Market Overview: High-Performance Smart Materials Reshaping Medical, Automotive & Aerospace Engineering

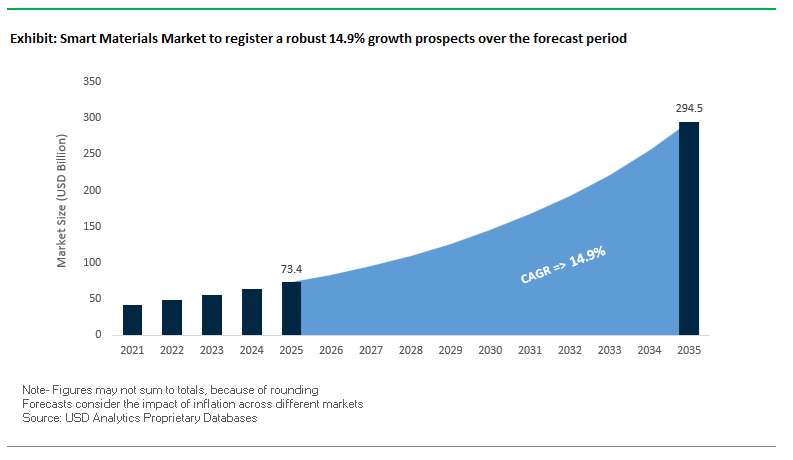

The Smart Materials Market is projected to grow from USD 73.4 billion in 2025 to USD 294.4 billion by 2035, advancing at a strong CAGR of 14.9% (2025–2035). This market expansion is fueled by the accelerated integration of Shape Memory Alloys (SMAs), Piezoelectric Ceramics, Electroactive Polymers (EAPs), and next-generation high-temperature SMAs across medical devices, soft robotics, advanced automotive systems, and aerospace actuation platforms. Manufacturers and vendors are increasingly prioritizing materials that offer large recoverable strain, high electromechanical conversion efficiency, extreme fatigue tolerance, and temperature resilience exceeding 400°C, enabling previously unattainable performance benchmarks in minimally invasive surgery, ADAS systems, industrial automation, and defense technologies.

The dominance of Nitinol (NiTi) continues due to its unparalleled superelastic strain recovery up to 10% and thermal shape memory strain up to 8%, far surpassing the limitations of traditional metal alloys. In parallel, Piezoelectric Ceramics like PZT remain indispensable due to their high electromechanical coupling (kp > 0.6) and charge coefficients exceeding 400 pC/N, supporting precision ultrasound imaging, injector actuators, and high-frequency industrial systems. Meanwhile, EAPs such as Ionic Polymer-Metal Composites (IPMCs) demonstrate bending strains up to 380% at low voltages, enabling disruptive innovation in soft robotics and biomimetic actuation. The industry is also witnessing the emergence of NiTiHf and NiTiPt SMAs, engineered to achieve stable phase transformation at >400°C, opening doors to hypersonic aerospace and jet engine control systems.

Key Insights for Manufacturers and Vendors

- Nitinol Advantage: Up to 10% superelastic strain recovery enables high-fatigue, high-precision deployment in vascular stents and neurovascular implants.

- PZT Performance Leadership: d33 > 400 pC/N and kp > 0.6 reinforce PZT’s dominance in ultrasound, actuators, and injector control systems.

- EAP Expansion: 380% bending strain places EAPs at the forefront of soft robotics and wearable actuation technologies.

- High-Temperature SMAs: NiTiHf/NiTiPt alloys exceed 400°C transformation temperatures, meeting aerospace hot-section requirements.

- Technological Convergence: Smart materials increasingly support integrated platforms combining motion control, haptics, sensing, micro-actuation, and structural adaptation.

Market Analysis: Rapid Material Innovation and Cross-Sector Adoption Driving Smart Materials Demand

Recent advances across the global Smart Materials Industry highlight a dynamic shift toward high-cycle actuation, flexible sensing, and environmentally compliant material systems. In December 2025, EPFL researchers achieved a major breakthrough by developing a Shape Memory Alloy (SMA) architecture capable of 35 Hz actuation cycle frequency using sequential activation and passive cooling—effectively overcoming conventional SMA thermal bottlenecks. This innovation positions SMAs for high-speed robotics, aerospace mechanisms, and advanced industrial actuation systems. Earlier, in Q3 2025, leading sensor manufacturers launched Flexible PVDF Piezoelectric Films, optimized for wearable medical devices and biometric monitoring systems. Their ultra-low power consumption and mechanical flexibility are accelerating commercial adoption across digital health ecosystems, sports analytics, and remote patient monitoring.

Corporate expansion and downstream adoption trends continue reshaping the supply chain. TDK Corporation’s Asia-Pacific MLCC expansion in October 2024 strengthened the manufacturing ecosystem for lead-free multilayer piezoelectric stacks, supplying critical components for automotive ADAS, ignition systems, and industrial automation. By June 2025, major European automotive OEMs intensified testing of Barium Titanate (BTO) lead-free piezoelectrics, aligning with global commitments to phase out toxic materials under tightening environmental regulations. In the biomedical domain, March 2024 marked a major milestone when a startup secured USD 50 million Series C funding to commercialize a fatigue-optimized Nitinol neurovascular stent capable of tolerating 100+ million cycles under physiological bending loads—significantly enhancing durability in life-critical implants.

Research and government investment further underscore the sector’s strategic importance. In January 2025, university researchers validated a 3D-printed Dielectric Elastomer Actuator (DEA) able to deliver 25% strain at 50 MV/m, paving the path for mass production of complex EAP-based haptic, robotic, and wearable systems. DARPA’s Q4 2024 investment into next-generation magnetostrictive materials for naval sonar applications reinforces the growing defense reliance on high-power-density smart materials. Lastly, September 2025 highlighted a market-wide sustainability shift, as manufacturers intensified R&D into lead-free piezoelectric ceramics using Bismuth Sodium Titanate (BNT) and Potassium Sodium Niobate (KNN) to meet stringent RoHS directives and global eco-compliance targets.

AI-Driven Predictive Design, Bio-Responsive Material Engineering, Autonomous Coatings, and Programmable Metamaterials Driving Next-Generation Smart Material Adoption

Market Trend 1: AI-Driven Predictive Modelling and Inverse Design Accelerating Smart Material Discovery and System Performance

Artificial intelligence is fundamentally reshaping the Smart Materials Market by enabling rapid and highly accurate prediction of material behavior, reducing development cycles, and enabling autonomous optimization workflows. Machine Learning (ML) models—including Support Vector Regression (SVR) and Artificial Neural Networks (ANNs)—are increasingly used to forecast complex structure–property relationships that previously required extensive experimentation. Notably, for Shape Memory Alloys (SMAs), SVR models have demonstrated R ≈ 0.92 accuracy when predicting Martensitic Transformation Temperatures for compositions not included in the training data, enabling highly precise alloy tuning for actuation, aerospace, and biomedical applications.

This computational acceleration is further amplified by AI-based inverse design, enabling researchers to map required mechanical, electrical, or thermal properties back to optimal molecular architectures and structural configurations. This reduces iterative trial-and-error cycles and shortens commercialization timelines for advanced piezoelectric, magnetostrictive, or shape memory systems. Autonomous Material Synthesis and Experimental (AMASE) platforms further accelerate innovation by generating real-time phase diagrams and characterizing multimodal performance without human intervention. Meanwhile, Physics-Informed Neural Networks (PINNs) ensure reliable prediction of microstructure evolution, stress–strain behavior, and polymer network dynamics by embedding conservation laws and physical constraints into the AI architecture. Collectively, these AI-driven advancements create a scalable path toward smart materials with predictable, customizable, and certifiable functional performance—core to next-generation robotics, medical devices, adaptive structures, and aerospace components.

Market Trend 2: Rise of Bio-Responsive and Biodegradable Smart Materials for Targeted Delivery, Regenerative Medicine, and Sustainable Applications

Biological responsiveness and controlled degradation kinetics are redefining the competitive landscape of smart materials, especially across biomedical devices, drug delivery systems, and eco-friendly polymers. Biodegradable polymers such as enzyme-cleavable polyesters and amide-based materials are engineered with labile chemical linkages that enable programmable degradation timelines. For instance, lower–molecular weight star-PCL (polycaprolactone) variants show significantly faster enzymatic degradation, allowing material scientists to fine-tune breakdown profiles for implants, tissue scaffolds, and resorbable medical devices.

Smart drug delivery materials offer another critical vector of innovation. Chitosan-based systems with low degrees of acetylation degrade under lysozyme exposure, enabling drug residence for several months in vivo and providing stable yet responsive therapeutic release. Hydrogels designed for soft-tissue regeneration also now integrate dynamic stiffness modulation, enabling Young’s Modulus values in the kPa range to actively guide cell differentiation—e.g., higher stiffness encouraging osteogenesis and lower stiffness promoting adipogenesis. pH-responsive systems undergo conformational changes in acidic microenvironments (pH 5.5–6.5), activating drug release in tumors or endosomes while remaining stable at physiological pH ≈ 7.4. This convergence of biodegradability, targeted responsiveness, and biocompatibility positions smart biological materials as a cornerstone for precision medicine, tissue engineering, and sustainable product development.

Market Opportunity 1: High-Durability, Self-Healing and Self-Powering Smart Coatings for Infrastructure and Industrial Monitoring

The Smart Materials Market is experiencing a substantial opportunity in the development of multifunctional coatings that autonomously repair mechanical damage and generate onboard energy for sensing. Self-healing coatings employing microcapsule-based or dynamic polymer networks now achieve 80–97% mechanical strength recovery, restoring structural integrity without manual intervention. These capabilities are critical for long-life applications in aerospace, maritime infrastructure, pipelines, and industrial machinery.

Beyond healing, self-powering functionality is emerging as a major differentiator. Triboelectric Nanogenerators (TENGs), embedded within coatings, convert vibrational or mechanical energy into electrical power for Structural Health Monitoring (SHM). High-performance TENG systems deliver up to 500 W/m² peak power density and 371.2 W·m⁻³·Hz⁻¹ volumetric power density, enabling distributed, maintenance-free sensor networks. Their durability is equally compelling—advanced TENG devices retain 80% efficiency after 1.5 million mechanical cycles, making them viable for high-vibration environments such as rail systems, wind turbines, and automotive structures. The convergence of self-healing chemistry with embedded energy harvesting establishes a new generation of smart coatings capable of enabling fully autonomous SHM ecosystems.

Market Opportunity 2: Programmable Phase-Change and Mechanically Adaptive Meta-Materials for Advanced Aerospace, Electronics, and Defense Applications

Programmable smart metamaterials represent a breakthrough opportunity for industries seeking tunable thermal, mechanical, and electromagnetic behavior. Architected metallic lattice structures infused with Phase Change Materials (PCMs) enable dynamic thermal regulation, achieving Effective Thermal Conductivity (ETC) enhancements up to 75% higher than foam-based thermal enhancers once the PCM transitions above its melting point. This creates a new class of reconfigurable thermal management solutions for high-power electronics, aerospace systems, and battery packs.

Mechanical programmability is also advancing rapidly through Liquid Crystal Elastomer (LCE) meta-materials. These systems exhibit near-zero stiffness up to a stretch ratio of 1.4, enabling large, reversible deformations ideal for morphing aircraft wings, soft robotics, and deployable space structures. On the electromagnetic front, nanophotonic metamaterials provide real-time control over emitted or reflected infrared signals via electronically or thermally induced changes in amplitude and phase—enabling adaptive IR camouflage and next-generation defense cloaking technologies. The ability to engineer materials with programmable stiffness, shape, conductivity, and thermal profiles positions smart metamaterials as one of the most transformative opportunity areas in the Smart Materials Market.

Smart Materials Market Share Analysis

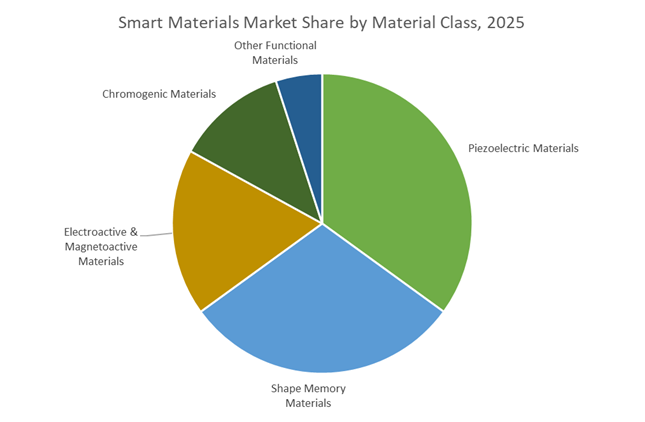

Market Share by Material Class: Piezoelectric Materials Lead Due to Superior Electromechanical Performance and Market Maturity

Piezoelectric materials, holding an estimated 35% share of the global smart materials market in 2025, remain the dominant material class due to their unparalleled electromechanical coupling efficiency and long-standing commercial maturity across high-performance sensing and actuation applications. Their ability to convert mechanical energy into electrical output—coupled with their ability to generate mechanical displacement when electrically stimulated—makes them indispensable for precision-driven industries seeking reliability, repeatability, and ultrafast response times. Lead Zirconate Titanate (PZT) continues to anchor this segment owing to its exceptionally high piezoelectric coefficient, robust thermal stability, and proven scalability in manufacturing. The material’s deep penetration into mass-market products—ranging from consumer audio devices and vehicle fuel injectors to advanced automation platforms—reinforces its strong revenue footprint. At the same time, rapid adoption in emerging technologies such as micro-positioning systems, ultrasonic surgical tools, and biomedical sensors fuels sustained expansion. As the broader smart materials industry pushes toward more integrated, miniaturized, and energy-efficient systems, piezoelectric materials remain the most commercially validated and technically indispensable category, securing their position as the highest-revenue contributor within the global market.

Market Share by End-Use Industry: Healthcare & Biomedical Dominates Through High-Value Diagnostic and Therapeutic Applications

The Healthcare & Biomedical sector, representing roughly 30% of global smart materials demand, leads the market due to its reliance on high-precision, biocompatible, and performance-critical material technologies for diagnostics, treatment, and therapeutic monitoring. Piezoelectric ceramics serve as the foundation of ultrasound imaging systems, one of the world’s highest-volume and highest-value diagnostic modalities, powering transducers that deliver real-time visualization with exceptional sensitivity. Simultaneously, shape memory polymers and alloys enable minimally invasive surgical tools, deployable stents, adaptive implants, and responsive drug-delivery mechanisms, reinforcing smart materials as essential enablers of next-generation medical innovation. Growing global healthcare expenditure, the rise of chronic diseases, and the accelerating demand for non-invasive diagnostics ensure sustained market leadership in this category. Furthermore, the premium pricing associated with medical-grade materials—necessitated by strict ISO, FDA, and biocompatibility compliance—elevates the revenue contribution from healthcare applications beyond that of automotive and aerospace sectors, despite their high-volume requirements. As digital health, wearables, personalized medicine, and robotic surgery continue to expand, smart materials remain integral to enabling precision, reliability, and patient-specific performance, solidifying the Healthcare & Biomedical segment as the dominant end-use industry driving market growth.

Country Analysis: Global Smart Materials Hotspots and Strategic Innovation Pathways

United States: Aerospace-Grade Smart Materials and Biomedical SMA Commercialization Accelerating National Innovation

The United States remains one of the most dynamic and innovation-centric markets for smart materials, with strong federal funding and private-sector activity pushing advancements in aerospace, biomedical engineering, and smart manufacturing systems. The U.S. Department of Energy’s $33 million funding opportunity (July 2024) specifically accelerates high-performance material platforms for clean energy, reinforcing the critical role of smart materials—particularly adaptive composites, electroactive polymers, and responsive alloys—in next-generation manufacturing systems. This commitment strengthens U.S. leadership in smart materials integration across industrial automation, renewable energy hardware, and intelligent infrastructure.

In aerospace, the expansion of ATI Inc.’s materials finishing operations (April 2024) has bolstered domestic production capabilities for high-quality titanium and nickel-based alloys—key precursors used in Nitinol Shape Memory Alloys (SMAs) for morphing structures, flight control actuators, and high-temperature systems. Moreover, the acquisition of Johnson Matthey’s Medical Device Components (March 2024) highlights the U.S. market's heightened focus on Nitinol-driven biomedical device applications, including minimally invasive surgical tools and stents. Complementing these developments, U.S. National Labs are advancing additive manufacturing of SMPs and composite smart structures, enabling unprecedented design flexibility for customized defense components and high-performance morphing architectures.

China: Industrial-Scale Commercialization of Shape Memory Alloys and Electroactive Polymers for Robotics and EV Manufacturing

China is accelerating industrial leadership in smart materials through expansive production capacity, strong policy incentives, and integration of advanced materials into high-growth industries such as EVs, robotics, and consumer electronics. The country’s strategic focus on Shape Memory Alloys (SMAs) and Electroactive Polymers (EAPs) aligns with national objectives to dominate global robotics and new-energy vehicle manufacturing. Chinese companies are rapidly advancing large-scale SMA applications for adaptive cooling systems, high-precision actuators, and smart mechanical components used throughout industrial automation lines.

A notable trend is the commercialization of Copper-based SMAs, which offer strong thermo-mechanical performance at significantly lower cost compared to Nitinol. This positions China to penetrate large-volume, price-sensitive sectors such as HVAC systems, industrial dampers, and automotive thermal management. China’s consumer electronics ecosystem also drives massive adoption of micro-SMA actuators for smartphone autofocus systems, vibration control, and camera stabilization, reflecting how high-volume production enables rapid deployment of smart materials in mainstream consumer technologies.

Germany/European Union: High-Precision Piezoelectrics and Sustainable Smart Material Solutions Under Horizon Europe Initiatives

Germany and the European Union represent a strategically regulated and innovation-intensive ecosystem for smart materials, with strong emphasis on sustainability, high-precision engineering, and energy-efficient infrastructure. Through the €93.5 billion Horizon Europe Programme (2021–2027), the EU continues to fund major research initiatives involving soft robotics, 2D materials, and electroactive polymers, ensuring sustained technological leadership across industrial and energy-transition applications.

Germany holds a central role through its advanced automotive and industrial technologies. Companies such as PI Ceramic GmbH and CeramTec GmbH lead in multilayer piezoelectric actuators based on PZT and emerging lead-free piezoceramics, enabling high-precision fuel injection systems, active vibration control, and adaptive suspension systems in luxury European vehicles. The region also demonstrates aggressive adoption of electrochromic smart windows, leveraging Prussian Blue, tungsten oxide, and other electrochromic thin films. As EU energy efficiency mandates tighten, demand for smart glazing and adaptive building materials continues to accelerate, enabling Europe to scale integrated smart-city infrastructure.

Japan: Precision Piezoelectric Materials and High-Temperature Shape Memory Alloys Powering Industrial and Sensor Innovation

Japan remains a global pioneer in high-performance piezoelectric materials, thermochromic materials, and advanced SMAs, supported by its unmatched expertise in functional ceramics and precision-engineered materials. Japanese manufacturers dominate global supply chains for Lead Zirconate Titanate (PZT) and increasingly advanced Barium Titanate (BaTiO₃) nanomaterials used in highly sensitive MEMS sensors, ultrasonic transducers, industrial NDT equipment, and miniaturized actuators.

The country also leads in developing high-temperature SMAs and specialty ceramics, enabling performance in extreme industrial environments including power generation, heavy machinery, and aerospace components. Japanese R&D continues to push the boundaries of adaptive materials for sensors, actuators, and optical monitoring systems, while thermochromic materials are increasingly used in precision industrial sensors and controllers. Japan’s smart materials landscape is shaped by a strong convergence of advanced robotics, automotive innovation, and electronics miniaturization.

South Korea: Flexible Electroactive Polymers and Biomedical Hydrogels Supporting Next-Generation Displays and Wearable Devices

South Korea is rapidly emerging as a powerhouse in flexible smart materials, especially Electroactive Polymers (EAPs) and smart hydrogels for biomedical and wearable applications. South Korean display leaders are integrating flexible EAPs into foldable and rollable display architectures, enabling thinner, lighter, and more responsive panels for next-generation smartphones and consumer electronics. These materials enhance touch sensitivity, provide dynamic haptic feedback, and support advanced gesture recognition.

At the same time, South Korean biomedical research institutions are investing heavily in smart hydrogels that mimic biological tissues and autonomously respond to physiological conditions. These innovations support new applications in drug delivery, wound management, and continuous health monitoring, aligning with South Korea’s broader push toward digital healthcare transformation. The nation’s strategic investments position it as a key contributor to global innovation in smart, bio-integrated materials.

Canada: Smart Coatings and Self-Healing Materials Advancing Infrastructure Durability and Harsh-Environment Performance

Canada is emerging as a significant innovation hub for smart coatings, self-healing polymers, and adaptive construction materials, fueled by government-supported R&D initiatives and an industry focus on infrastructure resilience. Canadian research centers continue to develop advanced self-healing coatings, capable of autonomously repairing micro-cracks and corrosion damage, enabling longer service life for bridges, pipelines, and offshore structures exposed to extreme weather and chemical environments.

Canadian material scientists are also applying smart materials to mining, marine, and Arctic infrastructure, where conditions demand durable, high-performance protective solutions. The nation’s emphasis on commercializing field-ready smart material technologies supports adoption across construction, energy, and heavy industrial sectors, reinforcing Canada’s position in the global market for smart and functional materials designed for extreme environments.

Competitive Landscape: Leading Smart Material Innovators and Their Strategic Growth Priorities

The Smart Materials Market is characterized by a mix of diversified materials companies, advanced ceramics producers, SMA specialists, and motion-control integrators. Competitiveness is driven by R&D depth, vertical integration, material purity, actuator efficiency, and domain-specific certification—particularly in biomedical, automotive, aerospace, and defense applications. Market leaders differentiate by developing customized, high-performance smart materials enabling next-generation actuation, sensing, damping, and ultrasonic capabilities.

Parker Hannifin Corporation: Advanced MR Fluids Strengthening Motion and Control Systems

Parker Hannifin’s LORD Division is a dominant player in magneto-rheological (MR) fluids, elastomeric bearings, vibration isolators, and engineered sensing materials. The company’s USD 3.675 billion acquisition of LORD significantly expanded its exposure to aerospace and automotive smart materials. Parker’s MR fluids—capable of instant viscosity change under magnetic fields—play a central role in adaptive damping, precision motion control, and high-reliability vibration mitigation. Its integration capabilities allow seamless deployment of MR-based systems in aircraft cockpit controls, electric vehicle suspension, industrial robotics, and thermal management solutions. Strategic alignment with aerospace OEMs ensures Parker LORD remains a preferred supplier for high-performance materials supporting dynamic load control and noise-vibration-harshness (NVH) optimization.

TDK Corporation: Lead-Free Piezoelectric Leadership in Automotive & Consumer Electronics

TDK Corporation continues to expand its stronghold in piezoelectric actuators, sensors, multilayer ceramics, and haptic components, supported by its EPCOS brand. Its strategic emphasis on miniaturization is central to high-volume production of Micro-Actuators for automotive lighting, high-precision ADAS systems, and compact consumer electronics. TDK is investing heavily in transitioning to environmentally compliant lead-free piezoelectric ceramics (KNN-based) driven by global environmental directives. Its CeraPlas® piezo-haptic actuators demonstrate the company’s innovation in compact, energy-efficient haptic interfaces for premium devices. TDK’s Asia-Pacific MLCC expansion strengthens supply chain resilience for automotive and electronics manufacturers adopting smart materials at scale.

Murata Manufacturing: High-Volume Miniaturized Piezo Solutions for IoT and Medical Devices

Murata is a global leader in piezoelectric ceramic filters, ultrasonic sensors, MEMS resonators, and piezo buzzers, leveraging its deep expertise in multilayer ceramic processing. Its dominance in compact passive components positions the company as a preferred supplier for IoT devices, smartphones, wearables, and advanced consumer electronics. Murata is expanding its footprint in medical and healthcare applications, especially through ultrasonic sensing technologies operating in the 5–20 MHz range for diagnostic and monitoring tools. Its focus on high-volume, precision miniaturization ensures continuous demand for Murata’s smart material components across emerging electronics applications.

Fort Wayne Metals: Precision Nitinol for High-Reliability Medical Implants

Fort Wayne Metals specializes in high-precision Nitinol wire, tube, and strip, with supporting alloys like MP35N® tailored for demanding biomedical applications. The company’s expertise lies in producing ultra-clean Nitinol with inclusion sizes below 10 μm, a critical determinant of long-term fatigue life in cardiovascular stents, neurovascular implants, and high-cycle medical components. With a nearly exclusive focus on medical device OEMs, Fort Wayne Metals emphasizes strict quality control, precision fabrication, and alloy customization to meet stringent regulatory and performance requirements. Its specialization enables the commercialization of next-generation implantable smart materials featuring improved fatigue resistance, flexibility, and biocompatibility.

CeramTec GmbH: High-Performance Piezoceramics for Ultrasound and Sonar Systems

CeramTec is a leading force in medical-grade piezoceramics, ultrasound transducers, and high-power piezoelectric components. Its materials exhibit superior dielectric constants and high-quality factors, supporting demanding applications in therapeutic ultrasound, sonar, industrial nondestructive testing, and high-power acoustic systems. CeramTec’s expertise in custom geometry fabrication (discs, plates, focus bowls) gives it a competitive edge in medical device manufacturing and minimally invasive diagnostics. Its portfolio includes both PZT and lead-free piezo ceramics, aligning with global environmental regulations and the transition toward safer, sustainable material systems.

Smart Materials Market Report Scope

Smart Materials Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$73.4 Billion

|

|

Market Size (2035)

|

$294.4 Billion

|

|

Market Growth Rate

|

14.9%

|

|

Segments

|

By Material Class (Shape Memory Materials, Piezoelectric Materials, Chromogenic Materials, Electroactive & Magnetoactive Materials, Other Functional Materials), By Stimulus Type (Physical Stimuli, Electrical & Magnetic Stimuli, Chemical & Biological Stimuli), By Application Function (Actuators & Motors, Sensors & Transducers, Structural/Adaptive Materials, Energy Conversion & Harvesting), By End-Use Industry (Aerospace & Defense, Automotive, Healthcare & Biomedical, Construction & Infrastructure, Consumer Electronics)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

BASF, DuPont, Covestro, TDK, 3M, LG Chem, Kyocera, ATI, Evonik, Lubrizol, Huntsman, Nitinol Devices & Components (NDC), CeramTec, Saint-Gobain, Hexcel

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Smart Materials Market Segmentation

By Material Class

- Shape Memory Materials

- Piezoelectric Materials

- Chromogenic Materials

- Electroactive & Magnetoactive Materials

- Other Functional Materials

By Stimulus Type

- Physical Stimuli

- Electrical & Magnetic Stimuli

- Chemical & Biological Stimuli

By Application Function

- Actuators & Motors

- Sensors & Transducers

- Structural / Adaptive Materials

- Energy Conversion & Harvesting

By End-Use Industry

- Aerospace & Defense

- Automotive

- Healthcare & Biomedical

- Construction & Infrastructure

- Consumer Electronics

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in Smart Materials Market

- BASF

- DuPont

- Covestro

- TDK

- 3M

- LG Chem

- Kyocera

- ATI

- Evonik

- Lubrizol

- Huntsman

- Nitinol Devices & Components (NDC)

- CeramTec

- Saint-Gobain

- Hexcel

*- List not Exhaustive

Research Coverage

The latest Smart Materials Market study from USDAnalytics delivers a deep-dive strategic assessment of how shape memory alloys, piezoelectric materials, electroactive polymers, chromogenic systems, and other functional materials are reshaping high-value applications across healthcare, automotive, aerospace, infrastructure, and electronics. Drawing on quantitative datasets and expert commentary, this report investigates multi-billion-dollar investment flows, technology roadmaps, qualification cycles, and supply-chain realignment as OEMs pivot toward high-strain, high-efficiency, and high-temperature smart material platforms. It highlights AI-enabled material design, bio-responsive polymers, self-healing and energy-harvesting coatings, programmable metamaterials, and lead-free piezoceramics as core innovation vectors, while analysis reviews compare performance benchmarks, integration challenges, and adoption barriers across key sectors and regions. The study further examines patent trends, regulatory and RoHS-driven material substitutions, capex plans of major producers, and partnership models linking materials suppliers with device, module, and system integrators. These breakthroughs and ecosystem shifts are mapped against 10-year revenue forecasts, scenario analyses, and competitive positioning matrices, making this report an essential resource for industry professionals, investors, and policymakers seeking to understand where value will concentrate in the global Smart Materials Market over the next decade.

Scope Highlights

- Segmentation:

By Material Class – Shape Memory Materials, Piezoelectric Materials, Chromogenic Materials, Electroactive & Magnetoactive Materials, Other Functional Materials

By Stimulus Type – Physical Stimuli; Electrical & Magnetic Stimuli; Chemical & Biological Stimuli

By Application Function – Actuators & Motors; Sensors & Transducers; Structural / Adaptive Materials; Energy Conversion & Harvesting

By End-Use Industry – Aerospace & Defense; Automotive; Healthcare & Biomedical; Construction & Infrastructure; Consumer Electronics

- Geographic Scope: Analysis spans 25+ countries across North America, Europe, Asia Pacific, Latin America, the Middle East & Africa.

- Timeframe: Historic data from 2021 to 2025 and forecast data from 2026 to 2034.

- Companies Covered: Analysis and profiles of 15+ leading participants across materials, components, and smart system integration in the global Smart Materials Market.