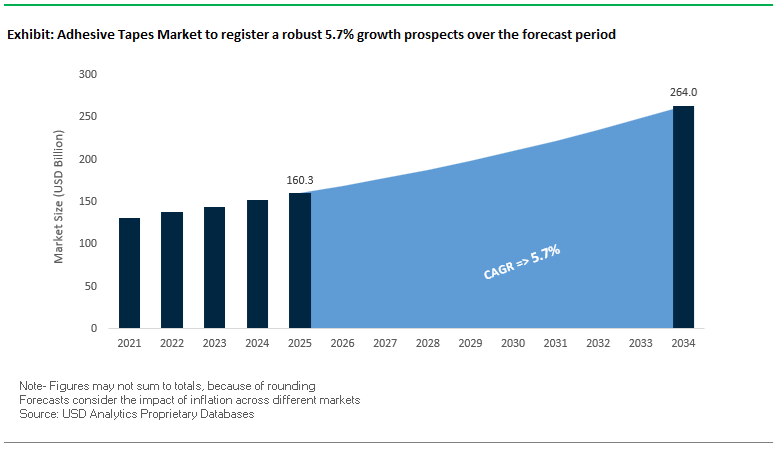

The global adhesive tapes market, projected to reach USD 160.3 billion in 2025 and expand to USD 264 billion by 2034 at a CAGR of 5.7%, is undergoing a structural transformation from commodity fastening products to engineered functional bonding systems. Leading manufacturers are no longer competing solely on adhesion strength, but on sustainability compliance, process compatibility, functional integration, and long-term reliability across automotive electrification, renewable energy, electronics miniaturization, medical wearables, and high-speed packaging.

From a manufacturing standpoint, adhesive tapes have become critical process enablers—replacing mechanical fasteners, liquid adhesives, and thermal greases with lighter, faster, and automation-ready bonding solutions. Pressure-sensitive adhesive (PSA) technologies dominate because they support instant bonding, robotic application, and consistent performance under demanding mechanical, thermal, and environmental loads. This shift is particularly visible in EV battery assembly, solar panel lamination, display bonding, and e-commerce logistics, where tapes must deliver structural strength, flame resistance, EMI shielding, and thermal management simultaneously.

Sustainability is a core design constraint rather than a secondary attribute. Major tape producers have publicly committed to PFAS elimination, solvent-free manufacturing, and high recycled or bio-based content, responding to tightening global regulations and OEM Scope-3 emission targets. The rapid expansion of PCR-based backings, paper-based reinforcing tapes, PVC-free constructions, and biomass-balanced acrylic systems reflects how adhesive chemistry is being re-engineered to align with circular-economy requirements—without sacrificing adhesion performance or durability.

Similarly, innovation in functional and smart tapes is redefining market value creation. Adhesive tapes are expected to provide thermal conductivity, electrical insulation, vibration damping, flame retardancy, optical clarity, and skin compatibility, particularly in EVs, electronics, and medical devices. This multifunctionality—combined with compatibility with automated, high-throughput manufacturing lines—is positioning adhesive tapes as indispensable components of next-generation industrial systems rather than consumables.

The adhesive tapes industry is undergoing a phase of accelerated innovation, characterized by sustainable product launches, automation-driven bonding solutions, and new material chemistries. In April 2025, Avery Dennison Performance Tapes introduced a Solar Panel Bonding Portfolio featuring UV-resistant PSA technology, providing an automatable and durable alternative to liquid adhesives in solar energy assembly. This launch highlights the growing importance of pressure-sensitive adhesive tapes in renewable energy applications and industrial automation. Similarly, Henkel AG reported in March 2025 that its Adhesive Technologies unit expects steady organic growth, reflecting continued resilience in industrial tapes and smart structural bonding for e-mobility.

Sustainability continues to define corporate strategies across the sector. In September 2025, tesa SE began a major rebranding and redesign of its consumer packaging line, renaming its tesa moll sealing range to tesa Insulation to highlight eco-certified insulation tapes and point-of-sale sustainability visibility. This follows Avery Dennison’s June 2024 launch of SP 1504 Easy Apply RS™, a PVC-free, halogen-free vehicle wrap film with a 53% reduction in greenhouse gas emissions, signaling a shift toward low-VOC and non-toxic adhesive systems. In the same period, 3M Corporation’s 2024 Annual Report revealed the introduction of 169 new products, focusing on automotive electrification, industrial automation, and sustainable production, reinforcing its commitment to innovation-led growth.

Beyond product launches, materials innovation is expanding through bio-based and solvent-free chemistries. Saint-Gobain’s R&D initiative (2024–2025) focuses on developing bio-based polyol adhesives using nut-shell oils, aimed at EV-grade flame-resistant tapes, while Nitto Denko Corporation continues to strengthen its low-VOC, solvent-free double-coated adhesive tape lines (e.g., No. 5000E series) that support indoor air quality compliance in automotive interiors and electronics. Similarly, in November 2023, a major packaging player launched Tesa 51345, a paper-based reinforcing tape supporting monomaterial packaging, marking a critical step toward recyclable, eco-friendly logistics solutions.

The transition toward recyclable, low-carbon, and bio-based adhesive tapes has become a defining global trend, driven by stricter environmental policies such as the EU Packaging and Packaging Waste Regulation (PPWR). The framework mandates all plastic packaging to be recyclable by 2030, compelling manufacturers to reformulate tapes used in lamination, labeling, and closures to ensure they do not obstruct mechanical recycling of major material streams like PET and HDPE.

Leading players such as BASF and Tesa are spearheading the move toward eco-designed adhesive systems. BASF’s development of water-based lamination adhesives enables easier delamination of PET/PE film layers, supporting circular packaging flows. In April 2024, Tesa introduced a double-sided tape utilizing biomass-balanced acrylic monomers and 90% post-consumer recycled (PCR) PET backing, achieving a 40% reduction in Product Carbon Footprint (PCF)—a benchmark for industrial-grade sustainability without compromising performance.

Further accelerating the trend, Tesa’s bio-based paper packaging tape with >85% bio-carbon content and solvent-free rubber adhesive underscores the viability of renewable feedstocks in high-performance packaging applications. Such chlorine-free, fully recyclable tapes are gaining widespread traction across e-commerce and logistics, aligning with global corporate sustainability goals.

At the same time, Avery Dennison’s pressure-sensitive label technology, verified by RecyClass, achieved 99% label removability in HDPE recycling—a milestone exceeding Europe’s recyclability threshold. The advancement highlights how adhesive chemistry directly influences material circularity, turning tapes and labels into enablers of Extended Producer Responsibility (EPR) compliance.

The rise of eco-efficient adhesive tapes illustrates the industry’s new sustainability paradigm—one that prioritizes low-VOC, recyclable, and renewable formulations as critical enablers for circular packaging and industrial decarbonization.

Adhesive tapes are evolving from passive bonding materials into smart, multifunctional enablers within electronics, automotive, and medical applications. The convergence of thermal management, electrical insulation, sensing, and flexibility in adhesive formulations is revolutionizing their role in critical systems, particularly EV batteries, flexible electronics, and wearable devices.

In the electric vehicle (EV) sector, manufacturers are adopting functional adhesive tapes engineered to meet UL 94 V-0 flame retardancy standards, offering flame-tough protection and thermal runaway mitigation for high-voltage batteries. Avery Dennison’s flame-resistant acrylic and silicone tapes exemplify the shift toward high-performance bonding solutions that combine structural strength, heat resistance, and safety compliance.

In the healthcare domain, 3M’s long-wear medical-grade adhesive tapes have doubled their wear duration to 28 days, supporting continuous glucose monitoring (CGM) sensors and next-generation health monitoring devices. These tapes are revolutionizing wearable medical technologies, enabling long-term skin contact without irritation and ensuring consistent data collection—key to remote and patient-centric care models.

In consumer electronics, viscoelastic acrylic foam tapes (e.g., 3M VHB series) deliver dual functionality—structural bonding and shock absorption—which is essential for smartphone and tablet assembly. Their elasticity and impact resistance minimize damage risks while maintaining waterproofing and dust sealing, addressing the industry’s growing demand for thin, lightweight, and durable device design.

The shift toward automated electric vehicle battery assembly represents one of the largest growth opportunities for the adhesive tapes industry. As EV production scales globally, pressure-sensitive adhesive (PSA) tapes are increasingly replacing mechanical fasteners to optimize assembly efficiency, weight reduction, and safety performance.

According to Avery Dennison’s automotive and eMobility division, PSA tapes are becoming integral to cell-to-cell bonding processes—facilitating instant adhesion, precise alignment, and consistent application in automated manufacturing environments. The transition reduces structural weight, enabling improved vehicle range and more efficient production throughput.

Additionally, Thermally Conductive Adhesive (TCA) films and tapes are indispensable for heat management within EV battery modules. Positioned between cells and cooling plates, these films enhance thermal uniformity, preventing localized overheating and extending battery life. With the EV market expanding exponentially, the need for fire-safe, thermally efficient, and automation-ready adhesive systems is expected to surge across OEM and tier-one supplier networks.

By replacing complex mechanical fastening and liquid adhesives, tape-based bonding systems are unlocking new levels of manufacturing flexibility, supporting the industry’s transition to scalable gigafactory production and sustainable electric mobility.

The global boom in wearable healthcare technology—from continuous glucose monitors to remote diagnostics—has unlocked significant opportunities for medical-grade adhesive tapes engineered for biocompatibility, comfort, and long wear duration.

Lohmann’s DuploMED line of skin adhesives, certified under ISO 10993 biocompatibility standards, delivers over 28 days of reliable wear, addressing the need for long-term adherence in continuous monitoring systems (CGM sensors). These tapes maintain skin integrity, offer high breathability, and are hypoallergenic—critical features for extended patient use in both clinical and home care environments.

Further, repositionable adhesive technologies allow for painless removal and reapplication, improving usability in drug delivery patches and flexible health sensors. The innovation enhances patient comfort while ensuring optimal device placement, making adhesive tapes an essential component of the decentralized, patient-driven healthcare ecosystem.

As medical device manufacturers increasingly integrate microelectronics and biosensors, adhesive tapes with precision bonding, biocompatibility, and moisture control are emerging as a foundation for scalable innovation. The continued intersection of adhesive chemistry and biomedical engineering is expected to propel strong growth in the global healthcare adhesives segment through 2030.

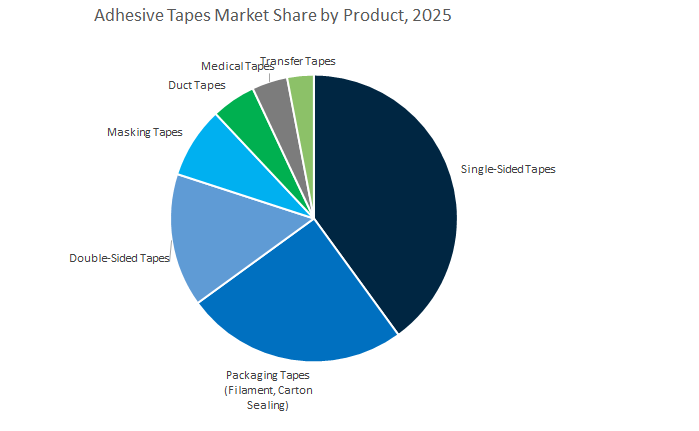

Adhesive Tapes Market Share Insights, 2025-2034

The single-sided tapes segment dominates the global adhesive tapes industry, accounting for an estimated 40% of total market share in 2025. This leadership stems from the versatility, affordability, and universal application range of single-sided adhesive tapes across virtually every industrial and consumer domain. These tapes are essential for sealing, bundling, insulation, masking, and surface protection, making them a fundamental commodity in manufacturing, logistics, and retail. Their extensive use in packaging lines, electrical insulation, and construction finishing reflects their adaptability to both high-speed automated and manual applications. Technological advancements in pressure-sensitive adhesives (PSAs)—particularly acrylic, rubber, and silicone chemistries—have improved adhesion strength, UV resistance, and temperature tolerance, expanding their usability in challenging environments. Moreover, the increasing adoption of eco-friendly and recyclable polyolefin backings is aligning this segment with global sustainability mandates. Given their combination of high-volume demand and broad usability, single-sided tapes remain the backbone of the adhesive tape industry, ensuring a steady revenue base across mature and emerging economies alike.

The packaging tapes segment, representing approximately 25% market share, serves as the industry’s largest volume driver, fueled by the exponential growth of e-commerce, logistics, and retail distribution networks. Packaging tapes—comprising filament, carton sealing, and BOPP-based tapes—are indispensable for carton closure, palletizing, and load stabilization in warehouses and shipping centers worldwide. Their strong adhesion, tear resistance, and low-cost performance make them a default choice for mass packaging operations. As sustainability becomes a competitive advantage, manufacturers are transitioning to water-based acrylic adhesives, paper-based tapes, and solvent-free formulations to meet environmental targets. Additionally, automated packaging lines and robotic sealing systems are driving demand for high-speed, temperature-stable tapes that ensure reliability under continuous operation. The combination of sustainability, speed, and strength continues to position packaging tapes as an essential, high-volume segment defining the industry’s production backbone.

The double-sided and transfer tapes segment represents the high-performance core of the adhesive tapes market, catering to industries where precision bonding, mounting, and structural integrity are critical. These tapes are widely used in automotive interior assembly, consumer electronics, display bonding (OCAs), and appliance manufacturing, replacing mechanical fasteners, screws, and liquid adhesives. Their rising adoption in Electric Vehicle (EV) battery modules, smartphone displays, and medical device assembly reflects the global trend toward lightweight, clean, and aesthetically superior bonding technologies. Innovations in acrylic foam, viscoelastic, and thermal conductive adhesive tapes have further expanded their capabilities for vibration damping, heat dissipation, and stress distribution. As manufacturers shift toward high-value and functionally engineered tapes, this segment is witnessing strong revenue growth despite lower overall volume compared to commodity categories. Its evolution underscores the industry’s transition toward performance-driven, multifunctional adhesive solutions.

The packaging industry remains the undisputed leader in the global adhesive tapes market, commanding approximately 35% of total market share in 2025. This dominance is fueled by the rapid proliferation of e-commerce, retail logistics, and global supply chain networks, which rely heavily on carton sealing, bundling, and labeling tapes for efficient shipment handling. The growing emphasis on tamper-evident, sustainable, and recyclable packaging materials is reshaping the adhesive tape ecosystem, encouraging the development of bio-based films, water-based adhesives, and solvent-free formulations. Packaging tapes, especially BOPP, kraft paper, and filament tapes, are being optimized for high-speed automated machinery that demands consistent tack and peel strength under variable temperatures. With continuous innovation in printed and branded adhesive tapes for product identification and marketing, this segment not only leads in volume but also in functional diversification, maintaining its dominance as the backbone of adhesive tape consumption globally.

The building and construction segment, holding around 20% market share, represents a mature yet indispensable pillar of the adhesive tapes industry. Tapes play an integral role in sealing, insulation attachment, surface protection, and structural joining applications across residential, commercial, and infrastructure projects. Aluminum foil tapes, butyl-based sealant tapes, and PE foam tapes are heavily used in HVAC duct sealing, window glazing, vapor barriers, and waterproof membranes, ensuring energy efficiency and air-tightness in modern buildings. As green construction practices and energy-efficient building codes become global standards, the demand for low-VOC, weather-resistant, and long-life adhesive tapes continues to rise. Additionally, innovations in fire-retardant and UV-resistant adhesive systems are enhancing safety and durability, positioning this segment as a consistent driver of industrial-grade adhesive tape demand.

The healthcare and medical segment is emerging as one of the fastest-growing high-value markets for adhesive tapes, driven by demand for biocompatible solutions used in surgical dressings, diagnostic sensors, wearable monitors, and advanced wound care, all requiring strong yet gentle adhesion that meets strict regulatory standards. Alongside this, the electrical and electronics sector continues to expand as polyester, polyimide, and flame-retardant acrylic tapes enable insulation, EMI shielding, component protection, and thermal management across consumer electronics, EV batteries, and 5G devices, with OCAs and conductive tapes representing cutting-edge applications. The automotive and transportation segment is likewise evolving into a performance-driven market where adhesive tapes support lightweighting, noise reduction, clean aesthetics, and EV battery safety through thermal conductive, flame-retardant, dielectric, and vibration-damping solutions.

The competitive landscape of the global adhesive tapes market is characterized by high R&D intensity, sustainability-driven innovation, and technology diversification. Industry leaders such as 3M Company, tesa SE, Avery Dennison, Nitto Denko Corporation, and Henkel AG & Co. KGaA dominate through their global distribution networks and differentiated adhesive platforms. These companies are focusing on solvent-free manufacturing, bio-based adhesives, automated bonding systems, and lightweight EV and electronics applications, reinforcing their leadership positions in a market shifting toward PFAS-free, circular, and low-emission products.

3M’s market strength lies in its VHB Extrudable Tape, designed for EV battery assembly and lightweighting, supported by automotive OEM partnerships. The company has pledged to eliminate PFAS by end of 2025, while targeting carbon neutrality by 2050, demonstrating leadership in environmental compliance. Its Microreplication Technology enhances bubble-free graphic film application and precision coating performance. Additionally, 3M’s Box Sealing Tape 570 represents its first eco-friendly packaging tape platform, catering to e-commerce logistics and sustainable shipments.

Tesa SE leads in PCR-based packaging tapes, utilizing 90% post-consumer recycled polyester for high-volume packaging applications. Its specialty functional tapes cater to the electronics industry, offering electrically conductive, thermal management, and light-blocking properties. In flexographic printing, tesa Twinlock sleeves enhance process efficiency with reusable, self-adhesive mounts. The company’s newly launched tesa Insulation line features third-party-certified sustainability claims, targeting energy-efficient building applications such as air-tight window and door sealing.

Avery Dennison has established a strong foothold in solar panel bonding tapes, offering UV-resistant PSA solutions that simplify automated manufacturing in renewable energy systems. Its SP 1504 Easy Apply RS™ film is PVC- and halogen-free, aligning with low-VOC sustainable manufacturing. The company also expands its low-VOC certified tape portfolio for HVAC and flooring installations, ensuring compliance with indoor air quality standards. Furthermore, its Easy Apply Adhesive technology with Air Egress channels enables bubble-free installation and faster assembly across commercial applications.

Nitto Denko specializes in low-VOC, solvent-free double-coated acrylic adhesive tapes, addressing stringent health and safety regulations in automotive and electronics manufacturing. Its NITOFOIL® CT-311E supports EMI shielding and grounding for 5G and advanced connectivity devices. The company’s No.5302A tape offers strong adhesion to silicone rubber, enhancing performance in medical and consumer electronics. Through Heat Activated Adhesive Sheets (HAAS), Nitto improves assembly efficiency and reduces liner waste, underscoring its manufacturing optimization strategy.

Henkel’s Adhesive Technologies unit emphasizes structural bonding tapes for EV batteries and electronics, aligning with global e-mobility trends. The company’s net-zero roadmap integrates solvent-free, low-energy curing adhesives to minimize the carbon footprint of industrial tapes. Its Liofol laminating adhesive range supports flexible packaging and recyclable FMCG applications, cementing Henkel’s leadership in sustainable industrial bonding solutions.

China continues to dominate the global adhesive tapes industry as the largest producer and consumer, supported by its thriving automotive, electrical & electronics, and e-commerce logistics sectors. The nation’s automotive electrification push has catalyzed the demand for high-performance thermal management and structural bonding tapes, particularly for EV battery modules and lightweight vehicle assemblies. The development of aluminum and carbon fiber-compatible bonding tapes has become a strategic focus, aligning with China’s lightweighting objectives to enhance EV efficiency and range.

Parallelly, the rapid growth in e-commerce and logistics continues to fuel massive consumption of BOPP (Biaxially Oriented Polypropylene) packing tapes, making them one of the country’s highest-volume adhesive tape segments. The expansion of coating and converting facilities, both state-backed and privately funded, is strengthening domestic supply capabilities for high-precision double-coated tapes and release liners—vital for electronics, packaging, and industrial applications.

Additionally, the government’s “Made in China 2025” initiative is propelling R&D in low-VOC, solvent-free, and sustainable adhesive technologies, encouraging local innovation in environmentally compliant tape products. China’s combination of scale, policy support, and manufacturing innovation positions it as a global hub for next-generation adhesive tapes, catering to diverse end-user industries with both cost-effective and technologically advanced solutions.

The United States adhesive tapes market is characterized by its leadership in sustainable materials, specialty adhesive systems, and high-end engineering applications. With growing emphasis on carbon reduction and recyclability, major U.S. companies are investing in bio-based adhesives and solvent-free pressure-sensitive technologies to meet evolving environmental standards. A key milestone in 2024 was the launch of recyclable packaging tapes that integrate bio-based adhesives and repulpable backings, aligning with North America’s circular packaging objectives, notably introduced by 3M Company.

The country’s infrastructure modernization initiatives have significantly boosted demand for weatherproofing, sealing, and acrylic foam tapes used in construction, roofing, and building envelope applications. Meanwhile, the electronics and micro-assembly sectors continue to drive advancements in optically clear adhesive (OCA) tapes and conductive tapes, essential for flexible displays, wearables, and microelectronic components. Academic and corporate collaborations are at the forefront of developing high-durability and recyclable adhesive materials, with particular focus on optical and electrical performance.

Additionally, U.S. defense and aerospace programs rely heavily on precision-engineered adhesive tapes for vibration control, insulation, and composite bonding in structural assemblies. Combined with substantial investments in material innovation and regulatory compliance, the United States stands as a pioneer in sustainable adhesive tape technologies, catering to medical, aerospace, packaging, and high-tech industrial sectors with advanced, regulation-ready solutions.

Germany serves as Europe’s technological nucleus for adhesive tape innovation, emphasizing precision engineering, e-mobility solutions, and sustainable material development. Industry leaders such as tesa SE, Lohmann, and Henkel AG & Co. KGaA continue to lead in high-performance automotive and industrial tapes, producing die-cut and customized solutions tailored for electric vehicles, aerospace, and renewable energy systems.

The country’s automotive sector is witnessing rapid adoption of new-generation assembly and insulation tapes capable of withstanding extreme temperature and mechanical stress, particularly within battery housings and EV chassis systems. Concurrently, the Industry 4.0 initiative is transforming manufacturing practices—integrating sensor-driven converting and coating systems that deliver real-time precision and defect control in tape production.

Germany’s regulatory landscape, guided by the upcoming EU Packaging and Packaging Waste Regulation (PPWR), is compelling manufacturers to pivot toward repulpable paper-based tapes and recyclable flexible packaging solutions. Furthermore, expanding smart factory capabilities and the rise of eco-compliant production lines underscore Germany’s position as a sustainability leader and innovation powerhouse in Europe’s adhesive tape industry.

Japan remains a global benchmark for high-precision adhesive tapes, supported by its deep expertise in microelectronics, semiconductor processing, and display manufacturing. Major Japanese corporations such as Nitto Denko Corporation and LINTEC Corporation dominate the market with ultra-thin adhesive tapes for smartphone assembly, OLED display lamination, and optical component integration. The country’s advanced UV-curable dicing tapes and protective films are indispensable in semiconductor wafer processing, ensuring flawless precision and clean release in microchip fabrication.

Japan’s R&D focus extends to thermally conductive and flame-retardant adhesive tapes, crucial for industrial machinery and next-generation electric vehicles requiring reliable heat management and electrical insulation. Moreover, Japanese innovators are setting global sustainability standards through the development of biopolymer-backed tapes that minimize environmental impact without compromising performance.

Continuous collaboration between chemical producers and electronics OEMs has accelerated breakthroughs in PSA (pressure-sensitive adhesive) films with high transparency and low haze—vital for display stack performance. Supported by strong government programs in material science and domestic supply chain security, Japan remains at the forefront of precision, reliability, and sustainability in the global adhesive tapes market.

South Korea’s adhesive tape industry is undergoing rapid modernization, anchored by its leadership in OLED displays, EV batteries, and semiconductor manufacturing. Major chemical and display producers such as LG Chem are investing heavily in advanced tape production lines for black masking, optical, and boundary tapes, catering to large-format and high-resolution display technologies.

The country’s fast-expanding EV battery market has created significant opportunities for insulation and flame-retardant tapes, which play a vital role in battery pack sealing and cell module safety. The government’s push toward industrial automation and self-sufficiency has also accelerated investments in domestic converting and lamination capabilities, improving South Korea’s competitiveness in global specialty tape exports.

Patent activity reveals strong innovation in reworkable and removable adhesive systems, supporting the repair and recycling of high-value electronics. Moreover, the semiconductor industry’s growth has led to increasing demand for protective and functional films used in wafer processing and cleanroom applications. With a strategic balance of R&D intensity, automation, and high-value manufacturing, South Korea continues to strengthen its position as a regional leader in adhesive tape technology and export capability.

India’s adhesive tapes market is experiencing exponential growth, driven by infrastructure expansion, e-commerce logistics, and industrial manufacturing investments. Massive government-backed projects under Smart Cities Mission and PM Gati Shakti have sharply increased the use of construction tapes, duct tapes, and insulation sealing systems in large-scale infrastructure development. The growth of ports, railways, and road networks continues to create new demand for durable, weather-resistant adhesive tape solutions for both temporary and structural applications.

In parallel, India’s booming e-commerce sector has transformed packaging consumption patterns, making BOPP and tamper-evident tapes essential for reliable sealing and brand visibility in high-volume logistics operations. Local manufacturers such as Pidilite and Ajit Industries are expanding their production footprint, while international leaders like Henkel AG are strengthening their Indian R&D and production facilities to meet domestic and export demand.

The country’s growing automotive and electronics assembly base is driving adoption of high-tensile, double-sided, and thermal management tapes, catering to OEMs in both domestic and export markets. Supported by government incentives for manufacturing localization and rapid industrialization, India is fast emerging as a strategic growth hub in the global adhesive tapes value chain, combining affordability with increasing technological sophistication.

Adhesive Tapes Market Report Scope

Adhesive Tapes Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$160.3 Billion

|

|

Market Size (2034)

|

$ 264 Billion

|

|

Market Growth Rate

|

5.7%

|

|

Segments

|

By Backing Material (Polypropylene (PP) Tapes, Paper Tapes, PVC Tapes, Foam Tapes, Cloth/Fabric Tapes, Film Tapes, Foil Tapes), By Adhesive Chemistry/Resin (Acrylic Adhesives, Rubber Adhesives, Silicone Adhesives, Polyurethane Adhesives, Epoxy Adhesives), By Product Type/Structure (Single-Sided Tapes, Double-Coated Tapes, Transfer Tapes, Filament Tapes, Masking Tapes, Duct Tapes, Medical Tapes), By Technology (Solvent-Based Adhesives, Water-Based Adhesives, Hot-Melt Adhesives, UV-Cured/Electron-Beam Cured), By End-Use Industry (Packaging Tapes, Automotive Tapes, Electrical & Electronics Tapes, Building & Construction Tapes, Healthcare & Medical Tapes, White Goods & Appliances, General Industrial), By Category (Commodity Tapes, Specialty Tapes

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

3M Company, Nitto Denko Corporation, Tesa SE (Beiersdorf Group), Avery Dennison Corporation, Henkel AG & Co. KGaA, LINTEC Corporation, Lohmann GmbH & Co. KG, Sekisui Chemical Co., Ltd., Berry Global Inc., Intertape Polymer Group (IPG), Saint-Gobain S.A. (Tape Solutions), NICHIBAN Co., Ltd., Shurtape Technologies, LLC, Scapa Group PLC (Mativ Holdings), H.B. Fuller Company

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

By Backing Material

- Polypropylene (PP) Tapes

- Paper Tapes

- PVC Tapes

- Foam Tapes

- Cloth/Fabric Tapes

- Film Tapes

- Foil Tapes

By Adhesive Chemistry/Resin

- Acrylic Adhesives

- Rubber Adhesives

- Silicone Adhesives

- Polyurethane Adhesives

- Epoxy Adhesives

By Product Type/Structure

- Single-Sided Tapes

- Double-Coated Tapes

- Transfer Tapes

- Filament Tapes

- Masking Tapes

- Duct Tapes

- Medical Tapes

By Technology

- Solvent-Based Adhesives

- Water-Based Adhesives

- Hot-Melt Adhesives

- UV-Cured/Electron-Beam Cured

By End-Use Industry

- Packaging Tapes

- Automotive Tapes

- Electrical & Electronics Tapes

- Building & Construction Tapes

- Healthcare & Medical Tapes

- White Goods & Appliances

- General Industrial

By Category

- Commodity Tapes

- Specialty Tapes

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

- 3M Company

- Nitto Denko Corporation

- Tesa SE (Beiersdorf Group)

- Avery Dennison Corporation

- Henkel AG & Co. KGaA

- LINTEC Corporation

- Lohmann GmbH & Co. KG

- Sekisui Chemical Co., Ltd.

- Berry Global Inc.

- Intertape Polymer Group (IPG)

- Saint-Gobain S.A. (Tape Solutions)

- NICHIBAN Co., Ltd.

- Shurtape Technologies, LLC

- Scapa Group PLC (Mativ Holdings)

- H.B. Fuller Company

*- List not Exhaustive

Research Coverage

This report investigates how the global Adhesive Tapes Market is evolving as PFAS-free chemistries, solvent-free manufacturing, and automation reshape bonding across packaging, electronics, construction, and e-mobility; it distills breakthroughs in pressure-sensitive systems, thermal/EMI functional tapes, recyclable backings, and bio-based polymers into board-ready takeaways. Produced by USDAnalytics, the study delivers analysis reviews of demand drivers (EV, renewable installations, e-commerce), cost-to-serve impacts (adhesive savings, cycle time), and specification trends that elevate performance under regulatory scrutiny. It highlights portfolio moves, plant upgrades, and smart converting that lift yield and sustainability KPIs while reducing total applied cost. By connecting engineering metrics with commercial outcomes, this report is an essential resource for executives, product leaders, sourcing teams, and process engineers planning 2025–2034 growth plays and compliance-ready tape platforms.

Scope Highlights

- By Backing Material: PP, Paper, PVC, Foam, Cloth/Fabric, Film, Foil.

- By Adhesive Chemistry/Resin: Acrylic, Rubber, Silicone, Polyurethane, Epoxy.

- By Product Type/Structure: Single-Sided, Double-Coated, Transfer, Filament, Masking, Duct, Medical.

- By Technology: Solvent-Based, Water-Based, Hot-Melt, UV/EB-Cured.

- By End-Use: Packaging, Automotive, Electrical & Electronics, Building & Construction, Healthcare & Medical, White Goods & Appliances, General Industrial.

- By Category: Commodity, Specialty.

- Geographic Scope: Analysis spans 25+ countries across North America, Europe, Asia Pacific, Latin America, the Middle East & Africa.

- Historic & Forecast Window: Historic data 2021–2024; forecasts 2025–2034.

- Companies: Analysis/profiles of 15+ companies.

Deliverables

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.