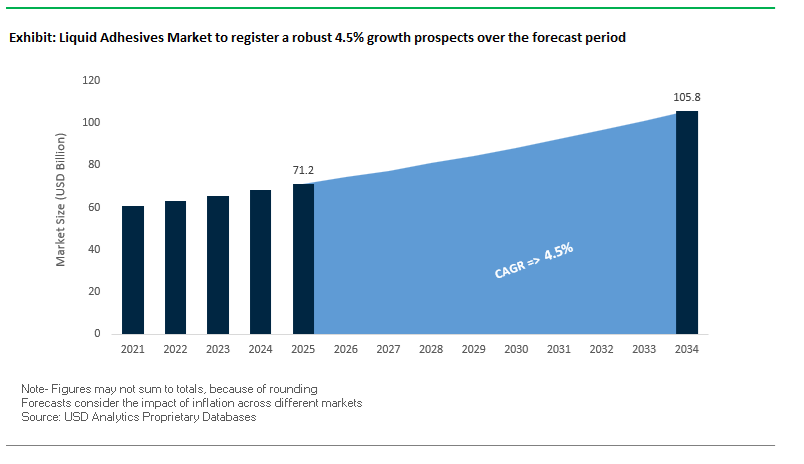

The Global Liquid Adhesives Market is projected to expand from USD 71.2 billion in 2025 to USD 105.8 billion by 2034, advancing at a CAGR of 4.5%, as liquid adhesives become process-critical materials in automated, regulation-constrained manufacturing environments. Growth is structurally anchored in automotive electrification, electronics miniaturization, and modern construction systems, where adhesive selection increasingly determines design freedom, production throughput, and regulatory compliance. Across these sectors, liquid adhesives are replacing mechanical fastening and solvent-heavy legacy chemistries, driven by sustainability targets and the need for consistent performance across complex, multi-material assemblies.

From a formulation and OEM-qualification perspective, manufacturers are rapidly shifting portfolios toward UV-curable, water-based, and low-monomer polyurethane systems to align with tightening REACH, EPA, and OSHA requirements while supporting faster cure cycles and automated dispensing. Leading suppliers have invested heavily in low-free-monomer PU platforms, high-performance epoxies, and structural acrylics that deliver high lap shear strength, fatigue resistance, and controlled flexibility without compromising worker safety. These systems are increasingly specified early in product design, particularly where dissimilar substrates—metals, engineering plastics, composites, and elastomers—must be bonded reliably under thermal cycling, vibration, and long-term load.

Operational economics and electrification trends are reinforcing this shift. In electronics manufacturing, UV-curable and cyanoacrylate liquid adhesives now dominate high-speed assembly lines, routinely achieving handling strength in under 15 seconds and supporting Industry 4.0 throughput targets. In automotive and e-mobility applications, the transition to cell-to-pack battery architectures and lightweight structures has materially increased adhesive intensity, with EV battery packs now consuming multiple times more liquid adhesive per unit than earlier-generation designs. Thermally conductive epoxies and flame-retardant polyurethane formulations are being specified not only for bonding, but also for vibration damping, thermal management, and structural integrity.

The Global Liquid Adhesives Industry is witnessing accelerated technological innovation, strategic consolidation, and regulatory adaptation. Leading chemical and adhesive manufacturers have focused investments on R&D efficiency, bio-based chemistry, and regional production capacity expansion to capture demand from EV, construction, and high-speed packaging markets.

In October 2025, Design Polymerics introduced a new series of polyurethane liquid roof mastics packaged in recycled pails, marking a tangible step toward circular economy adoption in roofing and construction adhesives. Around the same time, Henkel expanded its Brandon, South Dakota manufacturing facility, strengthening its North American base for industrial MRO adhesives and functional coatings, while aligning production with sustainability and supply chain resilience.

The electronics adhesives segment advanced notably in August 2025, with Epoxy Technology Inc. (Meridian Adhesives Group) launching its EPO-TEK® 353NDP two-part epoxy series tailored for optical communications and fiber bonding, crucial for high-speed data transmission applications. In June 2025, Meridian Adhesives Group established its Penang Application Development Center, reinforcing Asia’s role as a core hub for semiconductor packaging and liquid adhesive R&D.

H.B. Fuller’s March 2025 introduction of recyclable water-based polymer adhesives for flexible packaging highlighted the industry’s strong pivot toward sustainable liquid adhesive formulations that support mechanical recyclability and food-contact safety. Meanwhile, APPLIED Adhesives deepened its market presence through strategic acquisitions in April and July 2025, including BTmix and Adhesive Solutions, consolidating its North American distribution network for custom hot melt and liquid adhesive systems.

In November 2024, Henkel’s ultra-high temperature silicone adhesive received UL 746C certification, capable of maintaining bond integrity at 230°C, expanding its use in HVAC and appliance sealing. Finally, Avery Dennison’s December 2024 acquisition of Meridian’s Flooring Business (Taylor Adhesives and Polycom) signaled an industry consolidation wave, integrating flooring installation adhesives into a broader performance coatings portfolio.

Market Trend 1: Accelerated Formulation of Isocyanate-Free and Low-VOC Liquid Adhesive Systems

The regulatory environment surrounding polyurethane-based liquid adhesives is rapidly tightening, compelling manufacturers to reformulate their chemistries. The European Union’s REACH Regulation (Annex XVII, Entry 74) represents a major compliance inflection point, effective August 24, 2023, mandating that professional users handling polyurethane adhesives with ≥0.1% monomeric diisocyanates must undergo certified training on safe handling. The stringent requirement is driving the market toward isocyanate-free and micro-emission (ME) systems with <0.1% residual monomers, effectively bypassing the training obligation and enhancing worker safety compliance.

The regulatory push has ignited R&D in bio-based polyurethane adhesives, designed to reduce petrochemical dependence and volatile organic compound (VOC) emissions. Academic studies and industrial initiatives have demonstrated that bio-polyurethane liquid adhesives derived from vegetable oils—such as soybean or castor oil—can achieve performance parity or even exceed conventional PU adhesives in bonding strength, elasticity, and durability. These materials offer a measurable reduction in carbon footprint and appeal to sustainability-conscious OEMs across the automotive, electronics, and packaging industries.

Leading adhesive manufacturers are thus transitioning their portfolios toward low-VOC and solvent-free bio-polyurethane formulations, aligning with global environmental directives like CARB standards, China’s GB/T 33372-2020 VOC guidelines, and the EU Green Deal’s carbon neutrality targets. The shift marks a structural transition in the liquid adhesive market’s product lifecycle—from compliance-driven reformulation to strategic innovation, creating new competitive benchmarks for sustainable bonding technologies.

Market Trend 2: Adoption of Dual-Cure and Light-Cure Technologies for High-Speed Automated Manufacturing

In the era of Industry 4.0 and high-throughput manufacturing, dual-cure and light-curing liquid adhesives are revolutionizing assembly efficiency across automotive, electronics, and medical device sectors. These next-generation adhesives provide rapid, controllable curing cycles essential for high-volume production lines.

In automotive and electronic applications such as ADAS sensors (LiDAR/RADAR), micro-optics, and implantable medical devices, UV/LED light-curing adhesives can achieve full functional strength within 1 to 30 seconds, significantly reducing assembly time compared to conventional heat- or moisture-curing systems. The capability translates directly to lower energy consumption, reduced downtime, and greater production throughput, key performance parameters in advanced manufacturing ecosystems.

However, one of the critical limitations of light-curing systems—incomplete curing in shadowed or obstructed geometries—is being mitigated through dual-cure adhesive technology. By combining UV-curing for immediate fixation with secondary moisture or heat-curing mechanisms, these formulations ensure complete polymerization even in inaccessible areas, enhancing bond reliability across complex assemblies. Major adhesive producers are publishing technical process guides showcasing these dual-cure systems for applications in electronics encapsulation, structural sealing, and component bonding.

The technological advancement underpins a broader industrial shift: from purely chemical innovation to process-integrated performance optimization. Dual-cure systems are enabling seamless integration into robotic and automated dispensing platforms, contributing to predictable, high-precision assembly across critical industries, making them a cornerstone of the next-generation liquid adhesive market.

Market Opportunity 1: Servicing the Proliferation of Dissimilar Material Bonding in Electric Vehicle Lightweighting

The electric vehicle (EV) revolution is creating a new frontier for structural liquid adhesives designed to bond dissimilar materials—a key enabler of lightweighting and improved battery performance. As OEMs transition from steel-heavy architectures to aluminum, composites, and polymer hybrids, adhesives have replaced traditional welding and mechanical fastening as the primary bonding method due to their flexibility, corrosion resistance, and stress distribution capabilities.

Industry leaders are introducing specialized two-part epoxy and acrylic liquid structural adhesives engineered for xEV battery assembly and structural module integration. These adhesives provide exceptional fatigue resistance, crash energy absorption, and thermal management properties, ensuring safe operation even under the extreme temperature fluctuations typical in EV environments.

For instance, liquid structural adhesives used in battery tray assembly must bond aluminum trays to fiber-reinforced polymer covers, balancing thermal expansion mismatches and maintaining long-term sealing performance. The not only strengthens the vehicle structure but also contributes to extended driving range by minimizing vehicle weight.

The EV market’s rapid expansion is driving exponential demand for these specialized adhesives. With the global EV battery manufacturing capacity set to grow over fivefold by 2030, suppliers offering custom-formulated, thermally resilient, and high-shear adhesives are strategically positioned to capture significant market share. Adhesive manufacturers that align with automotive OEM qualification programs for lightweight and high-energy-density battery packs will dominate the evolving high-value segment of the liquid adhesives industry.

Market Opportunity 2: Development of On-Demand and Point-of-Use Dispensing Services for MRO and Construction Applications

Beyond formulation chemistry, an emerging opportunity lies in on-demand adhesive dispensing and smart process control systems for industrial and maintenance operations. The integration of Adaptive Process Control (APC) and real-time quality verification in liquid adhesive dispensing equipment is revolutionizing material efficiency, process precision, and operational cost savings—particularly in automotive, aerospace, and construction sectors.

In large-scale manufacturing environments such as automotive Body-in-White assembly, the deployment of smart dispensing systems capable of real-time monitoring of bead geometry, flow consistency, and cure status ensures consistent application quality. The precision allows design engineers to eliminate redundant mechanical fasteners or spot welds, translating into lighter structures, reduced assembly costs, and improved durability.

For maintenance, repair, and operations (MRO) in construction and infrastructure, portable and cartridge-based dispensing systems offering point-of-use adhesive mixing and application are gaining popularity. These systems minimize waste, improve curing control, and enable on-site customization of bonding performance for applications like structural sealing, concrete repair, and waterproofing.

The convergence of chemistry, automation, and digital quality assurance is redefining the competitive dynamics of the liquid adhesives market. Service-oriented adhesive models—where suppliers not only provide materials but also process integration, sensor-based feedback, and operator training—are unlocking new revenue channels. By shifting from product sales to performance-based service ecosystems, manufacturers can establish long-term customer partnerships, mirroring the trajectory of Industry 4.0-driven industrial transformation.

Liquid Adhesives Market Share Insights, 2025-2034

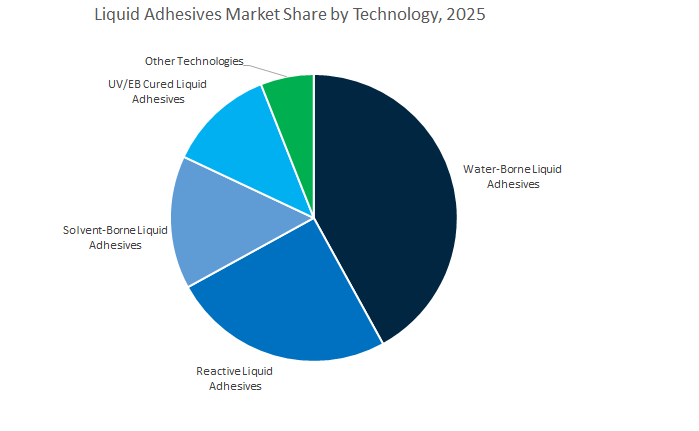

Market Share by Technology

The water-borne liquid adhesives segment dominates the global liquid adhesives market, holding an estimated 42.6% share in 2025, driven by stringent environmental standards and growing preference for low-VOC, non-flammable adhesive systems. Water-borne adhesives—based on PVA, acrylic, and polyurethane dispersions—have gained traction in packaging, woodworking, paper converting, and construction, thanks to their excellent adhesion to porous substrates, easy clean-up, and non-toxic formulation. As global manufacturers pursue sustainability certifications and compliance with REACH and EPA standards, water-borne adhesives have become the go-to solution for eco-conscious industries seeking high bond strength with minimal emissions. Technological advances in high-solids and hybrid polymer emulsions have enhanced performance in moisture-prone and temperature-variable environments, allowing these systems to rival the durability of solvent-based products while remaining cost-competitive.

Reactive liquid adhesives represent the market’s high-performance frontier, showing strong growth due to increasing demand for structural bonding and durability in automotive, wind energy, and construction sectors. These adhesives form crosslinked polymer networks upon curing, offering superior mechanical strength, chemical resistance, and long-term stability. Their role in EV battery assembly, composite structures, and advanced glazing underscores their contribution to lightweighting and sustainability in modern manufacturing. Solvent-borne liquid adhesives, though declining, remain vital for specific industrial and footwear applications that require deep substrate penetration, fast setting, and high bond integrity. Meanwhile, UV/EB-cured adhesives are emerging as a high-growth segment in electronics, optics, and medical devices, where precision, transparency, and rapid curing are paramount.

Market Share by End-Use Industry

The packaging and converting industry leads the global liquid adhesives market, capturing a 28.8% share in 2025, reflecting its dependence on adhesives for carton sealing, labeling, lamination, and flexible packaging production. Rising consumer demand for convenience foods, e-commerce shipments, and sustainable packaging materials has positioned liquid adhesives as a cornerstone of the modern packaging supply chain. These adhesives enable high-speed bonding, excellent printability, and substrate versatility, supporting applications across paperboard, plastics, and aluminum foils. The growth of recyclable and compostable packaging formats is driving the development of bio-based and water-borne liquid adhesives that maintain performance while meeting global sustainability standards.

The building and construction sector is another major market, where liquid adhesives are used for flooring, tiling, panel bonding, and sealing applications. Their role in modular construction, infrastructure repair, and insulation continues to expand, driven by urbanization and green building initiatives. In the automotive and transportation sector, liquid adhesives are gaining prominence in lightweight bonding, battery assembly, and vehicle interiors, replacing traditional fasteners to improve fuel efficiency and safety. The woodworking and furniture industry remains a core segment, leveraging liquid adhesives for cabinetry, veneer bonding, and edge laminations, with increased adoption of low-emission and water-resistant formulations.

The electronics and healthcare industries are emerging as high-value segments, utilizing liquid adhesives in semiconductor encapsulation, circuit bonding, and medical device assembly, where biocompatibility, transparency, and sterilization resistance are critical. Meanwhile, the industrial assembly and consumer/DIY markets sustain consistent demand for multipurpose adhesives used in repairs, appliances, and footwear manufacturing.

The competitive structure of the Global Liquid Adhesives Industry is defined by technological advancement, application diversity, and sustainability integration. Leading players such as Henkel, 3M, Sika, H.B. Fuller, and Dymax dominate due to their broad formulation range, application-specific expertise, and global R&D and manufacturing networks.

Henkel maintains global leadership in industrial liquid adhesives through its renowned LOCTITE® brand. With over 5,000 active formulations, it supports industrial MRO, electronics assembly, and construction applications. Henkel’s LOCTITE Pulse IIoT platform integrates adhesive monitoring and predictive maintenance within smart factories. Its E-Mobility portfolio features thermally conductive gap fillers and liquid encapsulants optimized for EV battery modules. The company is also pioneering bio-based PUR adhesives for structural timber and sustainable construction.

3M offers an extensive range of Scotch-Weld™ liquid structural adhesives, including epoxies, methyl methacrylates (MMAs), and urethanes, catering to automotive and aerospace Body-in-White applications. Its Bonding Process Center enables real-time collaboration with engineering clients for process optimization. 3M’s electronics adhesives—engineered for impact resistance and waterproofing—support next-generation smartphones and wearables. With over 60,000 adhesive SKUs, 3M integrates flexible liquid bonding solutions for everything from interior trim to consumer electronics encapsulation.

Sika’s Sikaflex® and SikaPower® brands are globally recognized for elastic and structural liquid bonding. Its Purform® technology, a low-monomer polyurethane system, is revolutionizing worker safety and REACH compliance in construction and transportation adhesives. Sika’s SikaPower® epoxies and SikaFast® acrylics, with SmartCore® toughening technology, provide unmatched fatigue resistance in metal-to-composite bonding. The company’s Sikadur® epoxies dominate bridge construction and repair, while SikaMelt® systems support vehicle assembly and energy-efficient construction sealing.

H.B. Fuller continues to lead with its Rakoll® and Swift® brands in woodworking and industrial lamination. The company’s water-based polymer adhesives enhance recyclability in flexible packaging, while its urethane and epoxy systems address the needs of EV assembly, roofing, and glass bonding. H.B. Fuller’s R&D Centers of Excellence work collaboratively with manufacturers to accelerate adhesive development cycles and tailor liquid formulations for automation. Its global innovation in liquid hot melt and reactive polyurethane positions it at the forefront of industrial bonding transformation.

Dymax Corporation specializes in UV/LED light-curable liquid adhesives, serving the medical, electronics, and optical device industries. Its one-part systems achieve instantaneous curing under light exposure, ideal for automated dispensing and zero-waste production environments. Dymax’s adhesives feature biocompatibility, low-outgassing, and sterilization resistance, making them indispensable in medical device assembly. By offering both adhesives and integrated curing systems, Dymax delivers turnkey bonding solutions tailored to precision manufacturing.

Liquid Adhesives Market Report Scope

Liquid Adhesives Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$71.2 Billion

|

|

Market Size (2034)

|

$105.8 Billion

|

|

Market Growth Rate

|

4.5%

|

|

Segments

|

By Technology (Water-Based, Solvent-Based, Reactive, Others), By Chemistry (Acrylic Copolymers, Polyurethanes (PU), Epoxies, Cyanoacrylates, Silicone), By End-Use Industry (Packaging, Building & Construction, Automotive & Transportation, Medical & Healthcare, Woodworking & Furniture, Electronics, Consumer/DIY

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Henkel AG & Co. KGaA, 3M Company, H.B. Fuller Company, Dow Inc, Sika AG, Arkema S.A. (Bostik) , Avery Dennison Corporation, Huntsman Corporation

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Liquid Adhesives Market Segmentation

By Technology/Formulation

- Water-Based

- Solvent-Based

- Reactive

- Others

By Chemistry (Resin Type)

- Acrylic Copolymers

- Polyurethanes (PU)

- Epoxies

- Cyanoacrylates

- Silicone

VAE/EVA

By End-Use Industry

- Packaging

- Building & Construction

- Automotive & Transportation

- Medical & Healthcare

- Woodworking & Furniture

- Electronics

- Consumer/DIY

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in the Global Liquid Adhesives Market

- Henkel AG & Co. KGaA

- 3M Company

- H.B. Fuller Company

- Dow Inc

- Sika AG

- Arkema S.A. (Bostik)

- Avery Dennison Corporation

- Huntsman Corporation

*- List not Exhaustive

Research Coverage

USDAnalytics delivers an executive-grade examination of the Global Liquid Adhesives Market, where this report investigates how e-mobility, sustainability, and automation are reshaping resin selection, curing strategies, and end-use qualification; captures breakthroughs in UV/LED light-cure, water-borne dispersions, and low-monomer polyurethane platforms; analysis reviews expansion moves, capacity adds, and compliance pivots across regions; and highlights the performance–safety trade-offs that govern bonding of metals, plastics, composites, and elastomers in high-throughput manufacturing. Anchored in specification-level metrics (lap-shear, elongation, thermal cycling endurance) and procurement realities (price/mix, cure windows, VOC thresholds), this report is an essential resource for product managers, sourcing leaders, process engineers, and QA/RA teams aligning 2025–2034 investment and compliance roadmaps with REACH/EPA mandates, Industry 4.0 automation, and EV lightweighting demand.

Scope Highlights

Segmentation (covered in this study):

- By Technology/Formulation: Water-Based; Solvent-Based; Reactive; Others

- By Chemistry (Resin Type): Acrylic Copolymers; Polyurethanes (PU); Epoxies; Cyanoacrylates; Silicone; VAE/EVA

- By End-Use Industry: Packaging; Building & Construction; Automotive & Transportation; Medical & Healthcare; Woodworking & Furniture; Electronics; Consumer/DIY

- By Region: North America (United States, Canada, Mexico); Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe); Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC); South & Central America (Brazil, Argentina, Rest of SCA); Middle East & Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Geographic Scope: Analysis spans 25+ countries across North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa.

Timeframe: Historic data 2021–2024 and forecasts 2025–2034.

Companies: Deep-dive analysis/profiles of 15+ companies.

Deliverables

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.