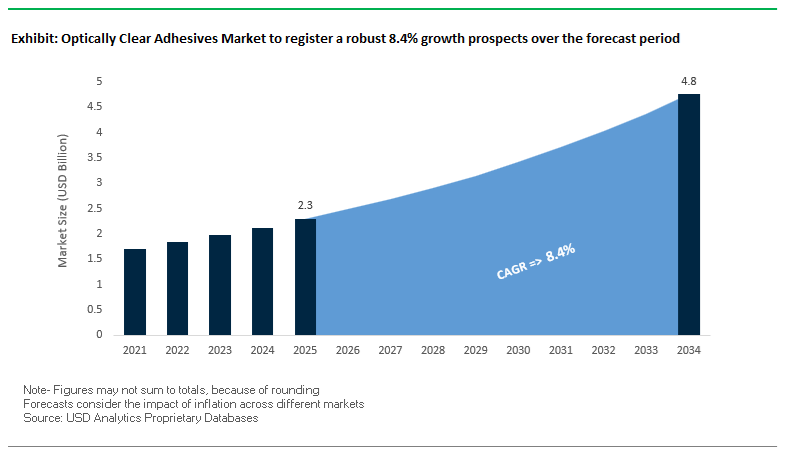

The Global Optically Clear Adhesives (OCA) Market is projected to expand from USD 2.3 billion in 2025 to USD 4.8 billion by 2034, advancing at a CAGR of 8.4%, as display architectures move decisively toward flexible, foldable, curved, and high-luminance formats. Growth is being driven less by panel volume alone and more by the tight coupling between adhesive behavior and display yield, optical performance, and field reliability across smartphones, wearables, automotive HMIs, and emerging Micro-LED platforms. In these systems, OCA and LOCA materials directly influence light efficiency, touch accuracy, rework rates, and long-term visual stability.

OCAs have become foundational to modern optical bonding because they deliver high light transmission, low haze, and mechanical compliance while maintaining adhesion across dissimilar substrates. As device designs transition from rigid stacks to foldable OLEDs and flexible displays, adhesive specifications are being rewritten around low modulus, high elasticity, and fatigue resistance. Leading suppliers such as Nitto, LG Chem, and 3M are advancing formulations that tolerate bending radii of 1–5 mm and retain optical and mechanical integrity beyond 100,000 dynamic folds, mitigating risks of yellowing, delamination, and optical distortion that directly impact warranty exposure and brand perception.

Automotive electronics are reinforcing parallel demand, but with a different performance bias. The rapid adoption of curved, large-format infotainment displays and LiDAR-integrated interfaces is increasing reliance on UV-curable and silicone-based LOCA systems, where thermal endurance and impact resistance are critical. Adhesives qualified to withstand 85°C/500-hour and 65°C/95% relative humidity endurance cycles are gaining importance as displays are pushed into harsher cabin and exterior environments. Manufacturers such as Dow and Shin-Etsu continue to expand optical-grade silicone portfolios to support non-birefringent performance and dimensional stability, ensuring glare-free, color-accurate output over extended service life.

Process economics and sustainability considerations are reshaping formulation roadmaps. The industry is rapidly shifting toward solvent-free, 100% solid-content OCA and LOCA systems, particularly across Asia where the bulk of global display manufacturing is concentrated and VOC regulations are tightening. At the same time, reworkable and recyclable OCA polymers are gaining traction as panel makers seek to reduce scrap rates and enable refurbishment of high-value flexible displays. Next-generation systems demonstrating >99% light transmission, non-birefringence, and >300% shear strain resistance are increasingly specified to support flexible, curved, and impact-resistant form factors without compromising throughput or optical fidelity.

The Optically Clear Adhesives (OCA) industry is experiencing an accelerated phase of technological innovation, capacity expansion, and sustainability-driven transformation, reshaping its supply and product ecosystem across Asia, Europe, and North America.

In November 2024, a leading U.S. chemicals manufacturer announced a $50 million capacity expansion in Asia-Pacific to meet surging demand for foldable display adhesives and OCA film laminates used in flexible electronics. This aligns with the ongoing shift of global electronics production to Asia’s high-growth markets, particularly in South Korea, China, and Vietnam.

The innovation landscape continued to evolve in October 2024, when a European specialty materials company launched a UV-curable LOCA series for in-cell touch panel lamination, achieving curing times under 10 seconds—optimizing high-volume smartphone assembly lines. Similarly, in September 2024, a Japanese electronics materials supplier partnered with an electric vehicle (EV) OEM to co-develop silicone-based OCAs with superior vibration absorption and optical stability for large curved automotive displays and LiDAR modules, underlining the increasing integration of optics in mobility electronics.

In August 2024, researchers published results on a thermo-reworkable OCA polymer, which can be cleanly debonded at 90°C, enabling recycling and rework of flexible displays—an innovation addressing one of the biggest sustainability challenges in consumer electronics manufacturing. Governments also played a role; in July 2024, regulatory bodies in Asia introduced stricter VOC emission limits for display bonding materials, pushing manufacturers toward solid-content and solvent-free OCAs, while also driving the adoption of cleanroom-grade formulations for improved yield.

Mergers and acquisitions continued to shape the competitive landscape. In June 2024, a global industrial materials conglomerate acquired a German silicone technology firm, integrating low-modulus silicone innovations into its OCA portfolio—enhancing performance for wearable electronics and stretchable sensors. Meanwhile, May 2024 saw the introduction of an ultra-thin (<10μm) OCA film engineered for Micro-LED bonding, reducing optical distortion and improving pixel density uniformity in ultra-high-resolution displays. In April 2024, a South Korean OCA producer inaugurated a 15m² cleanroom facility for aerospace and military-grade display adhesives, setting a new benchmark in contamination-free manufacturing.

Market Trend 1: Development of Ultra-Low Modulus and Anti-Reflective OCAs for Foldable and Curved Displays

The surge in foldable and flexible OLED display adoption has redefined the performance expectations for optically clear adhesives. Modern OCAs must combine mechanical flexibility, ultra-low modulus, and optical clarity while surviving hundreds of thousands of bending cycles without failure. Research indicates that high-performance foldable display OCAs must retain mechanical and optical integrity over 100,000 dynamic folds, even at folding radii between 1–5 mm, where shear strain can exceed 300%.

Finite Element Analysis (FEA) modeling reports that maintaining an adhesive shear modulus below 5×10⁴ Pa at room temperature is critical to mitigating strain accumulation and preventing creasing or delamination. Novel acrylate-based and hybrid OCA systems are being designed to maintain consistent elasticity across temperature ranges from -20°C to +85°C, ensuring high transparency and long-term adhesion durability.

A major breakthrough in the industry is the introduction of UV-blocking OCAs tailored for flexible OLED panels, featuring specialized photo-initiating systems that allow curing under visible light instead of high-energy UV. The innovation has increased production speed by up to tenfold, optimizing throughput in high-volume flexible display manufacturing. Further, anti-reflective coatings integrated into OCAs are minimizing light reflection losses and enhancing display contrast, a crucial advancement for curved and foldable AMOLED panels in next-generation smartphones and tablets.

Market Trend 2: Adoption of UV-LED Curing Systems and Low-Temperature Processable OCAs for Manufacturing Efficiency

The growing transition from traditional mercury lamps to UV-LED curing systems is transforming OCA processing efficiency across electronics and display manufacturing. Unlike conventional systems, UV-LED curing (365–405 nm) generates negligible infrared heat, thereby eliminating thermal distortion risks in temperature-sensitive substrates such as OLEDs and TFTs. The has made LED curing an essential enabler of low-thermal, energy-efficient display assembly.

Advanced UV-LED-curable OCAs polymerize in just a few seconds, drastically cutting production cycle times while maintaining positional precision in automated assembly lines. Studies confirm that low-temperature curing is vital for flexible electronic devices—one experiment recorded that adhesive stress at 85°C was 57.4% lower than at 30°C, confirming that reduced processing temperatures enhance long-term reliability and minimize internal stress.

Material advancements in low-shrinkage OCA formulations and optimized photoinitiator systems have further improved process control, enabling defect-free curing and bubble-free adhesion even in multilayer OLED and optical laminations. As manufacturers continue to prioritize energy efficiency and production speed, UV-LED processable OCAs have emerged as the new industry benchmark, combining precision curing, minimal outgassing, and improved optical performance.

Market Opportunity 1: Enabling the Commercialization of Augmented Reality (AR) Waveguides and Combiners

The rapid advancement of AR and mixed reality (MR) eyewear is unlocking new frontiers for optically clear adhesives in waveguide and combiner assembly. In AR systems, maintaining light uniformity, optical alignment, and refractive index consistency is critical to ensuring clear, undistorted visuals. The next generation of AR-grade OCAs is formulated with refractive indices ranging from 1.7 to 2.0, optimized for high-index glass substrates used in diffractive and reflective AR optics. The RI matching prevents light scattering and internal reflection losses, ensuring bright, high-fidelity imagery.

Optical lamination for diffractive AR waveguides requires adhesives with exceptional dimensional stability and shrinkage control—typically below 1.5% linear shrinkage—to maintain sub-micron accuracy across nano-structured grating layers. The slightest deformation during curing can distort diffraction angles, degrading display quality. Consequently, manufacturers are using precision-engineered OCAs that guarantee transmission rates exceeding 95% above 400 nm, with haze levels under 0.1%, preserving optical clarity and image resolution.

The emerging segment presents a high-margin opportunity as global AR device production scales. The convergence of optical-grade lamination adhesives, index-tunable polymers, and defect-free coating technologies positions OCAs as the enabling material for the commercial mass production of AR smart glasses and mixed reality headsets.

Market Opportunity 2: Servicing the Automotive Industry’s Shift Toward Large-Format, Curved, and Touch-Integrated Displays

The automotive industry’s pivot toward immersive, digital cockpit environments has created a robust demand for high-performance automotive OCAs capable of bonding large, curved, and touch-integrated display assemblies. Modern automotive cockpits incorporate panoramic displays exceeding 15 inches in size, which must endure extreme temperature cycling, UV exposure, and high humidity conditions over long service lifespans.

Automotive-grade OCAs are subjected to rigorous thermal shock testing, often involving 300+ rapid cycles between -40°C and +85°C without delamination or bubbling. They must also sustain clarity and adhesion during extended high-heat exposure (+95°C for 1,000 hours) and 85°C/85% RH environmental testing, confirming their resilience under harsh vehicular conditions.

For curved and large-format displays, flexible liquid or roll-based OCAs are engineered with low viscosity and high elongation to ensure perfect conformal bonding across complex geometries. In addition, UV-resistant OCA systems capable of withstanding over 500 hours of high-intensity exposure (0.55 W/m² at 340 nm) are essential to preventing yellowing and maintaining display readability.

These adhesive systems are a critical enabler of advanced infotainment displays, HUD (Head-Up Displays), and transparent OLED panels, serving as both the optical coupling medium and protective interface. As electric vehicles and autonomous platforms continue to integrate expansive visual systems, OCAs that combine optical precision, thermal endurance, and mechanical flexibility will dominate the automotive display bonding materials market.

Optically Clear Adhesives Market Share Insights, 2025-2034

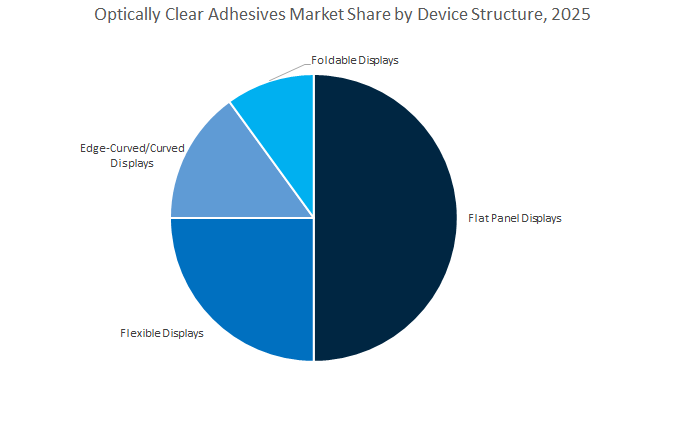

Market Share by Device Structure

The Flat Panel Display segment continues to dominate the global optically clear adhesives (OCA) market, accounting for a projected 52.3% share in 2025. This dominance is attributed to the widespread use of OCAs in smartphones, televisions, tablets, monitors, and laptops, which form the backbone of global display demand. The segment benefits from the massive installed base of LCD and OLED panels that require precise optical bonding for improved clarity, contrast ratio, and sunlight readability. OCAs provide exceptional light transmittance, low haze, and strong adhesion to both glass and polymer substrates, ensuring enhanced display performance and durability. As manufacturers focus on thinner, high-resolution screens, the use of UV-curable and pressure-sensitive OCA films is expanding rapidly across consumer electronics and digital signage.

Meanwhile, Flexible Displays are emerging as the fastest-growing application area within the OCA market. The rise of foldable smartphones, wearable devices, and automotive interiors is creating demand for highly elastic adhesives that maintain optical and mechanical integrity under repeated flexing. OCAs used in these applications are being engineered with low modulus polymers and enhanced reworkability, enabling durability without compromising transparency. Curved and Edge-Curved Displays—integral to premium smartphones, infotainment systems, and advanced monitors—require OCA formulations that can bond to complex geometries while maintaining consistent optical performance. The Foldable Display segment, though smaller in volume, represents a high-margin, innovation-driven niche, where advanced silicone and acrylic-based OCAs ensure bubble-free bonding and delamination resistance under mechanical stress.

Market Share by End-Use Industry

The Electrical & Electronics sector overwhelmingly dominates the global optically clear adhesives market, holding a projected 68.2% share in 2025. OCAs are indispensable in this sector for display lamination, touch panels, camera modules, and optical sensors, ensuring superior light transmission and minimal reflection. The proliferation of smartphones, tablets, AR/VR headsets, and wearables continues to drive OCA adoption, as manufacturers prioritize optical precision, thin-film adhesion, and durability. The rapid shift toward OLED and micro-LED display technologies has further reinforced demand for advanced OCAs with UV stability, reworkability, and compatibility with high-resolution screens. Additionally, electronics miniaturization and the emergence of transparent devices are expanding opportunities for nanostructured and low dielectric OCAs that combine optical clarity with electrical insulation.

The automotive industry represents the second-largest and fastest-growing segment, propelled by the increasing integration of digital cockpits, infotainment systems, and heads-up displays (HUDs). OCAs are used in bonding instrument clusters, touchscreens, and ambient lighting systems, ensuring vibration resistance and optical uniformity in dynamic environments. The medical devices segment leverages OCAs for optical sensors, diagnostic displays, and wearable medical monitors, where biocompatibility and resistance to sterilization processes are essential. Aerospace & Defense applications demand OCAs that maintain clarity and adhesion under extreme thermal and UV exposure, particularly for avionics and control displays. Industrial applications, though smaller in scale, utilize OCAs in ruggedized and outdoor display systems for machinery, automation panels, and marine navigation equipment.

The global Optically Clear Adhesives market is dominated by technology leaders such as 3M Company, Nitto Denko Corporation, DuPont de Nemours, Inc., and Henkel AG & Co. KGaA, each leveraging specialized R&D expertise, global manufacturing footprints, and cross-industry integration strategies to serve diverse applications across flexible displays, automotive optics, photonics, and high-durability touch interfaces.

3M remains the global benchmark for OCA technology with its 3M™ Optically Clear Adhesives (OCA) 821X series, known for >99% optical transmission and high adhesion performance in advanced touch panel and display lamination. The company’s Contrast Enhancement Films (CEF) are tailored for foldable OLED screens, offering low modulus and high stress-decoupling to prevent delamination under repeated folding. With advanced R&D tools like Finite Element Analysis (FEA) and Dynamic Mechanical Analysis (DMA), 3M simulates viscoelastic adhesive behavior across extreme temperature cycles. Its OCAs also find extensive use in avionics and military displays, valued for non-birefringence and thermal shock resistance between −40°C and +85°C.

Nitto Denko offers the LUCIACS™ CS986 Series, an ultra-thin OCA tape with excellent optical clarity and adhesion strength, used widely in flat-panel and cover glass bonding. Building on its polarizer film expertise, Nitto integrates OCA technology with optical management films to enhance visibility and contrast in high-end displays. Its Fiber PSA technology combines removability and flexibility, supporting next-generation flexible and rollable display applications. The firm’s latest innovation, RAYCREA, introduces advanced light-control layers that demand specialized OCA formulations for multi-layer optical film stacking.

DuPont’s Electronics & Industrials division is advancing high-purity adhesives for display assembly and semiconductor packaging, reinforcing its position in the MicroLED and OLED manufacturing ecosystem. In 2024, the company invested $30 million in its Zhangjiagang, China plant to expand adhesive production for automotive display bonding and EV lightweighting applications. DuPont’s Mobility & Materials division leverages multi-material bonding experience from vehicle structures and battery modules, translating these capabilities into rugged, thermally stable OCA systems. Its R&D focus remains on enabling next-generation display technologies through innovation in optical-grade polymer interfaces and high-durability transparent bonding materials.

Henkel continues to lead global adhesive innovation through its Adhesive Technologies division, offering UV-curable and silicone-based OCA solutions for applications in OLED, Micro-LED, fiber optics, and 5G infrastructure. The company’s formulations provide exceptional thermal stability, ultra-low yellowing, and high adhesion for optical fiber bonding, high-resolution displays, and precision sensors. Henkel’s sustainability-driven R&D is focused on solvent-free and bio-compatible adhesives, meeting environmental standards while maintaining high optical performance. Its extensive global network enables seamless delivery of high-reliability bonding materials for automotive, medical, and consumer electronics sectors.

Country Analysis: Global Optically Clear Adhesives (OCA) Industry — Innovation Hubs Driving Display and Photonics Evolution

United States: Innovation Powerhouse Driving High-Performance and Sustainable OCA Formulations

The United States leads in the development of advanced Optically Clear Adhesives (OCAs) that deliver superior optical clarity, environmental durability, and structural integrity across high-end applications. As of August 2025, leading material science companies and adhesive manufacturers have announced significant R&D investment increases, targeting the production of thin, flexible, and thermally stable adhesives for use in next-generation foldable displays, curved OLED panels, and touch-enabled automotive interfaces.

US-based innovators are also advancing UV-curable OCA systems optimized for high-speed, precision bonding in micro-assembly and optical device manufacturing, enabling faster throughput and improved optical alignment accuracy. The progress is critical for LiDAR and ADAS sensors, where reliable adhesion under mechanical vibration and temperature variation is essential. Additionally, defense sector modernization continues to stimulate demand for ruggedized optical display bonding materials used in cockpit instrumentation and battlefield visualization systems.

Medical technology is another strong driver: biocompatible OCAs and Optically Clear Resins (OCRs) are being tailored for medical imaging and diagnostic optics, ensuring minimal light refraction and long-term stability. Parallelly, the U.S. adhesive industry is adopting low-VOC, solvent-free, and recyclable adhesive chemistries in response to tightening environmental mandates—underscoring a nationwide transition toward sustainable optical adhesive manufacturing.

China: Expanding OCA Manufacturing Scale and Vertical Integration in Display Supply Chains

China stands as the largest manufacturing hub for Optically Clear Adhesives in Asia-Pacific, propelled by its extensive electronics, display, and EV industries. The country’s vertically integrated ecosystem, from raw polymer production to final adhesive formulation, gives it a dominant role in supplying OCAs to both domestic and global markets. Supported by the Ministry of Ecology and Environment and the National Development and Reform Commission (NDRC), Chinese manufacturers are investing in green chemistry and VOC-free adhesive production technologies to align with national environmental objectives.

The nation’s electronics sector, centered in Shenzhen, Suzhou, and Chengdu, continues to scale production for OLED and AMOLED panels, driving massive demand for non-yellowing, high-transparency liquid OCAs and OCA films. The Electric Vehicle (EV) industry has emerged as a parallel demand center, utilizing advanced OCAs for high-durability infotainment displays, digital dashboards, and ADAS systems. Domestic suppliers, such as Shenzhen Wason Tech, are rapidly expanding capacity for automotive-grade and foldable-display adhesives, enhancing China’s self-sufficiency in high-performance optical materials.

Additionally, PLI-style government initiatives aimed at boosting domestic electronics and semiconductor manufacturing are intensifying the need for premium adhesive solutions suited to bezel-less screens, camera modules, and flexible displays. As global supply chain localization accelerates, China’s OCA industry is positioned as the strategic production backbone for the global display ecosystem.

South Korea: Global Leader in Flexible, Ultra-Thin, and Quantum Dot Display OCA Technology

South Korea maintains its global leadership in OLED, AMOLED, and flexible display adhesives, backed by its massive display production capacity—exceeding 200 million OLED panels annually (2024). The nation’s material science companies and electronics conglomerates are at the forefront of next-generation OCA innovation, developing ultra-low modulus (≤5×10⁴ Pa), high-elongation adhesives that can endure over 100,000 bending cycles—a performance benchmark vital for foldable smartphones, tablets, and wearables.

The country’s material producers are also pioneering ultra-thin OCA films (as low as 20μm) that enable lightweight, multi-layer display structures without compromising transparency or adhesion. The materials are designed to maintain perfect optical clarity in curved and flexible devices, essential for aesthetic and functional performance in premium electronics. Collaborative R&D programs between major Korean display manufacturers and adhesive suppliers have produced proprietary OCA formulations optimized for light out-coupling efficiency, durability, and heat resistance.

Emerging research is focusing on Quantum Dot (QD) display bonding materials, ensuring color fidelity and environmental stability in advanced visual systems. In addition, the rise of Vehicle-to-Infrastructure (V2I) technologies and automotive OLED panels is driving innovation in impact-resistant and temperature-tolerant adhesives—solidifying South Korea’s reputation as the epicenter of foldable and quantum-grade OCA innovation.

Japan: Precision Engineering and Advanced Material Science in OCA Manufacturing

Japan’s OCA industry is deeply rooted in precision material science, producing the world’s most reliable and optically stable adhesives for displays, automotive optics, and photonics components. Japanese firms continue to dominate in the development of high-purity acrylic and silicone-based OCAs, optimized for complex lamination processes in OLED, Micro-LED, and advanced sensor systems.

The market is witnessing extensive R&D in Micro-LED display adhesives, engineered for ultra-fine alignment and ultra-thin bonding layers required by next-generation miniaturized displays. Similarly, Japan’s automotive sector is driving demand for temperature-stable OCAs used in ADAS cameras, lidar modules, and in-vehicle touch displays, where consistent optical performance under extreme environmental conditions is non-negotiable.

Sustainability remains central to Japan’s strategy. Manufacturers are investing in VOC-free, eco-friendly adhesive chemistries and recycling-integrated production systems in response to stringent domestic and global environmental standards. Concurrently, major Japanese conglomerates are expanding OCA production lines across Southeast Asia, aiming to meet regional electronics manufacturing growth while preserving Japanese precision quality standards. The continued focus on environmental responsibility, reliability, and high-precision performance keeps Japan at the forefront of optical adhesive engineering.

Germany (Europe): Automotive Displays, Industrial Bonding, and Regulatory-Driven Innovation

Germany and the wider European region represent a critical hub for automotive-grade and industrial optical adhesive innovation, shaped by the EU’s rigorous REACH and Green Deal regulations. German manufacturers are pioneers in integrating UV-curable and dual-curing OCA technologies, improving both manufacturing speed and optical bonding durability across consumer, automotive, and industrial electronics. Companies like DELO Industrial Adhesives are leading The advancement, providing high-transparency, low-outgassing OCAs optimized for digital instrument clusters, head-up displays (HUDs), and industrial touchscreen panels.

European automotive OEMs are increasingly specifying high-durability OCAs for curved, glare-resistant infotainment and navigation displays, reflecting the region’s premium vehicle design ethos. Additionally, as industrial automation and digital signage expand, the demand for optically stable, weather-resistant bonding adhesives is rising sharply, particularly for outdoor and factory-floor applications.

In alignment with REACH compliance, German and European adhesive formulators are eliminating SVHCs (Substances of Very High Concern) from formulations, transitioning toward safer, sustainable chemistries. Emerging academic and industrial R&D efforts are exploring self-healing OCAs—materials that autonomously repair minor defects—aimed at extending display longevity and reducing maintenance costs. Europe’s integration of regulatory rigor, sustainability leadership, and automotive precision ensures its pivotal role in shaping the future of optically clear bonding materials.

Optically Clear Adhesives Market Report Scope

Optically Clear Adhesives Market

|

Parameter

|

Details

|

|

Market Size (2025)

|

$2.3 Billion

|

|

Market Size (2034)

|

$4.8 Billion

|

|

Market Growth Rate

|

8.4%

|

|

Segments

|

By Resin Type (Acrylic, Silicone, Polyurethane, Epoxy, Polyvinyl Acetate, Others), By Form Factor (Film, Liquid, Resin, Optical Gel), By Device Structure (Flat Panel, Edge-Curved/Curved, Flexible, Foldable), By Substrate (Glass, Polycarbonate, Polymethyl Methacrylate, Polyethylene Terephthalate, Indium Tin Oxide, Metal), By Application (Mobile Phones/Smartphones, Tablets, Laptops/Monitors, Televisions, Wearable Devices, Outdoor Digital Signage/Kiosks, Electronic Blackboards/Interactive Whiteboards), By End-Use Industry (Electrical & Electronics, Automotive, Aerospace & Defense, Medical Devices, Industrial

|

|

Study Period

|

2019- 2024 and 2025-2034

|

|

Units

|

Revenue (USD)

|

|

Qualitative Analysis

|

Porter’s Five Forces, SWOT Profile, Market Share, Scenario Forecasts, Market Ecosystem, Company Ranking, Market Dynamics, Industry Benchmarking

|

|

Companies

|

Henkel AG & Co. KGaA, 3M Company, Dymax Corporation, DELO Industrial Adhesives LLC, Nitto Denko Corporation, Dow Inc., Dexerials Corporation, Lintec Corporation, Shin-Etsu Chemical Co., Ltd., DIC Corporation, Sika AG, Master Bond Inc., H.B. Fuller Company, Panacol-Elosol GmbH, Toray Industries, Inc.

|

|

Countries

|

US, Canada, Mexico, Germany, France, Spain, Italy, UK, Russia, China, India, Japan, South Korea, Australia, South East Asia, Brazil, Argentina, Middle East, Africa

|

By Resin Type

- Acrylic

- Silicone

- Polyurethane

- Epoxy

- Polyvinyl Acetate

- Others

By Form Factor

- Film

- Liquid

- Resin

- Optical Gel

By Device Structure

- Flat Panel

- Edge-Curved/Curved

- Flexible

- Foldable

By Substrate

- Glass

- Polycarbonate

- Polymethyl Methacrylate

- Polyethylene Terephthalate

- Indium Tin Oxide

- Metal

By Application

- Mobile Phones/Smartphones

- Tablets

- Laptops/Monitors

- Televisions

- Wearable Devices

- Outdoor Digital Signage/Kiosks

- Electronic Blackboards/Interactive Whiteboards

By End-Use Industry

- Electrical & Electronics

- Automotive

- Aerospace & Defense

- Medical Devices

- Industrial

By Region

- North America (United States, Canada, Mexico)

- Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe)

- Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC)

- South and Central America (Brazil, Argentina, Rest of SCA)

- Middle East and Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa)

Top Companies in Optically Clear Adhesives Market

- Henkel AG & Co. KGaA

- 3M Company

- Dymax Corporation

- DELO Industrial Adhesives LLC

- Nitto Denko Corporation

- Dow Inc.

- Dexerials Corporation

- Lintec Corporation

- Shin-Etsu Chemical Co., Ltd.

- DIC Corporation

- Sika AG

- Master Bond Inc.

- H.B. Fuller Company

- Panacol-Elosol GmbH

- Toray Industries, Inc.

*- List not Exhaustive

Research Coverage

This report investigates the Optically Clear Adhesives (OCA) Market, delivering analysis reviews on demand inflections from foldable/flexible OLED, automotive cockpits, Micro-LED, and wearables; it highlights performance breakthroughs in ultra-low-modulus, UV-LED curable, and solvent-free OCA/LOCA systems that sustain high transmission, low haze, and durability under 85/85 and thermal-shock regimes; it also benchmarks index control, shrinkage management, and reworkable/recyclable chemistries that unlock high-yield optical bonding at scale. Built by USDAnalytics, this report is an essential resource for display engineers, optics product managers, procurement leaders, and investors seeking defensible forecasts, competitor moves, and qualification pathways across consumer electronics, automotive, medical, and industrial visualization.

Scope Highlights

Segmentation:

- By Resin Type: Acrylic; Silicone; Polyurethane; Epoxy; Polyvinyl Acetate; Others.

- By Form Factor: Film; Liquid; Resin; Optical Gel.

- By Device Structure: Flat Panel; Edge-Curved/Curved; Flexible; Foldable.

- By Substrate: Glass; Polycarbonate; PMMA; PET; Indium Tin Oxide; Metal.

- By Application: Mobile Phones/Smartphones; Tablets; Laptops/Monitors; Televisions; Wearable Devices; Outdoor Digital Signage/Kiosks; Electronic Blackboards/Interactive Whiteboards.

- By End-Use Industry: Electrical & Electronics; Automotive; Aerospace & Defense; Medical Devices; Industrial.

- By Adhesive Thickness: Below 100 μm; 100–200 μm; 200–300 μm; 300–400 μm; 400 μm and Above.

- By Region: North America (United States, Canada, Mexico); Europe (Germany, France, United Kingdom, Spain, Italy, Rest of Europe); Asia Pacific (China, India, Japan, South Korea, Australia, Rest of APAC); South & Central America (Brazil, Argentina, Rest of SCA); Middle East & Africa (Saudi Arabia, UAE, South Africa, Rest of Middle East, Rest of Africa).

Geographic Scope: Analysis spans 25+ countries across North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa.

Timeframe: Historic data 2021–2024 and forecast data 2025–2034.

Companies: Analysis/profiles of 15+ companies.

Deliverables

- Comprehensive Market Research Report (PDF and Excel) with detailed tables, charts, and interactive visualizations.

- Country-Specific Forecasts & Analysis.

- Segment-Wise Revenue Forecasts (2025–2034).

- Competitive Analysis, Benchmarking, and SWOT Profiles.

- Recent Developments & Innovation Tracker.

- Executive Summary & Analyst Commentary.

- Post-Purchase Analyst Support for Client-Specific Questions and Custom Data Requirements.