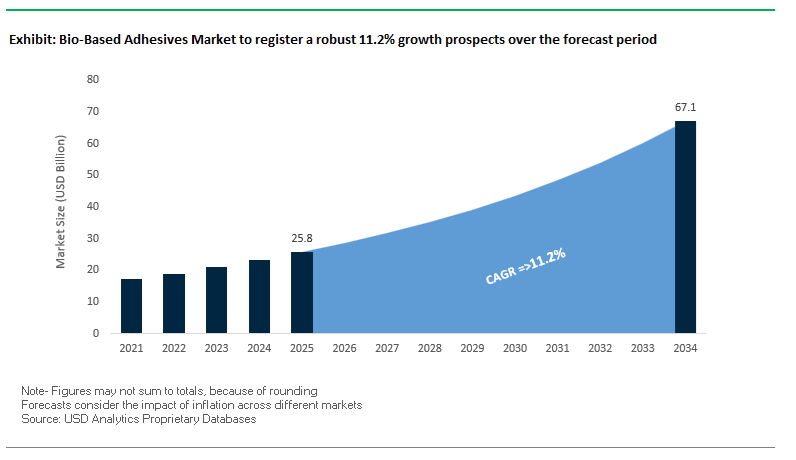

Bio-based adhesives have moved from niche sustainability solutions to strategically relevant industrial materials as OEMs across packaging, wood composites, construction, and consumer goods align material choices with decarbonization, VOC reduction, and renewable-content mandates. The market, forecast to expand from USD 25.8 billion in 2025 to USD 67.1 billion by 2034 at a CAGR of 11.2%, is being reshaped by procurement policies that increasingly prioritize bio-carbon content, formaldehyde-free systems, and traceable feedstock sourcing. For manufacturers, bio-based adhesives sit at the intersection of regulatory compliance, brand sustainability commitments, and performance parity with petrochemical incumbents.

The core structural shift is the transition from fossil-derived polymers to bio-circular resin platforms engineered to integrate into existing adhesive manufacturing and converting lines. Leading adhesive producers are incorporating ISCC PLUS–certified renewable inputs—such as tall-oil derivatives, sugarcane-based polyols, and bio-attributed tackifiers—while publicly targeting full renewable carbon substitution over the next decade. This shift is not cosmetic; it reflects OEM demand for verifiable carbon accounting and supply-chain transparency without sacrificing throughput or process stability. Bio-circular hot melt adhesives certified under ISCC PLUS are increasingly specified in high-volume packaging applications, where traceability and low-VOC processing are contractual requirements rather than optional differentiators.

Material substitution is accelerating as professionally engineered bio-resins close historical performance gaps. Glyoxal-modified and premethylolated lignin systems are achieving adhesion strengths up to 0.8 MPa in engineered wood panels, enabling replacement of conventional UF and PF resins in selected interior applications. In parallel, soy-protein adhesives crosslinked with polyamidoamine-epichlorohydrin (PAE) chemistries are delivering wet shear strengths approaching 3 MPa, directly addressing moisture resistance limitations that once constrained natural adhesives. These performance benchmarks translate into measurable business outcomes: reduced formaldehyde emissions, improved worker safety, compatibility with existing press cycles, and access to green building and eco-label certifications. Over the forecast period, continued innovation in renewable polyols, lignin functionalization, and cure-speed optimization positions bio-based adhesives as scalable, compliant solutions for both structural and high-performance bonding—provided manufacturers maintain feedstock certification, formulation consistency, and qualification alignment with evolving OEM and regulatory standards.

The bio-based adhesives industry is witnessing rapid innovation and investment across diverse end-use sectors—from packaging and construction to consumer goods and automotive interiors. Manufacturers are aggressively reformulating products to comply with stringent VOC limits, increase renewable content, and improve mechanical performance parity with petrochemical systems.

In September 2025, BioBond launched BioMelt™, a biodegradable, plant-derived nail adhesive targeting the beauty and consumer markets. This marked one of the first successful crossovers of bio-based polymers into high-value personal care applications, signifying the scalability of renewable polymer chemistry beyond industrial uses. By July 2025, H.B. Fuller advanced its Advantra® Earthic™ 9370 hot melt adhesive, featuring ISCC PLUS certified bio-circular content, further aligning packaging adhesives with low-carbon circularity goals. The same year, Ahlstrom expanded the applicability of lignin—a critical bio-adhesive precursor—by launching its ECO™ filtration range, validating lignin’s performance in automotive and industrial filtration systems.

Earlier, in February 2025, BioBond Adhesives introduced its BioAdhere™ line of zero-microplastic, odor-free, USDA BioPreferred adhesives, targeting wood and wallpaper markets. This underlines the commercial viability of bio-polymers in large-scale manufacturing.

Ahlstrom’s December 2024 unveiling of a fiber-based transparent tape backing represented another step toward plastic-free tapes, a development expected to accelerate demand for bio-compatible adhesive systems in labeling and packaging.

Beyond product launches, sustainability commitments remain a key driver of industry transformation. H.B. Fuller’s 2024 pledge to the Science Based Targets initiative (SBTi) marked a strategic milestone, incorporating Scope 3 emissions and compelling its raw material suppliers to transition to certified low-carbon feedstocks.

A major evolution is underway in the bio-based adhesives market as manufacturers transition from first-generation, food-competing feedstocks—such as corn starch and soy protein—to advanced non-food biomass sources like lignin, agricultural waste, and industrial by-products. The strategic shift not only reduces dependency on food crops but also strengthens the environmental credentials of bio-adhesive formulations, positioning them as essential components of the low-carbon materials economy.

Leading industrial wood product manufacturers, such as Latvijas Finieris, have integrated lignin-based adhesives in plywood production. These lignin-enhanced adhesives partially replace phenol-formaldehyde (PF) resins, delivering comparable or superior thermal stability and bonding strength while reducing petrochemical dependency. The innovation represents one of the most successful examples of valorizing lignin, a byproduct of the pulp and paper industry, into commercial-grade bio-adhesive applications.

A landmark initiative by Sweden’s innovation agency Vinnova, the BioGlue-Centre, has secured over SEK 100 million (≈ USD 9.5 million) in funding to accelerate research into high-performance bio-adhesives derived from forestry and agricultural by-products. The center—supported by 12 industry partners and multiple universities—aims to replace fossil-based binders across furniture, packaging, and construction applications, bridging the existing technological gap in scalable, non-food biomass adhesives.

At the Fraunhofer WKI Institute, humins—dark, viscous by-products from polyethylene furanoate (PEF) production—are being repurposed as sustainable adhesive binders for wood composites. The innovative utilization of industrial waste by-products transforms what was once an environmental challenge into a renewable adhesive solution. The approach aligns perfectly with EU circular bioeconomy goals, offering a scalable and resource-efficient alternative to fossil-derived resins.

Historically limited to low-stress applications like paper and packaging, bio-based adhesives are engineered for high-performance industrial environments—including construction, automotive, and textile manufacturing—where mechanical durability, water resistance, and thermal stability are paramount. The shift signifies a major technological leap toward functional parity with synthetic adhesives, supported by new chemical pathways and advanced polymer design.

Companies such as Dow are pioneering renewable bio-based polyols through technologies like RENUVA™, enabling the production of polyurethane (PU) adhesives that offer enhanced water resistance, flexibility, and chemical durability. These polyols can reduce fossil resource consumption by up to 60% while meeting the mechanical demands of construction, coatings, and industrial sealant applications, marking a crucial step toward sustainable performance parity.

In a groundbreaking study published in ACS Applied Materials & Interfaces, researchers formulated a zein (corn protein) and tannic acid-based adhesive that bonds effectively underwater and even increases bond strength over time in wet environments. The innovation eliminates one of the key performance limitations of bio-based adhesives—moisture sensitivity—opening the door to marine construction, infrastructure maintenance, and biomedical applications.

Cargill’s Priplast™ portfolio showcases 100% bio-based polyester polyols designed for adhesive and elastomeric applications where flexibility, strength, and chemical resistance are crucial. These bio-polyesters are being adopted in automotive bonding, textile laminations, and flexible sealants, replacing petroleum-based polyurethanes and establishing new standards for long-life, high-performance bio-based formulations.

The global regulatory landscape is reshaping the adhesive market, with stringent frameworks such as EU REACH, the U.S. EPA Safer Choice program, and the EU Packaging and Packaging Waste Regulation (PPWR) driving manufacturers to replace VOC-emitting, toxic, and PFAS-containing adhesives with environmentally safe, bio-based alternatives. The compliance-driven transformation presents a massive market entry opportunity for certified, low-VOC and non-toxic bio-based adhesives.

Under the EU’s REACH Regulation and national VOC standards—such as Germany’s ABG approval system—construction adhesives must comply with TVOC limits ≤1.0 mg/m³ after 28 days, drastically reducing the allowable solvent emissions. These stringent standards are accelerating the transition to waterborne and solvent-free bio-adhesive formulations, especially for flooring, wall paneling, and insulation bonding applications in sustainable building projects.

The upcoming EU PPWR (2025–2026) restricts the total concentration of heavy metals (Pb, Cd, Hg, Cr VI) to ≤100 mg/kg and bans PFAS in food-contact packaging by 2026. Since conventional adhesives often contain these substances, major packaging producers are transitioning toward PFAS-free, bio-based adhesive chemistries to maintain compliance, aligning sustainability with regulatory enforcement and consumer expectations for non-toxic materials.

Circular economy initiatives are redefining the adhesive market by promoting recyclable, compostable, and debonding-on-demand formulations that facilitate material recovery and waste reduction. Bio-based adhesives are central to the movement, offering end-of-life solutions compatible with industrial composting, bio-deinking, and material separation processes.

In a major consumer market breakthrough, BioBond Adhesives, Inc. introduced BioMelt™, a fully biodegradable, plant-derived adhesive for the artificial nail and beauty industry. The innovation replaces solvent-based glues with non-toxic, compostable formulations, creating a replicable model for broader adoption in packaging, textiles, and single-use consumer goods. The product drives a rising commercial focus on end-of-life biodegradability and consumer-driven sustainability.

Innovations in bio-deinking technologies for paper recycling have demonstrated remarkable efficiency gains. Enzyme-based bio-deinking processes improved pulp freeness by 18.3% and reduced dirt counts (including adhesive stickies) by 32.6% compared to conventional chemical methods. The breakthrough highlights the potential for bio-based deinkable adhesives to eliminate a critical recycling bottleneck and enable cleaner fiber recovery in the circular paper economy.

Bio-Based Adhesives Market Share Insights, 2025-2034

The plant-based bio-adhesives segment dominates the global bio-based adhesives industry, capturing approximately 87.8% of the total market share in 2025, owing to its scalability, versatility, and compatibility with high-volume industrial processes. These adhesives—derived primarily from soy protein, starch, lignin, tannins, and other renewable feedstocks—have gained mainstream acceptance as viable substitutes for petroleum-based formulations in key sectors such as wood composites, packaging, and paper converting. Their leadership is anchored in growing regulatory pressures to reduce VOC emissions and carbon footprints across industries, as well as in their superior supply chain availability compared to animal-based counterparts. Continuous advancements in crosslinking chemistries, enzymatic modification, and nanofiller reinforcement have dramatically improved their performance characteristics—enhancing water resistance, bonding strength, and thermal stability. This makes plant-based systems not only sustainable but also technically competitive with synthetic resins like PVA and urea-formaldehyde. Furthermore, leading manufacturers are leveraging agricultural waste and industrial by-products to improve feedstock economics, aligning with global circular economy principles. The segment’s growth trajectory is further reinforced by increasing corporate commitments to bio-preferred procurement and low-carbon materials, ensuring that plant-based bio-adhesives remain the core driver of the market’s evolution toward sustainability.

On the other hand, the animal-based bio-adhesives segment, holding about 12.2% of the global market share, is a specialized, high-value domain rather than a volume-driven one. Derived from collagen, casein, fibrin, and albumin, these adhesives are indispensable in medical, art restoration, and specialty industrial applications where unique mechanical or biological properties are required. Fibrin-based adhesives, for example, serve as biocompatible sealants and hemostatic agents in surgical applications, offering unmatched performance in wound closure and tissue bonding. Casein and gelatin-based formulations maintain niche demand in wood lamination, leather, and craftwork, where their flexibility, biodegradability, and aesthetic finish are valued. However, their broader scalability is limited by feedstock availability, ethical sourcing concerns, and evolving vegan product preferences.

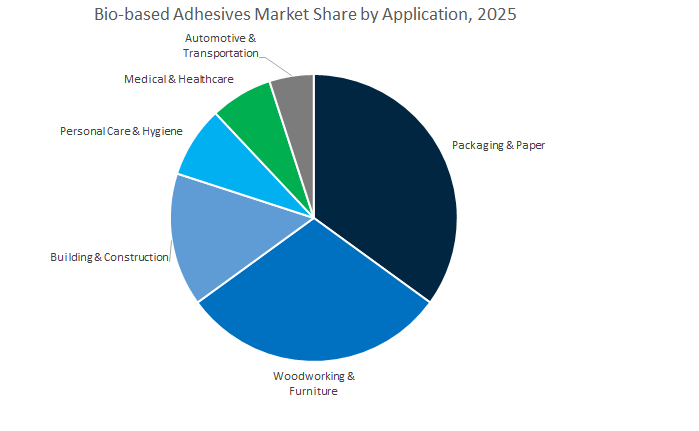

The packaging & paper segment holds the largest share of the global bio-based adhesives market, projected at 35.4% in 2025, underscoring its central role in the sustainability transformation of the packaging value chain. The segment’s leadership is driven by rising global demand for eco-friendly packaging solutions, particularly in corrugated board lamination, folding cartons, labels, and flexible packaging. Bio-adhesives derived from starch and dextrin are the backbone of this growth, offering high adhesion strength, biodegradability, and compatibility with recyclable paper substrates. Major packaging converters are shifting away from petroleum-based hot melts toward waterborne bio-adhesive systems to comply with stringent environmental mandates from brand owners and retailers. The expansion of e-commerce logistics, food-grade packaging, and paper-based alternatives to plastics further fuels this demand. Simultaneously, solvent-free processing and compostability certifications (e.g., ASTM D6400, EN 13432) are strengthening the preference for bio-adhesive solutions. This convergence of environmental regulation, brand sustainability commitments, and consumer eco-consciousness firmly establishes the packaging & paper segment as the engine of market volume growth for bio-based adhesives globally.

The woodworking & furniture segment, accounting for 30.8% of the market share, represents the second-largest end-use domain and is deeply tied to the green building and interior design revolution. The transition from formaldehyde-based synthetic resins to bio-based adhesives in engineered wood products—such as plywood, MDF, particleboard, and laminates—is driven by both environmental legislation and market differentiation. Manufacturers of interior furniture, flooring, and architectural components increasingly rely on soy protein and lignin-based adhesives that meet formaldehyde-free and low-VOC standards, aligning with LEED, BREEAM, and EPA compliance frameworks. Furthermore, the rise of mass timber construction (CLT, Glulam) has created significant opportunities for durable, high-bond bio-adhesive formulations capable of replacing polyurethane and phenolic resins. This segment also benefits from the consumer-driven preference for natural materials and the design industry’s focus on renewable sourcing. The ongoing integration of enzyme-modified starches, reactive crosslinkers, and nanocellulose reinforcement is further enhancing mechanical performance, positioning bio-based adhesives as the preferred solution for sustainable wood engineering and green furniture manufacturing.

The building & construction segment represents a rapidly expanding frontier for bio-based adhesives, driven by the industry’s accelerated decarbonization and the global pursuit of sustainable infrastructure solutions. Applications span from flooring, insulation, and wall panels to architectural laminates and structural wood assemblies, where the combination of strong adhesion, low toxicity, and environmental compliance is paramount. As developers aim to reduce embodied carbon in buildings, bio-based adhesives offer tangible value in achieving net-zero construction targets. Similarly, the medical & healthcare sector is witnessing steady adoption, with bio-adhesives such as fibrin, gelatin, and chitosan-based systems playing critical roles in wound healing, tissue repair, and surgical sealing. The growing integration of biocompatible, biodegradable adhesives aligns with the trend toward minimally invasive medical treatments. Meanwhile, the automotive & transportation segment is emerging as a strategic growth area, where manufacturers are incorporating bio-based bonding solutions in interior trim, acoustic insulation, and lightweight composites, particularly in electric vehicles (EVs) seeking sustainable material portfolios.

The competitive landscape of the bio-based adhesives market is defined by technological diversity, deep R&D pipelines, and an accelerating transition toward circular and low-carbon manufacturing systems. Industry leaders—including H.B. Fuller, Henkel, Ashland Global, Arkema, and Wacker Chemie—are actively investing in bio-polymer chemistry, renewable raw materials, and carbon certification frameworks. Their innovations encompass bio-circular hot melts, cellulose-based polymers, natural rubber PSAs, and biomass-balanced dispersions, each tailored to deliver performance equal to or superior to synthetic benchmarks.

H.B. Fuller continues to dominate the global sustainable adhesives segment, driven by its Advantra® Earthic™ 9370 launch—a bio-circular hot melt adhesive with ISCC PLUS certification and high renewable content. The company’s commitment to the Science Based Targets initiative (SBTi) guides its R&D toward low-carbon raw materials across Scope 3 supply chains.

Its Swift®tak range offers water-based, low-VOC bio-polymer adhesives for paper and packaging, while Foster® and Childers™ brands supply bio-based adhesives for insulating glass manufacturing, reducing energy use in construction.

Henkel leverages its global sustainability roadmap to promote fully recyclable and compostable bonding solutions. The company is heavily investing in bio-feedstock R&D aimed at substituting up to 100% of fossil-based carbon in adhesives. Its innovations in pressure-sensitive adhesives (PSAs), using bio-derived tackifiers and natural rubber, are expanding into medical, footwear, and label applications. Henkel’s efforts to enable recyclability in flexible packaging are redefining product lifecycle design in the adhesives sector.

Ashland Global stands at the intersection of polymer science and biotechnology, providing cellulosic and guar-based biopolymers that function as key components in bio-based waterborne adhesives. The company’s expertise in polymer modification allows natural feedstocks to achieve industrial-grade performance in shear strength and water resistance. Ashland is actively developing bio-based PVP alternatives to improve biodegradability in label adhesives and specialty films, aligning its innovation agenda with high-purity pharmaceutical and personal care applications.

Arkema, through its Bostik division, is at the forefront of bio-based polyurethane (PUD) and hot melt polyamide (HMPA) adhesive innovation. Its Pebax® Rnew® bio-elastomers, derived from castor beans, are revolutionizing flexible packaging and textile adhesives by providing high elasticity with renewable content. The company’s mass balance certification program verifies renewable carbon integration across its product line, ensuring traceable sustainability for industrial and packaging customers.

Wacker Chemie is advancing biomass-balanced VAE dispersions and SILRES® bio-based silicones, combining renewable chemistry with proven industrial performance. Its bio-based redispersible powder (RDP) products serve the construction and green building sectors, while PVA-based adhesives from renewable feedstocks cater to wood bonding and paper manufacturing.

Wacker’s innovations position it as a key European supplier for sustainable construction adhesives that meet EU Green Building standards and deliver consistent performance in wet environments.

The United States bio-based adhesives market is witnessing a surge in innovation, particularly in formaldehyde-free and PFAS-free formulations targeting both woodworking and industrial manufacturing applications. In 2025, BioBond Adhesives, Inc. launched its flagship product, BioBond Wood Adhesive, which is USDA BioPreferred-certified and specifically engineered for the woodworking and craft industries. The adhesive offers a high-performance, sustainable alternative to conventional phenol- and urea-formaldehyde-based products.

Financially, the launch was supported by Big Idea Ventures’ Generation Food Rural Partners Fund, which has allocated 70% of its total capital toward developing rural bio-based manufacturing ecosystems — a move designed to stimulate local job creation and decentralized material innovation. Additionally, 3M Company introduced a new reactive hot melt adhesive designed for electronics assembly, featuring enhanced heat and moisture resistance for devices such as smartphones and wearables, marking a strong integration of bio-derived materials in high-tech applications.

The U.S. also leads in the commercialization of lignin-based adhesives, with biorefinery advancements allowing lignin to replace petroleum-derived phenols in plywood and composite board manufacturing. As sustainability regulations tighten, such innovations are expected to become standard for green-certified construction and furniture sectors.

Germany continues to lead Europe’s bio-based adhesive innovation, with major chemical corporations like BASF SE and Henkel AG & Co. KGaA at the forefront of technological development. BASF’s Acrodur bio-based binder series remains a cornerstone of Europe’s transition toward sustainable composite manufacturing, widely used in automotive interiors, nonwovens, and wood composites. In early 2025, BASF expanded its Acrodur product line to meet the growing need for low-emission, high-durability binders that comply with stringent European VOC and formaldehyde emission standards.

Henkel’s strategic partnership with Kraton Corporation, announced in 2025, further strengthens Germany’s leadership in the bio-based adhesives and sealants market. The partnership integrates renewable feedstock polymers into Henkel’s advanced adhesive technologies, significantly reducing product carbon footprints and improving recyclability. Additionally, at the K 2025 trade fair in Düsseldorf, multiple exhibitors highlighted new bio-based raw materials and recycled compounds, underlining Germany’s push toward functional performance with environmental responsibility.

Across the European Union, coordinated research initiatives are advancing the next generation of formaldehyde-free, bio-based wood adhesives and sustainable polymer systems. The SUSBOARD project, a €6.9 million Horizon Europe initiative, officially launched in 2025 to develop the world’s first 100% bio-based, cost-competitive adhesive for particleboard (PB) and medium-density fiberboard (MDF). The project aims to replace traditional fossil-based resin systems with polylysine-based formulations, capable of reducing the carbon footprint of wood panels by up to 30% while maintaining industrial-grade strength.

Meanwhile, the Circular Bio-based Europe Joint Undertaking (CBE JU) has announced a €165 million (US$176 million) funding call focused on flagship innovation projects for bio-based drop-in chemicals, Safe and Sustainable by Design (SSbD) materials, and large-scale industrial demonstrators. The funding mechanisms directly support the commercialization of bio-adhesives derived from natural feedstocks such as soy, lignin, and starch, strengthening Europe’s competitive position in sustainable manufacturing.

China’s bio-based adhesives market is rapidly scaling as the country embraces green manufacturing standards across packaging, construction, and furniture sectors. In 2025, massive industrial adoption of starch-based and soy-based adhesives has accelerated, replacing conventional urea-formaldehyde and phenolic resins in plywood and composite board applications. The shift is supported by national policy measures mandating VOC emission reduction and the domestic sourcing of renewable materials to support its environmental sustainability targets.

Additionally, the Chinese government is heavily investing in biopolymer research programs to advance domestic production of renewable feedstocks for adhesives and sealants. Initiatives focused on bio-based structural adhesives for high-performance industrial applications are reducing reliance on imported materials and enhancing China’s self-sufficiency in green chemical production. As a result, the market is poised for rapid growth in low-cost, high-volume bio-adhesive solutions, particularly for packaging and woodworking industries aligned with urban development projects.

Sweden has positioned itself as a European research powerhouse in the bio-based adhesive industry through the establishment of the BioGlue-Centre, a multi-year initiative funded by Vinnova (SEK 36 million), running from 2024 to 2028. The center aims to develop a world-leading research environment for bio-based adhesives, integrating academic and industrial expertise across forest-based, packaging, and furniture sectors.

With fifteen consortium partners — including universities, material science firms, and forest-sector companies — the program focuses on fundamental research, industrial testing, and pilot-scale implementation of bio-adhesive systems. The goal is to significantly reduce Sweden’s dependence on fossil-based adhesives by commercializing new renewable polymer chemistries derived from lignocellulosic biomass. The initiative aligns closely with the nation’s carbon neutrality and circular economy objectives, positioning Sweden as a key European center for next-generation adhesive sustainability research.

India’s bio-based adhesives industry is expanding rapidly due to increasing emphasis on sustainable manufacturing, eco-friendly packaging, and green building initiatives. Domestic manufacturers are scaling the production of solventless polyurethane (PU) and waterborne adhesives, incorporating bio-derived raw materials to meet the sustainability goals of India’s fast-growing flexible packaging sector.

In parallel, India’s green construction ecosystem is driving the adoption of low-VOC, bio-based sealants and adhesives for flooring, insulation, and panel bonding applications, aligned with LEED and BREEAM certification standards. Furthermore, national programs under the Production Linked Incentive (PLI) Scheme for the EV and chemicals sectors are catalyzing investment in bio-based adhesive technologies for battery and component bonding. The advancements highlight India’s transition toward sustainable, locally sourced, and cost-efficient bio-adhesive solutions for industrial and consumer markets.

Bio-Based Adhesives Market Report Scope

Bio-Based Adhesives Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$25.8 Billion

|

|

Market Size (2034)

|

$67.1 Billion

|

|

Market Growth Rate

|

11.2%

|

|

Segments

|

By Type/Source (Plant-Based Bio-adhesives, Animal-Based Bio-adhesives), By Product Technology (Water-Based Bio-adhesives, Hot Melt Bio-adhesives, Reactive Bio-adhesives, Solvent-Free Bio-adhesives), By Application/End-Use (Packaging & Paper, Woodworking & Furniture, Building & Construction, Medical & Healthcare, Automotive & Transportation, Personal Care & Hygiene

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Henkel AG & Co. KGaA, H.B. Fuller Company, 3M Company, Arkema S.A., Sika AG, The Dow Chemical Company, BASF SE, Ashland Global Holdings Inc., Jowat SE, Tesa SE, EcoSynthetix Inc., Paramelt B.V., Tate & Lyle PLC, DIC Corporation, BioBond Adhesives, Inc.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

By Type/Source

- Plant-Based Bio-adhesives

- Animal-Based Bio-adhesives

By Product Technology

- Water-Based Bio-adhesives

- Hot Melt Bio-adhesives

- Reactive Bio-adhesives

- Solvent-Free Bio-adhesives

By Application/End-Use

- Packaging & Paper

- Woodworking & Furniture

- Building & Construction

- Medical & Healthcare

- Automotive & Transportation

- Personal Care & Hygiene

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

- Henkel AG & Co. KGaA

- H.B. Fuller Company

- 3M Company

- Arkema S.A.

- Sika AG

- The Dow Chemical Company

- BASF SE

- Ashland Global Holdings Inc.

- Jowat SE

- Tesa SE

- EcoSynthetix Inc.

- Paramelt B.V.

- Tate & Lyle PLC

- DIC Corporation

- BioBond Adhesives, Inc.

*- List not Exhaustive

Research Coverage

Prepared by USDAnalytics, this report investigates how bio-resin innovation and circular feedstocks are scaling from packaging to construction, furniture, and mobility; our analysis reviews lignin-enhanced, starch/soy systems, bio-polyurethane hybrids, and ISCC PLUS mass-balance hot melts against low-VOC and recyclability mandates. It highlights measurable performance parity—wet-shear, peel, and cure-speed—plus supply-risk, certification, and end-of-life pathways (compostable, de-inkable, debond-on-demand). We map policy momentum (REACH, PPWR, Safer Choice), procurement criteria (renewable carbon %, formaldehyde-free claims), and cost-in-use levers for converters and panel makers, surfacing breakthroughs from premethylolated lignin to bio-polyol PUs and enzyme-assisted recycling. For sourcing leaders, R&D, sustainability officers, and plant engineers, this report is an essential resource to benchmark materials, de-risk reformulation, and align 2025–2034 roadmaps with circular manufacturing.

Scope Includes

- By Type/Source: Plant-Based Bio-adhesives; Animal-Based Bio-adhesives

- By Product Technology: Water-Based; Hot Melt; Reactive; Solvent-Free

- By Application/End-Use: Packaging & Paper; Woodworking & Furniture; Building & Construction; Medical & Healthcare; Automotive & Transportation; Personal Care & Hygiene

- Geographic Scope: Analysis spans 25+ countries across North America, Europe, Asia Pacific, Latin America, the Middle East & Africa.

- Time Horizon: Historical 2021–2024; Forecast 2025–2034.

- Companies Covered: 15+ company analyses/profiles.

Deliverables

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.