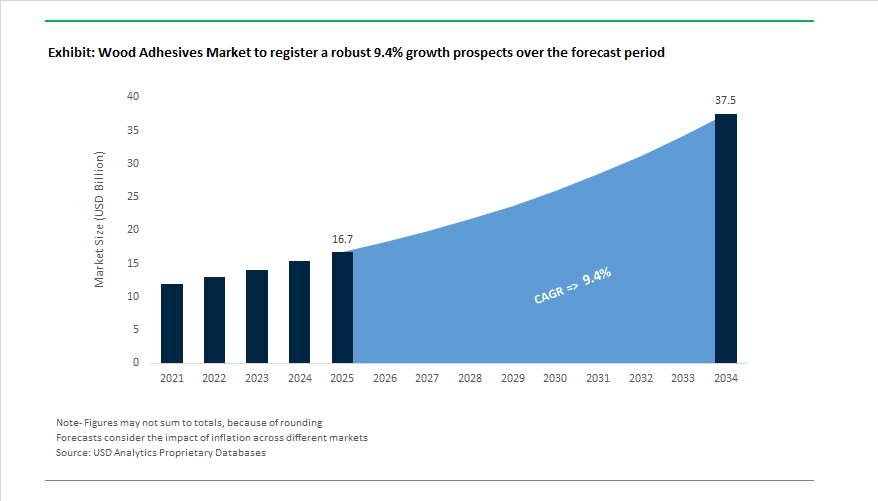

The Global Wood Adhesives Market is projected to expand from USD 16.7 billion in 2025 to USD 37.5 billion by 2034, advancing at a CAGR of 9.4%, reflecting a structural shift in how wood bonding systems are formulated, specified, and deployed across furniture, cabinetry, plywood, and engineered wood manufacturing. Growth is increasingly shaped by chemistry substitution, as producers accelerate the move away from formaldehyde-releasing systems toward bio-based, waterborne, and ultra-low-emission adhesives that align with tightening REACH, CARB, and EPA TSCA Title VI requirements. Adhesives have therefore become a regulatory and reputational lever, not just a cost input, in downstream wood products.

At the formulation level, the market is undergoing a decisive pivot toward waterborne and hybrid bio-based systems, supported by advances in polymer design and application engineering that reduce the historical trade-offs between emissions, curing speed, and bond strength. Soy-, starch-, and lignin-modified binders are moving from niche adoption into broader furniture and interior panel applications, while next-generation waterborne PU and acrylic systems are being optimized for shorter press times, lower drying energy, and compatibility with high-speed production lines. At the same time, conventional chemistries retain differentiated roles: UF systems continue to anchor cost-sensitive interior panels, while PUR and MDI-based adhesives gain share in moisture-exposed and higher-performance assemblies. This segmentation is reinforcing a two-track market—cost-optimized legacy binders alongside premium, regulation-ready solutions.

From a buyer and specifier perspective, adhesive selection is increasingly a multi-variable optimization exercise. Procurement decisions balance VOC and formaldehyde compliance, curing kinetics and line efficiency, and long-term bond durability across heterogeneous substrates, including solid wood, composite panels, and low-surface-energy laminates. As a result, investment priorities are shifting upstream into waterborne application equipment, drying and press optimization, and closer supplier partnerships that can de-risk raw-material volatility and ensure formulation continuity. Suppliers capable of combining chemistry innovation with process support are gaining preference, as wood manufacturers seek to protect throughput and margins while navigating rapid regulatory and sustainability transitions.

Product, process, and policy tailwinds converged through 2025. In May 2025, Henkel unveiled micro-emission hot-melt wood adhesives at Ligna (Hanover) with <0.1% diisocyanate emissions, boosting worker safety and REACH compliance for edge banding and lamination. Two months earlier, in March 2025, Henkel launched Loctite HB XE for CLT/GLT, meeting Eurocode 5 with an ≈0.65 mm/min linear charring rate, addressing the market’s push for fire-resistant, structural timber bonding.

Digitalisation and cost control also advanced. October 2025 analysis flagged AI-driven autonomous manufacturing reshaping engineered wood adhesives, improving quality and reducing conversion costs. In June 2025, H.B. Fuller posted +110 bps YoY expansion to 32.2% adjusted gross margin, reflecting pricing and productivity actions that cushion feedstock volatility. Parallel trade commentary in May 2025 warned that U.S. tariff escalation on petrochemicals/intermediates would pressure synthetic binder input costs—prompting dual-sourcing and formula flexibility.

The innovation funnel remains rich. Q3 2024 German research consortia accelerated bio-based binder development, signaling durable European support for renewable content. In July 2025, trackers noted intensified R&D—e.g., new G6520/SG6518 series from a peer—aimed at high-performance wood bonding. Strategic channel plays continued: October 2024 saw OEMs and adhesive majors cement long-term supply contracts with prefab/modular builders. The takeaway: micro-emission HM, structural PUR for mass timber, AI process control, and sourcing agility define competitive advantage as the market scales.

Market Trend 1: Accelerated Shift to Formaldehyde-Free Binders for Composite Wood Panels

The global wood adhesives industry is witnessing a sweeping transition toward formaldehyde-free binder systems driven by increasingly stringent indoor air quality regulations and sustainability mandates. Traditional urea-formaldehyde (UF) and phenol-formaldehyde (PF) resins, long used in plywood, particleboard, and MDF production, are being replaced by soy-based, PVA, and pMDI (polymeric MDI) formulations that eliminate formaldehyde emissions while maintaining structural performance.

The U.S. EPA TSCA Title VI rule and the EU REACH Annex XVII restriction (effective August 2026) have set a harmonized emission limit of 0.062 mg/m³ for wood-based panels and furniture, enforcing near-zero formaldehyde emissions across major economies. The alignment creates a unified global benchmark that mandates the use of low-emission, formaldehyde-free adhesives for manufacturers seeking market access in North America and Europe.

In parallel, Canada’s amendments to the Formaldehyde Emissions from Composite Wood Products Regulations cap emissions at 0.04 ppm for 90% of tested samples, a threshold substantially lower than the EU’s earlier E1 standard of 0.124 mg/m³. The regulatory tightening propels the industry toward Zero-Formaldehyde (NAUF) and Ultra-Low-Emission (ULEF) adhesive systems, particularly in interior-grade wood panels used for residential and office furniture.

From an innovation standpoint, the market has seen over 30% of new adhesive formulations introduced in 2024 based on renewable chemistries such as lignin, starch, and soy derivatives. The trend reflects a strong R&D reorientation toward bio-based, sustainable wood adhesives that meet both green building certifications (LEED, BREEAM) and indoor air quality standards (IAQ).

Market Trend 2: Adoption of Fast-Press, Room-Temperature Curing Adhesives for Mass Timber Construction

The rise of mass timber architecture, particularly Cross-Laminated Timber (CLT) and Glue-Laminated Timber (Glulam), has intensified the demand for fast-curing, room-temperature adhesives that enable high-throughput manufacturing with lower energy inputs. The structural transition from phenolic to one-component Polyurethane (PUR) systems represents one of the most significant shifts in the wood adhesives market to date.

European CLT manufacturers have reported that 1C-PUR structural adhesives reduce pressing and full-cure times to 1–4 hours, compared to over 6–8 hours required for traditional Phenol-Resorcinol-Formaldehyde (PRF) adhesives. The remarkable improvement in cycle time optimization enhances production capacity, supporting the global push toward industrial-scale CLT manufacturing for sustainable urban construction.

Another critical advantage of PUR adhesives is their room-temperature curing capability, which eliminates the need for energy-intensive hot presses, resulting in substantial reductions in embodied carbon. As the global construction sector seeks to minimize operational and embedded CO₂ emissions, low-energy-curing structural adhesives are becoming essential to net-zero building initiatives.

These technological advancements position Polyurethane (PUR) systems as a cornerstone in the ongoing green transition of engineered wood products (EWPs) manufacturing, ensuring a balance between performance, energy efficiency, and sustainability.

Market Opportunity 1: Development of Bio-Based Polyols for Sustainable Polyurethane Binders

The growing emphasis on carbon footprint reduction and corporate sustainability commitments is opening vast opportunities in the development of bio-based polyurethane (PU) adhesives. A major innovation frontier lies in the use of bio-based polyols derived from renewable feedstocks such as lignin, soybean oil, jatropha, and castor oil, which can replace petroleum-based polyols without compromising adhesive performance.

Recent academic findings demonstrate that isosorbide-derived polyols improve thermal degradation onset temperature by 25°C and glass transition temperature (Tg) by 10°C compared to conventional PU adhesives. The enhancement provides higher mechanical and thermal stability—key for structural bonding applications in plywood, LVL (Laminated Veneer Lumber), and flooring adhesives.

Further, vegetable oil polyols enable up to 35 wt% substitution of fossil-based polyols, maintaining comparable mechanical strength and adhesion. The global abundance and renewability of triglyceride-rich oils make them cost-competitive and scalable, providing a direct pathway to carbon-neutral adhesive production.

The evolution toward bio-based polyurethane binders aligns with global green chemistry initiatives and circular economy models, positioning renewable raw materials as the future backbone of sustainable wood adhesives manufacturing.

Market Opportunity 2: Engineering of Fire-Retardant, Intumescent Adhesives for Exposed Mass Timber Construction

With the 2021 International Building Code (IBC) expanding approvals for taller mass timber structures, the fire performance of wood adhesives has become a critical engineering parameter. The development of intumescent, fire-retardant adhesive systems capable of maintaining Glue Line Integrity in Fire (GLIF) is essential for ensuring life safety and achieving building code compliance in high-rise timber applications.

A key breakthrough comes from Loctite’s HB XE Line, a structural PUR adhesive certified to meet Eurocode 5 (EC5) fire protection standards. These systems actively slow the burn rate and prevent secondary flashover by maintaining structural integrity under fire exposure—a fundamental requirement for exposed CLT and Glulam structures.

Comparative testing of CLT walls indicates that traditional melamine-formaldehyde (MF) and melamine-urea-formaldehyde (MUF) adhesives lose bond strength twice as quickly under thermal stress compared to advanced PUR or intumescent systems. The data emphasizes the adhesive’s direct influence on the fire endurance and collapse resistance of mass timber assemblies.

Future innovation focuses on graphite-based intumescent fillers and nanocomposite additives that can form insulating char layers during combustion. These hybrid materials not only enhance fire performance but also align with sustainability objectives through halogen-free, non-toxic formulations.

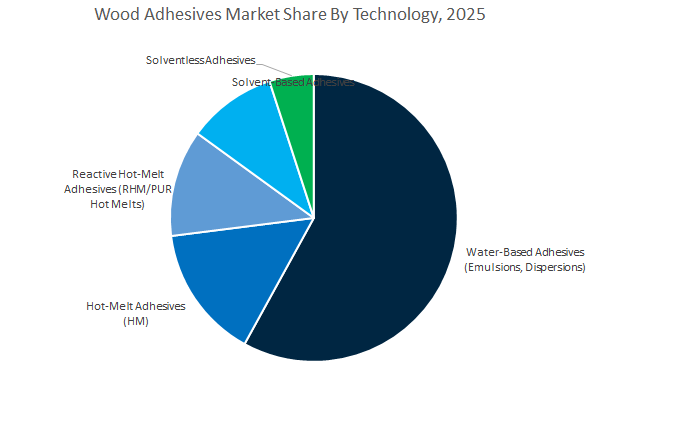

Wood Adhesives Market Share Insights, 2025-2034

Market Share by Technology

The water-based adhesives segment dominates the global wood adhesives industry, accounting for an estimated 54.9% of the projected 2025 market share, establishing itself as the most preferred formulation in wood bonding applications. These adhesives—predominantly polyvinyl acetate (PVAc) and vinyl acetate ethylene (VAE) emulsions—are favored for their low VOC content, environmental compliance, and excellent workability, aligning with global sustainability standards. Their ease of cleanup, strong bonding capacity for porous wood surfaces, and suitability for indoor furniture, cabinetry, and millwork applications make them the go-to choice for manufacturers prioritizing performance and safety. Moreover, the increasing enforcement of stringent environmental regulations in North America, Europe, and Asia-Pacific has accelerated the industry-wide transition toward waterborne formulations. Water-based adhesives continue to expand their footprint in woodworking and panel assembly, where fast-setting, eco-friendly solutions are replacing traditional solvent-based products.

Hot-Melt Adhesives (HMA) represent a key segment, crucial for high-speed, automated wood processing applications such as edge-banding, profile wrapping, and assembly line manufacturing. Their instant bonding capability, clean application, and compatibility with automated systems make them integral to mass production of furniture and decorative components. A particularly fast-growing subcategory is Reactive Hot-Melt (RHM/PUR) Adhesives, which combine the processing convenience of conventional hot-melts with the superior mechanical strength and moisture resistance of reactive curing. These PUR-based adhesives are widely adopted in flooring, architectural millwork, and outdoor furniture, where heat and humidity resistance are critical.

On the other hand, solvent-based adhesives are witnessing a steady decline due to their high VOC emissions, flammability, and environmental compliance costs. However, they retain niche relevance in applications that require strong adhesion to dense or oily wood species, or under extreme temperature variations. Meanwhile, solventless systems, which include 100% solids epoxy and polyurethane formulations, cater to specialized structural applications such as engineered wood bonding, mass timber construction, and marine joinery, where long-term performance and durability are non-negotiable.

Market Share by End-Use Industry

The furniture industry remains the single largest consumer of wood adhesives, commanding approximately 31.6% of the projected 2025 market share. The segment’s dominance stems from the mass production of cabinetry, case goods, and upholstered furniture frames, all of which rely heavily on water-based and hot-melt adhesives for assembly and surface bonding. Manufacturers prioritize adhesives that deliver strong initial tack, flexible open times, and long-term durability for wood joinery and panel lamination. Growth in this segment is fueled by the rising demand for ready-to-assemble (RTA) furniture, modular interiors, and custom cabinetry, especially across urban markets in Asia-Pacific and Europe. The sector’s focus on sustainability and indoor air quality also reinforces the transition to low-VOC, non-toxic adhesive formulations.

The construction sector represents the second-largest and most rapidly expanding end-use category, driven by the adoption of engineered wood and mass timber construction technologies such as CLT (Cross-Laminated Timber), Glulam (Glued Laminated Timber), and LVL (Laminated Veneer Lumber). These structural wood products rely on high-performance reactive adhesives—notably PUR, EPI, and PRF (Phenol-Resorcinol-Formaldehyde)—to achieve the strength and environmental durability needed for load-bearing applications. The ongoing global shift toward sustainable and carbon-neutral construction materials has significantly increased the demand for long-lasting, moisture-resistant adhesives in both residential and commercial building projects.

The Cabinets and Millwork segment represents a significant overlap between furniture and construction, emphasizing precision bonding, aesthetic finishes, and material versatility. It leverages PVAc for interior joints, PUR hot-melts for edge-banding, and water-resistant adhesives for laminates and veneers, reflecting the need for both performance and design flexibility. Meanwhile, the Flooring and Decking industry continues to be a consistent consumer of moisture-resistant and elastic adhesives for both installation and manufacturing processes, ensuring dimensional stability in changing temperature and humidity conditions.

H.B. Fuller positions as the largest pureplay adhesives provider, spanning hot-melt, reactive HM, solvent-based, and water-based platforms with depth in decorative lamination and door assembly. In Q2 2025, the firm reported 18.4% adjusted EBITDA margin (+130 bps YoY), underscoring disciplined pricing and cost takeout. Nearly 60% of new NPD targets sustainability (low-emission/NAF solutions), aligning with customer decarbonization roadmaps while preserving high-performance wood bonding at scale.

Henkel leads in structural wood adhesives with the Loctite HB XE line for CLT/Glulam (launched March 2025), engineered for Eurocode 5 fire performance. In May 2025, it debuted micro-emission hot melts (<0.1% diisocyanate) for safer, REACH-compliant edge-banding/lamination. Continued investment in global Technology Centers strengthens application collaboration, while formulations emphasize high heat/moisture resistance for interior and exterior assemblies.

3M offers structural adhesives, epoxies, polyurethane sealants (e.g., 3M™ Polyurethane Adhesive Sealant 550 Fast Cure) and broad spray adhesives (e.g., 3M™ Super 77™) for assembly and lamination. Its Scotch-Weld™ EPX™ dispensing ecosystem (mixers, nozzles, applicators) improves process stability and takt-time. 3M’s Sustainability Value Commitment attaches to each new product, ensuring innovations improve environmental and safety metrics across woodworking and composites.

Ashland supplies enabling polymer additives—Natrosol™ HEC, Aquaflow™—that deliver thickening, sag resistance, cohesion/adhesion, and foam control in water-based wood adhesives. Its chemistry is pivotal for non-staining wallpaper adhesives and panel lines, where viscosity control defines coat weight, penetration, and final bond. The company’s specialty focus supports low-VOC compliance while stabilizing line performance for converters and panel manufacturers.

Koleb is cited for a patented, non-toxic adhesive positioned as a direct, high-performance substitute for UF binders. Its strategy emphasizes licensing a bio-based, two-component water-based PU technology to majors and engineered-wood producers for on-site production, minimizing logistics and enabling rapid adoption. The VOC-free structural profile and cross-material bonding (concrete, ceramic, wood) reflect a materials-science breakthrough aimed at healthier indoor environments.

Country Analysis – Global Wood Adhesives Market Developments

United States: Regulatory Leadership and Bio-Adhesive Commercialization Drive Sustainable Growth

The United States wood adhesives market continues to lead globally in formaldehyde regulation, bio-based adhesive development, and structural timber innovation. The EPA’s TSCA Title VI remains the definitive benchmark for formaldehyde emission compliance, setting ultra-strict limits (≤0.05 ppm) across Hardwood Plywood, MDF, and Particleboard categories. The has accelerated the shift toward Ultra-Low-Emitting Formaldehyde (ULEF) and No-Added-Formaldehyde (NAF) adhesives. Manufacturers are increasingly replacing urea-formaldehyde resins with soy-based, phenol-resorcinol, and MDI-based systems, meeting not only EPA and CARB requirements but also the criteria for LEED and GreenGuard certification.

The U.S. is also witnessing a surge in Cross-Laminated Timber (CLT) and Glulam beam production, supported by federal infrastructure investments and the Department of Defense’s adoption of mass timber projects. The has strengthened demand for Polyurethane (PUR) and Phenol-Resorcinol-Formaldehyde (PRF) adhesives that deliver structural integrity, water resistance, and fire safety compliance. In 2024–2025, adhesive manufacturers such as H.B. Fuller and Franklin International introduced Moisture-Curing Polyurethane (MCPU) adhesives for high-humidity outdoor and structural bonding applications. Moreover, the EPA’s recent technical corrections to TSCA Title VI improved certification flexibility for remote audits—benefiting manufacturers adapting to hybrid production systems. The ongoing R&D momentum in soy-protein chemistry and bio-isocyanate systems continues to position the U.S. as the global leader in eco-innovation and sustainable wood adhesives.

China: Engineered Wood Expansion and Eco-Transition Drive Adhesive Innovation

China’s wood adhesives industry is expanding at an unprecedented scale, driven by rapid growth in engineered wood production and the transition toward low-emission adhesives. The country remains the world’s largest producer of wood-based panels, and recent industrial policies are prompting manufacturers to upgrade production lines with Melamine-Urea-Formaldehyde (MUF) and MDI-based adhesives to meet export-quality standards. Environmental regulations under China’s 14th Five-Year Plan and Made in China 2025 initiative emphasize VOC reduction and sustainable manufacturing, pushing a shift toward water-based and formaldehyde-free adhesive technologies.

The prefabricated housing and modular construction sectors are key growth drivers, demanding fast-curing Polyvinyl Acetate (PVAc) and Hot-Melt adhesives suitable for automated production. Meanwhile, bio-adhesive development is gaining traction as Chinese research institutions explore starch, lignin, and agricultural residue-based polymer systems. Manufacturers are also upgrading adhesive formulations to meet stringent TSCA Title VI and EU E1/E0 emission standards to maintain export competitiveness. In the context of expanding furniture, flooring, and decorative panel exports, local companies are investing in high-speed adhesive dispensing technology to improve precision and reduce curing times. China’s policy-supported modernization of its chemical and wood processing industries positions it as a dominant global hub for sustainable, high-performance wood adhesives.

Germany: Structural Timber Leadership and Eco-Innovation Define Market Strategy

Germany stands at the forefront of advanced wood adhesives R&D, regulatory compliance, and mass timber engineering innovation. As a leader in the European Mass Timber Construction ecosystem, Germany’s adhesive manufacturers focus on high-strength epoxy and polyurethane systems tailored for Cross-Laminated Timber (CLT) and Glued Laminated Timber (Glulam) production. Publicly funded R&D programs under the Federal Ministry for Economic Affairs and Climate Action (BMWK) are propelling the development of bio-based lignin, tannin, and carbohydrate-derived adhesives, aligning with EU Green Deal goals and the Circular Economy Action Plan.

German companies such as Henkel and Jowat SE are leading innovators in reactive hot-melt (PUR) and low-emission water-based adhesives for both structural and interior wood applications. In line with REACH and ECHA directives, manufacturers are moving toward non-toxic, recyclable adhesive systems to comply with the latest Annex XVII formaldehyde restrictions. The focus on E0-class emissions, indoor air quality, and digitalized manufacturing is reshaping the adhesives value chain across Germany’s premium furniture, automotive interior, and engineered wood sectors. Continuous investment in high-speed robotic adhesive application technology ensures consistent quality for industrial-scale production, solidifying Germany’s position as Europe’s innovation hub for eco-efficient wood adhesives.

Canada: Harmonized Standards and Mass Timber Expansion Propel Adhesive Growth

Canada’s wood adhesives market is growing rapidly, powered by the mass timber revolution and regulatory harmonization with the United States. The Canadian Formaldehyde Emission Regulations are aligning closely with U.S. TSCA Title VI, streamlining trade and certification for composite wood products. The country’s mass timber infrastructure push, supported by both federal and provincial initiatives, is generating substantial demand for high-strength polyurethane, epoxy, and one-component structural adhesives for CLT, LVL, and Glulam applications.

The Canadian government’s National Building Code amendments allowing taller mass timber buildings are further boosting investment in advanced wood adhesives capable of meeting fire and seismic safety criteria. Key R&D collaborations between FPInnovations, universities, and adhesive producers are focusing on bio-adhesive formulations compatible with native softwood species such as spruce, pine, and fir. Domestic manufacturers are strengthening supply chain resilience through local resin and hardener production facilities, reducing dependence on imported raw materials. Canada’s sustainable forestry practices, coupled with its leadership in carbon-neutral building technologies, continue to drive adoption of eco-certified and high-performance wood bonding agents.

Japan: Precision Manufacturing and Seismic-Resistant Adhesive Technologies

Japan’s wood adhesives industry is distinguished by its emphasis on seismic safety, durability, and craftsmanship precision. Stringent Japanese Agricultural Standards (JAS) regulate the use of Phenol-Resorcinol-Formaldehyde (PRF) and Melamine-Urea-Formaldehyde (MUF) adhesives for high-strength exterior-grade panels and engineered wood applications. Japanese manufacturers such as Aica Kogyo Co., Ltd. are global leaders in moisture-resistant, long-life adhesive systems used in structural Glulam beams and marine plywood.

The country’s R&D ecosystem is actively developing bio-based lignin and tannin adhesives, reflecting Japan’s commitment to reducing dependency on petrochemical feedstocks. Meanwhile, precision woodworking for high-end furniture and architectural interiors relies on Polyvinyl Acetate (PVAc) and Emulsion Polymer Isocyanate (EPI) adhesives for clean finishes and dimensional stability. In the context of automation, major investments are being made in reactive hot-melt systems for high-speed furniture and joinery manufacturing, improving both efficiency and sustainability. Japan’s dual focus on heritage woodworking and modern mass timber engineering ensures its continued leadership in the premium segment of the global wood adhesives market.

India: Domestic Manufacturing and Construction Boom Reshape Market Dynamics

India’s wood adhesives market is undergoing strong transformation, supported by construction growth, housing expansion, and localization of adhesive manufacturing. With rising demand for Plywood, MDF, and Particleboard, India is now one of Asia’s fastest-growing consumers of Urea-Formaldehyde (UF) and Polyvinyl Acetate (PVAc) adhesives. Domestic producers, led by Pidilite Industries Ltd., are investing heavily in manufacturing capacity expansion, focusing on multi-purpose, low-VOC, and heat-resistant adhesives tailored to India’s varied climatic conditions.

The ‘Make in India’ initiative and public housing programs are driving increased production of locally sourced water-based adhesives, gradually replacing solvent-based contact glues in small and mid-sized furniture workshops. Additionally, local R&D is targeting synthetic rubber and bio-based adhesive technologies, aimed at improving sustainability and export competitiveness. As Indian manufacturers begin aligning with global emission and quality standards, demand for formaldehyde-free and eco-certified adhesives is expected to surge. With rapid growth in furniture manufacturing and modular interiors, India’s transition toward environmentally responsible wood adhesives represents one of the most dynamic trends in the Asia-Pacific region.

Wood Adhesives Market Report Scope

Wood Adhesives Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$16.7 Billion

|

|

Market Size (2034)

|

$37.5 Billion

|

|

Market Growth Rate

|

9.4%

|

|

Segments

|

By Resin Type (Urea-Formaldehyde, Melamine-Urea-Formaldehyde, Phenol-Formaldehyde, Isocyanates, Polyvinyl Acetate, EPI, Polyurethane, Soy-Based, Epoxy), By Technology (Water-Based, Solvent-Based, Hot-Melt, Reactive Hot-Melt, Solventless), By Application (Plywood, Particleboard, MDF, OSB, LVL, Glulam, CLT, Finger-Jointed, Laminating), By End-Use Industry (Furniture, Construction, Flooring, Cabinets, DIY

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Henkel AG & Co. KGaA, H.B. Fuller Company, Sika AG, Arkema SA, 3M Company, The Dow Chemical Company, BASF SE, Huntsman Corporation, Franklin Adhesives & Polymers, Aica Kogyo Co., Ltd., Jowat SE, Pidilite Industries Ltd., Wacker Chemie AG, AkzoNobel N.V., Daiken Corporation

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

By Resin Type

- Urea-Formaldehyde

- Melamine-Urea-Formaldehyde

- Phenol-Formaldehyde

- Isocyanates

- Polyvinyl Acetate

- EPI

- Polyurethane

- Soy-Based

- Epoxy

By Technology

- Water-Based

- Solvent-Based

- Hot-Melt

- Reactive Hot-Melt

- Solventless

By Application

- Plywood

- Particleboard

- MDF

- OSB

- LVL

- Glulam

- CLT

- Finger-Jointed

- Laminating

By End-Use Industry

- Furniture

- Construction

- Flooring

- Cabinets

- DIY

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in Wood Adhesives Market-

- Henkel AG & Co. KGaA

- H.B. Fuller Company

- Sika AG

- Arkema SA

- 3M Company

- The Dow Chemical Company

- BASF SE

- Huntsman Corporation

- Franklin Adhesives & Polymers

- Aica Kogyo Co., Ltd.

- Jowat SE

- Pidilite Industries Ltd.

- Wacker Chemie AG

- AkzoNobel N.V.

- Daiken Corporation

*- List not Exhaustive

Research Coverage

Prepared by USDAnalytics, this report investigates the Global Wood Adhesives Market with a boardroom-ready lens on demand drivers, procurement risks, compliance thresholds, and performance benchmarks across furniture/cabinetry, plywood and engineered wood production lines; our analysis reviews manufacturing productivity levers (curing speed, press cycles, line efficiency), tracks regulatory momentum around VOC and REACH, and evaluates durability on diverse substrates and LSE laminates. It highlights breakthroughs in formaldehyde-free and bio-based chemistries (soy/starch/lignin), micro-emission hot-melts for safer operations, and structural PUR solutions for mass-timber applications—pinpointing where margin, reliability, and sustainability converge—making this report an essential resource for specifiers, plant managers, sourcing leaders, and investors seeking defensible growth strategies through 2034, etc……

Scope Highlights

Segmentation:

- By Resin Type: Urea-Formaldehyde; Melamine-Urea-Formaldehyde; Phenol-Formaldehyde; Isocyanates; Polyvinyl Acetate; EPI; Polyurethane; Soy-Based; Epoxy

- By Technology: Water-Based; Solvent-Based; Hot-Melt; Reactive Hot-Melt; Solventless

- By Application: Plywood; Particleboard; MDF; OSB; LVL; Glulam; CLT; Finger-Jointed; Laminating

- By End-Use Industry: Furniture; Construction; Flooring; Cabinets; DIY

- By Region: North America (United States, Canada, Mexico); Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe); Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC); South & Central America (Brazil, Argentina, Rest of SCA); Middle East & Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Geographic Scope: Analysis spans 25+ countries across North America, Europe, Asia Pacific, Latin America, the Middle East & Africa.

Time Horizon: Historic data 2021–2024 and forecast 2025–2034.

Companies (analysis/profiles of 15+): Henkel AG & Co. KGaA; H.B. Fuller Company; Sika AG; Arkema SA; 3M Company; The Dow Chemical Company; BASF SE; Huntsman Corporation; Franklin Adhesives & Polymers; Aica Kogyo Co., Ltd.; Jowat SE; Pidilite Industries Ltd.; Wacker Chemie AG; AkzoNobel N.V.; Daiken Corporation.

Deliverables

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.