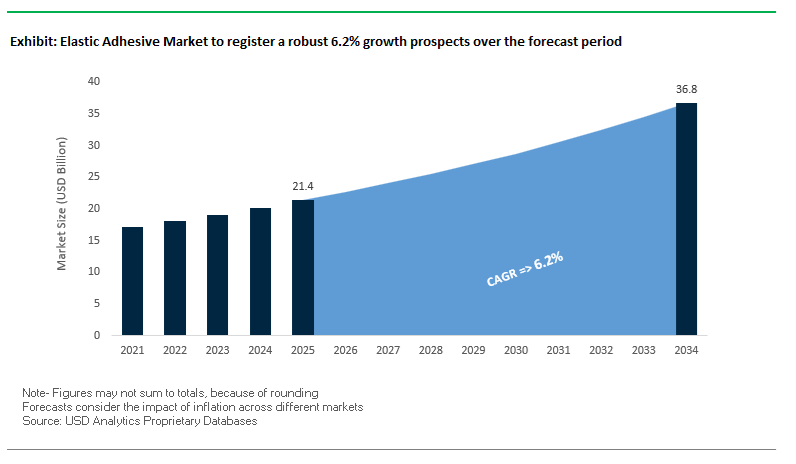

The Global Elastic Adhesive Market is projected to grow from $21.4 billion in 2025 to $36.8 billion by 2034, registering a CAGR of 6.2%. This growth is driven by surging demand from automotive, construction, transportation, and renewable energy sectors, where the need for durable, flexible, and low-emission bonding solutions is intensifying. The market’s technological landscape is evolving rapidly, manufacturers are shifting toward low-monomer polyurethane, silane-modified polymer (SMP), and silicone-based adhesives to meet REACH compliance and sustainability standards.

Elastic adhesives serve as critical enablers in modern lightweight design, noise-vibration-harshness (NVH) management, and modular construction systems. Their ability to absorb mechanical stress while maintaining high adhesion strength makes them indispensable in electric vehicle (EV) assembly, facade sealing, and marine composite bonding. Advanced two-component (2C) polyurethane systems, such as those leveraging Sika’s Powerflex® technology, can achieve tensile strengths exceeding 15 MPa while maintaining elongation above 100%, ensuring long-term stability across temperature ranges from −55°C to +200°C.

The market is also witnessing a sharp regulatory and material transformation. New-generation formulations, such as Sika Purform® and Henkel’s low-monomer polyurethanes, have reduced free diisocyanate content to below 0.1%, eliminating occupational safety training requirements under EU REACH directives. Meanwhile, silicone-based RTV adhesives (e.g., DOWSIL™) continue to dominate in high-temperature, UV-exposed environments due to their unmatched elasticity and aging resistance.

The elastic adhesive industry is undergoing a structural transformation, propelled by sustainability initiatives, raw material innovation, and industry collaborations. Key developments from January to September 2025 highlight a convergence of environmental compliance and advanced chemistry integration across leading global players such as Sika, Henkel, Bostik, Dow, and H.B. Fuller.

In September 2025, H.B. Fuller reinforced its leadership in butyl sealants and elastic tapes, underlining their long-term flexibility and moisture resistance for critical infrastructure and automotive sealing applications. During the same month, the company celebrated its role as the world’s largest pure-play adhesives provider, reaffirming its focus on sustainable, high-durability technologies that support the circular economy. Similarly, in August 2025, Arkema’s Bostik announced executive restructuring to align with its “smart adhesive solutions” strategy, enhancing its presence in mobility and construction sectors through elastic hybrid adhesives and bio-based sealant development.

Sustainability and compliance remain central themes. In July 2025, Henkel launched new recyclable pressure-sensitive adhesives (PSAs) and CO₂-reducing solutions, aligning with the EU Packaging and Packaging Waste Regulation (PPWR). Concurrently, Sika AG announced that all its new Purform® PU products are fully compliant with updated REACH 2025 requirements, ensuring end-user safety without mandatory diisocyanate training.

In May 2025, Dow Chemical highlighted its silicone PSA portfolio—engineered for long-term flexibility and clean removability across temperature extremes, supporting applications in protective films and electronic components. By April 2025, Bostik implemented a global 5–7% price increase, citing inflationary pressures on raw materials and energy, a critical factor influencing cost structures across elastic sealant production lines.

Notably, innovation in water-based systems is gaining traction. Sika’s Co-Elastic Technology (CET), published in January 2025, demonstrated that next-generation waterborne elastic sealants can achieve mechanical performance comparable to solvent-based PU systems, representing a significant milestone in sustainable construction adhesives.

The global architectural sector’s move toward sustainable, large-panel, and lightweight facades is accelerating the adoption of high-performance structural elastic adhesives capable of enduring extreme movement and environmental stress. Traditional mechanical anchors and rigid bonding systems are increasingly being replaced by one-part polyurethane and hybrid polymer sealants that deliver exceptional flexibility, long-term weather resistance, and superior aesthetic continuity in curtain wall and facade assemblies.

Leading adhesive producers have developed ASTM C719-compliant polyurethane sealants with extreme movement capabilities of +100%/-50%, enabling joints to adapt to thermal, mechanical, and wind-induced expansion without cracking or delamination. These properties are critical for Exterior Insulation and Finish Systems (EIFS) and unitized facade designs used in energy-efficient high-rise buildings.

In a landmark academic study on real-weather aging of façade adhesive joints, it was found that bonded joints endured thousands of additional stress cycles compared to conventional testing standards. Unlike mechanical joints that risk catastrophic cladding failure, elastic joints maintained performance stability, validating their superiority in modern structural design. Complementary to the, a major industry provider’s polyurethane-based structural adhesive demonstrated 80% elastic recovery after 28 days of curing, even under 100% elongation for 24 hours, confirming long-term durability and consistent facade alignment under cyclic thermal loads.

The electric vehicle (EV) revolution is fundamentally transforming the adhesives landscape, pushing the boundaries of performance through thermally conductive yet flexible adhesive systems. As EV manufacturers move toward high-energy-density, compact battery designs, maintaining mechanical stability while optimizing heat dissipation has become critical. The is driving R&D in 2K polyurethane-based thermally conductive adhesives (TCA) and silicone-based hybrid materials that combine mechanical damping with superior thermal management.

Advanced TCA formulations deliver thermal conductivities up to 1.5 W/m·K or higher, with elongation capacities sufficient to absorb expansion and contraction cycles within densely packed lithium-ion cells. These adhesives are pivotal for bonding, potting, and sealing within the Cell-to-Pack (CTP) and Cell-to-Chassis (CTC) architectures—both of which eliminate intermediate modules to improve power density and reduce assembly costs.

Epoxy-based adhesives remain dominant in structural load-bearing battery applications due to their compressive and shear strength, while silicone-based TCAs are preferred for their ability to withstand continuous temperatures up to 200°C, ensuring insulation and elasticity under high charging currents. As thermal runaway prevention becomes a major OEM priority, elastic adhesives are evolving from auxiliary materials into core components of EV battery pack integrity and safety systems.

The rise of Mass Timber Construction (MTC), particularly Cross-Laminated Timber (CLT) and Glued-Laminated Timber (Glulam), is creating a robust growth frontier for elastic wood adhesives. These advanced materials are uniquely suited to address moisture-induced dimensional changes in timber structures while preserving mechanical stability and architectural aesthetics.

Research on mass timber moisture dynamics highlights that timber moisture content can rise from 12–14% (fabrication) to 20% or higher during construction exposure, occasionally surpassing 30% in wetting conditions. Such fluctuations result in swelling, shrinkage, and internal tension, which can cause surface cracking and detachment if rigid adhesives are used. To mitigate the, high-elongation elastic sealants are increasingly specified to accommodate hygroscopic movement without compromising joint integrity or airtightness.

Industry studies confirm that cracks and surface checks often emerge when tensile stresses from moisture gradients exceed the strength of rigid bonding systems. In contrast, moisture-tolerant polyurethane and silane-modified polymer adhesives demonstrate superior resistance, maintaining elasticity over extended climatic cycles. With the mass timber market projected to grow rapidly across North America and Europe, high-durability elastic adhesives will become integral to sustainable hybrid construction and carbon-reduction building initiatives.

The emergence of Flexible Hybrid Electronics (FHE) and wearable technology represents one of the most promising new avenues for elastic adhesives—especially in medical diagnostics, consumer wearables, and industrial IoT devices. The ongoing miniaturization of electronic systems demands ultra-flexible conductive adhesives that maintain electrical integrity under repetitive mechanical deformation such as bending, folding, and stretching.

Government-led initiatives, including NextFlex (U.S.) and SmartEEs (EU), are directing millions in funding toward accelerating the domestic FHE ecosystem. These programs are fostering innovation in stretchable conductive adhesives, polymer-based conductive inks, and hybrid bonding materials designed for automated roll-to-roll and additive manufacturing processes.

Silver-based conductive formulations and elastomeric polymer matrices are key technologies enabling flexible circuit design. Research on printed conductive inks confirms that silver-based networks maintain conductivity stability even after 10,000 bending cycles, positioning them as the foundation for elastic conductive adhesives used in wearable biosensors, smart patches, and foldable displays.

As demand for skin-contact-safe, biocompatible, and highly elastic adhesives rises, manufacturers are also exploring silicone and polyurethane hybrid systems that offer both mechanical compliance and biocompatibility. The convergence of electronics and elastomer chemistry is expected to catalyze significant advancements in stretchable, fatigue-resistant adhesives tailored for next-generation wearable ecosystems.

Elastic Adhesive Market Share Insights, 2025-2034

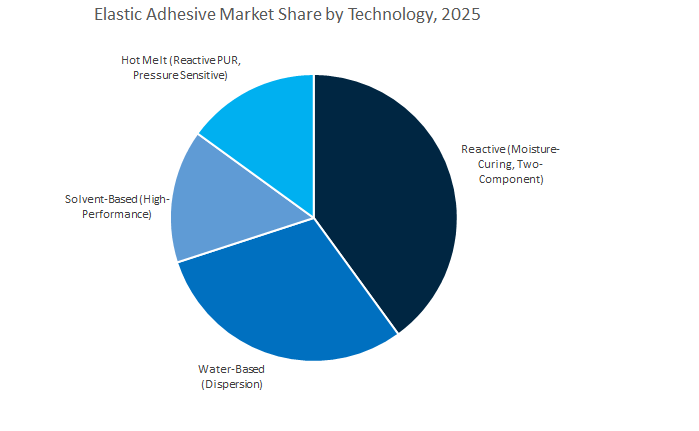

Reactive systems—comprising moisture-curing polyurethanes (PU), silane-modified polymers (SMP), and two-component systems—represent the largest share of the global elastic adhesive industry, accounting for approximately 40.6% of the market in 2025. These systems dominate due to their ability to form high-strength, flexible, and weather-resistant bonds that maintain elasticity even under thermal expansion, vibration, or mechanical stress. Reactive adhesives are indispensable in construction and transportation, particularly for structural glazing, façade bonding, and sealing expansion joints, where long-term adhesion and UV resistance are critical. In the automotive sector, they enable lightweighting by replacing mechanical fasteners and welding in body panel assembly and window bonding applications. The strong growth of hybrid polymer systems, such as SMPs (Silane-Modified Polymers), has further boosted the reactive segment’s dominance, offering the combined benefits of polyurethane toughness and silicone flexibility without isocyanates. Their superior weatherability, chemical resistance, and long service life continue to make reactive elastic adhesives the preferred choice across industrial and commercial environments requiring structural integrity and environmental resilience.

Water-based elastic adhesives are the second-largest segment and continue to expand due to increasing regulatory pressures and the global shift toward low-VOC and sustainable bonding solutions. These formulations are particularly favored in interior construction, furniture assembly, flooring installation, and automotive interiors, where strong yet non-toxic adhesives are required. Their high safety profile, ease of application, and odor-free nature make them ideal for confined spaces and consumer applications. In addition, the ability to adjust viscosity and working time gives manufacturers greater control during application in DIY and renovation markets. Water-based dispersions, primarily based on acrylic, EVA, and modified polyurethane chemistries, are increasingly being optimized for higher strength and faster drying, bridging the performance gap with solvent-based systems. As sustainability standards tighten in North America and Europe, and major construction contractors adopt green certification programs (LEED, BREEAM), the adoption of water-based elastic adhesives is expected to accelerate, solidifying their position as a major growth driver in environmentally responsible applications.

The building and construction sector is the cornerstone of the global elastic adhesive market, representing approximately 47.2% of total demand in 2025. Elastic adhesives are essential for this sector due to their ability to absorb joint movement, seal against weather ingress, and provide durable bonding under structural stress. They are extensively used in expansion joint sealing, façade bonding, flooring installation, and waterproofing, where flexibility, adhesion, and environmental resistance are vital. Modern architectural trends—such as modular construction, curtain wall façades, and energy-efficient building envelopes—are further driving adoption, as these techniques rely heavily on high-performance elastic bonding solutions instead of mechanical fasteners. Additionally, government initiatives promoting green buildings and sustainable infrastructure are pushing demand for low-VOC, isocyanate-free hybrid adhesives. In emerging economies, rapid urbanization and residential construction are expanding market volumes, while in developed regions, renovation and refurbishment projects sustain steady consumption of professional-grade and DIY sealants. This sector remains the dominant force shaping material innovation and formulation trends across the elastic adhesives landscape.

The automotive and transportation industry is the second-largest consumer segment, leveraging elastic adhesives for vehicle assembly, bonding, and sealing applications that demand long-term durability and vibration damping. These adhesives are crucial for bonding body panels, roof modules, glass assemblies, and interior trims, where their elastic nature allows for expansion, contraction, and dynamic load resistance. Their role has become even more pivotal with the rise of electric vehicles (EVs), where they are used to secure battery enclosures, thermal management systems, and sensor housings. Elastic adhesives help reduce vehicle weight by eliminating mechanical fasteners while improving noise, vibration, and harshness (NVH) characteristics—critical for passenger comfort and electric drivability. In rail, marine, and aerospace transportation, they are increasingly adopted for structural sealing and vibration absorption, contributing to improved fatigue life and performance efficiency. As global automakers prioritize sustainability, crash safety, and fuel efficiency, elastic adhesives are evolving to deliver multi-material compatibility and long-term environmental resistance, cementing their role in the mobility revolution.

The global elastic adhesive market is dominated by five leading players — Sika AG, Henkel AG, Bostik (Arkema), The Dow Chemical Company, and H.B. Fuller — each leveraging distinctive chemistries, global manufacturing reach, and sustainability frameworks. Their competitive edge is built on continuous innovation, low-emission product portfolios, and application-specific integration across construction, automotive, and industrial segments.

Sika AG leads the global elastic adhesives landscape with its Sikaflex®, SikaForce®, and Purform® technologies. Its one-component (1C) polyurethane sealants dominate the construction and automotive glazing markets, offering exceptional elasticity and adhesion. The Purform® prepolymer platform revolutionizes polyurethane adhesives by lowering free monomer diisocyanate content below 0.1%, making them REACH-compliant without added safety protocols. Sika’s Powerflex® technology combines high tensile strength with superior elongation, ideal for EV lightweight assemblies and composite structures. The company continues to expand globally through R&D hubs dedicated to hybrid PU–SMP systems that balance structural strength with long-term flexibility.

Henkel stands as the largest adhesive producer worldwide, with a robust portfolio of polyurethane, silicone, and acrylic elastic adhesives optimized for automotive, electronics, and packaging sectors. Through its Inspiration Center Düsseldorf (ICD), Henkel drives innovation in electrification, developing elastic solutions for EV battery bonding, structural sealing, and NVH management. Its Loctite® and Teroson® lines deliver durable bonding performance across varying cure systems—from instant adhesives to heat-curable formulations. The company is a front-runner in sustainable adhesive technologies, launching recyclable PSA systems that support the circular economy and CO₂ reduction mandates.

Bostik, the adhesive division of Arkema, focuses on smart, flexible adhesive systems aligned with the parent company’s sustainability goals. Its elastic adhesives serve critical roles in aerospace, automotive, and construction markets, combining elasticity, durability, and thermal stability. The company’s Wall & Floor system portfolio supports energy-efficient building practices, while its smart adhesives for lithium-ion battery assembly enhance thermal and vibration management in EVs. With Arkema’s specialty polymer expertise, Bostik delivers bio-based and solvent-free hybrid adhesives tailored for next-generation transportation and green buildings.

Dow’s DOWSIL™ brand defines industry benchmarks in silicone elastic adhesives and sealants, offering superior thermal stability, UV resistance, and chemical durability. Its RTV silicone technologies ensure elasticity from −56°C to +260°C, making them ideal for aerospace, electronics, and power module encapsulation. The company’s silicone PSAs cater to protective films and specialty tapes, enabling adhesion to low-energy substrates with clean removability. Dow’s current R&D initiatives focus on developing neutral-cure alkoxy systems that offer faster curing, low VOC content, and enhanced bonding strength, meeting global environmental and workplace safety standards.

H.B. Fuller leads as the world’s largest pure-play adhesives company, offering a comprehensive range of elastic polyurethane, butyl, and modified silane-based solutions for construction, automotive, and renewable energy applications. Its focus on durable assembly and multi-material bonding supports sectors demanding shock, vibration, and temperature tolerance. The company is expanding regionally through local manufacturing facilities, particularly in North America, to strengthen supply reliability. Fuller’s R&D efforts emphasize sustainability and circular design, promoting low-VOC, solvent-free elastic systems tailored for both industrial and consumer markets.

Germany continues to dominate the European elastic adhesive market, leveraging its world-class automotive engineering, industrial R&D, and sustainability initiatives. A leading German adhesive manufacturer has committed over €200 million toward developing low-VOC polyurethane (PU) and silyl-modified polymer (SMP) sealant systems, reinforcing its focus on eco-compliant elastic adhesives for electric vehicles (EVs) and modern construction. The investments align with Germany’s sustainability agenda and the EU Green Deal, which mandate the reduction of volatile organic compounds (VOCs) and promote circular economy materials.

The German automotive sector is increasingly relying on elastic structural adhesives to enhance NVH (Noise, Vibration, and Harshness) performance and improve Body-in-White (BIW) assembly efficiency. Companies like BMW and Volkswagen are integrating high-durability SMP adhesives for lightweight bonding between aluminum, CFRP (Carbon Fiber Reinforced Plastics), and steel, ensuring optimal strength and long-term fatigue resistance. In addition, digital lab technologies, such as the AI-driven formulation systems at Altana’s BYK division, are accelerating the creation of next-generation high-speed curing adhesives for precision industrial applications.

The United States elastic adhesive industry remains a global innovation hub, driven by its leadership in aerospace, electronics, and infrastructure modernization. American adhesive giants such as 3M and H.B. Fuller are pioneering reactive hot melt technologies and hybrid elastic formulations designed for applications that demand extreme durability, temperature resistance, and rapid curing. In 2024, 3M launched a new moisture-curing reactive hot melt adhesive, specifically tailored for wearable electronics, structural assembly, and high-end automotive components, delivering exceptional moisture resistance and long-term flexibility.

Federal regulations and EPA VOC emission limits are catalyzing the transition to solvent-free, waterborne, and SMP-based adhesives in the U.S. construction market. The Infrastructure Investment and Jobs Act (IIJA) is another major growth driver, spurring demand for weather-resistant polyurethane joint sealants and silicone-based elastic adhesives for bridges, tunnels, and transportation networks. Moreover, ongoing aerospace R&D projects are promoting the use of high-modulus elastic adhesives that can endure fluctuating thermal loads and mechanical stresses during high-altitude operations.

China’s elastic adhesives and sealants market is expanding at an accelerated pace due to the convergence of urbanization, EV manufacturing, and construction megaprojects. The country accounted for one of the largest shares of global demand in 2024, with strong momentum continuing into 2025. A major acquisition by a Swiss chemical giant—such as Sika’s acquisition of Shenzhen Landun Holding—has strengthened foreign participation in the domestic waterproofing and elastic bonding market, enabling broader access to China’s infrastructure boom.

The electric vehicle sector is a major catalyst, consuming large volumes of fast-curing, thermally resilient polyurethane and silicone-based elastic adhesives for battery module encapsulation, body panel bonding, and noise reduction applications. Simultaneously, China’s smart city and high-rise development projects are driving high demand for silicone-based façade sealants and hybrid SMP systems, essential for flexible structural glazing. Furthermore, China’s Five-Year Industrial Plan supports R&D in bio-based polymers and low-VOC formulations, positioning the nation as a dominant producer of eco-compliant elastic adhesives for both domestic use and export.

Japan continues to lead the Asia-Pacific elastic adhesives market through a relentless focus on precision engineering, advanced curing technologies, and materials innovation. Major Japanese manufacturers such as ThreeBond Co. Ltd. and Kuraray are developing rapid-curing elastic adhesive systems, exemplified by ThreeBond’s 3921/3926 product line, which reduces assembly time across applications in railway, automotive, and consumer electronics. The adhesives deliver superior flexibility, impact resistance, and substrate compatibility for high-speed industrial processes.

Japan’s materials science sector is also focusing on enhancing adhesion to lightweight substrates like carbon fiber, composites, and engineering plastics, ensuring structural integrity in aerospace and EV applications. The adoption of robotic adhesive dispensing in industrial manufacturing has increased, driving demand for low-viscosity elastic adhesives optimized for automated precision bonding. Furthermore, Japanese R&D continues to refine low-outgassing elastic sealants suitable for semiconductor assembly, solidifying Japan’s reputation for reliability in high-precision elastic bonding technologies.

Switzerland remains a pioneer in global elastic adhesive innovation, particularly through the technological leadership of Sika AG, a market-defining brand in structural elastic sealants and adhesives. Its proprietary Purform® technology represents a major advancement in low-monomer polyurethane prepolymers, delivering superior elasticity, chemical resistance, and environmental compliance. The technology has been integrated into Sika’s Sikaflex® product line, aligning with strict EU REACH safety regulations and setting new benchmarks for eco-friendly, high-performance bonding.

Strategic acquisitions in high-performance flooring and roofing materials have bolstered Switzerland’s footprint in construction and industrial markets, enabling the country to export specialized elastic polymer adhesives worldwide. With a focus on precision-engineered polyurethane chemistries and AI-assisted formulation, Swiss adhesive technology continues to lead the transition toward carbon-neutral and circular manufacturing in elastic bonding applications.

India’s elastic adhesive market is experiencing strong momentum due to extensive infrastructure investment and the “Make in India” initiative, which promotes local manufacturing of sealants and adhesives. Domestic producers such as Pidilite Industries are expanding production capacity for solvent-free and water-based elastic sealants, capitalizing on rising construction activity in residential, commercial, and industrial infrastructure. The adoption of hybrid polymer and silicone-based adhesives is growing rapidly, particularly for roofing, panel bonding, and waterproofing applications.

In addition, India’s e-commerce and fast-moving consumer goods (FMCG) sectors are driving new demand for pressure-sensitive elastic adhesives (PSAs) used in packaging and labeling applications. The trend toward flexible, high-tack adhesive films reflects the shift to automation in packaging operations and sustainable manufacturing. Combined with the expanding EV assembly ecosystem, India is emerging as a competitive hub for both construction-grade and industrial elastic adhesives tailored to domestic and export markets.

Elastic Adhesive Market Report Scope

Elastic Adhesive Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$21.4 Billion

|

|

Market Size (2034)

|

$36.8 Billion

|

|

Market Growth Rate

|

6.2%

|

|

Segments

|

By Resin Type (Polyurethane, Silyl-Modified Polymer, Silicone, Others), By Technology (Water-Based, Solvent-Based, Reactive, Hot Melt), By End-Use Industry (Automotive & Transportation, Building & Construction, Industrial Assembly, DIY/Consumer, Others

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Henkel AG & Co. KGaA, 3M Company, Sika AG, Arkema Group, H.B. Fuller Company, Wacker Chemie AG, Dow Inc., RPM International Inc., Huntsman Corporation, BASF SE, Nippon Paint Holdings Co., Ltd., Pidilite Industries Ltd., ThreeBond Holdings Co., Ltd., Illinois Tool Works Inc., Jowat SE

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

By Resin Type

- Polyurethane

- Silyl-Modified Polymer

- Silicone

- Others

By Technology / Chemistry

- Water-Based

- Solvent-Based

- Reactive

- Hot Melt

By End-Use Industry

- Automotive & Transportation

- Building & Construction

- Industrial Assembly

- DIY/Consumer

- Others

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

- Henkel AG & Co. KGaA

- 3M Company

- Sika AG

- Arkema Group

- H.B. Fuller Company

- Wacker Chemie AG

- Dow Inc.

- RPM International Inc.

- Huntsman Corporation

- BASF SE

- Nippon Paint Holdings Co., Ltd.

- Pidilite Industries Ltd.

- ThreeBond Holdings Co., Ltd.

- Illinois Tool Works Inc.

- Jowat SE

*- List not Exhaustive

Research Coverage

Prepared by USDAnalytics, this report investigates the Global Elastic Adhesive Market, delivering analysis reviews that benchmark performance, compliance, and cost-of-ownership across mission-critical use cases in mobility, construction, industrial assembly, renewables, and electronics. It highlights breakthroughs in ultra-low-monomer PU platforms, silane-modified polymer hybrids, high-temperature silicones, and water-based next-gen systems that balance tensile strength with elongation, fatigue resistance, and NVH damping. The study maps demand drivers from lightweighting and modular building to EV battery pack design and façade movement accommodation, quantifies specification shifts from solvented to low-VOC chemistries, and evaluates supply resilience, pricing, and formulation risks across major producers and converters. With clear side-by-side technology scoring, cure-profile comparators, and installation productivity lenses, this report is an essential resource for sourcing leaders, R&D chemists, application engineers, and strategy teams who need defensible guidance for material selection, supplier shortlisting, and investment planning.

Scope Highlights

Segmentation:

- By Resin Type: Polyurethane; Silyl-Modified Polymer; Silicone; Others.

- By Technology / Chemistry: Water-Based; Solvent-Based; Reactive; Hot Melt.

- By End-Use Industry: Automotive & Transportation; Building & Construction; Industrial Assembly; DIY/Consumer; Others.

Geographic Scope: Analysis spans 25+ countries across North America, Europe, Asia Pacific, Latin America, the Middle East & Africa.

Time Frame: Historic data 2021–2024 and forecasts 2025–2034.

Companies: 15+ company analyses/profiles covering portfolios, innovations, capex, M&A, sustainability roadmaps, and channel strategies.

Deliverables

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.