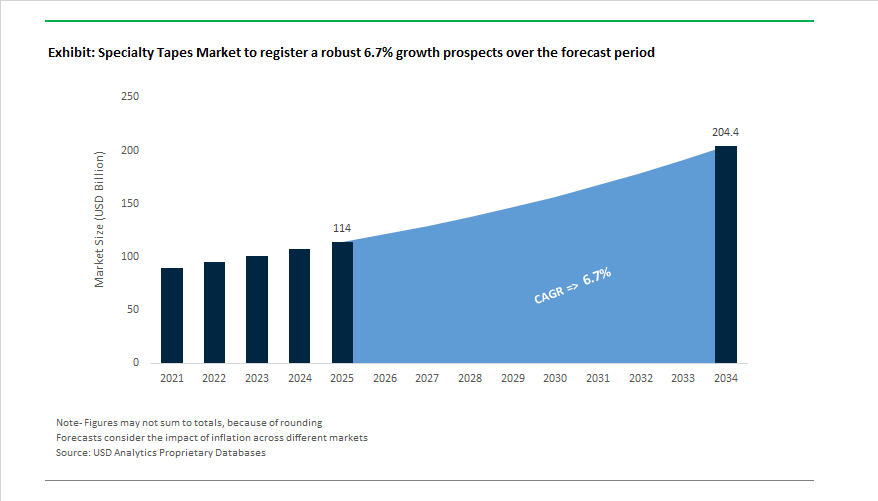

The Global Specialty Tapes Market is projected to expand from USD 114 billion in 2025 to USD 204.4 billion by 2034, registering a CAGR of 6.7%, reflecting a fundamental shift in how tapes are positioned within industrial value chains. Specialty tapes are increasingly engineered, qualified, and specified as functional material platforms that integrate bonding, insulation, protection, damping, and surface management into a single solution. This evolution has elevated tapes into a strategic materials category alongside adhesives, films, and coatings.

At the manufacturer level, the market is structurally shaped by technology-led portfolios rather than volume commoditization. Global leaders such as 3M, tesa SE, Nitto Denko, Avery Dennison, Saint-Gobain, and Lohmann anchor their tape businesses around proprietary adhesive chemistries, precision coating capabilities, and backing material science. Differentiation increasingly lies in the ability to control adhesive rheology, coat-weight uniformity, carrier performance, and long-term aging behavior, rather than simply offering adhesion strength. As a result, specialty tape suppliers operate closer to OEM engineering teams, with qualification cycles resembling those of structural adhesives rather than traditional tape products.

A defining structural driver of the market is the replacement of multi-component assemblies with single-tape solutions. Specialty tapes are being designed to eliminate fasteners, liquid adhesives, primers, and curing steps, reducing takt time and process variability in automated manufacturing. Acrylic foam tapes, high-temperature polyimide tapes, electrically insulating polyester tapes, and thermally conductive tape systems illustrate how tapes now deliver load distribution, thermal control, electrical isolation, and vibration damping simultaneously. This functional consolidation has materially expanded the addressable value per unit, supporting market growth even where underlying manufacturing volumes are maturing.

From a materials perspective, the industry is moving decisively toward sustainability-aligned tape architectures. Manufacturers are introducing bio-based backings, solvent-free and water-based adhesive systems, repulpable paper tapes, and mass-balance-certified polymers, responding to brand-owner ESG commitments and packaging recyclability standards. Importantly, these changes are being engineered without sacrificing performance consistency—critical in applications where tapes remain in service for years under thermal cycling, UV exposure, or mechanical stress. This balance between sustainability and durability represents a key competitive axis across leading suppliers.

The Specialty Tapes Industry continues to advance rapidly through technological innovation, ESG investments, and targeted acquisitions, with companies focusing on renewable energy, medical wearables, and electronics miniaturization as key growth pillars.

In April 2025, Avery Dennison Performance Tapes launched its Solar Panel Bonding Portfolio, introducing pressure-sensitive adhesive (PSA) tapes designed for UV stability, durability, and automation compatibility in solar module and junction box assembly. This move aligns with the surging demand for adhesive-based alternatives to mechanical fasteners in renewable energy manufacturing.

Also in April 2025, Tesa SE announced major progress toward its Scope 1 and 2 climate-neutral production targets, confirming that 90% of its electricity comes from renewable sources. The company reaffirmed its €300 million sustainability investment plan through 2030, signaling a strong corporate pivot toward carbon-neutral specialty adhesive production.

March 2025 marked a pivotal moment for 3M, which strengthened its advanced materials portfolio by expanding R&D on Boron Nitride-based thermal management fillers and Optically Clear Adhesives (OCAs) for high-resolution flexible displays and semiconductors. These materials are fundamental for next-generation electronics and display technologies, where thermal efficiency and optical precision determine product success.

In October 2024, Tesa SE also rolled out 13 new tape solutions for professional applications—many featuring 60%+ recycled content—demonstrating leadership in eco-friendly construction and industrial masking. Meanwhile, the September 2024 acquisition of Carrier’s Global Access Solutions by Honeywell for $4.95 billion highlighted industrial integration trends where smart building technologies increasingly rely on specialty tapes for sealing, vibration damping, and insulation.

3M India’s strategic merger (August 2024) with its electronics communication division underscored operational streamlining to support 5G network infrastructure, data centers, and electronic component manufacturing. Similarly, Nitto Denko’s R&D advancements (July 2024) in Fiber PSA technology have positioned it as a frontrunner in lightweight bonding solutions for structural applications and medical wearables.

By June 2024, escalating demand for biocompatible medical-grade specialty tapes spurred a $50 million North American manufacturing expansion, supporting the fast-growing wearable device and wound care sectors. This expansion highlights the growing intersection between adhesive engineering and biomedical innovation.

Market Trend 1: Rapid Integration of Functional Tapes for Electric Vehicle Battery Pack Assembly and Thermal Management

The electrification wave is redefining industrial adhesive design, and specialty functional tapes are at the core of the transformation. As EV batteries become denser, hotter, and more complex, the need for multi-functional adhesive tapes that combine thermal management, electrical insulation, and flame retardancy is escalating across the EV supply chain.

Leading manufacturers such as Lohmann have engineered double-sided thermally conductive tapes that operate effectively in the 20°C–35°C range, the optimal temperature for lithium-ion cell longevity. These tapes exhibit thermal conductivities of up to 2 W/mK (ASTM D5470), enabling uniform heat dissipation and maintaining ideal cell operating temperatures. The capability directly enhances battery performance, range, and service life—key parameters in EV design competitiveness.

Safety remains a paramount concern in EV development, and H.B. Fuller’s flame-retardant foam tapes, which meet UL 94 V-0 standards, exemplify industry leadership in thermal runaway mitigation. These flame-retardant adhesive systems prevent fire propagation within cylindrical and prismatic cell architectures, ensuring compliance with increasingly stringent battery safety regulations across major automotive markets.

In parallel, global players like Avery Dennison and Saint-Gobain are pioneering pressure-sensitive adhesive (PSA) tapes tailored for automated EV assembly. These tapes reduce manufacturing complexity, replacing mechanical fasteners with instant-bonding, lightweight alternatives. By minimizing adhesive curing times and optimizing process flow, PSA-based functional tapes are enabling faster cycle times, lighter assemblies, and lower production costs, aligning perfectly with the automation strategies of modern gigafactories.

Market Trend 2: Adoption of Sustainable and Circular Material Formulations Driven by Brand Owner Mandates

Sustainability imperatives are transforming the specialty tapes industry from petroleum-derived products to circular, bio-based, and solvent-free adhesive technologies. Global brand owners in consumer goods, logistics, and packaging are increasingly imposing strict sustainability criteria on suppliers, compelling the industry to redesign materials from the molecular level up.

tesa SE, a leader in industrial tapes, recently commercialized a bio-based paper packaging tape certified by DIN CERTCO for 92% bio-based carbon content—a milestone achievement in sustainable adhesive manufacturing. The product also scored 78/100 on the INGEDE recyclability scale, proving full compatibility with standard paper recycling streams. The innovation highlights the emergence of bio-based carton sealing tapes as high-performance, circular alternatives to traditional polymer-backed tapes.

Simultaneously, the incorporation of Post-Consumer Recycled (PCR) PET backings is becoming an industry standard. Specialty tape products feature up to 90% PCR PET content, a major advance in reducing reliance on virgin plastics. These tapes are engineered to maintain adhesion on challenging substrates like recycled cardboard, showcasing the technical maturity of circular adhesive systems. The production of such materials through solvent-free, energy-efficient processes aligns with global net-zero objectives and strengthens manufacturers’ ESG credentials.

Market Opportunity 1: Development of Advanced EMI Shielding Tapes for Proliferating 5G and mmWave Electronics

The explosive growth of 5G and millimeter-wave (mmWave) technologies has created an urgent need for lightweight, flexible EMI shielding tapes capable of maintaining electromagnetic compatibility in increasingly compact device architectures. These specialty tapes, designed for high-frequency electronics, serve a dual role—providing both mechanical adhesion and superior shielding performance.

Research in the field confirms that effective EMI shielding materials must combine high electrical conductivity with optimal magnetic permeability to block or absorb high-frequency interference. Copper foil-based conductive tapes, tested for shielding effectiveness (SE) values exceeding 60–80 dB, demonstrate outstanding performance in reducing signal loss and crosstalk in 5G communication modules.

In parallel, material science innovations are unlocking even greater potential. Next-generation graphene and carbon nanotube (CNT)-based composite tapes offer superior conductivity, durability, and flexibility, achieving ultra-thin, lightweight designs ideal for IoT devices, wearable electronics, and autonomous vehicle systems. The marriage of nanotechnology and adhesive engineering is thus establishing a new frontier for advanced EMI shielding tapes that combine mechanical integrity, corrosion resistance, and long-term signal reliability in extreme conditions.

Market Opportunity 2: Engineering of Smart Tapes with Integrated Sensing and Diagnostic Capabilities

The convergence of Internet of Things (IoT) technology and smart materials engineering is transforming traditional tapes into intelligent sensing platforms. These smart specialty tapes integrate embedded sensors capable of measuring strain, displacement, or temperature, unlocking new opportunities in aerospace, infrastructure, and industrial maintenance applications.

Research in Structural Health Monitoring (SHM) demonstrates that embedding passive wireless sensors—such as LC circuits or RFID modules—within adhesive matrices allows real-time monitoring of mechanical strain in bridges, pipelines, and aircraft fuselage panels. The innovation eliminates the need for complex sensor wiring or manual inspection, drastically reducing infrastructure maintenance costs.

In addition, adhesive-backed smart tapes can be programmed to memorize and record maximum strain thresholds, acting as diagnostic indicators for critical systems under load. These materials enable a shift from schedule-based to condition-based maintenance, enhancing safety and operational efficiency in high-value assets.

With increasing R&D collaboration between material scientists and IoT engineers, smart tapes are poised to revolutionize predictive maintenance, aerospace safety monitoring, and civil engineering diagnostics, marking a new era where adhesives function as data-generating components rather than passive bonding agents.

Specialty Tapes Market Share Insights, 2025-2034

Market Share by Product Type

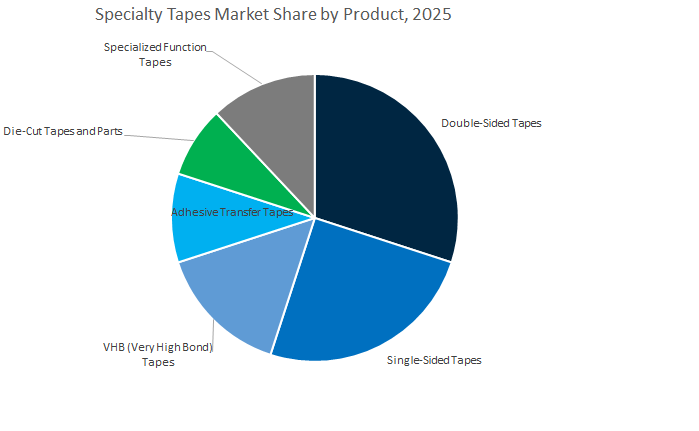

Double-sided tapes dominate the global specialty tapes industry, accounting for an estimated 31.8% market share by 2025, driven by their broad adoption across automotive, electronics, industrial assembly, and construction applications. These tapes provide superior bonding strength, clean aesthetics, and design flexibility, enabling manufacturers to replace traditional fastening methods such as rivets, screws, and welds. In the automotive sector, double-sided tapes are integral for badge mounting, trim attachment, and component bonding—supporting the ongoing trend toward vehicle lightweighting and improved fuel efficiency. The electronics industry heavily relies on these tapes for display module assembly, heat dissipation, and camera module alignment, particularly in smartphones and wearables. Their ability to bond dissimilar materials—including metals, plastics, glass, and composites—while resisting vibration, temperature fluctuations, and moisture ensures their dominance across multiple high-performance applications.

VHB (Very High Bond) tapes represent one of the fastest-growing and most valuable segments, offering structural-level adhesion for applications demanding exceptional durability and long-term reliability. They are widely used in automotive exteriors, building facades, and solar panel assembly, where they withstand thermal expansion and environmental stress. Meanwhile, adhesive transfer tapes serve critical roles in precision lamination and assembly processes in electronics, optics, and labeling. Die-cut tapes and parts continue to gain relevance in semiconductor packaging, medical devices, and microelectronics, where precision and material efficiency are paramount. Furthermore, specialized function tapes, including thermal, conductive, flame-retardant, and EMI shielding variants, are expanding rapidly due to technological advancements in EVs, 5G communication systems, and renewable energy equipment.

Market Share by End-Use Industry

Electrical & electronics remain the leading end-use industry, commanding around 28.4% of the global specialty tapes market by 2025, as manufacturers increasingly depend on high-precision adhesive tape solutions for device assembly, component protection, and heat management. Specialty tapes are indispensable in semiconductor packaging, display bonding, flexible circuits, and EMI shielding, particularly as miniaturization trends intensify with 5G-enabled and IoT devices. Adhesive tapes enable lightweight, residue-free, and cleanroom-compatible bonding, making them essential in advanced electronic production environments. Additionally, battery assembly and insulation tapes play critical roles in the fast-growing electric vehicle (EV) market, supporting safety and efficiency in high-voltage systems.

The automotive industry is another dominant and rapidly expanding segment, leveraging specialty tapes for lightweight assembly, noise reduction (NVH management), thermal protection, and decorative applications. As EV manufacturing expands, the use of high-temperature-resistant and flame-retardant tapes for battery pack insulation and wiring harness protection continues to rise sharply. In the healthcare and hygiene sector, specialty tapes are increasingly used for wearable sensors, surgical drapes, wound dressings, and transdermal patches, driven by growth in biocompatible, breathable, and skin-friendly materials. The building and construction sector maintains a strong position with demand for sealing, mounting, insulation, and waterproofing tapes in facades, flooring, and HVAC systems, emphasizing energy-efficient and low-VOC formulations.

Industrial and white goods applications rely on specialty tapes for equipment assembly, vibration damping, and surface protection, especially in consumer appliances and renewable energy equipment. The aerospace and defense segment, while smaller in volume, contributes significant value through the use of high-temperature, chemical-resistant, and flame-retardant tapes for composite bonding, insulation, and shielding applications. Meanwhile, retail, graphics, and printing industries continue to use pressure-sensitive and removable tapes for advertising, packaging, and point-of-sale displays.

The Global Specialty Tapes Market is characterized by a strong interplay of materials science innovation, sustainability leadership, and application-specific engineering. Market frontrunners—3M, tesa SE, Nitto Denko, Avery Dennison, and Lintec Corporation—are leveraging proprietary technologies, global footprints, and high-R&D intensity to dominate high-growth segments such as automotive e-mobility, flexible electronics, renewable energy, and healthcare applications.

3M Company leverages its 51 core technology platforms—including Adhesives, Materials Science, and Advanced Materials—to maintain global leadership in industrial and electronics bonding. Its VHB (Very High Bond) tapes replace mechanical fasteners, offering design flexibility for automotive and building facades. The company’s strategic investment in EV thermal management and EMI shielding tapes reinforces its foothold in e-mobility and digital infrastructure. Following its 2024 spin-off of Solventum, 3M is doubling down on its Industrial & Transportation segment, allocating R&D capital to structural bonding, high-temp insulation, and miniaturized electronics tapes.

Tesa SE stands at the forefront of sustainable adhesive innovation, committing €300 million toward climate-neutral production by 2030 and achieving a 39% CO₂ reduction in Scopes 1 & 2. Its Debonding on Demand technology enables reversible adhesion, facilitating component recycling and repairability in automotive and electronics sectors—a critical enabler of the circular economy. Tesa is also a global leader in wire harness bundling tapes offering abrasion protection, flame retardancy, and NVH dampening, widely specified by top automotive OEMs. Operating across five global plants, Tesa’s localization strategy enhances responsiveness in APAC and NAFTA industrial markets.

Nitto Denko is globally recognized for its specialty tapes and Optronics films, contributing significantly to the LCD/OLED display and semiconductor markets. Its Fiber PSA innovation improves lightweight adhesion and flexibility for structural and wearable applications. In its Human Life segment, Nitto leads in transdermal drug delivery patches and skin-friendly tapes, combining biocompatibility and advanced adhesion control. Its Open Technology platform accelerates joint R&D in heat-dissipating and conductive adhesive systems, underpinning Nitto’s position in high-reliability electronics and medical materials.

Avery Dennison’s Performance Tapes Division continues to grow its global leadership through sustainable and renewable-focused adhesive materials. The 2025 launch of its Solar Panel Bonding Portfolio marks a major advancement in UV-resistant, durable PSA tapes tailored for solar module assembly. The company aims for 70% of its revenues from sustainability-driven products by 2025, emphasizing recycled content and circularity. Avery’s converter partnerships enable customization of pressure-sensitive tapes for complex geometries in automotive, electronics, and building applications, ensuring agility in customer-specific design integration.

Lintec Corporation leads in semiconductor dicing and back-grinding tapes, supporting wafer thinning for SiC and GaN power devices. Its advanced tapes ensure stress mitigation and residue-free removal, essential for precision electronics manufacturing. Lintec’s ongoing investment in optical film bonding tapes enhances large-area display reliability, particularly in automotive HMI interfaces and flexible screens. Environmental innovation remains central, with repulpable and UV-curable adhesives designed for recyclability and residue-free release. This combination of technical precision and green innovation solidifies Lintec’s status as a critical supplier in the electronics and printing sectors.

Country Analysis: Regional Developments Shaping the Global Specialty Tapes Industry

China – Global Manufacturing Powerhouse and Core Consumer of Automotive & Electronics Specialty Tapes

China dominates the global specialty tapes industry as both the largest manufacturing hub and a key end-use market, driven by its advanced electronics, automotive, and renewable energy sectors. Domestic electronics producers are rapidly scaling demand for EMI shielding tapes and thermally conductive tapes, critical to 5G networks and miniaturized consumer devices. The New Energy Vehicle (NEV) industry, a national strategic focus, is driving the adoption of high-temperature acrylic foam tapes (AFT) for EV battery pack assembly, thermal interface management, and body structural bonding.

Environmental policies under China’s latest industrial plan are accelerating a structural shift away from solvent-based systems. Major domestic producers are investing heavily in water-based acrylic adhesive production lines and bio-based raw material R&D, reducing VOC emissions in compliance with national ecological targets. The solar industry also contributes to the upward trend, with weather-resistant and UV-stable specialty film tapes being deployed in panel sealing and junction box bonding. Simultaneously, the e-commerce packaging surge has fueled explosive growth in tear-strip, filament, and tamper-evident specialty tapes, highlighting China’s versatility in both high-volume and high-value segments.

United States – Innovation Leader in Next-Generation Specialty Tapes and Sustainable Adhesive Solutions

The U.S. specialty tapes market is anchored in high-performance innovation, sustainability, and advanced manufacturing applications, spanning aerospace, automotive, medical, and packaging industries. In 2024, leading American manufacturers accelerated R&D in Very High Bond (VHB) and structural acrylic foam tapes, designed for lightweight automotive assemblies and composite bonding in aerospace structures. Meanwhile, the Infrastructure Investment and Jobs Act (IIJA) is driving major demand for flashing, weatherproofing, and protective sealing tapes used in energy-efficient buildings and large-scale infrastructure renovation projects.

The U.S. also leads in biocompatible medical adhesive tapes, as wearable healthcare devices and continuous monitoring systems gain mainstream adoption. New ISO 10993-5-certified medical tapes offer breathability, skin adhesion, and long-term wear capabilities. Sustainability has become a defining trend, with companies like Shurtape Technologies introducing post-consumer recycled (PCR) content packaging tapes in 2024, aligning with corporate ESG goals. Advanced RFID-enabled smart adhesive tapes are emerging for logistics and inventory tracking, positioning the U.S. as the global epicenter for next-generation specialty tapes innovation.

Germany – European Precision Hub for Industrial, Automotive, and Sustainable Tape Technologies

Germany stands as the European hub for high-precision, sustainable specialty tapes, driven by its advanced automotive, electronics, and industrial sectors. Leading manufacturers such as tesa SE are expanding facilities dedicated to die-cut adhesive tape solutions used in complex automotive interior assembly and electronic component bonding. Compliance with EU air quality and sustainability regulations has accelerated the development of low-VOC adhesive systems and solvent-free manufacturing technologies, especially within the high-demand automotive market.

In late 2024, Ahlstrom launched MasterTape® Cristal, a fiber-based transparent backing tape that is both recyclable and compostable, marking a milestone in sustainable packaging solutions. Simultaneously, collaborations between German R&D institutes and adhesive producers are advancing high-temperature silicone tapes for electric drive insulation and industrial sealing applications. The country’s thriving luxury goods and display manufacturing sectors continue to drive demand for protective surface films and transport tapes engineered to safeguard delicate finishes, reinforcing Germany’s global reputation for technical precision and eco-conscious adhesive innovation.

Japan – Pioneering Ultra-Thin, Functional, and Semiconductor-Grade Specialty Tapes

Japan remains a global leader in advanced materials, leveraging precision polymer chemistry to pioneer thin-film and high-performance specialty tapes for electronics, displays, and semiconductor manufacturing. Market leaders such as Nitto Denko and Lintec Corporation are spearheading R&D into ultra-thin adhesive films and polyimide-based heat-resistant tapes for OLED displays, foldable devices, and high-speed computing systems. Japan’s leadership in electrically conductive and anti-static adhesives supports its dominance in next-generation telecommunications and chip fabrication.

The country also invests heavily in infrastructure preservation and marine anti-corrosion tapes, supported by government R&D funding in sustainable material sciences. Recent breakthroughs include proprietary polymer synthesis for clean-removal surface protection films, offering residue-free adhesion for sensitive optical and electronic components. Beyond electronics, Japan’s automotive and construction sectors increasingly rely on UV-resistant and high-tack specialty tapes that ensure durability under extreme temperature and weather conditions, cementing its position as the epicenter of high-value, technology-driven specialty tapes.

South Korea – Expanding Role in Electronics and Electric Vehicle Specialty Tape Production

South Korea’s specialty tapes industry is propelled by its dominance in electronics, displays, and EV manufacturing, positioning it as a key global production hub. The smartphone and large-format display sectors continue to drive rapid adoption of thermal management tapes, optical clear adhesives (OCA), and EMI shielding tapes essential for device assembly and protection. Korean manufacturers, including leading players in flexible display components, are investing aggressively in high-durability double-sided tapes (DST) designed for curved and ultra-thin device architectures.

The EV manufacturing surge adds another layer of growth, as structural bonding and insulation tapes are increasingly specified for battery cell wrapping, vibration damping, and electrical protection. Government-backed programs promoting materials self-sufficiency are accelerating innovation in advanced polymer adhesives, ensuring the country maintains technological competitiveness across its high-tech industrial base. As a result, South Korea is rapidly becoming the Asia-Pacific hub for next-generation specialty tapes in electronics, energy, and automotive applications.

India – High-Growth Market Fueled by Infrastructure, Manufacturing, and Renewable Expansion

India’s specialty tapes market is expanding rapidly, fueled by the government’s “Make in India” manufacturing initiative, massive infrastructure investments, and the surge in construction and renewable energy installations. The building and construction segment is witnessing significant adoption of HVAC foil tapes, waterproof sealing tapes, and joint-repair systems in large commercial and residential projects. With the solar industry scaling up under national renewable energy targets, UV- and heat-resistant tapes are in increasing demand for photovoltaic panel installation and cable protection.

The automotive sector is also a major growth driver, as domestic and global OEMs localize manufacturing to meet regional sourcing requirements. Specialty tapes for wire harnessing, insulation, and vibration control are gaining traction, supported by government subsidies for EV production. Simultaneously, India’s growing organized retail and e-commerce markets are propelling demand for high-performance packaging and tamper-evident tapes. Local producers and multinational brands are investing in R&D facilities and manufacturing expansions, strengthening India’s role as a strategic growth market for specialty tapes across multiple industrial verticals.

France – Center for Aerospace-Grade PTFE and High-Performance Polymer Tapes

France plays a specialized role in the global specialty tapes industry, focusing on aerospace, defense, and high-performance industrial applications. Global leader Saint-Gobain continues to expand its portfolio of PTFE and silicone-coated fabric tapes, known for their non-stick, dielectric, and heat-resistant properties, serving aerospace, composites, and energy markets. French manufacturers are investing in high-dielectric polymer films and laminated tapes engineered for electrical insulation in aerospace and high-voltage systems, aligning with stringent European safety and performance standards.

In line with EU sustainability directives, France is actively contributing to European collaborative research programs developing biodegradable backing films and eco-friendly adhesive chemistries. The innovation-driven ecosystem ensures that France remains a center of excellence for polymer science and aerospace-grade adhesive tape solutions, reinforcing its influence on European industrial standards for reliability, durability, and environmental performance.

Specialty Tapes Market Report Scope

Specialty Tapes Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$114 Billion

|

|

Market Size (2034)

|

$204.4 Billion

|

|

Market Growth Rate

|

6.7%

|

|

Segments

|

By Resin Type (Acrylic, Rubber, Silicone, Others), By Backing Material (Film, Foam, Paper, Woven/Non-Woven, Foil, Others), By Product Type (Single-Sided, Double-Sided, Adhesive Transfer, Specialized Function), By End-Use Industry (Automotive, Electrical & Electronics, Healthcare & Hygiene, Building & Construction, Aerospace & Defense, Industrial/White Goods, Paper, Printing & Graphics, Retail & Graphics

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

3M Company, Nitto Denko Corporation, tesa SE, Avery Dennison Corporation, Lintec Corporation, Lohmann GmbH & Co. KG, Scapa Group plc, Intertape Polymer Group, Inc. (IPG), Berry Global Inc., Saint-Gobain Performance Plastics Corporation, Sekisui Chemical Co., Ltd., Shurtape Technologies, LLC, NICHIBAN Co., Ltd., Coroplast Tape Corporation, Teraoka Seisakusho Co., Ltd.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

By Resin Type

- Acrylic

- Rubber

- Silicone

- Others

By Backing Material

- Film

- Foam

- Paper

- Woven/Non-Woven

- Foil

- Others

By Product Type/Function

- Single-Sided

- Double-Sided

- Adhesive Transfer

- Specialized Function

By End-Use Industry

- Automotive

- Electrical & Electronics

- Healthcare & Hygiene

- Building & Construction

- Aerospace & Defense

- Industrial/White Goods

- Paper, Printing & Graphics

- Retail & Graphics

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in Specialty Tapes Market

- 3M Company

- Nitto Denko Corporation

- tesa SE

- Avery Dennison Corporation

- Lintec Corporation

- Lohmann GmbH & Co. KG

- Scapa Group plc

- Intertape Polymer Group, Inc. (IPG)

- Berry Global Inc.

- Saint-Gobain Performance Plastics Corporation

- Sekisui Chemical Co., Ltd.

- Shurtape Technologies, LLC

- NICHIBAN Co., Ltd.

- Coroplast Tape Corporation

- Teraoka Seisakusho Co., Ltd.

*- List not Exhaustive

Research Coverage

Prepared by USDAnalytics, this report investigates the global Specialty Tapes Market with a solutions-first lens, connecting end-use performance needs to materials science breakthroughs and scalable manufacturing practices; it synthesizes technology roadmaps (thermal, optical, dielectric, and NVH functions), regulatory momentum (VOC-free/solvent-free transitions), and design shifts toward lightweight, repairable, and recyclable assemblies. Our analysis reviews competitive moves, patenting activity, and investment patterns across e-mobility, semiconductors, renewable energy, healthcare wearables, and high-efficiency construction, and highlights how precision coating, digital production, and localized supply models are reshaping cost-to-serve and time-to-market. By integrating evidence from product launches, qualification data, and OEM specification trends, the study benchmarks performance envelopes (temperature endurance, peel/loop tack stability, optical clarity retention, and insulation reliability) against deployment realities on modern lines. Framed for strategists, engineers, and sourcing leaders, this report is an essential resource for sizing opportunities, de-risking material transitions, and calibrating portfolio strategy in a market where adhesion is a functional architecture—not a commodity.

Scope Highlights

Segmentation:

- By Resin Type: Acrylic; Rubber; Silicone; Others

- By Backing Material: Film; Foam; Paper; Woven/Non-Woven; Foil; Others

- By Product Type/Function: Single-Sided; Double-Sided; Adhesive Transfer; Specialized Function

- By End-Use Industry: Automotive; Electrical & Electronics; Healthcare & Hygiene; Building & Construction; Aerospace & Defense; Industrial/White Goods; Paper, Printing & Graphics; Retail & Graphics

Geographic Scope: Analysis spans 25+ countries across North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa.

Time Horizon: Historic data 2021–2024; forecast 2025–2034.

Companies: Analysis/profiles of 15+ companies (e.g., 3M, Nitto Denko, tesa SE, Avery Dennison, Lintec, Lohmann, Scapa, IPG, Berry Global, Saint-Gobain Performance Plastics, Sekisui Chemical, Shurtape, NICHIBAN, Coroplast Tape, Teraoka Seisakusho).

Deliverables

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.