Market Overview: Transportation-Led Lightweighting and Fluoropolymer Criticality Are Structurally Expanding the High-Performance Plastics Market

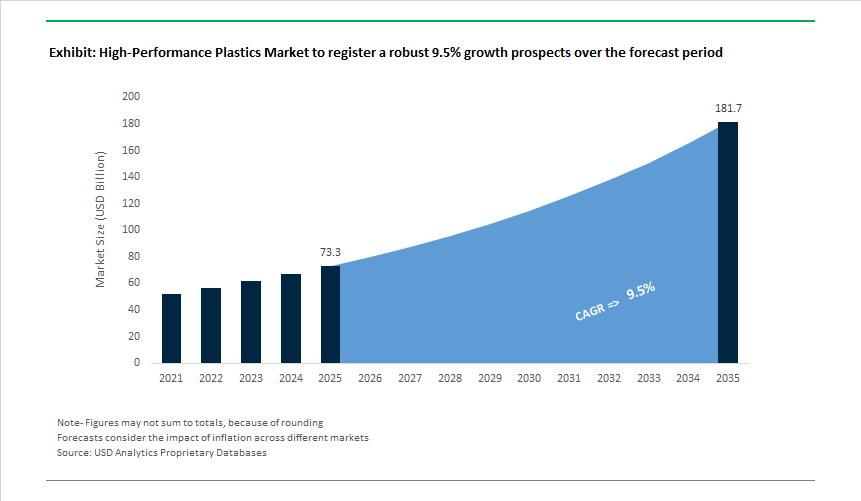

The High-Performance Plastics (HPP) Market (USD 73.3 billion in 2025; projected to reach USD 181.7 billion by 2035 at a 9.5% CAGR) is being structurally reshaped by the convergence of lightweighting mandates, electrification, and rising thermal and chemical performance thresholds across transportation, electronics, and industrial processing. Unlike commodity polymers, HPPs are specified where material failure directly translates into safety risk, yield loss, or regulatory non-compliance, positioning them as enablers of system-level performance rather than cost-driven substitutions.

Transportation remains the dominant demand engine, accounting for approximately 42% of global HPP consumption, as automotive and aerospace OEMs accelerate metal-to-polymer substitution in battery housings, under-the-hood components, structural brackets, fuel and fluid systems, and high-temperature electrical connectors. Materials such as PEEK, PEI, PPS, and LCPs are increasingly selected not only for weight reduction, but for their ability to withstand sustained temperatures above 150-250°C, aggressive chemicals, and repeated thermal cycling without dimensional drift. In electric vehicles in particular, HPPs support platform consolidation by enabling multifunctional parts that integrate electrical insulation, structural support, and thermal stability - reducing assembly complexity and total system mass.

Within the HPP portfolio, fluoropolymers represent the single largest revenue segment (~46.8%), reflecting their non-substitutable role in chemically aggressive and electrically demanding environments. Their combination of chemical inertness, low friction coefficients, and high dielectric strength underpins widespread use in semiconductor fabrication equipment, wire and cable insulation, chemical processing systems, and high-voltage electronics. Regionally, Asia-Pacific accounts for roughly 34% of global HPP consumption, supported by concentrated electronics manufacturing ecosystems, expanding EV production capacity, and continued investment in semiconductor and industrial infrastructure.

Over the forecast period, competitive advantage in the HPP market will be determined by application specificity and supply-chain control, not resin breadth alone. OEMs increasingly favor suppliers that can deliver tightly specified grades with validated long-term performance, tailored compounding for end-use conditions, and consistent global supply. At the same time, regulatory and customer pressure is accelerating development of recycled-content and bio-based HPP formulations, particularly for automotive and electronics platforms with public sustainability commitments. Manufacturers that combine vertical integration, application-focused compounding, and strategic partnerships with Tier-1 OEMs are best positioned to capture premium share as high-performance plastics continue to displace metals in mission-critical systems.

Market Analysis: New Grades, Regional Capacity Moves and Sustainability Pushes Reshaping HPP Supply

Industry activity over the past two years shows simultaneous advances in material innovation, capacity expansion and sustainability. In May 2024, BASF India increased compounding capacity for Ultramid (PA) and Ultradur (PBT) - a move that boosted regional supply by about 40% to meet rising Automotive and E&E demand in India and wider APAC markets. This trend toward localizing high-performance compounding continued into April 2025, when South Korean automakers teamed with material companies on carbon-fiber reinforced HPP composites for weight reduction in vehicle structures, underscoring the material shift in EV platforms.

Product innovation accelerated through 2025: May 2025 saw U.S. aerospace suppliers expand production of high-temperature PEEK and PEI grades for lightweight aircraft interiors and structural parts, addressing both thermal stability and flame-toxicity performance requirements. In July 2025, German producers introduced bio-based HPP grades that lower lifecycle carbon footprints without sacrificing mechanical strength - an explicit response to OEM sustainability targets and regulatory pressure. August 2025 witnessed broader adoption of LCPs by Japanese electronics manufacturers in high-frequency connectors and advanced IC packaging, aligning material selection with the global 5G and semiconductor build-out. Most recently, in September 2025, U.S. chemical manufacturers launched next-generation PEEK and PPS grades optimized for extreme environments, reinforcing a market push toward higher performance resins for aerospace, industrial and electronic applications.

High-Performance Plastics Market Trends and Opportunities

Market Trend 1: Direct Substitution of Metals in EV Battery & E-Drive Systems

The acceleration of electric vehicle platform redesigns is structurally shifting material selection away from metals toward high-performance plastics that combine lightweighting, flame retardancy, and electrical insulation. According to the U.S. Department of Energy, substituting metals with advanced plastics and composites can improve vehicle efficiency or driving range by 6–8%, a gain that becomes decisive as OEMs compete on battery size without increasing curb weight. During 2024–2025, Indian OEMs such as Mahindra and Tata Motors integrated next-generation battery packs using high-temperature thermoplastics in cell housings, covers, and busbar insulation to improve crash energy absorption and thermal isolation. Material innovation is enabling this shift at the system level: in late 2023, Solvay launched Ryton® Supreme HF and HV PPS grades engineered for high-voltage EV environments, maintaining dimensional stability and dielectric performance above 200 °C. These polymers outperform aluminum and steel in managing localized heat around inverters and power electronics while eliminating galvanic corrosion risks. From a safety standpoint, industry test data shows polymer-based spacers and enclosures slow thermal runaway propagation by acting as energy-absorbing barriers rather than heat conductors, reducing short-circuit risk during mechanical intrusion events. As EV architectures consolidate components and push toward higher voltages, high-performance plastics are moving from “cost-down alternatives” to mission-critical enablers of range, safety, and manufacturability.

Market Trend 2: Strategic Investment in Bio-Based and Circular Feedstocks

Embedded-carbon regulation and OEM Scope-3 pressure are forcing a fundamental rethink of feedstock strategy across the high-performance plastics value chain. Rather than incremental efficiency gains, chemical majors are reallocating capital toward bio-based and circular raw materials that preserve performance while lowering lifecycle emissions. At its 2025 Capital Markets Day, Evonik Industries AG disclosed plans to generate 50% of revenue from “Next Generation Solutions” by 2030, supported by investments in bio-based high-performance polymers and circular membranes to cut Scope 1 and 2 emissions by 25%. Capacity actions reinforce this direction: in May 2024, BASF expanded compounding capacity for Ultramid® (PA) and Ultradur® (PBT) in India by 40%, explicitly to scale biomass-balance and recycled feedstocks for automotive and electronics customers. Portfolio realignment is also accelerating through M&A; Arkema’s acquisition of a majority stake in PI Advanced Materials integrates bio-based polyimides aligned with energy transition and resource efficiency themes. These moves are not experimental—OEM sourcing contracts increasingly specify carbon-intensity thresholds alongside mechanical performance, making renewable feedstock integration a prerequisite for long-term qualification in mobility, electronics, and energy infrastructure.

Market Opportunity 1: Additive Manufacturing for Aerospace and Medical Parts

The transition of additive manufacturing from prototyping to certified serial production is opening a high-margin growth corridor for high-performance polymer powders and filaments. In aerospace, demand for PAEK-based materials surged in 2024 as OEMs adopted PEEK and PEKK to consolidate multi-part assemblies into single printed structures, reducing fasteners, assembly time, and structural mass. Volume growth of roughly 45% in aerospace AM polymers reflects this shift toward lightweight, topology-optimized components capable of withstanding aggressive thermal and chemical environments. In parallel, the medical sector is commercializing patient-specific implants at scale: during 2024–2025, osteoconductive PEEK filaments enabled 3D-printed spinal cages and surgical guides that combine radiolucency, sterilization resistance, and long-term biocompatibility—capabilities unattainable with metals. Industrial scale-up is now the inflection point. Advances in printer throughput, powder recycling, and automated post-processing are driving down cost-per-part, making AM competitive with CNC machining for low-to-mid-volume aerospace and healthcare production. For polymer producers, this creates a durable demand pocket where material performance, certification support, and application engineering command pricing power.

Market Opportunity 2: Specialty Polymers for Hydrogen Economy Infrastructure

The build-out of green hydrogen ecosystems is creating non-negotiable material requirements that favor high-performance plastics over metals in multiple infrastructure layers. At storage pressures up to 700 bar, Type IV hydrogen tanks rely on polymer liners and composite overwraps to prevent permeation and fatigue—functions conventional engineering plastics cannot reliably deliver. Research funded by the U.S. Department of Energy and HyMARC shows that nanocomposite polymer systems can outperform steel by avoiding hydrogen embrittlement, potentially cutting pipeline lifecycle maintenance costs by 15–20%. Electrolyzers further extend the opportunity set: high-performance sulfonated polymers are central to proton exchange membranes, where chemical stability, conductivity, and mechanical integrity directly influence hydrogen yield and operating life. As hydrogen projects scale from pilots to national infrastructure, material qualification cycles are tightening around durability under cryogenic temperatures, cyclic pressure, and aggressive chemical exposure. This positions specialty polymers not as auxiliary inputs, but as enabling materials that determine safety, efficiency, and bankability across the hydrogen value chain.

Market Share Analysis: High-Performance Plastics Market

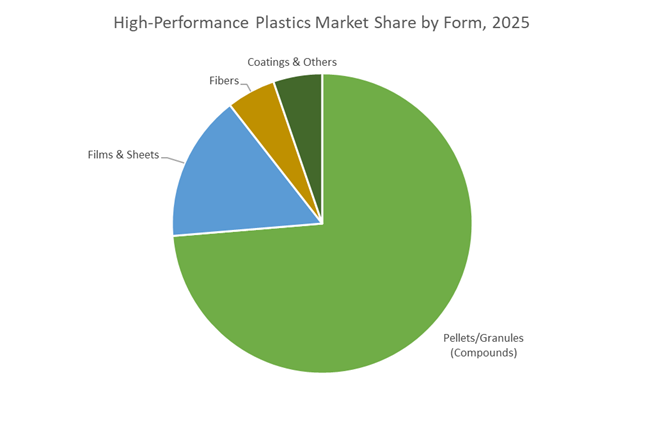

Market Share by Form: Pellets and Granules Anchor Industrial Scalability and Processing Efficiency

Pellets and granules command approximately 70% of the High-Performance Plastics Market because they align precisely with how modern manufacturing is organized—high-throughput, automated, and cost-sensitive. OEMs increasingly favor pre-compounded, ready-to-process high-performance plastic granules over raw polymers or semi-finished forms, as these materials integrate reinforcement, heat stabilization, and flame-retardant performance directly at the resin level. This shift eliminates downstream compounding steps, shortens production cycles, and improves batch-to-batch consistency—critical in regulated industries such as automotive, electronics, and industrial machinery. From a structural standpoint, pellets enable aggressive lightweighting without redesigning existing injection-molding or extrusion infrastructure, allowing manufacturers to substitute metals with minimal capex. Processing efficiency has become a decisive differentiator in 2025, as lower-melting advanced granules reduce energy intensity per part while maintaining extreme thermal and chemical resistance. Equally important, pelletized formats support closed-loop manufacturing and regrind compatibility, strengthening ESG narratives without sacrificing mechanical performance. These combined advantages—manufacturing speed, energy efficiency, design flexibility, and scalable supply chains—explain why pellets and granules remain the dominant commercial form factor in the global high-performance plastics ecosystem.

Market Share by End User: Automotive and Transportation Drive Volume Through Lightweighting and Electrification

Automotive and transportation account for around 30% of total demand, making this segment the single largest end-user of high-performance plastics. Its leadership is structurally linked to two irreversible industry shifts: vehicle lightweighting and electrification. As OEMs face tightening CO₂ regulations and range expectations in electric vehicles, high-performance polymers have moved from secondary materials to core structural and functional components. Advanced plastic compounds now replace metal in powertrain housings, battery enclosures, connectors, and thermal management systems—areas where weight reduction directly translates into efficiency gains and lower lifecycle emissions. The segment’s scale is reinforced by platform standardization: once a polymer compound is qualified for a vehicle architecture, it is deployed across millions of units, locking in long-term resin demand. Fire-retardant and electrically insulating grades have further accelerated adoption in EV platforms, where safety compliance and thermal stability are non-negotiable. Additionally, automotive procurement strategies increasingly prioritize cradle-to-gate carbon reduction, driving uptake of bio-based and low-energy-processed polymers that meet performance parity with fossil-based alternatives. Together, electrification economics, regulatory pressure, and platform-scale material lock-in position automotive and transportation as the most structurally resilient demand pillar for high-performance plastics through the next decade.

Competitive Landscape: Specialty Polymer Leaders Combining Global Scale, Material Breadth and Application-Tailored Solutions

The competitive topology is led by diversified chemicals and specialty polymer groups that pair deep R&D in fluoropolymers and high-temperature thermoplastics with global production footprints and targeted capacity investments. Companies differentiate on resin grade breadth (PEEK, PAI, PPS, LCPs), compounding and coloring capabilities, circularity programs, and close OEM partnerships in mobility, aerospace and semiconductor sectors.

BASF SE: Broad Engineering-Plastic Portfolio and India Capacity Surge To Capture Automotive and E&E Demand

BASF offers an integrated suite of engineering plastics-Ultramid (PA), Ultradur (PBT), Ultrason (PAES)-and is focused on novel PPA grades for high-end automotive and industrial applications. The company executed a 40% production capacity increase in India (May 2024) to supply regional automotive and electronics manufacturers, strengthening its position in Asia-Pacific. Strategic collaborations (e.g., with Avient) to deliver colored high-performance polymers highlight BASF’s aim to provide application-ready compounds for electrical, healthcare and mobility markets.

Solvay S.A.: Specialty Polymer Leader With PEEK, PAI and PPS Lines Targeted At Electric Mobility and Aerospace

Solvay’s KetaSpire PEEK, Torlon PAI and Ryton PPS form the backbone of its high-temperature, lightweight composite solutions. The company launched two Ryton PPS grades in Oct 2023 designed for electric mobility battery and powertrain needs, illustrating Solvay’s focus on polymer solutions that improve battery performance and vehicle range. With an extensive global network of production sites and R&D centers, Solvay supports customers across automotive, aviation and healthcare sectors with tailored high-performance materials.

Arkema S.A.: Polyimide Film Strength and Circularity Initiatives Expand HPP Reach Into Electronics and Mobility

Arkema broadened its high-performance film capability by acquiring a 54% stake in PI Advanced Materials (Dec 2023), enhancing its polyimide film portfolio for flexible displays and EV battery components. Its Kynar fluoropolymers, Rilsan polyamides and Pebax materials target lightweight, durable and bio-based applications. Arkema’s Virtucycle recycling program and investments in recycled polyamides underscore a strategic push toward material circularity in HPP supply chains.

Evonik Industries AG: PEEK and Polyamide Innovation With Additive-Manufacturing Specialization

Evonik is known for VESTAKEEP PEEK and VESTAMID polyamides, with specific emphasis on medical, aerospace and additive-manufacturing use cases. It has advanced PEEK formulations for implantable and high-temperature parts and has scaled PA12 capacity to meet demand for specialized automotive and electronic components. Evonik’s dedicated 3D-printing materials center accelerates qualification of HPPs for additive manufacturing, enabling rapid prototyping and low-volume production in critical sectors.

Dupont: Fluoropolymer Dominance and Advanced High-Performance Film and Resin Offerings For Electrification and Semiconductors

DuPont remains a dominant fluoropolymer provider (Teflon®, Vespel®) with unmatched chemical resistance and dielectric properties used across semiconductor, industrial and electrical insulation markets. DuPont’s Zytel nylon, Hytrel elastomers and specialty polyimides support sealing, thermal management and miniaturized electronic components. Ongoing R&D emphasizes next-generation high-performance films and resins to enable miniaturization and higher operating temperatures in advanced electronics and electric mobility systems.

The United States high-performance plastics (HPP) market in 2025 is being structurally reshaped by the convergence of semiconductor policy and advanced materials localization. The establishment of the U.S. Investment Accelerator within the Department of Commerce in March 2025 has redefined how CHIPS Act capital is deployed, explicitly prioritizing die-attach films, liquid crystal polymers (LCPs), fluoropolymers, and high-frequency substrate plastics used in 5G/6G and AI hardware. This oversight shift bridges a long-standing gap between silicon fabs and the polymer supply chains required for high-speed signal integrity and thermal stability.

Parallel executive orders issued in Q1 2025 to secure critical minerals and offshore resources have direct implications for fluoropolymers and high-temperature engineering plastics used in defense electronics and EV powertrains. With approximately USD 39 billion of CHIPS funding allocated toward fab construction—particularly mature-node semiconductors for the automotive sector—the U.S. market is witnessing a sharp rise in demand for under-the-hood (UTH) high-heat plastics, positioning HPPs as strategic infrastructure materials rather than commodity substitutes.

China: Export Controls and Whole-Chain Governance of Strategic Polymers

China’s high-performance plastics strategy has evolved from volume dominance to regulatory and lifecycle control. The MOFCOM export controls effective November 8, 2025, restrict global access to lithium battery equipment and superhard materials, directly impacting the supply of high-performance polymer films and battery separators critical to EV battery stacks. This policy effectively integrates materials into China’s broader geopolitical toolkit.

Domestically, the Plastic Pollution Control Action Plan (2021–2025) has reached its enforcement phase, compelling HPP manufacturers to adopt green polymer design, additive substitution, and advanced recycling compatibility. Capital support reinforces this shift: between 2024 and 2025, 700 billion yuan (USD 98 billion) in ultra-long bonds funded 1,465 major projects, many aimed at domesticating PEEK and PPS production to reach 70% self-sufficiency in strategic new materials, strengthening China’s end-to-end control over high-performance polymer value chains.

Japan: GX 2040 Vision Integrating High-Performance Plastics with 6G and Decarbonization

Japan’s high-performance plastics market is increasingly aligned with national decarbonization and digital infrastructure objectives under the GX 2040 Vision, approved by the Cabinet on January 18, 2025. The strategy emphasizes lightweighting in aerospace, low-dielectric-loss polymers for 6G, and materials that enable both energy efficiency and economic growth—placing advanced polymers at the center of Japan’s industrial future.

In February 2025, Japan Display Inc. demonstrated liquid crystal meta-surface reflectors for 5G/6G signal control, highlighting how specialty functional films and HPPs are converging with telecom hardware. Regulatory reinforcement followed in June 2025, when Japan updated its biodegradability assessment manual, setting new benchmarks for circular high-performance engineering plastics, signaling a shift toward sustainability without compromising advanced functionality.

Germany: Energy Shock Accelerates Pivot Toward Specialty and Circular HPPs

Germany’s HPP sector is undergoing a structural reset driven by energy costs, carbon pricing, and strategic refocusing. At K 2025 (October 2025), industry leaders highlighted Europe’s declining share of global plastics—from 22% in 2006 to 12% in 2024—with high energy prices forcing capacity rationalization. INEOS confirmed closures at its Rheinberg site, including allylics units vital for epoxy resins, underscoring the pressure on commodity polymer production.

In response, Germany is doubling down on high-margin specialty polymers. Late-2025 EU initiatives under the emerging Clean Industrial Deal emphasize CO₂ capture integration and metal-organic frameworks (MOFs) within high-performance polymers to enhance gas storage and emissions reduction. This strategic pivot was reinforced when BASF completed the €8.7 billion carve-out of its surface treatment and coatings division, signaling an industry-wide shift away from volume segments toward advanced, circular HPP solutions.

South Korea: HBM4 Scaling Drives Non-Conductive Film Polymer Leadership

South Korea’s high-performance plastics market is tightly coupled with its leadership in AI-specialized memory, particularly High Bandwidth Memory (HBM). In March 2025, SK hynix began sampling HBM4, a 16-layer architecture that depends on proprietary non-conductive films (NCF) and high-purity polymer systems to ensure mechanical integrity, electrical insulation, and thermal dissipation.

Policy support remains decisive. The USD 471 billion K-Semiconductor Belt entered its second phase in 2025, expanding tax credits for localizing photoresists, LCPs, and polymer precursors previously imported from Japan. Complementing organic growth, Korean firms are pursuing targeted M&A of global R&D specialists in liquid crystal polymers, securing intellectual property critical to the emerging 6G ecosystem and reinforcing Korea’s polymer–semiconductor symbiosis.

India: Component PLI and Infrastructure Demand Catalyze HPP Localization

India is rapidly emerging as a global manufacturing alternative for high-performance plastics, supported by robust domestic demand and targeted incentives. The ₹25,060 crore (USD 3 billion) Component PLI, announced in the 2025 Union Budget, explicitly targets high-performance engineering plastics used in smartphones, servers, and data-center hardware—marking a shift from assembly-centric growth to materials depth.

By September 2025, ₹2 lakh crore (USD 24 billion) in realized PLI investments across 14 sectors catalyzed major capacity expansions, including Saint-Gobain’s ₹3,400 crore technical materials complex in Chennai and Aarti Industries’ expansion into specialty polymers. In parallel, India’s medical device PLI reached a milestone with 21 projects manufacturing MRI and CT components, driving strong domestic demand for biocompatible, radiolucent HPPs such as PEEK and PPS.

2025 Strategic Matrix: High-Performance Plastics by Country

High-Performance Plastics Matrix

|

Country

|

Primary Technical Focus

|

Key 2025 Policy / Event

|

High-Performance Plastic Leadership

|

|

United States

|

AI & defense electronics

|

U.S. Investment Accelerator (CHIPS)

|

LCPs, fluoropolymers, UTH plastics

|

|

China

|

Resource sovereignty

|

MOFCOM export controls (Nov 2025)

|

Battery separators, PPS, PEEK

|

|

Japan

|

Green transformation & 6G

|

GX 2040 Vision approval

|

Low-loss polymers, meta-surfaces

|

|

Germany

|

Decarbonization & specialties

|

K 2025 crisis pivot; Clean Industrial Deal

|

Circular & carbon-capture HPPs

|

|

South Korea

|

AI memory packaging

|

HBM4 sampling by SK hynix

|

Non-conductive films (NCF)

|

|

India

|

Electronics & medical devices

|

₹25,060 Cr Component PLI

|

PEEK, PPS, fluoropolymers

|

High-Performance Plastics Market Report Scope

High-Performance Plastics Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$73.3 Billion

|

|

Market Size (2035)

|

$181.7 Billion

|

|

Market Growth Rate

|

9.5%

|

|

Segments

|

By Material Type (Fluoropolymers, High-Performance Polyamides, Sulfone Polymers, Liquid Crystal Polymers, Polyphenylene Sulfide, Polyaryletherketones, Polyimides), By Form (Pellets/Granules, Films & Sheets, Coatings, Fibers, Others), By Application (Lightweight Structural Parts, Thermal Management, Electrical Insulation, Medical Implants & Instruments, Chemical Processing), By End-User Industry (Automotive & Transportation, Electrical & Electronics, Industrial, Medical & Healthcare, Defense & Space)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

BASF SE, Solvay S.A., Evonik Industries AG, SABIC, Victrex plc, DuPont de Nemours Inc., Toray Industries Inc., Mitsubishi Chemical Group, Arkema S.A., Celanese Corporation, Covestro AG, Sumitomo Chemical Co. Ltd., Kuraray Co. Ltd., Teijin Limited, Daikin Industries Ltd.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

High-Performance Plastics Market Segmentation

By Material Type

- Fluoropolymers

- High-Performance Polyamides

- Sulfone Polymers

- Liquid Crystal Polymers

- Polyphenylene Sulfide

- Polyaryletherketones

- Polyimides

By Form

- Pellets/Granules

- Films & Sheets

- Coatings

- Fibers

- Others

By Application

- Lightweight Structural Parts

- Thermal Management

- Electrical Insulation

- Medical Implants & Instruments

- Chemical Processing

By End-User Industry

- Automotive and Transportation

- Electrical & Electronics

- Industrial

- Medical & Healthcare

- Defense & Space

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in High-Performance Plastics Market

- BASF SE

- Solvay S.A.

- Evonik Industries AG

- SABIC

- Victrex plc

- DuPont de Nemours, Inc.

- Toray Industries, Inc.

- Mitsubishi Chemical Group

- Arkema S.A.

- Celanese Corporation

- Covestro AG

- Sumitomo Chemical Co., Ltd.

- Kuraray Co., Ltd.

- Teijin Limited

- Daikin Industries, Ltd.

*- List not Exhaustive