Market Overview: High-Barrier, Optical-Grade & Reinforced Specialty Films Accelerate Growth Across Electronics, Medical & Sustainable Packaging Markets

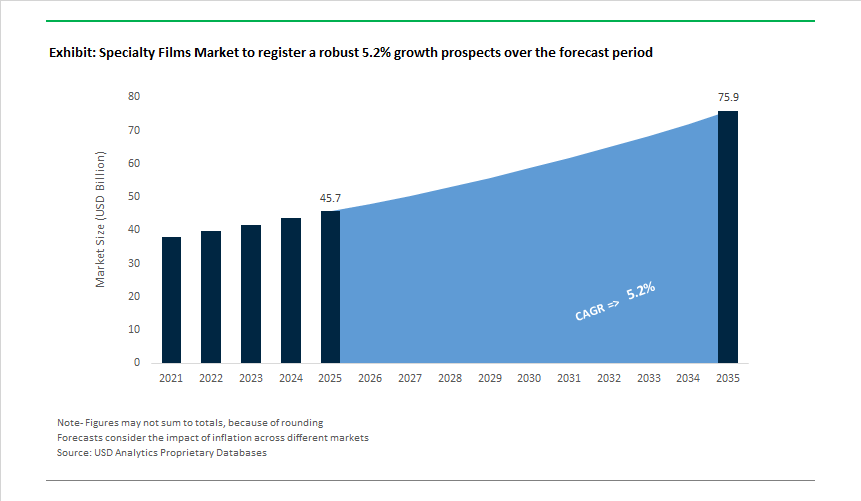

The Specialty Films Market, valued at USD 45.7 billion in 2025, is forecast to reach USD 75.9 billion by 2035 at a steady 5.2% CAGR, propelled by escalating demand for high-barrier packaging films, display-grade ultra-thin optical films, high-performance window films for automotive and buildings, and engineered films used in medical, semiconductor, and industrial environments. The shift toward oxygen- and moisture-critical packaging, thin-film optical precision for OLED and foldable displays, and high-reliability protective films for EV batteries, solar modules, and cleanroom semiconductor processes is redefining material performance expectations across global value chains.

Manufacturers are engineering films with sub-micron thickness uniformity, high optical clarity, enhanced thermal and UV protection, and superior mechanical strength, while meeting increasingly stringent sustainability mandates. This includes the transition toward recyclable mono-material barrier structures, solvent-reduced coating systems, and advanced polymer chemistries capable of delivering high transparency, improved modulus, and elevated thermal resistance. As brands and industrial users prioritize extended shelf life, device durability, and energy management, material suppliers must demonstrate precision manufacturing, robust barrier control, and validated performance under diverse operating conditions.

From a production standpoint, specialty film manufacturers are scaling capabilities in high-speed multi-layer extrusion, precision coating, nano-barrier deposition, and optical-grade surface control to serve end-markets such as food & pharma packaging, semiconductor lithography and carrier films, EV thermal barriers, architectural glazing, and sterile medical packaging. Market leadership is increasingly defined by the ability to deliver OTR <0.5 cc/m²/day, ±1 µm thickness uniformity for OLED films, Total Solar Energy Rejection (TSER) up to 65% with 99.9% UV block, and >200 N puncture resistance for sterile medical barrier applications-benchmarks that directly influence procurement specifications and long-term supplier contracts.

Market Analysis: Sustainability Approvals, Semiconductor Processing Films, and Packaging Innovations

Industry developments indicate a strong acceleration in specialty film innovation, with major moves in packaging circularity, display technology support, semiconductor wafer handling, and growth in optically advanced films. In January 2025, an Asian polyester film supplier commissioned a new high-strength, ultra-thin PET film line in Southeast Asia to address rising electronics demand-particularly flexible circuit substrates and high-dielectric capacitor films essential for EVs and portable devices. March 2025 further strengthened the innovation landscape when Nitto Denko received the Clarivate Global Innovator Award, highlighting its expanding intellectual property portfolio in adhesive films, optical enhancement films, and sealing layers used across smartphones, tablets, and displays.

By July 2025, sustainability-focused consolidation became visible as a European packaging film producer acquired a co-extrusion specialist to scale fully recyclable mono-material high-barrier films, aligning with EU circularity mandates. In August 2025, DuPont and other fluoropolymer film leaders began investing heavily in next-generation fluoropolymer chemistries to improve UV and thermal stability used in photovoltaic backsheets-critical as solar modules face harsher operating environments. This was followed in September 2025 by a joint development initiative between Mitsubishi Chemical, Sharp, NICT, and TECHLAB to create ultra-compact satellite communication terminals using advanced functional films for antenna substrates.

The industry’s focus on recyclability and high-barrier approval gained strong momentum in October 2025, when Mitsubishi Chemical’s multilayer films containing SoarnoL EVOH (10 wt%) obtained RecyClass Technology Approval, marking a commercial milestone for sustainable high-barrier packaging. In November 2025, 3M reinforced its market dominance by launching 70 new specialty films and adhesive-related products in Q3 alone, strengthening its footprint across industrial tapes, optical films, and protective films. Closing the year, Toray Industries introduced a cutting-edge temporary bonding material in December 2025 for ultra-thin semiconductor wafer processing, addressing critical yield and handling challenges for next-gen logic and memory devices. These sequential advances emphasise how specialty films increasingly intersect with high-tech manufacturing, renewable energy, smart mobility, and medical packaging segments.

Specialty Films Market: Trends and Opportunities

High-Barrier Monomaterial Films Replace Legacy Multilayer Laminates

The specialty films market is undergoing a structural redesign as brand owners and regulators converge on recyclable monomaterial architectures, particularly mono-PE and mono-PP, to replace unrecyclable multilayer laminates. This shift is most pronounced in food and healthcare packaging, where oxygen and moisture barriers are non-negotiable and compliance risk is high. A defining inflection came in April 2025 when Amcor plc completed its $24.7 billion acquisition of Berry Global. The transaction was strategically anchored in scaling recycle-ready barrier films by consolidating resin science, coating know-how, and global converting capacity—signaling that monomaterial performance has reached industrial viability.

Material innovation is closing the historical performance gap. Dow expanded its RecycleReady portfolio through specialized resins and compatibilizers that preserve shelf-life parity with multilayer structures while remaining compatible with store drop-off recycling. Regulatory pressure is accelerating adoption: in September 2025, Dow introduced non-fluorinated polymer processing aids (PPAs) that eliminate PFAS from high-clarity film production, aligning with tightening restrictions from both the European Chemicals Agency and the U.S. Environmental Protection Agency. Market recognition underscores readiness—at the 2025 Flexible Packaging Association awards, Amcor’s Eco-Tite® tubestock earned top honors after passing the APR Design® Guide for recyclability while using 29% less material than conventional shrink films. The result is a clear migration path from compliance-driven pilots to scaled, shelf-ready monomaterial solutions.

Advanced Optical Films Compress Form Factors in AR/VR and Spatial Computing

The rise of spatial computing has created a premium niche for specialty optical films that enable thinner, lighter, and more power-efficient near-eye displays. Devices such as Apple Vision Pro and the Meta Quest rely on films with precision micro-structures—pancake and Fresnel optics—and tunable refractive indices to reduce optical path length without sacrificing image quality. At Display Week 2025, engineering roadmaps emphasized Micro-LED integration with advanced films to boost luminous efficiency and extend battery life, now a gating factor for all-day wearability.

Dynamic optics are emerging as the next frontier. At Photonics West 2025, MKS Instruments highlighted varifocal optical films that modulate focal distance in real time, directly addressing the Vergence-Accommodation Conflict (VAC) that drives user fatigue and motion sickness. Manufacturing methods are also evolving. The 2025 adoption of Quantum X align enabled precision 3D printing of micro-optic films directly onto photonic substrates, unlocking folded optics geometries previously unattainable with extrusion or casting. Together, these advances position specialty optical films as performance multipliers, not passive components, in the AR/VR value chain.

Encapsulation Films Become Mission-Critical for Perovskite PV Commercialization

As perovskite photovoltaics transition from lab records to utility deployment, ultra-high-barrier encapsulation films have become the principal reliability bottleneck—and the clearest growth avenue for specialty film suppliers. Perovskites’ extreme moisture sensitivity demands WVTR levels far below conventional silicon modules, alongside UV stability and low-temperature lamination. In August 2025, Oxford PV set a world record with 25% efficient perovskite-on-silicon tandem panels, accelerating industrial rollouts that immediately raised demand for advanced encapsulants capable of 20-year durability. The momentum converted to revenue in September 2025 with the first commercial shipment of tandem panels to a U.S. utility—each module requiring specialized films to protect the perovskite layer during lamination.

Competitive pressure is intensifying. In April 2025, LONGi Solar reported a 34.85% efficiency record for perovskite-silicon tandem cells, reinforcing the industry’s trajectory beyond silicon’s practical limits. This race elevates the value of encapsulation films that balance UV stability, ultra-low moisture ingress, and high optical transmission—a combination that few materials can deliver at scale. For film producers, perovskite PV represents a technology-pull market where performance specs are dictated by cell physics rather than packaging conventions.

Thermal Management Films Address Heat Density in 5G and 800V EV Systems

Rising power densities in 5G/mmWave infrastructure and 800V EV architectures are overwhelming traditional air-cooling approaches, opening a strong opportunity for thermally conductive, electrically insulating (TCEI) specialty films. These films must dissipate heat while preserving dielectric integrity across compact, high-voltage assemblies. At SEMICON Taiwan 2025, Kaneka Corporation showcased polyimide-based thermal management films designed for Redistribution Layer (RDL) applications, emphasizing low CTE and high heat flux handling for advanced packaging.

Automotive integration is accelerating. At the 2025 Japan Mobility Show, Highly Marelli debuted EV thermal systems that harvest waste heat from traction motors—relying on specialty films and adhesives such as ThreeBond 2045B to ensure efficient heat transfer with electrical isolation inside battery enclosures. Material choices are shifting as well: high-performance polymers like Stanyl are increasingly used in battery power modules to tolerate immersion cooling and dielectric fluids. As 5G expands into harsher outdoor environments and EV fast-charging becomes mainstream, specialty films that combine thermal management, EMI shielding, and electrical insulation are moving from optional enhancements to system-critical components.

Market Share Analysis: Specialty Films Market

Market Share by Material Type: BOPET Films Anchor Performance-Driven Specialty Applications

Polyester-based biaxially oriented polyethylene terephthalate (BOPET) films account for approximately 25% of the global Specialty Films Market, reflecting their role as the high-performance backbone across demanding end-use sectors. This segment leads because biaxial orientation locks polymer chains into a highly ordered structure, delivering exceptional tensile strength, dimensional stability, and tear resistance at ultra-thin gauges. For manufacturers, this enables aggressive down-gauging, reducing material consumption while maintaining mechanical integrity—an increasingly important driver as brands target lightweighting and cost efficiency. BOPET’s wide thermal stability window further reinforces its market share, allowing consistent performance in high-temperature processing environments such as hot-fill food packaging and microwave-ready applications where alternative films fail. Optical performance is another decisive factor, as BOPET offers glass-like transparency and low haze that support premium product presentation and brand differentiation at retail. From a sustainability standpoint, the shift toward advanced and bio-based PET formulations has strengthened BOPET’s relevance by lowering lifecycle emissions without compromising performance. Collectively, these strength, clarity, heat resistance, and sustainability advantages explain why BOPET remains the material of choice for performance-critical specialty film applications, securing its leading share in the market.

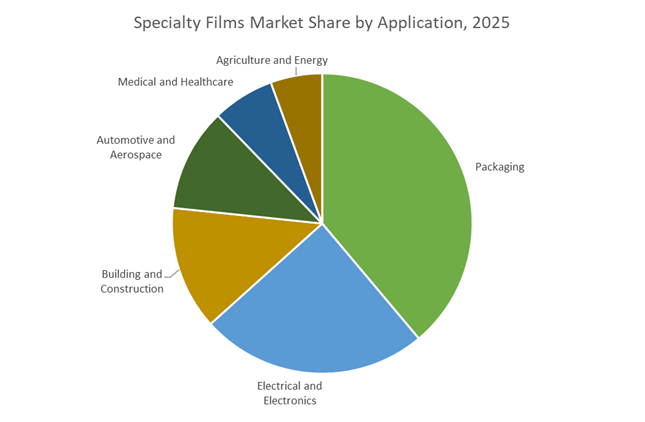

Market Share by Application: Packaging Drives Volume Growth and Innovation Adoption

The packaging segment represents approximately 35% of total demand in the Specialty Films Market, making it the largest and most commercially influential application area. Packaging dominates because it fully exploits the multifunctional advantages of specialty films—barrier protection, product visibility, and logistics efficiency—within a single solution. Multilayer BOPET-based structures deliver near-zero oxygen and moisture transmission, extending shelf life for food, pharmaceuticals, and medical supplies while preserving flavor and efficacy. Market share is further reinforced by the industry’s rapid transition toward recyclable mono-material packaging, where PET-based films align seamlessly with existing recycling infrastructure and help brand owners comply with tightening environmental regulations and plastic taxation policies. Lightweight flexible packaging also reduces transportation costs and carbon footprint compared to rigid alternatives, strengthening its economic appeal across global supply chains. In parallel, the emergence of bio-based PET films is accelerating adoption among sustainability-focused brands seeking measurable emissions reductions without sacrificing performance. As packaging requirements increasingly converge around protection, sustainability, and cost efficiency, this segment remains the primary demand engine for specialty films worldwide, anchoring its leading market share.

Competitive Landscape: Leading Manufacturers in High-Barrier, Optical, Adhesive, and High-Performance Film Technologies

The competitive landscape is shaped by companies that specialize in high-barrier packaging films, optical and electronic films for displays, advanced polymer chemistries, adhesive-based functional films, and PET/PP high-performance substrates for energy and semiconductor applications. Their strengths lie in deep material science expertise, co-extrusion engineering, surface modification, nanotechnology, and fully integrated manufacturing platforms. Many are expanding into recyclable barrier solutions, sustainable film architectures, and semiconductor-grade ultra-thin films to meet rising regulatory and performance demands.

3M Company - Diversified Materials and Adhesive Film Innovation

3M leverages its multidisciplinary material science platform-including adhesives, surface modification, and nanostructured film technology-to produce specialty films ranging from Optically Clear Adhesives (OCA) to Dichroic films, ESR reflectors, and protective layers for electronic displays. With an R&D investment plan of ≈USD 3.5 billion (2025-2027), 3M is aggressively expanding innovation across its industrial, electronics, and automotive film segments. Its eXcellence operational model has delivered supply chain and margin improvements, underpinning its ability to scale high-value functional films for global markets.

Mitsubishi Chemical Group - Multi-Layer Co-Extrusion and Advanced Polymer Films

Mitsubishi Chemical is distinguished by its polymer chemistry depth, enabling complex multilayer structures with tailored barrier, mechanical, and optical properties. Its portfolio includes OPL Film™ for LCD polarizing plates, MOSMITE™ anti-reflection films, and Hi-Selon™ water-soluble PVOH films. Recent innovations include the RecyClass approval of its SoarnoL EVOH-based recyclable high-barrier films, a significant step toward circular packaging. Strategically, Mitsubishi is advancing specialty films for data processing, high-performance displays, and sensor applications while scaling recyclable and sustainable film solutions globally.

Nitto Denko Corporation - Adhesive, Optical, and Electronic Interface Film Specialist

Nitto Denko leverages proprietary adhesive and coating technologies to produce high-performance specialty films, polarizers, optical films, and ultra-thin sealing materials essential for smartphones, tablets, and high-resolution displays. Its recognition as a Top 100 Global Innovator (2025) underscores its strength in intellectual property and R&D leadership. The company is also expanding into Power and Mobility films, offering thermal, NVH, and electrical insulation films for EV batteries and interiors, reinforcing its presence in growing electrification markets.

Toray Industries - High-End PET Films, Nanotechnology Films, and Semiconductor-Grade Solutions

Toray relies on advanced polymer science and nanotechnology to manufacture differentiated PET, PP, and functional films. With AP-G 2025 targeting ¥1,600 billion in sustainability innovation revenue, Toray is expanding sustainable and high-performance film lines. Its newly developed temporary bonding material for ultra-thin semiconductor wafers (Dec 2025) positions Toray as a trusted supplier to high-tech electronics manufacturing. Toray also remains a major provider of battery separator films and PV backsheets, reinforcing its leadership in renewable energy and advanced electronics materials.

India has emerged as the fastest-growing manufacturing hub for specialty films in 2025, driven by Production Linked Incentive (PLI) programs and a surge in private capital expenditure across packaging, electronics, and EV supply chains. Direct state–industry collaboration is translating into rapid capacity additions in BOPP and metallized film segments optimized for high-speed packaging and heat-resistant mono-material structures. Investments by Toppan Speciality Films and Cosmo First reflect a shift toward technologically advanced, recyclable substrates aligned with global sustainability norms. Policy extensions from MeitY for metallized capacitor films further anchor domestic demand from EV power electronics and LED applications, reinforcing India’s trajectory from import dependence to export-oriented specialty film production.

Japan’s Materials DX Integration for Semiconductor-Grade Specialty Films

Japan’s specialty films market is defined by deep integration between digital transformation (DX) platforms and semiconductor packaging demand. Hybrid manufacturing lines capable of producing both BOPP and BOPE films are enabling rapid transitions toward mono-material packaging formats demanded by European regulations. Electronics-focused players such as TOPPAN Inc. and LINTEC Corporation are anchoring growth through recycled PET solar control films and advanced packaging materials for chip-scale integration. Government-backed Materials Research DX initiatives are shortening R&D cycles for polyimide films used in flexible printed circuits, positioning Japan as a premium supplier of high-end electronic specialty films rather than a volume-driven market.

Germany and the European Union’s Regulatory-Driven Circular Specialty Films Transition

Across Germany and the wider EU, the specialty films market is being reshaped by the Packaging and Packaging Waste Regulation (PPWR) and decarbonization incentives. Corporate consolidation and capacity expansion are accelerating the transition toward recyclable mono-material films and solvent-free coating technologies. Strategic moves by Covestro-including portfolio expansion through acquisition-and capacity investments by Innovia Films underscore Europe’s emphasis on low-carbon BOPP substrates and medical-grade multilayer films. EU Innovation Fund grants are further reducing VOC emissions in barrier film production, reinforcing Europe’s leadership in regulation-compliant, circular specialty film ecosystems.

United States Reshoring Strategy and Protective Film Innovation

The U.S. specialty films market in 2025 is shaped by reshoring initiatives and application-specific innovation for pharmaceuticals, construction, and industrial protection. Capital consolidation by firms such as Transcendia Inc. is streamlining domestic production of engineered barrier films to reduce reliance on overseas suppliers. Product innovation, including high-strength protective shrink films with recycled content, highlights the U.S. focus on durability and sustainability in industrial applications. Federal funding under the Industrial Energy Transformation Fund is accelerating upgrades to energy-efficient coating, drying, and curing infrastructure, strengthening the competitiveness of U.S.-based specialty film manufacturing.

China’s Scale-Up for 800V EV and Energy Storage Films

China’s specialty films sector is pivoting decisively toward ultra-thin functional films for 800V EV battery architectures and renewable energy systems. Under the concluding 14th Five-Year Plan, mandated capacity increases in lithium-ion battery separators and capacitor films are driving investments in sub-5-micron film technologies. This technological push supports higher energy density and thermal stability in next-generation batteries. China’s advantage lies in rapid commercialization at scale, positioning domestic manufacturers as key suppliers of separator and PVDF films to global EV and energy storage OEMs.

United Kingdom’s Bio-Based Cellulose Film Niche

The United Kingdom is carving out a differentiated position in bio-based specialty films by converting legacy industrial sites into low-carbon cellulose film hubs. Targeted investments at facilities producing NatureFlex and Cellophane films are enhancing energy efficiency and sustainability credentials. Government support through the Industrial Energy Transformation Fund is enabling significant reductions in carbon intensity for biodegradable barrier films, reinforcing the UK’s role as a specialist supplier of compostable and renewable specialty film solutions.

National Strategic Development Matrix: Specialty Films Market (2025)

Specialty Films Market Development Matrix by Country

|

Country / Region

|

Primary Strategic Driver

|

2025 Key Development

|

Core Specialty Film Focus

|

|

India

|

PLI 2.0 & manufacturing localization

|

New BOPP/metallized film lines

|

Sustainable packaging, EV electronics

|

|

Japan

|

Materials DX & semiconductors

|

Hybrid BOPP–BOPE production

|

Semiconductor packaging, FPC films

|

|

Germany / EU

|

PPWR & circular economy

|

Solvent-free coatings, mono-materials

|

Recyclable food & medical films

|

|

United States

|

Reshoring & infrastructure

|

Barrier film consolidation, IETF grants

|

Pharma, construction, protective films

|

|

China

|

800V EV transition

|

Sub-5 μm separator film deployment

|

Battery separators, PVDF films

|

|

United Kingdom

|

Bio-based materials

|

Cellulose film decarbonization

|

Compostable barrier films

|

Specialty Films Market Report Scope

Specialty Films Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$45.7 Billion

|

|

Market Size (2035)

|

$75.9 Billion

|

|

Market Growth Rate

|

5.2%

|

|

Segments

|

By Material Type (Polyester, Nylon, Fluoropolymer, Polyimide, Polycarbonate, Polypropylene, Polyethylene, High-Performance Thermoplastics, Others), By Functionality (Barrier Films, Optical Films, Safety & Security Films, Protective Films, Shrink & Stretch Films, Conductive & Antistatic Films, Microporous Films, Decorative & Graphic Films), By Application (Packaging, Electrical & Electronics, Building & Construction, Automotive & Aerospace, Agriculture, Medical & Healthcare, Energy)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Berry Global Group Inc., Amcor plc, Toray Industries Inc., The Chemours Company, DuPont Teijin Films, Eastman Chemical Company, 3M Company, Mitsubishi Chemical Group Corporation, SKC Co., Ltd., Jindal Poly Films Limited, Uflex Limited, Mondi Group, Sealed Air Corporation, Covestro AG, Solvay S.A.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Specialty Films Market Segmentation

By Material Type

- Polyester

- Nylon

- Fluoropolymer

- Polyimide

- Polycarbonate

- Polypropylene

- Polyethylene

- High-Performance Thermoplastics

- Others

By Functionality

- Barrier Films

- Optical Films

- Safety and Security Films

- Protective Films

- Shrink and Stretch Films

- Conductive and Antistatic Films

- Microporous Films

- Decorative and Graphic Films

By Application

- Packaging

- Electrical and Electronics

- Building and Construction

- Automotive and Aerospace

- Agriculture

- Medical and Healthcare

- Energy

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in Specialty Films Market

- Berry Global Group, Inc.

- Amcor plc

- Toray Industries, Inc.

- The Chemours Company

- DuPont Teijin Films

- Eastman Chemical Company

- 3M Company

- Mitsubishi Chemical Group Corporation

- SKC Co., Ltd.

- Jindal Poly Films Limited

- Uflex Limited

- Mondi Group

- Sealed Air Corporation

- Covestro AG

- Solvay S.A.

*- List not Exhaustive