Market Overview: Superhard Materials Move From Tooling Consumables To Deterministic Performance Enablers

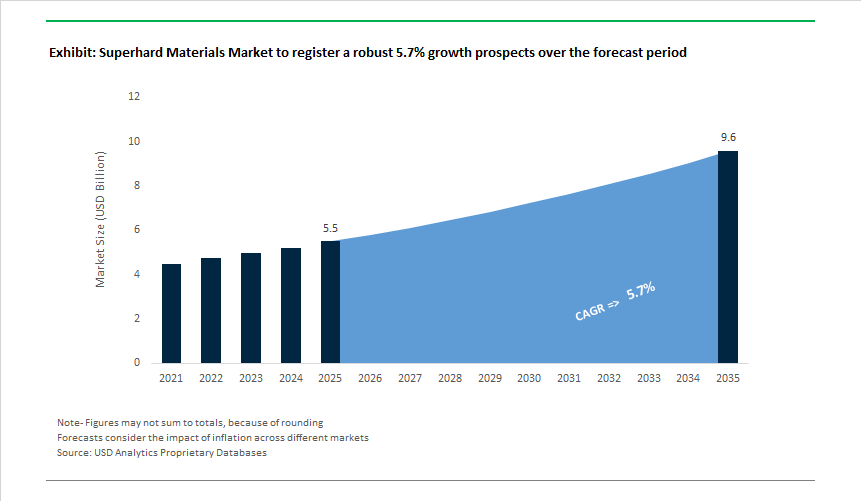

The Global Superhard Materials Market, valued at USD 5.5 billion in 2025, is projected to reach USD 9.6 billion by 2035, expanding at a 5.7% CAGR, as superhard materials transition from niche wear solutions to process-defining materials in advanced manufacturing, energy extraction, and electronics. Growth is no longer volume-led; it is being shaped by measurable performance benchmarks-tool life consistency, thermal survivability above 1,000 °C, and predictable machining economics-that conventional carbides and ceramics are increasingly unable to deliver.

At the core of this shift are synthetic diamond and cubic boron nitride (CBN) platforms engineered through tightly controlled HPHT and CVD manufacturing routes. Leading producers have moved beyond brute hardness as a selling point and are now differentiating on grain-size distribution control, binder chemistry, and intercrystalline bonding uniformity, which directly govern tool wear predictability and edge stability. In polycrystalline diamond (PCD) cutting tools, manufacturers are routinely delivering 10×-100× tool life versus tungsten carbide in high-speed machining of aluminum alloys, CFRP stacks, and EV motor components-reshaping OEM calculations around cost per part rather than upfront insert price.

In drilling and energy applications, HPHT diamond compacts designed for 5-6 GPa synthesis pressures and tailored cobalt binder architectures are enabling longer bit runs in abrasive formations, reducing tripping frequency and non-productive time. Oil & gas service providers increasingly specify application-specific diamond grades-rather than generic hardness classes-to manage vibration, thermal shock, and impact loading in extended-reach wells. This shift places a premium on suppliers capable of reproducible synthesis at scale.

Electronics and emerging quantum and photonics applications represent a structurally different demand driver. CVD diamond substrates with thermal conductivities approaching ~20 W/cm·K are being qualified for high-power RF devices, laser diodes, and advanced packaging, where heat flux densities exceed the limits of copper and aluminum nitride. Here, consistency in thickness, surface roughness, and defect density-rather than cutting performance-defines supplier competitiveness. Manufacturers investing in large-area, low-defect CVD growth and post-growth polishing technologies are positioning superhard materials as thermal management solutions rather than mechanical ones.

Market Analysis: Strategic Developments, Policy Shifts & Technology Adoption

The global superhard materials landscape experienced strategic transformation, driven by policy signals, quantum technology advancements, aerospace procurement, and expanded HPHT synthesis capacity. In Dec 2025, the U.S. Department of Commerce introduced heightened scrutiny and potential tariff exposure for imported cutting tool components, prompting manufacturers to diversify sourcing strategies and accelerate localization of PCD, PCBN, and diamond composites. In Nov 2025, Sandvik Coromant launched a new PCBN grade optimized for intermittent high-speed machining of EV powertrain gears and hardened shafts, aligning with the automotive industry's move toward lightweight EV architectures requiring precision machining at tighter tolerances.

A major innovation milestone emerged in Oct 2025, when Element Six and Bosch announced a joint venture integrating synthetic diamond technology into quantum sensing platforms, creating new demand for engineered NV-defect diamonds. During Sep 2025, Hyperion Materials expanded HPHT press capacity, supporting the scaling of large-format PCD cutters for oil & gas drilling-an area where tool durability directly influences exploration economics. On the other hand, Aug 2025 saw widespread adoption of AI-driven process optimization among Asia-Pacific HPHT and CVD manufacturers, reporting >95% batch-to-batch quality consistency, a key metric for premium abrasives and diamond tool reliability.

Technology diversification also accelerated in defense, aerospace, and electronics. Chinese manufacturers introduced boron-rich composites (B₄C) in May 2025, targeting next-generation armor systems requiring extreme hardness and impact resistance. In Mar 2025, major European aerospace firms secured long-term supply contracts for PCBN and diamond tooling to support precision machining of lightweight superalloys. In Feb 2025, an academic breakthrough demonstrated a synthesis method for diamonds with controlled NV ensembles, advancing commercial progress in room-temperature quantum computing sensors-a future growth vector for high-purity CVD diamond.

Superhard Materials Market: Trends and Opportunities

Finer-Grain and Nanostructured PCD Redefine Precision Machining Economics

The rapid shift toward high-silicon aluminum alloys, advanced lightweight castings, and carbon-fiber-reinforced plastics (CFRP) has fundamentally changed performance thresholds for cutting tools. Traditional coarse-grain polycrystalline diamond (PCD) is increasingly unable to deliver the edge stability and surface integrity required for EV drivetrains, battery housings, and aerospace structures. In response, toolmakers are scaling ultra-fine grain and nanostructured PCD, where reduced grain boundaries suppress micro-chipping and stabilize the cutting edge under high feed rates.

By 2025, industrial validation data shows that nanostructured PCD tools deliver 40–60% longer usable tool life than legacy PCD grades while maintaining dimensional tolerances below 5 μm—now a baseline requirement for EV battery casings and structural aluminum components. The productivity impact is material: in high-volume automotive lines, PCD and PCBN tools are delivering 3–5× longer service life than carbide, directly reducing tool-change downtime and scrap rates.

In composite machining, the value proposition is even clearer. Peer-reviewed research in 2025 confirmed that nanocrystalline diamond (NCD) coatings significantly outperform microcrystalline alternatives in CFRP drilling by preventing edge graphitization, the root cause of delamination and burr formation. As CFRP adoption expands in aerospace interiors and EV structural members, ultra-fine PCD is transitioning from a premium option to a cost-of-quality enabler across precision manufacturing.

Integrated Superhard Drilling Systems Transform Unconventional Energy

In upstream energy, the competitive frontier has moved from selling cutters to delivering integrated drilling outcomes. Service providers are combining optimized PCD/cBN cutter geometries with real-time sensing, closed-loop hydraulics, and AI-driven decision systems to address the extreme wear environments of shale, deepwater, and enhanced geothermal systems (EGS).

By late 2025, integrated drilling service contracts had become the preferred commercial model for complex wells. Halliburton secured multi-service contracts that bundle advanced directional bits with intelligent rotary steerable systems, demonstrating how superhard materials are now embedded within end-to-end performance guarantees rather than sold as discrete consumables. At the same time, SLB has accelerated deployment of AI-assisted wear-prediction platforms that use downhole sensor data to forecast PCD cutter degradation before failure, materially reducing non-productive time in deep and high-temperature wells.

Geothermal drilling is emerging as a structurally new demand vector. OEMs such as NOV are adapting superhard cutter designs—originally developed for oil and gas—to withstand higher temperatures, corrosive brines, and crystalline rock formations encountered in deep geothermal projects. This convergence positions superhard materials as a critical enabler not only of energy extraction, but of long-duration thermal storage and baseload renewable power.

Diamond Tooling Becomes Mission-Critical for Wide-Bandgap Semiconductors

The transition to 200 mm silicon carbide (SiC) and gallium nitride (GaN) wafers is reshaping demand for superhard materials in semiconductor manufacturing. SiC’s near-diamond hardness makes conventional tooling economically and technically unviable; only diamond-impregnated wire saws and planarization tools can achieve the flatness, low subsurface damage, and yield consistency required for high-power devices.

In 2025, fabs scaling 8-inch SiC production increasingly specified ultra-fine diamond wire saws (<0.5 mm diameter) capable of ductile-mode cutting. This approach minimizes micro-cracking and reduces post-processing losses, a decisive advantage as wafer costs escalate with size. Diamond tools are also central to back-grinding and extreme wafer thinning, which lowers thermal resistance in power modules—directly improving EV charging speed and inverter efficiency.

Sustainability considerations are reinforcing adoption. Diamond wire sawing significantly reduces kerf loss compared with slurry-based methods, aligning with “green fab” mandates focused on material efficiency and waste minimization. As wide-bandgap devices become the backbone of electrified transport and grid infrastructure, diamond tooling is moving from a niche consumable to a strategic manufacturing bottleneck.

Superhard Wear Components Enable Industrial-Scale Green Hydrogen

The industrialization of PEM and alkaline electrolyzers is opening a high-value opportunity for superhard materials in the forming and finishing of metallic bipolar plates—the structural and conductive core of hydrogen stacks. Scaling electrolyzer production from pilot to gigawatt levels requires tooling that can withstand millions of high-pressure stamping cycles without dimensional drift.

By 2025, hydrogen OEMs were increasingly specifying PCBN- and PCD-coated forming tools to maintain micron-level tolerances during repetitive stamping of stainless steel and coated alloys. This durability is critical as bipolar plate volumes accelerate and cost-per-plate becomes a dominant system metric. Superhard coatings are also under evaluation for corrosion-resistant surface layers that protect plates in aggressive electrochemical environments while preserving electrical conductivity.

Beyond stamping, superhard wear parts are gaining traction in high-temperature sintering presses used for composite bipolar plates. These applications demand tooling that maintains surface integrity over thousands of cycles, supporting the industry’s push toward standardized, high-throughput hydrogen manufacturing. As governments and utilities commit to large-scale electrolyzer deployment, superhard materials are emerging as quiet enablers of hydrogen system reliability and cost reduction.

Market Share Analysis: Superhard Materials Market

Market Share by Synthesis Method: HPHT Production Anchors Industrial Diamond Economics

High Pressure High Temperature (HPHT) synthesis accounts for approximately 55% of the global Superhard Materials Market, underscoring its role as the industrial backbone for high-volume diamond and polycrystalline diamond production. This dominance is structurally driven by HPHT’s unmatched scalability and cost efficiency, which allow manufacturers to supply massive quantities of industrial-grade diamond grit and PCD required by mining, construction, and manufacturing sectors. By replicating the extreme pressure and temperature conditions of the Earth’s mantle, HPHT produces dense, impact-resistant diamond crystals at a fraction of the time and cost associated with alternative synthesis routes. Market share is further reinforced by HPHT’s economic advantage in producing small to medium diamond sizes, which are essential for grinding wheels, cutting tools, and wear-resistant components used across heavy industry. Superior thermal conductivity also strengthens adoption, as HPHT diamonds dissipate heat rapidly during cutting and drilling, reducing tool wear and improving process stability in high-speed operations. Collectively, these throughput, cost, and performance advantages position HPHT as the default synthesis method for industrial superhard materials, securing its leading share in the global market.

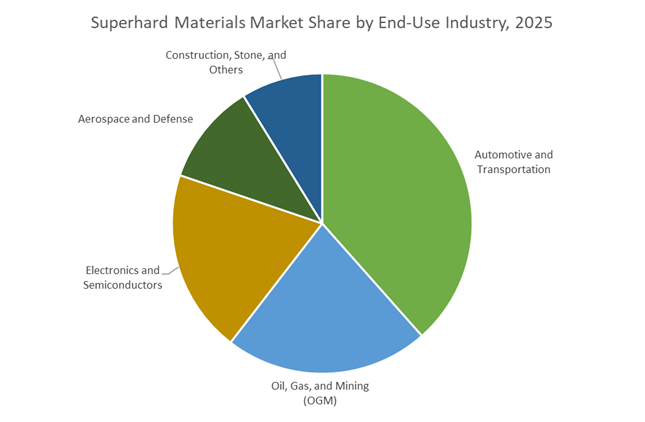

Market Share by End-Use Industry: Automotive and Transportation Drive High-Value Tool Demand

The automotive and transportation sector represents approximately 35% of total demand in the Superhard Materials Market, making it the largest and most strategically important end-use segment. This leadership is being amplified by the rapid shift toward electric vehicles and lightweight alloy architectures, which demand extreme machining precision and durability. Superhard materials, particularly PCD and PCBN, enable step-change improvements in tool life and machining speed when working with high-silicon aluminum, hardened steels, and advanced composites common in EV platforms. Market share is further reinforced by the sector’s focus on cycle time reduction and manufacturing uptime, as superhard tools dramatically extend tool life and minimize costly production interruptions. In EV battery manufacturing, ultra-precise cutting tools made from superhard materials play a critical role in maintaining electrode integrity and safety standards. As automotive OEMs and suppliers prioritize efficiency, quality, and throughput in electrified powertrain production, the automotive and transportation sector remains the primary demand engine for superhard materials, sustaining its dominant share in the global market.

Competitive Landscape: Global Leaders in PCD, PCBN, CVD Diamond & HPHT Superhard Solutions

The superhard materials industry is dominated by companies that excel in HPHT synthesis, CVD diamond engineering, precision tool integration, and quantum-grade diamond innovation. Competitive differentiation hinges on material purity, grit consistency, proprietary defect engineering, and tool geometry optimization for high-speed machining. The following company profiles outline the capabilities of top market participants across drilling, automotive machining, electronics, aerospace, and defense applications.

Sandvik Group - Integrating Superhard Materials Into Intelligent Machining Ecosystems

Sandvik, through its Sandvik Coromant division, emphasizes system-level optimization by pairing PCBN and PCD tooling with digital wear-monitoring technologies, enhancing machining efficiency and process automation. Leveraging 8,300+ active patents, the company co-optimizes tool geometry with superhard material grade selection to improve performance in high-speed, high-precision environments. The automotive sector-representing around 7% of Group revenue-relies heavily on Sandvik’s PCBN inserts for machining hardened transmission components. Recent R&D has targeted aluminum machining for EV platforms, driving expanded use of diamond-tipped tools to support vehicle lightweighting.

Element Six (De Beers Group) - Global Leader in HPHT & CVD Diamond Innovation

Element Six leads the industry with deep expertise in HPHT and CVD diamond synthesis, demonstrating unmatched purity and defect control. Its materials played a role in CERN’s Higgs boson identification (2012), highlighting its specialization in ultra-pure diamond solutions. The company’s patented DNV-B1™ quantum-grade diamond is engineered for NV-ensemble precision, enabling breakthroughs in computing and sensing. Element Six also offers non-abrasive applications such as CVD diamond speaker domes, exceeding one million global shipments. Its Suzhou (China) facility expands production of synthetic diamond for PCD applications, reinforcing global supply reliability.

Hyperion Materials & Technologies - Integrated Producer Of CBN, PCBN & PCD For Extreme Applications

Hyperion develops superhard materials with high thermal conductivity and excellent surface integrity, tailored for aerospace machining and oil & gas drilling. As one of few vertically integrated producers-from tungsten carbide powders through to PCBN/PCD finishing-it maintains tight control over material consistency and supply chain resilience. Hyperion is a major supplier of high-performance PCD cutters for demanding drilling environments, while its range of CBN grades offers twice the hardness and up to four times the abrasion resistance of conventional abrasives, supporting ferrous machining under severe wear conditions.

Zhongnan Diamond - High-Volume Hpht Producer Serving Abrasives, Drilling & Wire Manufacturing

Zhongnan Diamond ranks among the world's largest HPHT synthetic diamond manufacturers, supported by large-scale press capacity that ensures volume competitiveness in abrasive grit and powder markets. The company aligns closely with Chinese industrial policy, increasing output of PCD blanks for geotechnical drilling and infrastructure megaprojects. Significant R&D investment is directed at producing large-grain synthetic diamonds for wire drawing dies, supporting precision metal wire production. Zhongnan benefits from strong regional demand in automotive and construction sectors, where diamond tools are widely deployed in grinding and cutting operations.

Asahi Diamond Industrial - Precision Specialist For Semiconductor, Electronics & Optical Applications

Asahi Diamond Industrial focuses on ultra-precision diamond and CBN solutions for semiconductor wafer slicing, polishing, and micro-abrasive finishing. Its portfolio includes CVD thick-film diamond used in high-performance optical windows and lenses requiring broad electromagnetic transmission. The company delivers integrated systems combining superhard materials with machining equipment for advanced finishing applications. Asahi also engineers diamonds with enhanced thermal properties, making them essential for heat removal in 5G RF devices and compact high-frequency electronics.

China remains the dominant force in the global superhard materials market, accounting for more than four-fifths of synthetic diamond output, but 2025 marks a decisive shift from volume-driven exports to strategic regulation. The implementation of MOFCOM Announcement No. 55 in October 2025 fundamentally reclassified synthetic diamond and cubic boron nitride (cBN) as dual-use strategic materials. By introducing mandatory export licensing, China has effectively tightened global availability for applications spanning semiconductor thermal management, aerospace tooling, and quantum-grade substrates. This policy move is reinforcing China’s leverage over downstream industries while encouraging domestic upgrading toward high-purity HPHT and precision-engineered diamond products.

Henan Province continues to anchor this strategy, with industrial bases such as Zhecheng evolving into fully integrated ecosystems covering diamond micropowders, PCD tools, and advanced coatings. State recognition of firms like Huanghe Whirlwind as National Manufacturing Single Champions signals Beijing’s intent to consolidate leadership around fewer, technologically superior producers. Collectively, these measures are repositioning China as a gatekeeper of global superhard material flows rather than a low-cost supplier.

United States’ CHIPS Act Alignment with Thermal and Quantum Applications

The United States superhard materials market is increasingly tied to national semiconductor resilience and defense-grade electronics. Federal funding under the CHIPS National Advanced Packaging Manufacturing Program has accelerated the integration of synthetic diamond heat spreaders into glass-core and silicon-core substrates, directly addressing thermal bottlenecks in AI accelerators and high-performance computing. These initiatives are elevating diamond from a niche thermal solution to a strategic material within advanced packaging roadmaps.

Beyond commercial semiconductors, defense and quantum research are driving premium demand. Programs sponsored by DARPA are leveraging diamond’s extreme thermal conductivity and electric breakdown strength for ultra-wide bandgap (UWBG) devices. At the same time, the U.S. International Trade Commission’s enforcement actions against infringing imports underscore a parallel focus on intellectual property protection. This dual approach-heavy public funding combined with aggressive trade enforcement-positions the U.S. market as innovation-led but tightly controlled.

India’s Emergence as a Global CVD and Lab-Grown Diamond Export Hub

India has rapidly transformed its role in the superhard materials market, moving from a polishing-centric economy to a technology-driven exporter of CVD-grown diamonds. Fiscal incentives under long-term manufacturing frameworks and targeted R&D grants have enabled domestic players to scale industrial-grade lab-grown diamonds beyond jewelry into electronics, medical devices, and precision tooling. The allocation of specialized funding to institutions such as Indian Institute of Technology Madras for LGD seed and reactor development is particularly significant, as it reduces dependence on imported core technologies.

By 2025, India achieved record lab-grown diamond exports, supported by consistent double-digit growth in industrial applications. Even amid higher tariffs in select markets, Indian producers have diversified toward Europe and the Middle East, reinforcing the country’s position as a resilient and scalable alternative supplier in the global superhard ecosystem.

Japan’s Transition from Research to Pilot-Scale Diamond Semiconductors

Japan occupies a unique position in the superhard materials market as the leading innovator in diamond-based power electronics. Research milestones achieved between 2024 and 2025 demonstrated performance metrics far exceeding conventional silicon carbide, accelerating the shift from laboratory validation to pilot manufacturing. This transition is critical for applications requiring radiation hardness, extreme thermal stability, and ultra-high voltage operation.

The construction of dedicated diamond semiconductor facilities in Fukushima and strategic collaborations between domestic precision manufacturers and global diamond specialists are laying the groundwork for wafer-scale standardization. Japan’s focus is not on volume leadership but on defining next-generation device architectures where diamond becomes a functional semiconductor rather than merely a coating or heat spreader.

European Union’s Sustainability-Driven Demand and Environmental Applications

The European Union is differentiating its superhard materials market through sustainability and environmental remediation rather than pure electronics scale. Synthetic diamond electrodes are gaining prominence in wastewater treatment systems designed to destroy persistent pollutants, aligning with EU chemical safety and circular economy objectives. Recognition of such technologies at international innovation forums has accelerated adoption by municipal and industrial users.

Simultaneously, Europe’s aerospace and specialty metals industries continue to drive steady demand for polycrystalline diamond tooling, particularly in wire drawing and high-precision machining. EU-funded research programs are further expanding the use of superhard coatings to reduce friction and energy losses in hydrogen and next-generation propulsion systems, reinforcing a sustainability-led growth pathway.

National Competitive Matrix: Superhard Materials Market (2025)

Superhard Materials Market Development Matrix by Country

|

Country / Region

|

Strategic Focus

|

Key Policy or Event

|

Market Positioning

|

|

China

|

Supply chain control

|

MOFCOM export controls on superhard materials

|

Global volume leader, regulated exports

|

|

United States

|

Semiconductor thermal management

|

CHIPS Act advanced packaging funding

|

Innovation-led, IP-protected

|

|

India

|

CVD and LGD scaling

|

National R&D grants and export growth

|

Fastest-growing alternative supplier

|

|

Japan

|

Diamond semiconductors

|

Pilot-scale manufacturing initiatives

|

Technology benchmark for UWBG devices

|

|

European Union

|

Sustainability applications

|

Green technology and research funding

|

Environmental and aerospace specialization

|

Superhard Materials Market Report Scope

Superhard Materials Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$5.5 Billion

|

|

Market Size (2035)

|

$9.6 Billion

|

|

Market Growth Rate

|

5.7%

|

|

Segments

|

By Material Type (Synthetic Diamond, Cubic Boron Nitride, Composite Superhard Materials, Novel Superhard Materials), By Synthesis Method (High-Pressure High-Temperature, Chemical Vapor Deposition, Detonation Nanodiamond), By Application (Abrasives & Cutting Tools, Thermal Management, Electronics & Semiconductors, Quantum Technologies, Medical & Healthcare, Wear-Resistant Components), By End-Use Industry (Automotive, Aerospace & Defense, Electronics, Oil & Gas, Construction & Stone)

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Element Six (UK) Limited, Sumitomo Electric Industries Ltd., Hyperion Materials & Technologies Inc., Zhongnan Diamond Co., Ltd., Henan Huanghe Whirlwind Co., Ltd., ILJIN Diamond Co., Ltd., Sandvik AB, Zhengzhou Sino-Crystal Diamond Co., Ltd., Funik Ultra-Hard Material Co., Ltd., Tomei Diamond Co., Ltd., Saint-Gobain Abrasifs, Mitsubishi Materials Corporation, Applied Diamond Inc., New Diamond Technology LLC

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

Superhard Materials Market Segmentation

By Material Type

- Synthetic Diamond

- Cubic Boron Nitride

- Composite Superhard Materials

- Novel Superhard Materials

By Synthesis Method

- High-Pressure High-Temperature

- Chemical Vapor Deposition

- Detonation Nanodiamond

By Application

- Abrasives and Cutting Tools

- Thermal Management

- Electronics and Semiconductors

- Quantum Technologies

- Medical and Healthcare

- Wear-Resistant Components

By End-Use Industry

- Automotive

- Aerospace and Defense

- Electronics

- Oil and Gas

- Construction and Stone

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in Superhard Materials Market

- Element Six (UK) Limited

- Sumitomo Electric Industries, Ltd.

- Hyperion Materials & Technologies, Inc.

- Zhongnan Diamond Co., Ltd.

- Henan Huanghe Whirlwind Co., Ltd.

- ILJIN Diamond Co., Ltd.

- Sandvik AB

- Zhengzhou Sino-Crystal Diamond Co., Ltd.

- Funik Ultra-Hard Material Co., Ltd.

- Tomei Diamond Co., Ltd.

- Saint-Gobain Abrasifs

- Mitsubishi Materials Corporation

- Applied Diamond, Inc.

- New Diamond Technology LLC

*- List not Exhaustive