fast-curing, compatible sealants for modular replacement and secondary sealing applications are well-positioned to capture the rapidly expanding market, supported by government subsidies and green-building incentives.

Market Opportunity 2: R&D Acceleration in Vacuum Insulating Glass (VIG) Edge-Sealing Technologies

The emergence of Vacuum Insulating Glass (VIG) represents a game-changing advancement in thermal insulation for both commercial and residential glazing systems. Delivering U-values as low as 0.2 W/m²K, VIG technology is redefining the upper limit of window energy performance. However, the advancement relies heavily on breakthroughs in hermetic edge-sealing materials that can maintain a stable vacuum environment over decades of operational life.

Unlike traditional dual-seal IG systems, VIG requires ultra-low-permeability, gas-impermeable edge bonds that can sustain vacuum pressures and resist mechanical fatigue under temperature cycling. Research indicates that if just 25.6 million UK homes adopted VIG technology, national CO₂ emissions could drop by 40 million tonnes annually, underscoring its immense environmental potential and policy relevance.

To meet these demands, R&D efforts are increasingly focusing on laser-assisted hermetic sealing methods using glass frit inks for localized heating and bonding, offering scalable, low-cost manufacturing pathways that replace conventional organic sealants. These innovations, led by government-funded laboratories and industrial research alliances, are paving the way for commercial-scale production of next-generation VIG systems with superior gas retention and lifetime durability.

Adhesives and Sealants for Insulated Glass Market Share Insights, 2025-2034

The silicone segment leads the global adhesives and sealants for insulated glass (IG) industry, accounting for approximately 35% of total market share in 2025. Silicone remains the structural backbone of modern IG systems due to its exceptional UV stability, elasticity, and resistance to temperature extremes. It serves as the secondary sealant in dual-seal insulated glass units (IGUs), ensuring long-term adhesion between glass panes while maintaining flexibility under wind load and thermal stress. Its superior weatherability and compatibility with glass coatings make it indispensable in structural glazing, high-rise façades, and curtain wall systems, where mechanical durability and longevity are paramount. The growing demand for energy-efficient and aesthetically advanced architectural designs, especially in LEED and BREEAM-certified buildings, further strengthens silicone’s dominance. Moreover, advancements in neutral-cure and high-modulus silicone formulations have extended its usability in high-performance façade assemblies and triple-glazed systems, reinforcing its reputation as the industry’s gold standard for IG sealing applications.

The polyisobutylene (PIB) segment, holding around 25% market share, remains the irreplaceable primary sealant in insulated glass production. PIB’s unmatched moisture vapor transmission resistance (MVTR) is critical to preventing fogging and maintaining the thermal insulation efficiency of IGUs over decades of service life. Its flexibility and excellent adhesion to glass and spacer bars make it essential as the first line of defense against moisture ingress and gas leakage. PIB is typically used in combination with silicone, polyurethane, or polysulfide in dual-seal systems, providing both mechanical stability and long-term hermetic sealing. The continued focus on energy-efficient window systems and gas-filled glazing units (argon, krypton) sustains PIB’s dominant role, as no alternative material has yet matched its moisture barrier performance. As smart glass and dynamic glazing technologies advance, PIB’s compatibility with metallic spacers and coatings ensures its relevance in next-generation IG manufacturing, solidifying its position as the foundation of IG durability and performance.

The polyurethane and hybrid (SMP) segments are emerging as key growth drivers in the insulated glass adhesives and sealants market, with PURs valued for their mechanical strength and chemical resistance in automotive and industrial applications, and SMP hybrids gaining traction in architectural glazing as low-VOC, paintable, and durable solutions suited for modern façades and energy-efficient buildings. These hybrid systems offer strong adhesion to coated and low-energy glass while delivering superior aging resistance, aligning with global sustainability and green construction standards. In contrast, polysulfide and hot-melt acrylic sealants represent more mature segments, with polysulfides declining due to environmental and performance limitations despite their continued use in niche industrial applications. Hot-melt butyl and acrylic variants remain relevant in high-speed automated production environments where cost efficiency, processability, and rapid assembly are priorities, particularly in residential and mid-tier commercial glazing.

The building and construction segment overwhelmingly dominates the adhesives and sealants for insulated glass (IG) market, commanding an estimated 85% share in 2025. This dominance is driven by the global push for energy-efficient building envelopes, sustainable architecture, and advanced façade engineering. IG sealants are vital to ensuring the long-term structural integrity, thermal performance, and weatherproofing of double- and triple-glazed window units used in commercial towers, residential complexes, and institutional buildings. With net-zero energy goals and stringent building codes promoting low-emission and high-insulation glazing, the demand for high-performance IG sealants—particularly silicones and polyisobutylenes—has surged. In addition, modern architectural trends such as unitized curtain walls, frameless façades, and dynamic glass systems are increasing the technical requirements for sealant flexibility, adhesion, and UV stability. Leading global construction projects rely on sealant systems that can withstand decades of thermal expansion, wind load stress, and condensation resistance. The rapid adoption of smart glazing and solar control glass is also creating opportunities for advanced hybrid sealants that balance transparency, durability, and environmental compliance.

The automotive and transportation segment, accounting for around 10% of total market share, represents a specialized but growing niche within the insulated glass industry. IG adhesives and sealants are critical for panoramic sunroofs, heated windshields, and side glazing in high-end vehicles, where clarity, flexibility, and resistance to vibration and automotive fluids are essential. The rise of electric and autonomous vehicles (EVs and AVs) is reshaping automotive design, increasing the use of multi-layer glass assemblies for thermal insulation, noise reduction, and improved visibility. This evolution has boosted demand for high-performance polyurethane, silicone, and hybrid sealants capable of enduring extreme conditions such as temperature fluctuations, mechanical stress, and UV exposure. Moreover, automakers are emphasizing lightweight bonding materials to enhance efficiency without compromising safety, giving distributors and suppliers an opportunity to provide OEM-grade, high-specification IG sealants tailored to mobility applications. As automotive glazing transitions toward integrated smart glass and solar-absorbing technologies, the sealant market for this segment will continue expanding, driven by innovation and functional design integration.

Market Share by End-Use Application, 2025.png)

The appliances and specialty applications segment, though smaller, occupies an important role in the IG sealant ecosystem. This category includes applications in refrigeration units, oven doors, display cases, and solar panels, where IG assemblies must endure thermal cycling, condensation, and cleaning agent exposure. The segment’s growth is underpinned by the trend toward energy-efficient appliances and transparent insulation technologies, which require high-performing sealants with low outgassing and stable adhesion across temperature extremes. Silicone and hot-melt butyl sealants are particularly favored for refrigerator glass doors, while hybrid and acrylic sealants are used in solar collector panels and photovoltaic glass modules to ensure air-tightness and long-term UV stability.

The competitive landscape of the adhesives and sealants for insulated glass market is defined by innovation in silicone, polyurethane, and reactive thermoplastic technologies. Leading players—including H.B. Fuller, Sika AG, Dow Performance Silicones, Kömmerling Chemische Fabrik GmbH, and MAPEI Group—are focusing on sustainability, automation compatibility, and energy efficiency. Their strategies emphasize regional manufacturing expansion, digital integration, and carbon-neutral product portfolios, ensuring resilient supply chains and compliance with global performance standards.

H.B. Fuller stands as a leader in insulated glass sealants through its Kömmerling brand, leveraging reactive thermoplastic (4SG) technology that simplifies IGU production. Its KÖDISPACE 4SG system replaces conventional spacers and primary seals, reducing manufacturing steps and improving gas retention. The company’s focus on sustainable building materials aligns with its CO₂ reduction objectives and top-tier Psi values, which minimize heat loss at the glass edge. Furthermore, H.B. Fuller’s integration of single-line IG production technology supports efficiency in both residential and commercial façade glazing applications.

Sika AG continues to set the benchmark for structural glazing sealants with its Sikasil® IG-25 HM Plus, engineered for exceptional mechanical strength and 30-year gas retention. Its IG silicone line provides unmatched UV resistance and compliance with major international standards such as ASTM and EOTA ETAG. Beyond product performance, Sika supports design freedom by enabling slim-edge sealing systems in large glass façades, empowering architects to achieve visually striking and durable energy-efficient designs.

Dow Performance Silicones has taken a leadership position in low embodied carbon adhesives with its DOWSIL™ product range, which includes verified carbon-neutral formulations (PAS 2060). Its two-part, high-modulus sealants, such as DOWSIL™ 3362, enable faster curing times and higher throughput in automated IGU lines. Dow’s system compatibility with both traditional and thermoplastic spacers ensures seamless integration for modern insulated glass manufacturers pursuing net-zero-ready façades and sustainable construction goals.

As a dedicated glass and window adhesive specialist under H.B. Fuller, Kömmerling Chemische Fabrik GmbH continues to expand its global impact. Its product suite spans polysulfide, polyurethane, and silicone technologies for IG applications across architectural, transport, and renewable energy sectors. With a focus on high adhesion, vibration resistance, and UV stability, Kömmerling serves as a one-stop provider for globally certified IG sealant solutions, supported by H.B. Fuller’s extensive R&D and international supply chain.

MAPEI Group leverages its broad construction chemistry expertise to provide comprehensive solutions for IG and façade systems. With €4.4 billion in 2024 turnover and major investments exceeding €213 million, MAPEI is strengthening its sealant production and distribution networks across Europe, the Middle East, and North America. Its product range—MAPEFLEX MS hybrid sealants and MAPESIL AC silicones—supports a wide array of IG applications. MAPEI’s acquisitions of Wecal and Wykamol in 2025 enhance its offering of integrated waterproofing and insulation systems, positioning it as a holistic partner for sustainable building envelope solutions.

The United States insulated glass (IG) adhesives and sealants market is undergoing a period of rapid transformation, driven by technological innovation, sustainability mandates, and automation investment. Manufacturers are actively developing hybrid polymer and SMP-based (Silane Modified Polymer) sealants, which are increasingly dominating structural glazing applications due to their exceptional flexibility, weather resistance, and compliance with stringent U.S. building codes (2025). The technological evolution supports the industry’s push toward high-performance bonding systems capable of delivering long-term adhesion in energy-efficient façade and window installations.

The rising focus on low-VOC and environmentally sustainable sealants aligns with the nationwide growth of LEED-certified construction projects, where material selection directly influences compliance with sustainability certifications. Automation adoption is another defining trend — large-scale commercial projects are integrating robotic dispensing systems to enhance sealant application precision, reduce waste, and minimize labor costs (2024). The surge in energy-efficient retrofitting and window replacement projects, alongside a strong rebound in residential construction, is further propelling the market. With the integration of reactive adhesive chemistries and automation in manufacturing, the U.S. market is setting new benchmarks for high-performance, sustainable, and efficient insulated glass sealant systems.

Germany represents the epicenter of technological innovation and sustainability in the European insulated glass sealants market, propelled by sweeping EU regulatory frameworks. Manufacturers are aligning with the EU Energy Performance of Buildings Directive (EPBD), mandating Zero-Emission Buildings (ZEBs) by 2030, a regulation that places airtight, high-durability IG sealants at the core of compliance strategies (2024–2025). Additionally, the EU’s Whole Life Carbon Directive—requiring Global Warming Potential (GWP) disclosure from 2028 onwards—is catalyzing the development of low-embodied carbon PIB (Polyisobutylene) and polysulfide sealants, driving the shift toward circular, sustainable materials.

German R&D centers are leading breakthroughs in cold-bent glazing applications, where advanced PIB-based primary sealants and structural polysulfide systems ensure long-term gas retention and flexibility under thermal and mechanical stress. Industry-wide compliance with EN 1279 standards remains central, guiding both product certification and performance benchmarking across Europe’s architectural glazing market. The country’s expertise in energy-efficient building technologies, coupled with regulatory-driven innovation, solidifies Germany’s role as a leader in high-performance insulated glass sealant solutions for the European Union and beyond.

China’s insulated glass adhesives and sealants industry continues to expand on the back of massive infrastructure investments, automotive manufacturing growth, and domestic raw material production. The nation’s rapid urbanization and large-scale high-rise development are sustaining robust demand for silicone and PIB-based sealants in curtain wall and façade glazing (2024–2025). Simultaneously, China’s leadership in silicone feedstock production has made it a global supply chain influencer for structural glazing and IG sealant materials, with domestic manufacturers aggressively scaling production capacity to meet both domestic and export needs.

The country’s EV and transportation industries are emerging as new demand pillars, utilizing specialized PIB-enhanced bonding systems for battery pack assembly, noise insulation, and structural bonding. Moreover, China’s environmental policies are pushing adhesive producers to shift rapidly from solvent-based to water-based and solvent-free formulations, promoting green construction materials aligned with national sustainability goals. With growing government incentives for energy-efficient buildings and increased local innovation, China remains the largest and fastest-growing market for high-performance IG sealant systems worldwide.

The United Kingdom insulated glass adhesives and sealants market is being reshaped by tightening energy-efficiency regulations and future-focused building standards. The Future Homes Standard (FHS)—coming into force in 2025—mandates up to an 80% reduction in carbon emissions from new homes, necessitating the use of premium, high-performance secondary sealants that deliver superior airtightness and long-term insulation (2025). The regulatory shift is pushing both domestic and international manufacturers to accelerate innovation in low-emission and high-barrier IG sealing compounds.

Updates to Building Regulations Part L (focused on energy conservation) have elevated the minimum Window Energy Rating (WER) requirements, intensifying the need for high-thermal-performance IG units. In parallel, industry certification schemes such as FENSA are modernizing compliance protocols to ensure that both new installations and replacement glazing meet upgraded sealing and insulation standards. The reforms, combined with a growing focus on carbon-efficient construction materials, position the UK as one of Europe’s most regulation-driven and sustainability-oriented markets for IG adhesives and sealants.

Japan’s insulated glass adhesives and sealants industry emphasizes precision, safety, and technological resilience, reflecting the country’s unique geological and engineering challenges. A strong emphasis is placed on anti-seismic and high-modulus silicone formulations, specifically engineered for structural glazing systems capable of absorbing extreme stress and vibration. The advanced sealant technologies ensure long-term façade integrity in both high-rise and earthquake-prone regions (2024).

The market’s orientation toward high-tech and specialty applications extends to electronics, cleanroom construction, and advanced architectural glazing systems. Academic institutions and private R&D initiatives are increasingly collaborating to develop liquid silicone rubber (LSR) and hybrid polymer systems with improved elasticity, cure speed, and durability (2025). The material innovations are gradually influencing insulated glass production, driving greater performance uniformity and lifecycle efficiency. With its deep-rooted commitment to materials innovation and safety standards, Japan continues to define Asia’s benchmark for high-performance insulated glass sealant technology.

Canada’s insulated glass sealants market is expanding steadily, supported by provincial energy-efficiency codes and rapid adoption of triple-glazed IG units to improve thermal performance in extreme climates. New energy codes—implemented in provinces such as British Columbia and Ontario—are driving builders toward wider IG units, which require higher-grade primary and secondary sealants to ensure argon/krypton gas retention and long-term performance (2025).

Local manufacturers like PFG Glass are leading modernization efforts with fully automated IG lines (using Lisec and Forel systems), integrating precision PIB and silicone dispensing equipment with vacuum chambers for optimal gas fill. The automation investments underscore a shift toward mass production of high-quality, energy-efficient IG units. Compliance with ASTM E2190 standards remains a key certification benchmark for all materials, particularly sealants and spacers, ensuring durability and condensation resistance in cold climates. Canada’s dual focus on process automation and thermal code compliance positions it as a North American leader in energy-efficient insulated glazing solutions.

Adhesives and Sealants for Insulated Glass Market Report Scope

Adhesives and Sealants for Insulated Glass Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$8.7 Billion

|

|

Market Size (2034)

|

$15.7 Billion

|

|

Market Growth Rate

|

6.8%

|

|

Segments

|

By Product Type (Silicone, Polyisobutylene (PIB), Polysulfide, Polyurethane (PUR), Hot-Melt, Hybrid, Acrylic), By Function (Primary Sealants, Secondary Sealants), By Technology (Single-Component, Two-Component, Solvent-Based, Water-Based, Reactive, Hot-Melt), By End-Use (Building & Construction, Automotive & Transportation, Appliances & Others

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Dow Inc., Henkel AG & Co. KGaA, Sika AG, H.B. Fuller Company, Wacker Chemie AG, Tremco Group (RPM International Inc.), Arkema S.A. (Bostik), 3M Company, Momentive Performance Materials Inc., KCC Corporation, BASF SE, Gurit Holding AG, Ashland Global Holdings Inc., PPG Industries, Inc., Dymax Corporation

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

By Product Type (Sealant Resin)

- Silicone

- Polyisobutylene (PIB)

- Polysulfide

- Polyurethane (PUR)

- Hot-Melt

- Hybrid

- Acrylic

By Component/Function

- Primary Sealants (Gas/Moisture Barrier)

- Secondary Sealants (Structural/UV Resistance)

By Technology/Formulation

- Single-Component

- Two-Component

- Solvent-Based

- Water-Based

- Reactive

- Hot-Melt

By End-Use Industry

- Building & Construction

- Automotive & Transportation

- Appliances & Others

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

- Dow Inc.

- Henkel AG & Co. KGaA

- Sika AG

- H.B. Fuller Company

- Wacker Chemie AG

- Tremco Group (RPM International Inc.)

- Arkema S.A. (Bostik)

- 3M Company

- Momentive Performance Materials Inc.

- KCC Corporation

- BASF SE

- Gurit Holding AG

- Ashland Global Holdings Inc.

- PPG Industries, Inc.

- Dymax Corporation

*- List not Exhaustive

Research Coverage

This report investigates the growth mechanics of adhesives and sealants for insulated glass (IG) across building façades, retrofits, automotive glazing, and specialty appliances, mapping how codes, warm-edge spacers, and secondary silicone systems converge to lift long-life performance and energy yield. Compiled by USDAnalytics, the study’s analysis reviews regulatory inflection points (IECC/EPBD), durability benchmarks (gas retention, MVTR, UV stability), and supply moves (capacity, M&A) to isolate profit pools and risk. It surfaces breakthroughs in hybrid SMP silicones, vacuum insulating glass (VIG) edge technologies, carbon-neutral formulations, and automated IGU lines, and highlights sourcing and specification levers that compress total cost of ownership while meeting LEED/BREEAM targets. With scenario-tested forecasts to 2034, vendor scorecards, and retrofit playbooks, this report is an essential resource for product, procurement, technical, and sustainability leaders planning portfolios, plants, and partnerships in the IG value chain. Scope includes

- By Product Type (Sealant Resin): Silicone; Polyisobutylene (PIB); Polysulfide; Polyurethane (PUR); Hot-Melt; Hybrid; Acrylic.

- By Component/Function: Primary Sealants; Secondary Sealants.

- By Technology/Formulation: Single-Component; Two-Component; Solvent-Based; Water-Based; Reactive; Hot-Melt.

- By End-Use Industry: Building & Construction; Automotive & Transportation; Appliances & Others.

- Geographic Scope: Analysis spans 25+ countries across North America, Europe, Asia Pacific, Latin America, the Middle East & Africa.

- Historic & Forecast Window: 2021–2024 history and 2025–2034 forecasts.

- Companies: Analysis/profiles of 15+ companies.

Deliverables

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.