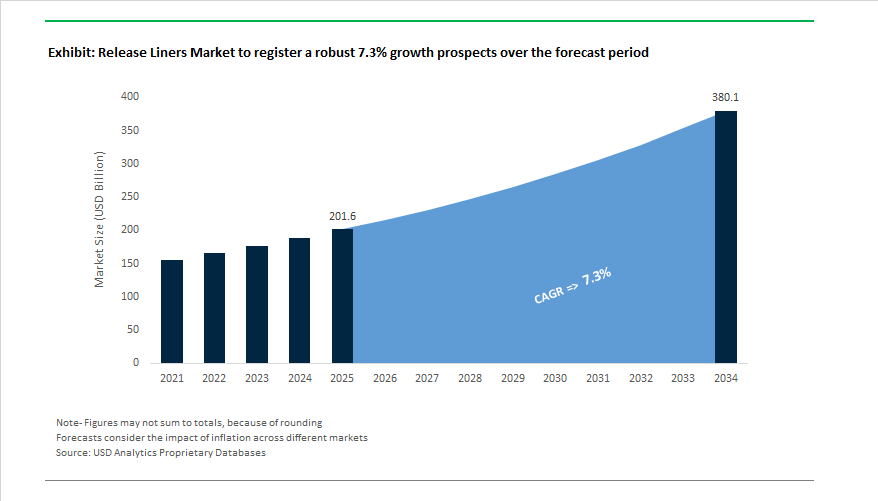

The Global Release Liners Market is projected to grow from $201.6 billion in 2025 to $380.1 billion by 2034, advancing at a healthy CAGR of 7.3%. This growth is propelled by rising demand across packaging, logistics, electronics, and construction industries, where release liners serve as essential backing materials for pressure-sensitive adhesives (PSA), medical tapes, graphic films, and industrial laminates. The expanding e-commerce ecosystem and increasing automation in labeling and converting processes are reinforcing the importance of durable, recyclable, and high-performance liner materials.

The pressure-sensitive labelstock segment remains the dominant application, underpinning its central role in the global packaging and logistics value chain. In North America, Glassine/SCK (Supercalendered Kraft) papers lead as the preferred substrate, valued for their smoothness, caliper control, and silicone anchorage properties. The industry is also experiencing a profound sustainability shift, which is rapidly gaining traction as a waste-free alternative to traditional liners.

Innovation is reshaping performance parameters in construction and industrial segments, as seen in Loparex’s Bubble Liner Technology (Feb 2024)—a breakthrough development offering anti-skid and enhanced handling characteristics for roofing membranes and waterproofing applications. Meanwhile, material circularity has advanced significantly with the launch of Ahlstrom’s Acti-V® RF liners (Sep 2025), integrating up to 15% post-consumer recycled (PCR) fibers, signaling a critical evolution toward a low-carbon, fiber-based release ecosystem.

The global release liners industry is entering a period of rapid innovation and structural transformation, characterized by fiber-based sustainability, circular product design, and digitalization in coating technologies. Leading companies including Ahlstrom, Loparex, Covestro, and Elkem are diversifying their portfolios through recycled material integration, acquisitions, and high-performance filmic substrate advancements.

In October 2025, Ahlstrom launched PurXcel™ molecular filtration media and GreenPod Home, a compostable coffee pod solution leveraging fiber-based release and barrier substrates, illustrating its cross-sector approach to sustainable materials. The following month, Ahlstrom expanded its Acti-V® RF Natural liner series (September 2025), incorporating 50% unbleached fibers and 15% PCR content, reducing total carbon emissions while improving silicone anchorage for high-speed label applications. Earlier in March 2025, the company broadened its North American production footprint by expanding creped base paper manufacturing, reinforcing its leadership in specialty tape release liners.

Meanwhile, Elkem ASA Silicones (April 2025) launched new SILCOLEASE® release coatings incorporating recycled silicone content, advancing its commitment to circularity and low-carbon solutions. Loparex, a long-standing pioneer, reinforced its ESG credentials through its 2024 sustainability report (Nov 2024), detailing renewable energy transitions and workplace safety milestones. In February 2024, Loparex’s introduction of Bubble Liner Technology marked a step forward in construction-grade release performance, offering enhanced elasticity and durability in heavy-duty applications.

Covestro, a major film substrate supplier, strengthened its position through strategic M&A activities—acquiring Pontacol (June 2025) and Vencorex’s US and Thailand sites (August 2025)—boosting its capability to supply specialty films and isocyanate materials for filmic release liners used in electronics and automotive. Ahlstrom’s December 2024 introduction of PFAS-free filtration and transparent tape backings further validated the industry’s commitment to reducing reliance on fluorochemicals and plastics. Concurrently, Techlan Ltd’s Re-Liner™ (Nov 2024), a 100% recycled PE-coated kraft liner, demonstrated scalable commercial viability for circular packaging initiatives.

Market Trend 1: Brand Owner Sustainability Mandates Accelerate Shift to Circular and Recyclable Substrates

The most dominant structural transformation in the release liners market is the accelerated migration toward sustainable, circular, and recyclable liner substrates, driven by top-down corporate mandates and stringent regulatory enforcement. The European Union’s Packaging and Packaging Waste Regulation (PPWR) has emerged as a cornerstone policy, mandating minimum recycled content targets of 30% for contact-sensitive plastic packaging by 2030. These rules indirectly influence non-packaging components like plastic release liners, compelling manufacturers to reengineer liner substrates for recyclability and material recovery.

The transition is being underpinned by large-scale infrastructure investments. For example, in May 2024, a leading global paper and packaging producer announced a €200 million investment to convert its Italian mill into a high-quality recycled containerboard facility with a 420,000-ton annual capacity. The reflects the industry’s pivot toward fiber-based, recycled-content release papers that align with the EU Green Deal’s circular economy goals and brand-owner packaging sustainability commitments.

Simultaneously, major consumer goods manufacturers are targeting 100% recyclable or reusable packaging by 2030, catalyzing the demand for recyclable film liners and bio-based linerstocks. The emphasis is shifting from product performance alone to the total lifecycle impact of liner materials, driving innovation in recycled PET (rPET), PE, and hybrid fiber-polymer composites that maintain release consistency while improving environmental performance.

Market Trend 2: High-Performance Release Liners Enabling EV Battery Manufacturing and Thermal Management

The surge in electric vehicle (EV) battery manufacturing has created a premium demand for high-performance, heat-resistant release liners designed for advanced lamination, insulation, and coating processes. These specialized liners play an essential role in the fabrication of battery separators, dielectric coatings, and thermal interface materials (TIMs)—all critical for maintaining battery safety, energy density, and heat dispersion.

High-performance fluoropolymers such as polyvinylidene fluoride (PVDF)—capable of withstanding thermal stability up to 342°C—are increasingly used in lithium-ion battery coatings. To support such high-temperature processes, durable release liners are required to resist deformation and maintain dimensional accuracy during lamination. The widespread use of vacuum and laser lamination technologies in electrode production further intensifies the need for chemically resistant, non-stick liners capable of operating in high-energy, clean-room environments.

In addition, ongoing R&D in EV battery thermal management is emphasizing the role of reactive adhesive systems and insulating layers, both of which depend on specialized release liners to prevent material contamination during precision coating and curing stages. Patent activity related to thermal runaway prevention and module encapsulation highlights the increasing use of high-tolerance release films in the emerging value chain.

Market Opportunity 1: Smart Release Liners with Integrated Sensing and Digital Traceability

The evolution of the digital supply chain and the rise of IoT-enabled traceability present a groundbreaking opportunity for smart release liners—liners embedded with sensors, printed electronics, or RFID/NFC identifiers to enhance transparency, authenticity, and performance monitoring.

According to a 2024 supply chain digitalization outlook, the rapid convergence of AI, big data analytics, and blockchain is pushing companies to integrate intelligence into even disposable components. Release liners, being ubiquitous across packaging, tapes, and labeling, offer an ideal low-cost substrate for digital traceability and authentication features.

These smart liners could track adhesive batch origins, monitor exposure conditions (temperature, humidity, pressure), and provide tamper evidence or real-time product validation. The ability to integrate such sensors during liner manufacturing opens a new dimension for quality control, anti-counterfeiting, and supply chain monitoring, particularly in pharmaceuticals, electronics, and high-value consumer goods.

In the longer term, the integration of conductive inks, piezoelectric sensors, and QR code micro-patterning into release liners is expected to redefine their functional role—transforming them from passive barriers into intelligent process enablers.

Market Opportunity 2: Ultra-Low Release Force Liners for Next-Generation Medical Hydrogel Adhesives

The expanding medical device and bioadhesive market, particularly in wearable sensors, wound care, and transdermal drug delivery, is creating unprecedented demand for ultra-low release force liners compatible with aggressive and hydrophilic hydrogel adhesives. These applications require precision-engineered liners that release cleanly without residue, maintain surface integrity, and comply with stringent biocompatibility standards.

Recent advancements from specialty materials manufacturers highlight the commercialization of ultra-low extractable silicone liners, offering extractable levels below 30 ng/cm², making them compliant with ISO 10993 medical device testing and regulatory benchmarks for biological safety and cytotoxicity. Such liners ensure that no silicone contamination interferes with drug formulations, biosensors, or adhesive functionality in long-term skin-contact applications.

Additionally, the ongoing phase-out of PFAS-based release coatings across the EU and U.S. is accelerating the shift toward non-fluorinated, organosilicon-based, and plasma-polymerized anti-stick systems. These next-generation coatings maintain low surface energy and moisture resistance, crucial for enabling clean release in hydrogel patches, wound dressings, and bioelectronic interfaces.

Release Liners Market Share Insights, 2025-2034

Market Share by Labeling Technology

Pressure-Sensitive Labeling (PSL) dominates the global release liners market, accounting for an estimated 63.9% share in 2025, driven by its unparalleled versatility and efficiency in high-speed packaging and labeling operations. The technology’s ability to adhere to a vast range of substrates — including glass, plastic, paperboard, and metal — makes it the go-to labeling solution across industries such as food & beverage, logistics, pharmaceuticals, and personal care. PSL technology benefits from easy application, superior print quality, and minimal setup time, enabling brand owners and converters to streamline production. The rise of digital printing, e-commerce packaging, and variable data labeling continues to accelerate demand for pressure-sensitive liners that deliver consistency and compatibility with both permanent and removable adhesives.

In-Mold Labeling (IML) is witnessing strong momentum, particularly in rigid packaging for consumer goods, food containers, and durable goods, offering a seamless aesthetic by integrating labels into molded products. The Glue-Applied/Wet Glue segment remains steady, favored in high-volume beverage and bottled goods packaging where cost-effectiveness is essential. Meanwhile, Shrink and Stretch Sleeve labeling technologies are rapidly growing, driven by the trend toward 360-degree branding and design flexibility in premium beverages, cosmetics, and household products. Linerless Labels represent the most disruptive innovation in the labeling ecosystem, gaining traction due to their sustainability and waste reduction benefits, as they eliminate the need for release liners entirely.

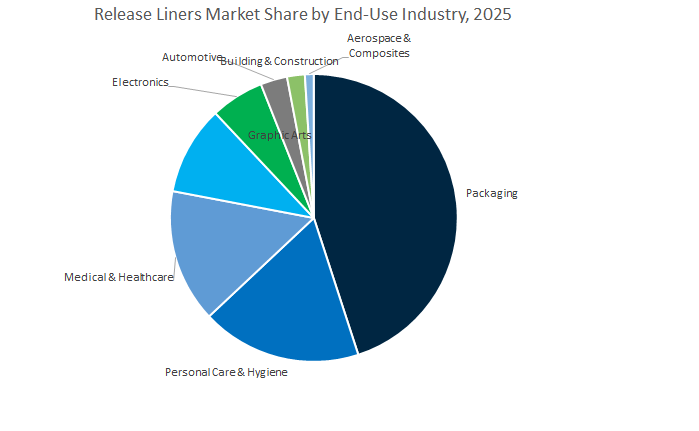

Market Share by End-Use Industry

Packaging leads the global release liners market with a commanding 44.2% share in 2025, propelled by expanding consumption across food, beverage, pharmaceutical, and consumer goods sectors. The segment benefits from continuous global e-commerce growth and the rising need for durable, high-quality, and recyclable label materials that maintain performance through demanding logistics chains. Release liners are indispensable in pressure-sensitive labeling, flexible packaging, and carton sealing, ensuring smooth adhesive application and product protection. Innovations in sustainable liner substrates, PET recyclability, and compostable paper backings are further enhancing the market’s growth trajectory in packaging.

Personal Care & Hygiene follows as a critical end-use segment, leveraging release liners in diaper construction, feminine hygiene products, and cosmetic labels, where precise coating control and skin-safe properties are vital. The Medical & Healthcare industry forms another high-value application area, requiring biocompatible and sterilization-resistant liners for wound care, transdermal patches, and diagnostic devices. Meanwhile, Graphic Arts and Electronics represent sophisticated technical segments, where liners enable lamination films, precision tapes, and electronic component fabrication. In Automotive, Construction, and Aerospace, release liners support industrial-grade bonding, insulation, and composite molding operations that demand heat resistance, chemical stability, and dimensional precision. These sectors rely on advanced liners that ensure reliable adhesive transfer and release under extreme conditions.

The competitive landscape of the Global Release Liners Market is dominated by major players such as Loparex, UPM Raflatac, Ahlstrom, and Lecta Group, each leveraging material innovation, circularity, and supply chain integration to strengthen their market position. Their combined focus on sustainability, high-speed coating performance, and fiber optimization is redefining industry benchmarks.

Loparex stands as a global leader in silicone release liners and films, with end-to-end capabilities spanning film extrusion, coating, and lamination. Its Bubble Liner Technology (Feb 2024) innovation provides superior anti-skid and elasticity performance, setting new standards for construction-grade release liners. The company’s ISCC PLUS certification pursuit (2025) for its Hammond and Malvern facilities underscores its shift toward certified sustainable feedstock utilization. As a founding member of CELAB, Loparex is actively advancing label liner recycling and circular recovery systems worldwide.

UPM Raflatac, a major division of UPM Group, continues to innovate across self-adhesive label materials and release liner technologies. Its portfolio includes high-performance Glassine, SCK, and filmic liners tailored for logistics, beverage labeling, and personal care packaging. With a robust Net debt/EBITDA ratio of 1.77 (Q1 2025), the company maintains strong financial leverage for innovation and sustainability investments. As the only forest industry firm listed on both Dow Jones Global and European Sustainability Indices (2024–2025), UPM is a frontrunner in responsible fiber sourcing. Its parent company’s large-scale investments in biorefinery assets and decarbonization projects are directly reducing the energy intensity of release liner production.

Ahlstrom leads the fiber-based specialty materials market, offering a comprehensive portfolio of Glassine, CCK, and SCK liners for PSA, tape, and medical applications. In September 2025, it launched Acti-V® RF Natural liners containing unbleached fibers and recycled content, aligning with customer sustainability goals. The acquisition of Stevens Point (2025) expanded its digital printing-grade liner capacity, while its LamiBak range (2024)—certified for food contact (BfR XXXVI/2)—opened new opportunities in baking and packaging applications. Ahlstrom’s strategy centers on reducing plastic dependency and promoting renewable, circular fiber innovations for next-gen release papers.

Lecta Group, through its Linerset and Adestor brands, is a key European force in paper-based release solutions. Its Linerset portfolio—including CCK, Glassine Y/W, and SCK grades—offers optimized siliconization performance, rigidity, and stability for converters. The company’s adherence to FSC™ and PEFC™ certifications ensures responsible forestry sourcing. In July 2025, Lecta’s Adestor division launched Clear-on-Clear label materials, employing high-transparency filmic liners to serve the premium beverage and cosmetics sectors. By expanding into barrier base papers (Linerset FP), Lecta is bridging the gap between release and flexible packaging markets, enhancing product diversification and sustainability performance.

Country Analysis: Key Regional Growth Drivers and Industrial Advancements in the Global Release Liners Industry

United States: Expanding Recycling Infrastructure and High-Performance Release Liner Innovation

The United States release liner industry continues to set global benchmarks for technical innovation, recycling integration, and sustainable manufacturing, led by advancements in pressure-sensitive adhesive (PSA) tapes, medical-grade liners, and EV-related applications. A major industry consortium partnered with a leading PSA film producer in Q3 2025 to scale PET film liner and silicone-coated paper recycling capacity in the Midwest, representing a critical shift toward circular material management in liner waste recovery. Meanwhile, the EV revolution is driving exponential demand for high-heat-resistant double-sided foam tape liners used in battery pack assembly and thermal management applications, positioning the U.S. as a leading innovation hub in automotive-grade liner technology.

The U.S. medical and electronics industries continue to push boundaries, investing in ultra-thin, cleanroom-ready PET release films for advanced wound care, transdermal patch systems, and precision electronic tape assembly. Furthermore, defense and aerospace manufacturers are adopting fluorosilicone-coated release films for their ability to perform under extreme temperature and altitude conditions. Sustainability commitments are also shaping the sector — a prominent converter pledged to source 100% certified sustainable base paper for glassine and PCK release liners by 2026, aligning with ESG and brand-owner mandates. Additionally, the growing adoption of Extended Producer Responsibility (EPR) legislation across several states is catalyzing investment in linerless label solutions, positioning the U.S. at the forefront of recyclable and waste-minimizing release liner innovation.

China: World’s Largest Production Base Embracing Green Manufacturing and Digital Label Expansion

China dominates the global release liner market, driven by industrial scale, government-backed R&D, and its rapidly expanding e-commerce and EV ecosystems. A major domestic substrate producer in Jiangsu province announced a Q1 2025 production line expansion, adding hundreds of millions of square meters in BOPP and PET release films capacity for label stock and flexible electronics applications. Parallel to The, China’s green packaging policy framework is catalyzing the shift to bio-based, compostable paper liners—particularly in FMCG and food packaging sectors—to meet strict low-VOC and waste-reduction mandates.

China’s logistics automation boom, powered by giants like Alibaba and JD.com, is boosting demand for cost-efficient PP film liners suitable for high-speed labeling and parcel sealing. Meanwhile, the country’s leadership in semiconductor and EV production is fostering innovation in polyimide (PI) and PET liners designed for particle-free, ultra-low release-force performance, essential for chip fabrication and battery assembly. To support The goals, government-funded R&D in Shanghai is developing domestic platinum catalysts for UV-curable silicone coatings, strengthening national raw material self-sufficiency. Combined with ongoing capital investment in PE-coated paper liners for construction and industrial tapes, China’s release liner market is rapidly evolving toward technologically advanced, sustainable, and self-reliant production capabilities.

Germany: Engineering Precision and Circular Economy Integration in Release Liner Manufacturing

Germany stands as Europe’s engineering and sustainability powerhouse in the release liner domain, with deep expertise in automotive-grade precision liners, renewable substrates, and non-silicone coating chemistry. The German automotive sector’s stringent OEM standards have led to the commercial launch of highly dimensionally stable PET film liners, delivering exceptional die-cutting accuracy for trim bonding, mirror mounting, and sensor adhesion tapes. Compliance with the EU’s circular economy and waste directives is driving participation in pan-European collection and recycling programs, ensuring the large-scale recovery of silicone-coated liner waste from converters.

Innovation is thriving in UV-curable, solvent-free coating systems, as demonstrated by a major German specialty chemicals company’s 2024 breakthrough in non-silicone UV-curable coatings, offering a sustainable alternative for label stock used in logistics and consumer goods packaging. At the same time, the growth of the wind energy industry is increasing demand for wide-format, high-temperature release films used in prepreg composites for turbine blades. Digital transformation is reshaping production efficiency, with major firms integrating AI and IoT-enabled sensors on coating lines to ensure uniform siliconization and defect-free surfaces, underscoring Germany’s leadership in high-precision, Industry 4.0-enabled release liner manufacturing.

India: Domestic Manufacturing Boom and Policy-Driven Market Expansion

India’s release liner market is in an accelerated growth phase, supported by government-led industrialization, infrastructure expansion, and green manufacturing mandates. The 2025 plastic waste management regulation, which mandates recycled content in packaging, has directly spurred the use of PCR-based PET film liners in the packaging and label stock sectors. The pharmaceutical industry continues to drive demand for high-security label liners, with a new release liner production facility in Gujarat (H1 2025) dedicated to tamper-evident and compliance-grade labeling for generic drug exports.

The e-commerce and retail logistics explosion has created unprecedented demand for lightweight glassine and PET film liners used in address labels and warehouse tracking systems. Local manufacturers, buoyed by the “Make in India” initiative, are scaling capacity for domestic PET film production, supported by government incentives for export-led manufacturing. Simultaneously, India’s adoption of the Eco-Mark Rules 2024 is driving the uptake of environmentally certified paper liners, further aligning its adhesive and coating sector with global sustainability frameworks. Through a combination of policy reform, localized production, and technology investment, India is emerging as one of the most dynamic release liner markets in the Asia-Pacific region.

Japan: Precision Coating Leadership and Advanced Hydrogen Fuel Cell Applications

Japan remains a global epicenter for ultra-high-precision release liner technology, catering to electronics, automotive, and hydrogen energy sectors. Major Japanese chemical firms are introducing polyethylene naphthalate (PEN) release liners for OLED displays and flexible circuit boards, where superior optical clarity and surface uniformity are non-negotiable. Innovation extends to the hydrogen economy, where R&D is focused on PTFE-coated and fluorosilicone release films engineered for fuel cell tape assembly, combining chemical inertness, dielectric stability, and long-term durability.

Leading manufacturers are also experimenting with bio-based PE-coated papers to replace traditional polyolefin liners, maintaining coatability while meeting the country’s carbon neutrality targets. The stringent precision standards in Japan’s medical and electronics manufacturing industries are fostering demand for caliper-stable film liners, capable of supporting micron-level die-cutting accuracy in miniaturized medical components. The innovations reinforce Japan’s global standing as a technology-driven leader in functional and sustainable release liner systems.

Finland: Fiber-Based Innovation and Circular Material Integration in Release Liner Production

Finland’s pulp and paper excellence positions it as a leader in sustainable fiber-based release liner innovation within the global market. Industry giants such as UPM and Ahlstrom are investing heavily in fiber-based barrier papers and silicone-coated sustainable liners that minimize polymer use while optimizing recyclability and fiber integrity. Collaborative R&D between Finnish universities and bio-materials companies is advancing the use of cellulose nanofibers (CNF) to develop lightweight, high-strength barrier layers for next-generation release liners.

The country’s integrated pulp and paper production infrastructure ensures a fully traceable, certified supply chain for glassine and calendered kraft substrates, aligning with EU environmental standards and brand transparency goals. Finland is also spearheading trials of linerless label solutions across logistics and supply chain networks, aiming to reduce overall waste from traditional silicone-coated liners. By combining forest-based circular innovation, advanced fiber chemistry, and renewable material science, Finland has become a critical node in the transition toward a sustainable, low-carbon release liner industry.

Release Liners Market Report Scope

Release Liners Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$201.6 Billion

|

|

Market Size (2034)

|

$380.1 Billion

|

|

Market Growth Rate

|

7.3%

|

|

Segments

|

By Material Type (Silicone, Non-Silicone), By Substrate Type (Paper-Based, Film-Based), By Labeling Technology (Pressure-Sensitive Labelling, Linerless, Glue-Applied/Wet Glue, In-Mold, Shrink/Stretch Sleeves), By Application (Label Stock, Pressure Sensitive Tapes, Medical & Hygiene, Industrial, Other Applications), By End-Use Industry (Packaging, Automotive, Electronics, Medical & Healthcare, Building & Construction, Personal Care & Hygiene, Graphic Arts, Aerospace & Composites

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Mondi Group, Avery Dennison Corporation, Loparex LLC, UPM Specialty Papers, LINTEC Corporation, Ahlstrom, Sappi Limited, Gascogne Papier, Polyplex Corporation Ltd., 3M Company, Elkem ASA, Felix Schoeller Group, Wausau Coated Products Inc., Mitsubishi Chemical Group Corporation, SWM International (Mativ)

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

By Material Type

By Substrate Type

By Labeling Technology

- Pressure-Sensitive Labelling

- Linerless

- Glue-Applied/Wet Glue

- In-Mold

- Shrink/Stretch Sleeves

By Application

- Label Stock

- Pressure Sensitive Tapes

- Medical & Hygiene

- Industrial

- Other Applications

By End-Use Industry

- Packaging

- Automotive

- Electronics

- Medical & Healthcare

- Building & Construction

- Personal Care & Hygiene

- Graphic Arts

- Aerospace & Composites

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in Release Liners Market

- Mondi Group

- Avery Dennison Corporation

- Loparex LLC

- UPM Specialty Papers

- LINTEC Corporation

- Ahlstrom

- Sappi Limited

- Gascogne Papier

- Polyplex Corporation Ltd.

- 3M Company

- Elkem ASA

- Felix Schoeller Group

- Wausau Coated Products Inc.

- Mitsubishi Chemical Group Corporation

- SWM International (Mativ)

*- List not Exhaustive

Research Coverage

Developed by USDAnalytics, this report investigates the Release Liners Market end-to-end, delivering analysis reviews on demand shifts, liner engineering, converting economics, and regulatory risk; it highlights breakthroughs in fiber-rich, recycled-content papers, low-platinum silicone systems, high-temperature film liners for EV batteries, linerless label architectures, and digital traceability features that elevate throughput and sustainability; benchmarking supplier strategies, cost drivers, and performance windows (release force, anchorage, caliper stability, and coat-weight control), this report maps how innovation and circularity reshape label stock, tapes, medical, electronics, and industrial workflows—this report is an essential resource for converters, packaging leaders, and procurement teams seeking specification clarity, reliable forecasts, and actionable competitive insight.

Scope Highlights

Segmentation:

- By Material Type: Silicone; Non-Silicone.

- By Substrate Type: Paper-Based; Film-Based.

- By Labeling Technology: Pressure-Sensitive Labelling; Linerless; Glue-Applied/Wet Glue; In-Mold; Shrink/Stretch Sleeves.

- By Application: Label Stock; Pressure Sensitive Tapes; Medical & Hygiene; Industrial; Other Applications.

- By End-Use Industry: Packaging; Automotive; Electronics; Medical & Healthcare; Building & Construction; Personal Care & Hygiene; Graphic Arts; Aerospace & Composites.

- By Region: North America (United States, Canada, Mexico); Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe); Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC); South & Central America (Brazil, Argentina, Rest of SCA); Middle East & Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa).

Geographic Scope: Analysis spans 25+ countries across North America, Europe, Asia Pacific, Latin America, the Middle East & Africa.

Time Horizon: Historic data 2021–2024 and forecast data 2025–2034.

Companies Covered: Analysis / profiles of 15+ companies (global leaders and regional specialists).

Deliverables

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.