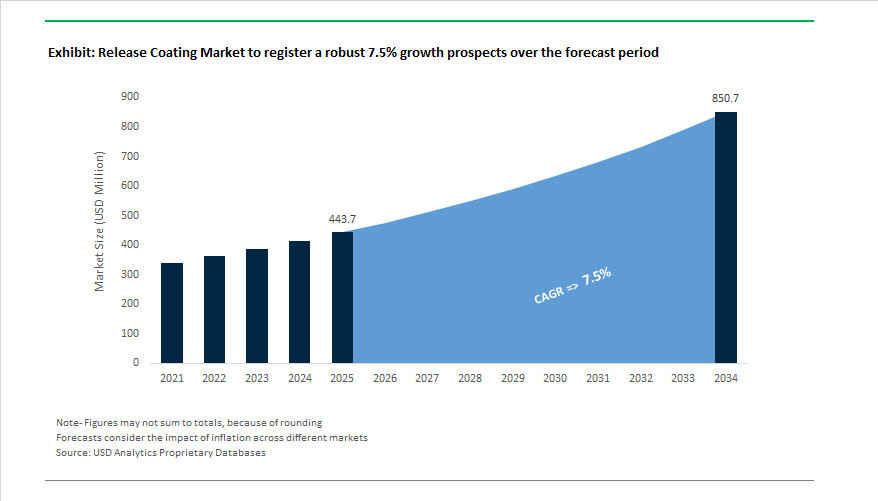

The Global Release Coating Market is poised to expand from $443.7 million in 2025 to $850.7 million by 2034, exhibiting a CAGR of 7.5%. The market’s acceleration is underpinned by the rising consumption of silicone-based release systems, the widespread adoption of solventless and UV-curable technologies, and strong growth across packaging, healthcare, and pressure-sensitive labeling industries. These coatings play a vital role in preventing adhesion during converting and manufacturing processes, ensuring material efficiency, recyclability, and high-speed production performance.

Silicone release agents dominate the landscape, driven by their unmatched thermal stability, non-reactivity, and substrate versatility. Within application segments, the packaging sector—particularly labels and tapes—represents the largest consumer base, reflecting the global demand for pressure-sensitive labeling in logistics, e-commerce, and consumer goods. The medical applications segment is emerging as one of the fastest-growing, spurred by the proliferation of wearable medical devices, wound dressings, and drug delivery patches that require biocompatible and precise release characteristics.

At the same time, the industry’s sustainability trajectory is accelerating with a shift toward solventless, UV-curable, and low-VOC silicone release systems, driven by stricter global environmental mandates and a preference for carbon-neutral formulations. Regions like North America are at the forefront of adopting these high-speed, energy-efficient release technologies, integrating automation and clean manufacturing standards.

The Global Release Coating Industry is undergoing a dynamic phase of transformation led by sustainability, innovation in curing chemistry, and significant investments in capacity expansion. Leading companies such as Dow, Elkem, BASF, Axalta, and Shin-Etsu have introduced carbon-neutral, recyclable, and next-generation coating systems designed for high-speed converting and low-environmental-impact production.

In September 2023, Dow launched its SYL-OFF Protect range, a carbon-neutral silicone release coating certified under PAS 2060, setting a new sustainability benchmark for pressure-sensitive label manufacturers. This product line combines low-carbon footprint performance with the same release efficiency as conventional systems, aligning with global decarbonization goals. Shortly after, in early 2024, Elkem Silicones announced that its silicone products manufactured in Europe and the Americas carry a 30% lower carbon footprint than the industry average, helping customers achieve Scope 3 emission reductions within the release liner value chain.

In 2024, Elkem further advanced circularity by investing in a chemical recycling pilot plant in France, transforming post-industrial silicone waste into recycled silicone polymers. This initiative directly supports the transition toward a closed-loop material economy in the release coating sector. Meanwhile, BASF’s October 2025 transaction with Carlyle to divest its automotive OEM coatings and refinish businesses highlights the growing focus on specialized performance coatings. BASF also introduced Ameriflor™ Calm (Oct 2025)—a high-purity, botanical-based ingredient derived from its specialty chemical research—demonstrating the crossover innovation that informs non-silicone release coating chemistry for medical and personal care applications.

Shin-Etsu Chemical reinforced its global leadership in silicone materials by announcing an ¥80 billion investment (FY 2023–2024) to expand capacity for advanced functional silicones used in high-performance release coatings, particularly for electronics and precision industrial films. Axalta Coating Systems made significant strides through product and strategic initiatives, unveiling Evergreen Sprint (Jan 2025) as the 2025 Global Automotive Color of the Year, which indirectly highlights evolving needs for temporary protective and masking release agents in automotive painting. Furthermore, Axalta’s partnership with Dürr (Q1 2025) signifies a leap toward digitally integrated coating systems, where release coatings contribute to streamlined, contamination-free surface treatments.

Across 2024–2025, leading producers like WACKER and Momentive maintained their R&D focus on UV-curing and electron beam (EB) release coating technologies, offering converters enhanced line speed, low energy consumption, and precise release control—a critical differentiator for high-speed label manufacturing and premium film applications.

Market Trend 1: Rapid Commercialization of Silicone-Free Release Coatings for Circular Packaging and Labeling

The most significant transformation in the release coating market is the shift from traditional silicone-based systems to silicone-free, recyclable, and bio-derived release coatings, driven by the global circular economy framework and EPR (Extended Producer Responsibility) obligations for packaging materials.

A surge in water-based and solvent-free emulsion PSAs is allowing manufacturers to produce durable, silicone-free release liners that maintain critical peel and release performance. A notable example is the 2024 launch by a major U.S.-based polymer producer of a new solvent-free PSA emulsion designed for durable labels and tape applications, offering both cost efficiency and low-VOC compliance. These formulations eliminate silicone waste from recycling streams, enabling mono-material packaging compatibility and supporting closed-loop sustainability objectives.

Data from the Ellen MacArthur Foundation’s Global Commitment Report (2024) shows that signatory corporations—responsible for around 20% of global plastic packaging output—are targeting significant virgin plastic reductions and recyclability compliance, which necessitates the adoption of silicone-free release papers and films. In addition, global CPG leaders like Unilever are investing in bio- and mineral-sourced coating materials for paper-based flexible packaging, using non-silicone internal release layers to replace multilayer plastic laminates.

The industry’s technological momentum is further strengthened by substrate innovation. The Bubble Liner Technology, introduced in early 2024, improved liner stability and substrate performance under diverse humidity and pressure conditions. The evolution drives the industry-wide focus on liner optimization and high-performance silicone-free commercial solutions, meeting sustainability targets while ensuring cost and performance parity with silicone-based products.

Market Trend 2: Integration of High-Temperature Durable Release Films in Electric Vehicle Battery Manufacturing

As the EV battery market scales rapidly, the demand for high-heat resistant and chemically stable release coatings has intensified. These specialized coatings are indispensable in the lamination, insulation, and encapsulation processes used during EV battery assembly.

During electrode lamination, where temperatures can exceed 160°C, high-temperature release films are critical for ensuring safe adhesion, uniform coating, and precise bonding between layers. Patented EV battery manufacturing processes highlight the importance of release films with superior dimensional stability and chemical resistance, preventing adhesion failure during solvent evaporation and high-pressure lamination stages.

Innovations such as laser lamination technologies in electrode fabrication require release coatings that can withstand localized energy bursts without deformation. These next-generation chemically resistant and thermally robust films are being integrated into EV production lines to support energy density optimization and thermal runaway prevention—two central challenges in modern battery manufacturing.

Further, clean-room production standards in battery assembly demand anti-contamination release liners with high dielectric performance to protect thermal interface materials (TIMs) and dielectric coatings. The has created a new premium market segment for durable release liners engineered for EV battery pack integrity and thermal control, expected to expand significantly through 2030.

Market Opportunity 1: Functionalized and Patterned Release Coatings for Additive Manufacturing Applications

The next frontier for the release coating market lies in functionalized, pattern-engineered coatings designed for 3D and 4D printing processes, enabling high-precision release, material control, and post-print functionalization.

According to 2024 studies on Functional Additive Manufacturing, advanced printing technologies increasingly demand patterned release surfaces capable of influencing part geometry, mechanical properties, or even chemical reactivity during and after printing. These coatings serve dual roles—facilitating separation while acting as functional templates or catalysts for the printed material.

In bio-printing and soft polymer fabrication, functionalized release coatings can impart surface texturing or hydrophilic/hydrophobic modulation, critical for producing hydrogel-based devices, flexible electronics, and polymer composites. Such coatings can enable architectural reconfiguration or biofunctionalization in post-processing, acting as temporary scaffolds for high-value biomedical and electronic components.

In the biomedical domain, particularly in microfluidic and diagnostic device manufacturing, engineered release coatings allow precise pattern transfer and controlled shrinkage in high-resolution lithographic processes. The makes them indispensable in next-generation lab-on-chip devices and flexible biosensor production, expanding their role beyond passive detachment layers to functional performance enhancers.

Market Opportunity 2: PFAS-Free, Low-Surface-Energy Release Coatings for the Medical Hydrogel Patch Market

The medical and pharmaceutical industries are at the forefront of adopting PFAS-free, non-fluorinated release coatings, driven by tightening regulatory scrutiny on per- and polyfluoroalkyl substances (PFAS) across Europe and North America.

The European Chemicals Agency (ECHA) has announced a proposal to restrict or ban PFAS usage by 2025, prompting medical device manufacturers to redesign their coating systems. The regulatory landscape is directly reshaping demand in the medical hydrogel patch and wound care sector, where ultra-low release force and hydrophilic compatibility are critical for skin-contact adhesives.

R&D initiatives led by organizations like the Fraunhofer-Gesellschaft have yielded organosilicon-based and plasma-polymer release systems, achieving equivalent or superior anti-stick performance to fluorinated coatings—without persistent environmental impact. These systems demonstrate reliable release behavior across a variety of medical-grade hydrogel adhesives and silicone gels, making them ideal for drug delivery patches, wound dressings, and wearable medical sensors.

Recent studies on ophthalmic hydrogel patches have showcased the precision required from release coatings—where low-surface-energy multilayer films enable accurate gel transfer onto ocular tissue, ensuring adhesive integrity, sterilization compatibility, and biocompatibility. Such innovations illustrate the growing market potential for PFAS-free, medical-grade release liners tailored to the next generation of bio-adhesive devices.

Release Coating Market Share Insights, 2025-2034

Market Share by Material Type / Chemistry

Silicone Release Coatings dominate the global release coating market, accounting for an estimated 77.6% share in 2025, driven by their unmatched performance versatility and broad compatibility across diverse substrates. Silicone systems deliver exceptional thermal stability, chemical resistance, and controlled release properties, making them indispensable in high-speed coating operations for labels, tapes, composites, and industrial films. Their adaptability across curing technologies — including addition-cure, condensation-cure, and UV-cure systems — allows formulators to tailor coatings for specific end-use performance, whether in low-friction industrial liners or premium-grade medical applications. The dominance of silicone-based coatings is further reinforced by their superior anchorage, release consistency, and resistance to migration, essential for critical uses in electronics, hygiene, and food-grade applications. As sustainability gains traction, major producers are advancing solvent-free, low-platinum, and high-solids silicone systems that enhance cost efficiency and environmental compliance, further consolidating silicone’s leadership position in the release coatings market.

Non-Silicone Release Coatings, while holding a smaller share, play a pivotal role in specialized markets demanding unique adhesion or sustainability characteristics. These include acrylate-based coatings used in printing and graphic applications, fluoropolymer-based formulations for extreme chemical and temperature resistance, and bio-based polymers catering to eco-friendly product lines. The ongoing shift toward recyclable and compostable substrates has prompted innovation in non-silicone and hybrid systems that deliver high release control without silicone migration, particularly for food packaging, hygiene products, and sustainable labeling.

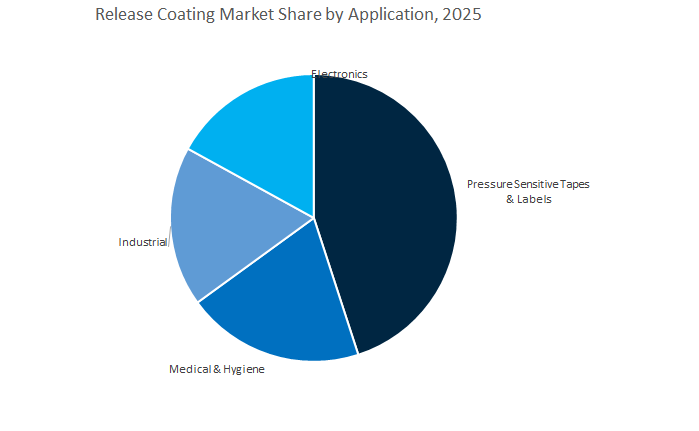

Market Share by Key Application

Pressure Sensitive Tapes and Labels remain the largest and most influential segment in the global release coatings industry, commanding approximately 44.4% market share by 2025. The dominance of this segment is attributed to the explosive global growth of packaging, logistics, and labeling industries, where release coatings are integral to producing self-adhesive labels, tapes, and protective films. Silicone release coatings, in particular, are preferred for pressure-sensitive adhesive (PSA) systems, ensuring consistent release force, clarity, and liner performance during high-speed production. The rapid expansion of e-commerce, FMCG, and retail labeling continues to boost demand for reliable, efficient release coatings that support diverse applications such as shipping labels, product identification, and tamper-evident packaging.

The medical and hygiene sector forms the second-largest and most innovation-driven end-use segment, relying on ultra-pure, skin-compatible release coatings for wound care products, surgical tapes, and transdermal drug delivery systems. These applications demand coatings with low migration, biocompatibility, and sterilization stability, driving the adoption of solvent-free silicone and UV-cured systems. Industrial applications represent a critical segment encompassing composite prepregs, mold release films, and food processing liners, where release coatings provide durability, precision, and chemical resistance under extreme conditions. In electronics, release coatings are gaining momentum as enablers of advanced manufacturing processes, including display films, semiconductor wafer processing, and flexible printed circuits, where high surface quality and precision are essential.

The Global Release Coating Market is driven by major chemical manufacturers—Dow, WACKER, Momentive, Shin-Etsu Chemical, and Elkem Silicones—who are reshaping the market with low-carbon technologies, next-generation UV-curing systems, and high-speed converting capabilities. Their competitive advantage lies in vertically integrated silicone production, strong R&D pipelines, and global supply chain resilience to serve the fast-evolving packaging, electronics, and healthcare industries.

Dow continues to dominate the release coating landscape through its flagship SYL-OFF™ brand, offering solventless, emulsion-based, and platinum-catalyzed silicone systems for film and paper substrates. The company’s SYL-OFF Protect range (Sept 2023) marked the industry’s first certified carbon-neutral silicone coating, helping label manufacturers reduce environmental impact without sacrificing line speed or cure reliability. Dow’s deep integration across siloxane production ensures unmatched control over raw material quality, while its fluorosilicone-based solutions extend performance for aggressive PSA and industrial films. With global service hubs and specialized technical teams, Dow continues to set the standard for sustainable, high-performance release technologies.

WACKER stands as a global leader in E-coating and silicone-based release systems, leveraging its WACKER® and E-PLEX® product lines to deliver solventless and UV-curable coatings optimized for energy efficiency and fast processing. The company’s focus on customized release profiles—from easy to tight release—caters to diverse industrial demands, while its innovations in linerless label formulations are redefining packaging efficiency by reducing waste. WACKER’s strategic investments in anchor optimization and substrate adhesion control enable converters to achieve superior bath life and uniform coating performance across challenging filmic substrates.

Momentive maintains a strong foothold in advanced silicone release coatings with expertise in thermal stability, non-stick performance, and electromechanical resistance. Its focus on 100% silicone-based and UV-curing systems has positioned it as a preferred partner for EV battery, protective film, and medical device applications. The company’s ongoing R&D initiatives target next-generation silicone chemistries for high-stress and high-temperature environments, ensuring reliability in automotive and healthcare uses. Momentive’s global supply reliability and diversified silicone product portfolio make it a trusted supplier to converters demanding consistency and regulatory compliance.

Shin-Etsu Chemical continues to strengthen its position through vertical integration and large-scale investments in functional silicone capacity. The company’s ¥80 billion capital plan (FY 2023–2024) supports the production of eco-efficient and specialty silicone materials for electronics, medical, and industrial film release coatings. By leveraging its global production footprint—spanning 67 overseas facilities in 17 countries—Shin-Etsu ensures unparalleled supply stability. Its focus on R&D-driven precision chemistry enables tailored release profiles for high-demand industries such as semiconductors and technical laminates, reaffirming its reputation for premium, high-consistency silicone systems.

Elkem Silicones leads the sustainability transition in the release coating space through its SILCOLEASE® product line and low-carbon production processes. Its Europe- and Americas-based silicone operations operate with a 30% lower carbon footprint than the industry average, leveraging renewable hydroelectric power and bio-based carbon sources. The company’s 2024 investment in a recycling pilot unit in France aims to chemically reclaim post-industrial silicone waste, underscoring its circular economy strategy. Elkem’s customized formulations deliver superior anchorage, fast curing, and high-speed coating performance, enabling customers to meet both sustainability and efficiency targets in industrial and packaging release applications.

Country Analysis: Regional Advancements and Innovation Trends in the Global Release Coating Industry

United States: Leading in Silicone and Non-Silicone Release Coating Technologies for High-Performance Applications

The United States release coating industry stands at the forefront of silicone and high-performance non-silicone innovation, driven by the expanding medical, automotive, aerospace, and specialty packaging sectors. In 2024, a major U.S.-headquartered specialty materials company launched a new generation of high-speed, low-platinum addition-cure silicone coatings tailored for pressure-sensitive adhesive (PSA) labels and industrial release liners, responding to the fast-evolving packaging and e-commerce ecosystem. A leading global materials conglomerate also announced a multi-million-dollar expansion at its Michigan facility to increase production capacity for fluorosilicone release coatings, catering to high-performance electronics and aerospace composite prepreg applications that demand extreme durability and chemical resistance.

Further strengthening The momentum, the FDA’s approval of next-generation polymeric materials has spurred development of medical-grade silicone release coatings used in advanced wound care and transdermal drug delivery systems, where ultra-consistent release profiles and low extractable content are critical. Academic and industrial R&D collaborations across the U.S. are now focused on bio-based, non-silicone alternatives, aimed at compostable and recyclable release liners that address sustainability concerns in e-commerce and food packaging. Additionally, a global chemical leader with extensive U.S. operations has pivoted its portfolio toward water-based silicone emulsions for zero-VOC baking papers and sustainable food-contact packaging, underlining America’s pivotal role in eco-conscious material transformation and functional coating innovation.

Germany: Sustainability-Led Growth and Automotive Adhesion Control Innovation

Germany’s release coating sector continues to lead European sustainable chemical manufacturing, propelled by stringent VOC regulations, automotive engineering excellence, and a push for circular economy solutions. The enforcement of EU-level directives on VOC emissions has accelerated the adoption of solventless and UV-LED-curable silicone coatings, particularly for technical tapes, protective films, and high-performance industrial labels. A major German specialty chemicals firm introduced organo-modified polysiloxane coatings in 2024, offering differential release performance ideal for high-tack acrylic and rubber-based PSA systems used in vehicle assembly and structural bonding.

In alignment with the EU’s sustainability objectives, a prominent German chemical producer commissioned a new production line dedicated to water-based non-silicone emulsions, addressing the rising demand for repulpable and recyclable paper-based release liners. Additionally, Germany’s academic institutions are deeply involved in functional coating R&D, collaborating with manufacturers to develop multi-functional coatings—for example, anti-scratch, anti-fouling, and UV-protective films with built-in release properties. The convergence of sustainability, precision engineering, and functional performance solidifies Germany’s position as a global hub for high-efficiency, next-generation release coatings that meet the evolving standards of automotive, packaging, and construction sectors.

China: Expanding Capacity and Technological Modernization in Release Coating Manufacturing

China remains the largest global production base for release coatings, underpinned by rapid industrial scaling, EV manufacturing expansion, and digital label adoption. Throughout 2024, several major domestic release liner manufacturers announced substantial capacity additions for CCK (Clay Coated Kraft) and Glassine paper with integrated silicone coating lines to meet skyrocketing domestic and export demand in the PSA label industry. The government’s push toward industrial digitization has fast-tracked the replacement of legacy solvent-based systems with high-speed UV-curable silicone coating technologies, improving productivity and compliance with national emission standards.

The nation’s growing EV battery manufacturing ecosystem has become a vital consumer of thermally stable polymeric film release liners, essential in producing battery cell components, protection films, and thermal management tapes. Moreover, provincial authorities are establishing high-end film and coating industrial parks designed to consolidate the release liner value chain, offering tax incentives to attract global and domestic players. The government’s environmental agenda is also stimulating R&D in bio-based, low-VOC coating chemistries, ensuring China maintains leadership not only in production capacity but also in the transition to green manufacturing for packaging, labels, and industrial applications.

Japan: Advancing Ultra-Precision and Non-Silicone Release Coatings for Electronics and Optical Films

Japan’s release coating market exemplifies technological precision, miniaturization, and material science excellence, particularly for semiconductors, optical films, and advanced display manufacturing. Domestic chemical innovators are pioneering non-silicone, polyacrylate-based release coatings compatible with UV-curing acrylic adhesives, providing contamination-free performance in OLED, microLED, and flexible display fabrication—where silicone migration is strictly restricted. A leading Japanese chemical manufacturer has also launched ultra-thin, high-uniformity silicone films for flexible printed circuit boards (FPCBs) and microelectronic assembly, achieving exceptional coat weight consistency critical to miniaturized device assembly.

Ongoing R&D investments aim to enhance the thermal stability, solvent resistance, and release durability of coatings for aerospace composite prepregs, which require stable performance under high-temperature curing cycles. Japan’s continuous innovation in non-silicone polymer technology, advanced process control, and hybrid coating systems keeps it at the forefront of the high-performance release liner market, setting global benchmarks in precision film technology and semiconductor-grade coating innovation.

India: Expanding Domestic Manufacturing and Packaging-Driven Release Coating Demand

India’s rapid industrialization and surging packaging consumption are catalyzing the growth of its release coating industry, particularly in pressure-sensitive labels, tapes, and food packaging. The “Make in India” initiative and accelerated modernization of the food and pharmaceutical sectors are strengthening domestic production capabilities for high-quality silicone-coated release liners used in pharmaceutical labeling and FMCG packaging. Rising e-commerce penetration and logistics digitization have further fueled demand for durable PSA release films that ensure product safety during transport.

Local coating manufacturers are transitioning toward water-based silicone emulsions and solventless thermal-cure coatings to balance cost competitiveness with environmental compliance. Simultaneously, several international specialty chemical companies have partnered with Indian firms to localize release coating production, enabling supply chain stability and import substitution. The construction of new coating plants and joint ventures in Gujarat and Maharashtra underscores India’s emergence as a regional production hub for eco-friendly, high-performance release coatings that serve the packaging, industrial tape, and hygiene film segments.

European Union (EU): Regulatory Transformation Driving Circular Economy and Linerless Technologies

The European Union’s sustainability agenda continues to define the global trajectory of release coating development, enforcing policies aligned with the European Green Deal and the Circular Economy Action Plan. The implementation of new food contact material regulations—restricting bisphenol A (BPA) and similar endocrine-disrupting substances—has accelerated the formulation of non-epoxy, non-silicone release coatings for food and pharmaceutical packaging.

Leading European materials firms are piloting fully recyclable, fiber-based release liners that utilize proprietary barrier coatings, maintaining high PSA performance while enabling paper recyclability. The region is also at the forefront of linerless label innovation, with investments from label manufacturers and trade associations in UV-curable, self-wound release coatings that eliminate liner waste entirely—reducing environmental impact across logistics and retail labeling applications. By combining stringent regulation, R&D leadership, and circular design, the EU remains a catalyst for sustainable transformation in the global release coating and liner substrate market.

Release Coating Market Report Scope

Release Coating Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$443.7 Million

|

|

Market Size (2034)

|

$850.7 Million

|

|

Market Growth Rate

|

7.5%

|

|

Segments

|

By Material Type (Silicone, Non-Silicone), By Formulation Technology (Solventless, Water-based, Solvent-borne, High-Solids), By Substrate (Paper-Based, Film-Based, Fabric/Non-woven), By Application (Pressure Sensitive Tapes & Labels, Industrial, Medical & Hygiene, Electronics

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Dow Inc., Wacker Chemie AG, Elkem ASA, Shin-Etsu Chemical Co., Ltd., Momentive Performance Materials, BASF SE, Evonik Industries AG, Avery Dennison Corporation, Loparex, LINTEC Corporation, Mitsubishi Chemical Corporation, Mondi Group, Fujifilm Holdings Corporation, Rayven Inc., Felix Schoeller Group

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

By Material Type / Chemistry

By Formulation Technology

- Solventless

- Water-based

- Solvent-borne

- High-Solids

By Substrate / Release Liner Type

- Paper-Based

- Film-Based

- Fabric/Non-woven

By Key Application / End-Use

- Pressure Sensitive Tapes & Labels

- Industrial

- Medical & Hygiene

- Electronics

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in Release Coating Market

- Dow Inc.

- Wacker Chemie AG

- Elkem ASA

- Shin-Etsu Chemical Co., Ltd.

- Momentive Performance Materials

- BASF SE

- Evonik Industries AG

- Avery Dennison Corporation

- Loparex

- LINTEC Corporation

- Mitsubishi Chemical Corporation

- Mondi Group

- Fujifilm Holdings Corporation

- Rayven Inc.

- Felix Schoeller Group

*- List not Exhaustive

Research Coverage

Developed by USDAnalytics, this report investigates the Release Coating Market, delivering analysis reviews of demand drivers, cost-in-use metrics, curing efficiencies, and end-use performance thresholds across packaging, medical & hygiene, electronics, and industrial applications; it highlights breakthroughs in solventless and UV-curable silicone systems, recyclable liner architectures, PFAS-free low-surface-energy coatings, and high-temperature release films for EV batteries—mapping specification needs (release force windows, anchorage, migration control, coat-weight uniformity) to converter line speed and sustainability compliance so decision-makers can benchmark technologies, suppliers, and routes-to-market with confidence; designed for engineers, procurement leaders, and product strategists, this report is an essential resource that integrates competitive moves, capacity expansions, regulatory momentum, and profitability levers across substrates and chemistries.

Scope Highlights

Segmentation:

- By Material Type / Chemistry: Silicone; Non-Silicone.

- By Formulation Technology: Solventless; Water-based; Solvent-borne; High-Solids.

- By Substrate / Release Liner Type: Paper-Based; Film-Based; Fabric/Non-woven.

- By Key Application / End-Use: Pressure Sensitive Tapes & Labels; Industrial; Medical & Hygiene; Electronics.

- By Region: North America (United States, Canada, Mexico); Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe); Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC); South & Central America (Brazil, Argentina, Rest of SCA); Middle East & Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa).

Geographic Scope: Analysis spans 25+ countries across North America, Europe, Asia Pacific, Latin America, the Middle East & Africa.

Time Horizon: Historic data 2021–2024 and forecast data 2025–2034.

Companies Covered: Analysis/profiles of 15+ companies (global leaders and regional specialists).

Deliverables

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.