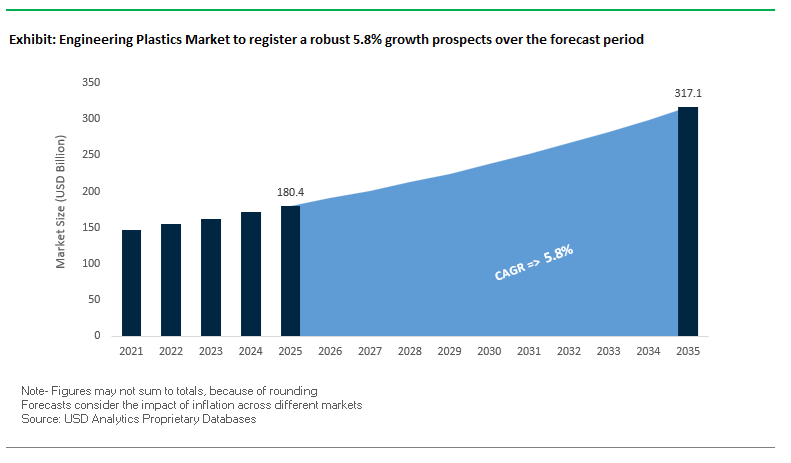

The Engineering Plastics Market, valued at USD 180.4 billion in 2025, is forecast to grow to USD 317 billion by 2035, expanding at a steady CAGR of 5.8%. Growth is driven by global megatrends including automotive lightweighting, the electrification of mobility, semiconductor purity requirements, structural integration in large molded parts, and aggressive sustainability targets across consumer, electronics, medical, and industrial sectors.

The engineering plastics industry is undergoing rapid transformation as automotive electrification, semiconductor scaling, medical device miniaturization, and sustainability commitments reshape global materials demand. Polymer manufacturers and OEMs are increasingly investing in high-heat engineering resins, lightweight composite alternatives, and sustainable feedstock integration. In January 2026, Mitsui Chemicals and Polyplastics began coordinated marketing operations for high-performance resins including ARLEN® Polyamide and AURUM® Thermoplastic Polyimide, aiming to expand penetration in automotive, electronics, and electrical systems requiring extreme thermal resistance. Meanwhile, sustainability leadership continues to differentiate market players; Covestro surpassed 10 million carbon credits in November 2025, reinforcing its commitment to decarbonizing polycarbonate and precursor value chains through pioneering nitrous oxide abatement technologies.

Innovation for e-mobility and large-part molding advanced significantly in October 2025 with SABIC launching its MEGAMOLDING platform, integrating material science, simulation, and data-driven design for large thermoplastic components including EV battery housings. In September 2025, BASF expanded its Ultramid® and Ultradur® compounding capacity in India by an estimated 40%, aligned with rising automotive and electronics production under regional PLI schemes and local semiconductor initiatives. The expansion strengthens the engineering plastics supply chain in Asia-Pacific, the fastest-growing region for high-performance polymers.

Healthcare and sustainable materials also gained momentum. DuPont acquired Donatelle Plastics in August 2025, enhancing its capabilities in producing biocompatible, precision-molded components for medical devices using high-performance plastics. Arkema’s investment in bio-based specialty polypropylene in May 2025 highlights the increasing commercial availability of renewable-source engineering polymers for consumer and industrial goods. Vertical integration strengthened further when Covestro acquired two Vencorex sites in April 2025, expanding production flexibility for specialty isocyanates used in thermoplastic polyurethanes (TPUs). Supporting building materials sustainability, Lanxess launched Levagard 2100 in March 2025, a reactive phosphorus-based flame retardant designed for chemically bonded, low-VOC insulation polymers—showcasing how regulation-driven material innovation is becoming a decisive market force.

Market Insights: Engineering Plastics Demand Accelerates with Lightweighting, Thermal Stability, and Circular Material Adoption

Engineering plastics including polyamides, polycarbonates, high-performance polyesters, fluoropolymers, PPAs, and long-fiber thermoplastics are increasingly central to achieving design optimization and system integration. The push for sustainable engineering plastics, where at least 25% of polymer grades contain recycled or bio-based feedstock, is fundamentally reshaping procurement decisions. Performance thresholds—like continuous operation above 150–200°C for EV power electronics—are moving the market toward thermally robust specialty polyamides and PPAs. Meanwhile, semiconductor purity requirements demanding <10 ppb extractable metal ions in fluoropolymers further highlight how engineering plastics underpin next-generation chip manufacturing.

- Automotive lightweighting initiatives enable a 20–50% weight reduction when metal components are replaced with high-performance engineering plastics, directly supporting EV range extension and fuel efficiency.

- Polyphthalamides (PPAs) and specialty polyamides withstand 150–200°C, enabling their use in EV power modules, battery housings, and under-the-hood environments.

- 25%+ of leading polymer producers’ portfolios include circular or bio-based materials, reinforcing sustainability as a top-tier procurement criterion.

- Long-fiber reinforced thermoplastics (LFRT) reduce assembly time and cost by up to 30%, consolidating multiple metal parts into a single molded component.

- Fluoropolymers for semiconductor production meet <10 ppb metal ion limits, ensuring purity, yield, and long equipment lifespans in advanced chip fabs.

Trend 1 - Engineering Plastics Drive Metal Replacement in EV Structural, High-Voltage, and Powertrain Systems

The global shift toward lightweight EV architecture is accelerating the adoption of engineering plastics in structural and high-load powertrain components, replacing metal to enhance efficiency, performance, and system-level integration. This trend is underpinned by robust empirical validation and OEM collaborations.

According to the U.S. Department of Energy (DOE), replacing cast iron and steel with lightweight materials-including glass fiber-reinforced engineering plastics-can reduce the body and chassis weight of a vehicle by up to 50%, dramatically improving EV range. Because battery mass is a fixed constraint, every 1% of vehicle weight reduction directly cuts electricity consumption by approximately 1%, making polymer substitution a quantifiable energy-efficiency enabler.

Leading material suppliers are driving commercialization of high-performance alternatives. Victrex’s PEEK solutions have demonstrated the ability to replace metal gears in demanding transmission systems, delivering up to 50% reduction in Noise, Vibration, and Harshness (NVH). This not only enhances efficiency but expands the applicability of engineering plastics into torque-critical and wear-intensive EV environments.

High-voltage systems highlight another pivotal area. Modern 800V e-motors require insulation materials capable of both electrical and thermal endurance. PEEK-based film slot liners allow up to 2% more copper fill, enabling a 5% improvement in continuous torque output, demonstrating the direct performance gains enabled by advanced plastics in high-energy-density applications.

Cost efficiency further strengthens the value proposition. Engineering plastics enable multi-functional integration-such as molding a complex battery cover section with integrated fastening points, seals, and heat management features-reducing both the component count and assembly time. This combination of weight savings, thermal reliability, mechanical durability, and cost reduction is firmly positioning engineering plastics as a core material category for next-generation EV platforms.

Trend 2 - High-Heat Engineering Plastics Become Mission-Critical for 5G Thermal and Electrical Performance

As electronics architectures shift to high-frequency, high-power-density designs-particularly in 5G Massive MIMO radios, radomes, and connectors-the need for thermally stable, electrically precise engineering plastics is escalating sharply. Thermal hotspots, high current density, and GHz-level electrical demands are driving accelerated qualification cycles for PPS, LCP, PEEK, and other advanced thermoplastics.

Polyphenylene Sulfide (PPS) remains a cornerstone due to its exceptional thermal stability. With decomposition temperatures above 500°C, long-term service temperatures exceeding 220°C, and ultra-low CLTE, PPS maintains dimensional stability under continuous heat exposure. This makes PPS indispensable for 5G connectors, RF housings, and antenna radomes where mechanical distortion must be avoided to preserve signal performance.

Liquid Crystal Polymers (LCPs) further enable high-frequency signal integrity. With dielectric constants as low as 2.9 at 10 GHz and dielectric losses as low as 0.0025, LCPs significantly minimize attenuation and reflection-critical advantages for 5G antenna arrays, high-speed connectors, and mmWave components used in user devices and base stations.

Engineering plastics are increasingly serving dual-purpose functions in thermal management. PEEK, PPS, and related high-heat thermoplastic compounds can be blended with thermally conductive fillers to simultaneously deliver electrical insulation and effective heat dissipation. For high-power 5G base stations, this multifunctional capability reduces reliance on metal heat spreaders, enabling lighter, more integrated system designs.

This migration toward high-heat, high-frequency engineering plastics marks a decisive materials shift, supporting the scalability and reliability of global 5G infrastructure.

Opportunity 1 - Closed-Loop Chemical Recycling Unlocks Circularity for High-Performance Engineering Plastics

Chemical recycling represents a transformative opportunity for engineering plastics, enabling virgin-equivalent polymer recovery from streams that cannot withstand traditional mechanical processing. With EV, electronics, and industrial applications generating complex, contaminated waste streams, chemical recycling is emerging as an essential technology for long-term material circularity.

A study by the European Commission Joint Research Centre (JRC) confirms that chemical recycling is a critical complement to mechanical recycling, particularly for mixed or contaminated waste streams typical of end-of-life engineering plastics. Unlike mechanical recycling, chemical depolymerization allows recovery of monomers without property degradation, ensuring suitability for high-performance re-manufacturing.

Environmental benefits are substantial. Recycling one ton of engineering plastics can prevent up to 2.5 tons of CO₂ equivalent compared with producing virgin fossil-based polymers-an impact scale that aligns with stricter sustainability objectives across automotive, electronics, and industrial supply chains.

Chemical recycling also addresses the industry’s most problematic waste streams, including high-performance polymers with complex additives, fiber-reinforced materials, and multi-material assemblies. European industry roadmaps highlight pyrolysis and advanced solvent-based processes as key technologies to unlock circularity for engineering plastics used in EV battery systems, high-temperature connectors, and electronic housings.

As policies and ESG commitments intensify across global supply chains, chemical recycling provides engineering plastics manufacturers with a high-value opportunity to deliver low-carbon, circular materials meeting the mechanical and thermal demands of high-performance applications.

Opportunity 2 - Development of Intrinsically Flame-Retardant, Halogen-Free Engineering Plastics for Global Safety Compliance

Growing restrictions on halogenated flame retardants and the need for high-purity, high-strength polymers in automotive, electrical, and telecom systems are creating strong demand for intrinsically flame-retardant (FR) engineering plastics. These materials must achieve regulatory ratings-including UL 94 V-0 and 5VA-without compromising performance or introducing hazardous chemicals.

Global safety and eco-regulatory frameworks drive this momentum. The UL 94 flammability standard, harmonized with IEC norms, mandates stringent burn and self-extinguishing requirements for critical components used in EV under-hood systems, switchgear, telecom hardware, industrial automation, and consumer electronics. Achieving these ratings without halogenated additives is now a key OEM requirement.

Material suppliers are rapidly scaling non-halogen technologies. Avient, among other compounders, is expanding its portfolio of Non-Halogen Flame Retardant (NHFR) polymers capable of meeting UL 94 V-0 and 5VA standards while maintaining mechanical strength and processability for extrusion and injection molding. These materials align with circularity objectives and emerging extended producer responsibility (EPR) mandates.

Importantly, certain engineering plastics-especially specific grades of Polyphenylene Sulfide (PPS)-possess inherent flame resistance due to their molecular structure. These materials can achieve UL 94 V-0 without added FR fillers, preserving dielectric strength, chemical resistance, and high-temperature durability. This intrinsic FR behavior is extremely attractive for applications demanding long-term reliability and uncompromised material purity.

Engineering Plastics Market Share Analysis

Market Share by Form/Additive: Glass Fiber Reinforced Plastics Lead Through Superior Strength, Heat Resistance, and Dimensional Stability

Glass Fiber Reinforced Plastics (GFRP) command the highest 30% share in the Engineering Plastics Market, driven by their unmatched ability to enhance the mechanical, thermal, and structural performance of base polymers at an economically scalable level. As industries transition away from metal-intensive designs, GFRP emerges as the most versatile reinforcement technology because the incorporation of glass fibers can boost tensile strength by 1.5× to 3×, enabling polymers such as PA6, PA66, and PBT to replace aluminum or steel in numerous load-bearing applications. This dramatic improvement in strength-to-weight ratio is a key driver of adoption across automotive, electrical, and industrial segments seeking structural durability without added mass. The reduction in Coefficient of Thermal Expansion (CTE) by 3× to 5× further positions GFRP as indispensable in high-precision components, particularly where plastics must maintain metal-like dimensional stability under thermal cycling, such as engine bay components or under-the-hood housings. Equally important is the significant enhancement in Heat Deflection Temperature (HDT)—often increasing by 50% to 100%—which enables GFRP compounds to withstand elevated temperatures in EV power electronics, high-voltage connectors, and high-power motors. These performance advantages, combined with mature processing technologies like injection molding and consistent supply chain availability, drive GFRP’s leading market share and reinforce its status as the foundational reinforcement in advanced engineering plastics.

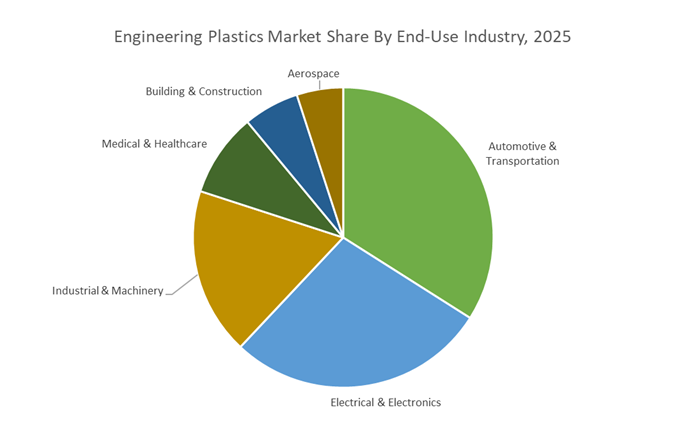

Market Share by End-Use Industry: Automotive & Transportation Dominates Through Lightweighting, Part Consolidation, and EV-Centric Demand

Automotive & Transportation accounts for the largest 34% share of engineering plastics demand, reflecting the sector’s aggressive pursuit of lightweighting and its accelerated investments in electric vehicle (EV) platforms. Engineering plastics deliver immediate value by reducing vehicle mass, with a 10% weight reduction improving fuel economy by ~6% in internal combustion vehicles and increasing driving range in battery electric vehicles by up to 14%. This direct correlation between weight reduction and energy efficiency makes advanced polymers essential in achieving OEM emissions targets, regulatory compliance, and EV range optimization. Furthermore, engineering plastics enable part consolidation, allowing complex assemblies traditionally made of several metal components to be replaced by a single molded part. This reduces not only weight but also manufacturing costs, assembly labor, and system complexity—critical advantages in large-scale automotive production.

In electric vehicles, demand intensifies due to stringent safety, insulation, and thermal management requirements. High-performance materials—often flame-retardant and UL 94 V-0 rated—are indispensable in battery module housings, cell spacers, and high-voltage connectors, where they prevent thermal runaway, ensure dielectric integrity, and improve heat dissipation. As EV architectures become more compact and power-dense, the need for engineering plastics with superior mechanical strength, chemical resistance, and electrical insulation continues to rise, reinforcing the automotive sector’s dominant share. Moreover, global transitions toward autonomous driving, electrified powertrains, and advanced sensor integration further expand the use of engineering plastics in radar housings, connector systems, and structural lightweight components, ensuring that Automotive & Transportation remains the leading end-use category in the market.

Country Analysis: Global Engineering Plastics Innovation Hubs

China: Policy-Led Engineering Plastics Expansion Driven by EV Lightweighting and Semiconductor Localization

China remains the epicenter of global engineering plastics demand, underpinned by sweeping national industrial policies and explosive growth in its electric vehicle (EV) and electronics manufacturing base. Government directives supporting Liquid Crystal Polymer (LCP) film manufacturing for IC substrates are tightly linking the telecommunications and semiconductor industries with the engineering plastics ecosystem. This policy push is reinforcing the domestic supply of Polyamides, Polycarbonate, ABS, and high-temperature specialty resins, enabling China to reduce its dependence on imported intermediates and raise competitiveness in high-end applications. The country's leadership in New Energy Vehicle (NEV) production—now a structural growth engine—has prompted OEMs to specify advanced Polycarbonate and Polyamide compounds for structural components, connectors, glazing, and under-hood applications aimed at reducing vehicle weight and improving energy efficiency.

Investment flows from global majors further accelerate China’s scaling capacity. Companies like BASF and SABIC have expanded production within China, with SABIC signing an agreement with the Fujian government to build a compounding facility tailored to the automotive, consumer electronics, and industrial sectors. Between 2020 and 2024, China added over 3 million tons per year of ABS and Polycarbonate capacity, intensifying domestic competition and lowering production costs. Growing tax incentives for service robotics are reshaping demand for UL 94 V-0 polyamides, impact-resistant polycarbonates, and tight-tolerance compounds, while the national localization mandate pushes resin manufacturers upstream into key monomer production to support high-temperature, flame-resistant engineering plastics. This combination of industrial policy, massive manufacturing scale, and aggressive R&D investment solidifies China's role as the world’s most influential engineering plastics growth hub.

Germany: Precision Engineering Driving Multimaterial Lightweighting and High-Performance Polyamide Innovations

Germany stands at the forefront of multimaterial lightweighting technologies, leveraging its dominant automotive and precision mechanical engineering sectors to advance demand for high-performance Polyamide, Polycarbonate, and composite-based engineering plastics. Supported by the Federal Ministry for Economic Affairs and Climate Action, Germany’s national Lightweighting Strategy recognizes polymer–composite systems as a critical enabler for industrial modernization, particularly in electrification and next-generation mobility solutions. This vision has catalyzed innovation among material suppliers—exemplified by Envalior’s (formerly DSM/LANXESS) recognition at the SPE Grand Innovation Awards 2025 for a fully recyclable composite roof cap replacing conventional metal structures in premium convertibles. The breakthrough demonstrates Germany’s leadership in designing structural Polyamide composites with mechanical strength, durability, and recyclability aligned with EU circular economy standards.

Germany’s EV ecosystem is further advancing polymer-metal hybrid solutions, including a collaborative project between Envalior and SABIC that produced a next-generation hybrid composite battery cover using a PP-glassfiber laminate with a flame-retardant core, dramatically improving battery enclosure safety and structural efficiency. The EU’s increasing regulatory pressure—such as new ecodesign and recyclability mandates—is accelerating the transition toward engineering plastics that support circularity targets in vehicle and industrial equipment manufacturing. Simultaneously, Germany’s industrial automation sector generates strong demand for dimensionally stable, low-friction engineering plastics used in sensors, gears, actuators, and robotic systems operating under high precision. This synergy between engineering excellence, regulatory frameworks, and sustainable design principles positions Germany as a global leader in high-value engineering plastics applications.

Japan: Global Pioneer in Super Engineering Plastics for Miniaturized Electronics and High-Temperature Applications

Japan maintains global leadership in Super Engineering Plastics, driven by its dominance in high-reliability electronics, medical devices, and semiconductor manufacturing. The country’s aggressive 5G deployment and capital expenditure incentives have dramatically accelerated demand for LCP and Polyimide films, which are essential for flexible printed circuits, millimeter-wave antenna modules, and high-frequency device packaging. These materials offer exceptional dielectric stability and heat resistance, making them central to Japan’s telecommunications and semiconductor competitiveness. Japanese innovation extends to ultra-high-performance polymers such as PEEK and PEI, with companies like Mitsubishi Chemical Group developing grades engineered for semiconductor back-end sockets that withstand reflow temperatures up to 260°C, ensuring dimensional stability and long-term reliability.

Japan’s material science ecosystem continues to focus on next-generation Polyamides and advanced Fluoropolymers, particularly as global regulatory pressure intensifies around PFAS phase-out and environmental compliance. This R&D emphasis is complemented by advancements in high-precision processing technologies, such as Daicel Corporation’s work in powdering engineering plastics for high-accuracy 3D printing, enabling rapid prototyping for medical, aerospace, and optoelectronic components. Japan also leads in high-temperature insulation materials through companies like Daikin Industries, supplying essential Fluoropolymers used in EUV lithography equipment, ultra-reliable cable insulation, and extreme-environment electronics. This specialization places Japan firmly at the center of global innovation for engineering plastics that require exceptional heat tolerance, dielectric performance, and long-term reliability.

Saudi Arabia: Engineering Plastics Expansion Fueled by Vision 2030 and Global Circular Economy Initiatives

Saudi Arabia is rapidly emerging as a strategic production hub for engineering plastics, driven by SABIC’s global footprint, rising domestic industrialization, and the national Vision 2030 transformation agenda. A key focus is outward expansion, highlighted by SABIC’s investment in China through a planned thermoplastic compounding plant in Fujian, designed to produce Polycarbonate and CYCOLOY blends for the rapidly growing automotive and 5G electronics sectors. This cross-border capacity expansion enhances Saudi Arabia’s influence in the global engineering plastics value chain. Domestically, the country is making significant progress in circular economy initiatives—SABIC’s April 2024 circular packaging product launch, which repurposes post-consumer plastics into specialty bread packaging materials, exemplifies its commitment to sustainable polymer innovation.

The nation is also strengthening local polymer conversion through corporate partnerships, such as the 2024 MoU between Alujain Corporation and Samvardhana Motherson International Ltd., aimed at manufacturing high-value engineering compounds within Saudi Arabia. Massive infrastructure projects—NEOM, the Riyadh Metro, and multi-billion-dollar urban mobility developments—are driving strong demand for lightweight, flame-retardant, impact-resistant engineering plastics for construction, transportation, and smart city applications. In electronics, SABIC’s introduction of the bio-based LNP ELCRIN EXL7414B copolymer reflects ongoing commitment to sustainability, providing low-carbon solutions for consumer electronics manufacturers pursuing net-zero emissions. Saudi Arabia’s expanding capacity, coupled with its circular economy progress and global strategic investments, positions it as a rising center of engineering plastics innovation and manufacturing.

Competitive Landscape: Global Leaders Advancing High-Heat Polymers, Circular Materials, and EV-Ready Composites

The competitive landscape in the Engineering Plastics Market is shaped by global polymer producers expanding their high-heat resin portfolios, integrating circular feedstocks, strengthening regional production networks, and pursuing vertical integration to secure supply chain resilience. Leading companies are prioritizing lightweight automotive structures, EV powertrain plastics, sustainable polycarbonate and polyamide systems, and high-purity materials for semiconductor and medical applications. These strategies reflect a shift toward multifunctional polymer systems that offer mechanical strength, thermal endurance, electrical insulation, and sustainability advantages over traditional materials.

SABIC maintains a leading position in high-heat and circular engineering plastics through its polycarbonate (LEXAN™), Ultem™ (PEI), and high-performance thermoplastic offerings. With strong alignment to e-mobility through its BLUEHERO program, SABIC provides solutions for EV battery modules, structural housings, and charging infrastructure components. Its TRUCIRCLE™ circularity platform continues to expand recycled and bio-based engineering plastics, while its long-term commitment to reduce GHG emissions by 30% by 2030 reinforces its sustainability leadership.

BASF is a major supplier of polyamides and thermoplastic polyesters including Ultramid® (PA) and Ultradur® (PBT), supported by its advanced Ultrasim® CAE engineering tools for application optimization. In 2025, BASF expanded its India compounding plant capacity by 40% to support regional demand from automotive, electronics, and appliance manufacturers. The company continues to grow its low-carbon footprint (LCF) engineering plastics and biopolymer portfolio, reinforcing its commitment to sustainable materials development.

DuPont delivers a wide range of specialty materials including Zytel® (PA), Delrin® (POM), and high-purity fluoropolymers required for semiconductor manufacturing, aerospace systems, and advanced medical applications. Its August 2025 acquisition of Donatelle Plastics strengthens its position in precision medical molding, enabling deeper vertical integration in biocompatible plastics. DuPont’s expertise in high-temperature polymer chemistry continues to support next-generation 5G, EV, and aerospace platforms.

Covestro is a leading producer of Makrolon® polycarbonates and specialty thermoplastic polyurethanes (TPUs), with a strategic focus on fully circular material systems. Its €100+ million R&D investments and recent progress in nitrous oxide abatement demonstrate a measurable commitment to lowering Scope 1 emissions. Covestro’s recycled-content polycarbonate grades are rapidly being adopted in electronics, LED lighting, and consumer goods, supporting OEM goals for recycled content integration.

Mitsubishi Chemical provides high-performance acrylics, polycarbonate grades, and specialty films including SUPERIO™ PEEK/PEI films used in aerospace, optics, and flexible electronics. The company is known for its innovation in high-heat and high-purity films essential for medical devices, dental systems, and electronic displays. Mitsubishi Chemical’s polymer platforms support applications requiring regulatory compliance, optical clarity, and mechanical endurance.

Lanxess is well established in performance polymers and additives, including PA6 and PBT engineering plastics, supported by a highly integrated value chain. Its strategic joint ventures have created a powerful platform for supplying high-performance engineering plastics to the global automotive and industrial sectors. The 2025 launch of Levagard 2100 reinforces Lanxess’s leadership in flame retardants for insulation materials, enabling low-VOC, durable polymer systems designed for energy-efficient buildings and EV components.

Engineering Plastics Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$180.4 Billion

|

|

Market Size (2035)

|

$317 Billion

|

|

Market Growth Rate

|

5.8%

|

|

Segments

|

By Resin Type (Standard Engineering Plastics, High-Performance Polymers, Specialty Plastics), By Form/Additive (Virgin Resin, Recycled/Bio-Based Polymers, Fiber-Reinforced Plastics, Mineral-Filled Compounds, Flame-Retardant Grades, Compound/Alloy Blends), By End-Use Industry (Automotive & Transportation, Electrical & Electronics, Industrial & Machinery, Medical & Healthcare, Aerospace, Building & Construction), By Application Function (Structural Components, Tribological Parts, Thermal Management, Electrical Insulation, Chemical Resistance)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

BASF SE, Covestro AG, SABIC, Celanese Corporation, DuPont de Nemours Inc., Victrex plc, Mitsubishi Chemical Group, Asahi Kasei Corporation, Solvay S.A., Lanxess AG, Envalior, Polyplastics Co. Ltd., Toray Industries Inc.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Engineering Plastics Market Segmentation

By Resin Type

- Standard Engineering Plastics

- High-Performance Polymers

- Specialty Plastics

By Form/Additive

- Virgin Resin

- Recycled/Bio-Based Polymers

- Glass Fiber Reinforced Plastics (GFRP)

- Carbon Fiber Reinforced Plastics (CFRP)

- Mineral-Filled Compounds

- Flame Retardant Grades (UL 94 V-0)

- Compound/Alloy Blends

By End-Use Industry

- Automotive & Transportation

- Electrical & Electronics

- Industrial & Machinery

- Medical & Healthcare

- Aerospace

- Building & Construction

By Application Function

- Structural Components (Metal Replacement)

- Tribological Parts (Low Friction, Wear-Resistant)

- Thermal Management (Heat Dissipation, Insulation)

- Electrical Insulation

- Chemical Resistance

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies: Key Engineering Plastics Manufacturers

- BASF SE

- Covestro AG

- SABIC

- Celanese Corporation

- DuPont de Nemours, Inc.

- Victrex plc

- Mitsubishi Chemical Group

- Asahi Kasei Corporation

- Solvay S.A.

- Lanxess AG

- Envalior

- Polyplastics Co., Ltd.

- Toray Industries, Inc.

*- List not Exhaustive