Market Overview: Bismuth Is Transitioning from By-Product Metal To Strategically Relevant Specialty Material

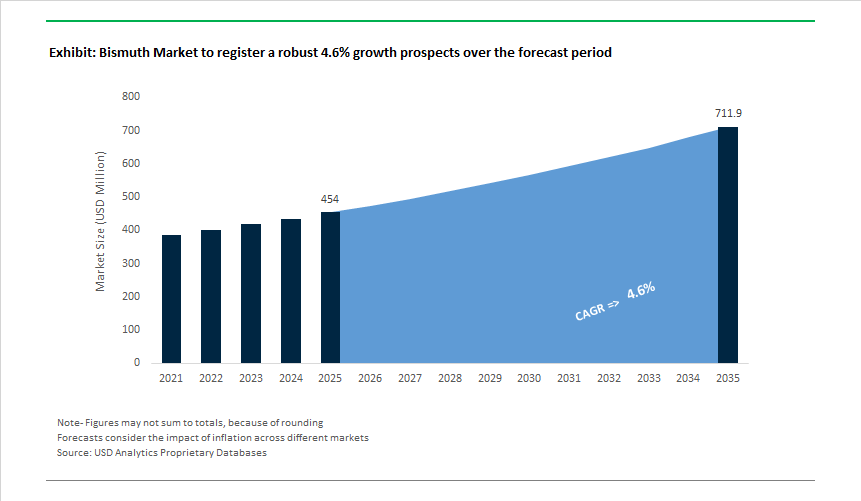

The global Bismuth Market is valued at USD 454 million in 2025 and is projected to reach USD 711.8 million by 2035, growing at a 4.6% CAGR as bismuth steadily moves up the value chain from a minor smelter by-product to a regulation-driven, purity-sensitive specialty metal. Today, bismuth demand is no longer opportunistic; it is being shaped by lead substitution mandates, pharmaceutical purity requirements, and functional materials demand in electronics and energy systems.

At the core of market expansion is regulatory-driven substitution of lead. Bismuth is now the preferred non-toxic alternative in low-melting alloys, lead-free solders, and fusible safety components, particularly in regions governed by RoHS, REACH, and medical device safety standards. Unlike many substitute metals, bismuth offers comparable melting behavior without introducing carcinogenic or bioaccumulative risk, allowing manufacturers to reformulate legacy lead systems with minimal process disruption. This substitution trend is structurally additive, contributing mid-single-digit annual demand growth in soldering, plumbing, fire-safety devices, and precision casting applications.

Parallel to substitution, high-purity bismuth compounds are gaining strategic importance in pharmaceuticals and electronics. In pharma, ultra-high-purity bismuth (4N-5N) is required for active pharmaceutical ingredients and medical formulations where trace-metal contamination thresholds are tightly controlled. In electronics, high-purity bismuth oxides and salts are increasingly specified in multilayer ceramic capacitors (MLCCs), varistors, and specialty dielectric formulations, linking bismuth demand to the growth of 5G infrastructure, IoT devices, and miniaturized electronics manufacturing, particularly across Asia-Pacific.

Supply dynamics are a defining strategic constraint. China accounts for roughly 84% of global primary bismuth production, largely as a by-product of lead, copper, and tungsten refining. This concentration creates persistent exposure to export controls, pricing volatility, and availability risk, especially for downstream users requiring consistent high-purity feedstock. As a result, manufacturers outside China are increasingly pursuing supply diversification strategies, including recovery from domestic smelter by-products, secondary refining, and recycled sourcing from solders and alloys. Bismuth is therefore shifting from a spot-purchased metal to a contracted, strategically sourced input.

Emerging functional applications reinforce the market’s long-term relevance. Bismuth telluride remains the dominant thermoelectric material for solid-state heating and cooling systems, enabling waste-heat recovery in automotive exhausts, industrial processes, and distributed energy systems. While volumes remain modest, these applications anchor bismuth demand in energy-efficiency and decarbonization roadmaps, adding optional upside beyond traditional metallurgy and chemicals.

Market Analysis: Recent Developments and Market Implications

The bismuth value chain has experienced price volatility, geographic production shifts, and an acceleration of high-purity product development that together are reshaping commercial strategies. In March 2024, Vietnam reported a dramatic production increase (≈+210% from 2020-2023) driven by improved recovery in tin smelting - this created a meaningful new non-Chinese feedstock corridor and showed how secondary recovery (from tin/lead smelters) can materially reduce source concentration risk. Also in March 2024, Shepherd Colour launched a bismuth vanadate yellow pigment, confirming continued industrial demand in specialty pigments and coatings.

Price and upstream dynamics tightened in January 2025, when monthly Rotterdam prices peaked (U.S. Geological Survey data) following elevated Chinese feedstock costs - the reported average price surged to around $6.29/lb in October 2024, highlighting raw material vulnerability and short-term margin pressure for downstream refiners. In March 2025 global R&D attention expanded into bismuth-based catalysts and green chemistry routes (CO₂ conversion), signaling growth beyond traditional metallurgy into higher-value chemical and catalyst markets. The same month, industry reporting indicated that JX Advanced Metals was progressing on an Arizona electronic-materials plant to supply high-purity sputtering targets for semiconductors - a strategic move toward localized high-purity supply for North American fabs.

Demand-side momentum strengthened through September 2025, as the Asia-Pacific electronics sector intensified purchases of high-purity bismuth oxide for MLCCs and varistors to support 5G and IoT device rollouts. Finally, December 2025 research disclosures around new RE3Bi7 bismuth compounds and advanced optics signalled potential future demand for ultra-high-purity and specialty crystalline bismuth materials - creating R&D-led premium use cases beyond classical markets.

Bismuth Market Trends and Opportunities

Trend 1: Structural Replacement of Lead in Potable Water System Components

The global removal of lead from drinking-water infrastructure is no longer incremental—it is becoming mandatory, funded, and enforceable, positioning bismuth as the only scalable metallurgical substitute that preserves casting and machining performance.

U.S. regulatory enforcement has crossed a tipping point. Under the EPA’s finalized Lead and Copper Rule Improvements (LCRI) in late 2024, more than $2.6 billion was allocated to identify and replace all lead service lines within a decade. This has accelerated adoption of copper–bismuth alloys (notably C89833) in valves, meters, and fittings. Bismuth’s high density (9.747 g/cm³) allows it to replicate lead’s role in improving molten fluidity and chip breakability—without the toxicity that violates the 0.25 wt% lead cap under the Safe Drinking Water Act.

In Europe, tightening enforcement under RoHS and EC 1272/2008 has pushed utilities and OEMs to qualify bismuth-bearing brasses (C87850, C89833) for long-life installations. Field studies conducted between 2024 and 2025 show these alloys achieving dezincification and pitting resistance on par with legacy C83600, eliminating a key technical objection to lead-free conversion.

From a manufacturing standpoint, recent 2025 metallurgical studies demonstrate that bismuth–antimony modified brasses reduce solidification shrinkage by 25–30% in low-pressure die casting. This directly protects yield economics, allowing producers to sustain ~80%+ throughput efficiency while remaining compliant—making bismuth substitution economically neutral rather than punitive.

Trend 2: High-Purity Bismuth Targets for Advanced Semiconductor Thin Films

As semiconductor nodes compress below 7 nm, bismuth is emerging as a critical enabler metal rather than a peripheral additive. The industry’s tolerance for metallic impurities is approaching zero, driving a decisive shift toward 5N–6N (99.999–99.9999%) bismuth sputtering targets.

In 2025, leading Asian fabs accelerated qualification of 6N bismuth targets for thin-film transistor layers, barrier coatings, and functional interfaces. At atomic dimensions, trace contaminants directly translate into yield loss; bismuth’s high atomic mass and clean evaporation behavior make it uniquely suited for defect-sensitive layers.

Beyond logic and memory, bismuth demand is expanding through Bi₂Te₃ thermoelectric thin films, increasingly integrated into on-chip cooling architectures for AI accelerators and advanced packaging. Late-2025 disclosures highlight bismuth’s role in photodetectors for autonomous systems and as back-contact materials in next-generation photovoltaics—applications where thermal stability and interface adhesion are non-negotiable.

The indirect effect is equally important: the surge in heterogeneous integration and 3D stacking for AI/ML chips is increasing consumption of specialty targets overall. Bismuth is benefiting as packaging architectures become more complex and material purity becomes a first-order design variable.

Opportunity 1: Bismuth-Based Coolants and Shielding in Small Modular Reactors (SMRs)

Nuclear innovation is reopening a high-value, long-duration opportunity for bismuth through lead–bismuth eutectic (LBE) systems in fast-spectrum reactors.

LBE’s low melting point (123.5 °C), chemical inertness with air and water, and low neutron activation provide decisive advantages over sodium or pure lead. The SVBR-100 reactor design, finalized in 2025, leverages LBE to enable passive safety, simplified containment, and compact modular layouts—attributes central to SMR economics.

Momentum accelerated in November 2025 with the announcement of the EAGL-1 LBE-cooled fast reactor in Indiana. The 240-MW closed-cycle design targets ~97% reduction in long-lived waste through on-site fuel recycling, exploiting bismuth’s favorable neutronic behavior. Parallel validation is underway at Belgium’s MYRRHA project, where LBE cooling is central to both accelerator-driven systems and future transmutation reactors.

For the bismuth market, SMRs represent low-volume but exceptionally high-value demand, characterized by long qualification cycles, premium purity requirements, and multi-decade operating lifetimes.

Opportunity 2: Pharmaceutical and Antimicrobial Drug Reformulations

Rising antimicrobial resistance (AMR) is restoring bismuth to the center of gastrointestinal and infectious-disease therapeutics—this time with modern clinical validation.

A 2025 global survey published in Gut documented clarithromycin resistance exceeding 15% in most regions, with extreme cases above 80%. As a result, bismuth-based quadruple therapy (BQT) has been reinstated as first-line treatment for Helicobacter pylori where legacy triple therapy success rates have collapsed below 70%.

Beyond GI disorders, late-2025 pharmacological studies show that bismuth compounds act as membrane-disrupting adjuvants, restoring the efficacy of older antibiotics against multi-drug-resistant Gram-negative pathogens. This positions bismuth not merely as an active ingredient, but as a resistance-mitigation platform—a rare attribute in modern drug development.

Emerging research into bismuth-derived anti-biofilm agents is opening adjacent opportunities in dermatology, wound care, and medical-device coatings. With a safety profile far superior to lead (LD₅₀ > 5,000 mg/kg), bismuth is increasingly attractive for OTC and chronic-use formulations, expanding its pharmaceutical footprint beyond acute GI therapies.

Market Share Analysis: Bismuth Market

Market Share by Purity: Commercial-Grade Bismuth Anchors Volume Through Alloying Economics and Regulatory Substitution

Commercial-grade bismuth (99.5%–99.99%) commands approximately 55% of global demand because it sits at the intersection of regulatory necessity, metallurgical efficiency, and scalable supply economics. In 2025, 99.99% (4N) purity has effectively become the global trading floor, as confirmed by refined-metal exporters such as Hunan Jinwang, since this grade feeds both downstream alloying and further purification without yield loss. The segment’s dominance is structurally tied to the global elimination of lead: bismuth-based solders now demonstrate double the reliability of early-generation lead-free alternatives in high-stress electronics, making commercial-grade material the preferred alloying input rather than costlier ultra-high-purity variants. In automotive and industrial steelmaking, micro-additions of 0.08–0.12% bismuth have proven to deliver ~20% machinability gains, reducing tool wear, cycle time, and energy consumption—an operational benefit that directly offsets bismuth’s price volatility. Critically, supply-side concentration reinforces buying urgency: nearly 70% of refined bismuth production is concentrated in China, creating a risk premium that encourages Western manufacturers to lock in commercial-grade volumes early rather than compete later for limited high-purity output. Together, these factors explain why commercial-grade bismuth functions as the market’s liquidity core rather than merely a mid-tier purity option.

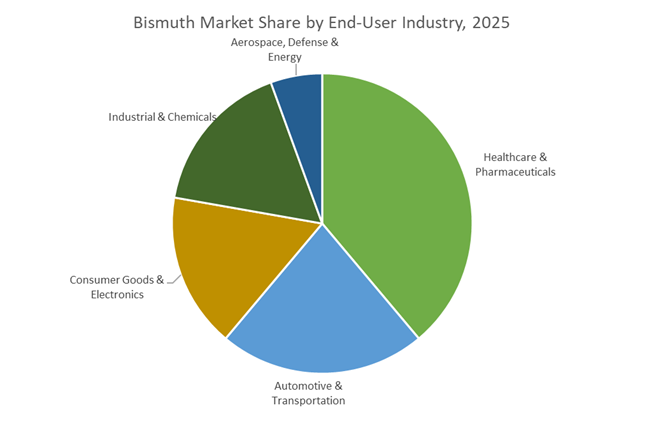

Market Share by Application: Healthcare & Pharmaceuticals Sustain Demand Through Non-Substitutability and Regulatory Lock-In

Healthcare and pharmaceuticals account for around 35% of bismuth consumption, not because of scale alone, but due to absolute non-substitutability in clinical protocols and regulatory frameworks. Roughly 40% of global bismuth chemical demand is tied to gastrointestinal therapies, driven by the worldwide adoption of bismuth-based quadruple therapy for H. pylori eradication—a standard that has no equivalent replacement using alternative metals. API-grade producers such as 5N Plus have expanded pharmaceutical bismuth output in response to sustained prescription growth in Asia-Pacific and Latin America, pushing the bismuth tripotassium dicitrate segment toward a projected USD 390 million valuation by 2035. Beyond GI treatments, healthcare demand is diversifying: bismuth’s low toxicity and high atomic number are enabling its substitution for lead in medical radiation shielding, reducing protective garment weight by up to 20%—a material advantage that aligns with occupational safety mandates in 2025 hospital infrastructure upgrades. Importantly, this segment is protected by regulatory lock-in: US-FDA and GMP certification requirements, including sub-1 ppm heavy-metal impurity thresholds, sharply limit supplier eligibility, insulating pharmaceutical demand from short-term price swings. As a result, healthcare represents the most inelastic, margin-stable end-use in the bismuth market, anchoring long-term demand even during cyclical downturns in metallurgy or electronics.

Competitive Landscape: Supply Concentration, High-Purity Specialists and Byproduct Miners

The competitive map is split between large, vertically integrated producers that dominate primary supply (China Minmetals), high-purity specialty refiners (5N Plus, Mitsubishi Materials), and miners/ smelter groups that recover bismuth as a byproduct (Industrias Peñoles). Each player competes on feedstock access, purification capability, product form (ingots, oxide, nitrate, sputtering targets), regulatory traceability, and the ability to supply premium pharmaceutical and semiconductor markets.

China Minmetals - The Large-Scale Primary Metal Anchor Shaping Global Availability

China Minmetals, through state-backed subsidiaries, controls the largest slice of primary bismuth supply and leverages vertical integration from mining and smelting to refining. Its scale enables global volume shipments of bismuth metal (ingots) into low-melting alloy and metallurgical markets, but the company is exposed to feedstock price swings and Chinese policy shifts that propagate through global pricing. For manufacturers seeking volume, Minmetals remains the default source - yet counterparties increasingly hedge by qualifying secondary and non-Chinese suppliers.

5N Plus - Premium High-Purity Bismuth Solutions For Advanced Electronics and Thermoelectrics

5N Plus is a global leader in ultra-high-purity bismuth compounds (4N-7N), serving semiconductors, optoelectronics, and thermoelectric material producers. Its advantage lies in advanced purification, tight traceability, and customized shapes (sputtering targets, powders) required by OEMs and fabs. 5N Plus’s ESG and process transparency differentiate it for Western and Japanese customers who pay premiums for auditable, low-impurity raw materials.

Industrias Peñoles - North American Byproduct Supply and Diversification Play

Industrias Peñoles recovers bismuth as a byproduct from its Torrejón non-ferrous complex, making it a crucial North American source that helps buyers diversify away from Asian concentration. Its integrated refinery capabilities allow supply into low-melting alloy and metallurgical markets across the Americas. For companies requiring regional supply assurance, Peñoles provides an important alternative and regional logistics advantage.

Hunan Jinwang - Chinese Compound Specialist With Strong Downstream Derivative Supply

Hunan Jinwang focuses on downstream bismuth compounds (BiOCl, Bi₂O₃, nitrates) for cosmetics, pigments, and pharmaceutical intermediates. Following its 2020 reorganization, it has strengthened capital and scale for compound processing, supplying global customers in cosmetics (pearl pigments) and specialty chemical markets where form and consistent compound quality are decisive.

Mitsubishi Materials - Recycler and High-Purity Japanese Supplier For Niche High-Value Applications

Mitsubishi Materials leverages recycling expertise and precision refining to supply high-purity bismuth for Japanese electronics, fiber-doped optical components, and pharmaceuticals. Its recycling footprint and ability to produce tightly specified bismuth grades make it a preferred supplier for Japanese OEMs that demand domestic provenance, strict quality control, and customized material forms.

China remains the world’s largest bismuth producer and refiner, but 2025 marks a decisive shift from export-driven dominance to state-controlled resource management. On February 4, 2025, the Ministry of Commerce (MOFCOM), in coordination with the General Administration of Customs, imposed strict export controls on bismuth, tungsten, and tellurium. Under this framework, all international shipments now require government permits, formally elevating bismuth to a national security material. This policy has directly constrained global availability, forcing downstream industries in semiconductors, nuclear technology, and advanced alloys to reassess sourcing strategies.

The immediate market impact was pronounced. Between Q2 and Q4 2025, international refined bismuth prices surged sharply—by as much as seven-fold in certain spot indices—reflecting panic buying and inventory hoarding outside China. Strategically, Beijing is using this leverage to retain bismuth domestically for value-added applications, including bismuth-based semiconductors, thermoelectric materials, and superconducting research under the “New Quality Productive Forces” initiative. As a result, China is transitioning from a bulk exporter to a gatekeeper of refined bismuth technology, reshaping global trade flows.

South Korea: Building a Critical Mineral Buffer for High-Tech Manufacturing

South Korea is emerging as a strategic alternative hub for refined bismuth, leveraging its world-class smelting infrastructure to insulate its semiconductor and electronics sectors from Chinese supply shocks. In December 2025, Korea Zinc announced a KRW 1.5 trillion (~$1.1 billion) domestic investment program extending to 2029, with a major allocation toward expanding bismuth output at its Onsan Smelter. This expansion is explicitly designed to stabilize supply for domestic and allied markets amid escalating export controls from China.

From a policy perspective, the Ministry of Trade, Industry and Energy (MOTIE) has classified bismuth as a National Strategic Technology material, recognizing its growing role in indium–bismuth–tin (InBiSn) low-temperature solders used in AI-driven semiconductor packaging and advanced chiplet architectures. Reinforcing its geopolitical positioning, South Korea finalized agreements in late 2025 to provide priority access to Korean-produced bismuth for U.S. government and defense-linked customers from 2026 onward, strengthening its role as a trusted supplier within allied supply chains.

United States: CHIPS Act–Backed Reshoring of Bismuth Refining

The United States has formally integrated bismuth into its critical minerals and semiconductor reshoring agenda, driven by supply chain vulnerabilities exposed by Chinese export controls. In December 2025, the U.S. Department of Commerce awarded $210 million in CHIPS and Science Act funding to Crucible Metals, a subsidiary of Korea Zinc. This funding underpins the construction of a $6.6 billion advanced smelter in Tennessee, representing the most significant U.S. investment in non-ferrous critical mineral refining in decades.

Once operational—targeted for 2029—the Tennessee facility will be capable of processing 13 critical minerals, including bismuth, gallium, and germanium, specifically for semiconductor manufacturing, defense systems, and atomic research. Complementing this industrial push, the U.S. Geological Survey (USGS) reaffirmed bismuth’s inclusion on its 2025 Critical Minerals List, citing its importance in non-toxic metal substitution and nuclear applications. Collectively, these moves position the U.S. to rebuild domestic bismuth refining sovereignty for the first time in a generation.

Canada: Advancing North American Bismuth Sovereignty via the NICO Project

Canada is developing the most strategically significant non-Chinese integrated bismuth project in the Western Hemisphere, centered on the NICO deposit in the Northwest Territories. In December 2025, Fortune Minerals completed the acquisition of its Alberta refinery site in Lamont County for C$6 million, a key step toward vertically integrated production. This refinery is designed to process concentrates from the NICO mine, which hosts an estimated 12% of global bismuth reserves, alongside cobalt and gold.

By 2025, Fortune Minerals had successfully validated bismuth ingot and bismuth oxide production, targeting long-term supply contracts for clean energy systems, electronics, and non-toxic lead replacement applications. The project is backed by a C$3.8 million loan from Prosper NWT, a public agency of the Government of the Northwest Territories, underscoring Canada’s policy commitment to domestic refining and supply chain independence. Strategically, NICO positions Canada as a cornerstone supplier for U.S. and European markets seeking secure, ESG-aligned bismuth sources.

Vietnam: Establishing Itself as a Dependable Non-Chinese Supplier

Vietnam is rapidly consolidating its position as a critical alternative supplier of bismuth, leveraging its polymetallic resource base to diversify global sourcing. In November 2025, Masan High-Tech Materials received government approval for an updated mining plan at the Nui Phao project, one of the largest bismuth and tungsten operations outside China. This approval enables production optimization and long-term output stability at a time of tightening global supply.

Vietnam’s strategic importance was further highlighted during the 2025 G20 Summit, where national leadership positioned Nui Phao as a pillar of the Strategic Minerals Framework aimed at reducing single-country dependency. In 2024–2025, Vietnamese bismuth exports accounted for a growing share of non-Chinese imports into the U.S. and Europe, reinforcing Vietnam’s reputation as a reliable supplier for high-tech and industrial consumers navigating geopolitical risk.

Australia: Mid-Stream Processing and By-Product Recovery Strategy

Australia’s bismuth strategy in 2025 centers on value-added recovery rather than primary mining, integrating bismuth extraction into its broader critical minerals ecosystem. Under the Australian Critical Minerals Strategy 2023–2030, Geoscience Australia expanded funding in 2025 for pre-competitive data acquisition, targeting bismuth-rich potential in existing lead, cobalt, and gold tailings. This approach aligns with Australia’s focus on ESG-compliant, low-impact resource development.

At the industrial level, projects such as the Kwinana Cobalt Refinery, led by Cobalt Blue, are being evaluated for their ability to recover bismuth as a high-value by-product. Supported indirectly by the government’s $4 billion Critical Minerals Facility, these initiatives aim to strengthen Australia’s role in mid-stream processing and rare metal recovery, supplying bismuth for advanced metallurgy and eco-friendly alloy applications.

2025 Strategic Matrix: Bismuth Market – National Comparison

Bismuth Market Strategic Matrix

|

Country

|

Strategic Driver

|

2025 Key Milestone

|

Primary Application Focus

|

|

China

|

Resource sovereignty

|

MOFCOM export controls (Feb 2025)

|

Semiconductors, defense alloys

|

|

South Korea

|

Supply chain de-risking

|

KRW 1.5T Onsan smelter expansion

|

Low-temp AI chip solders

|

|

United States

|

CHIPS Act reshoring

|

$210M funding for TN smelter

|

Semiconductor & atomic research

|

|

Canada

|

Integrated supply chain

|

Alberta refinery acquisition (NICO)

|

Non-toxic lead replacements

|

|

Vietnam

|

Supply diversification

|

Nui Phao mining plan approval

|

Polymetallic export growth

|

|

Australia

|

By-product recovery

|

Expanded critical minerals funding

|

Advanced metallurgy & green alloys

|

Bismuth Market Report Scope

Bismuth Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$454 Million

|

|

Market Size (2035)

|

$711.8 Million

|

|

Market Growth Rate

|

4.6%

|

|

Segments

|

By Derivative Type (Bismuth Oxide, Bismuth Nitrate, Bismuth Oxychloride, Bismuth Subsalicylate, Bismuth Subcarbonate, Bismuth Metal), By Purity Level (Commercial Grade, High Purity, Ultra-High Purity), By Application (Pharmaceuticals, Cosmetics & Pigments, Metallurgy, Electronics & Semiconductors, Chemicals), By End-User Industry (Healthcare, Automotive, Consumer Goods, Aerospace & Defense, Energy)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Hunan Jinwang Bismuth Industrial Co. Ltd., Korea Zinc Co. Ltd., 5N Plus Inc., Masan High-Tech Materials, Industrias Peñoles S.A.B. de C.V., Hunan Shizhuyuan Nonferrous Metals Co. Ltd., Merck KGaA, TIB Chemicals AG, BASF SE, Fortune Minerals Limited, Zhuzhou Keneng New Material Co. Ltd., Xianyang Yuehua Bismuth Co. Ltd., Umicore N.V., China Minmetals Corporation, Western Minmetals (SC) Corporation

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Bismuth Market Segmentation

By Derivative Type

- Bismuth Oxide

- Bismuth Nitrate

- Bismuth Oxychloride

- Bismuth Subsalicylate

- Bismuth Subcarbonate

- Bismuth Metal

By Purity Level

- Commercial Grade

- High Purity

- Ultra-High Purity

By End-User Industry

- Healthcare

- Automotive

- Consumer Goods

- Aerospace & Defense

- Energy

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in Bismuth Market

- Hunan Jinwang Bismuth Industrial Co., Ltd.

- Korea Zinc Co., Ltd.

- 5N Plus Inc.

- Masan High-Tech Materials

- Industrias Peñoles, S.A.B. de C.V.

- Hunan Shizhuyuan Nonferrous Metals Co., Ltd.

- Merck KGaA

- TIB Chemicals AG

- BASF SE

- Fortune Minerals Limited

- Zhuzhou Keneng New Material Co., Ltd.

- Xianyang Yuehua Bismuth Co., Ltd.

- Umicore N.V.

- China Minmetals Corporation

- Western Minmetals (SC) Corporation

*- List not Exhaustive