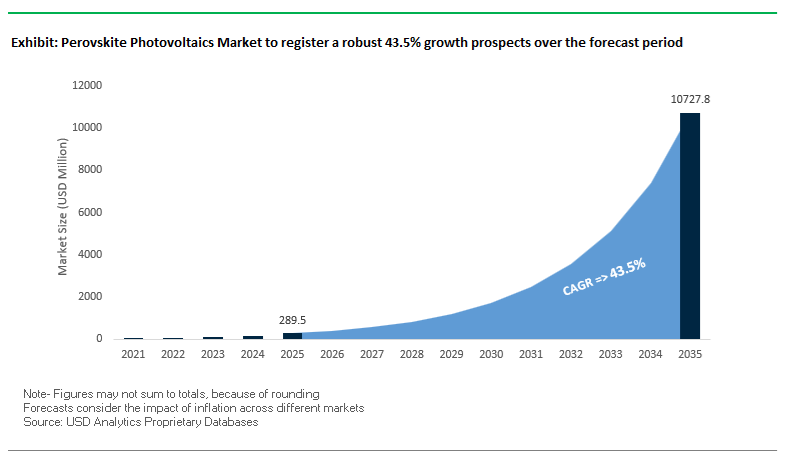

The Perovskite Photovoltaics Market, valued at USD 289.5 million in 2025, is poised for explosive expansion to reach USD 10,719.3 million by 2035, accelerating at an exceptional CAGR of 43.5%. The rapid acceleration is driven by three simultaneous advancements: tandem efficiency breakthroughs, module stability improvements, and drastic manufacturing cost reductions that position perovskite PV as a next-generation contender for ultra-low LCOE renewable energy systems.

The global perovskite photovoltaics industry accelerated dramatically in 2025, driven by world-record efficiencies, large-scale production line commissioning, and the first commercial shipments of tandem panels. In November 2025, JinkoSolar recorded a 34.76% efficiency world record for an N-type TOPCon-based perovskite tandem cell, cementing tandem technology as the successor to TOPCon in the crystalline silicon ecosystem. During the same month, LONGi Green Energy achieved a 33.4% certified efficiency for a flexible perovskite–silicon tandem device, delivering a remarkable 1.77 W/g power-to-weight ratio, positioning perovskites as a highly attractive solution for vehicle-integrated photovoltaics (VIPV), aerospace surfaces, and mobile applications.

Commercialization became a reality in September 2025, when Oxford PV executed the first commercial sale of perovskite-on-silicon tandem panels to a U.S. utility-scale customer, marking the most significant technology-to-market step in the industry’s history. The milestone demonstrates that tandem modules are not only manufacturable but also bankable when backed by strong warranties, stable performance data, and credible IP protection. Earlier, in July 2025, LONGi published academic research in Nature detailing the use of asymmetric self-assembled molecules to suppress non-radiative recombination—indicating that fundamental materials science continues to extend the industry’s efficiency frontier.

Meanwhile, the manufacturing landscape underwent a pivotal shift as UtmoLight commissioned its GW-scale perovskite module factory in May 2025, signaling the transition from pilot-scale to industrial-scale production. Chinese manufacturers intensified activity, with RenShine Solar launching a 150 MW flexible perovskite line in May 2025 targeting BIPV and lightweight indoor-outdoor applications. IP strategies also reshaped the sector’s competitive dynamics, exemplified by the April 2025 exclusive licensing agreement between Oxford PV and Trina Solar, granting the latter rights to manufacture and sell perovskite PV products within China. Earlier, in January 2025, the University of Science and Technology of China (USTC) achieved a 26.7% certified efficiency for single-junction perovskite cells, demonstrating that single-junction pathways remain highly relevant for specialized lightweight and flexible applications.

A defining milestone occurred in April 2025, when a silicon–perovskite tandem solar cell reached 34.85% certified efficiency, verified by NREL, creating a new benchmark that surpasses the Shockley–Queisser limit for single-junction crystalline silicon. Stability—a historic barrier—also crossed a major threshold as carbon-based perovskite mini-modules retained 90% performance after 3,260 hours in 85°C/85% RH Damp Heat aging, demonstrating credible progress toward a 20-year operational lifetime. Equally transformative is the 44%–51% manufacturing cost reduction potential identified in upscaled deposition methods using low-cost scribing and simplified module assembly. Furthermore, in August 2025, the industry achieved a world-record 25.0% efficiency on a 1.68 m² industrial-format tandem module, validating manufacturability for utility-scale deployment.

- 34.85% efficiency (Apr 2025, NREL) confirms perovskite-on-silicon tandems as the future ultra-high-efficiency PV standard.

- Long-term stability milestone: 3,260 hours at 85°C/85% RH with T90 retention signifies progress toward bankable lifespan.

- Industrial scalability proven: 25% efficiency on a 1.68 m² tandem module (Aug 2025) validates GW-scale manufacturing feasibility.

- Cost-down trajectory: 44–51% fabrication cost reduction possible via low-cost deposition and scribing processes, supporting low LCOE.

Industrial-Scale Tandem Architectures, Vapor-Phase Manufacturing, Flexible Modules, and Lead-Free Compositions Redefine the Perovskite Photovoltaics Market

Trend 1: Rapid Industry Prioritization of Perovskite–Silicon Tandem Solar Cells as the Commercial Front-Runner

The dominant commercialization pathway for perovskite photovoltaics is the Perovskite–Silicon Tandem Cell, where the combined absorber layers break the single-junction performance ceiling and push PV conversion efficiency into new territory. Global solar manufacturers are executing pilot lines, validating tandem architectures for utility-scale and rooftop applications, and positioning the technology as the successor to TOPCon and HJT over the next decade.

Key performance benchmarks include:

- Record tandem efficiencies of 33.84% (JinkoSolar claim) and 31.71% (independently certified), surpassing the 29.4% theoretical limit for single-junction c-Si technologies, and established as the highest-performing commercial-ready PV architecture.

- Commercial pilot line deployment by companies such as Tongwei, which has operationalized automated tandem production lines using standard industrial M10 wafers-reinforcing the technology’s compatibility with mainstream silicon manufacturing.

- Large-area tandem success, such as Qcells’ 28.6% efficiency on an M10-sized device, demonstrating manufacturability at commercial wafer scales.

- Exceptional voltage performance, with 4-terminal tandems achieving VOC values up to 1.954 V, more than double the voltage of standard silicon (≈0.7 V), enabling unprecedented power density and superior performance under field conditions.

This trend underscores the market’s shift toward ultra-high-efficiency solar modules, with perovskite–silicon tandems projected to enter mass-market adoption across utility-scale and distributed generation segments within the next 3–5 years.

Trend 2: Accelerated Commercial Validation of Vapor-Phase Deposition for Scalable Perovskite Manufacturing

To transition from laboratory-scale spin coating to industrial production, the perovskite sector is rapidly embracing vapor-phase deposition methods-a critical step toward achieving high-yield, large-area uniformity and production throughput comparable to CdTe, CIGS, and silicon manufacturing lines.

The industrial logic is clear:

- Superior film uniformity and compositional control-vapor-based processes such as PVD allow precise stoichiometry, uniform microstructure, and pinhole-free films, which are essential for high-efficiency modules.

- Strong manufacturing precedent-existing thin-film industries have already validated vapor deposition for high-volume production, making it a natural foundation for perovskite scale-up.

- High-efficiency vacuum-processed devices, with record efficiencies of 20.3%, proving that vapor-deposited perovskites are industrially viable.

- Simplified process control, relying on controllable parameters like deposition rate and pressure, eliminating the variability associated with solution methods and enabling line automation, higher yields, and consistent device performance.

The industry’s pivot toward vapor-phase techniques is establishing the foundational manufacturing ecosystem for Gigawatt-scale perovskite module production.

Opportunity 1: Expansion of Lightweight, Flexible Perovskite Modules for BIPV, Mobility, and Portable Power Applications

Perovskite solar cells’ compatibility with low-temperature processing enables ultra-light, flexible, and semi-transparent modules, creating new markets where crystalline silicon cannot compete. This opportunity spans Building-Integrated PV (BIPV), aerospace, electric vehicles, wearables, and portable electronics-segments demanding lightweight, high-efficiency, and customizable form factors.

Key commercial and research achievements include:

- Flexible PSCs reaching 23.35% certified efficiency with >5000 W/kg power-per-weight ratio, making them ideal for drones, aerospace, and EV applications where efficiency per gram is critical.

- Large-format flexible modules, such as a 1,200 × 1,600 mm perovskite module weighing only 2.04 kg, demonstrating scalability for architectural facades and curved structures.

- Mechanical durability, maintaining >91% of initial PCE after 5000 bending cycles, confirming suitability for rollable, foldable, and wearable energy systems.

- Aesthetic and functional BIPV integration, enabled by bandgap tunability, enabling modules that are semi-transparent, color-customizable, or patterned for architectural integration.

This opportunity positions perovskites as the enabler of next-generation lightweight solar technologies, expanding PV adoption beyond traditional rooftop and utility installations.

Opportunity 2: Advancing Lead-Free Perovskite Compositions and Encapsulation to Meet Global Regulatory and ESG Requirements

To achieve universal adoption, the perovskite industry must address concerns around lead content, particularly in consumer-facing and residential environments. The shift toward lead-free solutions-and robust encapsulation for lead-based products-offers a major commercialization opportunity aligned with environmental regulations such as EU RoHS and corporate ESG policies.

Key advancements include:

- Tin-based perovskites (FASnI₃) improving from 0.9% PCE in 2012 to 15.7% by 2024, marking significant progress toward viable lead-free formulations.

- Exceptional thermal stability in double perovskites like Cs₂TiBr₆, which maintained performance with no degradation at 200°C for 24 hours, highlighting their robustness under high-stress conditions.

- Encapsulation strategies-anti-diffusion barrier layers have been developed to contain lead in existing formulations, significantly reducing toxicity risk while preserving high efficiency.

- Broader research into low-toxicity alternatives, including bismuth (Bi) and antimony (Sb)-based perovskites, which offer favorable environmental profiles and promising long-term stability.

These developments position lead-free perovskites and advanced encapsulation as critical enablers for mass adoption, regulatory clearance, and consumer market expansion.

Perovskite Photovoltaics Market Share Analysis

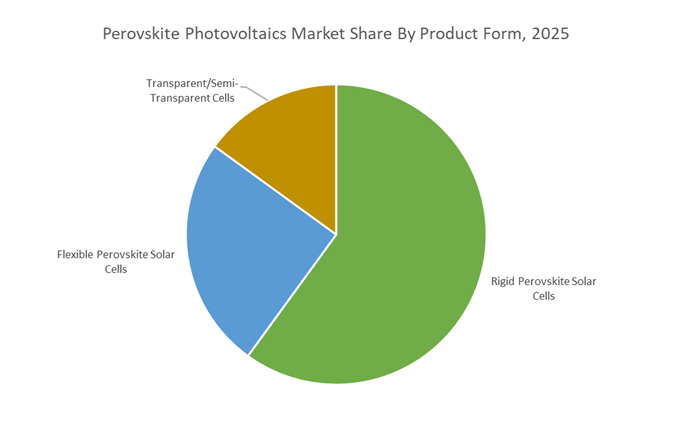

Market Share by Product Form: Rigid Perovskite Solar Cells Lead Through Efficiency Superiority, Glass-Based Durability, and Scalable Manufacturing Maturity

Rigid perovskite solar cells account for a dominant 60% share of the Perovskite Photovoltaics Market, driven by their unmatched performance in efficiency, stability, and manufacturability—three core metrics determining commercial readiness in the solar industry. Built on glass substrates, rigid perovskite cells consistently achieve the highest certified Power Conversion Efficiencies (26.1%–26.7%), outperforming flexible formats that typically reach 24.6%–25.1% due to inherent advantages in surface smoothness, thermal stability, and crystal film uniformity. This efficiency advantage is critical for developers and investors targeting the lowest Levelized Cost of Electricity (LCOE), as even minor gains in efficiency significantly improve energy yield per installed watt. Beyond performance, rigid glass substrates provide a hermetic, long-term barrier against moisture, oxygen, and thermal degradation—factors that historically limited perovskite adoption due to stability concerns. Glass-based encapsulation is currently the only proven pathway to meeting the 25-year operational lifetime required for commercialization in large-scale outdoor installations.

From a manufacturing perspective, rigid perovskite modules benefit from deep compatibility with existing glass-based sheet-to-sheet production lines widely used in the silicon PV industry. This alignment allows perovskite manufacturers—particularly tandem technology leaders like Oxford PV—to leverage mature, automated silicon module assembly practices without incurring the technical risks and high capex associated with early roll-to-roll flexible manufacturing. As a result, rigid perovskite formats offer the fastest route to industrial-scale deployment, making them the preferred product form for companies racing to bring high-efficiency perovskite and perovskite-silicon tandem modules to market.

Market Share by Application: Utility-Scale Solar Dominates as Perovskites Enable Record-Breaking Efficiency and Lowest LCOE in Gigawatt-Scale Projects

Utility-Scale Solar Panels represent the largest segment at 40% share, reflecting perovskite photovoltaics’ strong alignment with the cost and performance priorities of the global utility-scale PV industry. The most transformative driver is the perovskite–silicon tandem architecture, which has achieved certified efficiencies up to 33.7%–33.9%, surpassing the theoretical efficiency ceiling of single-junction silicon (~27%). For utility developers operating in a market where even a 1% efficiency improvement can materially lower LCOE and increase project bankability, the jump to >33% efficiency represents a structural shift in project economics, enabling more power generation per square meter, reduced land usage, and lower balance-of-system costs.

Perovskite technology also carries substantial long-term potential to reduce manufacturing costs due to low-temperature, solution-processed fabrication techniques (printing, coating, or evaporation), which contrast sharply with the energy-intensive, high-temperature processes required for crystalline silicon production. As production scales, this shift promises major CapEx and operational cost reductions, driving widespread adoption in large-scale solar fields where module cost competitiveness is paramount. With the global PV market now installing hundreds of gigawatts per year—and utility-scale deployments comprising the majority of this volume—any technology that delivers a meaningful efficiency advantage combined with strong cost-reduction potential is positioned to rapidly capture market share. This dynamic firmly positions perovskite-based modules, especially tandem architectures, as the most disruptive and strategically significant technology in the utility-scale solar segment.

Country Analysis: Global Perovskite Photovoltaics Commercialization Hubs

China – Global Leadership in Record-Breaking Tandem Efficiencies and the First Utility-Scale Perovskite Deployments

China dominates the Perovskite Photovoltaics Market through a combination of state-backed R&D, manufacturing investment, and world-leading efficiency breakthroughs. In April 2025, LONGi Green Energy achieved a certified world record of 34.85% efficiency for a crystalline silicon–perovskite tandem solar cell, independently verified by the U.S. National Renewable Energy Laboratory (NREL). This milestone positions China at the forefront of tandem perovskite commercialization just as global cell efficiency curves begin reaching the theoretical limits of conventional crystalline silicon. Another landmark innovation arrived in December 2025 when Nanjing University and international collaborators achieved 30.1% efficiency for a fully perovskite-based tandem (two perovskite layers), demonstrating scientific viability for all-perovskite architectures that circumvent silicon dependency.

China is also the first country to demonstrate large-area, utility-scale deployment of perovskite PV modules. In February 2025, a project in Zhejiang province installed an 8.6 MW perovskite solar plant using 95,648 modules supplied by Microquanta Semiconductor—the largest known real-world deployment to date. This installation validates field durability, energy yield, and operational reliability at a scale far beyond global pilot projects. On the manufacturing side, major players such as GCL Technology are investing heavily, with a 700 million yuan investment to build a 500 MW perovskite-silicon tandem module plant in Kunshan. Manufacturers like Renshine Solar are demonstrating scalability by achieving 19.42% module efficiency on a large 30×40 cm panel, strengthening China’s position as the undisputed leader in next-generation solar cell commercialization.

Germany & United Kingdom – First Commercial Perovskite Module Shipments and EU-Funded Industrial Pilot Lines

Europe’s leadership in perovskite–silicon tandem technology is driven by a combination of commercial breakthroughs (UK) and industrial pilot-line development (Germany), supported by Horizon Europe and national R&D programs. In September 2025, Oxford PV achieved a global industry milestone by completing the first commercial sale and shipment of tandem perovskite-silicon solar panels to a U.S. customer. These commercial-ready modules deliver a certified 24.5% efficiency, outperforming most conventional silicon modules and marking the transition of perovskite from a lab-scale innovation to a revenue-generating product class. Oxford PV’s commercialization progress positions the UK as the strategic spearhead for high-efficiency perovskite module market launches.

Germany is consolidating its role as the engineering and industrialization center for European perovskite PV manufacturing. The EU-funded PEPPERONI project, a collaboration involving Hanwha Qcells GmbH (Thalheim, Germany), secured €12.95 million under Horizon Europe to build Europe’s first industrial-grade perovskite/silicon tandem pilot line. The initiative aims to achieve 26% module efficiency on commercial-scale production equipment and meet >30-year operational stability targets, addressing bankability challenges. These combined advances, spanning commercial shipments in the UK and industrial pilot lines in Germany, demonstrate Europe’s intention to build a sovereign, high-efficiency perovskite PV manufacturing ecosystem under the broader EU energy resilience strategy.

United States – Flexible Perovskite Commercial Scale-Up and Defense-Driven Field Deployment

The United States is carving a distinctive leadership niche by focusing on flexible perovskite photovoltaics, defense applications, and the scale-up of domestic perovskite module manufacturing. In September 2025, Tandem PV raised $50 million to expand U.S.-based production facilities for commercial perovskite modules, addressing the national priority to establish secure, domestic supply chains for next-generation PV technologies. The scale-up is aligned with the broader DOE goal of reducing U.S. dependence on imported crystalline silicon modules while shifting toward higher-efficiency tandem architectures.

A major catalyst for U.S. adoption is the defense sector. In October 2025, Swift Solar deployed flexible perovskite modules as part of a Department of Defense operational trial to evaluate lightweight PV in microgrids and emergency infrastructure. Perovskite’s high power-to-weight ratio makes it ideal for military logistics, mobile communications, and energy-resilient field operations. Meanwhile, the U.S. Department of Energy’s Solar Energy Technologies Office (SETO) is channeling R&D funding toward solving the four commercial bottlenecks: stability, durability, manufacturability, and bankability. These initiatives position the U.S. as a strategic hub for the commercialization of flexible, ruggedized, and high-efficiency perovskite modules for both civilian and defense markets.

Japan – BIPV Perovskite Windows and Roll-to-Roll Manufacturing Technologies Lead Niche Commercialization

Japan is leveraging its strengths in industrial coatings, precision manufacturing, and advanced materials to lead in Building-Integrated Photovoltaics (BIPV) and flexible perovskite PV. A landmark initiative occurred in November 2025 when YKK AP and Panasonic HD began real-world testing of glass-type perovskite PV windows integrated directly into an occupied office building (Tanimachi YF Building). This demonstrates Japan’s strategic focus on embedding photovoltaics into architectural elements—balancing transparency, aesthetics, and energy generation—an area where perovskite’s tunability gives it a clear advantage over silicon.

Japan is also pursuing leadership in roll-to-roll and flexible module manufacturing, essential for non-rooftop PV applications such as curved building surfaces and portable power. J-POWER’s collaboration with U.S.-based Active Surfaces aims to pilot flexible perovskite modules across Japan, broadening deployment scenarios in harsh or space-constrained environments where rigid crystalline silicon modules underperform. This dual focus on BIPV and flexible PV integration positions Japan as a global pioneer in next-generation lightweight, multifunctional solar technologies that extend PV adoption far beyond traditional installations.

Competitive Landscape: Global Leaders Accelerating Tandem Adoption & Perovskite Industrialization

The competitive environment in the perovskite photovoltaics market is shaped by two core forces: (1) tandem technology pioneers pushing efficiency and IP leadership, and (2) industrial-scale manufacturers driving cost-down and scalable production. A mix of European innovators, Chinese large-scale manufacturers, and flexible-PV specialists are taking distinct strategic routes to capture emerging multi-billion-dollar opportunities across utility-scale, BIPV, VIPV, and IoT markets. Their competitive positioning increasingly depends on efficiency breakthroughs, stability data, patent portfolios, and the ability to scale to GW-class production.

Oxford PV remains the clearest global leader in perovskite-on-silicon tandem technology, backed by a strong European manufacturing base and a dominant IP position. The company marked a major commercial milestone in September 2025 by completing its first commercial sale of tandem panels to a U.S. utility-scale customer, validating product readiness beyond pilot volumes. In August 2025, Oxford PV achieved a 25.0% efficiency record on a 1.68 m² industrial-format tandem module, proving large-area manufacturing feasibility. Its April 2025 exclusive licensing partnership with Trina Solar underscores the high commercial value of its patent portfolio and supports high-volume scaling across the Chinese market.

LONGi has established itself as a powerhouse in tandem efficiency and interfacial engineering, setting the world record 34.85% tandem efficiency in April 2025. The was followed by a 33.4% flexible tandem efficiency record in November 2025, with exceptional 1.77 W/g power-to-weight ratio, enabling strategic expansion into vehicle-integrated and aerospace photovoltaics. LONGi further demonstrated scientific leadership through a July 2025 Nature publication detailing nanoscale defect passivation, reinforcing its long-term roadmap across both rigid and flexible perovskite-silicon tandem platforms.

JinkoSolar is aggressively pushing the industrialization of tandem technology through TOPCon–perovskite integration, achieving a 34.76% N-type TOPCon-perovskite tandem cell efficiency record in November 2025. The company’s R&D strategy focuses on novel perovskite crystallization methods and full-area passivated-contact engineering, preparing tandem architectures for high-volume mass production. JinkoSolar’s corporate vision positions tandem technology as the next major disruption following TOPCon’s global rollout, signaling a massive production shift likely beginning before the end of the decade.

UtmoLight is among the first companies to achieve full GW-scale perovskite module manufacturing, with its major facility going online in May 2025. The company specializes in slot-die coating, low-cost thermal processing, and large-area module fabrication, giving it a cost leadership position in the emerging utility-scale perovskite PV market. Its focus on ground-mounted and rooftop utility applications aligns with markets where module-level LCOE can be dramatically improved through large-scale, low-CAPEX perovskite processing.

Trina Solar is strategically positioning itself to industrialize tandem technology at scale. Its April 2025 exclusive patent licensing agreement with Oxford PV grants it access to critical tandem IP for manufacturing in the Chinese market. Trina combines the with its extensive global sales channels and GWh manufacturing capacity to accelerate commercialization. In parallel, its broader R&D strategy continues to diversify, supported by milestones including the 27.08% efficiency record for its N-type Cz-Si HJT cell in January 2025, illustrating its multi-path approach toward next-generation photovoltaic technologies.

Saule Technologies remains a pioneer in ultra-lightweight, flexible, semi-transparent perovskite photovoltaics using proprietary inkjet printing. Its products target high-value niches including BIPV façades, kinetic sunblinds, and IoT devices, where conventional silicon is impractical. Operating one of the world’s first commercial perovskite PV factories in Wrocław, Poland, Saule focuses on small-to-medium volume specialty applications where form factor and flexibility outweigh pure efficiency metrics.

Perovskite Photovoltaics Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$289.5 Million

|

|

Market Size (2035)

|

$10719.3 Million

|

|

Market Growth Rate

|

43.5%

|

|

Segments

|

By Device Structure (Perovskite-Silicon Tandem Cells, All-Perovskite Tandem Cells, Single-Junction Perovskite Solar Cells), By Cell Architecture (Planar Perovskite Solar Cells, Mesoporous Perovskite Solar Cells), By Product Form (Rigid Perovskite Solar Cells, Flexible Perovskite Solar Cells, Transparent/Semi-Transparent Cells), By Application (Utility-Scale Solar Panels, BIPV, Portable & Wearable Devices, Aerospace & Defense, Smart Glass & Automotive Glazing), By Manufacturing Method (Solution Processing, Vapor Deposition Methods, Vapor-Assisted Solution Methods)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Oxford PV, LONGi Green Energy Technology Co. Ltd., Microquanta Semiconductor Co. Ltd., Hanwha Qcells, GCL Technology, Swift Solar, Tandem PV, Saule Technologies, Perovskia Solar AG, UtmoLight, Renshine Solar, Meyer Burger Technology AG

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Perovskite Photovoltaics Market Segmentation

By Device Structure

- Perovskite-Silicon Tandem Cells

- All-Perovskite Tandem Cells

- Single-Junction Perovskite Solar Cells

By Cell Architecture

- Planar Perovskite Solar Cells

- Mesoporous Perovskite Solar Cells

By Product Form

- Rigid Perovskite Solar Cells

- Flexible Perovskite Solar Cells

- Transparent/Semi-Transparent Cells

By Application

- Utility-Scale Solar Panels

- BIPV

- Portable/Wearable Devices

- Aerospace & Defense

- Smart Glass/Automotive Glazing

By Manufacturing Method

- Solution Processing

- Vapor Deposition Methods (PVD/CVD)

- Vapor-Assisted Solution Method (Hybrid)

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies: Key Perovskite Photovoltaics Developers

- Oxford PV

- LONGi Green Energy Technology Co., Ltd.

- Microquanta Semiconductor Co. Ltd.

- Hanwha Q.CELLS GMBH (Qcells)

- GCL Technology

- Swift Solar

- Tandem PV

- Saule Technologies

- PEROVSKIA SOLAR AG

- UtmoLight

- Renshine Solar

- Meyer Burger Technology AG

*- List not Exhaustive